the international edition - gerald eve · engage speaks with renata osiecka, managing partner at...

TRANSCRIPT

ATIENGAGE SPRING 2015

8882538994992

ENGAGE SPRING 2015

2655378940092TINENGAGE SPRING 2015

6623689375672

ALDENGAGE SPRING 2015

9956827850286EVE

ENGAGE SPRING 2015

7835269004642

DESENGAGE SPRING 2015

8236445690001

GERENGAGE SPRING 2015

0000158842276

Euro-Vision

How a European marketplace has broken down borders

Rooms with a long-term view

Hotels’ new presences in Europe’s major destination cities

Where now for European real estate investment?

EuroProperty’s Mike Phillips follows the money

SPRING 2015 ISSUE NINE WWW.GERALDEVE.COM

THE INTERNATIONAL EDITION

WEST END FLOOR REVIEWA floor-by-floor analysis of the West End office market

Q1 2015

CITY FLOOR REVIEWA floor-by-floor analysis of the City office market

Q1 2015

02NEWS UPDATECatch up with the latest news and developments at Gerald Eve

01CONTENTSSPRING 2015

WWW.GERALDEVE.COM

07 PROPERTY TAXATIONIN EUROPE

ENGAGE looks at how property taxes compare across Europe’s major economies

16ANGLING FOR SUCCESS WITH SIMON PRICHARDEngage sits down with Simon Prichard to learn more about the man and his ambitions for the firm

ENGAGE talks to Cara Richardson of insurance brokerage Arthur J. Gallagher & Co

11INSURANCE PREMIUM

EURO-VISION – HOW A EUROPEAN MARKETPLACE HAS BROKEN DOWN BORDERS FOR INVESTORS AND THEIR ADVISERS

04

The debate surrounding the UK’s continued membership of the European Union has risen up the political agenda

19 22

WHERE NOW FOR EUROPEAN REAL ESTATE INVESTMENT?14

Mike Phillips, editor of EuroProperty, casts his eye over the investment market

Hotel brands old and new have spotted an opportunity to establish new presences in Europe’s major destination cities

ENGAGE speaks with Renata Osiecka, managing partner at AXI IMMO in Warsaw, part of Gerald Eve International, and her daughter Joanna

For more information please contact Fergus Jagger, +44 (0)20 7653 6831, [email protected] (City)Lloyd Davies, +44 (0)20 7333 6242, [email protected] (West End)

EDITOR’S NOTE

The past year has been a busy one for Gerald Eve, and one which has been characterised by change. There has been change in the marketplace to a more optimistic outlook across many sectors and there has been change internally, with many positive initiatives taking shape at Gerald Eve.

In response to client feedback we have launched Gerald Eve International, a best in class group of like-minded advisers in key locations throughout Europe and, ultimately, beyond. Since its launch at the end of the 2014, we have been involved in instructions in Ireland, Poland, India and France with further opportunities currently in the pipeline.

This edition of ENGAGE will have a distinctly international flavour as we are excited by the opportunities afforded by Gerald Eve International to date, and even more excited about the potential for future opportunities.

There have been further changes elsewhere within Gerald Eve as Simon Prichard takes over as Senior Partner from Hugh Bullock, who becomes Chairman. ENGAGE has an in-depth chat with Simon taking in his career to date and his future hopes and aspirations for Gerald Eve.

Looking outward, the emerging theme for the UK property market seems to be one of optimism, based on: substantial demand for property as an asset class; availability of overseas cash – particularly from North America; the return of bank liquidity and the prevalence of UK Retail Funds awash with cash.

But lest we get carried away on a wave of unbridled optimism, the recent election will inevitably have an impact on the market until there is more clarity on changes to taxation, housing and planning policies. The industry at large will be watching closely and hoping that the feel good factor will remain.

Amy Potter – [email protected]

ROOMS WITH A LONG-TERM VIEW

RELATIVELY SPEAKING

2017 RATING REVALUATION WINNERS AND LOSERS REVEALED

Gerald Eve is currently finalising its own ‘shadow revaluation’ of all 1.8m non-domestic properties in England and has forecast that retailers on Bond Street, Oxford Street and Regent Street will see their bills rise by 80% from April 2017. But many businesses will gain from the revaluation, with bills forecast to fall by up to 40% in Walsall, Stockton and Dewsbury. Gerald Eve is in the process of completing its research, including a similar exercise for Wales and Scotland.

Jerry Schurder, head of business rates at Gerald Eve, said: “We know how critical it is for our clients to be able to prepare accurate budgets and our shadow revaluation means we will have the capability to help them understand what their bills should be in two years’ time.”

Download Gerald Eve’s business rates app from https://www.geraldeve.com/get-the-data-web-app/for a wealth of information regarding business rates.

03ENGAGEISSUE NINE

NEWS UPDATESPRING 2015

WWW.GERALDEVE.COM

KEY DEAL FOR GERALD EVE INTERNATIONALGerald Eve’s London investment team has completed the £26.1m acquisition of 10 Dean Farrar Street for the CERN Pension Fund.

Located directly behind New Scotland Yard, the 30,000 sq ft multi-let freehold office building was let to five different tenants with a weighted average unexpired lease term of 3.5 years. The space had been recently refurbished and all of it let within the last three years.

Lloyd Davies, partner at Gerald Eve, comments: “Although the global investment appetite for London product is hardly a secret, it is particularly gratifying to have been introduced, via our international colleagues, to a blue-chip investor able to conclude a deal so swiftly.”

The deal represents a major transaction for Gerald Eve International. CERN is a long-standing client of Paris-based Estate Consultant, which specialises in investment consultancy and corporate real estate advice.

NEWS UPDATE

02 ENGAGEISSUE NINE

NEWS UPDATESPRING 2015

GERALD EVE TOPS RATING AGENTS TABLE

Gerald Eve has been named as the UK’s leading rating agent, advising on property with a combined rateable value in excess of £560m.

Analysis of Valuation Office Agency data relating to assessments with a rateable value greater than £10m, published by property industry news service CoStar, revealed Gerald Eve to be involved in appeals on real estate with an aggregate rateable value of £568,700,000 – nearly three times that of nearest competitor CBRE and more than the agents placed second to seventh put together.

GERALD EVE HIGHLY COMMENDED AT PROPERTY WEEK AWARDS

Congratulations to the Alternative Markets Team who were highly commended at the 2015 Property Awards in the Professional Agency of the Year category.

The Property Awards are the UK’s leading and most prestigious annual awards dedicated to the

property industry, celebrating excellence from both individuals and companies who have made a significant impact over the last year.

The results were announced on 21st April at a gala ceremony held at Grosvenor House in London.

GERALD EVE INTERNATIONAL EXPANDS IN NORTHERN EUROPE

Gerald Eve International has expanded with the addition of Austria and Slovakia. Modesta Real Estate, which has offices in Bratislava and Vienna, will provide vital coverage throughout this region. The firm, which specialises in office agency, industrial and logistics, CRE and investment consultancy, boasts a client list including Axa Real Estate, DHL, Prologis, P3 and Rolls Royce. Discussions are also underway with representatives in Switzerland (Geneva) and Russia (Moscow).

MITSUBISHI UNVEILS PLANS FOR 40-STOREY LANDMARK TOWER AT THE HEART OF THE CITY OF LONDON

Gerald Eve has submitted a planning application to the City Of London Corporation on behalf of Mitsubishi Estate London Limited for a 40-storey office tower at the heart of the City. The scheme has been conceived to be an exemplar in urban office design, featuring some of the highest sustainability and low energy features. Situated in the City’s Eastern Cluster of tall buildings the redevelopment of 6-8 Bishopsgate, EC2 and 150 Leadenhall Street, EC3 is rated as one of the most prized sites in the Square Mile.

Mitsubishi Estate, Japan’s leading developer, is seeking to bring forward the comprehensive regeneration of the site. The proposals provide an office-led, mixed-use tower with flexible retail use and a public access viewing gallery at level 40. The 71,501 (GEA) sq m building is designed by Wilkinson Eyre Architects.

Mr Naoki Umeda, managing director and CEO of Mitsubishi Estate London said: “The submission of this application represents Mitsubishi Estate’s confidence in the City of London’s long term growth prospects as a world financial centre, and its attractiveness for blue chip companies. We look forward to enhancing the offer of the City further by delivering a striking landmark building at this fantastic location.”

PRESTIGIOUS MANAGEMENT MANDATE SECURED FROM GLOBAL INSURANCE GIANTGlobal insurance brokerage Arthur J Gallagher & Co has appointed Gerald Eve on a three-year asset management brief encompassing its entire UK portfolio.

The appointment will see Gerald Eve take responsibility for full portfolio management services including lease advisory, disposals and acquisition, building consultancy and providing full rating advice.

Arthur J Gallagher’s UK portfolio comprises 115 properties with around 136 leases, including its flagship City HQ at the Walbrook Building.

Arthur J Gallagher has experienced significant growth over the past two years following its acquisition of the Giles Business and Oval insurance.

04 ENGAGEISSUE NINE

FEATURESPRING 2015

HOW A EUROPEAN MARKETPLACE HAS BROKEN DOWN BORDERS FOR INVESTORS AND THEIR ADVISERSFOR THE FIRST TIME IN THE BEST PART OF TWO DECADES THE TOPIC OF EUROPE AND, IN PARTICULAR, THE DEBATE SURROUNDING THE UK’S CONTINUED MEMBERSHIP OF THE EUROPEAN UNION HAS RISEN UP THE POLITICAL AGENDA.

EURO-VISION

The rise of the UK Independence Party (UKIP) prompted the mainstream parties into delivering euro-sceptic rhetoric which has,

in turn, fuelled debate and speculation in the media.

According to a recent survey by the CBI and YouGov, eight out of ten British businesses would prefer to see the UK remain in the EU. “Firms want what is best for jobs and growth and there is a genuine concern that an exit would hit business investment and access to the world’s largest trading bloc”, said the CBI’s director general, John Cridland, in response to the survey results.

A more recent survey by the law firm Maples Teesdale showed that just over half of UK property investors think an exit from the EU would be detrimental to their business. “What investors value above all else is certainty and the prospect of a referendum casts a shadow of uncertainty over a market in which cross-border investment activity has become the norm,” said Maples Teesdale partner Neil Sagoo.

By any measure, the property industry has been a net beneficiary of the single market afforded by the EU. The flow of capital across borders, the free movement of construction labour and an enhanced occupational market have all contributed to creating a more sophisticated and diverse property market. Within the European Union, investors are able to diversify their activities, spread their risk and pursue new opportunities on a level playing field. This has created new opportunities for property advisers and fuelled a frenetic round of M&A activity in the sector at the turn of the millennium.

In more recent years, Gerald Eve’s client base – both in terms of investors and corporate occupiers – has become more Euro-centric and the level of cross border activity has increased. This has led to the creation of Gerald Eve International (http://www.geraldeve.com/international/), a group of 15 associated companies offering best-in-class real estate expertise throughout Europe and on a case by case basis, work with other best-in-class companies in different European locations as well as in parts of Asia.

WWW.GERALDEVE.COM

05ENGAGEISSUE NINE

FEATURESPRING 2015

offer a best-in-class service which follows clients and gives them access to the advice they need, where they need it. This is why selecting the right partners with the right skillsets is crucial. We need to be comfortable knowing that our international partners will deliver a service comparable to what our clients have become accustomed to here in the ‘UK’.

Unlike many other international alliances, Gerald Eve International is non-exclusive and therefore doesn’t demand that associates work only with one another. This offers one significant advantage, according to LeMarechal, “Because everyone can work with whoever they want to, it places the emphasis on each individual associate to provide the best service and be as collaborative as they can, as there is no guarantee they will be instructed again otherwise.” This ethos is crucial to cementing the reputation of the group and in giving clients the assurance that they are working with the best people for the job, regardless of location.

Assembling the group took just over a year, with the process beginning

towards the end of 2013. The first part of the process involved engaging with clients to find out where they needed help, and the second part of the process was identifying the right partners in those locations. In some cases this was straightforward as existing relationships were in place. Additional associates were identified early in 2014 and, in June, shortlisted parties were invited to London to discuss the concept in more detail. Contracts were then put in place and the initiative was formalised by the end of 2014. Further associates will be added to the group during the course of this year, with target locations including the Channel Islands, Italy, Portugal and the USA.

According to LeMarechal, feedback from clients to date has been very positive, as she explains: “They are pleased that we have expanded our scope beyond the UK. They also see it as a real alternative to the existing offerings in the marketplace. Clearly as more and more our clients become aware of our capabilities within Gerald Eve International, more and more opportunities will arise.”

››

Gerald Eve International will provide a comprehensive international offering to clients across Europe. The first affiliates cover Belgium, France, Ireland, Luxembourg, The Netherlands, Poland, Spain, Turkey and Northern Ireland with more than one partner in certain locations to provide different geographical and sector specialisms.

As Patricia LeMarechal, the Gerald Eve partner tasked with co-ordinating the group, says: “Clients have been coming to us for some time now saying we are doing a great job for them and asking how we might help them in their activities outside the UK. Gerald Eve International is a direct response to this and our initial choice of partners reflects those regions in which clients need help and support.”

The rationale behind Gerald Eve International is to offer something different and to provide a service which is client-led above all else. It is not simply about scale and having offices everywhere – it is about offering a group of specialists across a range of disciplines. LeMarechal explains: “In order to be successful we need to

Because everyone can work with whoever they want to, it places the emphasis on each individual associate to provide the best service and be as collaborative as they can, as there is no guarantee they will be instructed again otherwise.

06 ENGAGEISSUE NINE

FEATURESPRING 2015 07ENGAGE

ISSUE NINEFACTS & FIGURESSPRING 2015

WWW.GERALDEVE.COM

JAMES MULHALL, MURPHY MULHALL (IRELAND)

With a thriving office and agency investment business in Dublin, James Mulhall was quick to spot the opportunities offered by Gerald Eve International, both in terms of attracting new investors into Ireland and serving his existing clients’ aspirations beyond the emerald isle. “One of the attractions of Gerald Eve International is a business culture that reflects our own. It is a peer-to-peer group which offers direct access to the business owners and which shares a deal-driven mentality,” he says.

As Ireland heads towards economic recovery, Mulhall believes it presents a real alternative to European investors. “2015 will be an interesting year with a number of loan portfolio sales being released, which potentially offers a great opportunity. Add to that a real lack of supply in the Dublin office market, which is driving rental growth of up 30%, and it’s easy to see why we’re confident of seeing investment activity increase in the coming year,” he says.

RENATA OSIECKA, AXI IMMO GROUP (POLAND)

As the market-leading industrial agency in Poland, Axo Immo is a natural fit with Gerald Eve International. Principal Renata Osiecka, believes the group presents a significant opportunity to expand her scope of services. “As a local company with a lot of international clients, the opportunity to expand our coverage is obviously very attractive. I also believe there is an opportunity to gain a collective reputation for excellence and to set a benchmark for service across the entire group,” says Osiecka.

Having worked at larger agencies during her career, Osiecka is a firm believer that Gerald Eve International offers something unique. She attributes much of this to the culture: “The involvement of all the partners in the group is much more intensive than I have seen in the past and there is a huge amount of knowledge exchange. Together I believe we have a very real opportunity to secure some major European mandates.”

FREDERIC PRENOT, SOROVIM (FRANCE)

With offices in Lyon, Sorovim is an investment specialist which advises a number of French institutions. Board member, Frederic Prenot, views Gerald Eve International as an opportunity to service major French investors in their overseas activities. “Many French investors are finding opportunities too limited in France and are beginning to look further afield. They are primarily focussed on staying within the Eurozone, though the UK is obviously an attractive market to them,” he says.

Explaining the appeal of Gerald Eve International, he says: “The fact that all the partners in the group are independently owned was also important to us as it offers direct contact with other business owners and a simple way of exchanging information. Hopefully it will give us the platform not only to follow our existing clients out of France, but also to gain access to other European investors.”

For further information please contact Patricia LeMarechal on +44 (0)20 7653 6851, [email protected]

ENGAGE TALKS TO SOME OF GERALD EVE INTERNATIONAL TO HEAR THE REASONS WHY THEY JOINED AND WHERE THEY SEE THE BUSINESS OPPORTUNITIES FOR THEM.

IN THE GLOBAL MARKETPLACE FOR INWARD INVESTMENT, ENGAGE LOOKS AT HOW PROPERTY TAXES COMPARE IN THE MAJOR ECONOMIES THROUGHOUT EUROPE. STATISTICS FROM 2013 (LATEST FIGURES) BY THE ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT SHOW THAT THE UK HAS THE HIGHEST LEVEL OF PROPERTY TAXATION IN EUROPE, ACCOUNTING FOR 3.2% OF GDP.

Property Tax is a major cost of occupation in the UK providing a large contribution to overall tax revenues, it is therefore easy to see the Government’s attraction to property taxes –

relatively easy to implement, difficult to evade – however there is a growing sense that the limits of what can be shouldered are being reached. As the burden increases, so does the possibility that investment will go elsewhere.

So how does the UK stack up against its European neighbours, the very countries competing for investment and looking to attract multinational companies to their shores? Put simply, it doesn’t compare well. To explore the topic further, Engage spoke to offices across the Gerald Eve International group to find out a bit more and compile the European property tax league.

PROPERTY TAXATIONIN EUROPE

*Comparable to others listed in this article.

TAX BASISTax on ownership of land and buildings currently between 0.1% and 0.6% of fair market value. Owner generally pays, but cost transferred to tenant.

APPEALS/RELIEFSReliefs granted under certain conditions.

GERMANY

COMPARABLE POSITION*

0.4%OF GDP

PROPERTY TAX REVENUE

1

08 FACTS & FIGURESSPRING 2015 09ENGAGE

ISSUE NINEFACTS & FIGURESSPRING 2015

WWW.GERALDEVE.COM

ENGAGEISSUE NINE

TAX BASISSimilar to UK system, liability is reached by multiplying ‘rateable valuation’ by the ‘annual rate on valuation’. Each local authority sets its own rate. There is currently a rolling revaluation process on a county by county basis, which is having a significant effect on multipliers.

APPEALS/RELIEFSValuations can be appealed. An established process is in place.

IRELAND

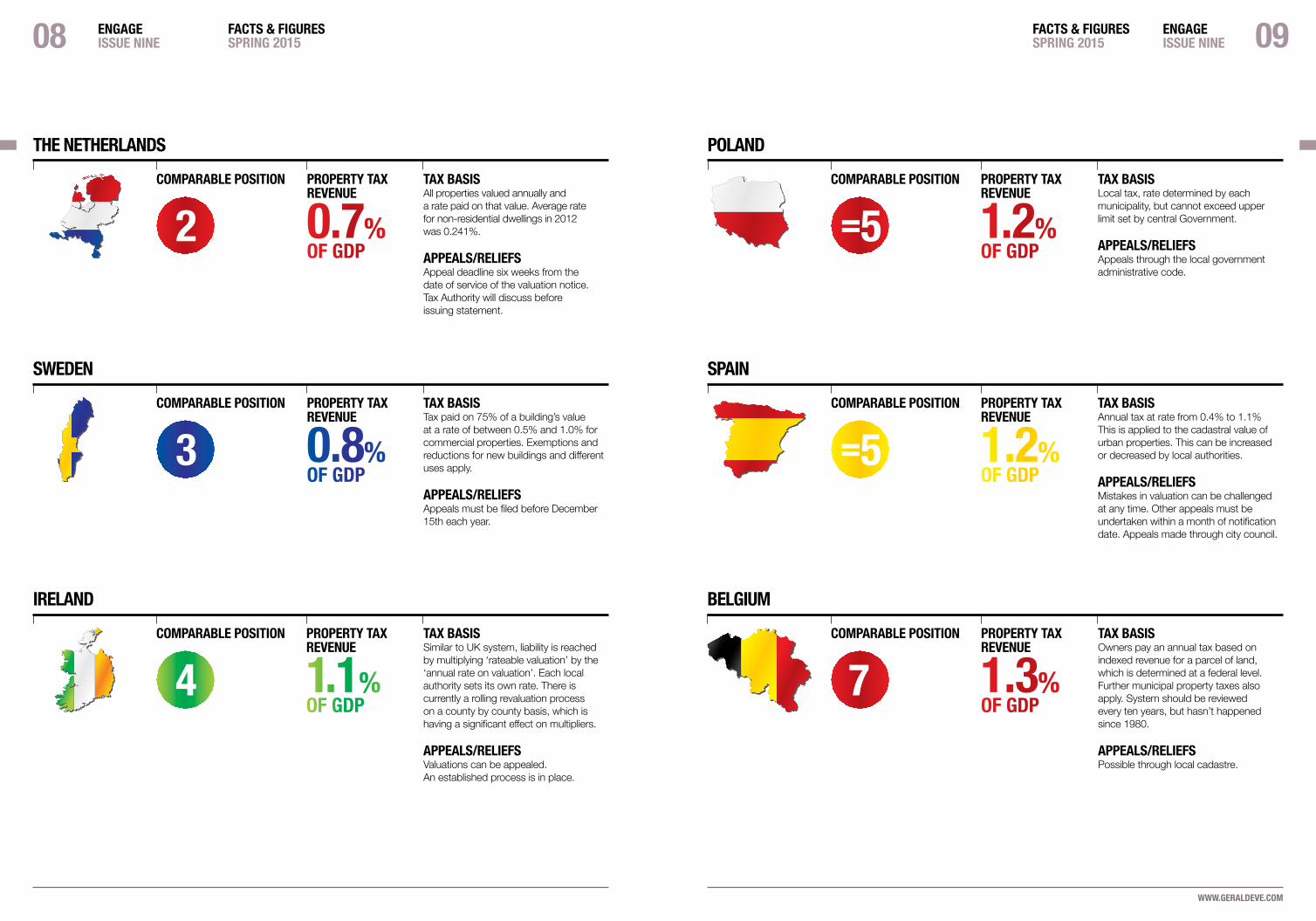

COMPARABLE POSITION

1.1%OF GDP

PROPERTY TAX REVENUE

4

POLAND

COMPARABLE POSITION

1.2%OF GDP

PROPERTY TAX REVENUE

=5TAX BASISLocal tax, rate determined by each municipality, but cannot exceed upper limit set by central Government.

APPEALS/RELIEFSAppeals through the local government administrative code.

TAX BASISAnnual tax at rate from 0.4% to 1.1% This is applied to the cadastral value of urban properties. This can be increased or decreased by local authorities.

APPEALS/RELIEFSMistakes in valuation can be challenged at any time. Other appeals must be undertaken within a month of notification date. Appeals made through city council.

SPAIN

COMPARABLE POSITION

1.2%OF GDP

PROPERTY TAX REVENUE

=5

TAX BASISAll properties valued annually and a rate paid on that value. Average rate for non-residential dwellings in 2012 was 0.241%.

APPEALS/RELIEFSAppeal deadline six weeks from the date of service of the valuation notice. Tax Authority will discuss before issuing statement.

THE NETHERLANDS

COMPARABLE POSITION

0.7%OF GDP

PROPERTY TAX REVENUE

2

TAX BASISTax paid on 75% of a building’s value at a rate of between 0.5% and 1.0% for commercial properties. Exemptions and reductions for new buildings and different uses apply.

APPEALS/RELIEFSAppeals must be filed before December 15th each year.

SWEDEN

COMPARABLE POSITION

0.8%OF GDP

PROPERTY TAX REVENUE

3

TAX BASISOwners pay an annual tax based on indexed revenue for a parcel of land, which is determined at a federal level. Further municipal property taxes also apply. System should be reviewed every ten years, but hasn’t happened since 1980.

APPEALS/RELIEFSPossible through local cadastre.

BELGIUM

COMPARABLE POSITION

1.3%OF GDP

PROPERTY TAX REVENUE

7

For City of London landlords, insurance companies can rarely have been so important. At a time when banks are consolidating their

space requirements, insurers have increased their London footprints by 20% over the past five years and are now the third largest occupier in the financial sector. Indicative of their current strength is the expansion of Arthur J. Gallagher & Co.

“When we appointed Gerald Eve three years ago we had 35 properties in the UK, today we have 110,” says Chicago-based Cara Richardson, a vice president at the global insurance brokerage with responsibility for the firm’s 660-strong global office portfolio. “That gives you some idea of the speed at which we’re growing.”

››

INSURANCE PREMIUMCARA RICHARDSON OF INSURANCE BROKERAGE ARTHUR J. GALLAGHER & CO OVERSEES A GLOBAL PORTFOLIO OF 660 OFFICES, WITH THE FIRM’S ONGOING EXPANSION PROVIDING PLENTY OF PROPERTY CHALLENGES. “REAL ESTATE SHOULDN’T DRIVE THE BUSINESS, THE BUSINESS SHOULD DRIVE REAL ESTATE,” SHE TELLS ENGAGE.

When we appointed Gerald Eve three years ago we had 35 properties in the UK, today we have 110...that gives you some idea of the speed at which we are growing.

SCOTLANDThe system is broadly the same as for England & Wales except it is procedurally more difficult to appeal. They are not date limited with backdated appeals. N. IRELANDThe system is broadly the same as for Great Britain. However, N. Ireland went ahead with a 2015 revaluation. This is currently an on-going process with established appeal procedures.

ACTIVITY TO DATEGerald Eve is actively assisting clients in markets where appeals are possible. To date Gerald Eve has secured savings of £1.6bn in the UK during the 2010 List and in conjunction with Murphy Mulhall has successfully acted on 49,000 sq m of space, achieving savings of up to 50% in Ireland. Gerald Eve and RHM Consultants are in the process of appeals in N. Ireland.

For further information please contact Steve Hile on +44 (0)20 7653 6841 or email [email protected]

UNITED KINGDOM

COMPARABLE POSITION

3.2%OF GDP

PROPERTY TAX REVENUE

9TAX BASISBusiness rates are based on the Rateable Value (RV) of each property which is based on a rental value at a predetermined valuation date. This is then multiplied by the uniform business rate set by national government bodies in each jurisdiction. City of London is an exemption with the ability to set its own rates. A revaluation has been carried out every five years since 1990, however, the current rating list has been extended by two years with five yearly revaluations due to resume in 2017.

APPEALS/RELIEFSThis differs for England & Wales. In Wales, the RV can still be challenged up until 31 March 2017 with the benefit of it being backdated to 1 April 2010. However, in England, the benefit is now only backdated to 1 April 2015.

10 FACTS & FIGURESSPRING 2015

ENGAGEISSUE NINE 11ENGAGE

ISSUE NINEINTERVIEWSPRING 2015

WWW.GERALDEVE.COM

FRANCE

COMPARABLE POSITION

2.5%OF GDP

PROPERTY TAX REVENUE

8TAX BASISFour municipal taxes: business tax; real property tax on undeveloped land; real property tax on buildings; and habitation tax. Level of tax varies by district.

APPEALS/RELIEFSFrance is currently going through a re-evaluation process. Procedures are in place to appeal, commonly through lawyers.

There is currently a reassessment process taking place in France and Gerald Eve may be able to look at this in conjunction with specialist lawyers in France to ensure the correct assessment is made on property.

13

LONDON CALLING If anything the expansion here has been even more dramatic, with staff numbers across the country increasing tenfold over the past few years to 4,500, of which around 1,000 are based at the firm’s UK headquarters in the City of London. The company was the first tenant at The Walbrook Building, EC4, when it took 60,000 sq ft across two floors at the scheme in early 2013. By the time staff moved to the new building from former offices at 6 and 9 Alie Street, EC1, a further floor at The Walbrook was required to accommodate the growing workforce.

And the expansion hasn’t stopped. Gerald Eve has recently advised the firm in its acquisition of an auxiliary office

12 ENGAGEISSUE NINE

INTERVIEWSPRING 2015

ENGAGEISSUE NINE

INTERVIEWSPRING 2015

WWW.GERALDEVE.COM

The company has grown very rapidly over the past 18 months, through a mixture of organic growth and acquisitions, and as a result is creating a number of real estate headaches. Space has to be found for new recruits while offices inherited from acquisitions create opportunities for rationalisation and consolidation. It is an ever-changing conundrum, to which today’s solution isn’t necessarily tomorrow’s answer.

“It’s almost like a Rubik’s Cube. Every day something has changed and we have to think about just how we’re going to fit it into the puzzle,” she says. “You have to constantly review the possibilities if you’re going to keep real estate flat, which is what we’re always aiming to do.”

Keeping real estate ‘flat’ is a hallmark of the company’s approach. Over the past four years the firm’s US real estate footprint has remained stable despite the number of employees rising by over 20%. The amount of space per person has fallen from 220 to 183 sq ft.

It’s almost like a Rubik’s Cube. Every day something has changed and we have to think about just how we’re going to fit it into the puzzle.

We’ve pretty much made solid business decisions that mean we haven’t been saddled with too much space. And based on these criteria, you have to say the policy has been a success.

“During a time of increasing staff numbers, we’ve effectively consolidated $20 million of real estate costs,” says Richardson.

Richardson makes such consolidation sound relatively simple, but surely it’s far from easy? And it must create friction, especially in the US where lower real estate costs – the company’s London offices cost four times their equivalent in Chicago – make larger footprints more common? “It has to be both consultative and collaborative,” continues Richardson. “We spot the opportunities and outline the options, but ultimately it’s a business decision. Real estate shouldn’t drive the business, the business should drive real estate.”

at Viridis Real Estate’s 67 Lombard Street where Arthur J. Gallagher & Co is set to take 54,000 sq ft at the redeveloped scheme.

The first thing any visitor to the Walbrook office notices is the ground floor “brokers’ lounge”. With a café station and comfortable chairs – as well as more formal booths for slightly more privacy – it is a hive of activity and the definition of a modern break-out area.

“It comes back to space management,” says Richardson. “We’ve been able to drastically reduce workspace per person while creating opportunities for more interaction. It’s something we’re working to incorporate into all our major offices. The success of Walbrook is a touchstone for how we do things in the future.”

The lessons are being learned in Chicago, where a new corporate headquarters is being built in the suburb of Rolling Meadows (the only office the company will own outright – everywhere else it leases space). Comprising a ‘rehabbed’ red-brick building and an additional new-build office, the HQ will incorporate the most successful features from Walbrook and be home to around 2,250 people.

“We appreciate there may be some resistance to the changes, but we figure if it can be done at HQ then it can be done anywhere,” says Richardson, adding with a wry smile, “of course, we’ll see how we get on in Texas, where everything is larger than life.”

FLEXIBILITY IS KEYFlexibility and efficiency in how space is used is one thing; flexibility in the terms on which space is held is quite another. So how does Richardson manage this, especially for a company whose space requirements change so regularly?“We don’t over-commit. In the US we take advantage of ‘right of first option’ clauses that allow us to take the space we need now with the option to lease more as the office grows. We’re happy to commit longer-term in larger markets – for example, I know we’ll always have an office in Los Angeles – but in smaller cities we target lease lengths of five years.

“We also look towards the wider economic climate when committing to space. It’s better to sign for office space in Houston when oil prices are low or falling. Similarly, San Francisco is a boom-and-bust town – at the moment space is expensive due to the technology sector, but when the economy turns there will be offices available for next-to-nothing.”

A strategic plan is put in place for each property, which is used to identify opportunities for efficiencies and consolidation. At any one time there are ongoing actions in place for up to 20% of the portfolio. Much of the work is generated by the new acquisitions and overlaps with existing real estate holdings.

“Insurance broking is an incredibly fragmented industry,” says Richardson, “and we’re making it our responsibility to consolidate the sector! What this means in practice is many purchases of small operators, often leading to overlaps. We don’t, for example, need four or five offices in Leeds, so with each acquisition we weigh up the options for the property commitments we inherit.”

So how is success for such portfolio management measured? Says Richardson: “Perhaps the best measure is the vacancy rate. During the recession we targeted – and hit – a vacancy rate of between 10% and 15%. Now that we’re expanding it’s a little higher than that, usually as a result of a slight lag following acquisitions, but not dramatically so.

“Of course there are always one or two outliers – there’s a floor of an office building in Melbourne I would love to let to you! – but so far we’ve pretty much made solid business decisions that mean we haven’t been saddled with too much space. And based on these criteria, you have to say the policy has been a success.”

The over-riding impression is of a portfolio in a constant state of flux. There are clearly manifold challenges created by an expansion policy that is so overtly ambitious, aggressive and acquisitive,

but it creates opportunities too. As an insurance brokerage, Arthur J. Gallagher & Co’s expertise lies in risk management; with the help of Gerald Eve it is certainly applying the same principles to its large and growing property portfolio.

15ENGAGEISSUE NINE

FEATURESPRING 2015

WWW.GERALDEVE.COM

WHERE NOW FOR EUROPEAN REAL ESTATE INVESTMENT? BY MIKE PHILLIPS

to $500m an acre, and is the equivalent of a full year of revenues for the company. Against this, even the record £70m an acre Qatari Diar paid for Chelsea Barracks in 2007 doesn’t look too bad.

And for the US private equity firms that are fuelling the secondary and tertiary markets again, compared to their home markets, where banks generally sold off their bad loans and assets in 2009 and 2010, and the sector has returned to stability due to highly liquid debt markets, Europe remains a huge opportunity. European banks still have more than EUR400bn of non-core loans, and the combination of public auctions for large portfolios and the potential for off-market deals in more opaque markets is the perfect storm, and interest is likely to continue.

So what does this mean for 2015? While it is hard to predict whether investment volumes will grow and prices continue to rise, there is little to suggest that they will fall significantly on a pan-European basis. A market likely to fare particularly well is the sale of large, pan-European portfolios.

On the face of it, you could be forgiven for wondering why global investors are bothering with European real estate investment at the moment. Prime yields in most big

cities are back to 2007 levels or, in some cases, even lower. Sluggish economic performance in many countries means rents are not rising as fast as was hoped. And the European Central Bank is battling hard to stave off deflation and the threat of the recession of the last seven years turning into a repeat of Japan’s lost two decades, which would bring further downward pressure on rents and values.

And yet European investment volumes are predicted to have reached EUR160bn in 2014, the highest figure since 2007. And there is seemingly no let up in capital focusing on the sector. Global institutions are planning on upping their commitment to real estate next year, according to placement agent Hodes Weill and US university Cornell, bringing $80bn of extra capital to the sector globally. And 44% of these investors said they were interested in Europe and the UK.

Within Europe itself, German property funds had a record year in 2014, taking in more than EUR6bn to October, according to German funds body BVI, and private equity funds have raised EUR24bn, according to Preqin, again touching 2007 levels.

This might seem hard to comprehend with the ghost of the last boom still stalking the memory of most people active in the market today, but take a global, multi-sector view it becomes easier to understand. When asked whether the Asian investors they advised were worried about deflation, one major money manger said: “It doesn’t even come up in conversation.” The far eastern investors who are now starting to shift some of the huge amount of savings built up by the growing middle glass of booming populations into real estate are not investing for the short or medium term. They believe in real assets like property and infrastructure, and they believe that Europe will return to growth eventually, albeit muted.

What is more, compared to their home markets, even core assets at record prices don’t look too expensive. In September a consortium led by car maker Hyundai paid $10bn for a 79,342 sq m site in the Gangnam region of Seoul, South Korea, where it will build a new corporate HQ complex. The price equates

14 ENGAGEISSUE NINE

FEATURESPRING 2015

Many of the new entrants targeting Europe are looking for scale and critical mass, and have the debt, equity and appetite for complexity needed to make large portfolio purchases – you don’t buy a portfolio these days, you buy a “platform”. A great example is North Star Asset Management, the New York-listed fund manager. It dipped its toe into the European market in April with the purchase of a stake in fund manager Aerium, but in November went under offer to buy two pan-European portfolios from SEB Asset Management and Provinzial NordWest, totaling EUR1.5bn, above the original asking price. We are now in a market where portfolios command a premium rather than a discount, so expect fund managers to start packaging non core assets to tap into demand which, in spite of the many good reasons you can find not to invest, seems unlikely to recede in the immediate future.

Mike Phillips, is editor of EuroProperty, the monthly magazine dedicated to European and UK crossborder property investment (www.europroperty.com)

Illustration: Jim Tsinganos

SIMON PRICHARDANGLING FOR SUCCESS WITH

Sweetings is very appropriate. Its wide range of sustainable fish offering is very attractive to keen angler Prichard. You get the

feeling that Prichard applies his self-deprecating humour with the same skill he deploys to reel a catch in. Whether speaking to clients or colleagues the feedback is he has a wicked sense of humour, but he is a straight talker and has an inherent sense of decency.

Simon Prichard: “I don’t think it came as a big surprise to the business when we announced the management changes at the end of last year. Hugh Bullock, our new Chairman and former Senior Partner feels very strongly about succession – a break with the old partnership idea that you served your time as Senior Partner and duly retired. This way change is telegraphed in advance – nobody feels bounced and continuity is maintained.”

ENGAGE: Where did it all begin?

SP: “This is where it all started for me here in Sweetings. This is where the clandestine meetings took place 16 years ago. Gerald Eve wanted to open a City and Canary Wharf business. But the City is very tight on relationships. You can’t put someone in there and expect them to build a business. You have to have a native. Our timing was good and I was fortunate to have some good people alongside me and the backing of the partnership from the outset.”

Within about 18 months of Simon joining the firm he was invited into the equity partnership.

SHORTLY AFTER HIS APPOINTMENT AS SENIOR PARTNER IN APRIL 2015, ENGAGE SITS DOWN WITH SIMON PRICHARD WHILST ENJOYING A CRAB SANDWICH IN CITY INSTITUTION SWEETINGS RESTAURANT TO LEARN MORE ABOUT THE MAN AND HIS AMBITIONS FOR THE FIRM.

16 ENGAGEISSUE NINE

INTERVIEWSPRING 2015 17ENGAGE

ISSUE NINEINTERVIEWSPRING 2015

WWW.GERALDEVE.COMPhotography: George Brooks

E: Why Gerald Eve?

SP: “The truth is that had you told me 17 years ago I would be at Gerald Eve let alone Senior Partner I would have laughed. I had no real knowledge of the firm other that it had a professional reputation. What I saw in Gerald Eve was a firm that was profitable, that had an amazing client base, intellectual rigour and the potential to change to be even better.”

E: What’s changed at Gerald Eve?

SP: “Communication and collaboration across the firm has never been better. This is down to a lot of hard work that the partners have done in recent times. Basic stuff like reducing financial silos, and building a reward structure that recognises collaboration. This is not to demean the individual, we have our superstars who of course deserve recognition, but by seeking to encourage greater collaboration we have really generated a positive effect on the business.”

E: What has been achieved during your time at Gerald Eve?

SP: “When I joined the Executive Board in 2008 our mantra was to adopt the best of partnership and the best of corporate. I think we’ve achieved that. We still have a collegiate partnership feel but also we have embraced modernisation and change. One of the key things we have learnt as a partnership in recent years is not to be afraid to change – we have and we are better for it.”

Gerald Eve has developed a unique multi-dimensional ethos. While continuing to value its great intellectual base, it has also brought in more sales-focused people. It is interesting to note that all of the top 12 firms are now run by transaction facing personnel. Head of planning, Bullock was the first market-facing Senior Partner the firm had and Simon is the second.

“This is a break with the past, but you have to get the balance right. We have brought in more transactional partners who are more gregarious characters but we mustn’t lose sight of the intellectual, professional base, that has underpinned this business for so long, and will continue to underpin it.”

E: What would you say your strengths and weaknesses are?

SP: “I have never claimed to be the most technically competent surveyor and in truth have never needed to be.

››

I’m nothing if not straight. Everyone should know exactly where they stand with me. If they ask me a direct question they will get a direct answer.

I am interested in people and am fortunate that in my role I get to meet some really interesting people. The key to understanding what somebody wants whether a colleague, client or family member is to listen to them. Am I a salesman? Well the truth is we are all selling something. At Gerald Eve it is our people and our brand which gives us a great head start on the competition.”

E: What motivates you?

SP: “One, it’s about testing yourself, two it’s about self-determination and three, deep down, I like being the underdog and taking on the big boys and winning,” he adds with an infectious smile. Although, intriguingly Prichard says he’s never been motivated by money. “I know Hugh before me wasn’t either. Of course I recognise its importance, but it’s never been the reason I’ve got out of bed and onto the train in the morning.”

E: What’s next for Gerald Eve?

SP: “Today we are in a good place and we should recognise that. We can thank our clients by ensuring they continue to receive the high levels of service they expect and demand. We can thank our people through a reward structure that reflects their considerable contribution.For us there are some fantastic opportunities available. Our partnership structure is extremely attractive to senior lateral hires and we must continue to show ambition and seek to recruit the best people at all levels.

Our financial model is not based purely on generating revenue like some of our competitors. Consequently, we can be far more strategic and long term in our thinking and this is partly why there is consistency and stability in our financial performance.

One of the more exciting new projects happening now has been the development of Gerald Eve International which was a direct reaction to listening to clients who told us that the part of the globe they really needed help with was continental Europe. This made particular sense to us with London being the landing stage for so much international capital”.

He says he spent a lot of time at this year’s MIPIM meeting his European partners and discussing very specific European investment opportunities and individual corporate occupier expansion strategies.

“It is worth pointing out a number of the big UK pension funds told me they will be putting more money into Europe than the UK this year. Suffice to say that we look forward to being involved in a number of interesting corporate occupier and investment transactions over the next few months.”

E: So keeping with the international theme if Gerald Eve was a country which country would it be?

SP: “That’s easy – Sweden – its independent, economically competent and very good looking – just like us!”

For further information please contact Simon Prichard on +44 (0)20 7653 6827, or email [email protected]

18 INTERVIEWSPRING 2015

ENGAGEISSUE NINE

Gerald Eve International was a direct reaction to listening to clients who told us that the part of the globe they really needed help with was continental Europe.

19ENGAGEISSUE NINE

FEATURESPRING 2015

WWW.GERALDEVE.COM

ROOMS WITH A LONG-TERM VIEW

With its own fleet of liveried Rolls Royces and views across Victoria Harbour to the massed skyscrapers of Hong Kong Island, The Peninsula has long been used as shorthand for a certain level of opulence. It is a reputation that has been parlayed into one of the world’s leading luxury

hotel groups, with ten locations across the globe and a further two on the drawing board. Although traditionally focused on major Asian and US cities, the hotel group has recently been looking further afield and in summer 2014 opened The Peninsula Paris, following a €338m refurbishment of what was formerly The Majestic. Designs for a London outpost situated on Hyde Park Corner are currently being worked up.

For those with an eye on the hotel sector, it is instructive that The Peninsula’s recent acquisitions have been in Paris and London, for both brands and investors are eyeing up Europe like never before. From Amsterdam to Athens and Barcelona to Berlin, hotel brands old and new have spotted an opportunity to establish new presences in Europe’s major destination cities, and where the brands are looking the property investors are not far behind.

— Show me the money —

Much of the money flowing into European hotels is from Asian investors and Middle Eastern sovereign wealth funds, seeking assets that not only generate decent returns but also have something of a cachet value. The august names of Europe’s leading hotels fit the bill nicely.

That said, there are a number of factors driving the inward investment. For Asian investors, dwindling yields in domestic markets are forcing Hong Kong and Singapore based funds to look increasingly further afield in search of better returns. The mainland China hotel market may well be maturing fast, and promises plenty of future success, but by most estimates it is still a decade or more away from stabilisation and decent investment performance.

Developing markets present some opportunities, but for many they are bit too hot to handle. Countries such as Myanmar boast high yields – and may well become established destinations – but there remain suspicions that the political situation is too volatile and the operating risk disproportionately high. And if an investor is seeking a prestigious asset with stable performance to form the centrepiece of its portfolio, the Rangoon Hilton is probably not going to cut it.

In the light of these factors, it is easy to understand the attractiveness to investors of European hotel assets. Not only do they continue to trade well and generate considerable income – major European cities are still among the world’s prime tourist and business destinations – but many hotels have not yet fully recovered from the price falls seen in the face of the global financial crisis. This is especially true in southern European cities such as Madrid, Barcelona, Rome and Athens that saw the worst of the crash and its pernicious ongoing after-effects. In short, hotels in these locations still look cheap.

››

WWW.GERALDEVE.COM

20 ENGAGEISSUE NINE

FEATURESPRING 2015

Illustration: Sam Chivers

ROOMS WITH A LONG-TERM VIEW CONTINUED

But it is London that has cornered the lion’s share of the investment to date. With a relative undersupply of hotel rooms (compared to many global cities) and growing numbers of both business travellers and tourists at all price points, London is an obvious first port of call for those looking to capitalise on the current clamour for European hotels.

— London calling —

For London the drivers of investment are slightly less prosaic, and are founded in sentiments similar to those that have fuelled the capital’s prime residential market in recent times. Despite central London prices having recovered – indeed, they have hit new highs in some instances – there remains a belief that there is still some way to go before yields can be compressed no further. The lure of some of the world’s most famous names – Claridge’s, The Connaught, The Savoy – is hard for many to resist; much like the Georgian townhouses of Knightsbridge, London’s luxury hotels offer the alluring combination of a safe haven and a trophy asset.

And brands’ interest in London – either to establish a new presence or build on existing operations – is very notable. It is rumoured that MGM and Hakkasan wish to build on their Las Vegas JV and acquire a site in the capital. The Langham is looking for further hotels in the capital to join its Portland Place flagship. Butterfly, a niche Hong Kong operator, is seeking acquisitions and management agreements, while earlier this year Millennium added Chelsea Harbour to its portfolio. At a different proposition, Dorsett has completed on a Sherpherd’s Bush location and is actively seeking a further two sites, while Nickelodeon is planning its first European branded hotel in Leicester Square.

The operator demand is there, but that is not to say it is limitless. London’s general under-supply of hotel rooms does suggest that long-term prospects are excellent, but there’s a growing realisation that hotels have to be in the right place, catering to the right clientele and, crucially, for sale at the right price; the market is not so constrained as to be without risk. And where operators are cautious, investors are even more so.

Sentiment towards the capital may well be positive, but investors are more than happy to look elsewhere if the price seems a bit ‘toppy’. Hotels might offer the highest-profile and arguably most-prestigious assets, but if alternative markets can provide better returns then the money will soon follow the yield. There is already anecdotal evidence of investors finding London a bit frothy and instead tentatively looking elsewhere, tiptoeing into regional centres such as Manchester and Edinburgh.

As with southern Europe, prices in these cities haven’t yet fully returned, while occupancy rates and income have held up well. It is unsurprising that attention is starting to turn to these locations as investors balk at the cost of establishing a London presence.

Much like other sectors, notably offices and residential, the UK’s hotel investment market is dominated by London, but money is slowly finding its way up the risk curve to embrace sites outside the capital. The under-supply of hotel rooms is just as much a fact of life – maybe even more so – in the UK’s regional cities, and as such it looks to be a good long-term bet for investors and operators alike.

The current interest in the European hotel market – and London in particular – represents a genuine vote of confidence in the future of these cities. Both operators and investors are looking at the region’s future prospects and, broadly speaking, like what they see. The attraction of Europe’s leading cities as destinations for both tourism and business never really went away; for those investors and brands with courage in their convictions and the confidence to seize this opportunity, some prosperous years are on the horizon.

For further information please contact James Innes on +44 (0)20 7333 6411, [email protected] or Peter Haigh on +44 (0)20 7333 6286, [email protected]

21ENGAGEISSUE NINE

FEATURESPRING 2015

It is a notable feature of the real estate sector that the profession so often runs in the family. Perhaps this results from children seeing the opportunities and experiences that a career in property gives to their

parents and decide to follow them into the industry.

For most people, aspiring to the same career as a parent doesn’t involve moving to another country, but that’s exactly what it meant for Joanna Osiecka when she came to the UK from Warsaw to study economics and geography in London. “A girl in my neighbourhood had studied in London and talked to me about how great it was there,” says Joanna, “so I applied to University College London (UCL). And when I was offered a place, it seemed silly not to take advantage of the opportunity.”

RELATIVELY SPEAKINGENGAGE TALKS TO RENATA OSIECKA, MANAGING PARTNER AT AXI IMMO IN WARSAW, PART OF GERALD EVE INTERNATIONAL, AND HER DAUGHTER JOANNA, WHO IS CURRENTLY UNDERTAKING A MASTERS AT THE LONDON SCHOOL OF ECONOMICS.

WWW.GERALDEVE.COM

“Moving from suburban Warsaw to student digs in Euston was a bit of a culture shock,” she adds, “but I very quickly loved living and studying in London.” Although she chose economics and geography rather than a specific route into property, she has decided to pursue a career in the sector. Joanna has had work experience placements at property firms and consultancies in both Poland and the UK, including Gerald Eve. Following graduation in summer 2014, she is now working towards a Masters degree in real estate economics and finance at the London School of Economics (LSE).

Real estate is a world that Joanna knows well and has seen at close quarters, as her mother Renata is one of the best-known faces in the Polish property market. Joanna didn’t feel under pressure to enter the sector – “Obviously I talked to mum, but it was my decision to embark on a path towards a career in real estate” – but it’s clear that Renata is pleased her daughter has followed her into real estate.

Whereas Joanna’s route into the sector is fairly orthodox– academic studies together with work experience – the trajectory of Renata’s career is more complex. With the fall of communism in 1989, there were suddenly many more opportunities available for young Poles, something that Renata took immediate advantage of. Deciding to become a teacher, she undertook an MA at Warsaw University and looked set to enter the world of education. “There was no modern real estate industry in Poland at the time,” says Renata, “and I’d never even considered it as a career.”

But fate would intervene. While studying for her degree, Renata was working part-time for Nick Evans, a British residential developer who was one of the first to build Western-style homes in Poland. “He recommended me to Prime Property, a US-owned agency that was an associate of what is now CBRE,” remembers Renata, “and that’s how my life as a real estate professional started.”

She worked hard to learn the ropes before studying remotely towards a degree in real estate from the University of Sheffield and then her RICS qualifications. It was around this time she also started a family. “It was difficult to juggle everything – work, studying, family,” she says, “and it probably took about ten years to finish everything. But it was worth it. Qualifications are important.”

She came to specialise in industrial property and was soon recruited by Colliers International as head of industrial in Poland. “I was the first woman to work in the Polish industrial sector,” she proudly claims, “but once I showed myself to be capable more and more women were taken on. In Poland now, a slight majority of property agents are women.”

A spell client-side at industrial developer Panattoni followed – “very intensive, much more difficult than agency, but it gave me a better understanding of the challenges facing developers” – before Renata established AXI IMMO with three colleagues in April 2009. Within six years it has grown to 30 people, with offices in Warsaw and Katowice and plans for a third, and has won industry awards for the past three years.

When approached by Gerald Eve in summer 2014 about the possibility of joining an international group of offices, it was an opportunity she jumped on. “We’d been offered associations with US firms in the past, but they were really just joint marketing platforms. Gerald Eve International is different,” says Renata, “it’s collaborative, and the clients of all the firms will benefit from the wider geographical reach. It’s an exciting time.”

AXI IMMO’s association with Gerald Eve International also gives Renata a good excuse for regular visits to London to visit Joanna, although possibly not for too much longer. “I’m really enjoying the course at LSE, especially its academic nature,” says Joanna, “but once it’s completed I’m thinking about working in the USA or perhaps Germany to gain experience of other markets. Long-term, however, I think I’ll return to Poland.”

So if Joanna did move back to Warsaw, do they think they could work together? “I think we’re probably too similar!” to which Renata agrees. “We’re both really strong personalities,” she says, “and I’m not too sure how we’d get on working in the same office! But we’re very close and have a great relationship, so maybe it would be easier than we think. Perhaps best not to rule it out – never say never!”

Gerald Eve International is different, it’s collaborative, and the clients of all the firms will benefit from the wider geographical reach. It’s an exciting time

23ENGAGEISSUE NINE

FEATURESPRING 201522 ENGAGE

ISSUE NINEFEATURESPRING 2015

Photography: George Brooks

PRIME LOGISTICSThe definitive guide to the UK’sdistribution property market

Q1 2015 Bulletin

QUARTERLY SUMMARY

• 12.6 million sq ft transacted in Q1, the largest quarterly volume of take-up since Q1 2006• Pre-lets and development sales account for 50% of all occupational transactions• Total availability bottoms-out, but new/refurbished supply continues to decline• 22 developments start construction, 10 of which speculatively• Prime headline rents grow in 30 out of 51 locations• Lack of product forces investors to widen their requirements

For more information please contact Sally Bruer on +44 (0)20 7333 6288 or [email protected]

Gerald Eve are proud supporters of Changing the Face of Property, an initiative to improve diversity and inclusion across the property profession.

Changing the Face of Property (CTFOP) is a diversity initiative to raise awareness of the property industry. Its aims are to increase diversity within

the industry and change the perception that a career in property means becoming an estate agent or working on a construction site.

www.propertyneedsyou.com

A joint initiative to improve diversity and inclusion in the property industry

Disclaimer & copyrightThe views expressed in this magazine are those of the contributors for which Gerald Eve accepts no responsibility. Readers should take appropriate professional advice before acting on any issue raised.

This magazine is a short summary and is not intended to be definitive advice.No responsibility can be accepted for loss or damage caused by reliance on it.

© All rights reserved

The reproduction of the whole or part of this publication is strictly prohibited without permission from Gerald Eve LLP.

05/15

www.geraldeve.com

For all enquiries please contact: Simon Prichard Senior Partner [email protected]

Designed by Philosophywww.philosophydesign.com

Contributing writers Grenadier

London (West End) 72 Welbeck StreetLondon W1G 0AYTel. +44 (0)20 7493 3338

London (City)46 Bow LaneLondon EC4M 9DLTel. +44 (0)20 7489 8900

BirminghamBank House8 Cherry StreetBirmingham B2 5ALTel. +44 (0)121 616 4800

Cardiff32 Windsor Place Cardiff CF10 3BZ Tel. +44 (0)29 2038 8044

Glasgow 140 West George Street Glasgow G2 2HG Tel. +44 (0)141 221 6397

Leeds1 York PlaceLeeds LS1 2DRTel. +44 (0)113 244 0708

ManchesterNo 1 Marsden StreetManchester M2 1HWTel. +44 (0)161 830 7070

Milton KeynesAvebury House201–249 Avebury BoulevardMilton Keynes MK9 1AUTel. +44 (0)1908 685950

West Malling35 Kings Hill AvenueWest MallingKent ME19 4DNTel. +44 (0)1732 229420

Gerald Eve International is located in the following countries

AustriaBelgiumFranceIrelandLuxembourgNetherlandsPolandSlovakiaSpainTurkeyUK

Case by case advice can also be provided in the following countries

GermanyItalyNorwaySwedenSwitzerlandAustraliaIndiaIndonesiaRussia