the growth imperative - innosight...the extreme power of granularity source: granularity of growth;...

TRANSCRIPT

THE GROWTH IMPERATIVECHOOSI NG T O L EAD T RANSFORMATI ONAL GROWT H

Patrick Viguerie, Managing Partner, Innosight

“THE COLLECTIVE POWER OF THOSE

INDEPENDENT ENOUGH NOT TO FOLLOW WILL

MOVE THE WORLD FORWARD”

Malala Yousafzai

Florence Nightingale

Little Rock Nine

Quentin TarantinoReed HastingsEd Catmull

Blake Mycoskie Mark Bertolini

Amelia EarhartLady Gaga Dick Fosbury

Andy WarholJackie Robinson

© 2018 Innosight Consulting, LLC and/or its affiliates 3

3

Creative destruction is alive and well

0

10

20

30

40

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

AVERAGE LIFESPAN ON S&P 500 IN YEARSRolling 7-year averages

PROJECTED

Source: “Corporate Longevity: Turbulence Ahead for Large Organizations,” Innosight briefing, Spring 2018, Dual Transformation

© 2018 Innosight Consulting, LLC and/or its affiliates 4

4

Choosing to grow – five key messages

Source: Granularity of Growth

Apply granularity to sharpen insights and decisions about

markets, opportunities, and your growth portfolio

Recognize that where-to-play choices will enable – or limit – your growth

Decide whether to grow or go ... Nothing else works over the long term

Determine whether to build a transformative growth platform or focus on the core …and either way, prepare to make some curve-bending moves

Anchor innovation in customer “jobs-to-be-done

1

2

3

4

5

© 2018 Innosight Consulting, LLC and/or its affiliates 5

Long-term value creation associated withrevenue growth, not margin expansion

Annualized TRS,May11 to May19

Diameter reflects

LFY Revenue

8-YEAR TRS, MARGIN EXPANSION & REVENUE GROWTHEstimate

5

10

15

20

25

30

-1500 -1000 -500 0 500 1000

Chg in Operating Margin, bps – Last 8 Fiscal YearsRevenue CAGR, % – Last 8 Fiscal Years

35

0

5 10 15 20 25 35 4530 40 50-5 0

R2 = 0.00R2 = 0.53

1Grow or go

Top 20 market cap S&P 500 companies, ex-financials

Note: Facebook on 7-year basis

Apple

United

Health

Amazon

HomeDepot

CiscoDisney

Merck

PfizerJNJ

Walmart

P&GVerizon

Coca-

Cola

AT&TChevron

XOM

Microsoft

Alphabet

© 2018 Innosight Consulting, LLC and/or its affiliates 6

40

30

25

20

15

10

5

Example of growth/return relationship across TMT sector

Annualized TRS,Apr 2011 to Apr 2019

Diameter reflects

LFY Revenue

Source: Company financials

10-YEAR TRS, MARGIN EXPANSION & REVENUE GROWTH (TMT)Estimate

-15 -10 -5 0 5 10 15

Op Margin Chg in bps

R2 = 0.14R2 = 0.56

Revenue CAGR

0

35

5 10 15 20 25 35 45 5530 40 500

1Grow or go

© 2018 Innosight Consulting, LLC and/or its affiliates 7

7

10.1

6.6

3.1

All growth comes from three growth cylinders – Where-to-play choices dominate

The revenue growth your company

achieves through growth of the

segments in your portfolio

Growth achieved through gaining

or losing share from competitors

Net revenue growth achieved when

making acquisitions or divestments

1 Includes companies analyzed during the period within 1999 and 2011 for various timeframes 2 Based on the average of 834 companies

Total

revenue

growth

Growth

cylinders

Market

momentum

Market out-

execution

M&A

Company average2

Average revenue growth disaggregation, percent, 1999-2006

0.4

Source: Granularity of Growth

2WTP choices

© 2018 Innosight Consulting, LLC and/or its affiliates 8

8

Where to play example: Almost no way to grow as an auto OEM early 2000s without a position in China or Luxury

$50

$140

$40

$25

$25

2000 China Luxury Exc. China Other 2014

OEM AUTOMOTIVE EBIT 2000-2014 (Billions)

Luxury $15

$90

2WTP choices

© 2018 Innosight Consulting, LLC and/or its affiliates 9

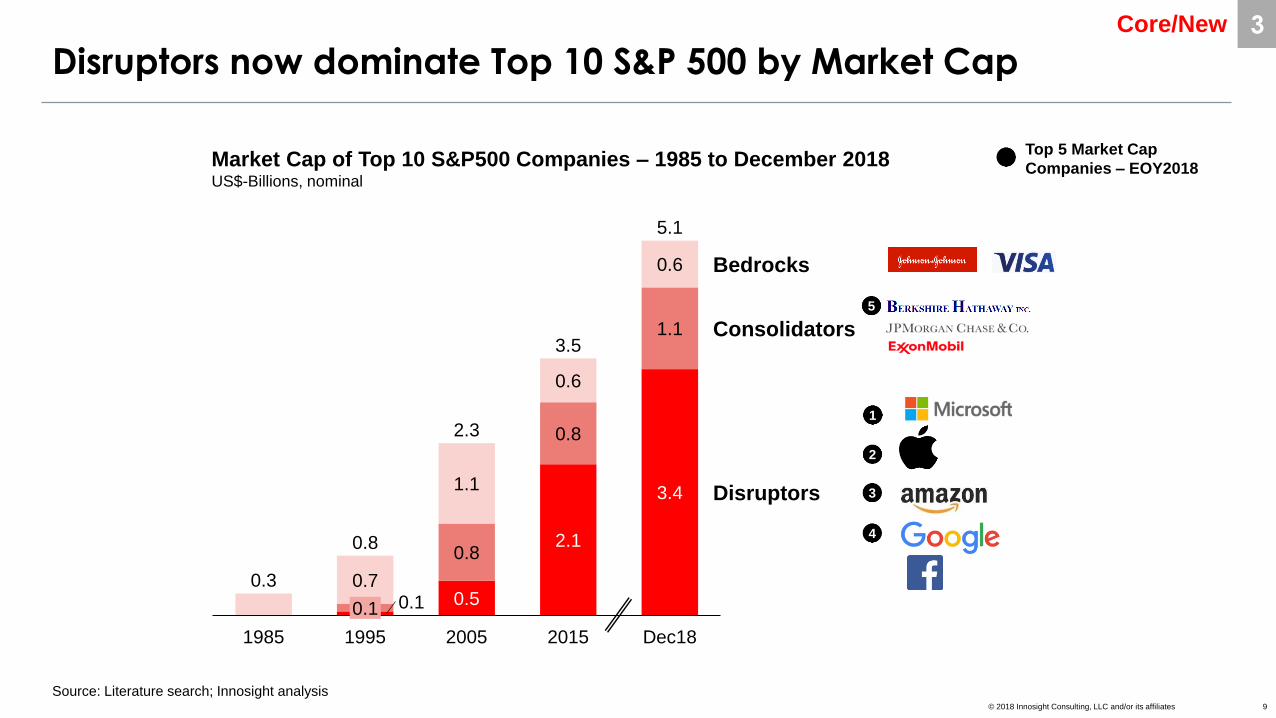

Disruptors now dominate Top 10 S&P 500 by Market Cap

0.8

1995

0.7

1985

0.1

Consolidators

Dec18

0.8

1.1

0.1 0.5

2005

0.6

2.1

2015

0.6

1.1

3.4

3.5

Bedrocks

Disruptors

0.8

0.3

2.3

5.1

Market Cap of Top 10 S&P500 Companies – 1985 to December 2018 US$-Billions, nominal

Source: Literature search; Innosight analysis

1

2

3

4

5

Top 5 Market Cap

Companies – EOY2018

3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 10

Sustaining innovations power incumbent growth

Source: Richard N. Foster; Creative Destruction

3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 11

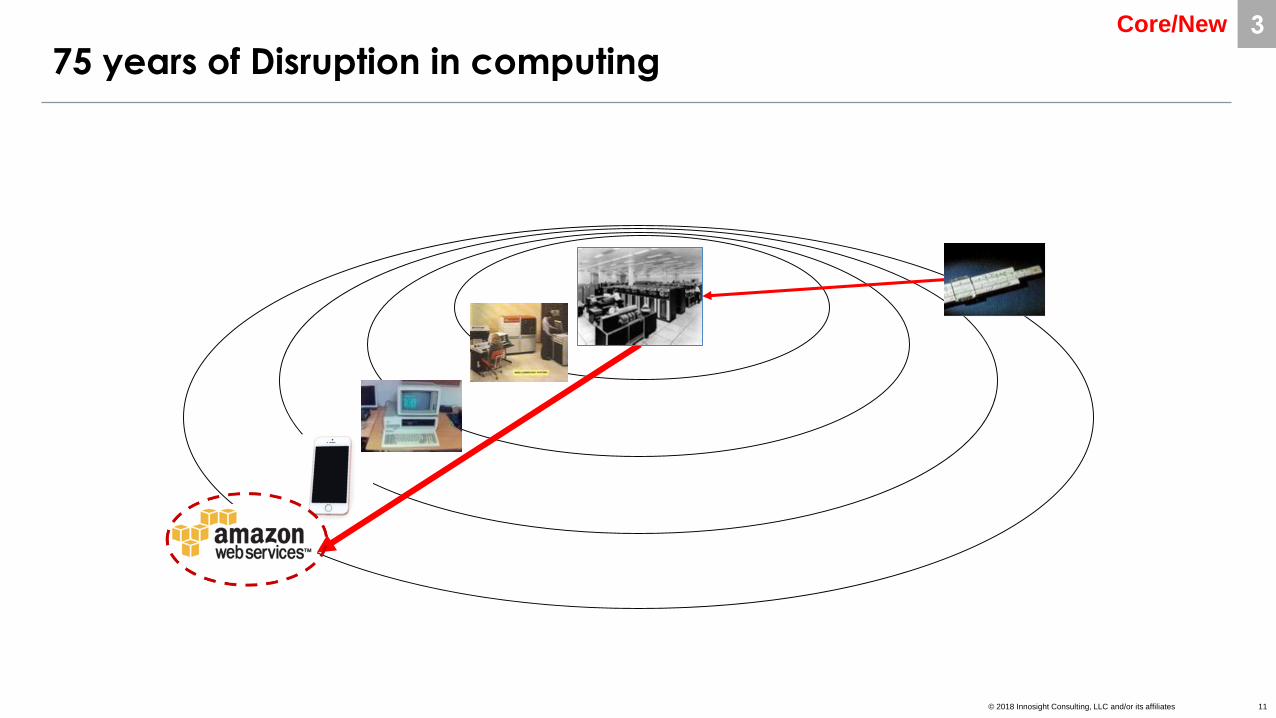

75 years of Disruption in computing3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 12

NO ONE HAS EVER BEATEN DISRUPTION

JUST BY TRYING TO DO

WHAT THEY CURRENTLY DO BETTER

© 2018 Innosight Consulting, LLC and/or its affiliates 13

Successful transformative platforms receive considerably higher revenue multiples vs. core / legacy players

Estimate

Core / Legacy

Transformative

EV-to-Revenue Multiples in Select Sectors

– April 2019

LFY EBITA Margin, %

Automotive / MobilityChemicals Healthcare

1.4

2.5

6.5

10

22

30

4.6

4.9

15.1

0.4

2.4

~8.0

1 Based on $90B expected public Valuation, $11b in 2018 Net Revenue

1

3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 14

Microsoft and Adobe enjoyed significant Multiple Expansion based on “Where to Play” Choices

Source: Company financials, websites

ENTERPRISE VALUE-TO-REVENUE MULTIPLE Dec12 v Apr19, x

Estimate

Enterprise Value 172 950 14417

74 110 94LFY Revenue

$-Billions

38 34 3328LFY EBITA Margin, %

2.3

8.6

Dec12 Apr19

3.9

15.9

Dec12 Apr19

3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 15

Revenue multiples show relative value of Core, Adjacent and Transformative innovation

2 3 4

24 2.6 2.8 2.9

28 3.1 3.4 3.6

32 3.6 4.0 4.2

EBITA

Margin Percent

Organic Revenue Growth – First 10 YearsPercent

EV-to-Revenue

Multiple1

Valuation Sensitivity based on Platform Type

Core / Adjacent

Transformative

Moderate, GDP Growth

Asset-Intensive2

High Growth

Asset-Light3

5 10 15

4.2 6.2 9.0

5.0 7.3 10.6

5.7 8.3 12.2

1 Global assumptions: WACC = 8%, Tax Rate = 25%

2 Operating Invested Capital [i.e., OIC] / Revenue = 1.6x,

3 OIC / Revenue = 0.2x

3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 16

16

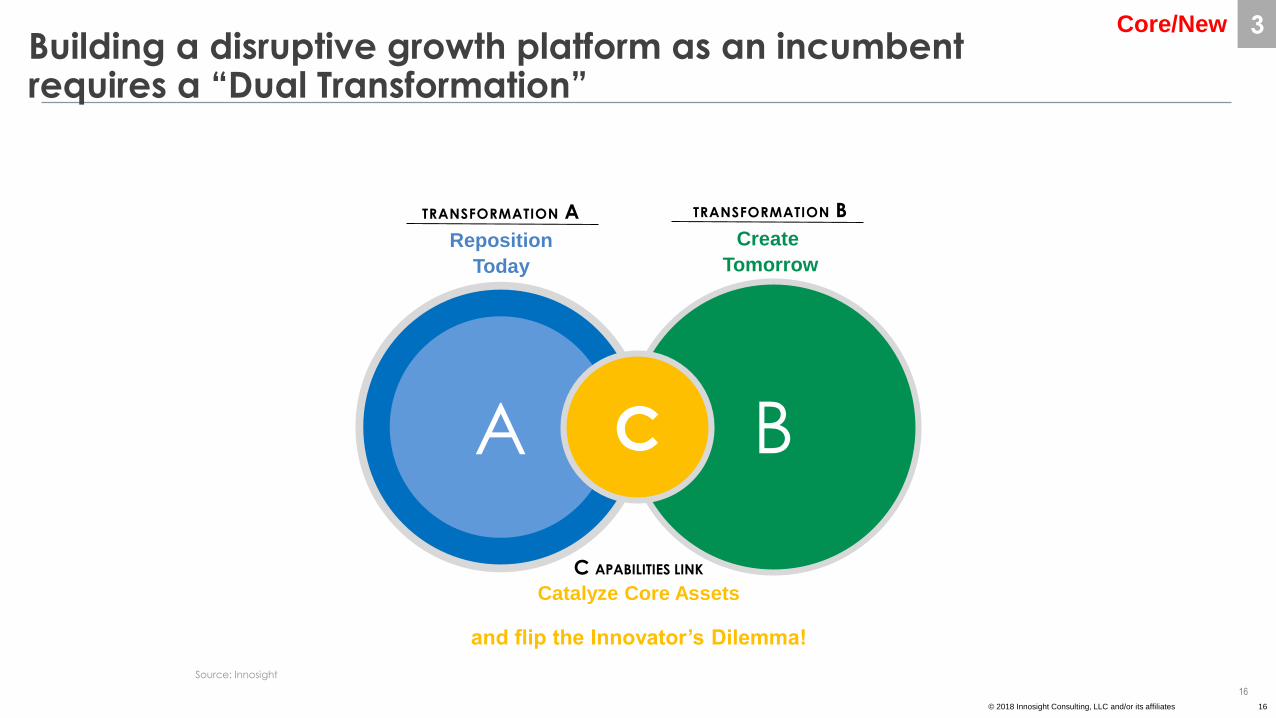

Building a disruptive growth platform as an incumbent requires a “Dual Transformation”

TRANSFORMATION A

Reposition

Today

TRANSFORMATION B

Create

Tomorrow

C APABILITIES LINK

Catalyze Core Assets

A BC

Source: Innosight

and flip the Innovator’s Dilemma!

3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 17

17

Big moves; big difference – what are your “curve benders?”

Source: Strategy Beyond the Hockey Stick

Productivity transformation

Significant resource reallocation

Sustained capital investment program

Programmatic M&A

Major business model differentiation improvement

1

2

3

4

5

3Core/New

© 2018 Innosight Consulting, LLC and/or its affiliates 18

Changing consumer expectations accelerate disruption

“When people say that an

entrant is disruptive in an

industry, what they really mean

is that customers are adopting

that new way. At Amazon, we’ve

had a lot of inventions that we

were very excited about, and

customers didn’t care at all. And

believe me, those inventions

were not disruptive in any way.

The only thing that’s

disruptive is customer

adoption. If you can invent a

better way, and if customers

agree that it’s a

better way, then they will

use that.”

4Jobs-to-be-done

© 2018 Innosight Consulting, LLC and/or its affiliates 19

Innovation should solve a customer’sJOBS-TO-BE-DONE

Enabling Access and Affordability

4Jobs-to-be-done

© 2018 Innosight Consulting, LLC and/or its affiliates 20

What is a JOB-TO-BE-DONE?

“People don’t want to buy a quarter-inch drill, they want a quarter-inch hole!” – Ted Levitt

VS.

The fundamental task (or problem) the consumer (or stakeholder) is trying to get done (or solve) in a particular circumstance

4Jobs-to-be-done

© 2018 Innosight Consulting, LLC and/or its affiliates 21

21

The extreme power of granularity

Source: Granularity of Growth; Google Earth

• Originally a scientific and engineering term, now a “household word” in business

• Refers to the size of the components of a larger system

• Cuts through the tyranny of the “averaged view”

5Granularity

© 2018 Innosight Consulting, LLC and/or its affiliates 22

22

Applying granularity to portfolio management can sharpen resource allocation choices …

Growth and ROIC

together drive value….

…Value is created AT

the granular level….

…Improvements “cascade

up” when made broadly

Company

BU

Geographies

Products

Customers

Value─30 +100

∑ = +70

Source: Granularity of Growth; Innosight

5Granularity

© 2018 Innosight Consulting, LLC and/or its affiliates 23

23

… across the portfolio

Source: McKinsey Granularity of Growth Initiative; Corporate Finance Practice

Revenue

Generating Units

Business Model

InnovationM&A

Legacy

Emerging

HEAT MAP ILLUSTRATION

Source: Granularity of Growth; Innosight

5Granularity

© 2018 Innosight Consulting, LLC and/or its affiliates 24

24

Choosing to grow – five key messages

Source: Granularity of Growth

Apply granularity to sharpen insights and decisions about

markets, opportunities, and your growth portfolio

Recognize that where-to-play choices will enable – or limit – your growth

Decide whether to grow or go ... Nothing else works over the long term

Determine whether to build a transformative growth platform or focus on the core …and either way, prepare to make some curve-bending moves

Anchor innovation in customer “jobs-to-be-done

1

2

3

4

5

© 2018 Innosight Consulting, LLC and/or its affiliates 25

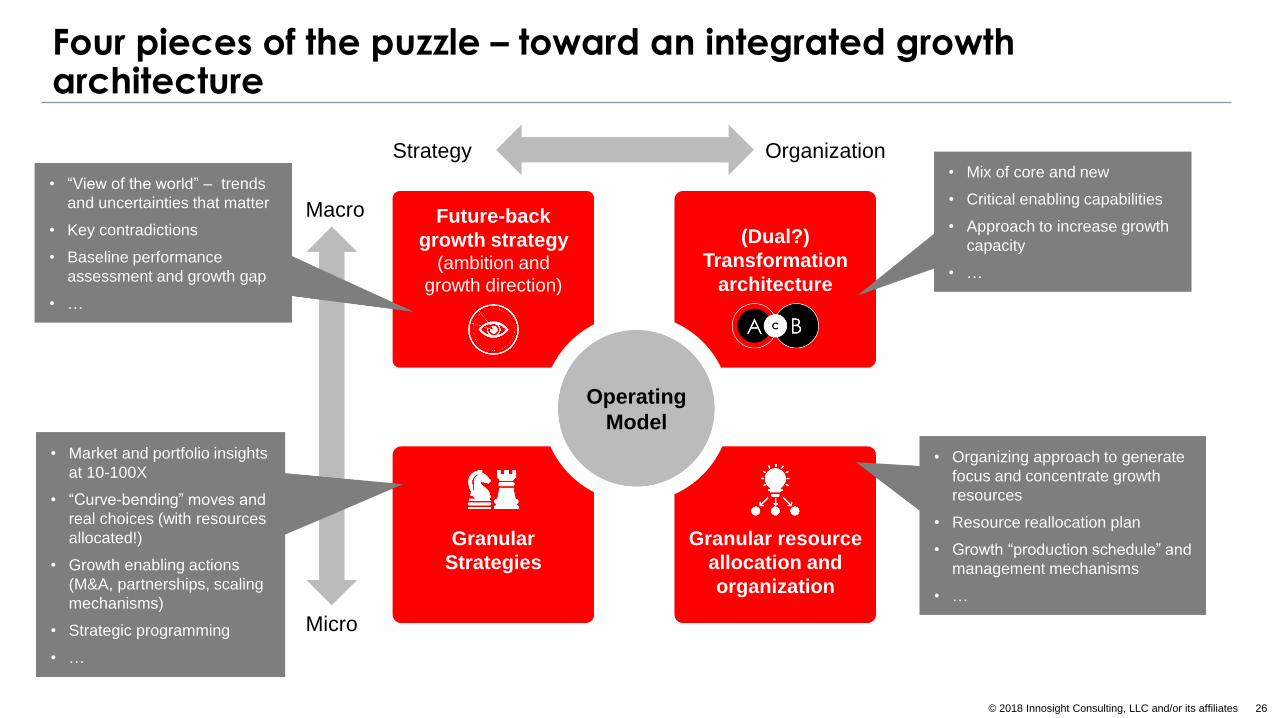

The pieces of the puzzle – toward an integrated growth architecture

Future-back

growth strategy (ambition and

growth direction)

Granular

Strategies

Granular resource

allocation and

organization

Macro

Micro

Strategy Organization

(Dual?)

Transformation

architecture

Operating

Model

© 2018 Innosight Consulting, LLC and/or its affiliates 26

Future-back

growth strategy (ambition and

growth direction)

(Dual?)

Transformation

architecture

Granular

Strategies

Granular resource

allocation and

organization

Operating

Model

Four pieces of the puzzle – toward an integrated growth architecture

• Mix of core and new

• Critical enabling capabilities

• Approach to increase growth

capacity

• …

• Organizing approach to generate

focus and concentrate growth

resources

• Resource reallocation plan

• Growth “production schedule” and

management mechanisms

• …

Strategy Organization

Macro

Micro

• “View of the world” – trends

and uncertainties that matter

• Key contradictions

• Baseline performance

assessment and growth gap

• …

• Market and portfolio insights

at 10-100X

• “Curve-bending” moves and

real choices (with resources

allocated!)

• Growth enabling actions

(M&A, partnerships, scaling

mechanisms)

• Strategic programming

• …

© Copyright 2013 Innosight LLC© 2018 Innosight Consulting, LLC and/or its affiliates

THANK YOU!