the innovator in bar-restaurant-entertainment hospitality...business, (ii) the business climates in...

TRANSCRIPT

NASDAQ: RICK Investor Presentation

March-April 2016 www.rcihospitality.com

The innovator in bar-restaurant-entertainment hospitality

2

Forward Looking Statements

Certain statements contained in this presentation regarding RCI Hospitality future operating results or performance or business plans or prospects and any other statements not constituting historical fact are "forward-looking statements" subject to the safe harbor created by the Private Securities Litigation Reform Act of 1995. Where possible, the "anticipate," "approximate, " "believe," "estimated," "expect," "goal," "intent," "outlook," "planned," "potential," "will," "would," and similar expressions, as they relate to the company or its management have been used to identify such forward-looking statements.

All forward-looking statements reflect only current beliefs and assumptions with respect to future business plans, prospects, decisions and results, and are based on information currently available to the company.

Accordingly, the statements are subject to significant risks, uncertainties and contingencies, which could cause the company‘s actual operating results, performance or business plans or prospects to differ materially from those expressed in, or implied by, these statements.

Such risks, uncertainties and contingencies include, but are not limited to, risks and uncertainties associated with (i) operating and managing an adult business, (ii) the business climates in cities where the company operates, (iii) the success or lack thereof in launching and building the company’s businesses, (iv) the operational and financial results of the company's adult nightclubs, (v) conditions relevant to real estate transactions, (vi) the loss of key personnel, (vii) laws governing the operation of adult entertainment businesses, and (viii) the inability to open and operate our restaurants at a profit.

Additional factors that could cause the company’s results to differ materially from those described in the forward-looking statements are described in forms filed with the SEC from time to time and available at www.rcihospitality.com or on the SEC's internet website at www.sec.gov.

Unless required by law, RCI Hospitality does not undertake any obligation to update publicly any forward-looking statements, whether as a result of new information, future events, or otherwise.

3

Overview

Three Parts to Our Presentation

• What do we do • Why it’s a good business • How we are growing EPS and cash flow, buying

back shares and now paying a dividend

4

Leader in Gentlemen’s Clubs

Subsidiaries own/operate 38 of the best venues in the US

• Powerful brands, quality environments, beautiful entertainers, excellent restaurants

• Larger units in major cities • Smaller ones in the South/Southwest

Licensing Limits Favor Acquisitions

• We acquired ~80% of clubs we own • Most municipal licenses tied to physical location • Few municipalities issuing new licenses

Goal: Acquire More of the Industry’s Best

• 3,500 clubs in the US / 500 meet our qualifications • Most long-term owners interested in selling • As only public company in the space, and with access to

bank financing, we are the acquirer of choice

Elegant clubs with restaurants

High-end, high-energy club for young professionals

Nation’s mega club with 74,000 square feet

High-end clubs for African-American professionals

Lively BYOB clubs for blue collar patrons and the college crowd

Lively BYOB clubs for blue collar patrons and the college crowd

5

Fast-Growing Bombshells Chain

First Military-Themed Franchise in Sports Bar Segment

• Leverages expertise in bars, restaurants and entertainment • Drives traffic through design strategy and attractive

Bombshell Girls in uniforms • Large venues (7,500-10,000 sq ft), full bar, scratch kitchen,

big flat screen TVs, live music, huge patio

Five Company Owned Units

• Houston (3), Dallas (1), Austin (1)

Franchising Approved in All 50 States

• Potential to develop a chain of ~100 units • Wider appeal than competitive brands • Attracts men, women, singles, couples, and families • Strong lunch, dinner and late night business

6

The Bar-Restaurant-Entertainment Spectrum

RCI Hospitality RCI Hospitality Dave & Buster’s Brinker International

38 clubs featuring beautiful dancers/entertainers

5 sports bars/restaurants featuring attractive

waitresses in uniform and live music

81 sports bars/restaurants with large arcades*

1,641 casual dining Chili’s and Maggiano’s with no

entertainment**

Entertainment Food

Key Traffic Driver

DAVE & BUSTER’S chili’s

* Source: Dave & Buster’s March 2016 Investor Presentation ** Source: Brinker International January 12, 2016 Investor Presentation

7

RCI Advantages: Nationwide Scale

Industry Makeup

• Most clubs individual owner operated

RCI’s Advantages

• Nationwide scale, resources and operating efficiencies • In business since 1983 • Sophisticated systems, purchasing, best practices,

training, and innovation • Ability to maximize management, marketing and

profitability • Platform for expanding along the spectrum of bar-

restaurant-entertainment businesses

8

RCI Advantages: Expanded Access to Bank Financing

More Banks Offering RCI Traditional Commercial Loans

• Finance real estate acquisitions • Refinance higher rate mortgages

RCI’s Advantages

• Our real estate is now a major source of collateral • Helps finance growth along with our strong free cash flow • Reduces interest rates on loans • Enhances profitability • Makes RCI the industry acquirer of choice

Recent Examples

Acquisition Financing Anticipated Benefit

Retail mall where Tootsie’s Cabaret is located (largest club)

• $4.0M cash • $11.3M, 5.45% bank loan

• $0.6M annual pre-tax profit • 15% cash on cash return

Building and land where Rick’s Cabaret NYC is located (2nd largest club)

• $10.0M, 5.00% bank loan • Reduces expenses more than $0.7M annually over term of the loan

9

2011 2015

Unit Growth

• 2011-2015: Period of major expansion • 9/30/15 units almost double from 9/30/11 • Took advantage of acquisitions and opportunities to create new clubs

Bombshells 5 units

Clubs 38 units

2015 Unit Mix

23 Units

43 Units

10

$83.5

2011 2015

Revenue Growth ($ in millions)

2011-2015: Compound annual growth rate of ~15%

Other 2% Clubs

(outside Texas) 44%

2015 Segment Mix Bombshells

13%

Clubs (in Texas)

41%

$144.7

11

Revenue Mix ($ in millions)

Food & Beverage

56%

RCI Fiscal 2015

Entertainment Related & Other

44% Food &

Beverage 47%

Dave & Buster’s Last 12 Months as of Q3*

Entertainment Related & Other

53%

* Source: Dave & Buster’s March 2016 Investor Presentation

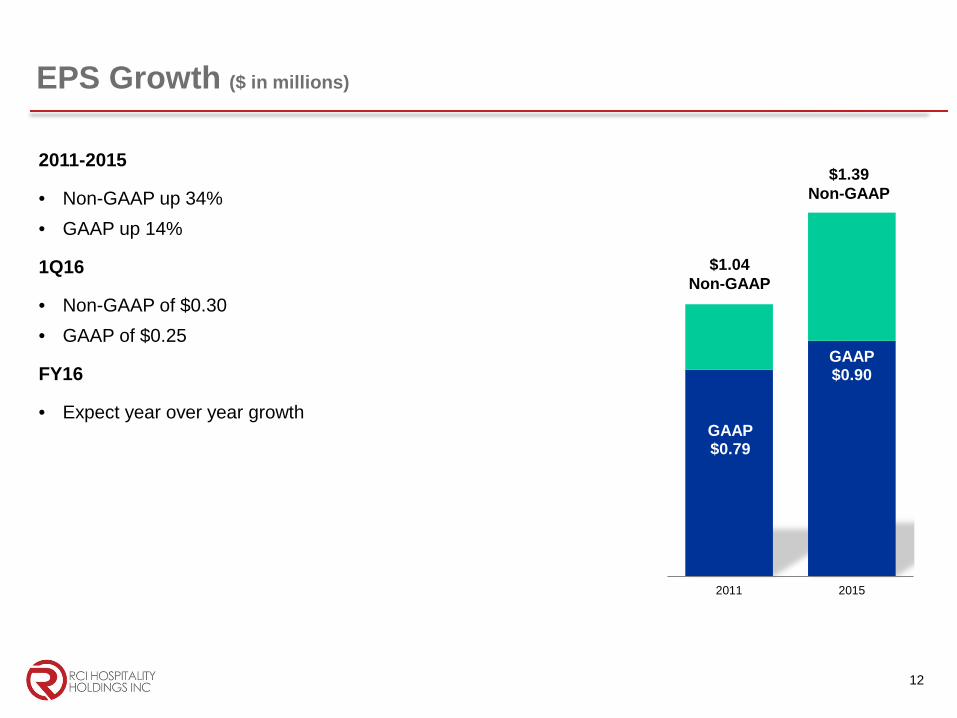

12

GAAP $0.79

GAAP $0.90

2011 2015

EPS Growth ($ in millions)

2011-2015

• Non-GAAP up 34% • GAAP up 14%

1Q16

• Non-GAAP of $0.30 • GAAP of $0.25

FY16

• Expect year over year growth

$1.04 Non-GAAP

$1.39 Non-GAAP

13

Strong Free Cash Flow ($ in millions)

Significant Feature of Clubs

• High gross margin business (86% in FY15) • Low capex • Inventory turns quickly

RCI’s FCF Performance

• Averaged 16% of revenues 2011-2015 • Defined as operating cash flow less maintenance capex

FY16 Target

• $15-$18M • 1Q16 on track with $3.9M

$14.9

2015 2016 Target

$15-$18

14

Disciplined Capital Allocation Strategy

19% 17%

15% 13% 12% 11%

37%

33% 30%

27% 24%

22%

0%

10%

20%

30%

40%

$8 $9 $10 $11 $12 $13

Afte

r Tax

Yie

ld

Stock Price

Return Using FCF to Buy Back Shares

Required Return Using FCF to Open / Acquire New Unit At Least 2X Return to Risk Adjust vs. Stock Buy Back

Use FCF to buy back shares

• Compelling after tax yield of 17% with shares in $9 range

Buy / open new units only if:

• Risk adjusted return rivals buying our assets in the market

• There is a significant strategic rationale

Higher after tax yield buying back stock vs. paying down debt

• Only at ~$17 does it make sense to pay down 13% debt at an accelerated rate (assuming no pre-payment penalty) Notes

• Based on annual FCF of $15M • Based on fully diluted share count at 12/31/15 incorporating

expected dilution from convertible securities as stock price rises • Conversion of these securities would reduce debt $3.8M

15

10.295

9.948

1/31/15 1/31/16

225,280

336,714

FY15 FY16 to Date as of1/31/16

$2.3

$3.3

FY15 FY16 to Date as of1/31/16

Capital Returned via Buybacks ($M)

Shares Retired via Buybacks Shares Outstanding (M)

Increased Share Buybacks in FY16

• We have already spent and bought back more shares FY16 to date than in all of FY15

Initiated Annual Cash Dividend

• $0.12 per common share, payable $0.03 quarterly • 1.3% yield on $9 per share • Payout ratio (8% of FY15 FCF) provides room for increases

Share Buy Backs & Cash Dividend

16

FY16 Plan to Expand Cash Flow

Reduce Costs

• Expanded access to bank financing enabling us to: Refinance high cost debt at lower interest rates

Extend amortizations

Buy properties to reduce occupancy costs

Improve Club Margins

• Eliminated 6 non-performing clubs in FY14-FY15

• Engaging new, lower cost social media marketing versus more expensive radio

• Re-launching two clubs with higher revenue generating prospects

Open New Units with Higher Return Potential

3.8%

4.3%

3.6%

3.3% 3.4%

3.6%

3.1%

2.8%

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

Rent Going Down (as % of revenues)

17

Open New Units with Higher Return Potential

3rd Club in NYC

• To open 2nd half of FY16 • Sports themed, first of its kind in Manhattan, near Madison Square Garden • Why returns should be higher 50-50 joint venture with landlord contributing adult license and real estate

Management and cost efficiencies with three NYC units

6th Bombshells

• To open 1Q17 • Demographics and location similar to No. 1 Bombshells unit in Houston • Why returns should be higher We already have most of the equipment necessary

Management and cost efficiencies with four Houston units

18

FY17 Preview

Strong Sports Line Up

• NFL “Big Game” in Houston (7 units) • NBA All Star Game in Charlotte (1 club) • Could add $1.5-$2M in incremental, high margin sales

Bombshells Expansion

• 6th unit to open 1Q17 • Expect to site a 7th unit • Franchise sales anticipated

Reduced Debt / Property Sales

• $2.0M used pay off convertibles in FY16 will be available • Expect to complete sales of real estate that is no longer

needed

19

Conclusion

Investment Opportunity

• Growing trend in bar-restaurant-entertainment • Clubs generate strong free cash flow • Implementing plan to grow FCF even more • Can finance growth without raising capital

Disciplined Capital Allocation

• Buying back significant number of shares • Initiated meaningful dividend • New units with higher return potential

Long-Term Growth

• Multiple club acquisition opportunities • Promising sports bar/restaurant franchise

Entrance to Rick’s Cabaret New York in Midtown Manhattan

20

Corporate Office 10959 Cutten Road Houston, TX 77066 Phone: (281) 397-6730 Investor Relations Gary Fishman Steven Anreder Phone: (212) 532-3232 IR Website www.rcihospitality.com Nasdaq: RICK

Contact Information

NASDAQ: RICK Investor Presentation Appendix

March-April 2016 www.rcihospitality.com

The innovator in bar-restaurant-entertainment hospitality

22

S&P 500 RICK

History

Timeline • 1983: Founded by Robert Watters as Rick’s Cabaret International • 1995: NASDAQ Initial Public Offering • 1998: Merged with Eric Langan’s publicly traded company of smaller

clubs • 1999: Langan named President and CEO • 2014: Name change reflected transformation to hospitality company • 2015: 20th year as a publicly traded company

Stock Performance: March 1999-March 2016*

• Total return has outperformed the S&P 500 by 7x • RICK: 810% with annualized return of 13.9% • S&P: 116% with annualized return of 4.6% 116%

810%

Total Return March 1999-March 2016

* Source: Bloomberg

23

Executive Background

Eric Langan Chairman, CEO, President

• President and CEO since 1999 • Involved in nightclub/restaurant business since 1989 • Acquired his first club at age 21 with proceeds from the sale of his baseball cards • Merged his XTC Cabaret chain with RCI in 1998

Ed Anakar Director of Operations

• Joined RCI 2003, Director of Operations since 2009 • Grew up in the hospitality industry – started at a young age as a waiter • Worked his way up to district manager for a large management company that operated

hotels, restaurants and nightclubs across the US • Launched and operated numerous RCI venues, including Tootsie’s Cabaret in Miami,

Rick’s Cabaret New York, Vivid Cabaret New York, and Bombshells

Phillip Marshall Chief Financial Officer

• Joined RCI 2007 as CFO • Began his public accounting career with KMG and became a partner in 1980 • Continued as a partner after merger with Peat Marwick • Partner in charge of the audit practice at Jackson & Rhodes 1992-2003 • Chief Financial Officer of CDT Systems, Inc. (publicly traded) 2003-2006

Travis Reese EVP & Director of Technology

• Joined RCI 1999 as VP-Director of Technology • VP with Digital Publishing Resources, Inc. 1995-1997 • Senior network administrator at St. Vincent's Hospital 1997-1999

Strong Management Team

24

Capital Allocation Metrics

After Tax Free Cash Flow (FCF) Yield of Buying Back Shares(1)

Annual Free Cash Flow (mm) $15.0 $15.0 $15.0 $15.0 $15.0 $15.0

Stock Price $8.00 $9.00 $10.00 $11.00 $12.00 $13.00

FD Shares at 12/31/15 with expected dilution from convertible securities as stock price rises (mm)(2) 10.023 10.023 10.023 10.216 10.216 10.397

Market Capitalization (mm) $80.2 $90.2 $100.2 $112.4 $122.6 $135.2

After Tax Yield (FCF/Market Cap) 18.7% 16.6% 15.0% 13.3% 12.2% 11.1%

Notes 1) RCI defines FCF as operating cash flow less maintenance capex 2) Conversion of these securities would result in $3.8M reduction of debt

After Tax Free Cash Flow (FCF) Yield of Paying Down Debt

Interest Rate on Debt (interest is tax deductible) 13.0% 12.0% 11.0% 10.0% 9.0% 8.0%

After Tax Yield (assuming 35% tax rate) 8.5% 7.8% 7.2% 6.5% 5.9% 5.2%

25

Long-Term Debt ($ in millions)

Total of $94.8 at 12/31/15

$60.3 Secured by Real Estate • Average weighted rate: 6.78% • $90.7 in net buildings and land on the

balance sheet • ~$50 in net real estate equity

$20.3 Secured by Subsidiary Stock • Average weighted rate: 10.61% • Secured by three of RICK’s more

profitable groups of subsidiaries

$6.8 Texas Comptroller Settlement • Average weighted rate: 9.58% • Imputed for accounting purposes • Paid in monthly installments of $0.12

$3.8 Convertible Debt • Average weighted rate: 9.02%

$3.6 Secured by Other Assets • Average weighted rate: 7.31%

26

Date / Time Event* April 12, 2016 2Q16 Club & Restaurant Sales

May 10, 2016 2Q16 & 6M16 Financial Results

July 12, 2016 3Q16 Club & Restaurant Sales

August 9, 2016 (tentative) 3Q16 & 9M16 Financial Results Date might be adjusted around 23rd Annual Gentlemen’s Club EXPO in New Orleans (August 7-10)

October 11, 2016 4Q16 Club & Restaurant Sales

December 14, 2016 4Q16 & FY16 Financial Results

Calendar

* RICK is looking at other investor conferences where we would like to present this year