the hon peter costello treasurer 2006-07 post-budget address

TRANSCRIPT

The Hon Peter CostelloTreasurer

2006-07 Post-Budget Address

Underlying cash balance

-3

-2

-1

0

1

2

3

1995-96 1999-00 2003-04 2007-08

-3

-2

-1

0

1

2

3

Ou

tco

me

s

Est

ima

tes

Pro

ject

ion

s

Per cent of GDP Per cent of GDP

General government sector net debt and net interest payments

-5

0

5

10

15

20

1981-82 1985-86 1989-90 1993-94 1997-98 2001-02 2005-06

-0.5

0.0

0.5

1.0

1.5

2.0

Net debt (LHS) Net interest payments (RHS)

Est

ima

tes

Ou

tco

me

s

Per cent of GDP Per cent of GDP

Ability to re-direct spending

0

10

20

30

40

1996-97 2006-07

0

10

20

30

40

Assistanceto families

with children

Hospitals& schools

Hospitals& schools

Assistanceto families

with children

Public debt interest

Public debtinterest

$billion $billion

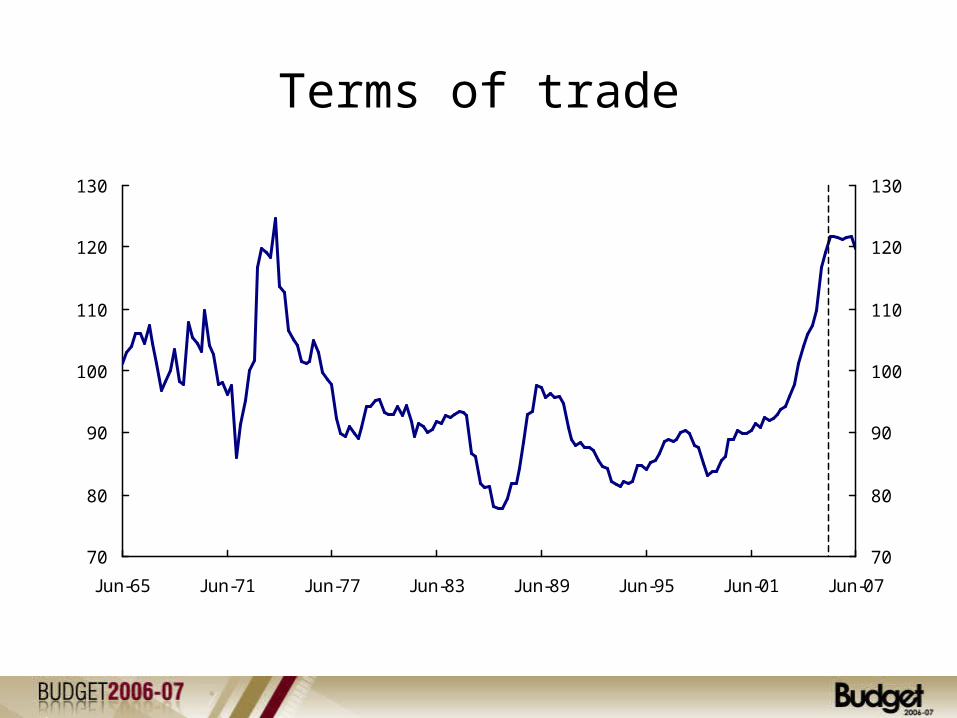

Terms of trade

70

80

90

100

110

120

130

Jun-65 Jun-71 Jun-77 Jun-83 Jun-89 Jun-95 Jun-01 Jun-07

70

80

90

100

110

120

130

Fo

reca

sts

Index (2003-04 = 100) Index (2003-04 = 100)

Personal income tax cuts

Current tax thresholds Tax rateIncome range ($) %0 - 6,000 06,001 - 21,600 1521,601 - 63,000 3063,001 - 95,000 4295,001 + 47

Current tax thresholds Tax rateIncome range ($) %0 - 6,000 06,001 - 21,600 1521,601 - 63,000 3063,001 - 95,000 4295,001 + 47

2005-06

• Low Income Tax Offset increase to $600 plus phase out from $25,000 (up from $21,600).

• Medicare levy phase-in halved.

New tax thresholds Tax rateIncome range ($) %0 - 6,000 06,001 - 25,000 1525,001 - 75,000 3075,001 - 150,000 40150,001 + 45

From 1 July 2006

Personal Income Tax Cuts

Income range Tax rate Income range Tax rate($) % ($) %0 - 5,400 0 0 - 6,000 05,401 - 20,700 20 6,001 - 25,000 15

20,701 - 38,000 34

38,001 - 50,000 43 25,001 - 75,000 30

50,001 + 4775,001 - 150,000 40150,001 + 45

1 July 1996 1 July 2006

Work incentives with income tax reform

0

10

20

30

40

50

60

70

80

90

100

10,000 30,000 50,000 70,000 90,000 110,000 130,000 150,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Tax savings - $ per year (RHS) Tax savings - percentage reduction (LHS)

Taxpayer's annual income ($)

Tax cut per year (% of tax paid) Tax cut per year ($)

A more competitive income tax system

0

2

4

6

8

10

12

Slo

vak

Re

pH

unga

ryIr

elan

dD

enm

ark

Luxe

mbo

urg

Bel

giu

mM

exic

oU

K

Ger

man

yN

eth

erla

nds

Ice

land NZ

Gre

ece

Sw

eden

Fin

land

Cze

ch R

epA

ustr

iaN

orw

ay

Tur

key

Spa

in

Fra

nce

Can

ada

Pol

and

Sw

itze

rland

Kor

ea

Japa

nP

ortu

gal

Ita

lyU

S

0

10

20

30

40

50

60

70

80

Australia (2004-05)Average

threshold = 2.4

Average top marginal tax rate = 46.7

Aus

tral

ia

Top threshold, multiple of the average wage (bars) Top marginal rate, per cent (dots)

A more competitive income tax system

0

2

4

6

8

10

12

Slo

vak

Re

pH

unga

ryIr

elan

dD

enm

ark

Luxe

mbo

urg

Bel

giu

mM

exic

oU

K

Ger

man

yN

eth

erla

nds

Ice

land NZ

Gre

ece

Sw

eden

Fin

land

Cze

ch R

epA

ustr

iaN

orw

ay

Tur

key

Spa

in

Fra

nce

Can

ada

Pol

and

Sw

itze

rland

Kor

ea

Japa

nP

ortu

gal

Ita

lyU

S

0

10

20

30

40

50

60

70

80

Australia (2004-05) Australia (2006-07)Average

threshold = 2.4

Average top marginal tax rate = 46.7

Aus

tral

ia

Aus

tral

ia

Top threshold, multiple of the average wage (bars) Top marginal rate, per cent (dots)

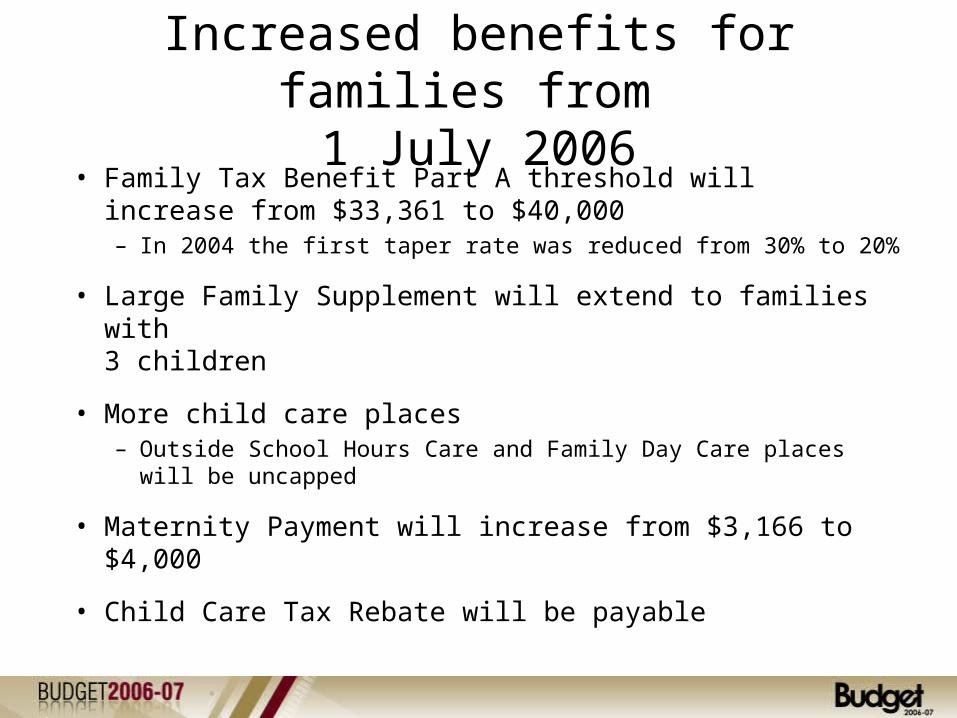

Increased benefits for families from 1 July 2006

• Family Tax Benefit Part A threshold will increase from $33,361 to $40,000– In 2004 the first taper rate was reduced from 30% to 20%

• Large Family Supplement will extend to families with 3 children

• More child care places– Outside School Hours Care and Family Day Care places will be

uncapped

• Maternity Payment will increase from $3,166 to $4,000

• Child Care Tax Rebate will be payable

Older Australians and carers

• One-off payment equal to Utilities Allowance ($102.80)– To pensioner households– To individual self-funded retirees– To households with recipients of Mature Age Allowance,

Partner Allowance, Widow Allowance

• Ongoing eligibility to Utilities Allowance extended to recipients of Mature Age Allowance, Partner Allowance and Widow Allowance– Six-monthly payments will commence in 2006-07

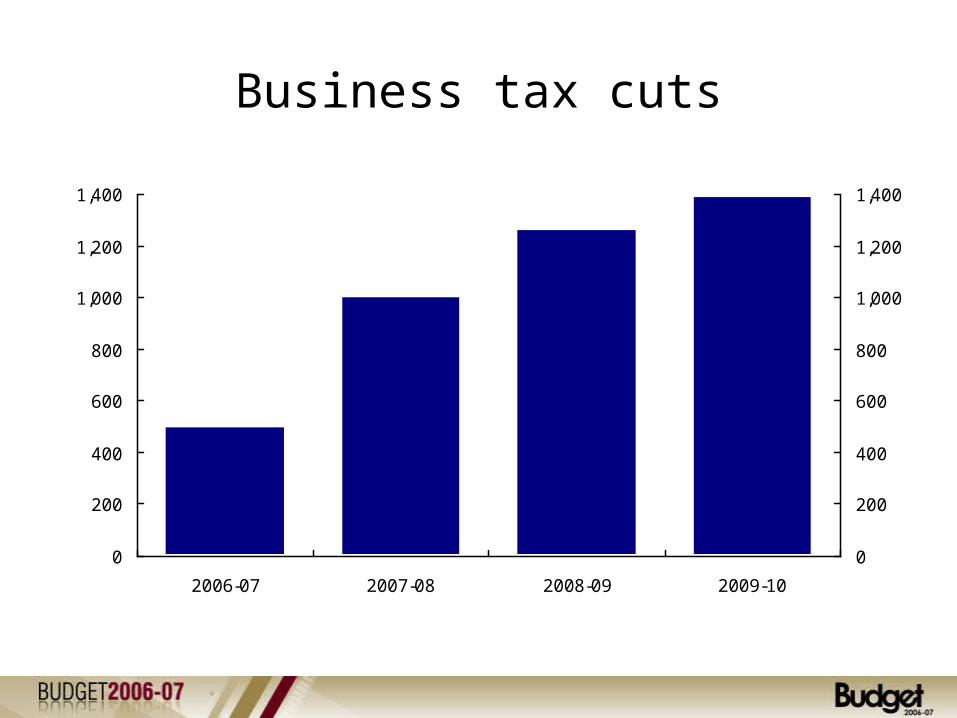

Business tax cuts

0

200

400

600

800

1,000

1,200

1,400

2006-07 2007-08 2008-09 2009-10

0

200

400

600

800

1,000

1,200

1,400$million $million

Superannuation proposals

• No benefits tax for retirees aged 60+– Simpler tax arrangements for retirees aged 55-60– Reasonable Benefit Limits abolished

• More generous pension assets test taper– Taper rate halved to $1.50 per $1,000 above $157,000

(single homeowner)

• Self-employed: full deductibility and access to co-contribution

• More flexibility for people who want to work longer

Simpler tax rules for retireesLump sums – Age 60+

Simpler tax rules for retireesSuperannuation pensions

Includes superannuation pensions commenced before 1 July 2007