the implications of dumping of agricultural products …

TRANSCRIPT

1THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

The Implications of Dumping ofAgricultural Products in Asia:Asian Farmers’ Untold Misery

IntroductionThe push for tariff reduction worldwide along

with the pressure to eliminate productionsubsidies, which has been largely commandedby the World Trade Organization (WTO), hasbrought serious repercussions to the dominantlyagrarian Asian economies. Across thesecountries, there have been unprecedenteddeclines in agricultural tariffs and other non-tariffbarriers as well as production support as a resultof their commitments to the WTO Agreement onAgriculture (AoA). Compounding the trend are theagreements being introduced either bilaterally orthrough the regional trade blocs, which are meantto ensure and fast-track the trade liberalisationthat has been time and again derailed in the WTOnegotiations.

The AoA has become one of the mostcontentious agreements because of itsfundamental flaws of subjecting subsistenceagriculture to trade liberalisation and increasingthe role of the corporation. Its impact on thelivelihood and survival of the small Asian farmershas been most illustrative of the basic argumentsagainst further agricultural trade reform. But apartfrom these key issues, the AoA and other tradeagreements in agriculture that tend to complementthe AoA have also institutionalised dumping – theunbridled and unprecedented influx of cheapagricultural products in Asia and elsewhere, whichhas hastened the erosion of the agrarianeconomies and their capacity for futureindustrialisation.

WTO Injustice: How Dumping isInstitutionalised

Dumping is the practice of a firm, wherein thefirm exports at a price that is lower than the priceof a similar product in the exporting country. Thedifference between the export price and thedomestic price (the price in the exporting country)is called the dumping margin. It is also considered

WriterRos-b Guzman (IBON Foundation Inc.)

Editor-in-chiefSarojeni Rengam (PAN AP)

Editor and Project CoordinatorGilbert Sape (PAN AP)

Production StaffXin Ying Tan (PAN AP)Norly Grace Mercado (PCFS)

Lay-out and Cover DesignSinag de Jesus (Red Leaf Designs)

ContentsIntroduction

WTO Injustice:How Dumping is Institutionalised

The Subsidy War:Simply an Inter-Imperialist Dispute

Globalising Asian Agriculture

Domestic Support

Market Distortions by the US and EU:Who suffers?

The Myriad of Catastrophes

Notes

Abbreviations

Definition of Terms

1

1

3

5

9

13

21

28

30

30

2 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

dumping when the export price is a lot lower thanthe combined cost of production, marketingexpenses and a reasonable profit.1

Dumping is an unfair trade practice becausethe firm undercuts its competitors. It is explicitlyprohibited in the WTO. But how exactly a firmmanages to lower its export price without losingits profit margin is one of the most interestingarguments against the WTO. It appears thatdumping prospers mainly through institutionalsupport, which interestingly has been provided bythe WTO.

The AoA has all the elements thatinstitutionalise and strengthen the practice ofdumping. The three main categories ofcommitments in the AoA, namely (1) marketaccess, (2) domestic support and (3) exportcompetition, which are purported to removedistortions to trade have only permitted developedcountries to do the reverse – increase theirdomestic subsidies, retain their export subsidies,and cushion their producers from imports surgesand price fluctuations.

The AoA binds all WTO member countries toreduce their tariff levels, abolish quantitativerestrictions, convert non-tariff barriers into tariffs,reduce domestic support, and reduce exportsubsidies. The developing countries are subjectedto the same rules in agricultural trade liberalisationas the developed countries, the only concessionbeing slightly lower reduction rates and slightlylonger time schedules. Least developed countries(LDCs), on the other hand, are not required toreduce tariffs or subsidies but just the same arenot allowed to raise them.2 In short, all WTOmember countries should go by a programme ofprogressive liberalisation that is supposedlydesigned to ‘level the playing field’ and bring abouthealthy competition in agricultural trade.

But the AoA is inherently imbalanced, the mainform of injustice being in the area of domesticsupport. There are three categories of domesticsupport measures that fall under what the WTOcalls “boxes”:

1. Amber Box – input subsidies and pricesupport – these are viewed to be trade-distorting and have repercussions onproduction2. Green Box – support for research, ruraldevelopment and public stockholding andmarketing – these are assumed to have noeffects on production

3. Blue Box – direct payments to farmers tocompensate them for programmes that limittheir production

Subsidies in the Amber Box are subject toreduction discipline. A certain limit of subsidiesmay be exempted – 5% of the total value ofagricultural production for developed countries and10% for developing countries. But subsidies abovesuch levels have to be reduced – 20% from their1986-88 levels in a period of six years fordeveloped countries and 13% over 10 years fordeveloping countries.

Subsidies in the Green Box and the Blue Box,on the other hand, are viewed as minimally trade-distorting and connected to production-limitingscheme therefore not subject to reduction.

There are two reasons that make the area ofdomestic support unfair. One, to begin with, poorcountries had already used minimal subsidies inthe past or had been asked by the InternationalMonetary Fund (IMF) to reduce subsidies as partof the IMF structural adjustment programme(SAPs) of liberalisation. Their percentages ofreduction, therefore, were already two-thirds oftheir existing subsidies; some even had zero-levelsubsidies, when the WTO-AoA came into force.On the contrary, percentages of reduction for richcountries, which have always used subsidiesheavily to support their agricultural production,represented only a small portion of their existingsubsidies.

As a result, while poor countries are nowprohibited from using or increasing domesticsupport beyond the de minimis level of 10% oftotal agricultural value, rich countries have retainedup to 80% of their subsidies even after the six-year implementation period.

Two, the U.S. and the E.U., by putting in severalsubsidies in the Green Box and the Blue Box, havesucceeded in excluding from reduction severaltypes of subsidies such as U.S. direct paymentsand E.U. compensation payments, along with along list of other non-actionable subsidyprogramme. As a result, the total domesticsubsidies in the rich countries are now even muchhigher compared to their 1986-88 base level.3

For instance, the E.U. 1986-88 subsidy levelwas USD83 billion and increased to USD95 billionin 1996. For the U.S., the base period subsidylevel of USD50 billion increased to USD59 billiononly in the first year of implementation. Accordingto the OECD, the total subsidy and all its

3THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

equivalents rose from USD99.6 billion in 1995 toUSD129.8 billion in 1998 in the E.U. and USD41.4billion to USD46.9 in the same period coverage inthe U.S. Another comprehensive calculation bythe OECD, the Total Support Estimate (TSE) for24 OECD countries, shows domestic supportrising from USD275.6 billion for the base year toUSD326 billion in 1999.4

Developing countries managed to gain minimalspecial and differential treatment (SDT) andexempt four items:

1. input subsidy given to poor farmers2. subsidy for land improvement3. diversion of land from production of illicitnarcotic crops4. provision of food subsidy to the poor

But these are minimal compared with the U.S.and E.U. exemptions, and hardly half a dozen ofthe poor countries use these subsidies.5 Inaddition, the U.S. and E.U. subsidies are alsoexempted from “due restraint” action by the WTOunder its dispute settlement process while thoseused by the poor countries are not immune fromcountervailing measures.

Developed countries have also retained 64%of their budget allocations for export subsidies and79% of their export subsidy coverage. Developingcountries meanwhile had not been using exportsubsidies for a long time, and if ever they hadminimal exceptions, should now reduce and stopusing such.6

With regard to market access, the AoA madelittle progress in reducing agricultural protectionin the developed countries. To illustrate, in the firstyear of AoA implementation, tariff rates for richcountries were so high – 244% for sugar in theU.S.; 213% for beef in the E.U; 353% for wheat inJapan; and 360% for butter in Canada – that evenif their rates were reduced by 36% on average toend-2000 would still be prohibitive.7

One area of inequity in market access is the‘special safeguard’ provision, whereby countriesthat went through tariffication may protect theirfarmers when imports rise above or prices fallbelow specified levels. But only few developingcountries undertook tariffication. Furthermore, thecriteria for the use of ‘special safeguard’ arestringent if not unclear in the WTO, aside fromthe fact that the requirements are hard todemonstrate in household subsistence agriculture.

Still, when the developing country is the

exporter, the developed countries may takesafeguard measures even if the exportingdeveloping country has low import base ordeclining production. Although there is a deminimis provision that says no safeguard actionwill be taken against the exporter as long as itsshare to total imports of the product in theimporting country does not exceed 3%, it is barelyfollowed by the developed countries.

Another area of inequity in the market accessis the ‘minimum access opportunity’, wherecountries, after tariff reduction in certain productshave not provided substantial market access, aremade to import modest amounts of these products.These high-tariff products are usually theabundantly produced and therefore mostprotected agricultural and food products of thedeveloping countries.8

Apart from the inherent imbalances of the AoA,it has the basic flaw of assuming that agriculturalproduction and trade in the developing world couldbe done commercially and that a “fair” tradeagreement could arise from decades of colonialtrade patterns between the developing anddeveloped countries. The combination of theseissues has led to unbridled and unprecedenteddumping of agricultural products in poor countriesand the consequent collapse of rural economies.

The Subsidy War: Simply an Inter-Imperialist Dispute

The AoA has a built-in mechanism that providesfor a scheduled review and renegotiations towardsfurther liberalisation despite protests overimbalances and implementation issues. This iswhy the controversy has not subsided even up tothe time of the collapse of the so-calledDevelopment Round in 2006.

In Doha in 2001, the WTO, despite thornyissues, launched the Development Round thatwas supposed to start in the MinisterialConference in Cancun in 2003 through anundemocratic process called ‘Chairman’sUnderstanding’ as reaching ‘consensus’ and theformation of the Trade Negotiations Committeetasked to prepare all requisites for a new round inCancun.

Cancun collapsed. In agriculture, the collapsewas due to the rejection of the Harbinson Text andthe joint U.S.-E.U. proposal that sparked debateson framework and modalities, summarised into thefollowing:

4 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

1.Further tariff reduction2.Inclusion of the remaining sensitive cropsof the developing countries in liberalisation3.Further increase in exempted domesticsubsidies enjoyed by the developedcountries4.Continuation of export subsidies enjoyedby the developed countries5.Reduction by 10% the list of products vitalto food security, rural development, andlivelihood security6.Redefinition of SSG measures in order toinclude subsidies of developed countries9

The emergence of clear country groupingsdivided the lines in Cancun. G21, later called G20,led by India and Brazil and composed of countriesactive in agricultural trade such as China,premised further market access on the reductionof subsidies by the developed countries. G33, ledby Indonesia, focused on the issue of dumping byproposing special products (SP) and specialsafeguard mechanism (SSM) provisions thatwould allow further tariff protection and safeguardsfor certain basic food and agricultural products.

The intensity of the debate was mainly broughtabout by increased dumping. Even before the timeof Cancun, developing countries alreadyexperienced devastating changes: skyrocketingworld commodity prices, depressed farmgateprices, massive farmers’ bankruptcies, and ruralunrest. These phenomena also prevented elitegovernments of the Third World from simplyallowing further market access and dumpingwithout clear concessions from the global powers.

But for the Ministerial Conference in Hong Kongin 2005, the Five Interested Parties (U.S., E.U.,Brazil, India and Australia) pushed for the JulyFramework Agreement, summarised as follows:

1.The North still defending their high levelsof subsidies (AoA)2.Bringing down non-agricultural tariffs(NAMA)3.Still pushing for the New Issues(Government Procurement, CompetitionPolicy, Investments, Trade Facilitation)4.Pushing to make offers for theliberalisation of services (GATS)10

In particular in agriculture, the July Frameworkproposed a new formula for further tariff reductionbased on ad valorem and offered milder NAMA

and GATS as compromises for increased marketaccess in agriculture. Rich countries alsoproposed to create a new restrictive categorycalled Sensitive Products, focusing on tariff-ratequotas only, which poor countries do not use. Yet,the July Framework set aside talks on thedemands of poor countries on SPs and SSMs.

Rich countries also skirted the issue of the“boxes”, promising nothing on the target date forthe phase-out of the Amber Box and still not puttingin place an overall ceiling for the Green Box. Yet,they proposed to include in the Blue Box subsidiesnot necessarily limiting production, thereby merelyshifting domestic support from the Amber to theBlue Box. The E.U. even offered to remove itsexport subsidies on the improbable condition thatthe U.S. removes its ‘food aid’, export credits andcredit guarantees, and monopoly of state tradingenterprises. The SDT for the poor countries andstate trading by net food importing countries werenot tackled at all.

Before Hong Kong, especially after the collapseof Cancun, trading and investment corporationswere already growing impatient over the slowWTO process, given endless disputes andinconclusive talks. Yet, despite setbacks, the DohaRound had undoubtedly inched ahead, and HongKong was thus intended not exactly to close theDoha Deal but to set the stage for its completion.

The timetable was that by April 2006 formulascalled modalities would have been incorporatedinto the countries’ tariffs and products. The overallidea was to conclude the talks by the end of 2006so that the Doha Round could be ratified in theU.S. legislature before the legislators’ terms endin mid-2007.11

In agriculture, the idea was to cluster tariffs intobands (or ranges of tariffs) with correspondingreduction for each band, minimizing the chancesof “hiding” low tariffs behind high tariffs. With regardto domestic support, nothing much was achievedin Hong Kong as the principle of “you first” stillprevailed between the U.S. and the E.U. The U.S.proposed to cut its subsidies by 60% if the E.U.would cut its subsidies by 83%, but the E.U. wouldonly go as far as 70 %. Moreover, both the U.S.and the E.U. managed to retain and even includeexemptions in the Blue Box and Green Box. Finally,with regard to the reduction of export subsidies,the compliance is still six years away in which timemuch may still be maneuvered. Still, even if theE.U. eventually complies, the reduction would onlybe around 10% of its total agricultural support.12

5THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

After Hong Kong, talks and several GeneralCouncil meetings were set in Geneva betweenMay and July 2006 to meet the Hong Kongdeadlines. Apart from these, small-groupmeetings, so-called green room sessions andmini-ministerials were happening round the worldto settle issues but in favor only for thoseattending.

The Group of Six (G6) meetings between theU.S., E.U., Japan, Australia, Brazil and India, inparticular, mandated by the heads of the G8,sought to settle issues on farm and industrialgoods. By July 24, however, these talks hadcollapsed as the G6, chaired by the WTO chiefPascal Lamy, failed to agree on the steps towardsfurther trade liberalisation. The failure had signaledthe breakdown of the five-year Doha Round.

The main cause of the WTO collapse was thestalemate on the key area of domestic agriculturalsupport where the U.S. did not budge an inch fromits original position and instead blamed the othersfor being inflexible on their tariff stands. Since then,the U.S. and the E.U. have engaged in a war ofwords and what the U.S. accused the E.U. of –‘blamesmanship’, further illustrating theirirreconcilable dispute.13

The collapse only shows that the majorstumbling block is still the inter-imperialist disputebetween the U.S. and the E.U. on subsidies.Despite having made significant headway towardsdrastic liberalisation of poor markets, toned downthe SP and SSM demands of the poor countries,and neutralized China, to name a few“achievements”, the U.S. and the E.U. still haveto confront each other on their own protectionism.

The collapse also exposes the emptiness ofWTO development rhetoric, with the U.S. and theE.U. dominating the trade body to serve theirnarrow interests, not to mention the arrogant andautocratic streak of the U.S.

On the other hand, although temporarily, theWTO collapse has stymied the fast and sweepingglobalisation process from opening up further themarkets of poor countries. And this provides anopportunity for poor countries to review the paceof agricultural trade liberalisation and its impacton the survival of the farming communities.

Globalising Asian AgricultureAgricultural trade liberalisation happened

drastically in Asia despite longer schedules andlower reduction rates. Asian agriculture was neverready for trade liberalisation due to its non-

commercial nature and subsistence level, and thefact that as a result, agricultural products were notexactly Asia’s relative advantage in world trade.

Prior to the WTO, most of Asian agriculture wasdevoted to domestic and household consumptionwith only about less than 10% of production tradedglobally. Agricultural products were produced onsmall-scale, with very few exceptions for export.Asian agriculture had little protection – lowdomestic support, no export subsidies, and onlyfew agricultural imports were imposed with non-tariff barriers.

In the advent of the WTO, Asia, especiallySouth, East and Southeast Asia, had the steepestdecline in tariff averages for all products. (SeeTables 1 and 2) In agriculture, the applied ratesof selected Asian countries were a lot lower thantheir bound rates, with Indonesia standing out withonly 5 % applied tariff. (See Table 3)

Applied tariffs were low because of tariffreforms that had been ongoing for a decade beforethe WTO, mostly as loan conditionality. But asidefrom being dictated by international creditors toreduce tariffs, as already mentioned, countriesalso committed to continue reducing applied tariffsafter the AoA implementation period by anunweighted average of 24% over 10 years, subjectto a minimum reduction of 10% in each tariff line.Given the big difference between bound andapplied rates, such commitment was notnecessary to reduce applied rates over theimplementation period, but countries havecontinued to reduce their applied tariffs anyway.Indonesia, for instance, has 5 percent averagetariff for agriculture as compared with the targetof 13.2 % for 2003 under its Pakmei ’95Programme. 14

Indonesia focused on non-tariff barriers (NTBs)such as import licensing restrictions in the 1990s,which affected 1,000 items. But the number hadfallen to 200 in 1996 and declined further asIndonesia committed to the WTO. In agriculture,the country bound 100% of its tariff lines andcommitted to remove all NTBs, including theremaining local content rules for soybean meanand dairy products, licensing rules for alcoholicbeverages, and public importation rights given forrice, soybeans, sugar, wheat and wheat flour toBULOG, the National Food Logistics Agency, andto Clove Marketing and Buffer Stock Agency(BPPC) for cloves.

In 1995, Indonesia implemented Pakmei ’95,a long-term tariff reduction package ending in 2003

6 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Developing countries

Africa

North Africa

Sub-Saharan Africa

Sub-Saharan Africa lessSouth Africa

america

Central America and theCarribean

South America

Asia

West Asia

South, East and South-EastAsia

South, East and South-EastAsia less China

Developing countries lessChina

Least developed countries

34.4

35.1

38.3

33.8

33.8

24.9

29.5

11.2

36.5

12.5

43.7

4.3

34

41.7

27.3

25.6

31.2

22.8

22.8

26.6

18.4

29.7

29.6

13.9

36.2

35.9

27.1

29.2

27.6

26.1

28.5

25.4

25.4

23.9

25.7

31

13

35.9

35.5

27.2

34.4

21.9

26.5

24.4

32.8

32.8

12.3

12.2

26.8

10.6

29.5

28.8

21.3

48.7

18

20.5

22.3

20

20.2

14

14.9

13.2

21

10.7

22.6

22.6

17.9

23.5

15

20.6

25

19.2

20.2

12.7

12.1

13.5

14.4

8.8

16.5

16.4

15.1

18.2

12.6

25.8

26.1

15

15.3

10.4

8.9

12.1

11.9

10.1

12.6

12.4

12.6

13.4

REGION 1980-1983 1984-1987 1988-1990 1991-1993 1994-1996 1997-1999 2000-2001

TABLE 1. UNWEIGHTED TARIFF AVERAGE IN PERCENT FOR ALL PRODUCTS

Source: UNCTAD

Developing countries

Africa

North Africa

Sub-Saharan Africa

Sub-Saharan Africa lessSouth Africa

america

Central America and theCarribean

South America

Asia

West Asia

South, East and South-EastAsia

South, East and South-EastAsia less China

Developing countries lessChina

Least developed countries

19.7

26.3

26.9

25.8

25.8

24.7

25.1

16.6

23.8

23.8

19.7

42.8

22.2

20.9

21.2

20.3

20.3

28.6

13.2

36.4

20.9

10.3

24

22.6

18.6

37.7

17.9

22.5

20

26.8

26.8

20

24.9

17.1

13.4

17.6

14.9

14.2

42

14.1

19.4

19.4

12.4

12.5

14.2

10.4

14.5

11.5

10.5

11.4

15.5

19.7

12.1

16

11.9

11.6

12.1

11

8.2

11.2

8.7

10

49

9.9

14.8

18.6

10.2

19.3

14.1

14.8

13.1

8.2

7.6

8.3

6.6

9.2

19.1

11

14

22.7

10.7

14.6

13.5

14.7

11.2

9.7

8.3

9.8

7.8

10.4

14.6

REGION 1980-1983 1984-1987 1988-1990 1991-1993 1994-1996 1997-1999 2000-2001

TABLE 2. WEIGHTED TARIFF AVERAGE IN PERCENT FOR ALL PRODUCTS

7THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

with a three-tiered tariff structure of 0, 5 and 10%. Approximately 20% of agricultural items suchas fruits and vegetables were exempted andaverage tariff for agriculture was targeted to bearound 13.2 % in the final year.

But the IMF Letter of Intent in 1998 (in theaftermath of the Asian financial crash) resulted in

a faster pace than that envisioned under Pakmei’95. To reduce the inflationary impact of the rupiahdepreciation on food prices, the Indonesiangovernment agreed to reduce all food tariffs to 5% and phase out all NTBs including BULOG’smonopoly over imports.

TABLE 3. BOUND AND APPLIED TARIFFS

Source: WTO Agreement on Agriculture: The Implementation Experience of Developing Countries, FAO CorporateDocument Repository, UNCTAD

Bangladesh*

Botswana*

Brazil

Costa Rica

Côte d’Ivoire

Egypt

Fiji

Guyana*

Honduras

India

Indonesia

Jamaica

Kenya*

Malawi

Morocco*

Pakistan*

Peru

Philippines

Senegal

Sri Lanka*

Thailand

Uganda

Zimbabwe

200% average (except 50% for13 lines) plus30%. Other duties or charges (ODC) on allproducts

Average n.a. (mostly in the range of 0-100%)

35% average (0-55% range)

n.a.

15% (except between 5 and 75% for 25 items)

62% in the base period, to fall to28% averagein 2004

40% (except for rice and milk powder boundat 60%, to be reduced to 46% by 2005)

100% average plus 40% ODCs

35% with some exceptions

116% average (about half of tariff lines at100%, and one-third at 150%)

Quite variable, averaging more than 70%

100% average plus 15% ODCs(higher ODCson 55 lines and three Harmonized System[HS] chapters)

100% average

125% generally except for a few products withceiling rates of50%, 55% and 65%

65% average (34% for 71% of the tariff lines)plus 15% ODCs

101% average

30% average (68% for 20 food products)

Average 13.26% in 2000; up to100% initiallyon sensitive commodities reducing to 30-50%

30% average + 150% ODCs

50% average

36% average

80% generally, with some between 40-70%

150% (with a few exceptions at25% and 40%)

25% average

Average 6% (typically 0-35%; formula duties for 6 lines

11% average (maximum of 20% linked to maximumMERCOSUR CET rate)

14.8%

16.4% (2001)

18.5% average (21.8% including ODCs)

Most agricultural imports 15%, and maximum rate 27%

Average n.a. (maximum rate is40% - the CARICOMCET rate)

11% with some higher rates

26% average (89% of tariff lines at 50% or lower,74% between25% and 50%)

5%, with 0% tariffs on food items except for rice and sugar

Average 20.2% (maximum applied rate is 40% - theCARICOM CET rate), additional stamp duties

17% average

15% average

n.a.

Maximum rate 35%

12% generally with maximum of20% for somesensitive products

Average n.a., but 10%, 20% or30%

Now range from 10% to 20%, in line with WAEMU CET

Maximum 35%, with some exceptions

32% average

11.2% average, plus ODCs of 6%

Applied rates average 4-6% up to75% by HS chapter

Country Bound rates Applied rates

8 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Although rice and sugar wereexempted from Indonesia’s IMFcommitment of zero tariffs for food itemsand BULOG’s monopoly over rice importswas not eliminated, Indonesia lateropened up rice trade to the private sectoras well. Beginning in January 2000, thecountry introduced new import licensingrestrictions to sugar processors but wouldhave to eliminate such under the WTO.15

Similarly, the Philippines went throughthe Tariff Reform Programme (TRP) underthe IMF prior to the WTO, which resultedin substantial tariff reduction. The firstphase of the TRP-I in the 1980s, implemented aspart of an IMF SAP, reduced tariff rates from 100% to between 10 and 50 %. This was interruptedby the political and economic crises at that timebut was continued by the former Philippinepresident Corazon Aquino’s administration in 1986after the ouster of the Marcos dictatorship.Agricultural export taxes were removed andfertiliser and wheat imports were liberalised. From1986 to 1988, a total of 2,287 items wereliberalised and this marked the end of the firstphase. The second phase of TRP-I liberalisedanother 185 items and tariffied QRs, affecting 36tariff lines including agricultural products.16

The Philippine government implemented TRP-II in 1991, which reduced the number of high-tariffcommodity lines over a five-year period ending in1995. Executive Order 8 issued in 1992 tariffiedQRs affecting 153 commodities and liberalisedanother 286 items. By the end of that year, only21 agricultural commodities were left regulated outof 632 in 1970.

This was however reversed by the MagnaCarta for Small Farmers Law in 1993, whichrequired QRs on agricultural products growndomestically in sufficient quantities, otherwisecalled sensitive crops. After the long-termProgramme of import liberalisation, the MagnaCarta (which was a protection mechanism) waspassed and re-instituted QRs on rice, corn, pork,poultry, garlic onion, vegetables, and coffee. Butbeef and sugar remained liberalised. Then lateron, the QRs (except for rice) were removed underthe WTO.17

The Philippine initial and bound tariffs for thesensitive crops were within the range of 95-100 %in 1995 and 1996. By the end of the AoA, boundtariffs for all sensitive agricultural commodities wouldfall within the range of 10-50 % (See Table 4).

The Philippines also committed minimumaccess volumes (MAVs) of 3% of 1986 to 1988domestic consumption for 1995 and 5% for 2004.It also committed to reduce bound tariffs by 24%with minimum 10% cut per tariff line from 1995 to2004.

On the contrary, Thailand had a policy ofprotectionism in agriculture up until the WTO. Thisincluded price intervention policy with publicpurchases at above market prices, lifting of exporttax measures that had burdened farmers,provision of credit incentives and the like.

In 1994, the country had to go through a tariffreform programme, which resulted in deeper tariffcuts than required under the WTO. Following the1997 financial crisis, tariffs were further reducedin 1999 and 2000, resulting in the removal of thebias against agricultural exports caused by theerstwhile protection.18

Under the AoA, Thailand made a commitmentto reduce tariffs on 740 tariff lines by an averagereduction of 24% over the 1995-2004 period, witha minimum reduction of 10% on all tariff lines.Thailand bound tariffs on 994 agricultural products– 100% of its agricultural tariff lines. The averagebound tariff rate was calculated to decline from49 % in 1995 to the final rate of 36 % in 2004.Thailand also tariffied non-tariff measures on 23agricultural products by converting them into tariffrate quotas (TRQs) with in-quota tariff ratesranging from 20 to 65 %. It reserved the right toresort to the SSG provision for 111 products, or11% of the aforementioned 994 agricultural tarifflines.19

Thailand had more drastic tariff reform bothbefore the conclusion of the WTO Uruguay Roundand after the 1997 financial crisis, which resultedin applied tariffs being lower than the WTO boundrates for all but a few tariff lines. The average

TariffRates

10-30

35-50

55-70

75-90

95-100

1995

1

23

14

8

50

1996

1

23

14

8

50

1997

1

36

9

50

0

1998

1

36

9

50

0

1999

1

44

51

0

0

2000

1

44

5

0

0

2001

1

44

1

0

0

2002

1

44

51

0

0

2003

1

90

0

0

0

2004

1

90

0

0

0

TABLE 4. FREQUENCY DISTRIBUTION OF TARIFF RATES ONSENSITIVE AGRICULTURAL PRODUCTS, 1995-2004 (PHILIPPINES)

Source: WTO Agreement on Agriculture: The Implementation Experienceof Developing Countries, FAO Corporate Document Repository, UNCTAD

9THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Country 1980-81 1985-87 1988-90 1991-92 1993-97mean

Standarddeviation

(%)

ThailandIndonesiaMalaysiaPhilippinesChinaJapanBangladeshIndiaPakistan

26.323.0

4.3---

70.769.665.1

28.014.7

8.6---

57.590.865.5

33.414.8

7.7---

72.569.953.7

26.213.6

7.3---

73.3a

44.954.1

40.312.3

4.128.917.8

9.1---

19.419.421.2

4.518.210.7

---

TABLE 5. TARIFF RATES AND DISPERSION* OF PRIMARYPRODUCTS IN SELECTED ASIAN COUNTRIES (UNWEIGHTED)

a1993Source: UNCTAD* Dispersion is a statistical term that refers to a method of getting average butassigning weights to each product, thus, the result is not actually an averagebut an index.

applied tariff rate for agricultural products hadgradually declined from 43.1 % in 1995 to 32.1 %in 1999 and 28 % in 2000.

But despite all these, interestingly, Thailand’sapplied tariff rate is still much higher than the ratesfor agricultural imports of most other Asiancountries. (See Table 5) This is so because dueto the long history of protection, after tariffliberalisation, Thailand still has 43% of all its tarifflines exceeding 30 % tariff. The tariff peaks arefound in meat and dairy products, sugar, alcoholicbeverages, tobacco, fruits and vegetable sectors.In addition, there are still 550 products whose

applied tariffs are higher than the bound rates.In South Asia, India is an important case.

Bangladesh, on the other hand, is special since itis classified as an LDC therefore not required toreduce tariffs. India had all its agricultural importscovered with QRs for balance of payments (BOP)reasons. For this, India just had to submit ceilingbindings without upper limit as long as the tariffshad not been bound in earlier negotiations. Inaddition, there was no obligation to reduce theseceiling bindings during the AoA implementationperiod.20

India had previously bound only some of itsagricultural tariffs. These included rice, coarsegrains, dairy products and edible oils – rice anddairy products in the Geneva Protocol (1947),maize and millet in the Torquay Protocol (1951),sorghum during the Dillon Round (1962), andsoybean and rapeseed oil in the Tokyo Round(1979). For other products for which no tariffs had

been bound earlier, India submitted very highceiling bindings of 100, 150 or 300 %.

When the QRs were removed, the new boundtariff rates for dairy products were 60 %; cereals,between 70 and 80 %; apples, from 40 to 50 %;rape, colza or mustard oil, from 45 to 75 %; andpreparations for infant use, from 17.5 to 50 %. Inexchange, bound rates for some items were lowered,which included vegetables (peas), fruits (oranges,lemons, grapefruit, pears and quinces, prunes), malt,chewing gum, fruits juices (orange juice), andindustrial fatty alcohols. (See Table 6)

As a consequence, about 82% of tariff lineshave bound rates between 75 and150 % and approximately 4% havebound tariffs of 300 %. Yet, theapplied tariff rates on mostagricultural products are quite low –for a little over 89% of tariff lines, theapplied rates are either below orequal to 50 %. There are only 9.4%of the tariff lines for which the appliedrates range between 50 and 100 %.

Bangladesh, being an LDC, is notrequired to undertake commitmentswith market access. However, it isnot allowed to increase its boundtariff, which was set at a uniformceiling rate of 200 % for allagricultural goods except 13 itemsfor which bound rate is 50 %. Boundtariff rates for two agriculturalproducts, namely green and black

tea are lower than actual tariff. Still, Bangladesh,as will be shown later, cannot take advantage ofthis trade opportunity as its production remainsbackward and costly.21

In sum, Asia in general had little protection priorto the WTO, thus, got its backward agriculturesubjected to extreme competition upon AoAimplementation. Tariffs that were meant to earnprecious revenues for industrialization, let aloneagricultural development, were almost given uplong before the WTO through the neo-liberalpolicies in the IMF SAPs and several otherprogrammes by the World Bank and the AsianDevelopment Bank.

Domestic SupportSuch wholesale restructuring would also

undermine Asian governments’ capacity to supporttheir agricultural sectors. Thus, the levels ofdomestic support as measured by the Aggregate

10 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Measure of Support (AMS) for most Asiancountries are already far below the permitted AMSlevels. Thailand’s utilisation ratio is the only oneon the higher side, but the rest of the selectedcountries use minimal subsidies. (See Table 7)

Developing countries without AMS in the baseperiod committed not to introduce support in thefuture, but may use de minimis levels defined assupport up to 10% of the value of individualcommodity production. Theoretically, even

Source: UNCTAD

Section No.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

Name of product

Skimmed milk powder - in powder granular formof fat content not exceeding 1.5 percent

Skimmed milk powder - not containing addedsugar or other sweetening material

Peas

Oranges

Lemons

Grapefruit

Fresh grapes

Apples

Pear and quinces

Prunes

Spelt wheat

Maize (seed)

Maize (other)

Rice in husk (paddy or rough)

Rice - husked

Rice - semi- or wholly milled

Rice - broken

Sorghum

Millet

Malt - not roasted

Olive oil, other than virgin

Rape, colza or mustard oil, crude

Rape, colza or mustard oil, other

Chewing gum - whether or not sugar coated

Preparations for infant use

Sweet biscuits, waffles and wafers

Other potato preparations - frozen

Orange juice - frozen

Orange juice - other

Industrial fatty alcohol

Old bound rate

0

0

100

100

100

100

100

40

40

40

0

0

0

0

0

0

0

0

0

100

45

45

45

150

17.5

150

55

85

85

150

New bound rate

60

60

50

40

40

25

40

50

35

25

80

70

60

80

80

70

80

80

70

40

40

75

75

45

50

45

35

35

35

50

TABLE 6. NEW BOUND RATES OF TARIFFS FOR SELECTED AGRICULTURAL PRODUCTS (INDIA)

11THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Source: Countries marked with an asterisk appeared in the earlier FAO study, and for these countries, the dataare from 1999 or the most recent available year before that date. For other countries, the data are drawn fromthe national case studies commissioned in 2002.

Country

Bangladesh*

Botswana*

Brazil

Costa Rica

Côte d’Ivoire

Egypt

Fiji

Guyana*

Honduras

India

Indonesia

Jamaica

Kenya*

Malawi

Morocco*

Pakistan*

Peru

Philippines

Senegal

Sri Lanka*

Thailand

Uganda

Zimbabwe

Information available

None

GB only

Detailed

GB, SDT, AMS

None

GB and SDT only

None

None

Only SDT

Detailed

GB, SDT, AMS (rice only)

GB only

GB only

None

Detailed

Detailed

GB and SDT only

None

GB and SDT only

None

Detailed

GB and SDT only

GB, SDT, de minimis

Comments

PS AMS negative; NPS AMS about 1% of VoP

GB level about 3% of VoP

PS AMS in 1995 and 1996, respectively, 27% and 23% ofpermitted levels; NPS AMS de minimis, much of it consisting ofcredit subsidies

GB outlays falling; no PS AMS used so far; NPS AMS only for1998 and 1999

Very low

-

-

-

SDT outlays increased

PS AMS negative; NPS AMS about 7.5% of VoP in 1995/96 butfell to about 1% subsequently; SDT not used fully but the rightto use reserved; unofficial estimates suggest this would reduceNPS AMS to 2.3% of VoP

SDT not used; only in 2000, rice AMS

GB outlay about 2% of VoP

-

-

AMS in current years 12-33% of permitted levels

PS AMS negative; NPS AMS about 3% of VoP; PS AMScalculated for one crop in1997-98 and 11 in 1986-88

GB 5 percent of VoP; PSAMS 0 percent; NP AMS 5.0-6.2% of VoP

Very low

85% of GB/SDT on water development

-

Current AMS 60-80% of permitted levels

Minimal support provided

No PS AMS

TABLE 7. SUMMARY OF INFORMATION ON DOMESTIC SUPPORT MEASURES

developing countries without an AMS entitlementcan provide support up to 20% of the value ofproduction – 10% for non-product related supportand 10% for product-related support. As alreadymentioned, they may also exempt subsidies underthe SDT.

However, as already pointed out, developingcountries used minimal subsidies in the past thusstarted from low bases. Except for Thailand, Asian

countries pale in comparison to developedcountries when it comes to domestic support. (SeeTable 8)

Indonesia maintains a number of domesticsupports that include general services,programmes to promote agricultural development,government stockholding, administered pricesystems for some commodities, and domestic foodaid. With the exception of administered prices, most

12 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Subsidy

AMS

AMS as a percentageof agricultural GDP

Green Box subsidy

S&D subsidy

De minimis

Total subsidy

Thailand’srank among41 countries

3

7

4

3

10

4

Subsidy(US$ million)

486

(11.6%)

1 290

247

12

2 035

Countries with thelargest subsidy

(1) Republic of Korea(2) Mexico

(1) Republic of Korea(2) Trinidad(3) Venezuela

(1) Republic of Korea(2) Brazil (3) India

(1) India (2) Turkey

(1) India (2) Turkey(3) Republic of Korea

(1) India (2) Republicof Korea (3) Brazil

TABLE 8. THAILAND’S RANK AMONG DEVELOPING COUNTRIES INTERMS OF SUBSIDIES

Note: Several countries did not notify the S&D, de minimis and AMS subsidies.Source: Compiled from ABARE, “Domestic Support of Agriculture”, CurrentIssues, May 2002.

1995366

3-

32401

2 249178

1996407

4-

38450

2 342192

1997557

5-

56618

2 909212

1998622

12411265

1 31010 014

131

1999826

15426347

1 6137 855

205

20001 057

1273 055

334 2728 421

507

General servicesPayments for natural disaster reliefDomestic food aidPublic stock holding of food securityTotal in rupiahExchange rate (Rp/US$)Green Box (US$ million)

Type of measure Monetary value of measure (billion rupiah)TABLE 9. INDONESIA’S GREEN BOX MEASURES

Source: Indonesia’s Notification to the WTO on Domestic Support

of these fall either under the Green Box or underSDT, and need not be reduced. (See Table 9)

But Indonesia did not offer an AMS level, thus,cannot provide support in excess of de minimislevel to any single product. By failing to give anAMS, Indonesia is subject to greater disciplinethan countries that made such commitment eventhough those countries provide far greater levelof support.22

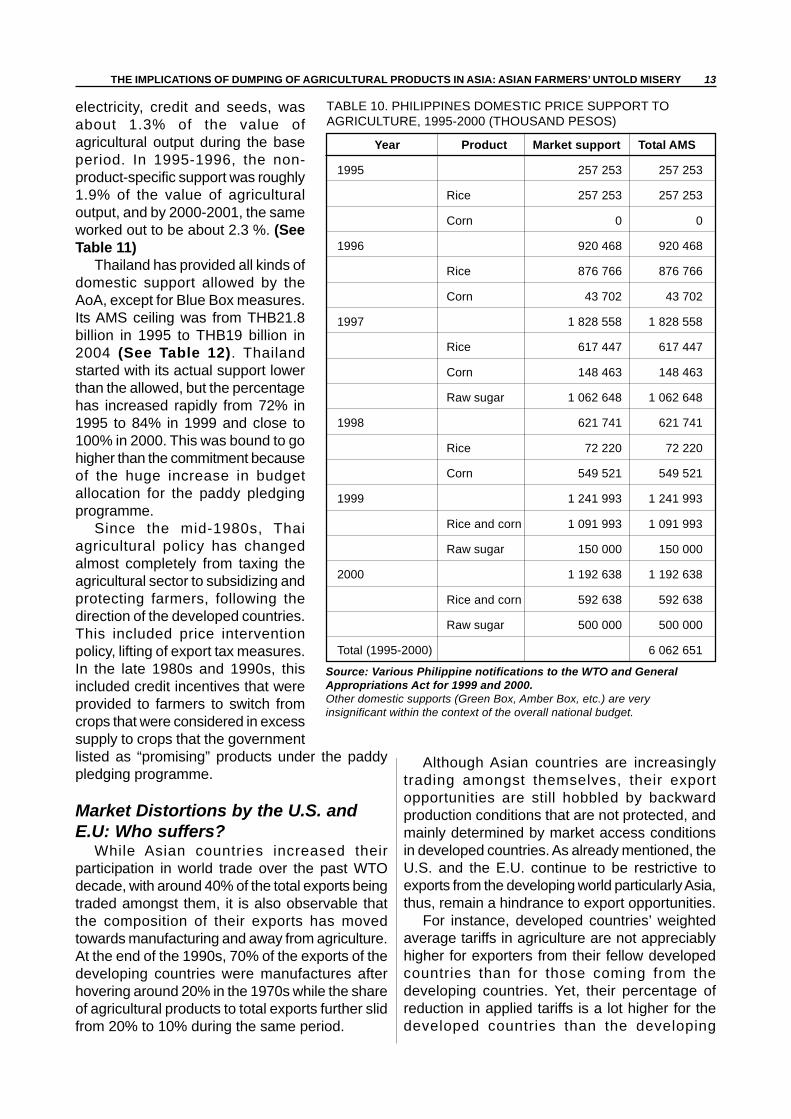

The Philippines maintained trade-distortingdomestic support such as input subsidies andprice support for rice, corn and sugar, but theseare way below the de minimis level, thus, neednot be reduced. Still, there has been a consciouseffort to phase out input subsidies in favour ofprivatised irrigation and market infrastructures.(See Table 10)

Rice price support, on the other hand, hasbecome useless if compared with farmgate prices.

From 1996 to 2000, the government support pricewas a lot higher than farm market prices.Compounding the problem is the limited publicfund and capability to procure rice, estimated atless than 4% of total production.23

India has a product price support system in theform of minimum support prices announced by thegovernment for different commodities. Based onthe computation by the Food and AgricultureOrganization, product-specific support for 18 majorcommodities during the base period amounted toUSD18.1 billion, equivalent to 26% of agriculturaloutput in the crop sector. In the first year of AoAimplementation, the estimated product-specificAMS turned out to be -34.4% of the value ofagricultural output, and by 2000-2001, the samestood at -28.6 %.24

The non-product-specific support, whichincludes subsidies on irrigation, fertilisers,

13THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

electricity, credit and seeds, wasabout 1.3% of the value ofagricultural output during the baseperiod. In 1995-1996, the non-product-specific support was roughly1.9% of the value of agriculturaloutput, and by 2000-2001, the sameworked out to be about 2.3 %. (SeeTable 11)

Thailand has provided all kinds ofdomestic support allowed by theAoA, except for Blue Box measures.Its AMS ceiling was from THB21.8billion in 1995 to THB19 billion in2004 (See Table 12). Thailandstarted with its actual support lowerthan the allowed, but the percentagehas increased rapidly from 72% in1995 to 84% in 1999 and close to100% in 2000. This was bound to gohigher than the commitment becauseof the huge increase in budgetallocation for the paddy pledgingprogramme.

Since the mid-1980s, Thaiagricultural policy has changedalmost completely from taxing theagricultural sector to subsidizing andprotecting farmers, following thedirection of the developed countries.This included price interventionpolicy, lifting of export tax measures.In the late 1980s and 1990s, thisincluded credit incentives that wereprovided to farmers to switch fromcrops that were considered in excesssupply to crops that the governmentlisted as “promising” products under the paddypledging programme.

Market Distortions by the U.S. andE.U: Who suffers?

While Asian countries increased theirparticipation in world trade over the past WTOdecade, with around 40% of the total exports beingtraded amongst them, it is also observable thatthe composition of their exports has movedtowards manufacturing and away from agriculture.At the end of the 1990s, 70% of the exports of thedeveloping countries were manufactures afterhovering around 20% in the 1970s while the shareof agricultural products to total exports further slidfrom 20% to 10% during the same period.

Source: Various Philippine notifications to the WTO and GeneralAppropriations Act for 1999 and 2000.Other domestic supports (Green Box, Amber Box, etc.) are veryinsignificant within the context of the overall national budget.

TABLE 10. PHILIPPINES DOMESTIC PRICE SUPPORT TOAGRICULTURE, 1995-2000 (THOUSAND PESOS)

Year

1995

1996

1997

1998

1999

2000

Total (1995-2000)

Product

Rice

Corn

Rice

Corn

Rice

Corn

Raw sugar

Rice

Corn

Rice and corn

Raw sugar

Rice and corn

Raw sugar

Market support

257 253

257 253

0

920 468

876 766

43 702

1 828 558

617 447

148 463

1 062 648

621 741

72 220

549 521

1 241 993

1 091 993

150 000

1 192 638

592 638

500 000

Total AMS

257 253

257 253

0

920 468

876 766

43 702

1 828 558

617 447

148 463

1 062 648

621 741

72 220

549 521

1 241 993

1 091 993

150 000

1 192 638

592 638

500 000

6 062 651

Although Asian countries are increasinglytrading amongst themselves, their exportopportunities are still hobbled by backwardproduction conditions that are not protected, andmainly determined by market access conditionsin developed countries. As already mentioned, theU.S. and the E.U. continue to be restrictive toexports from the developing world particularly Asia,thus, remain a hindrance to export opportunities.

For instance, developed countries’ weightedaverage tariffs in agriculture are not appreciablyhigher for exporters from their fellow developedcountries than for those coming from thedeveloping countries. Yet, their percentage ofreduction in applied tariffs is a lot higher for thedeveloped countries than the developing

14 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

countries. This only shows a great bias againstexports from the developing world. On the otherhand, developing countries have always beenrestrictive to the exports from their fellowdeveloping countries, but their average tariffs forboth developed and developing countries arealmost the same. (See Table 13)

According to the UNCTAD, tariff levels evenconceal the level of protection against developingcountries’ exports. Products of particular exportinterest for developing countries are also subjectto specific tariffs, tariff peaks and tariff escalationin developed country-markets.27 In the case ofspecific tariffs, the protection level increases wheninternational prices fall. In the U.S. and E.U.

including Japan, 30% of the agricultural tariff linescontain these specific tariffs. On the other hand,between 1994 and 2005, the number of tariff peakson agricultural exports of developing countries todeveloped countries more than doubled,comprising 29% of total tariff peaks in 2005. Lastly,tariff escalation is extremely applied on processedproducts and more pronounced in commoditiessuch as meat, sugar, fruit, coffee, cocoa and hidesand skins, which are of export interest to manypoor countries.28

In the area of domestic support, progress inreducing subsidies has been limited. As alreadymentioned, due to the existence of the peculiar“boxes”, there has been a shift in the developed

19951996199719981999a

20002001200220032004

21 816.4121 506.6421 196.8720 887.1020 577.3320 267.5619 957.7919 648.0219 338.2519 028.48

15 773.2512 932.4716 756.5816 402.1017 303.37

(20 846.08)b

n.a.n.a.n.a.n.a.

72.360.179.178.584.1

(100.0)(>100)c

---

33 594.3341 145.3147 595.8742 826.8235 948.93

-----

4 310.389 323.354 999.694 600.433 058.70

-----

1 051.512 893.961 902.23

529.2878.22

-----

Year Monetary value of measures exempt from thereduction commitment

Monetary value of measures committed to reduce

Bound AMSceiling

Actual AMS Actual as apercentage of

bound

Greenbox

Subsidy on input ofproduction (S&D)

Subsidy oninvestment (S&D)

(1) (2) (1)/(2)

a The figure is from preliminary data.b Estimated by the author from the Farmer Assistance Fund (THB5 189.1 billion), BAAC (THB9 872.96 billion) and BOT(THB5 784.01). The number is still an overestimate.c Available data suggest that actual support might be much larger than the committed support. The proposed budget wasB5.2 billion from BOT, B6.18 billion from FAF and THB19.96 billion from BAAC.

Source: Department of Business Economics, Ministry of Commerce

TABLE 12. MONETARY VALUE OF DISTORTING AND NON-DISTORTING MEASURES 1995-

Period

Base period (1986-87 to1988-89)

1995-96

1996-97

1997-98

1998-99

1999-2000

2000-01

Product specificsupport (US$

billion)

-18.11

-26.37

-27.67

-25.38

-27.75

-25.50

-26.00

As a percentage ofthe value of output ofthe agricultural sector

-26.10

-34.36

-32.44

-29.52

-30.13

-27.24

-28.58

Non-productspecific support

(US$ billion)

0.87

1.44

1.58

1.84

1.86

2.07

2.11

As a percentage ofthe value of output ofthe agricultural sector

1.25

1.88

1.86

2.14

2.02

2.21

2.32

Source: Computed. WTO Agreement on Agriculture: The Implementation Experience of Developing Countries, FAOCorporate Document Repository, UNCTAD

TABLE 11. DOMESTIC SUPPORT TO INDIAN AGRICULTURE

15THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Unlike other Asian countries, South Korea’sbound tariff rate on all agricultural products is64.1%, which poses a significant barrier toagricultural trade. South Korea bound 91.7%of its tariff line items.25

South Korea agreed to lower tariffs on morethan 30 agricultural products including mixedfeeds, feed corn, wheat, vegetable oils andmeals, and fruits and nuts between 1995 and2004, and has fully phased in those tariffreductions. But duties remain very high onmany high-value agricultural and fisheryproducts. South Korea imposes tariff rates of30 % or higher on most fruits and nuts, manyfresh vegetables, starches, peanuts, peanutbutter, various vegetable oils, juices, jams, beer,and some dairy products. Products of interestto U.S. suppliers, such as table grapes, beef,canned peaches, canned fruit cocktail, apples,pears, and a variety of citrus fruits are imposedtariff rates of 40% or higher. In many instances

South Korea andthe WTO

Korea applies prohibitively high tariffs despitethe absence of domestic production.26

South Korea also established TRQs meantto provide minimum access to previously closedmarkets. In-quota tariff rates are zero or verylow, but the out-quota tariff rates are prohibitive.Korea also implements QRs through its importlicensing system – it continues to restrictimportation of value-added soybean and cornproducts. Lastly, like Japan and the Philippines,South Korea also received a 10-year exceptionto tariffication of rice imports, and insteadnegotiated an MAV.

In domestic support, Korea agreed to reduceits AMS by 13% by 2004. But the South Koreangovernment substantially increased its level ofdomestic support to the cattle industry in 1997and 1998, consequently raising the overall AMSlevel. In 1999, the issue was raised by the U.S.and Australia in the WTO dispute settlementproceedings. The WTO Appellate Body ruledagainst South Korea, concluding that SouthKorea had not been computing the current levelof domestic support in a manner compatiblewith the requirements of the AoA.

countries in their domestic subsidies from directlyprice-related subsidies to direct payments and other‘indirect’ subsidies, thereby effectively increasingtheir overall level of domestic support withoutdecreasing their profit margin.

According to the OECD, the level of support toOECD countries remains high, having changedonly a little since 1995. As a share of gross farmreceipts, support given to producers fell from anaverage of 37% in 1986-1988 to only an averageof 30% in 1995-1997, and since then hasremained in the same level. In absolute terms, ithas increased from USD243 in billion in 1986-1988to USD279 billion in 2004.29

The E.U. is the bigger user of Blue Boxsubsidies than the U.S. and has substantiallyincreased its usage since 1995. On the other hand,the U.S. is the bigger Green Box user and haspractically maintained the level of subsidies underthis exemption. (See Tables 14 and 15) Yearly,on the average, the E.U. has used USD21 billionin direct payments to producers while the U.S. haspaid almost USD50 billion to so-called ruraldevelopment such as grants and loans to agri-business and rural enterprises.

The E.U. Blue Box payments represent around10% of its value of production. It increased from1995 to 2002 and may have even gone throughthe 1992 ceiling.30 The OECD calculates thesupport given each product in 1992 and comparesthis with those under the Blue Box, which gives abetter idea how subsidies have been shifted tothe Blue Box. (See Table 16) The U.S. on the otherhand had moved its subsidies from the Amber Boxto the Green Box, and Green box subsidies havedominated U.S. subsidies since 1998.

The Common Agricultural Policy (CAP) of theE.U. as well as the U.S. Farm Bill reflect thedirections of both markets towards maintainingtheir subsidies. For instance, 90% of the CAPbudget is for price-based subsidies, but this isbeing reduced to 21% in order to increase directpayments to farmers to 68% of the CAP budget.Examples of direct payments are those madesupposedly to limit production (Blue Box) and arepaid on the basis of area grown and/or a fixednumber of livestock owned, and are thusconsidered not directly linked to production. In fact,the E.U. made early revisions in the CAP, i.e.introducing direct payments in 1992, in order to

16 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

Sour

ce: U

NC

TAD

, Tra

de A

naly

sis

and

Info

rmat

ion

Syst

em (T

RA

INS)

Dat

abas

e at

the

Wor

ld In

tegr

ated

Tra

de S

olut

ion

(WIT

S).

Not

e: B

ased

on

the

near

est y

ear f

or w

hich

tarif

f dat

a ar

e av

aila

ble.

TABL

E 13

. EFF

ECTI

VELY

APP

LIED

TAR

IFFS

IN D

EVEL

OPE

D A

ND

DEV

ELO

PIN

G C

OU

NTR

IES

BY S

ELEC

TED

PR

OD

UC

T G

RO

UP,

199

4 AN

D 2

005

(PER

CEN

T)

3.80

9.87

3.02

11.5

9

3.94

9.68

8.44

13.8

6

2.13

8.60

-53.

2

-51.

5

2.0

-21.

9

-58.

5

-54.

6

-47.

2

-54.

2

-64.

0

-54.

8

-33.

7

-50.

6

-2.9

-38.

9

-36.

6

-51.

9

-27.

2

-48.

2

-44.

1

-53.

4

3.32

13.1

5

4.88

11.2

0

3.25

13.6

5

8.90

23.5

5

2.98

13.3

6

4.47

14.7

1

2.83

14.0

4

5.18

16.8

3

11.1

9

31.9

6

2.83

14.3

1

1.29

5.85

2.98

12.6

2

1.14

5.13

4.33

6.92

1.03

5.10

2.12

4.88

2.48

12.1

2

2.39

4.38

9.32

7.33

0.88

4.03

-61.

1

-55.

5

-38.

9

12.7

-64.

9

-62.

4

-51.

3

-70.

6

-65.

4

-61.

8

-52.

6

-66.

8

-12.

4

-13.

7

-53.

9

-74.

0

-16.

7

-77.

1

-68.

9

-71.

8

Deve

lopi

ngco

untri

esDe

velo

ped

coun

tries

Deve

lopi

ngco

untri

esDe

velo

ped

coun

tries

Deve

lopi

ngco

untri

esDe

velo

ped

coun

tries

Deve

lopi

ngco

untri

esDe

velo

ped

coun

tries

Deve

lopi

ngco

untri

es

2005

Perc

enta

ge c

hang

e19

9420

05Pe

rcen

tage

cha

nge

Sim

ple

Ave

rage

Wei

ghte

d A

vera

ge

Expo

rtin

g R

egio

ns

5.43

18.8

3

5.09

19.9

2

5.49

18.7

6

9.35

26.0

7

4.56

17.8

5

5.73

19.9

6

3.11

18.9

8

6.21

20.1

3

11.5

9

26.7

4

3.81

18.4

7

2.54

9.14

5.19

15.5

5

2.28

8.52

4.94

11.9

5

1.64

8.06

Deve

lope

dco

untri

esDe

velo

ping

coun

tries

Deve

lope

dco

untri

es

1994

All

prod

ucts

Dev

elop

ed c

ount

ries

Dev

elop

ing

coun

tries

Agr

icul

ture

Dev

elop

ed c

ount

ries

Dev

elop

ing

coun

tries

Man

ufac

ture

s

Dev

elop

ed c

ount

ries

Dev

elop

ing

coun

tries

L

abou

r-in

tens

ive

man

ufac

ture

s

Dev

elop

ed c

ount

ries

Dev

elop

ing

coun

tries

O

ther

man

ufac

ture

s

Dev

elop

ed c

ount

ries

Dev

elop

ing

coun

tries

17THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

TABLE 14.FIGURES AND GRAPHS OF THE DIFFERENT AGRICULTURAL SUPPORT MEASURES FOR THEEUROPEAN UNION, ICELAND, JAPAN, NORWAY, SLOVENIA, THE SLOVAK REPUBLIC AND THE UNITED STATES

Expenditures of domestic supports as classified underthe different boxes in the European Union

De minimisBlue BoxGreen BoxTotal AMS

1995825

208461877950030

1996747

215212213051009

1997544

204431816750194

1998379

205041916846683

1999308

197921993147886

Shares of domestic supports along the different boxes in the European Union

Blue BoxGreen BoxTotal AMSDe minimis

199523.020.855.3

0.9

199622.623.253.5

0.8

199722.920.356.2

0.6

199823.622.153.8

0.4

199922.522.754.5

0.4

Source: UNCTAD, Trade Analysis and Information System (TRAINS) Database at the WorldIntegrated Trade Solution (WITS).

Blue BoxGreen BoxTotal AMSDe minimisTotal

1995208461877950030

82590480.01

1996215212213051009

74795407.4

1997204431816750194

54489347.8

1998205041916846683

37986733.4

1999197921993147886

30887916.5

European Communities (million EUR)

18 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

TABLE 15. FIGURES AND GRAPHS OF THE DIFFERENT AGRICULTURAL SUPPORT MEASURES FOR THEEUROPEAN UNION, ICELAND, JAPAN, NORWAY, SLOVENIA, THE SLOVAK REPUBLIC AND THE UNITED STATES

Blue BoxGreen BoxTotal AMSDe minimisTotal

19957030

4603362141641

60918.08

19960

5181558981153

58865.86

19970

512526238

81258302

19980

4982010392

475064961.6

19990

4974916862

740574016

United States (million USD)

Expenditures of domestic supports as classified underthe different boxes in the United States

De minimisBlue BoxTotal AMSGreen Box

1995164170306214

46033

19961153

05898

51815

1997812

06238

51252

19984750

01039249820

19997405

01686249749

Shares of domestic supports along the different boxes in the United States

Blue BoxGreen BoxTotal AMSDe minimisTotal

199511.575.610.2

2.7100

19960.0

88.010.0

2.0100

19970.0

87.910.7

1.4100

19980.0

76.716.0

7.3100

19990.0

67.222.810.0100

Source: UNCTAD, Trade Analysis and Information System (TRAINS) Database atthe World Integrated Trade Solution (WITS).

19THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

compensate for cuts in market price supports orsimply to continue supporting a sector.31

The U.S. on the other hand succeeded inincluding its Farm Bill counter-cyclical paymentsin the Blue Box, i.e. subsidies that are expandingwhen world prices fall and vice versa. Thesepayments are provided in 8 sectors, all consideredsensitive crops in the developing countries –cotton, wheat, corn, soybeans, rice, barley, oatsand sorghum- and given to producers based onfixed areas and yields in reference to pastproduction. These cover around USD9-10 billiona year of the Farm Bill budget.32

In the end, with the CAP, agriculture is still thesingle biggest expenditure of the E.U. despitepronouncements of declining price supports. Thelevel of support to producers has even reachedhistoric highs. Meanwhile, with the Farm Bill, theU.S. has increased support spending by 63 %.33

The Farm Bill now includes over USD135 billionin new subsidies over the next 10 years. It isestimated that the rice farmers in the U.S. receiveUSD75,000 per household from the governmentin the form of direct payments.34

On the other hand, from 1995 to 2000, onaverage USD6.2 billion was spent annually onexport subsidies, reaching USD11 billion in 2000for 25 subsidising countries. The E.U. accountedfor almost 90%.

Almost 35% of export subsidies are for dairyproducts and 23% for meat. Beef makes up almost60% of meat subsidies and producers of cerealsand sugar also receive a considerable amount.

Some countries pay export subsidies in orderto dispose of their surplus agricultural productionon world markets – a surplus production that isstimulated by domestic supports and high importtariffs. The E.U. is by far the largest provider of

these export subsidies. Meanwhile, the use ofexport credits, or loans provided to effectagricultural exportation, has been expanding inrecent years. In this connection, the U.S. is thelargest provider.35

Overall, according to the U.S. Department ofAgriculture, market distortions in agriculture are52% caused by tariffs, 13% by export subsidiesand 31% by domestic support. Whether or notsuch summary is accurate, one thing is clear: suchdistortions have had grave impact on Asianagriculture.

The primary outcome of market distortions hasbeen the practice of dumping. Subsidies and hightariff walls have resulted in artificially high farmproduction levels that allow producers to dumptheir surplus in other countries at less than theproduction cost. This has been made even morepossible in the ‘subsidy-shifting’ pulled off by theU.S. and the E.U.

Shifting subsidies from the Amber Box to theBlue Box and Green Box in reality does not lowerthe profit margin of the producer. In fact, it evenallows the producer to have artificially highproduction levels that in turn are so trade distortivethat they could send weaker agricultures into atailspin. Martin Khor of Third World Networkexplained this clearly.

According to Khor, it is not so important for theproducer whether he gets revenue over and abovehis production cost and makes a profit from ahigher price presumably brought about by pricesupport measures or from direct payments. Whatis important for him is to obtain the revenue andprofit, period. Whatever form of subsidy that helpshim make revenue and maintain or increaseprofitability is significant to his production andmarket.

TABLE 16. SUBSIDIES BY COMMODITIES IN 1992 AND FROM 1995 TO 1999 IN THE E.U. (MILLIONS IN EUR)

WheatCoarse grainsCereals Rice Oilseeds Beef and veal SheepmeatTotal

PSE in 199269817940

14921421

299514997

412437458

PSE less OS in 199260186844

12862363

258212927

355532289

1995

12672

238138761321

20486

1996

12910

243933221007

21521

1997

1182240

236930811171

20443

1998

1163781

226429901536

20504

1999

11696124

131829301734

19792

Blue Box payments

Source: UNCTAD

PSE - Producer Support EquivalentOS - Other Support

20 THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

the intervention price. Secondly, this has been madepossible through high tariff barriers imposed on sugarexporters to the E.U. particularly former E.U. colonieswho have the preferential sugar quotas. Lastly, highinternal prices are maintained by exporting thesurplus production of sugar with some form ofsubsidy. Export refunds total around 1.5 billion EUR(the difference between the internal and globalprices), which allows inefficient farms to sell at pricesbelow the internal price and cost of production. Likewith wheat, it is the big farmers, sugar beetprocessing companies and companies getting theexport refunds that benefit from protectionism.37

On the other hand, the U.S. guarantees sugarprices, restricts imports with a quota ceiling of 1.1million tons divided amongst 40 countries and witha tariff on imports above the quota at a little below100 %. This regime affords refiners and growersUSD2 billion a year in higher prices at the expenseof the sugar users.38

Meanwhile, in a study conducted by theInstitute for Agriculture and Trade Policy (IATP), ithas been revealed that the U.S.-based global foodcompanies continue rampant dumping. In 2003,these companies sold super below the cost ofproduction: wheat at an average price of 28%below production cost; soybeans at 10%; corn,10%; and rice, 26%. This has been made possiblethrough the U.S. Farm Bill, which at the behest ofagribusiness, abandoned interventionmechanisms and sent agricultural prices into afreefall. To arrest the downfall of U.S. agriculture,Congress introduced “counter-cyclical payments”.

Before deregulation, the U.S. market had onestructural flaw: there were millions of producersand only few commodity buyers and processors.Intervention therefore set a floor price thatcommodity buyers had to pay farmers. Under theFarm Bill, farms have become expensive butcontradictions between farmers and commoditybuyers and processors have intensified.

More significantly, the U.S. Farm Billinstitutionalised dumping on world markets.Dumping of wheat increased from 27% annuallyin 1990-1996 to 37% per year post-1996; soybeanfrom 2% to 11.8%; maize from an annual averageof 6.8% to 19.2%; cotton, 29.4% to 48.4%; andrice from 13.5 to 19.2 %. Clearly, it is the largestcommodity traders, such as Archer DanielsMidland, Cargill and Bunge Ltd. that dominatefinancing trades, processing and shipping thatbenefit immensely from dumping. They arevertically integrated, buy cheaply and control thevalue-added stages of production.39

Under the Amber Box (price support):

1.The farmer receives a price support.2.Domestic price is pulled up a lot higherthan the world price because of pricesupport.3.This allows the farmer’s revenue to beover production cost, thus resulting in profit.4.Farm is viable even if production cost ishigher than world price.5.If bulk of production is exported, which isusually the case; this is made possiblethrough an export subsidy equal to the worldprice.

Under the Blue Box and Green Box (directpayments):

1.Domestic price is the same or even lowerthan the world price.2.The farmer gets a price that is lower thanthe production cost.3.But then, he receives a high subsidy asdirect payment.4.He thus gets the same revenue and profitas the farmer under the Amber Box.5.Farm remains viable even if it is alreadyinefficient.6.The direct payment allows the farmer tosell at price below the world price and exportat a competitive price that is artificially lowbecause of the subsidy. In effect the farmerdoes not even need an export subsidyanymore in order to sell abroad.

The U.S. is a heavy dumper of wheat,soybeans, maize, cotton and rice while the E.U.dumps sugar, beef and together with the U.K.,wheat. The consequences would be obvious sincethese are agricultural and food products that Asiancountries produce sufficiently for domesticconsumption or export to earn revenues.

In the study done by the Action Aid, it has beenrevealed that in 2000 and 2001 the average worldprice of wheat was only 73 GBP per ton but U.K.’saverage cost of production was about 113-124 GBPand the U.K. price was 70-78 GBP. Thus wheatsold in the global market was about 35-40% belowproduction cost. The biggest 28% of U.K. arablefarms got 78% of the direct payments, with thelargest farms and richest people getting the bulk.36

E.U. sugar prices, on the other hand, aremaintained through three complementarymechanisms: intervention price, import tariffs andexport refunds. Since 1981, however, the E.U. hasnot used the intervention price much since E.U.internal sugar prices have always been higher than

21THE IMPLICATIONS OF DUMPING OF AGRICULTURAL PRODUCTS IN ASIA: ASIAN FARMERS’ UNTOLD MISERY

The Myriad of CatastrophesMarket distortions have had disastrous

consequences on the domestic production andexport opportunities of developing countries. Thesmall-scale farmers who make up around 80% ofthe producers in Asia for instance suffer the impactof dumping the most. They suffer in two ways:shrinking production levels and lost exportopportunities – both result in untold misery not onlyfor the peasantry but also for the general public.

To illustrate, Indonesia is not a wheat producingcountry. But since the Indonesian government hasa long-term policy to veer away from the country’sheavy reliance on rice, it has encouraged theconsumption of wheat-based foods such as noodles,bread, etc. Since the 1970s, Indonesia has importedan increasing quantity of wheat flour and nationalcompanies have increased wheat processing. Withthe increasing demand coupled with tradeliberalisation, wheat imports leapt from 40,000 tonsin 1998-1999 to 220,000 tons in 1999-2000.40

This has sent local rice producers and smalland medium-scale domestic wheat millers tobankruptcy. Cheap wheat imports are depressingdomestic prices and marginalizing rice farmers.In 1999, for instance, imported flour was onlyUSD220 per ton as compared with the local priceof USD280 per ton. The Indonesian Anti-DumpingCommittee (KADI) found Australia, the E.U. andthe United Arab Emirates guilty of dumping andlinked this with the displacement of local flour. Butbusiness lobbied the Indonesian government notto increase duties.41

On the other hand, the price of Indonesiandomestic sugar has always been higher than theworld price. The Indonesian governmentattempted to control this with BULOG’s monopolyover sugar and other important food commodities.But this came to an end in 1998 following the IMFagreement related to the Asian financial crashwherein the IMF required liberalisation of sugarimports and deregulation of sugar production.Although sugar was exempted from zero tariffunder the AoA, the IMF agreement imposed zerotariffs and 48% market access up to 2001. Sugarimports increased from 975,000 tons in 1996 to1.95 million in 1999 and eventually imported sugaraccounted for 60% of national consumption.

The traders such as the distributors andretailers, mostly foreign, have gained immenselyfrom import liberalisation since through monopolypricing they can import sugar cheaply and sellexpensively in the local market. Smuggling andhoarding of sugar stock have also become

rampant due to this traders’ regime. This has putthe farmers and sugar factories to thedisadvantage, recently prompting the Indonesiangovernment to reinstate BULOG’s role in sugarimportation. Unfortunately, however, withoutnotice, BULOG assigned Cargill to do the task.42

Philippine meat importation, on the other hand,has dramatically increased under the AoA, withbeef imports growing three times faster thandomestic production. In 2000, beef importsaccounted for 19% of total supply.

The landed costs of meat imports are a lot lowerthan the price of domestically produced meat.Because of high production and marketing costson one hand and depressed farmgate prices onthe other hand, productivity and profitability oflivestock and poultry raising in the Philippines ismarginal – 56 centavos (10 cents) per kilo forswine, PHP14.02 (27 cents) per kilo for chicken,and PHP 1,590 per head for cattle raised in sixmonths or roughly PHP 53 (USD1) per day. In themain, raisers’ productivity and profitability isdictated by the traders-integrators who monopoliseinputs and trade. With the influx of cheap importedmeat, the traders bid even lower than usual andpit one province against another to get the lowestprice per kilo liveweight, making local productionpractically pointless.43

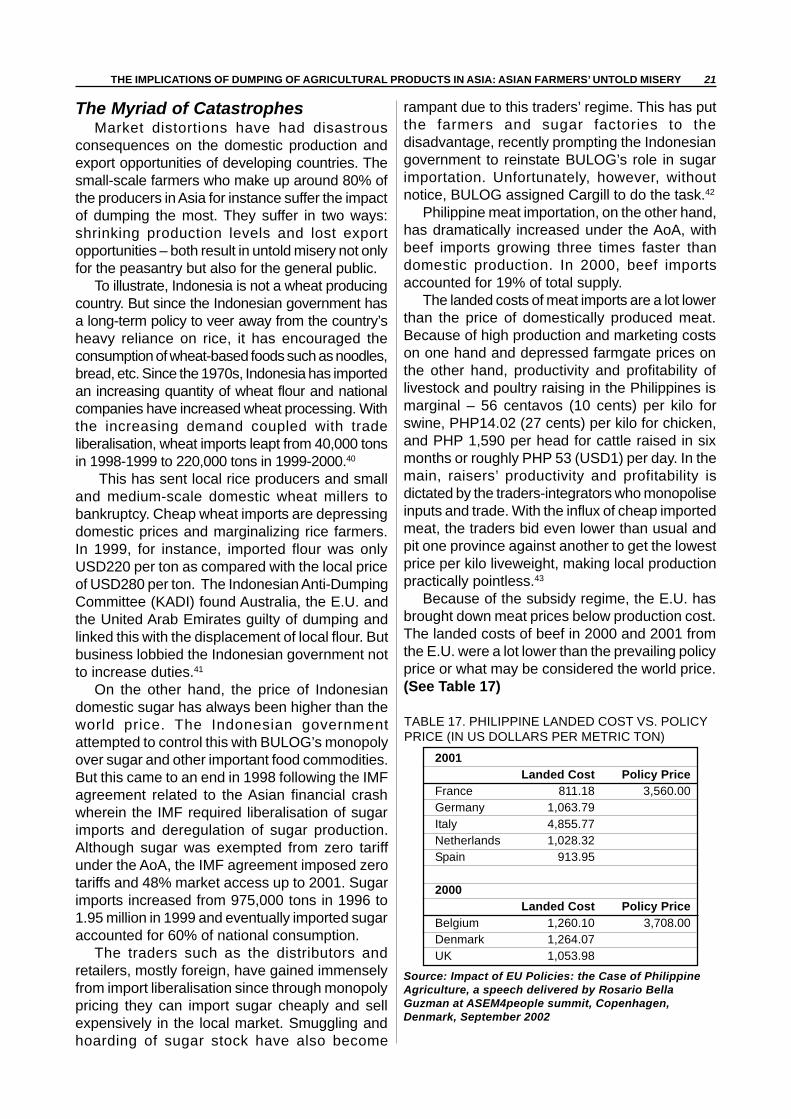

Because of the subsidy regime, the E.U. hasbrought down meat prices below production cost.The landed costs of beef in 2000 and 2001 fromthe E.U. were a lot lower than the prevailing policyprice or what may be considered the world price.(See Table 17)

TABLE 17. PHILIPPINE LANDED COST VS. POLICYPRICE (IN US DOLLARS PER METRIC TON)

2001

FranceGermanyItalyNetherlandsSpain

2000

BelgiumDenmarkUK

Landed Cost811.18

1,063.79 4,855.77 1,028.32 913.95

Landed Cost 1,260.10 1,264.07 1,053.98

Policy Price3,560.00

Policy Price 3,708.00

Source: Impact of EU Policies: the Case of PhilippineAgriculture, a speech delivered by Rosario BellaGuzman at ASEM4people summit, Copenhagen,Denmark, September 2002