the ingredients and challenges of sustained growth michael spence cape town june 2007

TRANSCRIPT

The Ingredients and Challenges of Sustained Growth

Michael SpenceCape Town June 2007

Outline

• Sustained High Growth– Ingredients– China and India

• Income inequality• Comparative Advantage• Leadership and political transitions• Urbanization• Demand Shock• Resource rich economies

Sustained High Growth• Growth > 7% for twenty plus years• There are 11 cases• 8 in Asia• (Botswana, China, Hong Kong, Indonesia,

Korea, Malaysia, Malta, Oman, Singapore, Taiwan and Thailand)

• Japan was close - India is about to join in• All post WW II• All leverage the global economy

Growth is a Recent Phenomenon

21st?

Ingredients

• Functioning market system• High levels of savings and investment

– Public and private• Resource mobility

– The microeconomic evolution of a rapidly growing economy

• Leveraging the global economy– Demand– Comparative Advantage– Technology and know-how

China and India

• China has been in this high growth mode since 1978

• India is about to jump into the high growth category • India’s current five year plan (just started) has

average growth over 9% accelerating to over 10%• There are formidable challenges for each country• They will have substantial and increasing impacts

on their neighbors, other developing countries, and the global economy

The two most populous countries, accounting for 40% of the world’s population, are the fastest growing economies in the world, one a complex democracy and the other a socialist market economy

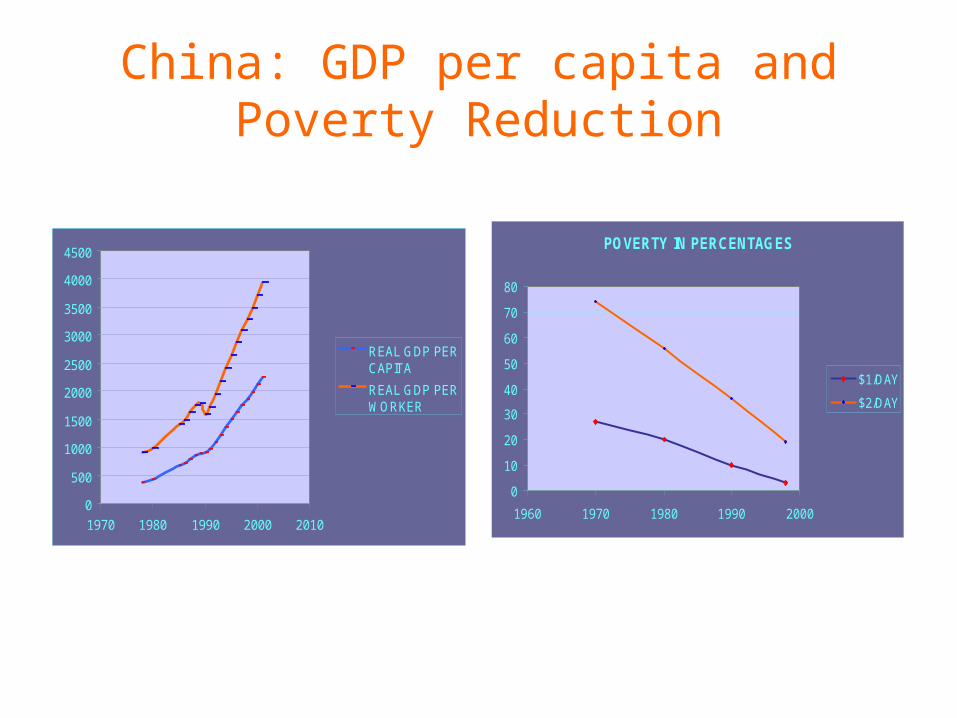

China: GDP per capita and Poverty Reduction

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1970 1980 1990 2000 2010

REAL GDP PERCAPITA

REAL GDP PERWORKER

POVERTY IN PERCENTAGES

0

10

20

30

40

50

60

70

80

1960 1970 1980 1990 2000

$1/DAY

$2/DAY

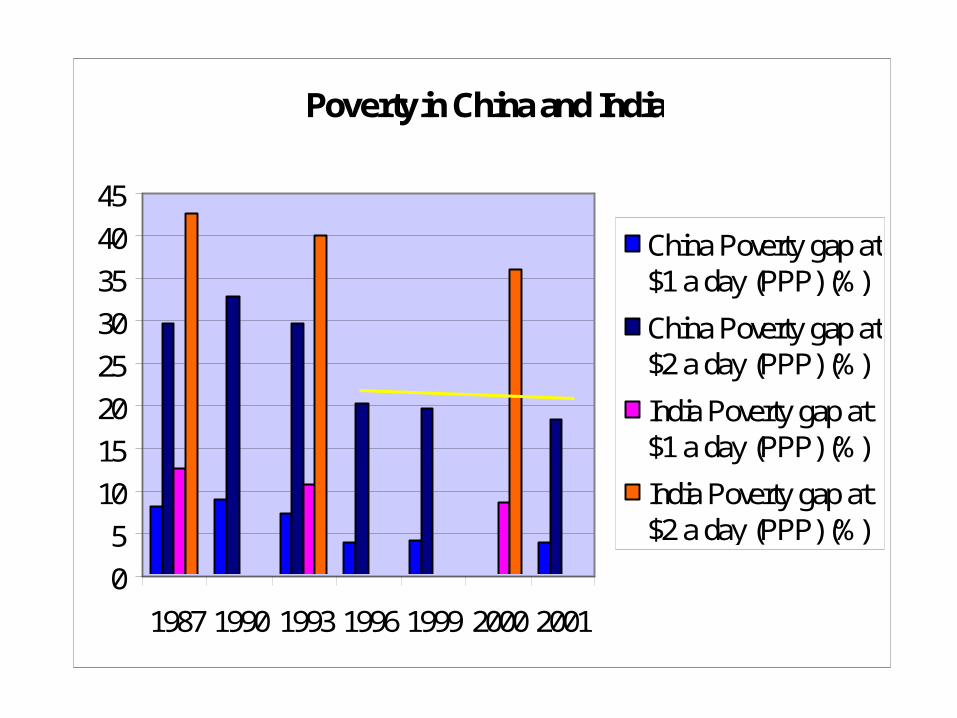

Poverty in China and India

0

5

10

15

20

25

30

35

40

45

1987 1990 1993 1996 1999 2000 2001

China Poverty gap at$1 a day (PPP) (%)

China Poverty gap at$2 a day (PPP) (%)

India Poverty gap at$1 a day (PPP) (%)

India Poverty gap at$2 a day (PPP) (%)

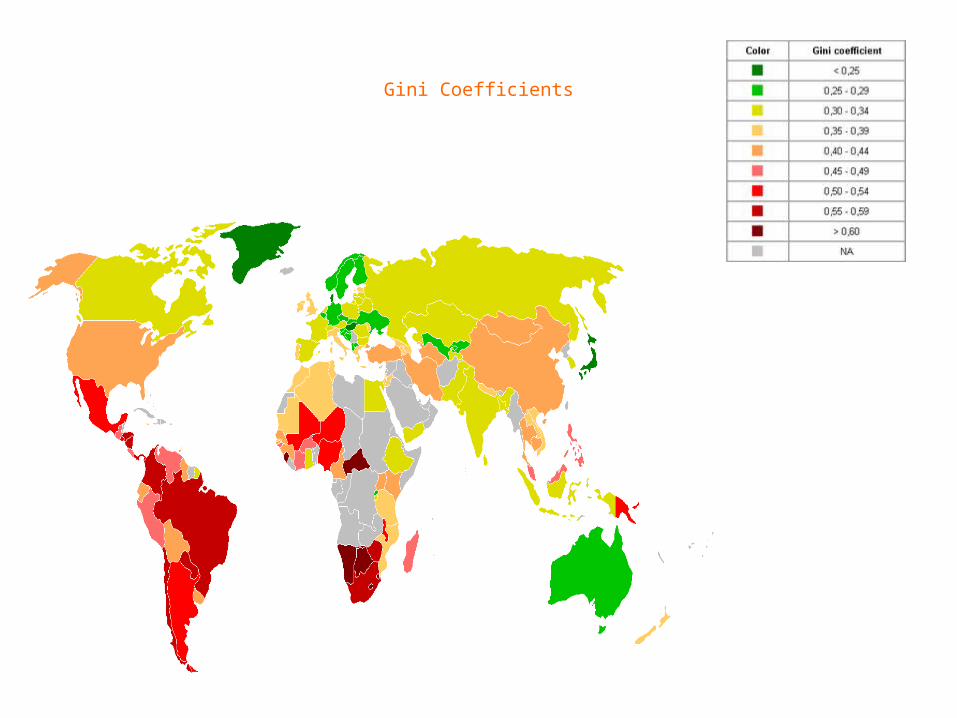

Income Inequality

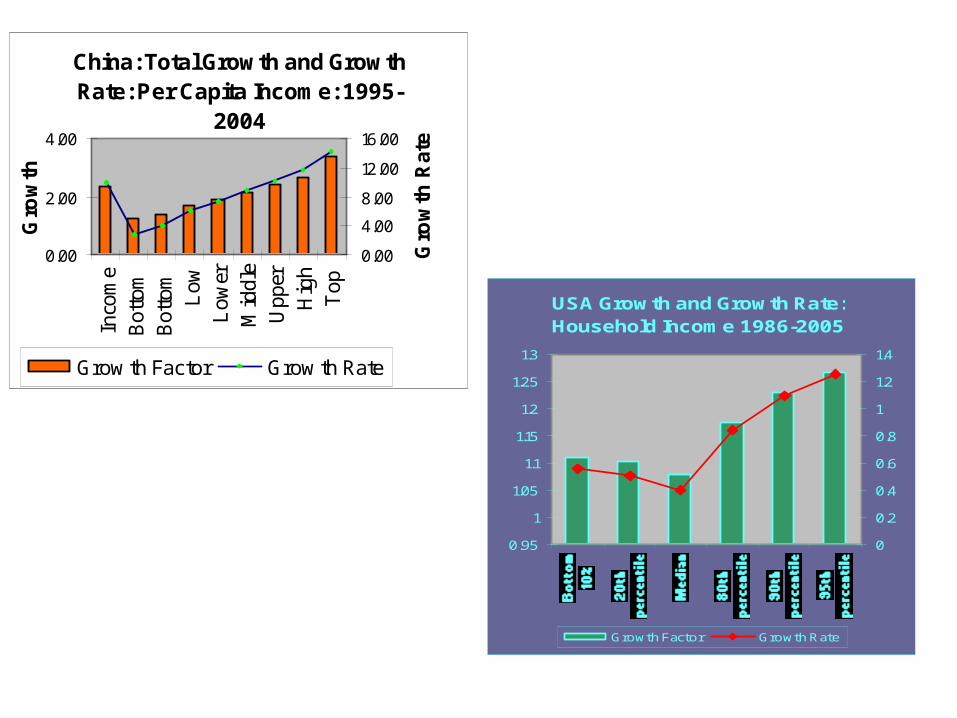

China: Total Growth and Growth Rate: Per Capita Income: 1995-2004

0.00

2.00

4.00

Gro

wth

0.00

4.00

8.00

12.00

16.00

Gro

wth

Rat

e

Grow th Factor Grow th Rate

GDP per capita: China and India (constant 2000 US$)

0

200

400

600

800

1000

1200

1400

1600

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

India GDP per capita(constant 2000 US$)

China GDP per capita(constant 2000 US$)

Rural Populations Decline

Rural Population Percentage

50

55

60

65

70

75

80

85

China Rural populationpercentage

India Rural populationpercentage

Saving and Investment

Savings and Investment in India and China

0

5

10

15

2025

30

35

40

45

1980 1984 1988 1992 1996 2000 2004

InvestmentRate (% ofGDP) IndiaSavings Rate(% of GD) India

Gross capitalformation (% ofGDP) ChinaGross savings(% of GDP)China

Leveraging the Global Economy

Trade in Relation to GDP China

0

10

20

30

40

50

60

70

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

China NE.IMP.GNFS.ZSImports of goods andservices (% of GDP)

China NE.EXP.GNFS.ZSExports of goods andservices (% of GDP)

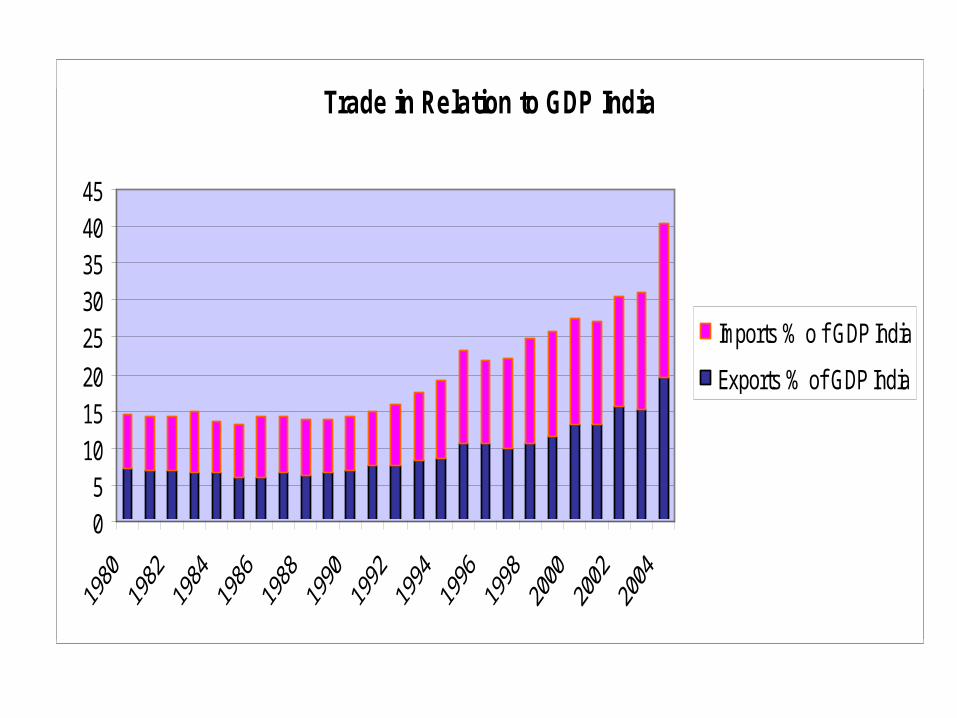

Trade in Relation to GDP India

05

1015202530354045

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Imports % o f GDP India

Exports % of GDP India

Trade in Relation to GDP India

05

101520

2530354045

Imports % o f GDP India

Exports % of GDP India

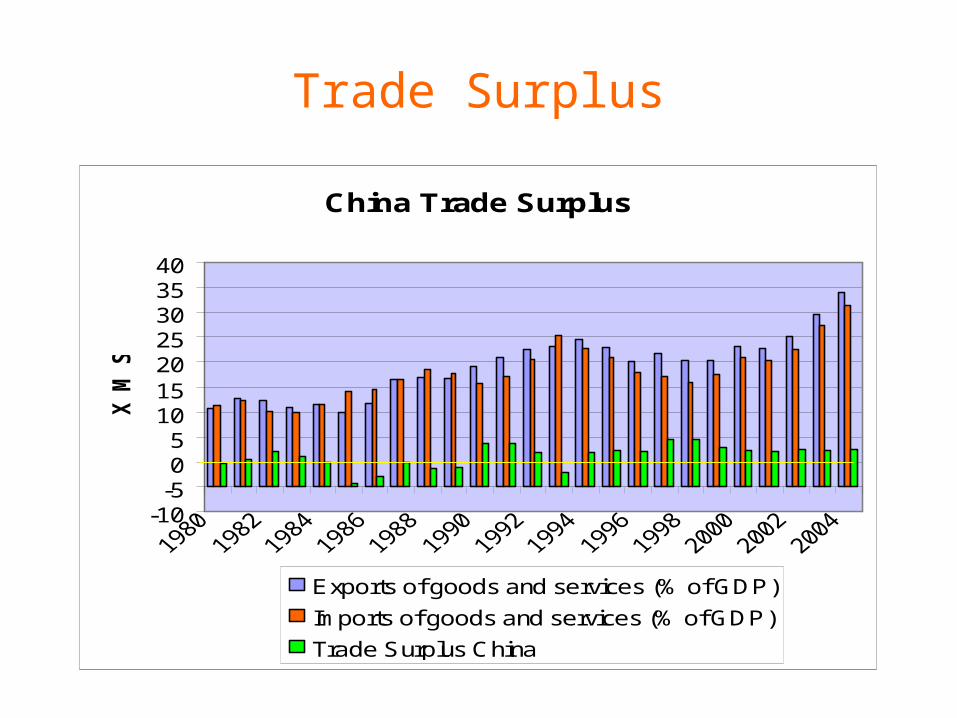

Trade Surplus

China Trade Surplus

-10-505

10152025303540

X M

S

Exports of goods and services (% of GDP)

Imports of goods and services (% of GDP)

Trade Surplus China

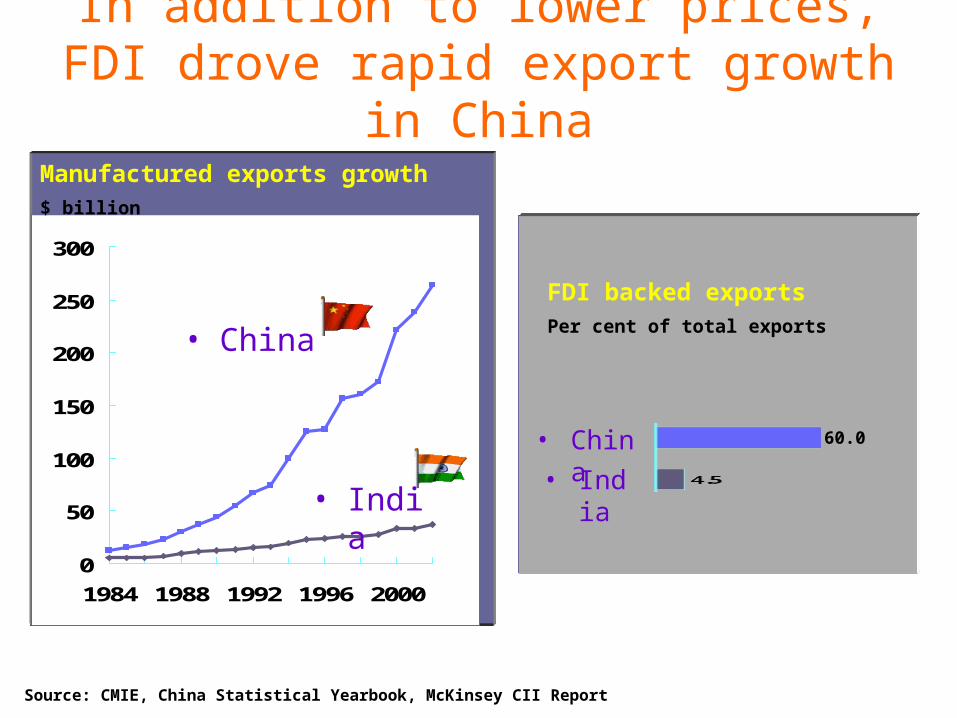

In addition to lower prices, FDI drove rapid export growth in China

0

50

100

150

200

250

300

1984 1988 1992 1996 2000

Manufactured exports growth$ billion

FDI backed exportsPer cent of total exports

• China• India

60.0

• India

• China

Source: CMIE, China Statistical Yearbook, McKinsey CII Report

China vs India - Infrastructure Formation

0306090

120

150180210240270

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

China India

India (RHS)

China (LHS)

US$ bn

Source: The World Bank; Deutsche Bank; CMIE

US$50 bn over the next 3 years

Public debt: China 24.4% of GDP (2005 est.)

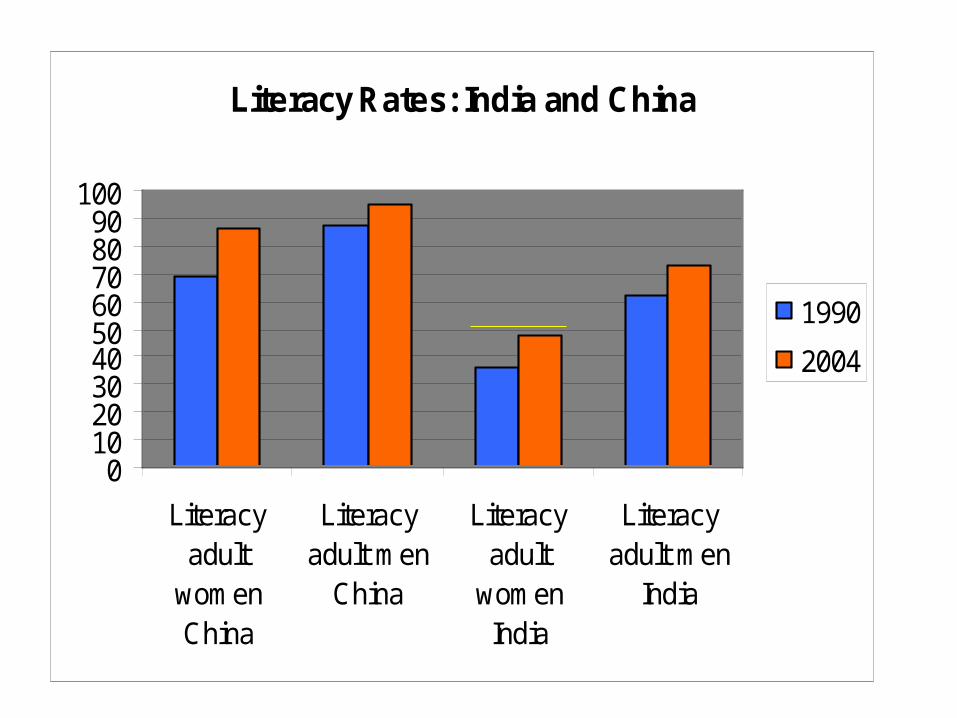

Literacy Rates: India and China

0102030405060708090

100

Literacyadult

womenChina

Literacyadult men

China

Literacyadult

womenIndia

Literacyadult men

India

1990

2004

Deng Xiaoping’s biography in brief

Secretary of Party under Mao

Banished to a tractor factory in Cultural Revolution

Returned under wing of Zhou Enlai

Banished by Gang of Four

Replace Hua Guofeng

Left Hua in Central Committee (essentially for life)

Challenges for China

• Maintaining high growth is the overriding goal– Managing economic relations with the rest of

the world• Managing Rural to Urban Migration – 13 to 15

Million People a Year• Absence of social insurance and services• Huge urban-rural productivity differentials• State Owned Enterprises – SOE’s

– Government Ownership

Capital Markets and Diversifying Sources of Growth

• Capital Markets and investment efficiency– Capital markets are quite underdeveloped

• Exchange Rate and External Imbalance– PBC (our Federal Reserve) accumulation of

foreign reserves • Diversifying sources of growth

– Manufacturing sectors– Service sector– Domestic Market

• “China is several different economies at different stages of development”

Capital Composition

Aside: Global Capital Markets

Gradual Appreciation of Currency is Likely

• The continuing need for direct credit and other controls on investment– Response to interest rates unclear

• Continuing capital controls are required to have a monetary policy targeted to inflation and growth and at the same time retain some control over the exchange rate.

• In addition with immature capital markets, there is the risk of destructive volatility – without capital controls

• Phasing these out at the proper rate as the capital markets develop is a key policy challenge

• Building capital markets and increasing efficiency of investment is a high current priority

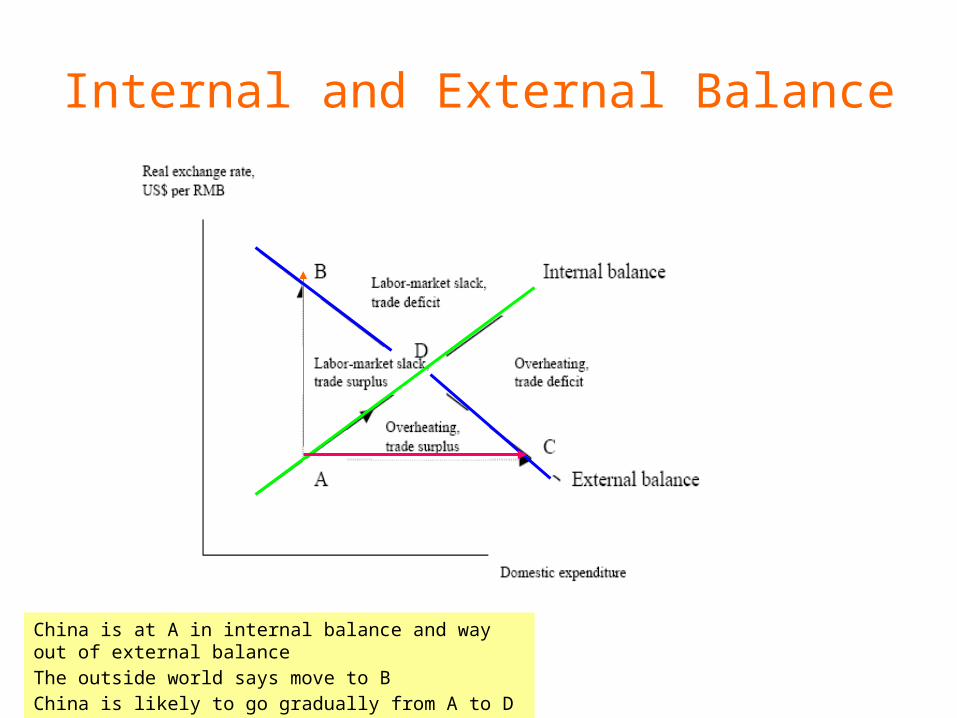

China is at A in internal balance and way out of external balanceThe outside world says move to BChina is likely to go gradually from A to D

Internal and External Balance

Reserves

Foreign Reserve Holdings at the End of 2006

0

200

400

600

800

1000

1200

China

Jap

an

Rus

sia

Rep

ublic

of C

hina

(Taiw

an)

Sout

h Kor

ea In

dia

Sin

gapo

re

Hon

g Kon

g, C

hina

Ger

man

y

Bill

ions

$

Recent Trends

• In 2007 in China– GDP: $2.8 trillion– Forecast trade surplus: $250-$300 billion– Surplus/GDP 10% or more– Investment/GDP: 40-45%– Savings/GDP: 50-55%– Exports + Imports as percentage of GDP: 70%– Reserves at the end of 2006: $1.2 trillion– Likely reserve additions: $400 billion or more– Reserves at the end of 2007: $1.6 trillion

40

50

60

70

80

90

100

110

120

Source: Bloomberg

Jun 97 October 22, 2003

Korean Won

Japanese Yen

Taiwan $

Thai Baht

Chinese Renminbi

China During Currency Crisis1997-1998

Challenges (continued)• Environment Problems - these are huge• Energy efficiency and security

– China plans to double its energy efficiency in the next decade

– Economic growth will still cause energy consumption to rise

• Rising Income Inequality• Overinvestment in infrastructure - underinvestment in

higher education• Internal market fragmentation – developing the domestic

market• Restoration of pension system and medical care –

especially in the rural areas

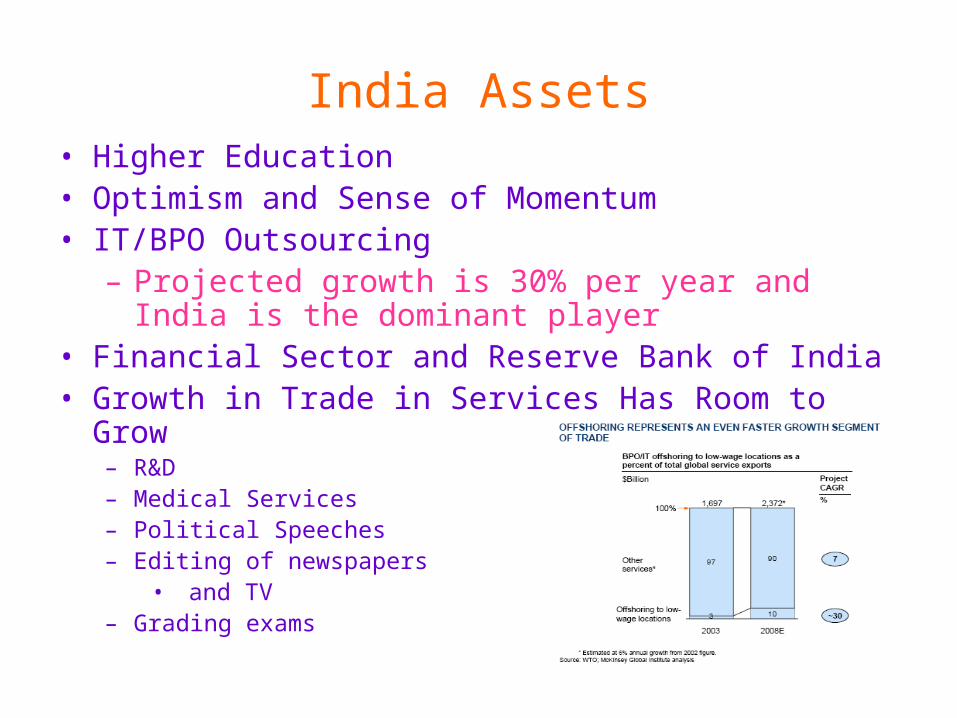

India Assets• Higher Education• Optimism and Sense of Momentum• IT/BPO Outsourcing

– Projected growth is 30% per year and India is the dominant player

• Financial Sector and Reserve Bank of India• Growth in Trade in Services Has Room to Grow

– R&D– Medical Services– Political Speeches– Editing of newspapers

• and TV– Grading exams

But

• This is not enough to produce and sustain high and inclusive growth – Doesn’t employ enough people

• India needs an additional powerful productive employment-generating engine

• This is very well understood by India’s leaders• Labor intensive manufacturing and exports

– Add the China approach to the portfolio• Open up to FDI• Special Export Zones (400+)

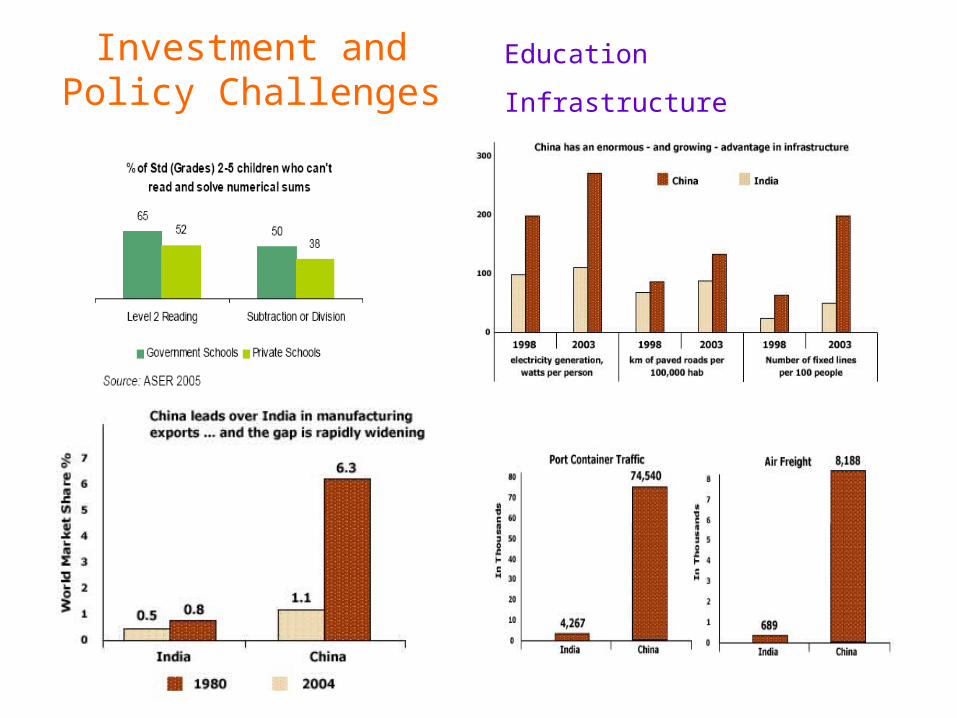

Investment and Policy Challenges

Education

Infrastructure

Efficiency and Investment in Agriculture

Impacts on Global Economy

• Rapidly growing trade with each other• Very large regional impact in east and south Asia

– Demand and imports from each other and more advanced neighbors

– Intense competition for less developed neighbors

• Competitive pressure on advanced economies– Europe in particular with less flexible labor

markets and social safety nets that constrain competitive responses

Demand for Energy and Commodities

• Large incremental demand for raw materials and commodities with effects of prices (China’s equivalent of our interstate highway system is an example)

• Potential scramble for energy security – because of the size of the demand shock

• Increased influence in Africa and other parts of the world

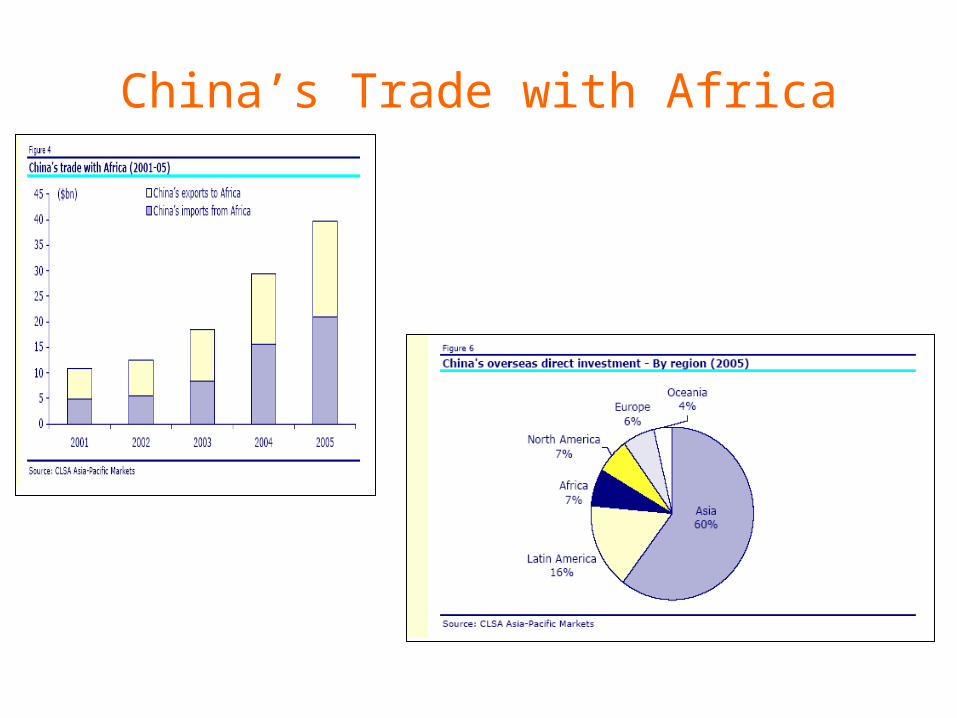

China’s Trade with Africa

Magnitude of Impacts Becoming Material

• In 1980 when China grew ten percent, the absolute increment to global GDP and global demand was insignificant.

• Now the GDP is about 2.22 trillion $, and a ten percent increment is large in absolute terms – The rough equivalent (in terms of global

demand) of about a 1.78% increment in US GDP growth

Demonstration Effects

• India has been galvanized by China’s growth• High growth is possible in a complex democracy• Can other developing countries compete with

China and India– locating comparative advantage

• Quality of the economic policy debate

The Latest Entrant: Vietnam

Vietnam: GDP per capita

0

500

1000

1500

2000

2500

3000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

GDP per capita, PPP (constant 2000 international $)

Growth Rate 5.88%

South Africa: GDP/capita PPP adjusted constant dollars

0

2000

4000

6000

8000

10000

12000

South Africa: Saving and Investment

05

10152025303540

Gross capital formation (% of GDP)

Gross domestic savings (% of GDP)

South Africa Gini Coefficient

0

10

20

30

40

50

60

70

Rising Income Inequality and Resistance to Globalization

• Developed Countries– Middle income lag– Protectionist sentiment– Trade in services and

globalization of some labor markets

– Impact of technology

• Developing Countries– Rising inequality side

effect of benign growth dynamics (China and India)

– “Inclusiveness”– Unequal distribution of

assets can retard growth

USA Growth and Growth Rate: Household Income 1986-2005

0.95

1

1.05

1.1

1.15

1.2

1.25

1.3

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Growth Factor Growth Rate

China: Total Growth and Growth Rate: Per Capita Income: 1995-

2004

0.00

2.00

4.00

Income

Bottom

Bottom

Low

Lower

Middle

Upper

High

Top

Gro

wth

0.00

4.00

8.00

12.00

16.00

Gro

wth

Rat

e

Grow th Factor Grow th Rate

Global Warming

• Decision making under extreme uncertainty– Very long time horizons– Large ranges in the estimates of climate

impacts– These will decline over time as the

science becomes more precise• The stocks and the flows of green house

gases– The Kyoto impasse– How to allocate the emissions rights

equitably

Three Major Sets of Issues

• 1. Mitigation – Allocation of emissions rights across countries– Efficiency – carbon trading market mechanisms

• 2. Technology – Reduction of the costs of mitigation– Subsidies and rapid transfer globally

• 3. Adaptation– Capacity to adapt to climate change that does

occur– Poorer country problem

• RESPONDING TO CLIMATE CHANGE IS A MAJOR TEST OF OUR COLLECTIVE CAPACITY FOR GLOBAL GOVERNANCE

Demand for Energy and Commodities

• Large incremental demand for raw materials, commodities, and energy with effects on prices (China’s construction of the equivalent of the US interstate highway system is an example)

• For developing countries with commodity exports, the effect can be beneficial in the short run – but rising commodity prices is not a basis for sustained growth

• Generally rising energy costs hurt poor countries more than richer ones

• Potentially damaging scramble for energy security – because of the size of the demand shock – and the potential for supply problems in unstable regions

Global “Imbalances”

United States Savings and Foreign Reserves

Foreign Reserve Holdings at the End of 2006

0

200

400

600

800

1000

1200

China

Jap

an

Rus

sia

Rep

ublic

of C

hina

(Taiw

an)

Sout

h Kor

ea In

dia

Sin

gapor

e

Hon

g Kon

g, C

hina

Ger

man

y

Bill

ions

$

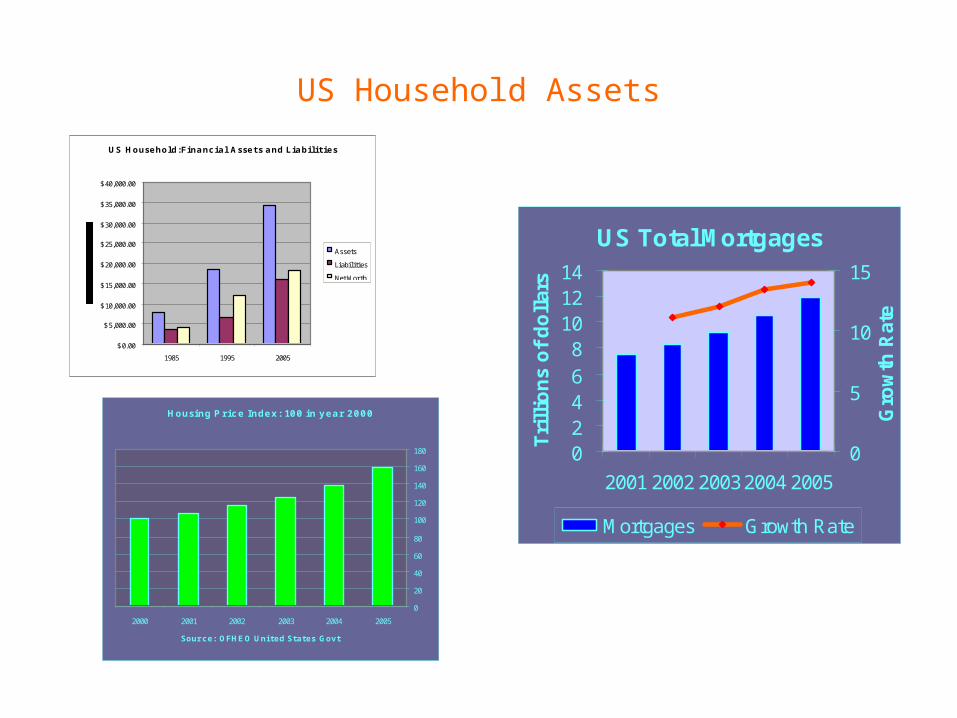

US Household Assets

US Household:Financial Assets and Liabilities

$0.00

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

$35,000.00

$40,000.00

1985 1995 2005

Assets

Liabilities

Net Worth

US Total Mortgages

02468

101214

2001 2002 20032004 2005

Tri

llio

ns

of

do

llar

s

0

5

10

15

Gro

wth

Rat

e

Mortgages Growth Rate

Housing Price Index: 100 in year 2000

0

20

40

60

80

100

120

140

160

180

200520042003200220012000

Source: OFHEO Uni ted States Govt

Recent Trends

• In 2007 in China– GDP: $2.8 trillion– Forecast trade surplus: $250-$300 billion– Surplus/GDP 10% or more– Investment/GDP: 40-45%– Savings/GDP: 50-55%– Exports + Imports as percentage of GDP: 70%– Reserves at the end of 2006: $1.2 trillion– Likely reserve additions: $400 billion or more– Reserves at the end of 2007: $1.6 trillion