the impact of firm strategies on stock market value in the biotechnology industry

TRANSCRIPT

This article was downloaded by: [The Aga Khan University]On: 10 October 2014, At: 21:36Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House,37-41 Mortimer Street, London W1T 3JH, UK

Applied Financial EconomicsPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/rafe20

The impact of firm strategies on stock market value inthe biotechnology industryNoah Patrick Stefanec aa Department of Economics , Miami University , 114 University Hall, Hamilton, OH 45056,USAPublished online: 17 Nov 2010.

To cite this article: Noah Patrick Stefanec (2011) The impact of firm strategies on stock market value in the biotechnologyindustry, Applied Financial Economics, 21:5, 343-352, DOI: 10.1080/09603107.2010.530214

To link to this article: http://dx.doi.org/10.1080/09603107.2010.530214

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) containedin the publications on our platform. However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of theContent. Any opinions and views expressed in this publication are the opinions and views of the authors, andare not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon andshould be independently verified with primary sources of information. Taylor and Francis shall not be liable forany losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoeveror howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use ofthe Content.

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Applied Financial Economics, 2011, 21, 343–352

The impact of firm strategies on

stock market value in the

biotechnology industry

Noah Patrick Stefanec

Department of Economics, Miami University, 114 University Hall,

Hamilton, OH 45056, USA

E-mail: [email protected]; [email protected]

To what degree do stock holders extend or withhold external finance to or

from publicly traded biotech firms and why? To address this question, two

firms are considered here; the results suggest that the most significant

events favourably altering investor valuation of firms in the diagnostic

segment of the biotechnology market are those which are distributional

and knowledge-gathering in nature. Buyouts of firms in the therapeutic

segment of the biotechnology market play a large role in the extraction of

external finance, particularly because the purchasing of another firms’

previous labours can significantly lower the costs of bringing new products

to market.

I. Introduction

Biotechnology firms employ living organisms orderivatives thereof to develop products for both

medical and nonmedical markets. Medical-marketbiotechnology firms in the US are the focus of these

two particular case studies. These typically small,research-intensive firms are classified as either diag-nostic or therapeutic in their area of specialization;

the former develops the technology to noninvasivelydetect the risk of disease and the contamination of

cells by foreign agents while the latter innovatesspecialty pharmaceuticals and gene therapy drugsspecifically designed to target Acquired

Immunodeficiency Syndrome (AIDS), Parkinson’sdisease and various forms of cancer (Paugh andLaFrance, 1997).

This industry is especially pertinent to academic

examination because the stock of knowledge capital isgrowing so rapidly that it carries with it the enormous

potential of enhancing the overall standard of livingby improving the health, welfare and future produc-tivity of our society. While most researchers find case

studies to be uninformative due to generalizationproblems, most would concede that isolating the

tactics required for the extraction of external financeis principally important, chiefly because the key togrowth in the biotech industry lies in a (publiclytraded) firm’s ability to secure capital.

Biotechnology firms rely heavily on outside invest-ment because they produce few profitable products

relative to the large costs associated with the research,development and testing of new ideas. Economicallyspeaking, the advances, successes and failuresendured within the biotech industry are reflective ofthe various strategies each firm employs, thus making

the reaction of stock holders to informational eventscritical to the success of the industry. This analysisaims to estimate the impact of specific ‘focus strat-egies’ on the stock market value of biotechnology

firms using event study methodology, and provide thejustification for why rational investors formulate theobserved choices.

Event studies are most commonly employed tomeasure the effects of new information (i.e. aneconomic event) on firm value. Under the basic

Applied Financial Economics ISSN 0960–3107 print/ISSN 1466–4305 online � 2011 Taylor & Francis 343http://www.informaworld.com

DOI: 10.1080/09603107.2010.530214

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

assumption of rational traders, new information isexpected to reach the market rather quickly and alteran individual’s appraisal of a particular firm (Muth,1961). Two medical-market biotechnology firms areanalysed in this case study. These firms areCambridge Heart and Triangle Pharmaceuticals,Inc.: the former, riskier, and more speculative firmfocuses on the diagnostic applications of biotechnol-ogy while the latter, a more stable firm focuses on thetherapeutic aspects of biotechnology. While neitherfirm is archetypal within the industry, these firmswere randomly selected in an attempt to minimizegeneralization problems associated with selectionbias, although this is not always possible with anycase study. Details regarding these firms, descriptionsand sources of the data can be found in ‘Data’ and‘Firm descriptions’ of Section II.

In this examination, nine possible firm strategiesare assumed to be causal mechanisms which affectfirm valuation: Acquisition or signalling of knowl-edge capital, strategic alliance formations (specificallythose affecting Research and Development; R&D),patent acquisitions, the regulatory influence of theFood and Drug Administration (FDA), tacticaldistributional alliances, personnel alterations, acqui-sitions, buyouts and financial announcements. Pastresearch regarding the existing and newly proposedstrategies and inclusion criteria can be found in‘Details of strategies’ of Section II.

An attempt to distinguish various firm strategieswas attempted here for two purposes: isolation andidentification of the marginal effects individual eventsengender on the market value of a biotech firm(Abnormal Returns (AR)) as well being able todiscern the overall effect each group of strategiesengenders on the market value of a biotech firm(Cumulative Abnormal Returns (CAR)).Econometric details expanding on this procedureare presented in Section III.

Results are accessible in Section IV. A few exam-ples of events which incited AR in the financialmarket include the publication of record third quarterrevenue by Cambridge Heart, the declaration thatMedicare will be picking up coverage for a specificCambridge Heart product (the Microvolt T-WaveAlternans test) and the replacement of TrianglePharmaceuticals, Inc.’s CEO. In a more aggregatesense, estimates of CAR demonstrate that tacticaldistributional alliances and knowledge acquisitionmost appreciated the value of Cambridge Heart(producing a CAR of 2.50 and 0.879, respectively).This result is consistent with the idea that extractionof external finance is an increasing function of ariskier firm’s perceived favourable strategies. News ofTriangle’s acquisition by Gilead Sciences, Inc. in 2003

generated a CAR of (roughly) 0.320 and thus withrespect to the therapeutic segment of the biotechnol-ogy market, buyouts of firms in the this segment ofthe biotechnology market play a large role in theextraction of external finance, particularly becausethe purchasing of another firms’ previous labours cansignificantly lower the costs of bringing new productsto market.

II. Data, Firm Descriptions and Details ofStrategies

The Institute for Biotechnology Information (IBI)reports that (roughly) 30% of all biotechnologycompanies are publicly-traded, yet relatively little isknown about the exact degree to which investorsevaluate various types of firm strategies and thedegree to which their reaction affects the marketplacevaluation of a biotech firm. That is, how muchemphasis do stock holders place on various informa-tional events with respect to their decision to extendor withhold external finance, and why? To investi-gate these questions, event studies are conducted ontwo USA medical-market biotechnology firms:Cambridge Heart and Triangle Pharmaceuticals,Inc., both of which are publicly traded companieswhich operate competitively in different segments ofthe market.

Data

Information regarding events and daily adjustedclosing prices can be easily gathered from a varietyof sources. With respect to Cambridge Heart, strat-egies and their respective announcement dates weretaken from press releases reported on the firm’swebsite and supplemented by press releases congre-gated from Lexus-Nexus. With respect to TrianglePharmaceuticals, Inc., all press releases were obtainedfrom Lexus-Nexus. Data on daily adjusted closingprices for firms as well as the Standard and Poor’s500 Index (S&P 500) were collected from Yahoo!Financial and the Wharton Research Data Service(WRDS).

Summary statistics regarding these firms are pre-sented in Table 1. A larger number of observationsand events survive for Cambridge Heart due to thelonger time frame from which it is analysed. Theauthor does acknowledge the possibility of general-ization problems resulting from selection bias.Selection of firms from both segments of the marketattempts to limit this bias, but the listing of the

344 N. P. Stefanec

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

various firms does suggest the presence of someselection bias, implying a trade-off here.

For instance, firms traded on the Over the CounterBulletin Board (OTC BB) market typically do notmeet the requirements to be listed on the NationalAssociation of Securities Dealers AutomatedQuotation System (NASDAQ) market, mostly dueto their weaker balance sheets and lower stock prices.OTC BB stocks are typically considered riskier andmore speculative, and it is also unusual for one ofthese companies to strengthen their balance sheet andmeet the requirements to be listed on the NASDAQ.Using this guideline as a proxy, it is a reasonableclaim that Cambridge Heart is a riskier investmentthan Triangle Pharmaceuticals, Inc.

Upon investigation of Table 1, it is clear that bothfirms have similar average daily returns as well aslarger average daily returns and a higher varianceof returns relative to the S&P 500, suggesting thisselection concern is minimized, possibly becausearbitrage makes any market price equivalent.Descriptions of these firms and their respectivemission statements were taken from each firm’srespective website and followed directly.

Firm descriptions

In general, these firms were chosen specificallybecause they are not archetypes in their respectiveindustries, as this would no doubt exaggerate anyselection bias. Based out of Massachusetts,Cambridge Heart is a ‘ . . . healthcare company

engaged in the research, development and commer-

cialization of products for the non-invasive diagnosis

of cardiac disease which addresses a key problem in

cardiac diagnosis-the identification of those at risk of

sudden cardiac death . . .which accounts for approx-

imately one third of all cardiac deaths, or over

400 000 deaths, in the United States each year . . . ’

(www.cambridgeheart.com). The company went

public in August of 1996, is currently listed on the

OTC BB market, and significantly underperformed

relative to the S&P 500 Index over the considered

time period (i.e. from the Initial Public Offering (IPO)

date through 20 November 2006).Triangle Pharmaceuticals, Inc., formerly based out

of North Carolina, is a ‘ . . . specialty pharmaceutical

company engaged in the development of new anti-

viral drug candidates, with a particular focus on

therapies for the human immunodeficiency virus

(HIV) and the hepatitis B virus. Triangle’s proprie-

tary drug candidates under development for HIV

and/or hepatitis B include Coviracil� (emtricitabine),

amdoxovir (formerly DAPD) and clevudine (for-

merly L-FMAU) . . . ’ (www.gilead.com). In late 2003,

when significantly underperforming relative to the

S&P 500 Index, Triangle Pharmaceuticals, Inc. was

acquired by Gilead Sciences, Inc.1 Prior to acquisi-

tion, public ownership of Triangle Pharmaceuticals,

Inc. was traded on the NASDAQ index. Observations

encompass the time period from the IPO date

(1 November 1996) through the buyout which

occurred in January of 2003.

Table 1. Summary statistics

CambridgeHeart

TrianglePharmaceuticals, Inc.

Observations 2581 1564Year founded 1990 1995Country/state USA/MA USA/NCIPO date 2 August 1996 1 November 1996Last observation 20 November 2006 23 January 2003Number of events 110 69Average adjusted close 3.68 11.50Average daily returns 0.002 0.001SD of returns 0.068 0.059Average daily returns (S&P 500 Index) 0.0004 0.0002SD of returns (S&P 500 Index) 0.011 0.013

Sources: Yahoo! Financial (Cambridge Heart), WRDS (Triangle Pharmaceuticals).Notes: Both firms are in the USA medical-market biotechnology industry. Cambridge Heart(CAMH.OB) is currently traded on the OTC BB market. Triangle Pharmaceuticals(NASDAQ: VIRS) was acquired by Gilead Sciences, Inc. in 2003.

1Gilead Science, Inc. employs ‘combinatorial chemistry’, in which scientists synthesize large amounts of molecules quicklyand isolate the most active compounds for treating a particular ailment (Paugh and LaFrance, 1997).

Impact of firm strategies on stock market value 345

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

Details of strategies

While most studies focus directly upon a singlestrategy, this piece differentiates between nine strat-egies which can be employed by biotech firms toextract external financing. Few other papers conductcase studies which discriminate strategies in a similarfashion. For instance, a recent study of e-commercefirms (e.g. Amazon.com, BarnesandNoble.com) dif-ferentiated firm strategies into alliance formation,offline expansion, pricing, product line expansion andservice improvement (Filson, 2004).2

Both firms are assumed to employ the same generalstrategies, which are grouped here into nine catego-ries. The first category is the acquisition or signallingof knowledge capital. This category includes (forexample) the hiring of new scientists and researchers,press releases of new breakthroughs by staff scientistsand independent confirmation of staff results viapublication in peer-reviewed journal articles. Theliterature also suggests that world-class scientists areoften drawn to the more successful, high-return, yethigh-stakes firms; it has also been shown that forfirms with two SDs more knowledge capital arevalued 10–50% more than other firms, ceteris paribus(Darby et al., 2004). Thus, stock market value isexpected to vary positively with knowledge-capitalintensity.

Biotech firms are the most research intensive in allof civilian manufacturing (Paugh and LaFrance,1997). Thus, the second category is strategic allianceformations, such as cooperative marketing agree-ments and more importantly, knowledge-sharingprograms with other firms (i.e. technological alliancesregarding R&D). Conventional wisdom backed byempirical evidence suggests that a firm which spendslarger sums of money on R&D will experience agreater likelihood of producing a profitable product,especially because previous research suggests thatinnovative knowledge is priced by rational investorsfor the reason that they expect a future return oncethe product materializes in the market (Rzakhanov,2004).3

The benefits of achieving synergy through thesharing of common resources have also been well-documented, but note that not all types of alliancesgenerate the same returns because the size and scopeof the firm is taken into consideration by investors.For instance, Das et al. (1998) find that smaller firmsare expected by the market to experience the greatest

benefits of strategic synergy, and their research

reveals that technological alliances generate greater

AR than marketing alliances. Baum et al. (2000)

argue the former effect is due to the disproportion-

ately larger benefits smaller firms enjoy from newlycreated long-term relationships with buyers and

suppliers.Other important insights into technological alli-

ances have been investigated in the past; for example,

Aghion and Tirole (1994) argue that coalitions

between smaller, more innovative (yet fund-lacking)R&D firms are often forced to align themselves with

larger corporations, leading to an unenforceable

contract issue with respect to the outcomes of the

R&D. In other words, they suggest that the proper

allocation of contractually unenforceable ‘controlrights’ should be allocated as to maximize the total

value of the joint output. In addition, Lerner and

Merges (1998) find that the financial condition of the

research firm has a more profound effect on the

allocation of control rights rather than the communal

concern regarding the maximization of joint output.Put differently, they find that the control rights

allocated to the research firm is an increasing

function of their financial resources.Shifting focus to the regulatory environment, it is

clear that government intervention functions in the

biotechnology industry across a multitude of dimen-sions. Accordingly, the third category is the consid-

eration of patents. Prior work has identified the

importance of intangible assets, innovative output

and patent scope on firm value (Austin, 1993; Lerner,

1994). Patents are expected to facilitate R&D, aid inproduct commercialization and perhaps most impor-

tantly, secure property rights. This responsibility

generally falls to the Patent and Trademark Office

(PTO) of the Department of Commerce, which

typically grants intellectual property rights to a firm

for a 20-year term from the date of filing. Finally, ithas also been shown the foreign investment into

biotech firms is an increasing function of a firm’s level

of patent activity (Shan and Song, 1997).In addition to allocating property rights, govern-

ment regulation functions across another dimension

with regard to the success of biotechnology firms.Hence, the fourth category considered is the involve-

ment of the FDA. Typically, long periods of time

elapse from the initial development and testing of a

product to the stage where the product can be sold for

2 Examples of event studies which do not discriminate strategies in a similar fashion include Chauvin and Hirschey (1993),Sundaram et al. (1996) and Chan et al. (1997).3 From a historical perspective, Galambos and Sturchio (1998) trace the development of strategic alliances during thetwentieth century with a particular focus on the newest shift to molecular genetics and recombinant Deoxyribonucleic Acid(DNA) technology which began in the early 1970s.

346 N. P. Stefanec

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

profit in the marketplace. Case in point, biotechnol-ogy firms must first employ animal testing (Phase I)before they can proceed to human testing. Humantesting initially begins on smaller samples (Phase II)before proceeding to larger samples (Phase III). TheFDA must approve each stage of development andthus their intervention is crucial to the (potential)future returns of any given product. Thus, informa-tion reaching a rational trader with regard to aregulatory FDA setback should result in a decision towithhold external finance (and vice versa).

The fifth category under consideration is distribu-tional strategies, such as tactical alliances, the peti-tioning of insurance companies for expanded coverageof forthcoming products, licensing agreements andproduct line expansions. Tactical distributionalarrangements in the biotechnology industry are dif-ferent from those in other industries because theylargely depend on government and third-party inter-vention, such as FDA approvals of such alliances andinsurance coverage decisions. Generally, any strategydesigned to increase the availability of a potential orcurrently existing product is included in this category.

The sixth strategic event expected to generate AR inthe financial market is personnel changes and leader-ship alterations. This can include the replacement ofthe Board of Directors (BOD), the hiring of a newmanagement staff or the appointment of a new CEO.The seventh and eighth categories, respectively, areacquisitions and buyouts, both of which can signifi-cantly alter a rational investor’s appraisal of a firm inalmost any market. Particularly, note that it is notuncommon for larger biotechnology firms to invest inand/or outright acquire smaller firms which focus onthe early stages of specialized research because buy-outs of smaller firms allow for lower cost commer-cialization of new drugs. The final category consists ofbasic financial announcements, such as quarterly fiscalreports. Before proceeding to the results, the econo-metric procedure is outlined in the following section.4

III. Econometric Details

In general, two canonical procedures exist for calcu-lating AR. Both abnormal and CAR in this analysis

are relative to the S&P 500 Index. The basic under-

lying assumption is that of rational traders; thus,

stock prices are affected by new information (i.e.

events) in a short period of time.5

Following MacKinlay (1997), the first method is to

estimate a simple Capital Asset Pricing Model

(CAPM) such as

Rit ¼ �þ �Rmt þ "it ð1Þ

where the dependent variable Rit is firm i’s stock

market return on day t, Rmt is the market returns for

the S&P 500 Index on day t and "it is the firm i’s error

in period t, which is distributed Nð0, �2i Þ. � and � are

the estimated coefficients of the market model, which

are consistent under general conditions and efficient

under normality.Once the Ordinary Least Squares (OLS) estimates

of these coefficients (defined as �̂ and �̂) are obtained,the goal of the analysis is to then isolate and

statistically test idiosyncratic eit’s, which are defined

as AR (i.e. those which cannot be explained by

normal market fluctuations). AR are given by

ARit ¼ Rit � EðRit jXtÞ ð2Þ

where ARit is the abnormal return on security i at

time t, Rit is the actual return on security i at time t

and EðRit jXtÞ is the normal return given information

Xt. The latter term is essentially the expected return

without conditioning upon the event taking place.

Under the null hypothesis, the event has no effect on

stock prices. Denote L1 ¼ T1 � T0 as the length of

the estimation window, L2 ¼ T2 � T1 as the length of

the event window and � ¼ 0 as the event date. It is

assumed that AR, which are fundamentally forecast

errors, are jointly normally distributed such that

ARit � Nð0, �2ðARitÞÞ. The SE of AR (in practice) is

given by

�2ðARitÞ ¼ �̂2i 1þ

1

L1þ

Rmt � �̂mð Þ2

L1�̂2m

" #ð3Þ

where �̂m ¼1L1

PL1Rmt, �̂

2m ¼

1L1

PL1

Rmt � �̂mð Þ2 and

�̂2i ¼1

L1�2

PL1

�Rit � �̂� �̂Rmt

�2.

4An effort was made through inductive reasoning to discover a possible tenth strategy but was unsuccessful. The author doesrecommend that future case studies look for large movements in the stock prices of the firms being evaluated on days when themarket itself remains rather stable in an effort to expand the number of strategies which cannot be explained via the nine listedhere.5 Because approximately 70% of biotech firms are privately held, this suggests the existence of informational asymmetriesbetween publicly traded firms and privately held firms. An important consequence of this insight is that it impliesinformational events (strategies) only reflect public knowledge. Furthermore, it needs to be emphasized that the stock holdersare evaluating the importance of events, not necessarily the firms themselves.

Impact of firm strategies on stock market value 347

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

CARs are then simply defined as the sum of the ARon security i over T1 � t1 � t2 � T2 where

CARiðt1, t2Þ ¼Xt2t¼t1

ARit ð4Þ

Alternatively, following Filson (2004), the esti-mated effects of individual events on daily returns canbe estimated using a more parsimonious approachsuch as estimating the model

Rit ¼ �þ �Rmt þXJj¼1

�jdj þ "t ð5Þ

where the dependent variable Rit is firm i’s stockmarket return on day t, Rmt is the market returns forthe S&P 500 Index on day t and "t is the error inperiod t; �, � and � are the estimated coefficients(OLS estimates of these coefficients are given by �̂, �̂and �̂). J is the total number of events for eachcompany, and dj takes on unity during event j’s eventwindow [�2, 1] and zero otherwise. The event windowis typically chosen to be larger than the specific eventdate to allow for leaks/anticipations of announce-ments as well as lags in the reaction time of themarket (this particular case confines itself to 2-dayleaks and 1-day lags, the adjustment of which did notalter the results robustly). CARs are then calculatedby multiplying �j by the length of the event window.

The foremost advantage of the second approach isthat it avoids double-counting AR when there areoverlapping events in the particular event window(‘clustering’), allowing for CARs to be independentacross securities. Close inspection of the data revealsno incidences of clustering, thus the choice betweenestimating model (1) and model (5) is a ratherarbitrary consideration (the second approach isemployed here). Investigation of AR for CambridgeHeart is considered first, followed directly byTriangle Pharmaceuticals, Inc., and then the calcula-tions of cumulative AR for both firms are given,respectively.

IV. Results

The marginal effects of individual events on dailyreturns as estimated by �̂ in Equation 5 can be foundin Table 2. Column 1 contains the estimated coeffi-cient on the binary variable for Cambridge Heart,whereas column 2 contains the estimated coefficienton the binary variable for Triangle Pharmaceuticals,

Inc.; the marginal effect as calculated by �̂ can beinterpreted as a discrete increase or decrease in thestock’s returns as measured by a simple growth rateformula. The null hypothesis is that the event has noimpact on the market value of the firm. Column 3features a summary description of each event corre-sponding to each particular statistically significantmarginal effect.

Cambridge Heart

Model (5) found in Table 2 (column 1) explainsroughly 7.3% (3.2% adjusted) variation in the stockvaluation of this firm.6 The first significant event forCambridge Heart (Table 2, column 1) was a distri-butional agreement allowing their goods to be soldalongside Hewlett-Packard products. This strategy(5 June 1997) increased their market value byapproximately 6.2%. The second significant eventfor Cambridge Heart was the financial announcementof record third quarter revenues on 21 October 1998;their stock price increased by approximately 8%. Thethird significant event for Cambridge Heart was theirdeclaration of personnel changes, specifically to theirBOD (4 January 2000). An increase in their stockprice of approximately 5.7% was the result of thismodification.

On 14 June 2000, Cambridge Heart announcedFDA clearance for their HearTwave System forpredicting heart arrhythmias; this advancementincreased their market return by approximately7.2%. The fifth significant event for CambridgeHeart was their announcement of Medicare reim-bursement for their Microvolt T-Wave Alternans teston 2 November 2001, increasing market return byapproximately 16.1%. The sixth significant event forCambridge Heart was their announcement to com-mence trading on the OTC BB on 7 May 2003; thisstrategy increased their market valuation by approx-imately 9.8%.

The seventh significant event for Cambridge Heartwas the announcement of a JACC study on 20 June2003 which increased market assessment by approx-imately 6%. The eighth significant event forCambridge Heart was their financial announcementof preliminary fourth quarter results on 7 January2004; this announcement increased market appraisalby approximately 12.9%. Cambridge Heart’ssecond announcement of a JACC study on 15December 2005 increased their market value byapproximately 8%.

The tenth significant event for Cambridge Heartwas the announcement of a national coverage

6 The SE of the regression is 0.067.

348 N. P. Stefanec

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

decision by Medicare/Medicaid on 22 December2005; this strategy increased market assessment byapproximately 12.7%. On 13 March 2006,Cambridge Heart announced a coverage policy

revision, increasing their market value by roughly15.3%. The twelfth significant event for CambridgeHeart was another announcement of a coveragepolicy decision on 28 June 2006, resulting in an

Table 2. Estimated marginal effects on AR

(1) (2) (3)

CambridgeHeart

TrianglePharmaceuticals

Descriptionof event

Constant �0.001 0.002(0.001) (0.002)

S&P 500 returns 0.601*** 0.836***(0.012) (0.110)

5 June 1997 0.062* – Cambridge Heart announces a distribution agreement where they willsell their products alongside Hewlett-Packard medical products(0.034) –

21 October 1998 0.080** – Cambridge Heart announces record third quarter revenue(0.034) –

10 December 1999 – �0.105*** Triangle Pharmaceuticals announces that FDA requires additionalPhase III testing for their HIV drug Coactinon– (0.029)

4 January 2000 0.057* – Cambridge Heart announces two changes to their BOD.(0.034) –

20 March 2000 – �0.068** Triangle Pharmaceuticals announces formation of new health infor-mation technology firm– (0.029)

14 June 2000 0.072** – Cambridge Heart announces FDA clearance for HearTwave System forprediction of life-threatening heart rhythm disturbances(0.034) –

25 September 2000 – �0.075*** Triangle Pharmaceuticals announces management changes.– (0.029)

6 August 2001 – �0.062** Triangle Pharmaceuticals announces layoffs, financial results anddecreased cash usage through 2002– (0.029)

24 August 2001 – 0.066** Triangle Pharmaceuticals announces $75 million dollars worth ofprivate placement financing– (0.029)

2 November 2001 0.161*** – Cambridge Heart announces Medicare reimbursement for Microvolt T-Wave Alternans test, allowing for greater market penetration(0.034) –

5 August 2002 – 0.049* Triangle Pharmaceuticals names new chairman and CEO– (0.029)

4 December 2002 – 0.077*** Gilead Science, Inc. announces they will acquire TrianglePharmaceuticals for $464 million– (0.029)

7 May 2003 0.098*** – Cambridge Heart agrees to commence trading on the OTC BB to gaincompliance with the $1.00 per share minimum bid requirement forlisting on the NASDAQ SmallCap Market

(0.034) –

20 June 2003 0.060* – Study in the Journal of the American College of Cardiology (JACC )confirms the reliability and importance of Cambridge Heart’sMicrovolt T-Wave Alternans test

(0.034) –

7 January 2004 0.129*** – Cambridge Heart announces preliminary fourth quarter and 2003revenue results showing solid growth(0.034) –

15 December 2005 0.080** – Study in JACC confirms and extends prior results showing the reliabilityand importance of Cambridge Heart’s Microvolt T-Wave Alternanstest

(0.034) –

22 December 2005 0.127*** – Centers for Medicare and Medicaid services proposes national coveragedecision which includes Cambridge Heart’s Microvolt T-WaveAlternans test

(0.034) –

13 March 2006 0.153*** – Aetna revises Coverage Policy Bulletin to include Cambridge Heart’sMicrovolt T-Wave Alternans test(0.034) –

28 June 2006 0.057* – CIGNA revises Coverage Policy Bulletin to include Cambridge Heart’sMicrovolt T-Wave Alternans test(0.034) –

R2 0.073 0.074�R2 0.032 0.058

Notes: The values of SEs are given within parentheses. Only statistically significant events are presented. The day of event iscatalogued and the event window is [�2, 1].*, ** and *** denote significance at the 0.10, 0.05 and 0.01 levels, respectively, two-tailed test.

Impact of firm strategies on stock market value 349

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

increase in market value of approximately 5.7%. Ingeneral, the majority of the significant events forCambridge Heart were with regard to tactical distri-butional alliances, which were closely tied to insur-ance coverage decisions, therefore expanding usageby doctors and patients.

Triangle Pharmaceuticals, Inc.

Model (5) found in Table 2 (column 2) explainsroughly 7.4% (5.8% adjusted) variation in the stockvaluation of this firm.7 The first significant event forTriangle Pharmaceuticals, Inc. (Table 2, column 2)was their announcement that FDA required addi-tional product testing on 10 December 1999;this setback decreased their market appraisal byapproximately 10.5%. The second significant eventfor Triangle Pharmaceuticals, Inc. was theannouncement of an expensive informational alliance

on 20 March 2000, decreasing their market valueby approximately 6.8%. Announcement of personnelchanges to the management staff on 25September 2000 decreased their stock value byapproximately 7.5%.

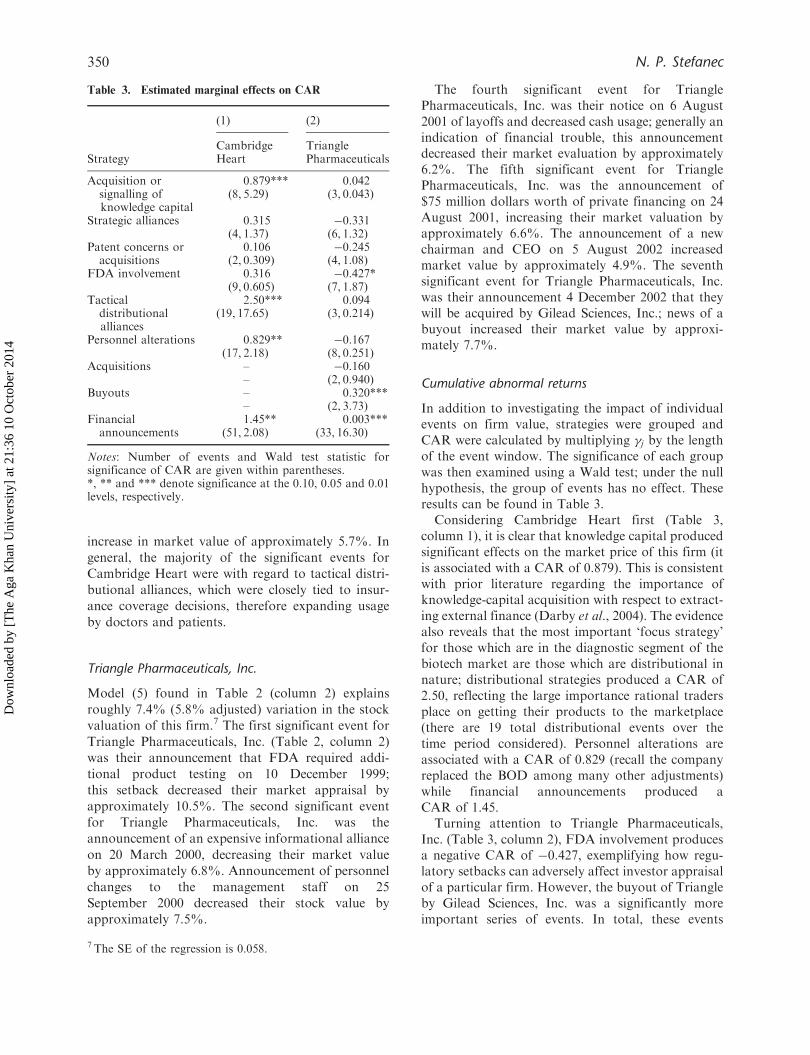

The fourth significant event for TrianglePharmaceuticals, Inc. was their notice on 6 August2001 of layoffs and decreased cash usage; generally anindication of financial trouble, this announcementdecreased their market evaluation by approximately6.2%. The fifth significant event for TrianglePharmaceuticals, Inc. was the announcement of$75 million dollars worth of private financing on 24August 2001, increasing their market valuation byapproximately 6.6%. The announcement of a newchairman and CEO on 5 August 2002 increasedmarket value by approximately 4.9%. The seventhsignificant event for Triangle Pharmaceuticals, Inc.was their announcement 4 December 2002 that theywill be acquired by Gilead Sciences, Inc.; news of abuyout increased their market value by approxi-mately 7.7%.

Cumulative abnormal returns

In addition to investigating the impact of individualevents on firm value, strategies were grouped andCAR were calculated by multiplying �j by the lengthof the event window. The significance of each groupwas then examined using a Wald test; under the nullhypothesis, the group of events has no effect. Theseresults can be found in Table 3.

Considering Cambridge Heart first (Table 3,column 1), it is clear that knowledge capital producedsignificant effects on the market price of this firm (itis associated with a CAR of 0.879). This is consistentwith prior literature regarding the importance ofknowledge-capital acquisition with respect to extract-ing external finance (Darby et al., 2004). The evidencealso reveals that the most important ‘focus strategy’for those which are in the diagnostic segment of thebiotech market are those which are distributional innature; distributional strategies produced a CAR of2.50, reflecting the large importance rational tradersplace on getting their products to the marketplace(there are 19 total distributional events over thetime period considered). Personnel alterations areassociated with a CAR of 0.829 (recall the companyreplaced the BOD among many other adjustments)while financial announcements produced aCAR of 1.45.

Turning attention to Triangle Pharmaceuticals,Inc. (Table 3, column 2), FDA involvement producesa negative CAR of �0.427, exemplifying how regu-latory setbacks can adversely affect investor appraisalof a particular firm. However, the buyout of Triangleby Gilead Sciences, Inc. was a significantly moreimportant series of events. In total, these events

Table 3. Estimated marginal effects on CAR

(1) (2)

StrategyCambridgeHeart

TrianglePharmaceuticals

Acquisition or 0.879*** 0.042signalling ofknowledge capital

(8, 5.29) (3, 0.043)

Strategic alliances 0.315 �0.331(4, 1.37) (6, 1.32)

Patent concerns or 0.106 �0.245acquisitions (2, 0.309) (4, 1.08)

FDA involvement 0.316 �0.427*(9, 0.605) (7, 1.87)

Tactical 2.50*** 0.094distributionalalliances

(19, 17.65) (3, 0.214)

Personnel alterations 0.829** �0.167(17, 2.18) (8, 0.251)

Acquisitions – �0.160– (2, 0.940)

Buyouts – 0.320***– (2, 3.73)

Financial 1.45** 0.003***announcements (51, 2.08) (33, 16.30)

Notes: Number of events and Wald test statistic forsignificance of CAR are given within parentheses.*, ** and *** denote significance at the 0.10, 0.05 and 0.01levels, respectively.

7 The SE of the regression is 0.058.

350 N. P. Stefanec

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

produced a CAR of 0.320; recall buyouts cansignificantly lower the costs of bringing new productsto the marketplace, suggesting the importance of suchevents to rational investors with regard to thetherapeutic portion of the biotech market.8

V. Conclusion

The goal of this research was to shed light on thedegree to which rational investors react to variousfinancial strategies which promote investment gainsin the medical-market biotechnology industry byemploying event study methodology. In total, ninedifferent firm strategies suspected of possessing acausal relationship with market valuation are con-sidered. Of these various strategies, the results suggestthat the most significant events favourably alteringinvestor valuation of firms in the diagnostic segmentof the biotechnology market are those which aredistributional and knowledge-gathering in nature.With respect to the therapeutic segment of thebiotechnology market, buyouts of smaller, morespecialized firms by those of larger scope play alarge role in the extraction of external finance,particularly because smaller, more specialized, firmsare considered riskier yet with a higher reward.Although this research has shown these results to berather robust, they may suffer from selection bias andthus provide a useful guide for future research.

Given that the firms chosen for this study are notarchetypical, the author admits the existence of anempirical trade-off between selection bias and gener-alization of the results, although every effort wasmade to minimize this possibility. Accordingly, futurestudies employing different and/or more exemplaryfirms may be a useful approach in the generalizationof the results found here. Furthermore, a study ofinformational asymmetries within the industry maybe of interest. Available information about biotechfirms is limited as only 30% of biotech firms arepublicly traded. For example, how would alliancesexisting amongst publicly and privately held firms beaffected by informational asymmetries?

Aside from empirical issues, there are other fruitfulareas of interest within this industry, which may helpeconomists and financial experts understand themechanisms by which biotechnology firms attractexternal finance. First, this study was limited to theUSA market although the US will soon face greater

competition, specifically from the EU and Japan(Paugh and LaFrance, 1997). The effects of global-ization and trade in this industry have not yet beeninvestigated in-depth by economists and financialexperts, but research along these lines could providelucid insights into a variety of economic theories.

Second, studies of the nonmedical and/or foreignbiotechnology markets may also help to furthergeneralize the results found in this study. Futureeconomic research devoted to the nonmedical biotechmarket, which includes applications of biotechnologyto agriculture (e.g. genetic food modificationsdesigned to increase crop yields, advances in freshwater aquaculture) and to environmental protection(e.g. decreasing environmental contaminants,advancing new energy sources, industrial waste man-agement), may prove enlightening. The latter exten-sion also makes the regulatory influence of theEnvironmental Protection Agency (EPA) relevant tothe discussion.

Finally, embryonic stem cell research shows someof the greatest hope for researchers solving themysteries of various diseases and ailments, such asType I diabetes, Alzheimer’s and multiple sclerosis(all of which have no cure and affect millions ofindividuals everyday). With the recent ban on embry-onic stem cell research in the USA being lifted, it ismore important than ever to understand the mech-anisms by which rational investors channel financialcapital into this industry; for example, there mayprove to exist a trade-off between the willingness toextend finance to a firm engaging in this line ofresearch and an individual’s moral preferences(Gilgoff, 2009).

Acknowledgements

The author thanks Michael Steinberger, KeithDownard and anonymous reviewers for their valu-able comments.

References

Aghion, P. and Tirole, J. (1994) On the management ofinnovation, Quarterly Journal of Economics, 109,1185–207.

Austin, D. (1993) An event-study approach to measuringinnovative output: the case of biotechnology, TheAmerican Economic Review, 83, 253–8.

8 Interestingly, neither strategic alliances nor patent acquisitions produced statistically significant CARs as would have beenexpected. Most likely, this is due to the small number of events which occurred regarding these particular concerns (four andtwo events, respectively), suggesting this study does not adequately address these issues.

Impact of firm strategies on stock market value 351

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014

Baum, J., Calabrese, T. and Silverman, B. (2000) Don’t goit alone: alliance network composition and startupsperformance in Canadian biotechnology, StrategicManagement Journal, 21, 267–94.

Chan, S., Keown, K. and John, M. (1997) Do strategicalliances create value?, Journal of Financial Economics,46, 199–221.

Chauvin, K. W. and Hirschey, M. (1993) Advertising,research-and-development, expenditures and themarket value of the firm, Financial Management, 22,128–40.

Darby, M., Liu, Q. and Zucker, L. (2004) High stakes inhigh technology: high-tech market values as options,Journal of Economic Inquiry, 42, 351–69.

Das, S., Sen, P. and Sengupta, S. (1998) Impact of strategicalliances on firm valuation, The Academy ofManagement Journal, 41, 27–41.

Filson, D. (2004) The impact of e-commerce strategies onfirm value: lessons from Amazon.com and its earlycompetitors, Journal of Business, 77, 135–54.

Galambos, L. and Sturchio, J. (1998) Pharmaceutical firmsand the transition to biotechnology: a study in strategicinnovation, The Business History Review, 72, 250–78.

Gilgoff, D. (2009) Obama’s stem cell order reopens theculture wars, US News and World Report, 19 March2009.

Lerner, J. (1994) The importance of patent scope: anempirical analysis, The RAND Journal of Economics,25, 319–33.

Lerner, J. and Merges, R. (1998) The control oftechnology alliances: an empirical analysis of thebiotechnology industry, The Journal of IndustrialEconomics, 46, 125–56 (Inside the Pin-Factory:Empirical Studies Augmented by ManagerInterviews: a Symposium).

MacKinlay, A. C. (1997) Event studies in economicsand finance, Journal of Economic Literature, 25,13–39.

Muth, J. (1961) Rational expectations and the theory ofprice movements, Econometrica, 29, 315–35.

Paugh, J. and LaFrance, J. (Eds) (1997) Meeting theChallenge: US Industry Faces the 21st Century, The USBiotechnology Industry, US Department ofCommerce, Office of Technology Policy,Washington, DC.

Rzakhanov, Z. (2004) Innovation, product development,and market value: evidence from the biotechnologyindustry, Economics of Innovation and NewTechnology, 13, 747–60.

Shan, W. and Song, J. (1997) Foreign direct invest-ment and the sourcing of technological advan-tage: evidence from the biotechnology industry,Journal of International Business Studies, 28,267–84.

Sundaram, A., Teresa, J. and Kose, J. (1996) An empiricalanalysis of strategic competition and firm values: thecase of R&D competition, Journal of FinancialEconomics, 40, 459–86.

352 N. P. Stefanec

Dow

nloa

ded

by [

The

Aga

Kha

n U

nive

rsity

] at

21:

36 1

0 O

ctob

er 2

014