the latin american retail environment

TRANSCRIPT

This article was downloaded by: [Uppsala universitetsbibliotek]On: 11 October 2014, At: 06:25Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH,UK

Journal of Food ProductsMarketingPublication details, including instructions forauthors and subscription information:http://www.tandfonline.com/loi/wfpm20

The Latin American RetailEnvironmentJohn L. Stanton Jr. aa Food Marketing Research, Department of FoodMarketing , St. Joseph's University , 5600 CityAvenue, Philadelphia, PA, 19131-1395, USAPublished online: 11 Oct 2008.

To cite this article: John L. Stanton Jr. (2001) The Latin American RetailEnvironment, Journal of Food Products Marketing, 6:4, 3-8, DOI: 10.1300/J038v06n04_02

To link to this article: http://dx.doi.org/10.1300/J038v06n04_02

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all theinformation (the “Content”) contained in the publications on our platform.However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness,or suitability for any purpose of the Content. Any opinions and viewsexpressed in this publication are the opinions and views of the authors, andare not the views of or endorsed by Taylor & Francis. The accuracy of theContent should not be relied upon and should be independently verified withprimary sources of information. Taylor and Francis shall not be liable for anylosses, actions, claims, proceedings, demands, costs, expenses, damages,and other liabilities whatsoever or howsoever caused arising directly orindirectly in connection with, in relation to or arising out of the use of theContent.

This article may be used for research, teaching, and private study purposes.Any substantial or systematic reproduction, redistribution, reselling, loan,sub-licensing, systematic supply, or distribution in any form to anyone isexpressly forbidden. Terms & Conditions of access and use can be found athttp://www.tandfonline.com/page/terms-and-conditions

Dow

nloa

ded

by [

Upp

sala

uni

vers

itets

bibl

iote

k] a

t 06:

25 1

1 O

ctob

er 2

014

The Latin American Retail Environment

John L. Stanton, Jr.

ABSTRACT. One of the hot markets in the world for food companieshas been Latin America. This article reviews the current situation anddiscusses some of the advantages and disadvantages of the variousmarkets. [Article copies available for a fee from The Haworth Document Deliv-ery Service: 1-800-342-9678. E-mail address: <[email protected]>Website: <http://www.HaworthPress.com> E 2001 by The Haworth Press, Inc.All rights reserved.]

KEYWORDS. Latin America, retailing, food

Any food marketer who travels to Latin America or Brazil usually noticestwo aspects of life. The upper middle class areas seem to have very welldeveloped food-shopping opportunities and the poorer sections seem to stilluse traditional corner stores or Bodegas. However, as each country continuesits economic development so goes the development of the sophisticated su-permarkets. There are three key questions to be answered when consideringentering these markets. First, is the well-developed market large enough towarrant entry of another food company? Second, can I make a profit servingthe underdeveloped? Third, how fast is the rate of change between the twogroups?The answer to these questions of course varies by each of the various

countries. Some countries such as Brazil, Argentina, and Mexico have well-developed food markets and currently use the most sophisticated methods tomarket and distribute food. Others such as Peru, Chile, and Equador are notas far along especially outside the capital city.I would like to focus attention on three key countries in Latin America:

John L. Stanton, Jr. is Professor of Food Marketing Research, Department ofFood Marketing, St. Joseph’s University, 5600 City Avenue, Philadelphia, PA19131-1395 (E-mail: [email protected]).

Journal of Food Products Marketing, Vol. 6(4) 2001E 2001 by The Haworth Press, Inc. All rights reserved. 3

Dow

nloa

ded

by [

Upp

sala

uni

vers

itets

bibl

iote

k] a

t 06:

25 1

1 O

ctob

er 2

014

JOURNAL OF FOOD PRODUCTS MARKETING4

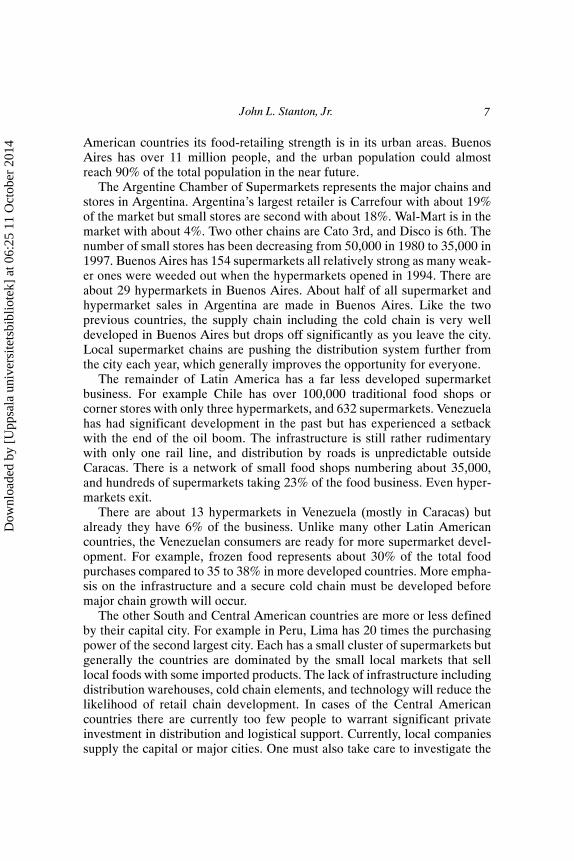

Brazil, Argentina, and Mexico. These countries have 66% of the total popula-tion of all Latin America, and have the most developed supermarket systemsas can be seen in Table I.Brazil, the giant of South America, stands out as a leader in the develop-

ment of the retail food business in South America. It has a supermarketassociation, ABRAS, that facilitates the development of the industry by keep-ing it attuned to all worldwide trends and developments. The annual ABRASconference ranks among the world’s best including FMI in the US (Chicago)and ANUGA in Germany (Koln). Brazilian supermarket sales were almostUS$50 billion last year, with over 48,000 self-service stores. There is still anopportunity for development of the industry as the largest 20 supermarketchains represent only about 40% of the total sales whereas in the US the topfive chains have about that same percentage of sales.There should be no mistake, in Brazil as in all the other Latin American

countries, there are still a large number of small, traditional food shops that

TABLE I. Population and Per Capita Income

Country Population Per Capita(millions) Income

In US$

Argentina 36.1 $8,470

Bolivia 8 $1,081

Brazil 167 $5,450

Chile 14.8 $5,680

Colombia 38.6 $2,140

Ecuador 12 $1,390

Paraguay 5.1 $1,690

Peru 26.1 $2,420

Uruguay 3.2 $5,170

Venezuela 23.3 $3,020

Belize 0.2 $2,630

Costa Rica 3.5 $2,610

Guatemala 11.2 $1,340

Nicaragua 4.4 $380

Mexico 98 $3,670

Dow

nloa

ded

by [

Upp

sala

uni

vers

itets

bibl

iote

k] a

t 06:

25 1

1 O

ctob

er 2

014

John L. Stanton, Jr. 5

serve the interior of the country and the poorer sections of the cities. Thereare still over 250,000 neighborhood stores but in Brazil the average store sizehas increased from about 1,000 square meters in 1987 to over 2,500 squaremeters in 1997. The increase comes not only from building larger stores butthere are fewer small stores. One major change taking place in Brazilianretailing is that the large hypermarkets such as Carrefour and Sendas thatwere once selling 70% non-food and 30% food have reversed the situation to70% food and 30% non-food.Brazil also has a very well developed infrastructure for the supermarket

industry. Today about 60% of all industry sales are in stores that are com-pletely automated including both checkout and internal operations. This au-tomation coupled with increases in average store size has led to significantincreases in productivity over the past years. Brazil’s supermarket associationABRAS has been a leader in advancing techniques such as ECR (EfficientConsumer Response), pallet standardization, category management and othersupply chain activities into many chains. The top 20 chains have reported a63% increase in productivity in 1997.A very exciting prospect for any potential investor or food marketer is that

the incredible high food sales levels are concentrated in a small geographicarea. The Southeastern area including São Paulo and Rio de Janeiro has only36% of the stores but 56% of sales. If you add the next largest region,Southern including the state of Rio Grande de Sul, you have about 75% of thecountry is supermarket sales. The high geographic concentration makes dis-tribution and logistics much easier and more efficient.Brazil has also been a major player in a regional organization that will

further standardize the supermarket business in the ‘‘southern cone’’ of SouthAmerica.Mercosur is an affiliation of Brazil, Argentina, Uruguay, Paraguay,Chile and Bolivia which should make the food industry in general much morefriendly to all aspects of food trade including food retailing.There is still not a significant amount of foreign investment in the food

retailing industry in Brazil with the exception of Carrefour, a French compa-ny that is the largest food retailer in Brazil, and Ahold. Wal-Mart has alsomade an entry into the Brazilian market so one can expect to see many othersmake more investment in this country in the next few years. New investorsmust recognize that Brazil is larger than continental US, and has tremendousregional variation and preferences. A successful business must adapt to thatvariation.Mexico also has a well-developed supermarket industry if for no other

reason than the total population is close to 100 million people. But thespending power is concentrated in the urban areas where 70% of the popula-tion resides and particularly in Mexico City, Guadalajara and Monterey.Mexico is also a desirable market because such a high percentage of the

Dow

nloa

ded

by [

Upp

sala

uni

vers

itets

bibl

iote

k] a

t 06:

25 1

1 O

ctob

er 2

014

JOURNAL OF FOOD PRODUCTS MARKETING6

population is young. About 35% of the population are under 15 and only 4%are over 65. These young markets will provide economically active familiesfor many years, and make more effective the loyalty programs currentlybeing developed in that country. Additionally, the large supermarket chainsthat will offer a wide variety for one stop shopping and convenience foodswill likely be more successful with Mexican women who are entering thelabor force at record rates. The percentage of females in the work force variesfrom region to region with a high of 43% in NE areas. These women cannotafford the daily trips to the market.The supermarket environment in Mexico is probably just as sophisticated

as the Brazilian market. The supermarket association, ‘‘La Asociacion Nacio-nal de Tiendas y Autoservicio y Departamentales’’ (ANTAD) is dedicated toimproving the distribution and business practices of its members. ANTAD isworking closely with the SECOFI, the Ministry of Commerce, to create acredible and efficient supply chain that will encourage further growth in thesupermarket industry. There are now about 3,850 supermarkets in Mexicocalled tienda de autoservicio, with several new store openings throughoutMexico each week. The small shops and corner stores are not giving upeasily, so some chains offer ‘‘tianguis days’’ which emphasize the low pricesof the small markets.The Mexican consumer is relatively sophisticated as a food shopper. They

are influenced by family and friends that cross the border to the US as well asby media that spills across the border. Self-service supermarkets are the mostshopped stores in Mexico, with 57% indicating they shop most often in thatformat. While 9% claimed they shopped most often in traditional cornerstores, 4% claimed to shop most often in hypermarkets. It is interesting tonote that in the smaller cities of Mexico 84% of shoppers claim supermarketsas the primary shopping store while only 12% claim corner stores. Thissuggests that the grocery distribution system is well developed throughoutMexico. Another positive aspect to the Mexican food business is that familyexpenditures have increased significantly over the past few years. From 1993the average weekly expenditure on food was P$242 and increased to P$365in 1998 (about 50%).Besides a wide assortment of Mexican supermarket operators, HE Butt

from Texas, Wal-Mart and Carrefour are in the Mexican market. These inter-national players demonstrate that Mexico will continue to be a major marketfor food retailers.Argentina is the third of the key countries for food retailing in South

America. It has the third largest population with over 36 million people and aper capita GNP of $8,030. It has all the ingredients to grow into one of themost developed countries as well. The people are very well educated, very‘‘cosmopolitan,’’ and the country has a sound fiscal policy. Like most Latin

Dow

nloa

ded

by [

Upp

sala

uni

vers

itets

bibl

iote

k] a

t 06:

25 1

1 O

ctob

er 2

014

John L. Stanton, Jr. 7

American countries its food-retailing strength is in its urban areas. BuenosAires has over 11 million people, and the urban population could almostreach 90% of the total population in the near future.The Argentine Chamber of Supermarkets represents the major chains and

stores in Argentina. Argentina’s largest retailer is Carrefour with about 19%of the market but small stores are second with about 18%. Wal-Mart is in themarket with about 4%. Two other chains are Cato 3rd, and Disco is 6th. Thenumber of small stores has been decreasing from 50,000 in 1980 to 35,000 in1997. Buenos Aires has 154 supermarkets all relatively strong as many weak-er ones were weeded out when the hypermarkets opened in 1994. There areabout 29 hypermarkets in Buenos Aires. About half of all supermarket andhypermarket sales in Argentina are made in Buenos Aires. Like the twoprevious countries, the supply chain including the cold chain is very welldeveloped in Buenos Aires but drops off significantly as you leave the city.Local supermarket chains are pushing the distribution system further fromthe city each year, which generally improves the opportunity for everyone.The remainder of Latin America has a far less developed supermarket

business. For example Chile has over 100,000 traditional food shops orcorner stores with only three hypermarkets, and 632 supermarkets. Venezuelahas had significant development in the past but has experienced a setbackwith the end of the oil boom. The infrastructure is still rather rudimentarywith only one rail line, and distribution by roads is unpredictable outsideCaracas. There is a network of small food shops numbering about 35,000,and hundreds of supermarkets taking 23% of the food business. Even hyper-markets exit.There are about 13 hypermarkets in Venezuela (mostly in Caracas) but

already they have 6% of the business. Unlike many other Latin Americancountries, the Venezuelan consumers are ready for more supermarket devel-opment. For example, frozen food represents about 30% of the total foodpurchases compared to 35 to 38% in more developed countries. More empha-sis on the infrastructure and a secure cold chain must be developed beforemajor chain growth will occur.The other South and Central American countries are more or less defined

by their capital city. For example in Peru, Lima has 20 times the purchasingpower of the second largest city. Each has a small cluster of supermarkets butgenerally the countries are dominated by the small local markets that selllocal foods with some imported products. The lack of infrastructure includingdistribution warehouses, cold chain elements, and technology will reduce thelikelihood of retail chain development. In cases of the Central Americancountries there are currently too few people to warrant significant privateinvestment in distribution and logistical support. Currently, local companiessupply the capital or major cities. One must also take care to investigate the

Dow

nloa

ded

by [

Upp

sala

uni

vers

itets

bibl

iote

k] a

t 06:

25 1

1 O

ctob

er 2

014

JOURNAL OF FOOD PRODUCTS MARKETING8

percentage of the population that is ‘‘economically active.’’ In some coun-tries only a small percentage have enough disposable income to shop insupermarkets. For example, in Equador with a population of about 12 millionpeople only 4 million are estimated to be economically active.One small country that deserves some special attention is Uruguay. While

small in geographic area and population, it is a developed country in manyother ways. It is a model for economic development and has had a very stableeconomy for years. Its population is well educated and sophisticated. Its foodretail business has not only local operators but is influenced by both Argenti-na and Brazil’s supermarket business. If it were not for its small population itwould be an ideal market for any investment in food retail.Two factors will lead to an expansion of major supermarket chains

throughout Latin America. That is the growth of the TV set ownership anduse of the Internet. TV ownership is as high as 40 million TV sets in Brazil,over 17 million in Mexico, and 10 million in Argentina. There are alsogrowing numbers of Internet site and therefore Internet users in the countriesas well. Brazil leads the way with over 77,000 web site hosts, Mexico withover 29,000, and Argentina with over 12,000. These factors are importantbecause they permit the more efficient communication of branded food andkindred products to the consumers making it more attractive to enter themarket. For example, Argentine TV advertising now has over 50% of shareof advertising expenditures. It also increases the possibility of cable andsatellite use providing examples of lifestyles from around the world.Latin America can be a great potential for food retailing both in the near

and far future. Each country has its own idiosyncrasies and its own specialcultures. To be successful in any of these cultures a potential investor may getclose to the market and understand the consumers as well as the supply chain.Profit will be the reward of those that take the time to learn about these greatcountries.

Dow

nloa

ded

by [

Upp

sala

uni

vers

itets

bibl

iote

k] a

t 06:

25 1

1 O

ctob

er 2

014