the internet of things: a prime opportunity for merchant acquirers

TRANSCRIPT

The Internet of Things: A Prime Opportunity for Merchant Acquirers The IoT and its ecosystems allow merchant acquirers to discover new sources of revenue and add more value for the customers they serve.

2 KEEP CHALLENGING November 2016

Executive SummaryThe payments industry, like many others, is undergoing

unprecedented change. Consumers’ experiences with online retailers

and “born digital” companies have raised their expectations of

digital interactions and transactions with financial institutions,

utilities companies and government agencies alike. To improve the

digital experiences they afford, merchant acquirers must deepen

their understanding of customer behavior, the current regulatory

environment, technology advances and options, and what

competitors are doing.

For example, emerging financial technology companies (fin-techs)

are already setting a high bar. Along with more progressive financial

institutions, they are churning out a slew of innovations that make

the ever-changing payments landscape even more complex and

challenging. Against this backdrop, payments players must work

harder to insulate their existing systems and processes from the ever-

present threat of fraud and security breaches.

2 KEEP CHALLENGING November 2016

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 3

As was evident during the adoption of EMV regulations in the U.S.,1

merchant acquirers are late in reacting to industry processes and

underlying changes.

To rectify this situation and succeed in the age of digital, these

companies can take advantage of the Internet of Things (IoT) –

the global network of small, powerful sensors and interconnected

“things” that enables physical devices objects – from desktop and

notebook computers, to wearables and smartphones – to link and

share data through the Internet. The IoT holds immense potential

for merchant acquirers to partner with device manufacturers to

generate new revenue streams and remain relevant in this continually

changing environment.

This white paper provides recommendations on how merchant acquirers

can tap into the IoT’s potential, take advantage of market dynamics and

trends, and confront the key challenges of the IoT’s growing network –

with the goal of giving decision makers the insights they need to define

and implement an effective IoT investment strategy.

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 3

4 KEEP CHALLENGING November 2016

The Changing Dynamics of the Acquiring Industry

Consumer BehaviorsToday’s financial Institutions face ever-increasing consumer and corporate demands – starting with the pressure to address the growing number of digital payment channels (mobile point of sale, contactless, near field communications (NFC) and wearables, for example). The surge of smart devices and applications has created a culture where immediate, secure access to information and services is not only expected, but demanded.

Increasingly, consumers expect a digital experience that approximates an ideal physical setting. Aside from one-click, type-or-swipe access, they look for fast, highly personalized service on demand, any time, at every encounter. They also expect these services to cost less. Financial institutions are quickly learning that it’s not just about processing transactions; it’s about engaging customers and delivering value throughout the transaction cycle.

New Competitive ThreatsEstablished payment institutions face competition from both traditional and non-banking players, such

as fin-techs. In fact, the competitive landscape is now populated with companies looking to expand their global footprint.

2 One of the most successful, Payoneer,

is ranked among the top 100 of Inc. 5000’s financial services companies. Its cross-border payments platform connects businesses, professionals and currencies in more than 200 countries. Established institutions are innovating by creating light-weight and offshoot brands. But the most notable developments have been seen in digital-born organizations such as PayPal, Google, Amazon, Apple and Square Inc., which have created services to complement their core business. Emerging digital wallets and the rapid proliferation of app-based mobile payments have enabled non-payment technology players to challenge, if not disrupt, the tradi-tional payment space.

There is a distinct possibility that credit card use will decline as consumers explore alternate modes of payment. As more innovations enter the marketplace, acquirers and other traditional payment companies will have to develop solutions that anticipate and accommodate consumer preferences and impending technologies.

For example, Square, Inc., develops and provides payment processing, point-of-sale (POS), financial and marketing services worldwide. The company automated its customer-onboarding and underwriting processes, significantly reducing the time it takes to get merchants up and running – from a few days or even weeks, to a few minutes. MasterCard already announced a program that it informally calls the “Internet of Payment Things” (IoPT). The goal is to turn any consumer gadget, accessory or wearable into a payment device – from a ring to a fitness tracker, to car keys and more.3

Due to their infrastructure and technology requirements, these kind of innovations are forcing conventional payment firms to strengthen their capabilities, particularly in back-office processing.

Financial institutions are quickly learning that it’s not just

about processing transactions; it’s about engaging customers and

delivering value throughout the transaction lifecycle.

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 5

Fraud: A Growing ConcernFraud remains a major issue throughout the payments industry – particularly in light of the increasing incidents of stolen credit-card numbers and personal data breaches that take place at various layers of the payments ecosystem (retailers, banks and acquirers). EMV provides a level of assurance by countering fraud with card-present transactions. But the cat-and-mouse game played by hackers suggests that threats will continue for the foreseeable future.

In 2015, card fraud reached $21.84 million – a figure that is expected to rise to $31.67 billion by 2020 – up 20.6% from 2014. According to Nilson, card fraud can now be attributed to the migration of card payments from magnetic stripes to EMV chips and pins.

4 Interestingly, a 2015 report from Barclays states that the U.S. leads

the way in credit card fraud, accounting for 47% of the total share. This in spite of the fact that the country makes up only 24% of the global card volume.

5

Assessing the Iot’s PotentialImagine that every single article in your pocket, in your briefcase and on your body could be used to make a payment. It is not far-fetched to think of a day when consumers will be able to use their car keys or finger rings to make payments in the grocery store. (The Internet of Things’ connected devices and mesh networks are among Gartner’s Top 10 Strategic Technology Trends for 2016).6

Thanks to the explosive growth of smartphones and tablets, and the increasing number of devices connected to the Internet at a much faster rate, the mobile payments market is expected to grow 122% from $325 billion in 2014 to $721 billion in 2017. By then, the use of mobile wallets is projected to increase 183%, and be available to over 43% of smartphone owners.

7 If all the devices

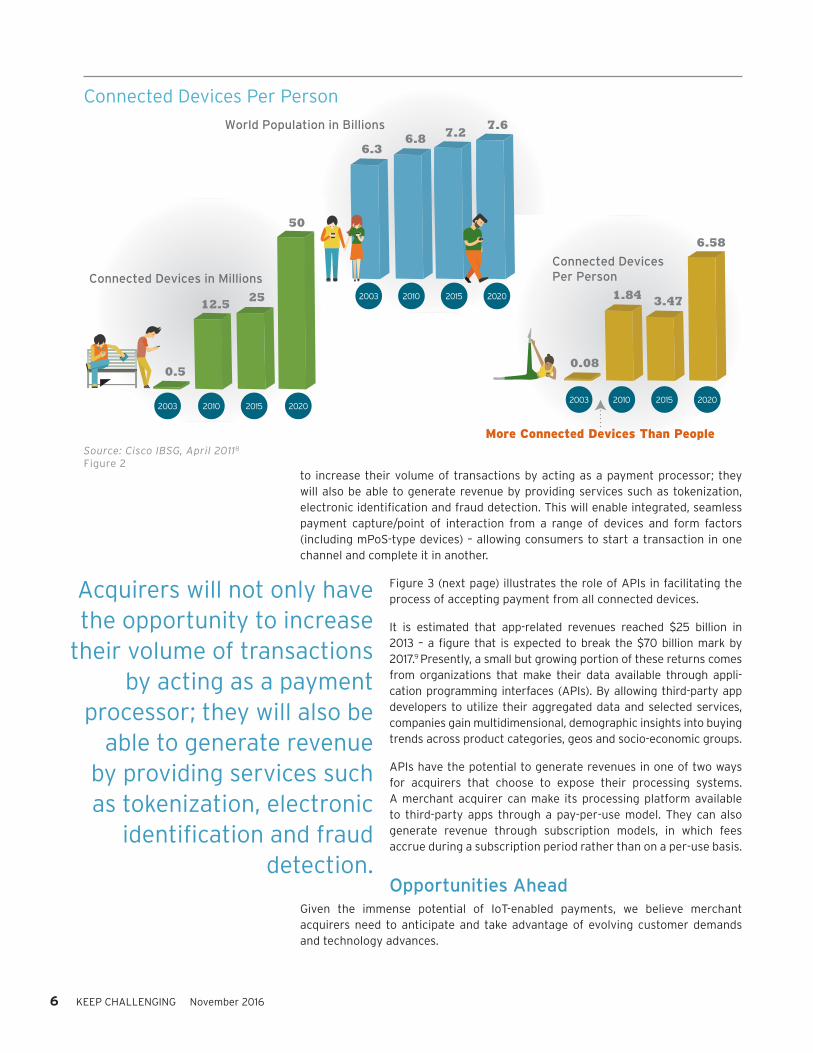

used for payment transactions are included, the market for payments processing would grow exponentially (see Figure 2).

The IoT represents the next stage of Internet development, and a major stride in how companies gather, analyze and distribute data. Over time, data and payments will become inextricably bonded; users will have a “digital identity” that stores everything from their payment details to digital signatures and biometric data.

Contextual Commerce for Merchants & AcquirersContextual commerce makes purchasing natural and simple – taking into account a person’s interests and intent to buy. For merchants, the Internet of Things’ vast connectivity makes it easy for consumers to purchase within an environment that is intuitive, familiar and comfortable. (Consider the recent “buy” buttons appearing on Facebook, Pinterest and other social media sites). For acquirers, there is the opportunity to provide various interfaces for accepting payments from all connected touchpoints, creating an omnichannel experience for customers.

At the same time, acquirers must be able to accept payments from all IoT touchpoints. Once merchants incorporate APIs into their open platforms (which they can either rent or buy), users can connect, manage and control all of their smart, IoT-linked devices in one place. Acquirers will not only have the opportunity

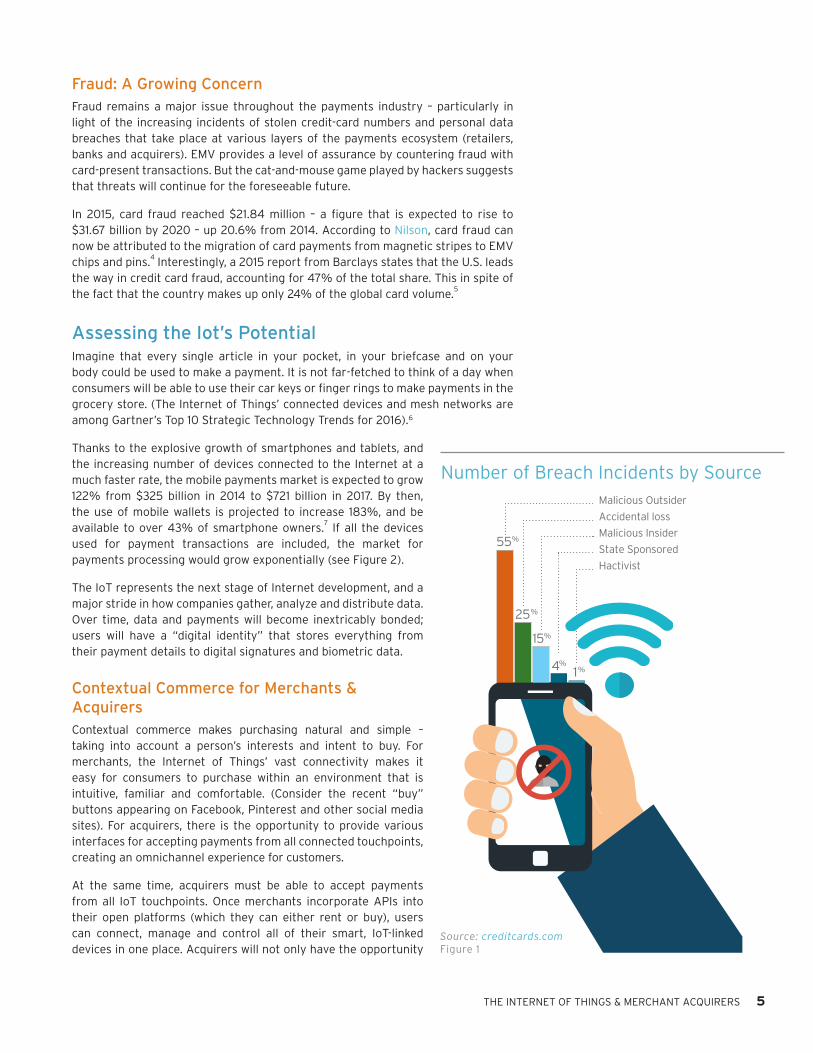

Number of Breach Incidents by SourceMalicious Outsider

Accidental loss

Malicious Insider

State Sponsored

Hactivist

55%

25%

15%

4%

1%

Source: creditcards.comFigure 1

6 KEEP CHALLENGING November 2016

to increase their volume of transactions by acting as a payment processor; they will also be able to generate revenue by providing services such as tokenization, electronic identification and fraud detection. This will enable integrated, seamless payment capture/point of interaction from a range of devices and form factors (including mPoS-type devices) – allowing consumers to start a transaction in one channel and complete it in another.

Figure 3 (next page) illustrates the role of APIs in facilitating the process of accepting payment from all connected devices.

It is estimated that app-related revenues reached $25 billion in 2013 – a figure that is expected to break the $70 billion mark by 2017.9 Presently, a small but growing portion of these returns comes from organizations that make their data available through appli-cation programming interfaces (APIs). By allowing third-party app developers to utilize their aggregated data and selected services, companies gain multidimensional, demographic insights into buying trends across product categories, geos and socio-economic groups.

APIs have the potential to generate revenues in one of two ways for acquirers that choose to expose their processing systems. A merchant acquirer can make its processing platform available to third-party apps through a pay-per-use model. They can also generate revenue through subscription models, in which fees accrue during a subscription period rather than on a per-use basis.

Opportunities AheadGiven the immense potential of IoT-enabled payments, we believe merchant acquirers need to anticipate and take advantage of evolving customer demands and technology advances.

Source: Cisco IBSG, April 20118

Figure 2

6.36.8 7.2

7.6

0.5

12.5 25

50

2003 2010 2015 2020

Connected Devices in Millions2003 2010 2015 2020

World Population in Billions

0.08

1.84 3.47

6.58

2003 2010 2015 2020

Connected DevicesPer Person

More Connected Devices Than People

Connected Devices Per Person

Acquirers will not only have the opportunity to increase

their volume of transactions by acting as a payment

processor; they will also be able to generate revenue

by providing services such as tokenization, electronic

identification and fraud detection.

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 7

Following are trends that the payments industry must prepare to act on and accom-modate in the near future.

Connecting All CustomersWhile mobile wallets make the payment process simpler and faster by taking plastic cards out of the equation, the industry needs to focus on a time in the not-too-distant future when virtually all devices will be connected through the Internet of Things and linked via standard Internet Protocols (IP) – resulting in a seamless, efficient and highly secure payment process.

For example, analytics will be used to predict a customer’s needs and make sug-gestions that the customer will see as valuable; in another scenario, companies can use inventory analysis and customer spending trends to offer customers options at the time of payment, such as similar products that are less expensive or have higher customer ratings. This can dramatically improve customer loyalty, increase mindshare and help improve the brand’s standing in the marketplace.

Ending the Checkout LineAn effective and feasible solution for minimizing lines in physical stores is long overdue. In the near future, consumers will not be expected to use their smart-phones to find items inside or outside a store, nor will they have to wait patiently in line to pay for their items with a plastic card as they do today. And they won’t have to perform contactless transactions by tapping their phones or watches against

Plug-and-Play Payment Processing

Source: McKinsey & CompanyFigure 3

Food Manager

Connected Devices

Token Service Provider

Secure PaymentGateway

8 KEEP CHALLENGING November 2016

a POS terminal. Instead, they will use cloud-based apps on their smartphones to check out purchases inside the store and, increasingly, use these devices to pay for items before they enter the store. These capabilities will be made possible by the many connected end points of the Internet of Things.

Complementing the Connected CarIn 2015, Visa unveiled its connected car proof-of-concept, which enables vehicles to not only communicate with each other on the road, but potentially become an extension of payment cards. This capability will enable seamless, on-the-go trans-actions, supported by advanced auto infotainment systems and critical safety

features. (See Figure 4).

The Smart ATMSince many acquirers have invested heavily in the ATM business, it’s important that they explore and exploit all the opportunities presented by smart ATM solutions, which leverage the Internet of Things to provide superior customer experiences, high security, and advanced analytical capabilities. Figure 5 illustrates the possibili-ties of smart ATMs, such as location-based messages/offers, behavioral messages/offers, wearables-based customer authentication, and predictive maintenance.

The Smart KioskThe smart kiosk is another example of solutions made possible by the IoT. It is imperative that acquirers invest in this channel to further enhance the customer experience. Figure 6 shows how smart kiosks can help increase customer satisfaction and loyalty, and support cross-selling and up-selling for retailers. These channels also enable retail distribution partners to offer advanced and efficient digital gifting solutions to consumers – creating a win-win for merchants and gift-card issuers.

Figure 4

The pump beacon senses a car’s arrival

at the station.

The beacon and the car app communicate to determine the amount of fuel needed

and place the order.

The customer pays from his car and

checks merchants’ loyalty offers.

Pay for Fuel, Compliments of the Connected Car

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 9

Smart ReplenishmentFuture devices will be smarter – able to take appropriate actions such as making purchases or payments. Amazon’s DRS (Dash Replenishment Service) is a notable example. DRS can be integrated with devices in two ways to place an order with Amazon. Device makers can either build a physical button into their hardware to reorder consumables, or measure consumable use so reordering can happen automatically. For example, an automatic milk dispenser with built-in sensors can measure the amount of milk remaining in its container and place an order before the milk runs out. Interestingly, device makers can start using DRS with as few as 10 lines of code.10 Acquirers need to develop a business model to tap into this payment market and other value-added services associated with it.

Predictive Analytics & Maintenance

Security &Validation

Customer PersonalizationBased on Environment

ProcessOptimization

Behavior Tracking

Customer AuthenticationIdentification Methods

Utilizes machine and location/environment sensors to better understand operational requirements (service, replenishment, etc.).

Uses data from location/environment sensors to further personalize the customer experience; for example, how long did they wait in line?

Employ environment and machine sensors to better understand and respond to the collective behaviors of a customer.

Expand customer authentication methods through the integration of sensor-based IoT solutions, such as smart watches.

Leverage machine and location/environment sensors to understand and prevent security and/or fraud incidents.

Use environment and machine-level data collected from IOT sensors to understand and improve operational and customer processes.

The Smart ATM

Figure 5

Figure 6

The Smart Kiosk

A Better & FasterBuying Experience

Digital Gifting, Rewards & Loyalty

Video Conferencing &Service Transactions

Instant Product Enrollment

Increased CustomerEngagement & Brand Loyalty

Campaign

Commerce & Services Anywhere

Engaging & Personalized

Integrated Experience

Augmented Reality Impending IoT payment trends include the use of augmented reality (AR) and virtual reality (VR) technologies. Consider a scenario in which a consumer uses a VR device to visit virtual stores; browse aisles and sample merchandise; then pay with their smartphone or another IoT-connected device — all without leaving the virtual world. With the advent of the IoT, companies should be able to apply AR and VR-related machine thinking to gather payment-related insights from the massive amounts of data generated by smart devices.

BlockchainNew machine-to-machine (M2M) and peer-to-peer (P2P) payment methods, including the cryptocurrency known as Bitcoin, are already staking their claim. Payment to a recipient (e.g., service provider) takes place when a prescribed set of conditions are met. The power of scriptable payments complements the intel-ligence of connected devices. Blockchain start-up Ethereum extended its reach into the IoT market by providing a decentralized virtual machine capable of executing peer-to-peer contracts using a crypto asset called Ether.11

APIs are simplifying the amalgamation and connections between connected devices, retailers and payment providers. The security measures of card networks in an open Internet domain can be made nearly impregnable with blockchain technology, which makes it possible to maintain an accurate, immutable record of transactions – adding another layer of IoT payment transactions and strengthening trust among all parties.

Countering FraudFraud continues to be among the biggest threats to financial institutions.12 Even with numerous technological advances such as EMV, the industry has not been able to create an impenetrable environment.

Examples of alternate payment types that might stand up to the persistent threat of fraud include:

InjectablesPositiveID, formerly known as VeriChip Corp., is a leading healthcare company in the U.S. It has made heavy investments in creating and testing syringe-injectable microchip implants for humans that can be used for cash and credit card transac-tions. This mode of payment would not only be fraud-proof, but also act as a barrier to identity fraud, since the device itself would be biometric in nature.

ImplantationsThe U.S. Food and Drug Administration (FDA) approved RFID chip implantation, a technology that is already being adopted in other countries, including Spain.13 These half-inch implants are useful payment methods that can help people avoid long lines and pay for beverages at a few exclusive clubs.

Fraud continues to be among the biggest threats to financial institutions. Even with numerous

technological advances such as EMV, the industry has not been able to create an impenetrable environment.

10 KEEP CHALLENGING November 2016

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 11

The emphasis on customer monitoring is a direct result of increasing incidents of online fraud and the ever-present possibility of hacked computer systems, especially those of retailers (in a card-not-present environment). The question is, will consumers be willing to replace their web site login data, credit cards, etc., with an embedded chip under their skin?

The use of injectables and implantations is a few years away from large-scale adoption, and their impact on the payments space isn’t a near-term concern. However, authorizing a transaction with a “selfie” is something that is already practiced. The industry’s consistent focus on technology innovation makes it essential for acquirers to prepare for the use of the IoT in biometrics, injectables and implanta-tions to counter the threat of fraud.

Words to the Wise

Consumer PrivacyWith sensors embedded in human beings, objects and places, the entire physical world is becoming orchestrated, intelligent, contextual and traceable. On the flip side, these capabilities are vulnerable to significant privacy and security loopholes.

A recent Altimeter Group survey of 2,062 U.S. consumers regarding IoT privacy found that at least half of respondents expressed extreme discomfort with potential encroachments of their privacy, as well as the use and sale of their data in the public space.14 These findings should be viewed not only in the context of citizens’ concerns about the confidentiality of their data, but also as an opportunity to develop and build stronger, lasting customer relationships.

That said, the Internet of Things poses some real risks to consumer privacy:

• Greater security exposures due to data-sharing across all connected devices.

• Ubiquitous data collection.

• The potential adverse consequences that may result from unexpected use of consumer data.

These exposures undermine consumer trust – making it extremely important for merchant acquirers and other payments players to take the necessary steps to assure consumer privacy and security:

• Build security into devices from the outset using techniques such as security risk assessment, rigorous security testing, smart defaults and encryption.

• Reduce data by collecting the minimal amount required for a specific purpose, and thereafter ensure its safe deposition. (This concept conflicts with the known benefits of big data, and is subject to further scrutiny).

• Assure that consumers give consent to collect and/or use their data.

Accommodating Colossal Data StoresThe Internet of Things will have a major impact on data-storage requirements, given that both personal (consumer-driven) and enterprise data will have to be stored. Big data is changing the way companies adapt to, scale to and analyze large, fast-moving streams of ambiguous data. Key verticals, such as healthcare and financial services, are already addressing this challenge. The role of IT admin-

The question is, will consumers be willing to replace their web site login data, credit cards, etc., with an embedded chip under their skin?

12 KEEP CHALLENGING November 2016

istrators will also evolve – requiring them to quickly figure out how to store and protect incoming data while making it accessible. Physical capabilities exist to meet the data-storage requirements for the Internet of Things, but managing the data is an entirely different problem. Unlike the current trend of centralized storage, organizations may need to store IoT data in distributed sites, then extract relevant data to a central site for downstream processing.

An Optimal Approach to IoT AdoptionIoT payments can range from traditional e-commerce/m-commerce to payment apps, near field communications, sensors and tracking devices. The acquirer system should be able to accept payment from all of these sources and process them effi-ciently and securely under current regulatory standards. Figure 7 below shows the payment value chain from an acquirer perspective.

Acquirers will need to consider the impact on the key processes that are necessary for IoT enablement:

Interface/API ManagementDeveloping APIs for the Internet of Things has many advantages. For example, acquirers will be able to process more transactions. And by integrating the entire range of IoT products and platforms via APIs, they will have the opportunity to generate additional revenue through subscription models.

Open APIs are required in order to read, send and access information among the connected devices and the server. However, designing open APIs at all levels of the IoT ecosystem, developing standardized formats for describing data generated by IoT devices, and allowing for the integration of data originating from various domains and providers remains a challenge.

Figure 7

The Payment Value Chain

Card

Check

Wallet

PaymentInstruments

POS

ATM

Phone/IVR

Mobile

Internet/IOT

AccountSetup

PaymentInitiation

Authentication &Authorization

Clearing & Settlement

Net Settle

LiquidityManagement

Fund Transfer

Statement

Accounting

Reconciliation

Capture

Validation &Enrichment

Fee Calculation

Posting

NetworkInterchange

AccountMaintenance

Fraud & RiskManagement

Security, Audit &Compliance

ExceptionManagement

BI &Reporting

InterfaceManagement

CustomerService

Fulfillment Services

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 13

When it comes to making or accepting payments from IoT devices, the following scenarios apply:

• Customers make payments from their own IoT-enabled devices. This can be browser- or app-based. The transactions will be treated as typical card not present (CNP) transactions – subject to compliance with relevant security regulations. IoT device manufacturers make software or hardware-level (e.g. NFC, eSE15) changes to enable payment and may be required to go through compliance certification (e.g. Visa Ready16) if applicable. Acquirers need to provide payment APIs that mer-chants or app developers can embed in their platform, which will enable users to make payments from all of their smart and IoT-based devices. The API would connect to the acquirer gateway for payment processing. Additional opportunity for acquirers lies in IoT device certification with pay-ment associations (e.g., Visa).

• Customers make payments from an acquirer-operated smart IoT kiosk or vending machine. To support these transactions, acquirers will need a gateway to an API-based connector for payment hardware installed on the IoT device. This will require partnering with a hardware provider that can build the right API to accept payments.

Acquirers will also need a way to identify these transactions as separate IoT transactions for differential processing, billing, reporting, etc.

Account Setup & MaintenanceMerchants that choose to accept transactions from IoT-enabled devices will want to have this feature enabled for them. The service provider should indicate the subscription model as well as the boarding system, which requires capturing and passing on this information for subsequent processing (e.g., authorization, clearing, settlement).

Authentication, Authorization & Data CaptureWhen it comes to payments, it is important to remember that people’s money is at stake. Therefore, acquirers must have control of actual payments in terms of authentication and authorization. Autho-rization data from gateway APIs for all IoT devices will have to be reformatted to industry-standard formats. This could involve additional data elements, depending on the compliance guidelines (e.g., EMV tokenization) and acquirer-specific reporting capability.

Interchange Fees & Compliance Transactions originating from IoT devices will oblige acquirers to make changes to their back-office processing to comply with regulatory mandates covering IoT payments. For example, Visa has extended its Visa Ready program for IoT payments, and will allow partners to implement EMV tokenization standards for such transactions.

Exception Management Dispute processing will be impacted by regulatory standards, which can change periodically. Acquirers need to continually update their systems to remain compliant.

Business Intelligence, Reporting & Analytics There will be a wealth of data generated from IoT transactions – compelling acquirers to employ analytics to generate actionable insights for merchants as a value-added service. IoT data can also be used for targeted marketing and promotions.

Merchant Education Merchants will have apprehensions and uncertainties during the various stages of IoT adoption. Therefore, from the acquirer’s point of view, merchant education and change management will assume an important role. This includes teaching merchants how to properly capture IoT-enabled transactions and comply with rules and regulations.

14 KEEP CHALLENGING November 2016

Putting IoT Payments in ContextAcquirers’ processes and back-end systems may not require major changes, since transactions generated from IoT devices should be treated like others. However, acquirers will need to add data elements in order for IoT payments to comply with regulatory standards and support additional business intelligence (BI) and reporting.

The Internet of Things presents two major challenges: standardiza-tion and security. This includes standardizing IoT protocols being used on top of existing architecture models. The good news is that payments are not particularly affected by the demands of stan-dardization, and even basic security issues can be overcome. The payments world already has a robust set of controls that can be plugged into any transactional scenario; the key issue is more about how to connect those devices to payment gateways.

The Road AheadMerchant acquirers face immense competition from new fin-tech players and established technology purveyors alike. As quality, simplicity, security, speed and multichannel consistency separate leaders from laggards, innovative products and services can open a world of possibilities for traditional acquirers and others across the payments processing space.

A new world is emerging where people will manage all of their payments-related data from a card, contactless, connected devices or even a biometric chip. The pro-liferation of mobile devices and consumers’ increasing need to remain connected quickly and safely – and have fast, easy and safe access to places and informa-

The payments world already has a solid set of controls

that can be plugged into any transactional scenario;

the issue is more about how to connect devices

to payment gateways for executing payments.

Figure 8

QualityFailure NotTolerated

PersonalizationUnderstanding the Individual

SecurityCreating Customer

Confidence

Participation The Active Customer

SustainabilityEnvironmental

Awareness

IntegrationCapitalizing on

Connections

Multichannel Anywhere. Anytime.

Any Device

Mobility No Gaps Allowed

ImmediacyNow or Not At All

SimplicityA Requirementfor Acceptance

Simplicity

The Attributes of a Winning Payments Play

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 15

tion paves the way for merchant acquirers to sharpen their competitive edge with payment options that suit the “connected life.”

The Internet of Things will provide a much-needed boost to traditional payment players and acquirers – allowing them to win and win back loyal customers and counter threats posed by non-traditional, nimble-footed competitors. Considering that the focus of newer payments players is to innovate and captivate customers, merchant acquirers will need to fall in line and set their sights on developing appli-cation protocols and tools that support new and innovative modes of payments and provide customers with a rich, consistent omnichannel experience.

Footnotes1 EMV stands for the first initials of Europay, MasterCard and Visa, the three

companies that created the standard. The U.S. is the last major country to adopt EMV chip technology in its payment cards. http://www.northbaybiz.com/General_Articles/General_Articles/In_the_Cards.php.

2 “25 FinTech Startups That Expanded Globally Despite Regulations & Other Problems,” https://letstalkpayments.com/25-fintech-startups-that-expanded-globally-despite-regulations-other-problems/.

3 MasterCard IoPT program press release. http://newsroom.mastercard.com/press-releases/mastercard-launches-new-program-that-can-turn-any-consumer-gadget-accessory-or-wearable-into-a-payment-device/.

4 Card Fraud Worldwide, The Nilson Report, October 2016, ISSUE 096. http://www.businesswire.com/news/home/20150804007054/en/Global-Card-Fraud-Losses-Reach-16.31-Billion.

5 “Credit Card Fraud and ID Theft Statistics,” September 16, 2015. www.creditcards.com/credit-card-news/credit-card-security-id-theft-fraud-statistics-1276.php.

6 “Gartner Identifies the Top 10 Strategic Technology Trends for 2016,” October 2015. http://www.gartner.com/newsroom/id/3143521.

7 “Two In Five Americans Will Use Mobile Wallets By 2017,” January 9, 2016. http://www.businessinsider.in/Two-In-Five-Americans-Will-Use-Mobile-Wallets-By-2017/articleshow/28598110.cms.

Quick Take

• Provide developer-friendly APIs so merchants and device-specific app developers can easily process payment transactions from all types of consumer devices and gadgets.

• Leverage open APIs and standardized data formats to integrate processing systems with transactions originating from the IoT network.

• Utilize the power of big data to support merchant requirements and generate actionable insights from

the volumes of transactions originating from IoT devices.

• Provide merchants and app developers with the option to use pay-per-use or subscription models to access processing platforms through the APIs.

• Establish a dedicated change management team to educate merchants on the pros and cons of the IoT.

• Address security-related challenges.

Merchant acquirers looking to employ the Internet of Things should consider the following:

16 KEEP CHALLENGING November 2016

8 “How the Next Evolution of the Internet Is Changing Everything,” CISCO, April 2011. http://www.cisco.com/c/dam/en_us/about/ac79/docs/innov/IoT_IBSG_0411FINAL.pdf.

9 “Monetizing Mobile Apps: Striking the right balance,” McKinsey Quarterly, June, 2014. http://www.mckinsey.com/industries/high-tech/our-insights/monetizing-mobile-apps.

10 Amazon DRS. https://www.amazon.com/oc/dash-replenishment-service.

11 Ethereum project. https://www.ethereum.org/.

12 Top Fraud Risks for Financial Institutions in 2016. https://securitytoday.com/Articles/2016/01/27/5-Top-Fraud-Risks-for-Financial-Institutions-in-2016.aspx?Page=1.

13 RFID Implantation in Barcelona. http://news.bbc.co.uk/2/hi/technology/3697940.stm.

14 Altimeter Group Survey of Privacy in the IoT. http://www.altimetergroup.com/2015/06/.

15 eSE (embedded secure element) is a tamper-proof chip available in different sizes and designs that can be embedded in any mobile device to ensure safety of the data stored.

16 Visa Ready program for IoT. https://usa.visa.com/visa-everywhere/innovation/visa-brings-secure-payments-to-internet-of-things.html.

References• “Gartner Says by 2016, 25 Percent of the Top 50 Global Banks Will Have Launched

a Banking App Store for Customers,” Gartner Newsroom, June 4, 2014. http://www.gartner.com/newsroom/id/2758617

• “Era of Mass Customization in Banking,” Bank Innovation, April 17, 2014. http://bankinnovation.net/2014/04/era-of-mass-customization-in-banking/

• “Monetizing mobile apps: Striking the right balance,” McKinsey Quarterly, June, 2014. http://www.mckinsey.com/insights/high_tech_telecoms_internet/monetizing_mobile_apps

• “A key focus of ASB’s API move is addressing real issues in corporate, commercial and rural banking, executive says, in ‘bridges not walls’ move,” interest.co.nz, October 21, 2014. http://www.interest.co.nz/business/72519/key-focus-asbs-api-move-addressing-real-issues-corporate-commercial-and-rural-banking

• “Open API for Bank Apps: Can Credit Agricole’s Model Work Here?” American Banker, July 29, 2013. http://www.americanbanker.com/magazine/123_8/open-api-for-bank-apps-can-credit-agricoles-model-work-1060535-1.html

• “Samsung and Visa Take NFC Mobile Payments Global,” Mashable, February 25, 2013. http://mashable.com/2013/02/25/samsung-visa-nfc/

• “Amazon to move into P2P and in-store payments,” Finextra, January 30, 2014. http://www.finextra.com/news/fullstory.aspx?newsitemid=25675

• “Alternative Payments and the Internet of Things,” FIS Payments Leader, September 18, 2014. http://www.paymentsleader.com/alternative-payments-and-the-internet-of-things/

• Opening Remarks of FTC Chairwoman Edith Ramirez on “Privacy and the IoT: Navigating Policy Issues,” International Consumer Electronics Show, January 6, 2015. https://www.ftc.gov/system/files/documents/public_statements/617191/150106cesspeech.pdf

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 17

About the Authors

Arijit Mukherjee is a Business Analyst in Cognizant’s Banking and Financial Services Payments Practice. He has worked in the IT industry for over 11 years, leveraging strong development and strategic planning skills with deep knowledge of the payments business. He has worked in several strategic engagements for key acquirers in North America and is also actively involved in business model analysis and process design activities for the practice. He can be reached at [email protected] | LinkedIn: https://www.linkedin.com/in/arijit-mukherjee-ab442436.

Soumya Das is a Delivery Manager within Cognizant’s Banking and Financial Services Payments Practice. With over 13 years of industry experience, he possesses strong program and delivery management skills combined with in-depth knowledge of the banking and financial services domain. He has successfully managed end-to-end delivery of several key engagements and is also actively involved in business development activities for the business unit. He can be reached at [email protected] | LinkedIn: https://www.linkedin.com/in/soumyad1.

Sanjoy Anand works within Cognizant’s Banking and Financial Services’ North America Payments Practice and has spent over 17 years in the payments business. He has worked at Cognizant since 1998 and has served in several roles from development through project, program and delivery management. He is currently a Program Manager for a leading payments services customer in the U.S., and manages large program implementations in the U.S., Europe and LATAM. He can be reached at [email protected] | LinkedIn: https://www.linkedin.com/in/sanjoyanand.

Vijay Venkataraman is a Practice Leader within the Connected Ecosystems Lab in Cognizant’s Global Technology Office. With over 20 years in leadership roles for technology practices such as enterprise content management, portals and cloud, he has provided solutions for diverse industry verticals such as banking and financial services, insurance, healthcare, manufacturing, logistics, and energy and utilities, among others. Currently, he leads platforms, solutions and consulting initiatives focused on helping customers solve their business problems – leveraging the IoT, cloud and related technologies. He can be reached at [email protected] | LinkedIn: https://www.linkedin.com/in/vijay-venkataraman-96620766.

Pushpendu Gupta is part of the Cognizant Business Consulting team’s Payments Practice. Through his rich experience across diverse client engagements, he brings valuable industry insights and perspectives in business functions. He is an integral part of the consulting team driving digital initiatives, and works closely with many of our large clients – helping them define and build industry-y relevant offerings and services. He can be reached at [email protected] | LinkedIn: https://www.linkedin.com/in/pushpendu-gupta-70a6a92.

• “The Six Things That Will Define Payments In 2016”, PYMNTS.com, January 4, 2016. http://www.pymnts.com/news/mobile-commerce/2016/the-six-things-that-will-define-payments-in-2016/

• “The connected car: Visa looks ahead, Visa. https://usa.visa.com/visa-everywhere/innovation/visa-connected-car.html

18 KEEP CHALLENGING November 2016

THE INTERNET OF THINGS & MERCHANT ACQUIRERS 19

World Headquarters500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233

Fax: +1 201 801 0243Toll Free: +1 888 937 3277

European Headquarters1 Kingdom Street

Paddington CentralLondon W2 6BD

Phone: +44 (0) 207 297 7600Fax: +44 (0) 207 121 0102

India Operations Headquarters#5/535, Old Mahabalipuram Road

Okkiyam Pettai, ThoraipakkamChennai, 600 096 India

Phone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060

© Copyright 2016, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

Codex 2042

About Cognizant Banking & Financial Services Cognizant’s Banking and Financial Services business unit, which includes consumer lending, commercial finance, leasing insur-ance, cards, payments, banking, investment banking, wealth management and transaction processing, is the company’s larg-est industry segment, serving leading financial institutions in North America, Europe, and Asia-Pacific. These include six out of the top 10 North American financial institutions and nine out of the top 10 European banks. The practice leverages its deep domain and consulting expertise to provide solutions across the entire financial services spectrum, and enables our clients to manage business transformation challenges, drive revenue and cost optimization, create new capabilities, mitigate risks, com-ply with regulations, capitalize on new business opportunities, and drive efficiency, effectiveness, innovation and virtualization.

For more, please visit http://www.cognizant.com/banking-financial-services.

About CognizantCognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process services, dedicated to helping the world’s leading companies build stronger busi-nesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innova-tion, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 100 development and delivery centers worldwide and ap-proximately 255,800 employees as of September 30, 2016, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world.

Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.