the impact of directive 2000/36/ec on the economies of ... chain and price developments..... 83...

TRANSCRIPT

LMC INTERNATIONAL

Prepared for:

European Commission - DG Agriculture and Rural Development Rue de la Loi 130 B - 1049 Brussels

Belgium

This study has been financed by the Commission of the European Union. The conclusions, recommendations and opinions presented in this report reflect the opinion of the consultant and

do not necessarily reflect the opinion of the Commission.

LMC International Ltd LMC International Ltd 14-16 George Street 1841 Broadway Oxford OX1 2AF New York, NY 10023 England USA Tel: +44 1865 791737 Tel: +1 (212) 586-2427 Fax: +44 1865 791739 Fax: +1 (212) 397-4756 Email: [email protected] Email: [email protected]

Website: http://www.lmc.co.uk

Ccsa501 June 2006

The Impact of Directive 2000/36/EC on the Economies of those Countries

Producing Cocoa and Vegetable Fats other than Cocoa Butter

Main Report

While LMC International has endeavoured to ensure the accuracy of the data, estimates and forecasts contained in this study, any decisions based on them (including those involving investment and planning) are at the client's own risk. LMC International can accept no liability regarding information, analysis and forecasts contained in this study.

Contents (i)

Table of Contents

Executive Summary....................................................................................................E1

EU Chocolate Consumption and Cocoa Imports ..........................................................E1 Vegetable Fat Imports and CBE Production.................................................................E2 Impact of the Directive on Cocoa and Vegetable Fat Producers..................................E7

Cocoa Producers.................................................................................................E7 Vegetable Fat Producers.....................................................................................E7

Conclusions ..................................................................................................................E8

Chapter 1: Background and Introduction................................................................... 1

Introduction..................................................................................................................... 1 CBE Manufacture ........................................................................................................... 2 Adoption of the Directive................................................................................................. 3

Chapter 2: EU Chocolate Consumption and Production .......................................... 6

EU-15.............................................................................................................................. 6

Chocolate Product Consumption........................................................................... 6 Chocolate Product Trade .................................................................................... 10 Chocolate Product Production............................................................................. 11

Retail Chocolate Prices ................................................................................................ 13 Central and Eastern Europe ......................................................................................... 14

Chocolate Consumption ...................................................................................... 14 Chocolate Trade.................................................................................................. 15 Chocolate Production .......................................................................................... 16

Chapter 3: The EU Market for Cocoa ........................................................................ 19

Net Imports ................................................................................................................... 19 Imports by Origin .......................................................................................................... 23 EU grindings ................................................................................................................. 27 Intra EU-15 Trade......................................................................................................... 28 Impact of the Directive on cocoa imports...................................................................... 28 EU-10 Cocoa Demand.................................................................................................. 30

Chapter 4: EU-15 Imports of Vegetable Fats Allowed by Directive 2000/36/EC for the Manufacturer of Chocolate ............................................................................ 32

Exotics .......................................................................................................................... 33

Sheanuts and Butter............................................................................................ 33 Sal, Mango Kernel and Kokum............................................................................ 37 Total Exotic Imports............................................................................................. 39

Contents (ii)

Palm Oil ........................................................................................................................ 40

Chapter 5: The Use of Vegetable Fats in Chocolate in the EU-15 and CBE Production................................................................................................................... 42

The use of the permitted fats for the production of Chocolate in the EU-15................. 42

Countries that Permitted the Use of CBEs Prior to 2000..................................... 42 Countries Not Permitting the Use of CBEs Prior to 2000 .................................... 46 Artisanal Production ............................................................................................ 50 Private and Own Label ........................................................................................ 51

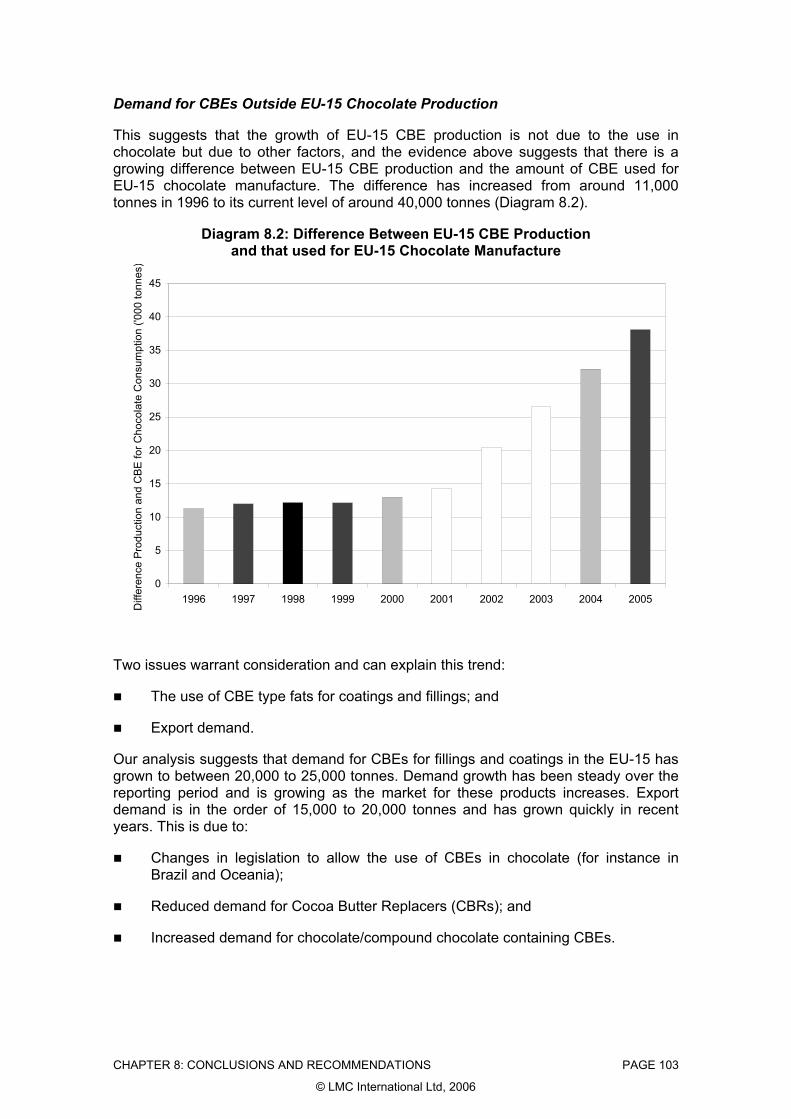

EU-15 CBE Production ................................................................................................. 51 Demand for CBEs outside EU-15 Chocolate Production.............................................. 52

Coatings and Fillings ........................................................................................... 53 Export Demand ................................................................................................... 54

Prices and Margins ....................................................................................................... 54 The Importance of the CBE Industry to the EU-15 ....................................................... 55 Summary ...................................................................................................................... 56

Chapter 6: Impact of the Directive on Cocoa Producers ........................................ 57

Economic Developments .............................................................................................. 57 Importance of the Cocoa Sector ................................................................................... 57 Overview of Production and Export Trends .................................................................. 59

Production Trends ............................................................................................... 59 Export Trends...................................................................................................... 62

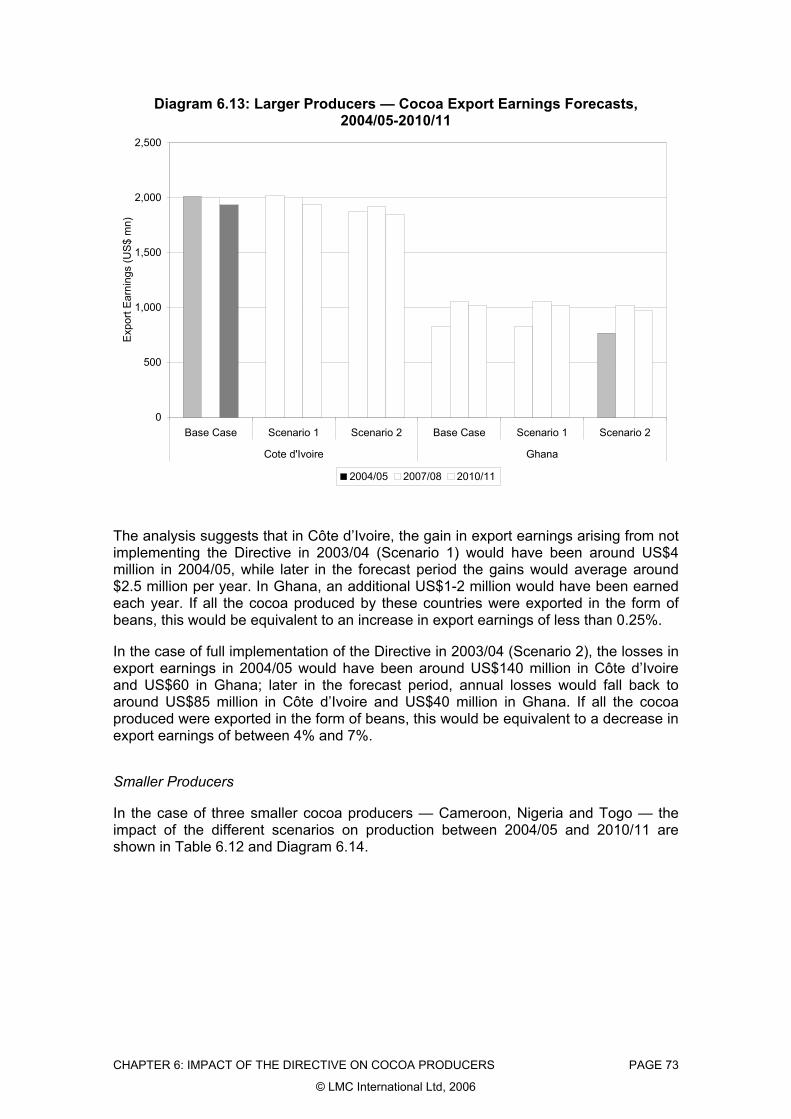

Value Addition............................................................................................................... 65 Price Developments...................................................................................................... 66 Impact of the Directive .................................................................................................. 69

Estimating The Impact Using LMC’s Forecasting Model..................................... 69 Results ................................................................................................................ 70

Chapter 7: Impact of the Directive on Vegetable Oil Producers ............................ 79

Sheanuts....................................................................................................................... 79

Importance of Exotic Fats to the Economy.......................................................... 79 Value Chain and Price Developments................................................................. 83 Impact of the Directive......................................................................................... 86

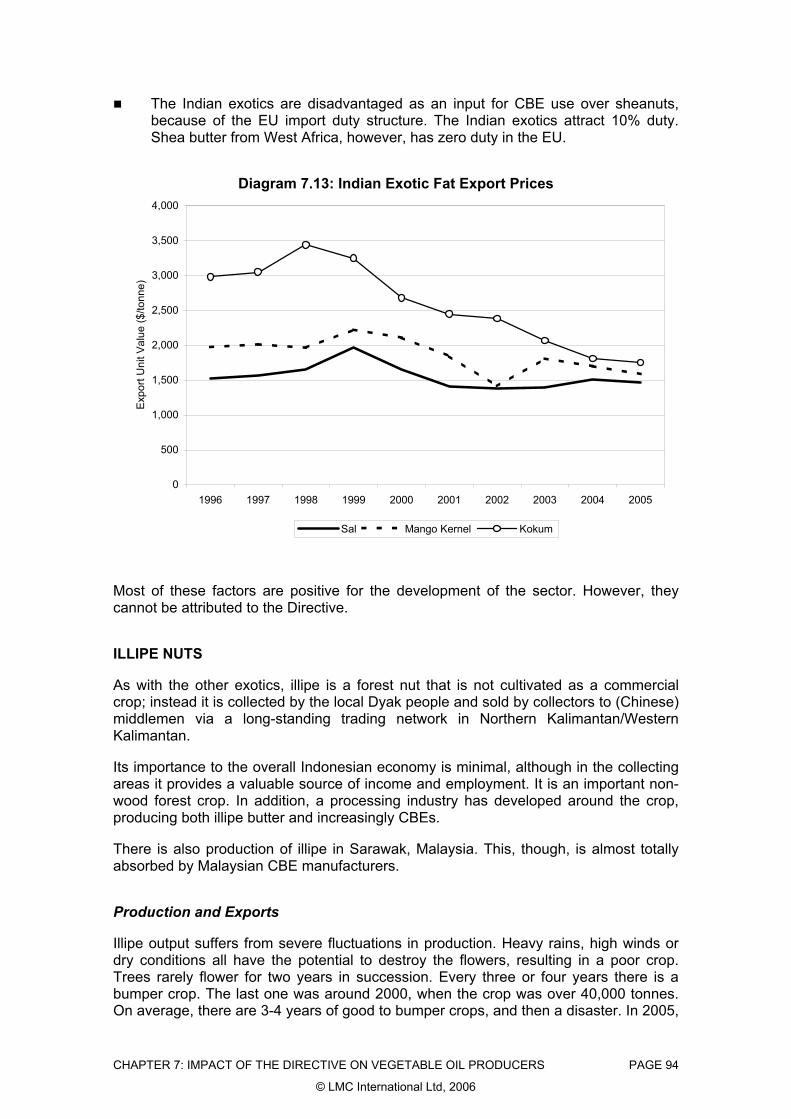

Indian Exotic Fats ......................................................................................................... 87

Importance of Exotic Fats to the Economy.......................................................... 87 Sal ....................................................................................................................... 87 Mango Kernel Oil................................................................................................. 89 Kokum ................................................................................................................. 92 Impact of the Directive......................................................................................... 93

Contents (iii)

Illipe Nuts ...................................................................................................................... 94

Impact of the Directive......................................................................................... 96

Palm Oil ........................................................................................................................ 96 Conclusions .................................................................................................................. 98

Chapter 8: Conclusions and Recommendations................................................... 100

Conclusions ................................................................................................................ 100

EU Chocolate Consumption and Cocoa Imports............................................... 100 Vegetable Fat Imports and CBE Production ..................................................... 101 Impact of the Directive on Cocoa and Vegetable Fat Producers ...................... 104

Conclusion.................................................................................................................. 105

Contents (iv)

List of Tables

Table EXEC.1: EU-15 Exotic Fat Imports ....................................................................E3 Table EXEC.2: Forecast Global Cocoa Prices, 2003/04-2010/11 ...............................E7

Table 1.1: Permitted Fats and Main Producing Countries ..................................... 1 Table 1.2: Implementation of Directive 2000/36/EC............................................... 4

Table 2.1: EU-15 Chocolate Consumption............................................................. 7 Table 2.2: Consumption by Type, UK, Germany, France and Italy........................ 9 Table 2.3: EU-15 Chocolate Production............................................................... 12 Table 2.4: Central European Member States — Chocolate Product

Consumption ....................................................................................... 14 Table 2.5: Central European Member States — Chocolate Trade ...................... 15 Table 2.6: Central European Member States — Chocolate Production............... 16 Table 2.7: Poland and Hungary — Chocolate Production by Type...................... 17

Table 3.1: Net Imports of Cocoa Beans and Cocoa Products by Major EU-15 Importers ............................................................................................. 20

Table 3.2: Net Imports of Cocoa Beans and Cocoa Products by Product Category.............................................................................................. 22

Table 3.3: Imports of Cocoa Beans and Cocoa Products by Exporting Region and Country......................................................................................... 24

Table 3.4: Western Europe — Cocoa Grindings, 1999-2005............................... 27 Table 3.5: Intra-EU Trade in Cocoa Beans and Cocoa Products by Product

Category.............................................................................................. 29 Table 3.6: EC-10 — Net Cocoa Bean and Product Imports by Country .............. 30 Table 3.7: EC-10 — Net Cocoa Bean and Product Imports by Type................... 30

Table 4.1: EU-15 Sheanut Imports....................................................................... 33 Table 4.2: EU-15 Shea Butter Imports ................................................................. 34 Table 4.3: Estimated Indian Exotic Oil Exports to EU-15..................................... 37 Table 4.4: Illipe Imports to the EU-15................................................................... 39

Table 5.1: Chocolate Product Consumption Countries Permitting CBEs Prior to 2000 ................................................................................................ 43

Table 5.2: Chocolate Biscuit Consumption Countries Permitting CBEs Prior to 2000 ................................................................................................ 43

Table 5.3: Cadbury Dairy Milk, Filling Weights .................................................... 44 Table 5.4: UK Chocolate Bar Production by Type ............................................... 44 Table 5.5: Impact of the Directive on CBE Consumption in EU-15 Countries

Permitting the Use of CBEs Prior to 2000........................................... 47 Table 5.6: Chocolate Product Consumption in EU-15 Countries Not Permitting

CBEs Prior to 2000 ............................................................................. 47 Table 5.7: Chocolate Biscuit Consumption in EU-15 Countries Not Permitting

CBEs Prior to 2000 ............................................................................. 48 Table 5.8: Estimated EU-15 CBE Production ...................................................... 52

Table 6.1: Côte d’Ivoire, Ghana and Togo — Macroeconomic Data ................... 58

Contents (v)

Table 6.2: Importance of Cocoa as % of Total Export Earnings .......................... 59 Table 6.3: Cocoa Production, 1995/96-2004/05 .................................................. 61 Table 6.4: Exports of Cocoa Beans and Cocoa Products, 2001/02-2004/05....... 62 Table 6.5: Exports of Cocoa Beans and Cocoa Products by Destination,

2001/02-2004/05 ................................................................................. 63 Table 6.6: Cocoa Exports by Type, 2001/02-2004/05.......................................... 65 Table 6.7: Cocoa Bean Export Prices, 1995/96-2004/05..................................... 66 Table 6.8: Cocoa Product Export Prices, 2001/02-2004/05................................. 68 Table 6.9: Forecast Global Cocoa Prices, 2003/04-2010/11 ............................... 70 Table 6.10: Larger Producers — Cocoa Production Forecasts,

2004/05-2010/11 ................................................................................. 71 Table 6.11: Larger Producers — Cocoa Export Earnings Forecasts,

2004/05-2010/11 ................................................................................. 72 Table 6.12: Smaller Producers — Cocoa Production Forecasts,

2004/05-2010/11 ................................................................................. 74 Table 6.13: Smaller Producers — Cocoa Export Earnings Forecasts,

2004/05-2010/11 ................................................................................. 75

Table 7.1: Shea Producing Countries, Average Per Capita Income .................... 79 Table 7.2: Estimated Local Shea Consumption ................................................... 81 Table 7.3: Sheanut Exports.................................................................................. 82 Table 7.4: Per Annum Collected Sheanuts .......................................................... 83 Table 7.5: Estimated Collector Prices, 2004/05 ................................................... 85 Table 7.6: Estimated Sal Exports......................................................................... 88 Table 7.7: Estimated Mango Kernel Exports........................................................ 91 Table 7.8: Estimated Kokum Butter Exports ........................................................ 92

Table 8.1: EU-15 Exotic Fat Imports .................................................................. 101 Table 8.2: Forecast Global Cocoa Prices, 2003/04-2010/11 ............................. 104

Contents (vi)

List of Diagrams

Diagram EXEC 1: Total EU-15 Net Imports of Cocoa Beans and Cocoa Products .....E2 Diagram EXEC 2: EU-15 CBE Production....................................................................E3 Diagram EXEC 3: EU-15 CBE Consumption for Chocolate Production .......................E5 Diagram EXEC 4: Difference Between EU-15 CBE Production ...................................E6

Diagram 1.1: Palm Mid-fraction Production ........................................................... 3 Diagram 1.2: Labelling Requirements.................................................................... 5

Diagram 2.1: Change in Consumption 2003 v 2005 .............................................. 8 Diagram 2.2: Per Capita Chocolate Consumption, 2005 ....................................... 8 Diagram 2.3: Consumption by Type....................................................................... 9 Diagram 2.4: Intra-EU Chocolate Product Trade ................................................. 10 Diagram 2.5: Net EU-15 Exports.......................................................................... 11 Diagram 2.6: France Chocolate Retail Price Index .............................................. 13 Diagram 2.7: Germany Milk Chocolate Retail Price Index ................................... 14 Diagram 2.8: Central European Member States —Chocolate Product

Consumption .................................................................................. 15 Diagram 2.9: Central European Member States — Chocolate Trade.................. 16 Diagram 2.10: Central European Member States — Chocolate Production .......... 17 Diagram 2.11: Poland and Hungary — Chocolate Production by Type ................. 18

Diagram 3.1: Total EU-15 Net Imports of Cocoa Beans and Cocoa Products..... 21 Diagram 3.2: EU-15 Cocoa Imports % of Total.................................................... 25 Diagram 3.3: EU-15 Share of Total Cocoa Exports by Producing Countries....... 26 Diagram 3.4: EU-15 Share of Total Cocoa Exports ............................................. 26 Diagram 3.5: Western Europe – Cocoa Grindings............................................... 27 Diagram 3.6: EU-15 Share of Total Cocoa Exports ............................................. 28 Diagram 3.7: EC-10 — Changes in Net Cocoa Bean and Product Imports by

Type................................................................................................ 31

Diagram 4.1: EU-15 Sheanut Imports, 1996–2005 .............................................. 34 Diagram 4.2: EU-15 Shea Butter Imports ............................................................ 35 Diagram 4.3: India — Sheanut Imports................................................................ 36 Diagram 4.4: EU-15 Sheanut Imports .................................................................. 36 Diagram 4.5: India — Exotic Oil Exports.............................................................. 38 Diagram 4.6: Sal, Kokum and Mango Kernel Exports from India to the EU-15 ... 38 Diagram 4.7: Exotic Fat Imports to EU-15 ........................................................... 40 Diagram 4.8: EU-15 Palm Oil Imports.................................................................. 41

Diagram 5.1: Chocolate Use in EU-15 Countries Permitting CBEs Prior to 2000................................................................................................ 45

Diagram 5.2: CBE Demand in EU-15 Countries .................................................. 46 Diagram 5.3: Chocolate Product Consumption in Countries................................ 49 Diagram 5.4: Difference Between EU-15 CBE Production and that used for

EU-15 Chocolate Manufacture ....................................................... 53 Diagram 5.5: Estimated CBE Prices .................................................................... 55 Diagram 5.6: Estimated CBE Use in EU-15 Chocolate........................................ 56

Contents (vii)

Diagram 6.1: Ghana and Côte d’Ivoire: Cocoa as % of Total Export Earnings and Cocoa Prices ........................................................................... 59

Diagram 6.2: West Africa — Cocoa Production ................................................... 60 Diagram 6.3: West Africa — Global Cocoa Production Shares ........................... 60 Diagram 6.4: Exports of Cocoa Beans and Cocoa Products ............................... 63 Diagram 6.5: Exports of Cocoa Beans and Cocoa Products by Destination ....... 64 Diagram 6.6: EU-15 Shares of Cocoa Exports .................................................... 64 Diagram 6.7: Cocoa Exports by Type .................................................................. 66 Diagram 6.8: Cocoa Bean Export Prices and Global Supply-Demand Balance .. 67 Diagram 6.9: Producer Shares of Cocoa Bean Export Prices ............................. 68 Diagram 6.10: Cocoa Product Export Prices ......................................................... 69 Diagram 6.11: Forecast Global Cocoa Prices, 2003/04-2010/11........................... 71 Diagram 6.12: Larger Producers — Cocoa Production Forecasts,

2004/05-2010/11 ............................................................................ 72 Diagram 6.13: Larger Producers — Cocoa Export Earnings Forecasts,

2004/05-2010/11 ............................................................................ 73 Diagram 6.14: Smaller Producers — Cocoa Production Forecasts,

2004/05-2010/11 ............................................................................ 74 Diagram 6.15: Smaller Producers — Cocoa Export Earnings Forecasts,

2004/05-2010/11 ............................................................................ 75 Diagram 6.16: Cocoa Exports as % of GDP .......................................................... 76 Diagram 6.17: Changes in Cocoa Tax Revenue.................................................... 77 Diagram 6.18: Changes in Yields........................................................................... 78 Diagram 6.19: Changes in Harvested Area ........................................................... 78

Diagram 7.1: Average GDP Growth ................................................................... 80 Diagram 7.2: Importance of Sheanuts to Export Earnings................................... 80 Diagram 7.3: Regional Sheanut Exports.............................................................. 82 Diagram 7.4: Sheanut Marketing Chain ............................................................... 84 Diagram 7.5: Estimated Sheanut Export Prices................................................... 85 Diagram 7.6: Stylised Sheanut Value Chain, 2004 .............................................. 86 Diagram 7.7: Estimated Sal Production ............................................................... 87 Diagram 7.8: Sal Prices and Margins................................................................... 89 Diagram 7.9: Mango Kernel Harvested Production.............................................. 90 Diagram 7.10: Mango Kernel Marketing Margins, 2005......................................... 91 Diagram 7.11: Estimated Kokum Nut Production................................................... 92 Diagram 7.12: Kokum Marketing Margins, 2005.................................................... 93 Diagram 7.13: Indian Exotic Fat Export Prices ...................................................... 94 Diagram 7.14: EU-15 Illipe Butter Imports ............................................................. 95 Diagram 7.15: Estimated Illipe Butter Export Unit Values...................................... 96 Diagram 7.16: Palm Oil Production, 1996-2005..................................................... 97 Diagram 7.17: Palm Olein Prices, c.i.f. Europe...................................................... 98

Diagram 8.1: EU-15 CBE Production................................................................. 102 Diagram 8.2: Difference Between EU-15 CBE Production and that used for

EU-15 Chocolate Manufacture ..................................................... 103

EXECUTIVE SUMMARY PAGE E1

© LMC International Ltd, 2006

Executive Summary

The European Parliament and Council adopted Directive 2000/36/EC on 23 June 2000. The aim of the Directive was to allow the use of up to 5% of a limited number of vegetable fats in the production of chocolate. The objective of the Directive was to simplify Community provisions concerning chocolate, with a view to allowing the free movement of chocolate products within the Internal Market. The Directive was implemented by member states during 2003.

The vegetable fats that were permitted for use required strict technical characteristics and were limited to six (Illipe, palm oil, sal, shea, kokum gurgi, and mango kernel). Five of these (illipe, sal, shea, kokum gurgi and mango kernel) can be classed as exotic fats; that is, the fat is obtained from the seeds/nuts of trees that are mainly growing wild in the tropics. Enzymic modification of the fats was prohibited.

This study provides an evaluation of the impact of the Directive as required under the Directive. The aim of the evaluation is to:

Determine the impact of Directive 2000/36/EC on the economies of those countries producing cocoa and vegetable fats other than cocoa butter; and

Provide guidance to the Commission on whether or not to amend the list of vegetable fats other than cocoa butter that are permitted for use in chocolate. In this regard, three options are considered:

― To maintain the list for a further period of time;

― To shorten the list; or

― To extend the list.

EU CHOCOLATE CONSUMPTION AND COCOA IMPORTS

EU-15 consumption of chocolate products is around 2.2 million tonnes. There has been little change in total consumption since the Directive was adopted in 2003. Four markets, UK, Germany, Italy and France account for close to 80% of EU-15 chocolate consumption.

There are a number of reasons for the slow growth in consumption:

Slow growth in income. Per capita consumption is related to per capita incomes, and the slow growth of incomes in recent years adversely affected demand;

Market saturation in some of the mature markets; and

Increasing concerns over obesity.

Not all segments of the market have experienced the same growth rates; in particular there has been growth in whole bar (tablet) consumption over other products. This has been driven by campaigns highlighting the benefits of cocoa consumption (in particular, the presence of the antioxidant flavanol which has been found to reduce blood pressure) and the growth of speciality products such as single origin bars. Both of these types of products have a higher cocoa content.

EXECUTIVE SUMMARY PAGE E2

© LMC International Ltd, 2006

Net imports of cocoa beans and cocoa products in bean equivalent (b.e.) terms from outside the EU-15 countries have increased from around 1.2 million tonnes in 1996 to over 1.4 million tonnes in 2005, recording an average annual growth rate of 2.1% over the last 10 years (Diagram EXEC 1). This is somewhat higher than the growth of chocolate production and consumption, which has grown by 0.6% per annum over the period. Over the last two years, since the adoption of the Directive, the rate of growth of net cocoa imports has accelerated to 3.5% despite a flat chocolate product market. This points towards the increased cocoa solids content of chocolate as well as the increased use of cocoa products for other food applications.

Diagram EXEC 1: Total EU-15 Net Imports of Cocoa Beans and Cocoa Products

0

200

400

600

800

1,000

1,200

1,400

1,600

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Net

Coc

oa Im

ports

('00

0 to

nnes

b.e

.)

Total Trend

EXECUTIVE SUMMARY PAGE E3

© LMC International Ltd, 2006

VEGETABLE FAT IMPORTS AND CBE PRODUCTION

When converted to the raw materials that are used for CBE manufacture, exotic fat imports have increased from 8,000 tonnes in 1996 to 24,500 tonnes in 2005 (Table EXEC 1). Since the adoption of the Directive, imports of these exotic fat raw materials have increased by 25%.

Table EXEC.1: EU-15 Exotic Fat Imports (tonnes)

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Sheanuts 31,938 24,856 52,757 30,155 29,396 59,575 48,787 80,802 67,626 85,040Shea butter 138 241 1,542 3,543 1,590 2,177 7,502 10,358 7,049 15,397Sal Oil 278 324 174 177 330 401 230 544 201 900Sal Stearin 650 757 405 412 770 936 537 1,269 469 2,100Mango Kernel Stearin 331 1,001 142 1,300 0 125 141 744 146 437Illipe nuts 30 20 19 24 4 4 4,187 44 2 52Illipe butter 1,688 857 327 47 31 9 121 646 193 1,446 CBE raw material 7,987 6,865 9,884 8,587 6,285 11,393 11,776 19,638 14,979 24,459

Source: LMC.

While it is possible to get an impression of the level of exotic fat imports and use in CBEs, the level of palm oil (or more specifically palm mid-fraction) is more difficult to gauge owing to the large number of end uses. The use of palm mid-fraction (PMF) varies between 10% to 100% of the weight of a CBE, depending upon what the product is to be used for. A lower proportion of exotics are used in “soft” CBEs (up to 30% exotic) while a higher proportion is used in “hard” CBEs (greater than 30%). The choice of CBE depends on the market and application.

Typically, soft CBEs are used in the UK and Ireland, and hard CBEs are used elsewhere. Splitting exotic fat use this way, with the balance being made up of PMF gives total EU-15 CBE production of 58,600 tonnes in 2005. Production has grown by 11% per annum since 2000 and at a similar rate since the adoption of the Directive (Diagram EXEC 2).

EXECUTIVE SUMMARY PAGE E4

© LMC International Ltd, 2006

Diagram EXEC 2: EU-15 CBE Production

0

10

20

30

40

50

60

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

EU-1

5 C

BE P

rodu

ctio

n ('

000

tonn

es)

While exotic fat imports and CBE production have increased, the key question is: “Is this due to increased demand from chocolate manufacturers in the EU-15 following the implementation of the Directive? Or, are there other explanations?”

The Use of CBEs in EU-15 Chocolate

To determine the use of CBEs in EU-15 chocolate it is helpful to split the EU-15 market into two segments: those that permitted the use of CBEs in chocolate prior to 2000; and those that did not, and consider trends in each of these segments.

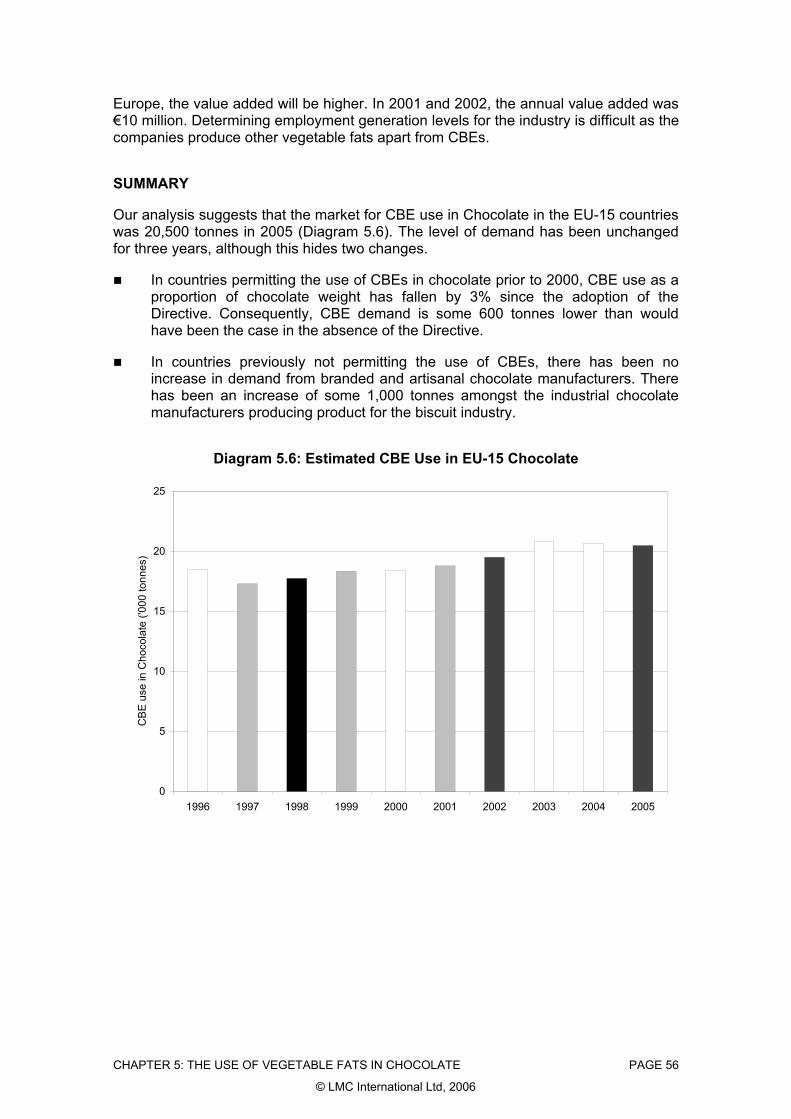

Our analysis suggests that the market for CBE use in chocolate in the EU-15 countries was 20,500 tonnes in 2005 (Diagram EXEC 3). This level of demand has been unchanged for three years, although this hides two changes:

In countries permitting the use of CBEs in chocolate prior to 2000, CBE use as a proportion of chocolate weight has fallen by 3% since the adoption of the Directive. This is due to the Directive’s definition of milk chocolate. Under the definition, vegetable fat is not included in the calculation of total fat that must be a minimum of 25% for a product to be called milk chocolate. Thus for a typical low cost milk chocolate recipe with 28.3% fat, the maximum vegetable fat that can be added is 3.3%. If 5% was previously being used then the amount of permitted vegetable fat has fallen. Consequently, we estimate that CBE demand is some 600 tonnes lower than would have been the case in the absence of the Directive.

In countries previously not permitting the use of CBEs in chocolate, there has been no increase in demand from branded and artisanal chocolate manufacturers. There has been an increase of some 1,000 tonnes amongst the industrial chocolate manufacturers producing product for the biscuit and ice cream industries.

EXECUTIVE SUMMARY PAGE E5

© LMC International Ltd, 2006

Net, there has been a 400 tonne increase in CBE demand since the adoption of the Directive.

Diagram EXEC 3: EU-15 CBE Consumption for Chocolate Production

0

5

10

15

20

25

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

CB

E D

eman

d ('0

00 to

nnes

)

DEMAND FOR CBES OUTSIDE EU-15 CHOCOLATE PRODUCTION

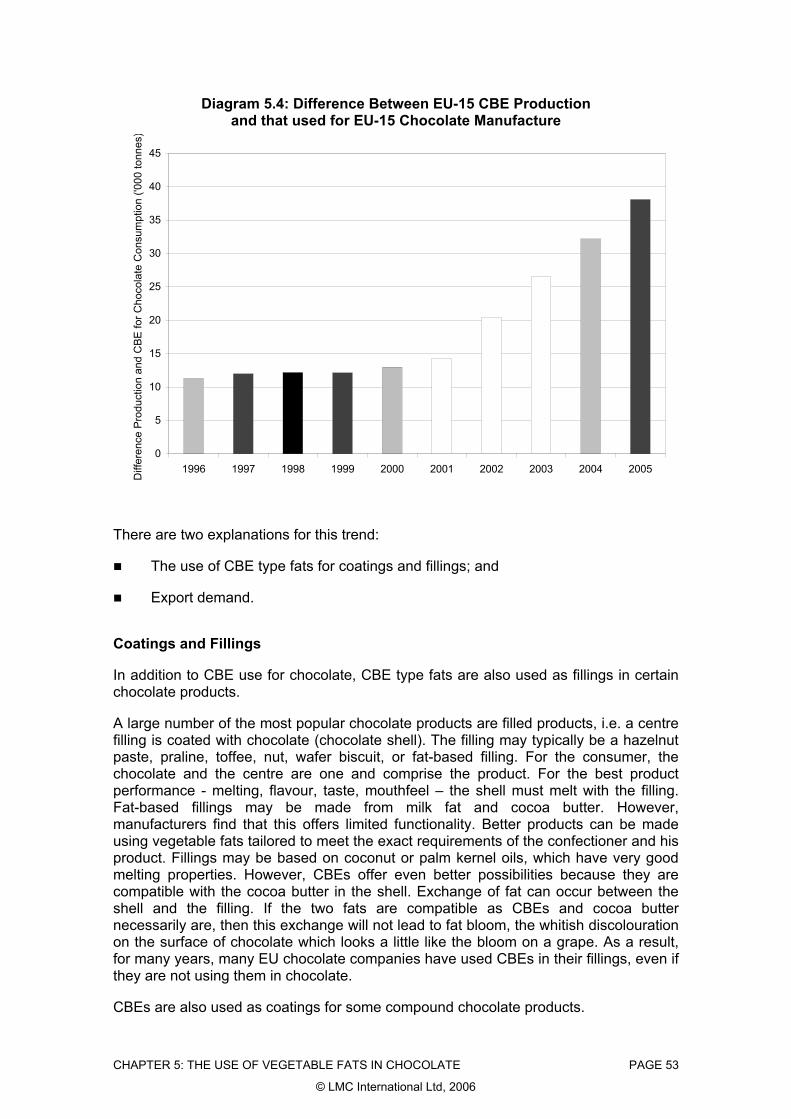

This suggests that the growth of EU-15 CBE production has not been due to CBE use in EU-15 chocolate but due to other factors. The evidence above suggests that there is a growing difference between EU-15 CBE production and the amount of CBE used for EU-15 chocolate manufacture. The difference has increased from around 11,000 tonnes in 1996 to its current level of around 40,000 tonnes (Diagram EXEC 4).

EXECUTIVE SUMMARY PAGE E6

© LMC International Ltd, 2006

Diagram EXEC 4: Difference Between EU-15 CBE Production and that used for EU-15 Chocolate Manufacture

0

5

10

15

20

25

30

35

40

45

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Diff

eren

ce P

rodu

ctio

n an

d C

BE fo

r Cho

cola

te C

onsu

mpt

ion

('000

tonn

es)

Two issues warrant consideration and can explain this trend:

The use of CBE-type fats for coatings and fillings; and

Export demand.

For many years, EU chocolate companies have used CBEs in their fillings, even if they are not using them in chocolate. The Directive does not cover this use of CBEs. Our analysis suggests that demand for CBEs for fillings and coatings in the EU-15 has grown to between 20,000 to 25,000 tonnes. Demand growth has been steady over the reporting period and is growing as the market for these products increases.

Export demand is in the order of 15,000 to 20,000 tonnes and has grown sharply in recent years. This is due to:

Changes in legislation to allow the use of CBEs in chocolate (for instance, in Brazil and Oceania);

Substitution of Cocoa Butter Replacers (CBRs) in compound chocolate by CBEs. This is because CBRs are high in transfats; and

Increased demand for chocolate/compound chocolate containing CBEs.

IMPACT OF THE DIRECTIVE ON COCOA AND VEGETABLE FAT PRODUCERS

Cocoa Producers

Cocoa typically accounts for over one third of total export earnings in Ghana and Côte d’Ivoire, and around 10% in the case of Cameroon. It is less important in

EXECUTIVE SUMMARY PAGE E7

© LMC International Ltd, 2006

Nigeria and Togo. As would be expected, cocoa prices are a major determinant of cocoa’s share of export earnings in Ghana and Côte d’Ivoire.

As can be surmised from the above, the Directive has had little impact on cocoa producers to date. We have calculated the impact (and potential impact) of the Directive under three scenarios.

― The base case scenario calculates the impact of the Directive on the market to date;

― Scenario 1 calculates what would have been the state of the market had the Directive not been implemented in 2003/04; and

― Scenario 2 calculates what would have been the impact of the Directive if it had been fully implemented in 2003/04, i.e., CBE usage in chocolate rose to 5% in the EU-8.

The forecast levels of prices under the different scenarios between 2003/04 and 2010/11 are shown in Table EXEC.2.

Table EXEC.2: Forecast Global Cocoa Prices, 2003/04-2010/11 (Real US$ per tonne)

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

Base Case 1,431 1,419 1,439 1,554 1,649 1,604 1,559 1,531 Scenario 1 1,435 1,421 1,441 1,555 1,650 1,605 1,560 1,532 Scenario 2 1,311 1,344 1,384 1,521 1,625 1,561 1,514 1,490

Source: LMC.

Comparing the prices forecast under the base case scenario with those forecast under Scenario 1 suggests that the impact of not implementing the Directive in 2003/04 would have been modest i.e. a price difference of less than $5 per tonne.

Were the Directive to have been implemented fully in 2003/04, the results suggest that the price impact would have been more pronounced.

Vegetable Fat Producers

In terms of the total economy, the importance of the exotic fats is relatively small. However, in the regions where they are collected, they are very important for employment and income generation. In the case of shea, collection is primarily by women, while for illipe and the Indian exotics, collection is by tribal people living off non-timber forest products.

For sheanuts, demand is from both the local market and for export. The other exotics are primarily export orientated, the only exception being for sal when production is higher than that which can be absorbed by the export market. In this case, the balance is used domestically.

For all the exotics, with the exception of kokum, there can be extreme fluctuations in production between years. This is due to the uncultivated nature of production.

EXECUTIVE SUMMARY PAGE E8

© LMC International Ltd, 2006

There has been an increase in demand for exotics from the European CBE manufacturers: for shea since 2000, sal since 2003 and illipe in 2005.

Trends in prices follow the supply-demand balance of the individual crops, thus in years of high production there is a tendency for prices to fall and vice-versa.

For the Indian exotic fats and illipe, almost all processing occurs at origin and processed products are exported. This is not the case with sheanuts where the export is more of nuts than products.

Both shea and the Indian exotics remain underdeveloped in terms of their potential. In both cases, there is scope to increase collection and improve the quality of the product, although whether this occurs is partly dependent upon the price paid to collectors. In the case of shea, some governments have recognised the crop’s potential and are seeking to increase the development of the crop as part of a diversification strategy. For illipe, production potential is declining as palm oil development reduces the illipe forests.

Palm oil production has grown dramatically since the adoption of the Directive. However, the growth of CBE demand is small in relation to the total volumes of palm oil produced and marketed.

The increase in demand for these products, although beneficial for the sector, cannot be attributed to the Directive.

CONCLUSIONS

Our analysis suggests that the Directive has had very little impact on the global cocoa market as very few EU-15 chocolate manufacturers have incorporated CBEs into their recipes. The same is true of the vegetable fat producers, although increased demand for CBEs from outside of the EU-15 chocolate market has increased demand for their products. However, although the Directive was passed in 2000, it was only implemented in 2003. Hence the market has only had two years to adjust to the new realities.

On the basis of this evidence, there is no need to change the list of permitted fats and our recommendation is to maintain the list for a further period of time, until the impact of the use of vegetable fats other than cocoa butter on the economies of developing countries can be further assessed.

There are a number of additional considerations:

Two years is a very short time period for end users to make wholesale changes to recipes. A further review of the market in five to ten years time would be useful. This would allow time for manufacturers to work though the implications of the Directive and test consumer perceptions of products containing CBEs. As yet, this has not been possible, as no one has changed recipes.

The shortage of shea and sal during 2005/06 has reduced exotic availability and led to a run down in exotic fat stocks. This has increased exotic prices and placed pressure on CBE manufacturers. This highlights the dangers of restricting the number of fats, as it reduces the scope for substitution. Any reduction in the list of permitted fats would create a worse situation.

EXECUTIVE SUMMARY PAGE E9

© LMC International Ltd, 2006

With the global market for CBEs increasing and the variability of annual exotic fat production, in the longer term there is potential for a shortage of exotic fats. This suggests that in the longer term, consideration could be given to one or all of the following:

― Crop development for the permitted exotics. At present shea, sal and mango kernel are all underdeveloped wild crops. There is scope, in the longer term, to increase crop potential. For instance, in West Africa the local production of shea butter could be enhanced though the provision of basic hand expellers. This would reduce the time needed to produce local shea butter and increase processing efficiency. In both cases, the provision of nuts would increase: first, by allowing more time for nut collection; and, second, by reducing the quantity of nuts required to yield a certain volume of butter. Additionally it could be possible to reduce the gestation period for the trees. In the case of sal, the proportion of the crop collected is small in relation to total production.

― Expanding the list of permitted fats. However, the number of possible fats is limited, with aceituno oil probably the largest.

CHAPTER 1: BACKGROUND AND INTRODUCTION PAGE 1

© LMC International Ltd, 2006

Chapter 1: Background and Introduction

INTRODUCTION

The European Parliament and Council adopted Directive 2000/36/EC on 23 June 2000. The aim of the Directive was to allow the use of up to 5% of a limited number of vegetable fats in the production of chocolate. The objective of the Directive was to simplify Community provisions concerning chocolate with a view to allowing the free movement of chocolate products within the Internal Market. Member States were obliged to enact the Directive by August 2003.

The vegetable fats that were permitted for use required strict technical characteristics as set out in Annex II of the Directive and were limited to six (Illipe, palm oil, sal, shea, kokum gurgi, and mango kernel), see Table 1.1. Five of these (illipe, sal, shea, kokum gurgi and mango kernel) can be classed as exotic fats; that is, the fat is obtained from the seeds/nuts of trees that are mainly growing wild in the tropics.

Table 1.1: Permitted Fats and Main Producing Countries

Fat Main regions of production

Shea butter West Africa Illipe fat South East Asia Sal fat India Kokum gurgi oil India Mango kernel oil India Palm oil South East Asia

Source: EU Directive and LMC

Prior to the passing of the Directive, eight of the EU-15 countries prohibited the use of vegetable fats in chocolate production; namely, Germany, France, Netherlands, Belgium, Luxembourg, Italy, Greece and Spain. If the chocolate manufacturers changed their recipes for products sold in these markets, there would be two direct outcomes upon producers:

For cocoa producers, a loss of market; and

For producers of the other vegetable fats, an increase in demand.

This study provides an evaluation of the impact of the Directive as required under the Directive. The aim of the evaluation is to:

Determine the impact of Directive 2000/36/EC on the economies of those countries producing cocoa and vegetable fats other than cocoa butter; and

Provide guidance to the Commission on whether or not to amend the list of vegetable fats other than cocoa butter that are permitted for use in chocolate. In this regard, three options are considered:

CHAPTER 1: BACKGROUND AND INTRODUCTION PAGE 2

© LMC International Ltd, 2006

― To maintain the list for a further period of time, until the impact of the use of vegetable fats other than cocoa butter on the economies of developing countries can be further assessed.

― To shorten the list, assessing whether this may lead to a reduction of the quantities of vegetable fats other than cocoa butter in the production of chocolate.

― To extend the list, considering which other vegetable fats other than cocoa butter from developing countries could be allowed for use in the manufacture of chocolate.

The report is in eight chapters. Chapter 1 outlines the scope of the evaluation, presents a background to the manufacture of CBEs and discusses the implementation of the Directive in the individual member states; Chapter 2 examines trends in EU chocolate production and consumption; Chapter 3 presents trends in cocoa bean and product imports; while Chapter 4 discusses trends in the importation of the permitted vegetable fats. Chapter 5 examines what has happened in the chocolate industry since the introduction of the Directive, and Chapters 6 and 7 discuss the impact of the Directive on cocoa and vegetable oils producers, respectively. Chapter 8 presents the conclusions and recommendations.

CBE MANUFACTURE

In this report, we refer to blends of the permitted fats as cocoa butter equivalents (CBEs). CBEs are fats, which behave like and are compatible with cocoa butter in any proportion. For a product to be called chocolate in the EU the proportion of CBEs used cannot exceed 5% of the chocolate and the choice of fat is limited to the above.

Furthermore, all the fats have to comply with the following criteria:

1. They are non-lauric fats which are rich in symmetrical triglycerides of the type POP, POS, SOS;

2. They are miscible in any proportion with cocoa butter and are compatible with its physical properties (melting point and crystallisation temperature, melting rate and need for a tempering phase);

3. They are obtained only by the process of refining and/or fractionation, which excludes enzymatic modification of the triglyceride structure1.

The choice of fat blend used in a particular CBE is dependent upon the end use of that CBE. A standard CBE would typically contain 50% of an exotic fat or its fraction and 50% palm oil mid-fraction (PMF). However, technical improvements in the production of CBEs mean that they are becoming increasingly specialised according to the requirements of end users: where a CBE is being used as a Cocoa Butter Improver (CBI), to increase the hardness of a product for instance, the proportion of the exotic fat used will be higher; where the CBE is being used in a reformulation of the whole fat phase to achieve specific desirable functional properties, the proportion of PMF will probably be higher.

1 Specifically this prohibits interesterification, which can be used to transform the properties of palm oil.

CHAPTER 1: BACKGROUND AND INTRODUCTION PAGE 3

© LMC International Ltd, 2006

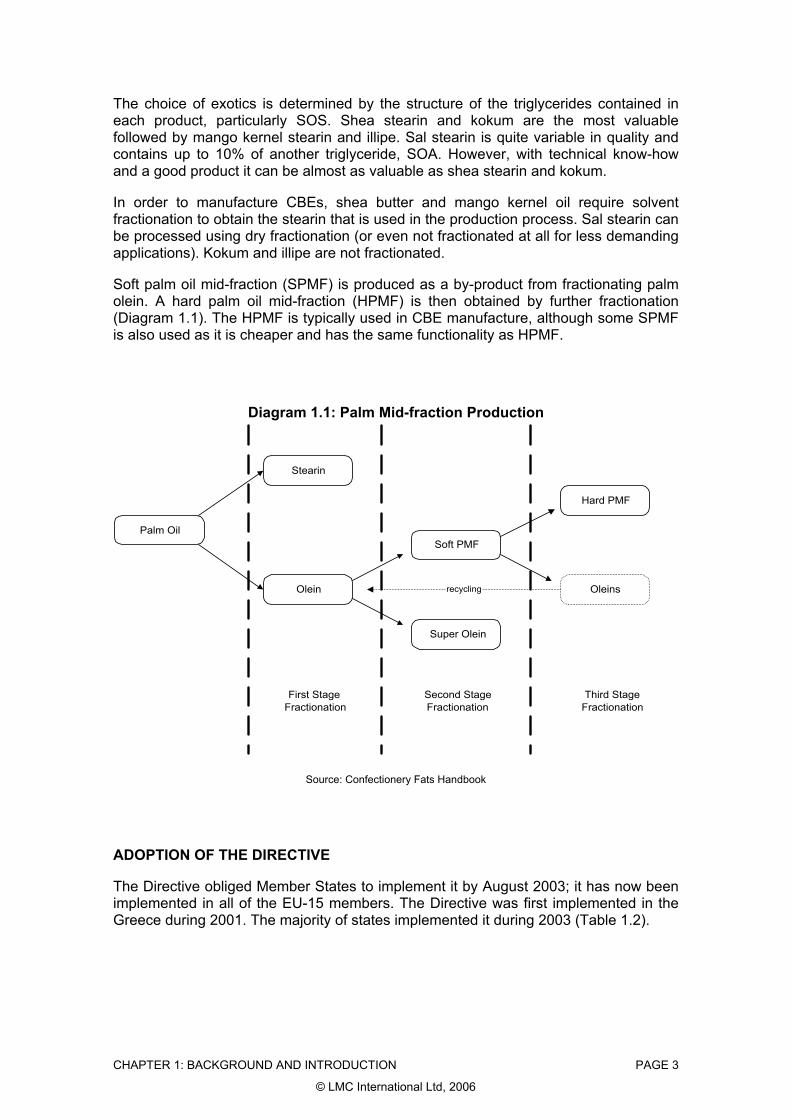

The choice of exotics is determined by the structure of the triglycerides contained in each product, particularly SOS. Shea stearin and kokum are the most valuable followed by mango kernel stearin and illipe. Sal stearin is quite variable in quality and contains up to 10% of another triglyceride, SOA. However, with technical know-how and a good product it can be almost as valuable as shea stearin and kokum.

In order to manufacture CBEs, shea butter and mango kernel oil require solvent fractionation to obtain the stearin that is used in the production process. Sal stearin can be processed using dry fractionation (or even not fractionated at all for less demanding applications). Kokum and illipe are not fractionated.

Soft palm oil mid-fraction (SPMF) is produced as a by-product from fractionating palm olein. A hard palm oil mid-fraction (HPMF) is then obtained by further fractionation (Diagram 1.1). The HPMF is typically used in CBE manufacture, although some SPMF is also used as it is cheaper and has the same functionality as HPMF.

Diagram 1.1: Palm Mid-fraction Production

Palm OilSoft PMF

Olein

Stearin

Super Olein

Hard PMF

Third StageFractionation

Second StageFractionation

First StageFractionation

Oleinsrecycling

Source: Confectionery Fats Handbook

ADOPTION OF THE DIRECTIVE

The Directive obliged Member States to implement it by August 2003; it has now been implemented in all of the EU-15 members. The Directive was first implemented in the Greece during 2001. The majority of states implemented it during 2003 (Table 1.2).

CHAPTER 1: BACKGROUND AND INTRODUCTION PAGE 4

© LMC International Ltd, 2006

Table 1.2: Implementation of Directive 2000/36/EC

Date of Implementation

UK 03-Aug-03 Sweden 03-Aug-03 Greece 01-Feb-01 Denmark 03-Aug-03 Belgium 29-Mar-03 France 29-Jul-03 Ireland 11-Jun-03 Austria 30-Dec-03 Germany 15-Dec-03 Luxembourg 25-Jul-03 Netherlands 02-Nov-01 Finland 03-Aug-03 Portugal 27-Sep-03 Spain 03-Aug-03 Italy 03-Aug-03

Note: In Germany, manufacturers were able to maintain recipes for 6 months after the implementation of the Directive. In Italy, the regulations contained a provision for "pure chocolate".

Source: National Regulation.

The regulations cover all chocolate products packaged after the date of adoption of the Directive. For products containing vegetable fats the product needs to be labelled “contains vegetable fats in addition to cocoa butter”. This labelling only appears after the date of implementation, hence for a period two differently labelled products appeared side by side on supermarket shelves; products that were packaged before the implementation date and those packaged afterwards. How long this occurred for depends on the distribution of chocolate production during the year and the shelf life of chocolate products. For example, assuming that production was equally distributed throughout the year and that the shelf life of a product is 12 months, newly packaged products would appear side by side for a 12-month period, with the proportion of old packaged products declining over time (Diagram 1.2).

CHAPTER 1: BACKGROUND AND INTRODUCTION PAGE 5

© LMC International Ltd, 2006

Diagram 1.2: Labelling Requirements

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

J F M A M J J A S O N D J

Labe

ls a

s a

% o

f Mar

ket

New labels Old Labels

For the purpose of this evaluation, we assume that the Directive was fully implemented by the end of 2003 and we compare the position before and after 2003.

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 6

© LMC International Ltd, 2006

Chapter 2: EU Chocolate Consumption and Production

This chapter examines chocolate consumption and production trends in the EU over the reporting period. The first part of the chapter considers the EU-15, while the second part considers the EU-10 accession states.

EU-15

Chocolate Product Consumption

Data on chocolate product1 production and consumption to 2004 were provided by Caobisco. These data were supplemented by consumer market research data for the major markets for 2005. For the other smaller markets, we assume that consumption continues to follow its longer term trend. Trade data are from Eurostat.

EU-15 consumption of chocolate products is around 2.2 million tonnes. There has been little change in total consumption since the Directive was adopted in 2003, although there are variations between countries (Diagram 2.1). Four markets, UK, Germany, Italy and France account for close to 80% of EU-15 chocolate consumption. Per capita consumption levels are highest in UK, Ireland and Germany (Diagram 2.2).

1 Chocolate products are defined as chocolate confectionery i.e., the chocolate plus the filling or other non-

chocolate components, i.e., added fruit and nuts. This comprises the Caobisco categories of unfilled bars, filled bars, bonbon, and sugar containing cocoa.

Table 2.1: EU-15 Chocolate Consumption (tonnes)

1996 2000 2001 2002 2003 2004 2005 Annual Growth since 2003

Annual Growth 5 years

Annual Growth 10 years

UK 487,415 491,516 475,981 509,241 530,226 529,187 500,381 -1.9% 1.0% 0.3% Austria 70,235 50,013 60,183 53,225 49,688 54,322 53,676 2.6% -2.3% -2.7% Sweden 52,265 56,708 59,239 60,899 58,173 59,742 58,447 0.2% -0.3% 1.1% Ireland 30,458 31,839 30,726 32,827 35,192 34,460 33,426 -1.7% 1.7% 0.9% Finland 18,245 27,942 30,511 30,364 31,157 32,289 32,612 1.5% 1.3% 6.0% Denmark 38,575 40,942 42,971 44,217 40,977 42,594 41,596 0.5% -0.6% 0.8% Portugal 11,660 21,229 24,598 25,213 21,695 19,237 20,500 -1.9% -3.6% 5.8% Germany 689,620 677,128 666,786 670,859 661,870 681,941 668,746 0.3% 0.1% -0.3% France 270,405 297,435 287,510 287,990 280,616 280,231 285,064 0.5% -0.2% 0.5% Netherlands 70,395 76,105 74,900 74,200 71,300 73,100 73,300 0.9% -0.4% 0.4% Italy 150,730 162,932 169,959 183,821 191,570 196,915 202,490 1.9% 3.6% 3.0% Belgium 55,225 60,863 49,072 63,612 68,295 71,545 70,912 1.3% 7.6% 2.5% Spain 64,175 61,025 64,250 64,655 65,285 68,235 71,874 3.3% 2.3% 1.1% Greece 24,700 29,045 30,591 32,502 34,781 37,131 39,226 4.1% 5.1% 4.7% Total 2,034,103 2,084,721 2,067,278 2,133,625 2,140,824 2,180,927 2,152,250 0.2% 0.8% 0.6%

Source: CAOBISCO, Market Research Data, LMC.

CH

AP

TER

2: EU

CH

OC

OLA

TE C

ON

SUM

PTIO

N A

ND

PR

OD

UC

TION

P

AG

E 7

© LM

C International Ltd, 2006

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 8

© LMC International Ltd, 2006

Diagram 2.1: Change in Consumption 2003 v 2005

-3% -2% -1% 0% 1% 2% 3% 4% 5%

UK

Austria

Sweden

Ireland

Finland

Denmark

Portugal

Germany

France

Netherlands

Italy

Belgium

Spain

Greece

Total

Consumption Change since 2003 (%)

Diagram 2.2: Per Capita Chocolate Consumption, 2005

0

1

2

3

4

5

6

7

8

9

Spain

Portug

alIta

ly

Greece

Netherl

ands

France

Finlan

d

Sweden

Austria

Belgium

Denmark

German

y

Irelan

d UK

Per c

apita

con

sum

ptio

n (k

g)

There are a number of reasons for the slow growth in consumption:

Slow growth in income. Per capita consumption is related to per capita incomes and the slow growth of incomes in recent years has adversely affected demand;

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 9

© LMC International Ltd, 2006

In some of the mature markets, the market is saturated; and

Increasing concerns over obesity.

Not all segments of the market have experienced the same level of growth. There has been growth in whole bar (tablet) consumption which has been driven by campaigns highlighting the benefits of cocoa consumption. This is due to the presence of the antioxidant flavanol which has been found to reduce blood pressure. In addition, there has been growth in speciality/gourmet products, such as single origin and dark chocolate. Both of these products have a higher cocoa content and are positioned as premium products with a higher price.

The strongest growth, albeit from a low base, has been for the small bite segment (Table 2.2 and Diagram 2.3).

Table 2.2: Consumption by Type, UK, Germany, France and Italy (tonnes)

2003 2004 2005

Tablets 446,230 458,289 449,096 Bars 435,069 429,092 407,497 Box/pralines 244,374 252,183 243,388 Small bites 120,319 125,234 131,583 Seasonal/selection 196,867 200,935 195,562 Total 1,442,859 1,465,733 1,427,126

Source: Market Research Data

Diagram 2.3: Consumption by Type

85

90

95

100

105

110

115

2003 2004 2005

cons

umpt

ion

Inde

x (2

003

= 10

0)

Tablets Bars Box/pralines Small bites Seasonal/selection

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 10

© LMC International Ltd, 2006

Chocolate Product Trade

Increasing volumes of chocolate products are being shipped around the EU-15 as the confectionery industry consolidates. This is due to the economies of scale in the production of chocolate products. The volume of intra-regional trade (i.e., trade between the EU-15 member states) increased from 624,000 tonnes to 834,000 tonnes between 1997 and 2004. The traded volume fell back in 2005 (Diagram 2.4). This means that there is increasing dislocation of consumption and production.

Diagram 2.4: Intra-EU Chocolate Product Trade

500

550

600

650

700

750

800

850

900

1997 1998 1999 2000 2001 2002 2003 2004 2005

Intra

-EU

Impo

rts (0

00 to

nnes

)

The EU-15 is a net exporter of chocolate products. Net exports (to countries outside of the EU-15) fell substantially in 1997 and 1998 as exports to Eastern Europe declined. However, since then net exports have remained stable at around 140,000 tonnes per annum (Diagram 2.5)

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 11

© LMC International Ltd, 2006

Diagram 2.5: Net EU-15 Exports

100

150

200

250

300

350

1997 1998 1999 2000 2001 2002 2003 2004 2005

Intra

-EU

Impo

rts (0

00 to

nnes

)

Chocolate Product Production

Chocolate product production is defined as:

Production = Consumption + Exports – Imports.

Table 2.3 highlights the major trends. Total EU-15 production has been unchanged since the adoption of the Directive, although this hides trends in individual countries. Of the major producers production has fallen by 5% in the UK as imports have increased.

Table 2.3: EU-15 Chocolate Production (tonnes)

1996 2000 2001 2002 2003 2004 2005 Annual Growth since 2003

Annual Growth 5 years

Annual Growth 10 years

UK 515,620 473,255 469,300 464,245 482,238 459,637 406,375 -5.5% -2.8% -2.4% Austria 55,640 56,860 63,030 56,175 55,285 55,160 58,807 2.1% -1.4% 0.6% Sweden 52,265 52,075 51,650 50,325 47,970 45,027 46,144 -1.3% -2.2% -1.2% Ireland 59,823 58,473 56,811 68,563 75,109 63,640 59,962 -7.2% 1.1% 0.0% Finland 35,105 33,910 34,080 34,050 33,015 32,395 31,518 -1.5% -1.6% -1.1% Denmark 20,130 24,440 27,550 25,795 25,660 28,195 28,827 4.0% 0.9% 3.7% Portugal 2,465 2,305 2,800 1,545 1,040 1,230 1,262 6.7% -14.7% -6.5% Germany 811,871 719,175 730,660 751,410 753,208 798,599 786,169 1.4% 1.5% -0.3% France 282,335 275,971 275,403 281,061 264,626 284,050 268,146 0.4% -0.5% -0.5% Netherlands 173,205 185,866 188,597 182,353 180,387 162,498 185,265 0.9% -0.4% 0.7% Italy 166,655 165,800 174,300 189,550 193,800 201,500 204,047 1.7% 3.2% 2.0% Belgium 131,515 173,665 171,605 195,850 196,405 218,765 214,866 3.0% 4.6% 5.0% Spain 69,565 38,615 46,165 50,780 47,149 52,460 62,678 10.0% 6.3% -1.0% Greece 22,300 20,700 21,000 21,200 22,000 22,500 26,675 6.6% 4.9% 1.8% Total 2,398,494 2,281,110 2,312,950 2,372,902 2,377,893 2,425,656 2,380,741 0.0% 0.6% -0.1%

Source: LMC

CH

AP

TER

2: EU

CH

OC

OLA

TE C

ON

SUM

PTIO

N A

ND

PR

OD

UC

TION

P

AG

E 12

© LM

C International Ltd, 2006

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 13

© LMC International Ltd, 2006

RETAIL CHOCOLATE PRICES

Of the major EU chocolate producers, retail price data (as collected for consumer price indices) only include chocolate in two cases: France and Germany. These data suggest the real prices have risen by 1.5% per annum in Germany, but have fallen by 1.2% per annum in France since the adoption of the Directive.

Diagram 2.6: France Chocolate Retail Price Index

90

95

100

105

110

115

120

125

130

135

140

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Pric

e In

dex

(199

6=10

0)

Nominal Price Real Price

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 14

© LMC International Ltd, 2006

Diagram 2.7: Germany Milk Chocolate Retail Price Index

80

90

100

110

120

130

140

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Pric

e In

dex

(199

6=10

0)

Nominal Price Real Price

CENTRAL AND EASTERN EUROPE

Confectionery markets are growing more quickly in the EU-10 accession countries than is the case in the EU-15. Poland is the hub, both in terms of consumption and production. There has also been an increase in the export of chocolate products.

Chocolate Consumption

The chocolate confectionery market in the Central European member states is estimated at around 200,000 tonnes in 2005, having grown by 3% per year on average over the last five years. The most rapid growth has been in Poland, which is also by far the largest market, accounting for approaching 100,000 tonnes (Table 2.4 and Diagram 2.8).

Table 2.4: Central European Member States — Chocolate Product Consumption (tonnes)

1999 2001 2001 2002 2003 2004 2005 Growth 5 years

Czech Rep 28,096 29,032 30,000 31,000 32,000 33,000 33,000 2% Poland 69,342 72,115 75,000 78,000 80,000 89,000 97,000 5% Hungary 35,078 36,026 37,000 38,000 39,000 39,000 40,000 2% Slovakia 20,000 20,000 20,000 20,000 20,000 20,000 21,000 1% Slovenia 6,652 6,484 6,324 6,755 6,998 6,289 7,328 3% Total 159,168 163,658 168,324 173,755 177,998 187,289 198,328 3%

Source: NCA, LMC.

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 15

© LMC International Ltd, 2006

Diagram 2.8: Central European Member States — Chocolate Product Consumption

0

20

40

60

80

100

120

140

160

180

200

1999 2001 2001 2002 2003 2004 2005

Sale

s ('0

00 to

nnes

)

Poland Hungary Czech Rep Slovakia Slovenia

Chocolate Trade

As is the case with the EU-15, there is an increasing volume of trade in chocolate confectionery products between both within the EU-10 (particularly the Central European member states) and with the EU-15. Poland is becoming the regional hub and has become a significant net exporter. This is partly the influence of the EU-15 chocolate manufacturers who over the last ten years have made significant acquisitions in the market and are using the country as a base for production for both the local market and for export.

Net chocolate exports by Poland have grown from below 16,000 tonnes in 2001 to almost 35,000 tonnes in 2005, an average annual increase of 17%. Over the same period, net imports by Hungary, the Czech Republic and Slovenia have risen by an average of 13% per year (Table 2.5 and Diagram 2.9).

Table 2.5: Central European Member States — Chocolate Trade (tonnes)

1999 2001 2001 2002 2003 2004 2005 Growth 5 years

Net Exports Poland 10,317 16,759 15,695 11,809 10,008 28,883 34,955 17% Slovakia -252 822 1,535 2,032 2,108 5,373 3,622 19% Total 10,065 17,581 17,230 13,841 12,116 34,256 38,577 17%

Net Imports Hungary -3,600 -1,191 -8,384 -7,056 -842 -10,652 -14,106 11% Czech Rep -7,312 -7,125 -4,252 -8,040 -9,682 -10,494 -12,848 25% Slovenia -6,652 -6,484 -6,324 -6,755 -6,998 -6,289 -7,328 3% Total -17,565 -14,800 -18,960 -21,851 -17,523 -27,435 -34,283 13%

Source: Eurostat.

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 16

© LMC International Ltd, 2006

Diagram 2.9: Central European Member States — Chocolate Trade

-20,000 -10,000 0 10,000 20,000 30,000 40,000

Poland

Slovakia

Hungary

Czech Rep

SloveniaN

et E

xpor

tsN

et Im

ports

Chocolate Trade (tonnes)

1999 2001 2001 2002 2003 2004 2005

Chocolate Production

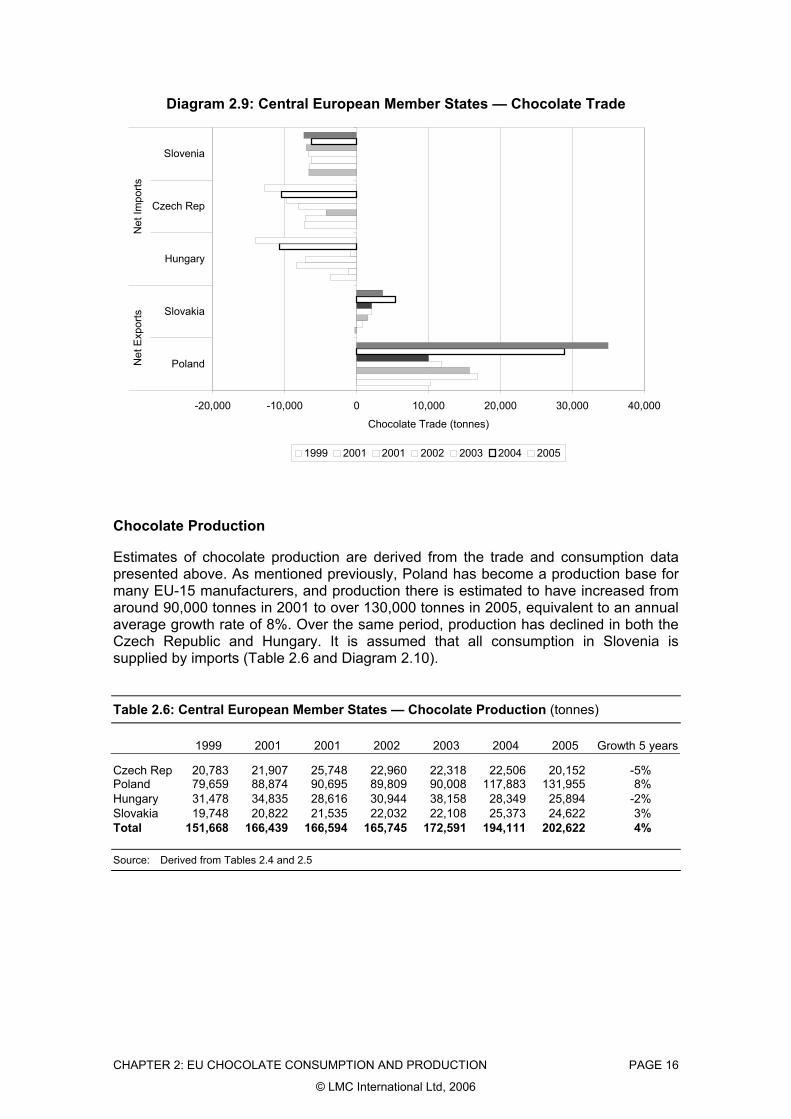

Estimates of chocolate production are derived from the trade and consumption data presented above. As mentioned previously, Poland has become a production base for many EU-15 manufacturers, and production there is estimated to have increased from around 90,000 tonnes in 2001 to over 130,000 tonnes in 2005, equivalent to an annual average growth rate of 8%. Over the same period, production has declined in both the Czech Republic and Hungary. It is assumed that all consumption in Slovenia is supplied by imports (Table 2.6 and Diagram 2.10).

Table 2.6: Central European Member States — Chocolate Production (tonnes)

1999 2001 2001 2002 2003 2004 2005 Growth 5 years

Czech Rep 20,783 21,907 25,748 22,960 22,318 22,506 20,152 -5% Poland 79,659 88,874 90,695 89,809 90,008 117,883 131,955 8% Hungary 31,478 34,835 28,616 30,944 38,158 28,349 25,894 -2% Slovakia 19,748 20,822 21,535 22,032 22,108 25,373 24,622 3% Total 151,668 166,439 166,594 165,745 172,591 194,111 202,622 4%

Source: Derived from Tables 2.4 and 2.5

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 17

© LMC International Ltd, 2006

Diagram 2.10: Central European Member States — Chocolate Production

0

20

40

60

80

100

120

140

1999 2001 2001 2002 2003 2004 2005

Prod

uctio

n ('0

00 to

nnes

)

Poland Hungary Slovakia Czech Rep

The derived production estimates are supported by the Prodcom data, which also show how production is broken down by type in Poland and Hungary. In Poland, production of unfilled bars (which account for over half of total output) and bonbons grew by an annual average of 13% between 2002 and 2004. In Hungary, the data suggests a sharp fall in chocolate bar production (Table 2.7 and Diagram 2.11).

Table 2.7: Poland and Hungary — Chocolate Production by Type (tonnes)

2002 2003 2004 Growth 3 Years

Poland Unfilled Bars 46,750 52,822 67,885 13% Filled Bars 23,063 25,183 28,878 8% Bonbons 16,722 22,557 24,406 13%

Hungary Unfilled Bars 10,158 8,824 3,707 -29% Filled Bars 10,706 8,481 5,392 -20% Bonbons 6,519 8,353 8,405 9%

Source: Prodcom.

CHAPTER 2: EU CHOCOLATE CONSUMPTION AND PRODUCTION PAGE 18

© LMC International Ltd, 2006

Diagram 2.11: Poland and Hungary — Chocolate Production by Type

0

10

20

30

40

50

60

70

Unfilled Bars Filled Bars Bonbons Unfilled Bars Filled Bars Bonbons

Poland Hungary

Prod

uctio

n ('0

00 to

nnes

)

2002 2003 2004

The data point to strong growth in chocolate production in Poland over the last few years as EU-15 manufacturers have established their operations there. However, there is considerable over-capacity in the Polish market and a degree of consolidation is taking place:

In 2005, Nestlé Polska sold its Poznan production facility (which manufactures Goplana brand confectionery) to a local manufacturer, Jutrzenka;

In 2005, the Swedish manufacturer Cloetta Fazer closed its Polish subsidiary in Gdansk due to falling sales;

In 2006, Barry Callebaut announced plans to construct a 25,000 tonne chocolate factory in Russia, a market that it had previously supplied from its Polish plant.

CHAPTER 3: THE EU MARKET FOR COCOA PAGE 19

© LMC International Ltd, 2006

Chapter 3: The EU Market for Cocoa

As cocoa and the vegetable fats used in the manufacture of chocolate are produced outside of the EU, import data can be used to gain an indication of the market size. This chapter examines trends in both cocoa and cocoa product imports, while the following chapter examines the imports of the vegetable fats permitted for use in chocolate.

NET IMPORTS

The EU imports cocoa beans as well as cocoa mass (liquor), cocoa butter and cocoa powder/cake. In order to determine the level of net imports on a consistent basis, cocoa product imports have to be converted to a cocoa bean equivalent. For this, we have used the ICCO’s standard conversions1.

Net imports of cocoa beans and cocoa products in bean equivalent (b.e.) terms from outside the EU-15 countries have increased from around 1.2 million tonnes in 1996 to over 1.4 million tonnes in 2005, recording an average annual growth rate of 2.1% over the last 10 years. Since 2003, the growth rate has increased to 3.5%; almost all of this growth occurred in 2005. The major EU-15 importers are the Netherlands (accounting for 38% of net imports in 2005), France (16%), Belgium (14%) and the UK (10%). Net imports into Belgium have grown by 16% per year since 2003, while German and Italian net imports have fallen (Table 3.1 and Diagram 3.1).

1 The ICCO conversions are: Beans: liquor /mass/paste 1.25:1 Beans: butter 1.33:1 Beans: powder/cake 1.18:1

Table 3.1: Net Imports of Cocoa Beans and Cocoa Products by Major EU-15 Importers (tonnes b.e.)

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Annual Growth since 2003

Belgium (and Luxembourg) 55,222 87,379 92,962 47,139 105,001 92,496 123,981 122,463 148,399 190,842 15.9% France 172,996 134,467 141,070 164,282 169,436 195,709 176,114 197,999 217,498 214,683 2.7% Germany 188,195 185,615 182,347 161,424 159,844 143,441 134,032 134,951 104,271 134,321 -0.2% Italy 74,937 69,756 68,206 65,821 73,285 66,221 53,303 70,448 59,036 60,836 -4.8% Netherlands 383,902 211,688 243,741 437,294 369,189 471,517 392,195 517,750 514,723 549,120 2.0% Spain 53,921 62,527 69,988 72,494 72,735 77,007 82,019 82,915 86,258 94,789 4.6% UK 197,513 144,571 171,663 217,090 128,707 139,052 121,820 135,244 140,603 139,546 1.0% Other EU-15 27,684 33,887 33,336 17,865 28,139 15,815 17,372 11,673 14,388 27,794 33.5% Total EU-15 1,154,370 929,889 1,003,312 1,183,410 1,106,335 1,201,257 1,100,836 1,273,444 1,285,176 1,411,931 3.5%

Source: Eurostat.

CH

AP

TER

3: THE

EU

MA

RK

ET FO

R C

OC

OA

P

AG

E 20

© LM

C International Ltd, 2006

CHAPTER 3: THE EU MARKET FOR COCOA PAGE 21

© LMC International Ltd, 2006

Diagram 3.1: Total EU-15 Net Imports of Cocoa Beans and Cocoa Products

0

200

400

600

800

1,000

1,200

1,400

1,600

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Net

Coc

oa Im

ports

('00

0 to

nnes

b.e

.)

Total Trend

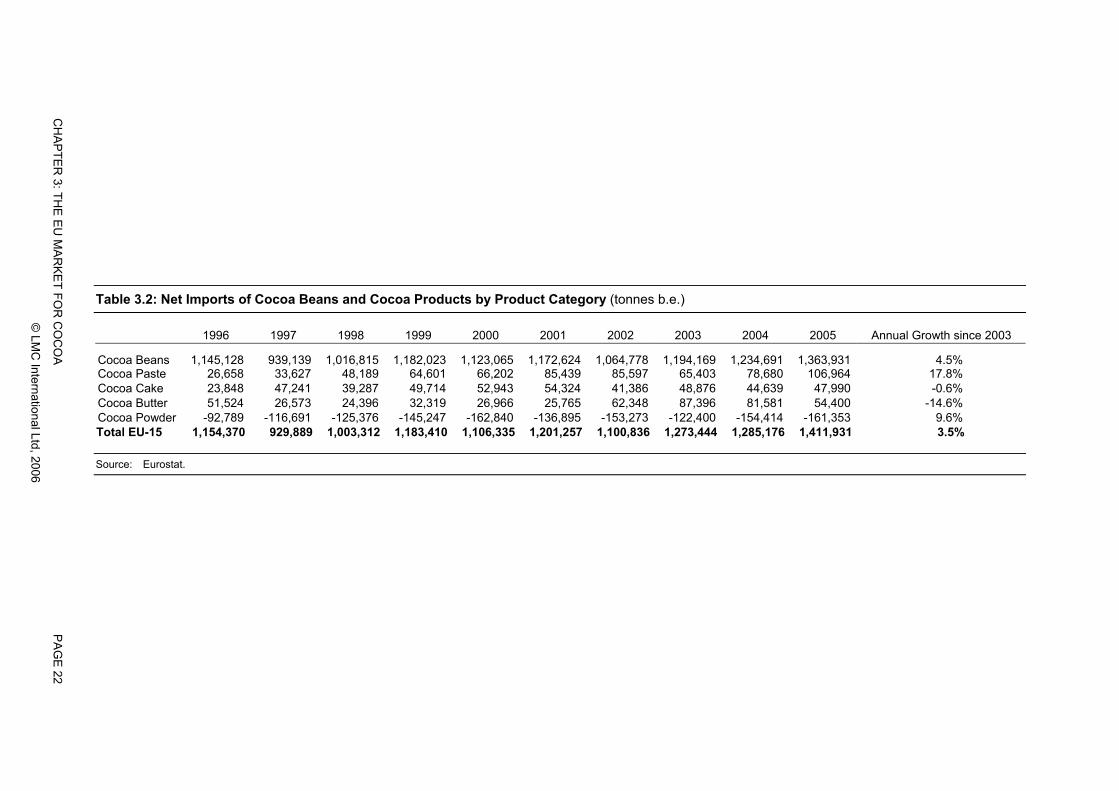

The majority of EU-15 cocoa imports are in the form of raw beans. Cocoa product imports, particularly of paste, have grown more rapidly, mainly due to the increase in downstream processing in producing countries such as Côte d’Ivoire. The EU-15 is a net exporter of cocoa powder (Table 3.2).

This growth in processing at origin has been led by the multinational cocoa processors increasing their investment at origin. These products can be incorporated into standard blends and the companies have invested in good quality control procedures that ensure that bacterial contamination, particularly of paste products, can be avoided.

Factors that have encouraged this downstream processing are:

Access to beans, including the lower quality mid-crop beans, which can be obtained at a discount. In Côte d’Ivoire though, over the last two years, high demand has forced the price of mid-crop beans upwards;

Advantageous export tax rates for processed products;

Investment incentives; and

Lower average shipping costs as shell is not being exported.

Table 3.2: Net Imports of Cocoa Beans and Cocoa Products by Product Category (tonnes b.e.)

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Annual Growth since 2003

Cocoa Beans 1,145,128 939,139 1,016,815 1,182,023 1,123,065 1,172,624 1,064,778 1,194,169 1,234,691 1,363,931 4.5% Cocoa Paste 26,658 33,627 48,189 64,601 66,202 85,439 85,597 65,403 78,680 106,964 17.8% Cocoa Cake 23,848 47,241 39,287 49,714 52,943 54,324 41,386 48,876 44,639 47,990 -0.6% Cocoa Butter 51,524 26,573 24,396 32,319 26,966 25,765 62,348 87,396 81,581 54,400 -14.6% Cocoa Powder -92,789 -116,691 -125,376 -145,247 -162,840 -136,895 -153,273 -122,400 -154,414 -161,353 9.6% Total EU-15 1,154,370 929,889 1,003,312 1,183,410 1,106,335 1,201,257 1,100,836 1,273,444 1,285,176 1,411,931 3.5%

Source: Eurostat.

CH

AP

TER

3: THE

EU

MA

RK

ET FO

R C

OC

OA

P

AG

E 22

© LM

C International Ltd, 2006

CHAPTER 3: THE EU MARKET FOR COCOA PAGE 23

© LMC International Ltd, 2006

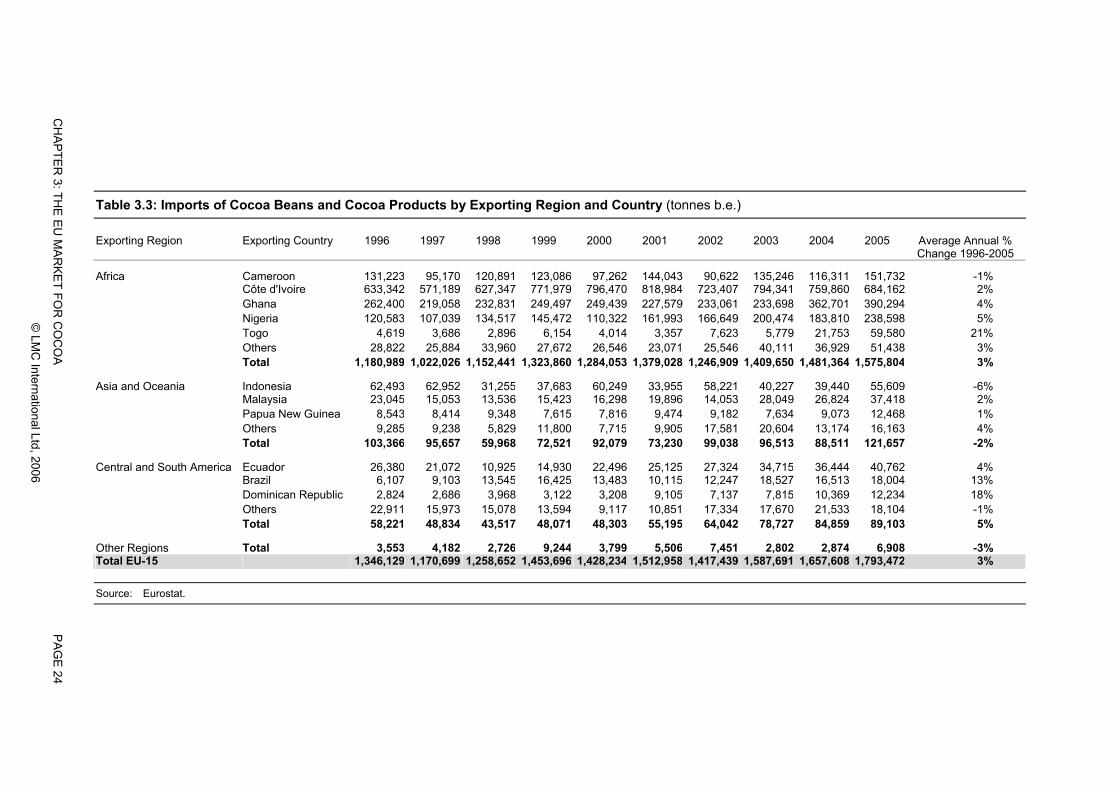

IMPORTS BY ORIGIN

The majority of EU-15 cocoa imports are from West Africa, which supplied approaching 1.6 million tonnes of beans and cocoa products in 2005. Côte d’Ivoire alone accounted for 33% of total 2005 imports, with three other West African origins (Ghana, Nigeria and Cameroon) accounting for a further 49%. Imports from Central and South America have grown by an average of 5% per year, although the region’s import share is still only 5%, similar to that of Asia and Oceania (Table 3.3).

Over the reporting period, imports from Côte d’Ivoire as a proportion of total imports peaked in 2000 and have fallen since. Exports from other West African producers have increased to compensate (Diagram 3.2).

In any one year changes in imports by country, on top of the underlying trend growth, can be attributed to:

Statistical error;

Seasonal fluctuation in the timing of the crop: for instance, as the crop is harvested towards the end of a calendar year, an early crop could see an increase in imports in December as opposed to January; and

Cross-border movements: There has long been a trade in cocoa between Ghana and East Côte d’Ivoire, with the direction of the trade depending upon relative prices. In addition, the rise in imports from Togo since 2003 is largely attributed to increased smuggling from Côte d’Ivoire.

Table 3.3: Imports of Cocoa Beans and Cocoa Products by Exporting Region and Country (tonnes b.e.) Exporting Region Exporting Country 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Average Annual %

Change 1996-2005

Africa Cameroon 131,223 95,170 120,891 123,086 97,262 144,043 90,622 135,246 116,311 151,732 -1% Côte d'Ivoire 633,342 571,189 627,347 771,979 796,470 818,984 723,407 794,341 759,860 684,162 2% Ghana 262,400 219,058 232,831 249,497 249,439 227,579 233,061 233,698 362,701 390,294 4% Nigeria 120,583 107,039 134,517 145,472 110,322 161,993 166,649 200,474 183,810 238,598 5% Togo 4,619 3,686 2,896 6,154 4,014 3,357 7,623 5,779 21,753 59,580 21% Others 28,822 25,884 33,960 27,672 26,546 23,071 25,546 40,111 36,929 51,438 3% Total 1,180,989 1,022,026 1,152,441 1,323,860 1,284,053 1,379,028 1,246,909 1,409,650 1,481,364 1,575,804 3%

Asia and Oceania Indonesia 62,493 62,952 31,255 37,683 60,249 33,955 58,221 40,227 39,440 55,609 -6% Malaysia 23,045 15,053 13,536 15,423 16,298 19,896 14,053 28,049 26,824 37,418 2% Papua New Guinea 8,543 8,414 9,348 7,615 7,816 9,474 9,182 7,634 9,073 12,468 1% Others 9,285 9,238 5,829 11,800 7,715 9,905 17,581 20,604 13,174 16,163 4% Total 103,366 95,657 59,968 72,521 92,079 73,230 99,038 96,513 88,511 121,657 -2%

Central and South America Ecuador 26,380 21,072 10,925 14,930 22,496 25,125 27,324 34,715 36,444 40,762 4% Brazil 6,107 9,103 13,545 16,425 13,483 10,115 12,247 18,527 16,513 18,004 13% Dominican Republic 2,824 2,686 3,968 3,122 3,208 9,105 7,137 7,815 10,369 12,234 18% Others 22,911 15,973 15,078 13,594 9,117 10,851 17,334 17,670 21,533 18,104 -1% Total 58,221 48,834 43,517 48,071 48,303 55,195 64,042 78,727 84,859 89,103 5%

Other Regions Total 3,553 4,182 2,726 9,244 3,799 5,506 7,451 2,802 2,874 6,908 -3% Total EU-15 1,346,129 1,170,699 1,258,652 1,453,696 1,428,234 1,512,958 1,417,439 1,587,691 1,657,608 1,793,472 3%

Source: Eurostat.

CH

AP

TER

3: THE

EU

MA

RK

ET FO

R C

OC

OA

P

AG

E 24

© LM

C International Ltd, 2006

CHAPTER 3: THE EU MARKET FOR COCOA PAGE 25

© LMC International Ltd, 2006

Diagram 3.2: EU-15 Cocoa Imports % of Total

0%

10%

20%

30%

40%

50%

60%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Tota

l Im

ports

(%)

Cameroon Côte d'Ivoire Ghana NigeriaTogo Indonesia Ecuador Other

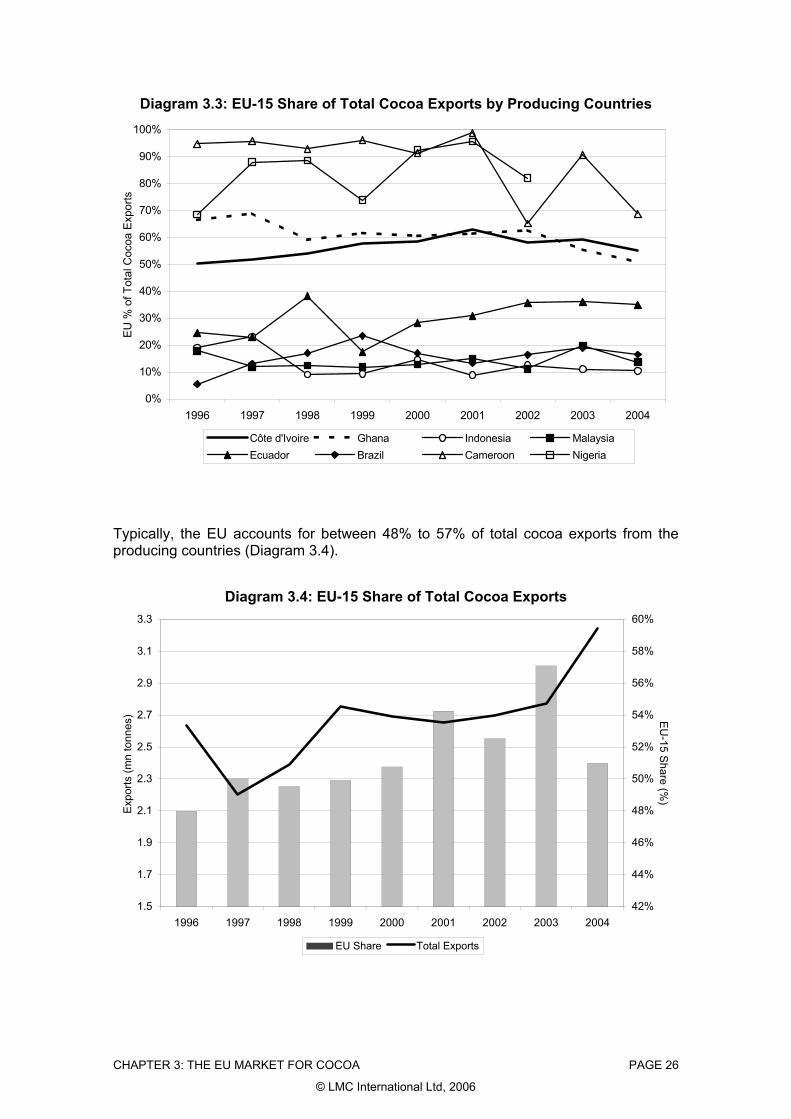

In order to illustrate the importance of the EU-15 markets to cocoa producing countries, a comparison has been made between the import data and export data mainly compiled from official sources by the International Cocoa Organisation (ICCO).

This analysis shows that, in the case of Cameroon and Nigeria, EU-15 imports typically account for around 80% of total cocoa exports, while for Côte d’Ivoire and Ghana, the share is over 50%. These are much higher shares than those for exports from Asian producers, such as Indonesia and Malaysia (both less than 20%), and from South American producers, such as Ecuador (less than 40%) and Brazil (less than 25%) (Diagram 3.3).

CHAPTER 3: THE EU MARKET FOR COCOA PAGE 26

© LMC International Ltd, 2006

Diagram 3.3: EU-15 Share of Total Cocoa Exports by Producing Countries

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1996 1997 1998 1999 2000 2001 2002 2003 2004

EU %

of T

otal

Coc

oa E

xpor

ts

Côte d'Ivoire Ghana Indonesia MalaysiaEcuador Brazil Cameroon Nigeria

Typically, the EU accounts for between 48% to 57% of total cocoa exports from the producing countries (Diagram 3.4).

Diagram 3.4: EU-15 Share of Total Cocoa Exports

1.5

1.7

1.9

2.1