the jobs act implementation update

TRANSCRIPT

Monthly Webinar Series

presents

The JOBS Act Implementation Update

October 11, 2012

Panelists David Weild, Grant Thornton, CMA Partners John D. Hogoboom, Lowenstein Sandler

Tim Keating, Keating Capital

Moderator Brett Goetschius, Growth Capital Investor

Thank you for participating in “The JOBS Act Implementation Update.” This manual contains information you will need to prepare for this webinar.

CONFERENCE MANUAL

This manual contains:

•Dial-‐in/log-‐on instructions.

Speaker bio and contact information. •Tips for submitting questions. •Pertinent information from the pages of Growth Capital Investor.

CONFERENCE DETAILS

The webinar is scheduled for Thursday, October 11, 2012 at 2:00 p.m. EDT, 1:00 p.m. CDT, 12:00 p.m. MDT, and 11:00 a.m. PDT. It will last 110 minutes.

HOW TO JOIN THE WEBINAR

Online With Streaming Audio •Go to http://web.beaconlive.com

•On the “Join a Meeting” side of the login page, enter meeting room: mnm2 •Enter your unique PIN (same as the audio PIN you received). •Click on “Join Meeting” to access the presentation.

Optional Telephone Access If you have trouble streaming the sound through your computer, please follow these instructions to listen by phone:

•Dial 1-‐ 866-‐953-‐3919 about 5-‐10 minutes before the start of the conference. •Enter your unique PIN (sent in your e-‐mail confirmation). •You will hear music on hold until the conference has started or be connected directly if it has already begun. •If you have trouble with your PIN stay on the line and an operator will assist you.

•If you are using a speakerphone, put the phone on MUTE for the best sound quality. •If you are disconnected at any point, just repeat the processes above.

PLEASE NOTE: Only one dial in and one log on per PIN are allowed.

If you have problems accessing the webinar, please call 877-‐297-‐2901. HOW TO SUBMIT QUESTIONS

Questions may be submitted at any time during the call using the chat function on the web interface in the lower left corner of your screen. Just type in your question and send it to “Q&A session” in the drop-‐down menu.

Conference Manual Page 1

SPEAKER BIOS AND CONTACT INFORMATION

David Weild IV is Chairman and CEO of Capital Markets Advisory Partners and heads Capital Markets at Grant Thornton. He was a former Vice Chairman and executive committee member of The NASDAQ Stock Market. David is an expert on how stock market structure impacts capital formation and job creation. Together with Ed Kim, their work created the rationale that gave rise to The JOBS Act. David and co-‐author Ed Kim’s written work was the first to identify how changes in stock market structure are harming capital formation and job growth in the United States. He was also a member of the NYSE and NVCA’s (National Venture Capital Association) Blue Ribbon Panel to restore liquidity in the US venture capital industry and his work was cited in the NVCA’s final report.

CONTACT David Weild IV Chairman and CEO Capital Markets Advisory Partners [email protected] [email protected] 212-‐542-‐9979

Conference Manual Page 2

© Grant Thornton LLP. All rights reserved.

The JOBS Act: David Weild: How It Came About October 11, 2012

Conference Manual Page 3

© Grant Thornton LLP. All rights reserved. 2

Important publications Contain exhibits that helped identify the problem for Congress Contain recommendations that are now found in the JOBS Act

- Cited in Congress - Cited by the U.S. Treasury - Cited by the SEC - Cited by the Senate - Cited by The President's Jobs Council

Subscribe to the Capital Markets Series at www.GrantThornton.com/subscribe

November 2008 November 2009 June 2010 October 2011 September 2012

Conference Manual Page 4

© Grant Thornton LLP. All rights reserved. 3

Attended the signing of the JOBS Act in the White House Rose GardenThought leadership citations and public policy activity

“The problems documented by [Weild & Kim's] studies led to

the JOBS Act (HR 3606)."

"Broken Markets" Sal Arnuk and Joseph Saluzzi

page 198 FT Press

May 2012

Conference Manual Page 5

© Grant Thornton LLP. All rights reserved. 4

Small IPO collapse before Decimalization and Sarbanes-Oxley Earlier version show in the House Subcommittee on Capital Markets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

Perc

enta

ge o

f tot

al U

.S. I

POs

Order Handling Rules

Regulation NMS

Regulation ATS

Decimalization

Sources: Grant Thornton LLP, Capital Markets Advisory Partners LLC and DealogicData includes corporate IPOs as of Dec. 31, 2011, excluding funds, REITs, SPACs and LPs.

Transactions raising less than $50 million

Transactions raising at least $50 million

Major U.S. regulations

Sarbanes-Oxley

Conference Manual Page 6

© Grant Thornton LLP. All rights reserved. 5

U.S. has lost over 43.5% of publicly listed companies since 1997 Earlier version shown in the House Subcommittee on Capital Markets

(100)

(50)

0

50

100

150

200

250

'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11Inde

xed

valu

e of

sel

ecte

d gl

obal

exc

hang

e lis

tings

(199

7 =

0)

The U.S. listed markets—unlike other developed markets—have been in steady decline, with no rebound, since 1997

Hong Kong

China

Australia

United States

Deutsche BörseTokyo

Toronto London

Sources: Capital Markets Advisory Partners LLC and World Federation of ExchangesBased on the number of listed companies at year-end, excluding funds. Data as of Dec. 31, 2011.

Conference Manual Page 7

© Grant Thornton LLP. All rights reserved. 6

The JOBS Act Seminal events NYSE/NVCA Blue Ribbon Task Force 2008

2009 Senator Kaufman speech on the floor of the U.S. Senate

CFTC-SEC Joint Panel on Emerging Regulatory Issues

2010

2011 Title IV - House subcommittee on capital markets (testimony 3/16) President Obama cites IPO market problems (9/8 speech)

SEC Small Business Forum (testimony 11/17)

Signing of The JOBS Act SEC Advisory Committee testimony (Decimalization) Congressional testimony (Decimalization)

2012

"How can we create a market structure that works for a $25 million IPO—both in the offering and the secondary aftermarket. If we can answer that question, this country will be back in business."

Title I - Met with to interest Kate Mitchell who later Chaired the IPO Task Force for the US Treasury

Why are IPOs in the ICU? (11/2008)

Titles II, V, VI - A wake up call for America (11/2009)

"We’re also planning to cut away the red tape that prevents too many rapidly growing startup companies from raising capital and going public."

Conference Manual Page 8

© Grant Thornton LLP. All rights reserved. 7

IPO crisis led to higher unemployment Millions of jobs were likely lost to the U.S. economy

-

5

10

15

20

0

200

400

600

800

1,000

1,200

'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

Addi

tiona

l job

sM

illion

s

Dom

estic

com

pani

es g

oing

pub

lic in

the

U.S

.

Minimum additional jobs (direct plus private market effect)*

+3.1 million jobs (direct)

*Best estimate of the multiplier effect in the private market of more companies going public

Sources: Grant Thornton LLP, Dealogic and the U.S. Department of Commerce Bureau of Economic AnalysisDomestic corporate companies going public in the U.S. as of Dec. 31, 2011, excluding funds, REITs and other trusts, SPACs and LPs.Assumes an annual growth rate of 2.57% (U.S. real GDP growth, 1991-2011) and 822 jobs created on average post-IPO (see "Post-IPO Employment and Revenue Growth for U.S. IPOs," Kauffman Foundation).

+6.2 million jobs (direct plus private market effect)

+9.4 million jobs (direct)

+18.8 million jobs (direct plus private market effect)

Minimum additional IPOs

Actual number of domestic IPOs

Maximum additional IPOs

Minimum additional jobs (direct)

Maximum additional jobs (direct plus private market effect)*

Maximum additional jobs (direct)

A major contributor to employment

Conference Manual Page 9

John D. Hogoboom is a founding member of the Lowenstein Sandler Specialty Finance Group and is co-‐chair of the Life Sciences group. He specializes in representing clients in the life sciences and other industries in mergers and acquisitions, public and private securities offerings, private equity investments and general corporate and securities law. John is listed among The Best Lawyers in America in the 2007-‐2012 editions of the publication in both the corporate law and securities law categories.

CONTACT John D. Hogoboom Founding Member Lowenstein Sandler Specialty Finance Group 973-‐597-‐2382 [email protected]

Conference Manual Page 10

Jumpstart Our Business Startups Act (“JOBS Act”)

General Solicitation Provisions

October 2012

Conference Manual Page 11

JOBS Act – General Solicitation

Section 201(a) of the JOBS Act required the SEC to adopt final rules on or before July 4, 2012 permitting widespread advertising and other forms of “general solicitation” in private offerings in reliance on Rule 506 under Regulation D or Rule 144A so long as all of the actual purchasers of the securities were “accredited investors” (in the case of Regulation D) or “qualified institutional buyers” (in the case of Rule 144A).

SEC failed to meet the required deadline.

On August 29, 2012, the SEC proposed amendments to Rule 506 of Regulation D and Rule 144A to implement the requirements of Section 201(a).

Comments on the proposed rules were due by October 5, 2012. Expect final rules to be issued shortly.

Conference Manual Page 12

Summary of Proposed Rules

Rule 506 would be amended to add paragraph (c), providing a new and separate exemption under the Rule that would permit an issuer to use general solicitation and general advertising to offer securities, provided that the issuer takes reasonable steps to verify that all purchasers of the securities are accredited investors. The proposed rules would continue to apply the “reasonable belief” standard to the condition that all purchasers are accredited investors. Whether the steps taken by the issuer to verify the accredited investor status of the purchasers are “reasonable” would be an objective determination, based on the particular facts and circumstances of each offering and investor. The proposed rules do not prescribe particular verification procedures.

Conference Manual Page 13

Effects on Other Requirements

The SEC confirmed in the proposing release that: – Consistent with the historical treatment of concurrent Regulation S

and Rule 144A/Rule 506 offerings, concurrent offshore offerings that are conducted in compliance with Regulation S would not be integrated with domestic unregistered offerings that are conducted in compliance with Rule 506 or Rule 144A, as proposed to be amended.

– Privately offered funds would be permitted to make a general solicitation under amended Rule 506 without losing the ability to rely on Sections 3(c)(1) and 3(c)(7) of the Investment Company Act, which provide commonly used exclusions from the definition of “investment company”.

Conference Manual Page 14

Proposed Rule 506(c)

Under proposed Rule 506(c), an issuer (and any selling agents) would be permitted to use general solicitation and general advertising to offer and sell securities, provided that the following conditions are satisfied: – The issuer must take reasonable steps to verify that all purchasers of the

securities are accredited investors. – All purchasers of the securities must be accredited investors, either because

they come within one of the enumerated categories of persons that qualify as accredited investors or because the issuer reasonably believes that they do, at the time of the sale of the securities, in each case as defined under existing Rule 501 of Regulation D.

– All terms and conditions of existing Rules 501 (definitions), 502(a) (integration restriction) and 502(d) (resale limitations) of Regulation D must be satisfied. Existing Rule 502(c), prohibiting general solicitation and general advertising, would not apply.

Conference Manual Page 15

Verification Requirement

In the proposing release, the SEC did not propose specific verification methods.

Objective test determining the reasonableness of the verification steps

The issuer must consider the facts and circumstances of the transaction, including, among other things: – The nature of the purchaser and the type of accredited investor that the purchaser claims to be.

§ For example, more may be required to verify information about an individual using the net worth test than about an institutional investor.

– The amount and type of information that the issuer has about the purchaser. § The more information an issuer has, the fewer steps would be required to verify the purchaser’s status.

- Publicly available filings - Third-party evidence such as W-2s - Third-party verification (including by broker-dealers) so long as issuer has a reasonable basis to rely on the verification - If issuer has pre-existing, substantive relationship with proposed investor, may not be required to verify the investor’s status

– The nature of the offering, such as the manner in which the purchaser was solicited to participate in the offering,

and the terms of the offering, such as a minimum investment amount. § Require more to verify an unknown purchaser solicited through general advertisement § Not sufficient to check a box or sign a form absent other information § Higher the minimum investment amount, less likely that a non-accredited investor would be able to purchase

Issuers must maintain adequate records documenting the verification process.

Many existing practices may satisfy the new verification requirements.

Exemption continues to be based on reasonable belief. Presence of a non-accredited investor not

fatal as long as the issuer had a reasonable belief that the investor was accredited.

Conference Manual Page 16

No impact on existing Rule 506

New verification requirement would only apply to offerings of securities conducted pursuant to the new Rule 506(c). Other offerings conducted pursuant to existing Rule 506(b) that do not involve general solicitation or general advertising will not be subject to the verification requirement.

506(c) not likely to benefit existing public companies who have other compelling reasons to maintain confidentiality of offering process.

Conference Manual Page 17

Impact on other requirements Proposed Amendments to Rule 144A

– Under the proposed amendments to Rule 144A, securities sold pursuant to Rule 144A may be

offered to persons other than “qualified institutional buyers”, including by means of general solicitation or general advertising, provided that the securities are sold only to persons that the seller and any person acting on behalf of the seller reasonably believe is a qualified institutional buyer.

Impact on Concurrent Regulation S Offerings – Regulation S provides a safe harbor for offers and sales of securities outside the United States,

provided that the securities are sold in an offshore transaction and the issuer has not engaged in any “directed selling efforts” in the United States. In the proposing release, the SEC confirmed that concurrent offshore offerings that are conducted in compliance with Regulation S would not be integrated with domestic unregistered offerings that are conducted in compliance with Rule 506 or Rule 144A, as proposed to be amended.

Investment Company Act Exclusion for Private Funds – Privately offered funds, such as hedge funds, venture capital funds and private equity funds,

generally rely on exclusions in the Investment Company Act that are not available if the fund makes a public offering of securities. In the proposing release, the SEC affirmed its belief that Section 201(b) of the JOBS Act, which provides that offers and sales exempt under Rule 506 of Regulation D (as revised pursuant to the JOBS Act) “shall not be deemed public offerings under the Federal securities laws as a result of general advertising or general solicitation”, permits privately offered funds to make a general solicitation under proposed new Rule 506(c) without losing the benefit of the exclusions under the Investment Company Act.

Conference Manual Page 18

SEC Monitoring Potential Abuse

The SEC has noted that the proposed rules are narrowly focused on implementing the statutory mandate under Section 201(a) of the JOBS Act and that the SEC and its staff will continue to monitor the private placement market as a whole to analyze the impact, including any unintended consequences, of the proposed rules on investors, issuers and the markets. The SEC also noted that that the Dodd-Frank Act requires ongoing evaluations of the definition of “accredited investor” that would give the SEC flexibility to combat abusive practices. Pursuant to the Dodd-Frank Act, the SEC has proposed rules disqualifying felons and other “bad actors” from relying on the Rule 506 exemption to offer and sell securities.

Conference Manual Page 19

Other Considerations

Unclear what the impact of proposed Rule 506(c) will be on state securities regulations, many of which condition exemptions on the lack of general solicitation. Will the SEC acknowledge that rules permitting general solicitation mean that public and “private” deals now can be done side-by-side. Will issuers use third-party verification services?

Conference Manual Page 20

JOBS Act – Analyst Provisions

Section 105 of the JOBS Act contains provisions allowing greater analyst participation in initial public offerings for “emerging growth companies”.

Conference Manual Page 21

Summary of Analyst Provisions

Section 105 of the JOBS Act:

§ Permits a broker or dealer to publish research on an emerging growth company that is the subject of a proposed public offering at any time even if the broker or dealer is participating in the offering (not limited to IPOs);

§ Permits publication of research on an emerging growth company after its IPO without complying with any waiting period or waiting for the expiration of any lock-up agreement;

§ Prohibits the SEC or any national securities association from adopting or maintaining any rule

restricting, based on functional role, which associated persons of a broker, dealer, or member of a national securities association, may arrange for communications between a securities analyst and a potential investor in an IPO of an emerging growth company; and

§ Prohibits the SEC or any national securities association from adopting or maintaining any rule restricting a securities analyst from participating in any communications with the management of an emerging growth company that is also attended by any other non-research employee.

Conference Manual Page 22

Staff FAQs

On August 22, 2012, the Staff of the SEC issued a series of “frequently asked questions” relating to the analyst provisions in the JOBS Act.

The provisions of the JOBS Act do not amend or modify the Global Research Settlement (the "Settlement"). Any firm subject to the Settlement would have to petition the court for a modification of the Settlement in order to take advantage of the JOBS Act provisions.

The "test the waters" provisions of the JOBS Act allow underwriters to seek nonbinding

indications of interest but not to ask for a purchase commitment from customers. The JOBS Act does not address communications where investors are present together

with company management, analysts and investment banking personnel. Accordingly, analysts remain prohibited from participating in road shows or otherwise engaging in communications with customers about a transaction while in the presence of investment bankers or company management.

The Staff indicates that further updates to these FAQs may be provided.

Conference Manual Page 23

Continuing Analyst Prohibitions

The Staff believes that, consistent with current SEC and SRO rules, analysts may attend meetings with management of an emerging-growth company and investment banking personnel.

Analysts continue to be subject to existing restrictions, such as:

– prohibitions on soliciting investment banking business, – changing a recommendation in exchange for investment banking business, – exchanging favorable recommendations for investment banking business, and – publishing research with which the analyst personally disagrees.

Investment banking personnel may not direct an analyst to engage in sales and marketing efforts

relating to a proposed offering.

Analysts continue to be prohibited from participating in roadshows or otherwise engaging in communications with customers about an investment banking transaction in the presence of investment bankers or the company’s management.

SRO rules regarding supervision, compensation or evaluation of analysts have not changed.

Firms are cautioned to ensure that they institute and enforce appropriate controls to ensure that analysts are not engaging in prohibited conduct, including solicitations, at meetings that are also attended by investment banking personnel.

Conference Manual Page 24

Permissible Analyst Activities

Prior to engagement, at meetings with management and investment banking personnel, analysts at firms not subject to the Settlement can

– introduce themselves, – outline their research program and the types of factors that the analyst would consider in his or her analysis, and – ask follow-up questions to better understand factual statements made by company management.

After engagement, such analysts can

– participate in presentations by management of an emerging-growth company to sales forces (but only to avoid the need to make separate presentations to the analysts),

– discuss industry trends, – provide information obtained from investing customers and – communicate their views.

Investment bankers can forward a list of clients to an analyst for the analyst to contact.

An analyst may provide a list of potential clients he or she intends to contact for investment banking personnel "to facilitate scheduling.“

Bankers can also arrange, but may not participate in, calls analysts have with clients.

Deemed not to be directing an analyst to engage in sales or marketing efforts in violation of FINRA

and NYSE rules.

Conference Manual Page 25

Free-Writing

The Staff believes that, consistent with the intent of the JOBS Act, research reports should be allowed to be published with respect to an emerging-growth company during all quiet periods — whether before or after the expiration, termination or waiver of a lockup period or whether the lockup relates to an IPO or a secondary offering of the company's securities.

On September 28, FINRA filed a notice of proposed rule change with the SEC to conform applicable NASD rules to the FAQs. The notice indicates that FINRA intends to eliminate the following quiet periods: – 40-day period for manager or co-manager of an IPO – 25-day period for other IPO participants – 15-day period applicable to manager or co-manager of an IPO prior to expiration, waiver or

termination of a lock-up agreement. – 10-day quiet period on manager or co-manager of a secondary offering – All quiet periods applicable after the expiration, termination or waiver of a lock-up agreement.

FINRA is seeking SEC approval for these changes prior to the end of the normal 30-pay

post publication period and that the approval be retroactive to April 5, 2012 (the date of enactment of the JOBS Act).

Conference Manual Page 26

Summary of Proposed Rules

Rule 506 would be amended to add paragraph (c), providing a new and separate exemption under the Rule that would permit an issuer to use general solicitation and general advertising to offer securities, provided that the issuer takes reasonable steps to verify that all purchasers of the securities are accredited investors. The proposed rules would continue to apply the “reasonable belief” standard to the condition that all purchasers are accredited investors. Whether the steps taken by the issuer to verify the accredited investor status of the purchasers are “reasonable” would be an objective determination, based on the particular facts and circumstances of each offering and investor. The proposed rules do not prescribe particular verification procedures.

Conference Manual Page 27

Effects on Other Requirements

The SEC confirmed in the proposing release that: – Consistent with the historical treatment of concurrent Regulation S

and Rule 144A/Rule 506 offerings, concurrent offshore offerings that are conducted in compliance with Regulation S would not be integrated with domestic unregistered offerings that are conducted in compliance with Rule 506 or Rule 144A, as proposed to be amended.

– Privately offered funds would be permitted to make a general solicitation under amended Rule 506 without losing the ability to rely on Sections 3(c)(1) and 3(c)(7) of the Investment Company Act, which provide commonly used exclusions from the definition of “investment company”.

Conference Manual Page 28

Proposed Rule 506(c)

Under proposed Rule 506(c), an issuer (and any selling agents) would be permitted to use general solicitation and general advertising to offer and sell securities, provided that the following conditions are satisfied: – The issuer must take reasonable steps to verify that all purchasers of the

securities are accredited investors. – All purchasers of the securities must be accredited investors, either because

they come within one of the enumerated categories of persons that qualify as accredited investors or because the issuer reasonably believes that they do, at the time of the sale of the securities, in each case as defined under existing Rule 501 of Regulation D.

– All terms and conditions of existing Rules 501 (definitions), 502(a) (integration restriction) and 502(d) (resale limitations) of Regulation D must be satisfied. Existing Rule 502(c), prohibiting general solicitation and general advertising, would not apply.

Conference Manual Page 29

Verification Requirement In the proposing release, the SEC did not propose specific verification methods.

Objective test determining the reasonableness of the verification steps

The issuer must consider the facts and circumstances of the transaction, including, among other

things:

– The nature of the purchaser and the type of accredited investor that the purchaser claims to be. § For example, more may be required to verify information about an individual using the net worth test than about an institutional

investor.

– The amount and type of information that the issuer has about the purchaser. § The more information an issuer has, the fewer steps would be required to verify the purchaser’s status.

- Publicly available filings - Third-party evidence such as W-2s - Third-party verification (including by broker-dealers) so long as issuer has a reasonable basis to rely on the verification - If issuer has pre-existing, substantive relationship with proposed investor, may not be required to verify the investor’s status

– The nature of the offering, such as the manner in which the purchaser was solicited to participate in the offering, and the terms of the offering, such as a minimum investment amount. § Require more to verify an unknown purchaser solicited through general advertisement § Not sufficient to check a box or sign a form absent other information § Higher the minimum investment amount, less likely that a non-accredited investor would be able to purchase

Issuers must maintain adequate records documenting the verification process.

Many existing practices may satisfy the new verification requirements.

Exemption continues to be based on reasonable belief. Presence of a non-accredited investor not fatal as long as the issuer had a reasonable belief that the investor was accredited.

Conference Manual Page 30

No impact on existing Rule 506

New verification requirement would only apply to offerings of securities conducted pursuant to the new Rule 506(c). Other offerings conducted pursuant to existing Rule 506(b) that do not involve general solicitation or general advertising will not be subject to the verification requirement.

506(c) not likely to benefit existing public companies who have other

compelling reasons to maintain confidentiality of offering process.

Conference Manual Page 31

Impact on other requirements Proposed Amendments to Rule 144A

– Under the proposed amendments to Rule 144A, securities sold pursuant to Rule 144A may be

offered to persons other than “qualified institutional buyers”, including by means of general solicitation or general advertising, provided that the securities are sold only to persons that the seller and any person acting on behalf of the seller reasonably believe is a qualified institutional buyer.

Impact on Concurrent Regulation S Offerings – Regulation S provides a safe harbor for offers and sales of securities outside the United States,

provided that the securities are sold in an offshore transaction and the issuer has not engaged in any “directed selling efforts” in the United States. In the proposing release, the SEC confirmed that concurrent offshore offerings that are conducted in compliance with Regulation S would not be integrated with domestic unregistered offerings that are conducted in compliance with Rule 506 or Rule 144A, as proposed to be amended.

Investment Company Act Exclusion for Private Funds – Privately offered funds, such as hedge funds, venture capital funds and private equity funds,

generally rely on exclusions in the Investment Company Act that are not available if the fund makes a public offering of securities. In the proposing release, the SEC affirmed its belief that Section 201(b) of the JOBS Act, which provides that offers and sales exempt under Rule 506 of Regulation D (as revised pursuant to the JOBS Act) “shall not be deemed public offerings under the Federal securities laws as a result of general advertising or general solicitation”, permits privately offered funds to make a general solicitation under proposed new Rule 506(c) without losing the benefit of the exclusions under the Investment Company Act.

Conference Manual Page 32

SEC Monitoring Potential Abuse

The SEC has noted that the proposed rules are narrowly focused on implementing the statutory mandate under Section 201(a) of the JOBS Act and that the SEC and its staff will continue to monitor the private placement market as a whole to analyze the impact, including any unintended consequences, of the proposed rules on investors, issuers and the markets.

The SEC also noted that that the Dodd-Frank Act requires ongoing evaluations of the definition of “accredited investor” that would give the SEC flexibility to combat abusive practices.

Pursuant to the Dodd-Frank Act, the SEC has proposed rules disqualifying felons and other “bad actors” from relying on the Rule 506 exemption to offer and sell securities.

Conference Manual Page 33

Other Considerations

Unclear what the impact of proposed Rule 506(c) will be on state securities regulations, many of which condition exemptions on the lack of general solicitation.

Comments on the proposed rules were due by October 5, 2012.

Conference Manual Page 34

Legal Disclaimer

Although this presentation may provide information concerning potential legal issues, it is not a substitute for legal advice from qualified counsel. The presentation is not created or designed to address the unique facts of circumstances that may arise in any specific instance, and you should not and are not authorized to rely on the contents of this presentation as a source of legal advice and this presentation material does not create any attorney-client relationship between you and Lowenstein Sandler PC.

Conference Manual Page 35

Tim Keating is the Chief Executive Officer of Keating Capital, Inc. (Nasdaq: KIPO), a publicly traded business development company that specializes in making pre-‐IPO investments in innovative, emerging growth companies that are committed to and capable of becoming public. Previously, he held senior management positions in the Equity and Equity Derivatives departments of Bear Stearns, Nomura and Kidder, Peabody in both London and New York. Tim has been widely quoted in the national media, including publications such as The Wall Street Journal, Forbes, SmartMoney and the Venture Capital Journal. Tim has also been a guest contributor to Forbes.com and InvestmentNews.

CONTACT Tim Keating Chief Executive Officer Keating Capital, Inc. 720-‐889-‐0139 [email protected]

Conference Manual Page 36

www.KeatingCapital.com

JOBS Act Presentation

Investor Perspective of the IPO On-Ramp October 11, 2012

Buy Privately, Sell Publicly, Capture the Difference™

Conference Manual Page 37

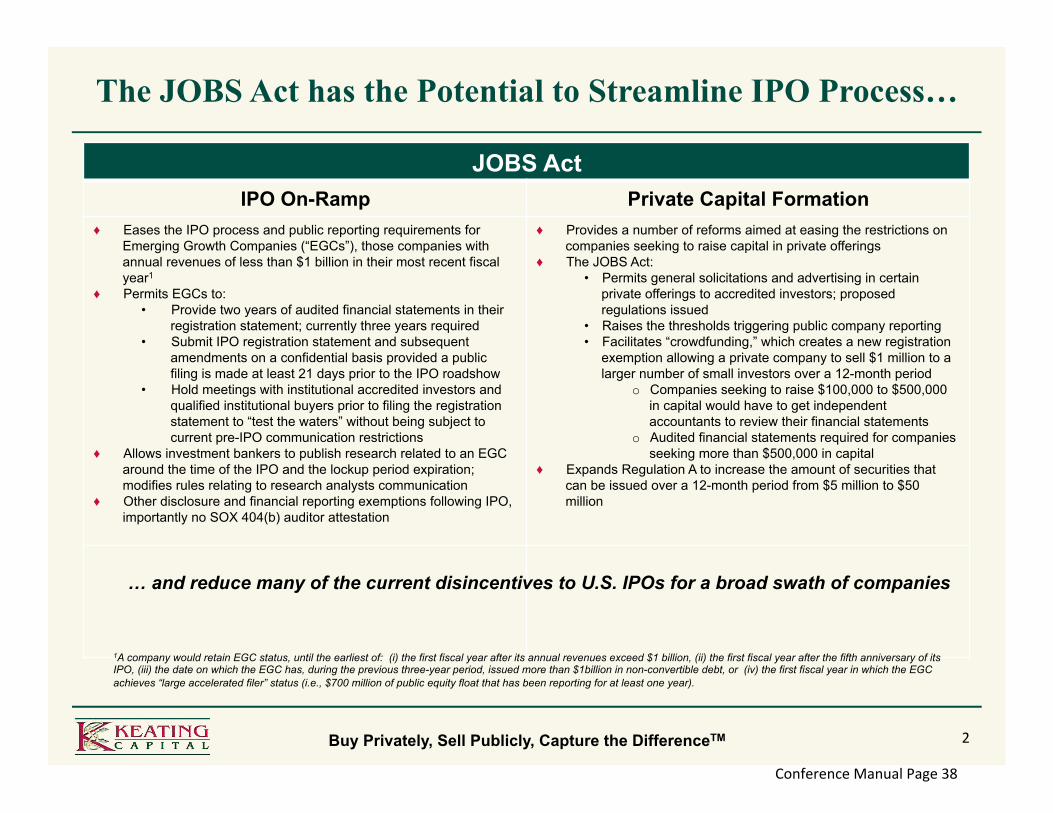

The JOBS Act has the Potential to Streamline IPO Process…

JOBS Act IPO On-Ramp Private Capital Formation

♦ Eases the IPO process and public reporting requirements for Emerging Growth Companies (“EGCs”), those companies with annual revenues of less than $1 billion in their most recent fiscal year1

♦ Permits EGCs to: Provide two years of audited financial statements in their

registration statement; currently three years required Submit IPO registration statement and subsequent

amendments on a confidential basis provided a public filing is made at least 21 days prior to the IPO roadshow

Hold meetings with institutional accredited investors and qualified institutional buyers prior to filing the registration statement to “test the waters” without being subject to current pre-IPO communication restrictions

♦ Allows investment bankers to publish research related to an EGC around the time of the IPO and the lockup period expiration; modifies rules relating to research analysts communication

♦ Other disclosure and financial reporting exemptions following IPO, importantly no SOX 404(b) auditor attestation

♦ Provides a number of reforms aimed at easing the restrictions on companies seeking to raise capital in private offerings

♦ The JOBS Act: Permits general solicitations and advertising in certain

private offerings to accredited investors; proposed regulations issued

Raises the thresholds triggering public company reporting Facilitates “crowdfunding,” which creates a new registration

exemption allowing a private company to sell $1 million to a larger number of small investors over a 12-month period

o Companies seeking to raise $100,000 to $500,000 in capital would have to get independent accountants to review their financial statements

o Audited financial statements required for companies seeking more than $500,000 in capital

♦ Expands Regulation A to increase the amount of securities that can be issued over a 12-month period from $5 million to $50 million

… and reduce many of the current disincentives to U.S. IPOs for a broad swath of companies

1A company would retain EGC status, until the earliest of: (i) the first fiscal year after its annual revenues exceed $1 billion, (ii) the first fiscal year after the fifth anniversary of its IPO, (iii) the date on which the EGC has, during the previous three-year period, issued more than $1billion in non-convertible debt, or (iv) the first fiscal year in which the EGC achieves “large accelerated filer” status (i.e., $700 million of public equity float that has been reporting for at least one year).

2 Buy Privately, Sell Publicly, Capture the DifferenceTM

Conference Manual Page 38

Negative

JOBS Act Report Card: Private Capital Formation

♦ General Solicitation ♦ Public Company Reporting Thresholds ♦ Regulation A

♦ Crowdfunding

Neutral Positive

3 Buy Privately, Sell Publicly, Capture the DifferenceTM

Conference Manual Page 39

Negative

JOBS Act Report Card: IPO On-Ramp

♦ Research Reports ♦ Securities Analyst Communications ♦ Communications Before and During the Offering Process

♦ Auditor Attestation on Internal Controls

♦ Financial Information in SEC Filings ♦ Accounting Standards ♦ Auditor Rotation and Other PCAOB Rules ♦ Executive Compensation Disclosure ♦ Say on Pay

♦ Confidential Filings

Neutral Positive

4 Buy Privately, Sell Publicly, Capture the DifferenceTM

Conference Manual Page 40

Research Reports and Analyst Communications

Reform Current Rule Under the JOBS Act Research Reports/Analyst Communications

♦ Generally, managing underwriters in an IPO are prohibited from: (i) publishing or distributing research on the issuer until 40 days after the IPO, (ii) making any public appearance for 25 days following the IPO date, if participating, (iii) publishing or distributing any research report or making any public appearance during the 15 days before and after the lockup expiration

♦ Communications by analysts with EGCs and potential IPO investors are subject to a number of conflicts of interest and other restrictions

♦ Permits the publication and distribution of research reports and public appearances with respect to securities of EGC any time after IPO (including quiet periods), even if research reports issued by brokers that are participating or will participate in the offering

♦ Analysts can attend meetings with EGC’s management and investment bankers (avoids separate and duplicate management presentations to analysts), but analysts remain subject to existing conflicts of interest restrictions

♦ Analysts of non-Global Settlement firms can attend pre-engagement meetings, i.e., pitch meetings, with EGC management and investment bankers to introduce themselves and to outline their research program and factors that analysts may consider, and to ask management questions to better understand factual matters, but still prohibited from soliciting investment banking business

♦ After underwriter engaged, non-Global Settlement firm analysts can participate in EGC management presentations to sales teams, discuss industry trends and communicate their views

♦ SRO rules still prohibit analysts from participating in roadshows or communicating with investors about an IPO in the presence of investment bankers or EGC’s management (intended to reduce pressure on analyst’s assessment of the offering and keep analyst from being viewed as part of sales team)

♦ Bankers can arrange, but not participate in, calls between analysts and investors

Keating Perspective

♦ Improves communication and transparency before and after IPO ♦ Asymmetry of information available to individual and institutional investors is conceptually highly problematic and

contrary to the intent of Regulation FD (currently permitted oral communications or “whispers” outside prospectus disclosure to investment bankers clients needs to be corrected)

♦ Bulge bracket firms that are party to Global Settlement are still subject to the terms of that agreement and therefore not able to avail themselves of all relief that is available to others under the JOBS Act; but middle market firms will also not avail themselves of this relief for fear of being frozen out of public offerings controlled by the bulge bracket firms (however, middle market firms may have potential to provide significant value add)

♦ Additional reform is urgently needed in this area to rectify this regulatory anomaly

5 Buy Privately, Sell Publicly, Capture the DifferenceTM

Conference Manual Page 41

Communications Before/During the Offering Process

Reform Current Rule Under the JOBS Act Communications Before and During the Offering Process

♦ “Test the waters” communications with respect to public offering not allowed prior to filing of registration statement

♦ Limited ability to “test the waters” after registration statement filed

♦ After filing of registration statement, underwriters required to provide sales representatives with preliminary prospectus before soliciting customer orders

♦ Expand permissible communications to allow EGCs and their underwriters, both before and after filing a registration statement, to “test the waters” by engaging in oral or written communications with qualified institutional buyers and institutional accredited investors to determine interest in an offering

♦ Following the “filing” of registration statement, “test the waters” communications can continue without the underwriter making available preliminary prospectus to its sales representatives as long as only non-binding indications of interest and not purchase commitments are sought from potential investors, i.e., not soliciting customer order)

♦ Submitting confidential draft registration statement for SEC review is not considered a “filing” of a registration statement

Keating Perspective

♦ Improves communication with investors ♦ Extremely important for issuers to be able to determine the viability of a public offering before publicly

disclosing business and financial information, which could affect competitive landscape or harm reputation if IPO not pursued

♦ Ideally will serve to clear the zombies in the SEC registration queue

6 Buy Privately, Sell Publicly, Capture the DifferenceTM

Conference Manual Page 42

Auditor Attestation on Internal Controls

Reform Current Rule Under the JOBS Act Auditor Attestation on Internal Controls

♦ Auditor attestation on effectiveness of internal controls over financial reporting required in second annual report after IPO

♦ Non-accelerated filers currently not required to comply

♦ Transition period for compliance up to 5 years, i.e., for so long as the issuer is deemed to be an EGC

Keating Perspective

♦ Reduces public company costs ♦ Single most important reform in the JOBS Act ♦ Will provide greater cost relief to EGCs (which represent 90% of all companies that go public) relative to the

costs incurred by large companies ♦ While the cost savings are important, they are dwarfed in comparison to the positive boost in psychology in the

venture capital community ♦ After a decade of “why would any company want to go public?” mentality in Silicon Valley, we're thankfully

getting back to a mindset where the IPO is the ultimate end game

7 Buy Privately, Sell Publicly, Capture the DifferenceTM

Conference Manual Page 43

Confidential Submissions of Draft IPO Registration Statements

Reform Current Rule Under the JOBS Act Confidential Submissions of Draft IPO Registration Statements

♦ Historically only foreign issuers were permitted to submit confidential draft registration statements with the SEC

♦ In December 2011, the SEC announced that it would only review submissions by foreign private issuers on a confidential basis in specified circumstances; as a result, many non-U.S. companies submitting their initial registration statement to the SEC in connection with a U.S. IPO or listing will have to do so via a public filing

♦ An EGC is permitted to submit to the SEC a draft IPO registration statement for confidential review prior to public filing

♦ However, public filing of any confidential submission and any amendments must be made with the SEC not later than 21 days before the EGC begins its roadshow

Keating Perspective

♦ Worsens communication ♦ Dubious value, if any, to any party especially since the “test the waters” process should ferret out investor

interest ♦ No compelling reasons why EGCs should be given the ability to confidentially assess whether the SEC has

concerns with their financial and business disclosures ♦ Risk of scarce SEC resources being consumed and bandwidth clogged by issuers that are not serious about

taking an IPO to completion ♦ Instead of creating a level playing field for domestic issuers, the better solution would have been for the SEC to

abolish confidential filings for all parties

8 Buy Privately, Sell Publicly, Capture the DifferenceTM

Conference Manual Page 44

© Grant Thornton LLP. All rights reserved.

The JOBS Act: David Weild: The Next Chapter

Conference Manual Page 45

© Grant Thornton LLP. All rights reserved. 10

SEC issued its study on decimalization in July

Conference Manual Page 46

© Grant Thornton LLP. All rights reserved. 11

The JOBS Act provided two of the three legs we believe are needed to revive capital formation

Improved issuer communication with investors ü

Lowered cost for issuers ü

Improve economic incentives to support

especially small-cap stocks (increases in tick sizes)

Conference Manual Page 47

© Grant Thornton LLP. All rights reserved. 12

Grant Thornton issued its study on decimalization Request a copy at www.grantthornton.com/ticksizes

Conference Manual Page 48

© Grant Thornton LLP. All rights reserved. 13

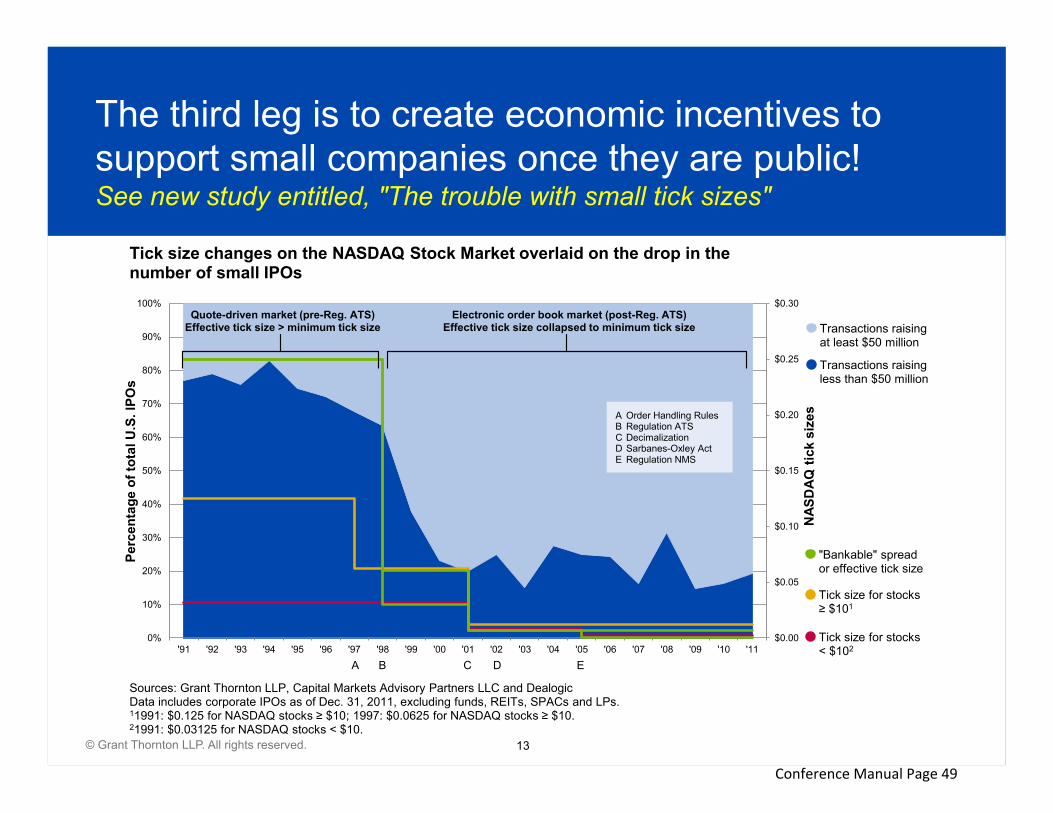

The third leg is to create economic incentives to support small companies once they are public! See new study entitled, "The trouble with small tick sizes"

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

NAS

DAQ

tick

siz

es

Perc

enta

ge o

f tot

al U

.S. I

POs

Sources: Grant Thornton LLP, Capital Markets Advisory Partners LLC and DealogicData includes corporate IPOs as of Dec. 31, 2011, excluding funds, REITs, SPACs and LPs.11991: $0.125 for NASDAQ stocks ≥ $10; 1997: $0.0625 for NASDAQ stocks ≥ $10.21991: $0.03125 for NASDAQ stocks < $10.

Tick size changes on the NASDAQ Stock Market overlaid on the drop in the number of small IPOs

A Order Handling RulesB Regulation ATSC DecimalizationD Sarbanes-Oxley ActE Regulation NMS

A B C D E

Quote-driven market (pre-Reg. ATS)Effective tick size > minimum tick size

Electronic order book market (post-Reg. ATS)Effective tick size collapsed to minimum tick size

Transactions raising less than $50 million

Transactions raising at least $50 million

Tick size for stocks ≥ $101

"Bankable" spread or effective tick size

Tick size for stocks < $102

Conference Manual Page 49

© Grant Thornton LLP. All rights reserved. 14

Small tick sizes, commission compression and electronic trading together caused a collapse

Small-cap companies and capital formation

Before 1997 After 2001 % change

Tick sizes (“bankable spread”) $0.25 per share $0.01 per share -96%

Retail commissions $250 per trade $5 per trade -98%

Investment banks (acting as a bookrunner) 167 (1994) 39 (2006) -77%

Small company IPOs 2,990 (1991–1997) 233 (2001–2007) -92%

As popularized by free market economist Milton Friedman: "There's no such thing as a free lunch."

Conference Manual Page 50

© Grant Thornton LLP. All rights reserved. 15

IPOs maintaining IPO price 30 days after the offering (trailing 30 IPOs)

Facebook – Not an anomaly – Unintentional – Underlying causes

Distribution of Wall Street is too narrow (Problem we work with issuers to neutralize)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Success rate of IPOs maintaining issue price one month after going public

Source: Capital Markets Advisory Partners LLC, All rights reservedIncludes only corporate issuers, excluding funds, MLPs, SPACs and REITs.Based on the average success rate of the last 30 filed deals, up to one month ago. A successful deal is defined as trading at or above issue price one month after pricing.

Conference Manual Page 51

© Grant Thornton LLP. All rights reserved. 16

Changing tick sizes impacts short- and long-term market quality

Larger tick sizes will improve investor confidence, capital formation and job growth

Large-cap stocks (naturally liquid) Small- and micro-cap stocks (naturally illiquid)

Smal

ler t

ick

size

s

Decreases order depth Decreases order depth

Increases liquidity Decreases liquidity

Increases stepping ahead/gaming Increases stepping ahead/gaming

Increases quote flickering Discourages marketing (sales) support

Undermines investor confidence Discourages active research support

Discourages capital commitment

Undermines investor confidence

Larg

er ti

ck s

izes

Increases order depth Increases order depth

Decreases liquidity (but stocks are still extremely liquid)

Increases liquidity Discourages stepping ahead/gaming

Limits stepping ahead/gaming Encourages marketing (sales) support

Decreases quote flickering Encourages active research support

Improves investor confidence (market seems more transparent)

Incentivizes capital commitment Improves investor confidence

Sources: Grant Thornton LLP and Capital Markets Advisory Partners LLC.

Conference Manual Page 52

© Grant Thornton LLP. All rights reserved. 17

Quote: Bright Trading, 2012 Smaller tick sizes harming liquidity

"I think many of our problems with market liquidity in small and mid-caps can be traced right back to decimalization [tick sizes]," said Dennis Dick, prop trader at Bright Trading in Detroit. "Where decimalization has helped to reduce spreads in the large-cap space, it has actually harmed liquidity in the small- and mid-cap space." For blocks, "It's nearly impossible to execute any sizable order without significant price impact," Dick said.

SEC to Examine Tick Size for Small Caps Traders Magazine Online News April 17, 2012 John D'Antona Jr.

Conference Manual Page 53

© Grant Thornton LLP. All rights reserved. 18

The JOBS Act, Part 2: Two alternative solutions

Could be used individually or in combination:

1. Issuer choice of tick size, where issuers of all sizes, but small-cap companies in particular, are given the authority to choose their own tick size within a range (e.g., up to 5 percent of share price)

2. Algorithmic customization of tick size, where the SEC could automate the “mass customization” of tick sizes via a simple algorithm (e.g., tick size = natural spread TTM or natural spread TTM/2)

Conference Manual Page 54

© Grant Thornton LLP. All rights reserved. 19

What to expect going forward

Continued focus by Congress on improving our capital markets Is capital formation growing? Are the markets improving for smaller public companies and their

investors? Is investor confidence improving? Are jobs being created? Does SEC rulemaking reflect the intent of Congress with regard to

the JOBS Act.

Possible pause after the elections – Changes in Congressional leadership – Possible vacancies at the SEC

Conference Manual Page 55

© Grant Thornton LLP. All rights reserved.

David Weild [email protected] [email protected] 212-542-9979

Conference Manual Page 56

Growth Capital Investor

Investment ($B) Deals

0

$1

$2

$3

$4 billion

Jan. Feb. Mar. Apr. May June July Aug.

36

51

42

49 48

40 39

44

Growth Capital EPPs 2012

Source: PlacementTracker, a service of Sagient Research

Vol. I Issue 4 The Journal of Emerging Growth Company Finance September 3, 2012

SEC Cans Ad Ban on Private Placements

by Joe Gose

It’s hard to imagine any one constituent group being overly enthused about the Securities and Exchange Commission’s effort to write rules that implement general solicitation in private offerings as mandated by the JOBS Act. Although the proposal was accepted on a vote of 4-1, lawmakers and some

commissioners voiced displeasure that the SEC failed to meet the law’s proscribed 90-day deadline and that SEC Chairman Mary Schapiro late in the game elected to issue a proposal and take comments for 30 days instead releasing of an interim final rule. State regulators and other organizations predicting widespread fraud can’t be pleased that the proposal didn’t include their suggestions for strict, well-defined procedures for issuers to follow when verifying that a purchaser is an accredited investor.

Parties that lobbied to keep the verification process the same as it is today – largely certification by buyers that they are accredited investors via questionnaires – may be uncomfortable with the proposed “facts and circumstances” test to es-tablish a “reasonable belief ” that a purchaser is in fact an accredited investor. And although allowing general solicitation has been a centerpiece of discussion among market participants over the last several months, practitioners may nevertheless have a tough time wrapping their minds around the change.

“It’s kind of weird because you can now conduct a private placement and yet have general solicitation as long as your buyers are OK,” said Dean Hanley, a

SEC Files New Complaint Against NIR’s Ribotsky, Dworkin

by Paul Springer

The Securities and Exchange Commission filed an amended complaint against NIR Group, its founder Corey Ribotsky, and former analyst Daryl Dworkin. The document reiterates most of the commission’s al-

legations that Ribotsky engaged in fraudulent accounting, lied to investors and stole over $1 million from one of his funds, but it also provides new specifics to the regulator’s claims that Ribotsky profited from management fees from phan-tom gains and engaged in questionable accounting.

The suit was originally filed last September in Manhattan’s U.S. District Court.

Funds managed by NIR, which include four AJW entities and New Mil-lennium Capital Partners II, committed $225 million to 144 PIPEs from 1999 through 2010, according to PlacementTracker data.

IN THIS ISSUE Shells Brandish Emerging Growth

Company LabelThe JOBS Act is fueling a boom in the “emerging growth company shell” .........................................2

Turmoil at Direct Markets/Rodman & RenshawDisarray, losses, employee exodus, and regulatory censure take their toll at top PIPE banker. ..............3

Funds Sue DJSP Over Post-SPAC DisclosureTwo hedge funds are suing a foreclosure processing business that merged with a SPAC in 2010. ..........4

ALSO INSIDEBaystar’s Goldfarb Still Fighting Prosecution; Hedge Funds Say China Medical CEO Tanked Company; SEC Sues E-Lionheart for Dumping Billions of Shares; LuxeYard’s One Luxurious Deal; TJ Management in Bogus Placements, SEC Says; and other stories .....6

EPP, PIPE & APO MARKET DATAAggregate Year-to-Date Market Activity ...............17Deal Performance – Growth Capital EPPs ...........18Growth Capital EPP Candidates ..........................20Growth Capital and PIPE League Tables ..............21SPACs and Reverse Merger APOs ........................24

See Ad Ban on page 25

See Ribotsky on page 26

September 3, 2012 Copyright © 2012 MarketNexus Media, Inc. 25

Growth Capital Investor

partner in the Boston office of Foley Hoag. “It’s so foreign to the way people have been brought up on these issues.”

Reasonable TestsThe SEC’s long-awaited say on general solicitation stems

from Title II of the JOBS Act. Under the provision, Congress eliminated the ban on general solicitation in private offerings conducted under Rule 506 of Regulation D, provided issuers take “reasonable steps” – as determined by the commission – to verify that only accredited investors participate. Previously, is-suers were generally required to have a prior relationship with investors in such deals.

Individuals or couples that have net worth exceeding $1 million – excluding the value of a primary residence – as well as an individual with income of more than $200,000 or a couple with joint income in excess of $300,000 in each of the two pre-ceding years qualify as accredited investors.

Private placement issuers, including private and publicly traded companies and private investment funds, typically rely on the registration exemption provided by Rule 506. To implement the JOBS Act’s provision to end the ban on general solicitation, the commission is proposing to create Rule 506(c), under which issuers can advertise their offerings provided that certain condi-tions are satisfied. Not only must issuers take reasonable steps to verify that securities purchasers are accredited investors, they also must reasonably believe that buyers are accredited investors at the time of the offering.

Instead of establishing hard and fast steps that would pro-vide issuers with safe harbor – checking boxes that W-2s, tax returns or financial statements have been reviewed, for instance – the commission said it proposed the facts and circumstances test to provide flexibility to varying kinds of issuers and offerings.

To determine whether they’re reasonably verifying accred-ited investor status in any given transaction, issuers would con-sider several factors. Those include the nature of the purchaser and the type of accredited investor it claims to be, the amount and type of information that the issuer has about the purchaser, and the nature of the offering in terms of how the purchaser was solicited and the minimum investment amount.

In one example, the commission noted that the less infor-mation that an issuer has about a purchaser, the more steps it would have to take to verify accredited investor status, and vice versa. Additional steps an issuer could rely on include reviews of W-2s, reviews of industry trade publications that disclose com-pensation for certain employee levels, or the receipt of third-par-ty verification from a broker-dealer or accountant.

What’s more, the SEC said that an issuer using a website or social media to solicit buyers would probably be obligated to pursue more verification measures compared with targeting a list of pre-screened accredited investors compiled and verified by a broker-dealer. In other cases, if a minimum cash investment is so large that only an accredited investor could participate, no other

steps may be necessary, as long as the issuer has verified the buyer isn’t using third-party financing, the commission said.

Under the proposal, issuers would not lose the Rule 506(c) exemption if a non-accredited investor circumvented the rules and participated in the offering as long as issuers took reasonable verification steps and reasonably believed a purchaser was an ac-credited investor.

On balance, the facts-and-circumstances approach to deter-mining the “reasonableness” of an issuer’s means of qualifying buyers of Rule 506-exempted securities will likely mean restrict-ed securities purchasers will be required to disclose and confirm more financial information to issuers than has been the case in the past, when a short questionnaire and simple declaration of eligibility by would-be accredited investors was enough to satisfy the qualification requirements, said John Hogoboom of Lowen-stein Sandler.

“Now the question is, what are people going to do now?” he said. “I think the investor is going to have to disclose more information.”

Hogoboom also echoed the warnings of other securities counsel that relaxed federal general solicitation rules may conflict with individual states’ Blue Sky laws, particularly those states that had yet to adopt a Uniform Limited Offering Exemption rule for 506 offerings, noting that federal pre-emption cannot be relied upon to prevail in such instances.

Among other changes, the commission is proposing to add a check box to Form D for Rule 506(c) issuers so that the SEC can monitor its use. (Two commissioners urged the SEC to consider revising the final rule so that issuers would be required to file Form D prior to the offering to better prevent fraud. Issuers now file the form within 15 days after the first sale.)

The agency also is proposing to maintain Rule 506 and its ban on general solicitation, suggesting that some issuers may not want to comply with Rule 506(c) rules and may want to contin-ue to offer securities to up to 35 non-accredited investors.

Opening MarketsEliminating general solicitation restrictions could help small

private companies and hedge funds tap deeper reservoirs of capi-tal in a crowdfunding type of structure, predicted Alexander Da-vie, a partner with the Nashville, Tenn.-based Riggs Davie law firm. Angel investor networks are popping up in several markets around the country, he said, and issuers could conduct online offerings targeting those groups. The angel networks themselves could provide third-party accredited investor verification, he added.

“There are already networks in place that invest together in different local ventures, but they’ve always operated in a legal gray area because it’s possible that there have been violations of the general solicitation ban,” Davie said. “This section of the JOBS Act allows start-ups to market to people they don’t know at all. It has real potential.”

Ad Ban continued from front page

September 3, 2012 Copyright © 2012 MarketNexus Media, Inc. 26

Growth Capital Investor

On the other hand, Anna Pinedo, a partner in the New York office of Morrison & Foerster, echoed the conventional wisdom that small public companies likely wouldn’t use general solicita-tion in private placements. After all, what issuer wants to precip-itate a sell-off or shorting of its stock by announcing that they are about to launch a private transaction?

One issue that the SEC acknowledged in the proposal, but declined to address, centers on the content of potential advertis-ing materials. Some letter writers pointed out that hedge funds use different criteria to measure performance, which could con-fuse people, said David Pankey, a partner in the Washington,

D.C., office of McGuireWoods. Years ago mutual fund com-panies advertised using differing criteria as well, he added, but the commission eventually imposed a fairly standardized regime. Uncertainty over content could ultimately make some issuers hesitant to use Rule 506(c), he suggested.

“Some people think that the only folks who are going to use ad-vertising initially are those who are not credible,” Pankey said. “We don’t know that for sure, but there probably will need to be a fairly high confidence level for a majority of industry participants as to what the practice should be before they start advertising. Maybe the SEC will put something in the adopting release to clarify that.”

Dworkin plead guilty to charges of securities fraud in a sep-arate criminal case in 2010. Ribotsky resigned earlier this year from his management role at the AJW funds.

While the original complaint touched on Ribotsky’s educa-tional background, the new version is more direct.

“Defendants lied about the educational background of its principal,” the complaint says. “For example, the 2006 Offshore Private Placement Memorandum claimed that Ribotsky ‘re-ceived an MBA in finance and operations from New York Uni-versity, Leonard N. Stern Graduate School of Business.’ This was false. Ribotsky also gave the erroneous impression to investors at in-person meetings that he was a lawyer and had an MBA.”

The commission continues to maintain that Ribotsky and his firm The NIR Group LLC repeatedly lied to investors to hide the truth that his PIPE investment strategy was failing during the financial crisis. And the commission continues to state that although the manager told clients he could liquidate his PIPE in-vestments in four years, independent liquidity analysis indicates that some positions would have taken literal centuries to sell off.

One new allegation is that Ribotsky actually avoided realiz-ing gains when nebulous unrealized gains were more profitable to him personally. “Defendants never disclosed to investors that they declined the chance to realize some gains, albeit at some loss from face value, preferring to incur phantom unrealized gains on which management and performance fees could be charged,” the amended complaint alleges.

“NIR continued to earn management and performance fees that were calculated, in part, by reference to the period-over-pe-riod increase in unrealized gains for the AJW Funds’ now illiq-uid PIPE investment portfolio,” the SEC claims. “For example, during the first six months of 2008, NIR earned approximately $7.5 million in management fees.”

The commission had previously alleged that Ribotsky had created an investment entity called “Equilibrium Equity” that he used as part of a scheme to liquidate client assets and use the pro-ceeds for personal expenses. The new complaint says Ribotsky was warned by both NIR’s CFO and an outside accountant that

he should not take distributions from Equilibrium. The outside accountant said Ribotsky had improperly reclassified distribu-tions as loans, though there was no loan documentation or evi-dence or repayment.

Ribotsky lied to clients about liquidity in person and in written communications, the SEC alleges. “Ribotsky participat-ed in almost every meeting with prospective investors,” accord-ing to the SEC. “These misrepresentations about the time to exit investments were made to investors in all funds at numerous meetings, and were common to all NIR efforts to market the AJW Funds.”

The commission has added some detail to its accounts of Ribotsky’s dealings with “the Purchaser,” an individual the SEC does not identify other than generically as a finder. The purchase involved nine sales totaling $42.3 million of AJW Funds’ con-vertible PIPE debenture assets that allegedly had an actual face value of $12.6 million.

The commission cites an email communication as an in-dication that the sale was engineered to avoid recording a loss that would have to be revealed to fund investors. “We sell it to you,” Ribotsky purportedly said in an email to the Purchaser. “For marked value. So we don’t take a hit on the books.”

“The email exchange between Ribotsky and the Purchaser predating the transaction is telling in how nakedly it reveals that a major motivation for Defendants was not the best interests of the funds they managed, but preserving their fees,” the SEC said.

The commission’s attorneys continued, “As another email from the Purchaser noted, even though the note isn’t realized it ‘doesn’t have to be marked to market because it’s not a publicly traded security. Goes on your books but eliminates the aged pa-per off your books.’”

“Obviously if we do this,” Ribotsky allegedly replied, “this remains hush hush.”

The Purchaser defaulted on the note, to the detriment of fund investors, but the commission alleges Ribotsky had ample reason to have been suspicious of the Purchaser ahead of the transaction.

Ribotsky continued from front page

Growth Capital Investor

Investment ($B) Deals

0

$1

$2

$3

$4 billion

Apr. May June July Aug. Sept.

49 48

40 39

44

20

Growth Capital EPPs 2012

Source: PlacementTracker, a service of Sagient Research. September data thru 9/14/12.

Vol. I Issue 5 The Journal of Emerging Growth Company Finance September 17, 2012

Emerging Growth Issuers Largely Immune to Broad Market Sentiment

by Joe Gose

For all the focus being placed on boosting small business to create jobs and fuel an economic recovery, emerging growth companies struggling to find traction in the public markets.

As a group, small issuers that have conducted private placements over the last several months have generally lagged the stock market’s rise over the last year – the Dow Jones Industrial Average Index has risen 20% – suggesting that the firms are less influenced by broad market sentiment.

But exactly how far out of whack is the performance of small private place-ment issuers with the rest of the market? Growth Capital Investor reviewed equity private placement (EPP) activity from June 1, 2011 through May 30, 2012, using Sagient Research’s PlacementTracker database.

The analysis focused on growth equity private placements (GEPPs): unregis-tered and registered common stock sales, rights offerings, fixed-price convertible issuances, and non-convertible debt and preferred stock sales, issued at fixed-price issuance and conversion terms. No placements involving variable-priced securities, equity lines or at-the-market offerings were included. The issuer parameters fo-cused on emerging growth companies that had a minimum share price of $1 and market capitalizations ranging from $10 million to $1 billion.

The goal was to get a snapshot of how companies and a handful of active sectors performed following the transactions against comparable indices. While

SEC Forgoes Rule Making and Addresses Research Analyst Reforms under JOBS Act in FAQ

by Brett Goetschius

While much of the emerging growth capital market was fixated over the past two weeks on the Securities and Exchange Commission’s vague proposals lifting the ban on public solicitation for investments

in private placements, the agency issued a FAQ outlining its stance on the JOBS Act’s repeal of restrictions on sell-side research analysts’ participation in investment banking activities. While similarly paradigm-shifting in its impact on capital rais-ing, the release of the interpretative document has received little attention outside of securities law circles.

The SEC’s Division of Trading and Markets issued the FAQ in late August as an alternative to new rulemaking vis-à-vis the JOBS Act, which explicitly forbids

IN THIS ISSUE Muddy Solicitation Proposal Takes

Wind Out of CrowdfundersThe SEC’s proposed rules on general solicitation of investments draws jeers from the crowd cap-italists ..............................................................2

NIR Group Investors Faced with 97% LossInvestors in beleaguered PIPE fund manager received harsh news last week ............................................3

PIPE Player Rodman Closes Banking BusinessThe long-time most active banker in the PIPE market closes its doors .......................................................4

ALSO INSIDEDirect Markets Investor Pared Holdings Ahead of News; Internal Fixation Accused of Manipulation, Misleading Reporting; China Hydroelectric Sues Dissidents in Value Fracas; Fairfax Financial Shorting Case Tossed; SEC Suspends Shell Accountant Hatfield; SEC Sues China Sky One for Fake Revenue; and other stories ....................................................................5

EPP, PIPE & APO MARKET DATAAggregate Year-to-Date Market Activity ...............12Deal Performance – Growth Capital EPPs ...........13Growth Capital EPP Candidates ..........................15

See Immune on page 16

See FAQ on page 17

September 17, 2012 Copyright © 2012 MarketNexus Media, Inc. 17

Growth Capital Investor

and Needham & Co. The agents earned a cash fee of more than $4.4 million, or 3%.

The shares of New York-based application developer Viggle (VGGL), formerly Function (X), have fared the worst. They’ve plunged 94% since the company sold 14 million shares for $2.50 each – a 61.5% discount – to raise $35 million in August 2011. The deal also included three-year warrants to purchase another 14 million shares at an exercise price of $4 a share.

Banks Consistent PerformersBanks have exhibited the most consistent performance rela-

tive to a comparable index among the sectors reviewed. Shares of savings institutions that raised $1 billion in 18 transactions have climbed an average of 25% since their respective closings. That’s just 10 percentage points behind the KBW Bank Index (BKX)’s return performance over the 12 months ended Sept. 10.

Shares of Wheeling, Ill.-based Taylor Capital Group (TAYC) posted the best performance, surging 115% since it closed a 35 million rights offering in December. The biggest loser

was Norfolk, Va.-based Hampton Roads Bankshares (HMPR). Its shares fell 24% following its $45 million rights offering that closed in May.

Energy issuers, on the other hand, have woefully lagged the broader market. While the SIG Oil Exploration & Production Index (EPX) has fallen 3% over 12 months ended Sept. 10, oil and exploration companies that raised $1.4 billion in 19 private placements from June 1, 2011 to May 30, 2012 have seen their shares drop an average of 35% since the close of their respective deals.

Houston-based Halcon Resources Corp. (HK), formerly RAM Energy Resources, raised $900 million in three deals that closed in December, February and March. Its shares are up 140% following its December transaction, but they’ve tumbled 22% and 25% since the February and March closings, respectively. Hunts-ville, Tenn.-based Miller Energy Resources (MILL), which has seen its stock price appreciate 13% since raising $10 million in a non-convertible preferred stock deal in April, represents the only other oil and gas issuer with a positive performance.

preventing analysts from participating in capital raising meetings with investors and company management teams. That had been the case since the Global Analyst Research Settlement agreement on sell-side research activities was adopted in 2003. The post-JOBS Act interpretation of permitted analyst conduct construes the Act’s provisions “narrowly” according to Sidley Austin’s Jim Brigagliano, a former deputy director at the SEC, in a client briefing published in late August.

Brigagliano wrote that the SEC interprets the JOBS Act changes to provide that:

• Investment banking personnel may play a role in arrang-ing analyst communications with investors.

• Analysts may participate with investment banking person-nel in meetings with emerging growth company (EGC) management but may not solicit investment banking business.

• Analysts may not participate in road shows.• Research concerning EGCs may be published, post-of-

fering, without restriction both before and after lock-up agreements end, however they end—whether by expira-tion, termination, or waiver—as well as after both prima-ry (IPO) and secondary offerings of EGC securities.

• The Global Settlement was not affected by JOBS Act and Global Settlement firms must continue to comply with its applicable provisions unless and until such provisions are amended by court order or superseded by Commission or SRO rule.

With regard to analyst communications with investors and company management, Goodwin Proctor’s Eric Fischer noted

that while the SEC stated explicitly that the JOBS Act did not change the terms of engagement for any firm that was a party to the Global Settlement, “ firms not subject to the Global Settle-ment may permit research analysts and investment banking per-sonnel to attend meetings with company management, provided that the firm’s personnel do not otherwise violate the intent of the research analysts rules. This would happen if, for example, investment banking personnel at the meeting attempted to influ-ence the research analyst’s views or recommendations.”

Bingham’s Amy Natterson Kroll goes further, stating, “an analyst cannot change his or her research in an effort to obtain investment banking business, cannot allow an expectation of fa-vorable research coverage if the analyst’s firm is chosen to un-derwrite the IPO, cannot provide research that is inconsistent with the analyst’s personal views, and cannot engage in sales or marketing efforts related to an investment banking transaction.”

David Jenson of Leonard, Street and Deinhard adds that due to the SEC’s highly restrictive interpretation of the JOBS Act’s Section 105(b) “research analysts are still prohibited by NASD Rule 2711 from participating in road shows or engaging in communications with customers about an investment bank-ing transaction in the presence of investment bankers. Research analysts are also unable to participate in ‘test the waters’ commu-nications.”

The JOBS Act’s repeal of the ban on publishing sell-side research during an investment banking client’s IPO quiet period was not interpreted narrowly, but rather explicitly, by the agency, according to Kroll. “The SEC staff interprets [the act’s] Section 105(d)(2) broadly to override all quiet periods in the SRO rules

FAQ continued from front page

September 17, 2012 Copyright © 2012 MarketNexus Media, Inc. 18

Growth Capital Investor

Sign Up for a Subscription$1,995/year, includes complete online access to all articles.

n Invoice me n Charge my credit card

Card Number

Expiration Security Code

Signature

Name

Title

Company

Street

City State

Zip Country

Phone Fax

Growth Capital Investor

Fax this form to: 360-364-2752

Or mail to:MarketNexus Media, Inc.

P.O. Box 7172 Petaluma, CA 94955

Or send an email to:[email protected]

Questions? Call 707-364-2757

Satisfaction Guaranteed. If for any reason you are not satisfied with the publication, you may cancel at any time and receive a full refund of the unused portion of your subscription.