the global subsea irm sector - championing the uk subsea sector asia - jason... · 2015-03-31 ·...

TRANSCRIPT

1 SUT London ndash February 2011

The Global

Subsea IRM Sector

Jason Waldie Associate Director

Douglas-Westwood

Subsea Asia Conference Kuala Lumpur 2nd June 2011

2 SUT London ndash February 2011

wwwdw-1com

Our Business

LNG

offshore

onshore

downstream

power

LNG

renewables

History and Locations

bull Established 1990

bull Aberdeen New York amp Canterbury

Setting up in Singapore

Activities amp Service Lines

bull Market research amp analysis

bull Commercial due-diligence

bull Business strategy amp advisory

bull Published market studies

Industry Sector Coverage

bull Oil amp Gas

bull Renewables

bull Power

Large Diversified Client Base

bull 650 projects 400 clients 70 countries

bull Leading global corporates

bull Energy majors and their suppliers

bull Investment banks amp PE firms

bull Government agencies

copy Douglas-Westwood Limited 2011

3 SUT London ndash February 2011

Financial Transaction Credentials Includehellip

Market amp commercial due diligence as part of financial transactions

is one of our largest activities

Further information at wwwdw-1com

copy Douglas-Westwood Limited 2009

euro670 acquisition by

Ferd Private Equity

Fund-raising for rig

newbuild programme

Acquisition by Cable

Solutions Group Inc pound319 million IPO

$768 million IPO Arcapita completes

acquisition of Roxar

Perry Slingsby Systems

capital acquired by Triton

Group Holdings pound535m finance facility

Songa Drilling

pound29 million

Refinancing

pound345 million Rovtech

acquired by Fugro

Acquisition Growth and

Working Capital Facilities

pound15 million MBO of

Motherwell Bridge

Expro Group $675m

acquisition of Powerwell

Services

Inflexion Private Equity

Backs pound22m MBO of

Viking Moorings

pound50 million credit facility

for Sovereigns

acquisition of Forfab

Investor syndicate

$925m acquisition of

ABB Oil amp Gas

$280m acquisition of

KBR Production

Services

pound130m debt facility

to finance the

construction of two

specialist vessels

Epcon Offshore AS

acquisition by M-I

SWACO

Serimer Holdings

acquisition of the UMAX

group

UMAX Ltd

Recapitalisation

pound755 million MBO $719 million IPO AGT Energy acquisition of

50 share of Oilflow

Solutions from Vienco

Management buyout of ESS

Steel Holdings

$305 million project

financing of FPSO RJS-409

(Espadarte Sul)

$180 million project

financing of FSO Cidade de

Macae MV15

Acquisition by

Inflexion Private

Equity

pound142m

acquisition by

Close Brothers

Private Equity

Sale of Motherwell

Bridge to Kuwait Finance

House

NOK 43 billion

joint acquisition

by First Reserve

amp DOF

Acquisition of

APAC division

by Champ

Ventures

Borets Group $150

million debt facility led

by EBRD

MBO backed by

HSBC Private

Equity

Acquisition by SCF

Partners

Acquisition of Anson by

NOV

Acquisition of ASEP by

NOV

Equity investments in

Advantec

4 SUT London ndash February 2011

Energy Macro Factors

Offshore Oil amp Gas

Lifecycle Opportunities

Conclusions

5 SUT London ndash February 2011

Energy Macro Factors

A global drive for energy that is

Sustainable

Secure

Affordable

A growing demand driven by

Population growth

GDP growth

6 SUT London ndash February 2011

The Importance of Oil

Oil is the fuel of

transportation

Demand is growing

Supplies are limited

Prices will rise

Other energy prices often

linked to oil

7 SUT London ndash February 2011 Source Financial Times London 5 January 2011

Source BP

Energy Consumption 1965-2009

00

05

10

15

20

25

30

35

40

45

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

Bill

ion to

nnes o

f o

il eq

uiv

ele

nt

North America

S amp Cent America

Europe amp Eurasia

Middle East

Africa

Asia Pacif ic

Energy Demand Growth ndash Historic amp Outlook

bull Energy demand growth outpaces population growth (95 v 55)

bull Close correlation between GDP growth and energy consumption

bull Recently driven by growth in China and India

8

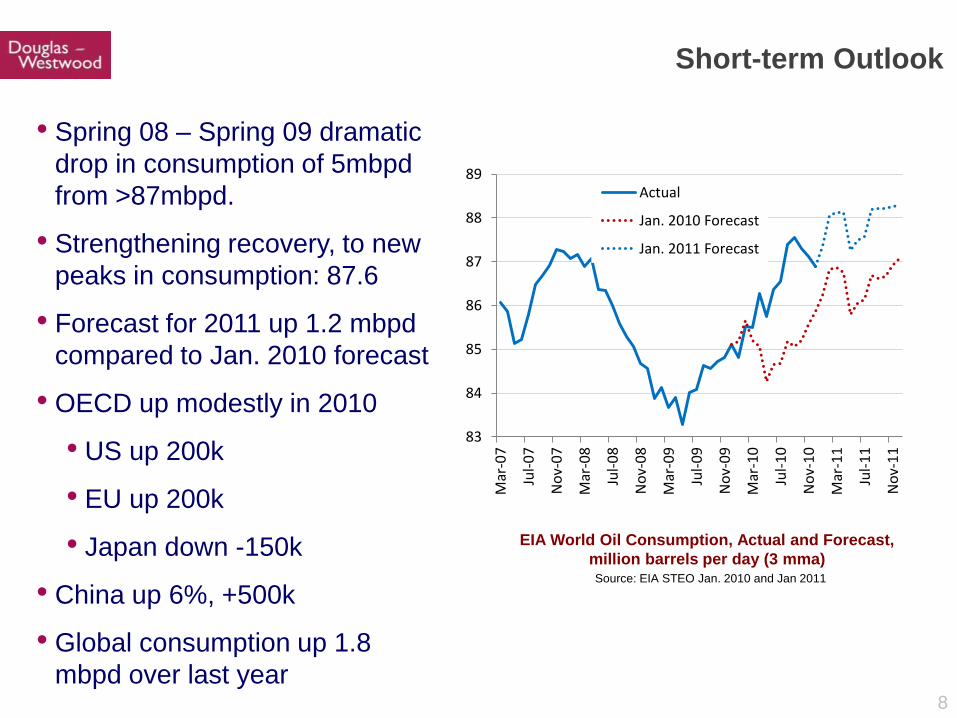

bull Spring 08 ndash Spring 09 dramatic

drop in consumption of 5mbpd

from gt87mbpd

bull Strengthening recovery to new

peaks in consumption 876

bull Forecast for 2011 up 12 mbpd

compared to Jan 2010 forecast

bull OECD up modestly in 2010

bull US up 200k

bull EU up 200k

bull Japan down -150k

bull China up 6 +500k

bull Global consumption up 18

mbpd over last year

Source EIA STEO Jan 2010 and Jan 2011

EIA World Oil Consumption Actual and Forecast

million barrels per day (3 mma)

83

84

85

86

87

88

89

Mar

-07

Jul-

07

No

v-0

7

Mar

-08

Jul-

08

No

v-0

8

Mar

-09

Jul-

09

No

v-0

9

Mar

-10

Jul-

10

No

v-1

0

Mar

-11

Jul-

11

No

v-1

1

Actual

Jan 2010 Forecast

Jan 2011 Forecast

Short-term Outlook

9

bull Worldlsquos second largest economy 10 GDP growth

bull ―Astonishing oil demand growth

bull 18 million light vehicle sales vs 136 million prior year (126 m for US in 2010)

bull 120 million new cars by 2015 = all passenger vehicles UK + France + Germany

bull In 2010 China was 13 of total global oil demand growth (less than other Asia and

non-OECD)

bull Chinalsquos foreign oil dependence rises from 1 in 2 bbls to potentially 9 in 10 by 2030

Source EIA Douglas-Westwood Analysis

China Crude Oil Production and Constrained Demand

0

2

4

6

8

10

12

14

16

18

20

Mill

ions o

f barr

els

per

Day

Onshore oil production

Offshore oil production

Oil consumption

5

10

15

20

25

30

35

40

45

50

55

mill

ion b

arr

els

per

day

China as Japan(1960-1973)

China as Korea(1976-1996)

China - EIA IEO2010

Source EIA Douglas-Westwood Analysis

China Unconstrained Demand

Longer Term Outlook China Chinaand Others

For more information please

contact Douglas-Westwood

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

10

bull North Sea and Mexico continue

decline

bull Canada flat

bull Brazil underperforms

bull FSUmdashmostly Azerbaijanmdash

doing well

bull China and USA at front of the

pack

bull OPEC NGLs are leading the

way

bull Total world supply up 20 mbpd

half is NGLs

bull EIA expects 2011 largely flat

Source EIA STEO Jan 2011

World Liquids Production Growth 2010

million barrels per day

(600)

(400)

(200)

-

200

400

600

800

1000

Liquids Supply in 2010

11 SUT London ndash February 2011

bull Iraq

bull Output up 300 kbpd to 27 mbpd

bull Potential to increase by 05 mbpd per year to 6-7 mbpd

bull Bakken

bull Output up 80 kpbd to 380000 bpd

bull Potential to add 80 kbpd year potentially to greater than 1 mpbd or more

bull Like gas shales production is front-loaded

bull More to come from other sources

Supply Risks Iraq and Bakken

12

$50

$60

$70

$80

$90

$100

$110

$120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WTI

Cru

de

Oil

Spo

t P

rice

- A

nn

ual

B

asis

- C

urr

en

t D

olla

rs

Actual WTI

EIA - Reference Case

DWL - Base Case

bull We assume supply is flat to modestly increasing

bull Historically US could not add oil consumption at more than 4 of

GDPmdashequals $86

bull In last three months of 2010 US up 230 kbpd at average $85

bull US up 700 kbpd in December at $89

bull WTI at $92mdashabove our expectation of mid-to-high $80s for 2011

bull If US can reset to a higher tolerance for oil prices a substantial oil

price rally could be in store

Source EIA AEO ( adjusted RACC + $150) Douglas-Westwood

Annual WTI Spot Oil Price Forecasts EIA Douglas-Westwood

bull

Current oil price

Medium Term Oil Price Outlook

For more information please

contact Douglas-Westwood

13

0

20

40

60

80

100

Year 2030

Uppsala University

IEA EIA IOClsquos

Douglas-Westwood

Total Production Capacity

Current Production

Only material difference between

Uppsala and IEA is depletion rates

on fields to be discovered and

developed to 2030

Range of Global Oil Supply Forecasts ndash 2030 ndash All

Liquids Source various

bull Petroleum liquids

supply forecasts from

75 ndash 105 mbpd for

2030

bull All are essentially

peak oil forecasts

bull Quiet consensus has

emergedmdash

disagreements are

increasingly narrow

and specific

Long-term Outlook A Narrowing of Views

14

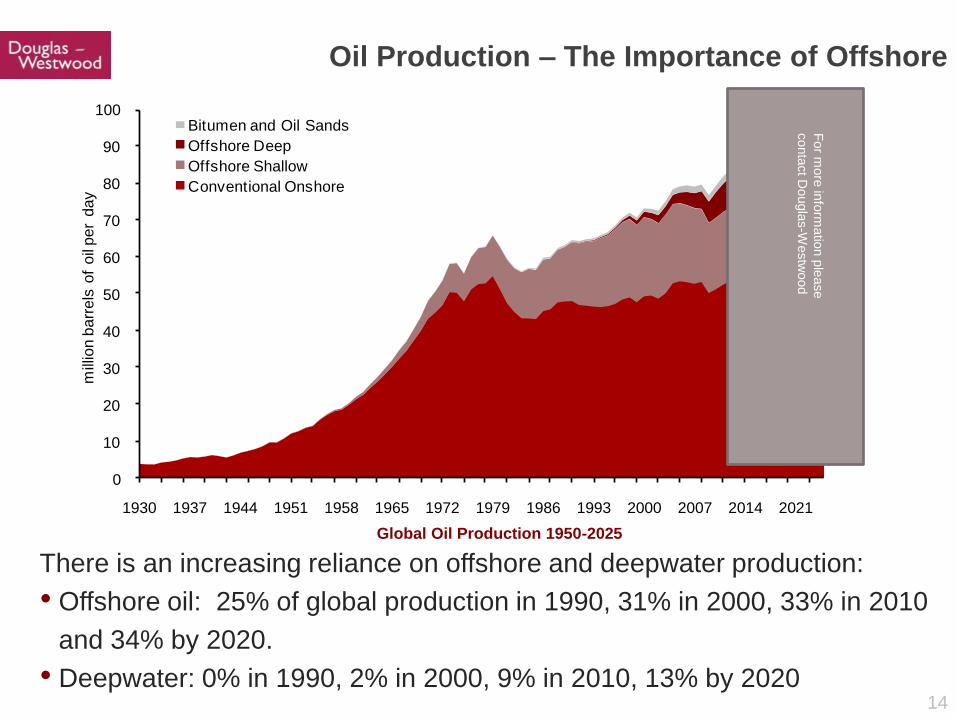

Oil Production ndash The Importance of Offshore

There is an increasing reliance on offshore and deepwater production

bull Offshore oil 25 of global production in 1990 31 in 2000 33 in 2010

and 34 by 2020

bull Deepwater 0 in 1990 2 in 2000 9 in 2010 13 by 2020

Global Oil Production 1950-2025

0

10

20

30

40

50

60

70

80

90

100

1930 1937 1944 1951 1958 1965 1972 1979 1986 1993 2000 2007 2014 2021

mill

ion b

arr

els

of

oil

per

day

Bitumen and Oil Sands

Offshore Deep

Offshore Shallow

Conventional Onshore

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

15

Peak Oil is a Reality

Data Petroleum Review May 2010

bull With most of the easy oillsquo in the hands of the NOCs

majors are scrambling to replace reserves and off-

set production decline

bull They are moving to harsh environments ndash offshore

deepwater politically difficult geographically remote

Peak Year

2002 2003 2004 2005 2006 2007 2008 2009

ExxonMobil 2496 2516 2571 2523 2681 2616 2404 2387

BP 2018 2121 2531 2562 2475 2414 2410 2535

PetroChina 2109 2119 2233 2270 2276 2312 2380 2311

Shell 2359 2379 2253 2093 2030 1899 1771 1680

Petrobras 1533 1701 1661 1847 1908 1920 1996 2103

Chevron 1897 1823 1737 1701 1759 1783 1676 1872

Total 1589 1661 1695 1621 1506 1509 1456 1381

ConocoPhillips 891 1237 1242 1447 1698 1644 1367 1615

ENI 921 981 1034 1111 1079 1020 1026 1007

StatoilHydro 1112 1132 1135 1102 1058 1054 1056 1067

Source Offshore Technology

NOCs (limited equity access )

78

NOCs (equity access)

10

New Russian Companies

6

Full IOC access6

Restricted access to oil reserves

16 SUT London ndash February 2011

85

86

87

88

89

90

91

92

93

94

95

2009 2010 2011 2012 2013

mill

ion

bar

rels

pe

r d

ay

Demand Growth as 2002-2005

Demand Growth as 1976-1979

IEA Supply Demand Forecast

Effective Global Liquids Production Capacity

Medium term outlook risks of oil shock growing

bull Adequate spare capacity today ndash

but frac34 of it is in Saudi

bull IEA sees demand rising slowly

less than 14 mbpd year in 2011

bull Previous recoveries saw strong

demand growth during first three

years

bull After 2002 77 mbpd

bull After 1976 73 mbpd

bull If previous patterns hold true a

possible supply crunch in

20122013

bull What will Saudi do Source IEA Douglas-Westwood analysis

Oil Demand under Three Scenarios and Global

Liquids Production Capacity

Oil shock

IEA forecast (2010)

Surplus Capacity

bull Dec 2010 demand

Spare Capacity at Saudi 10 mbpd limit

bull Jan 2011 forecast

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

17 SUT London ndash February 2011

The WikiLeaks Saudi cables

Crude oil reserves may have been overstated by as much as 300bn barrels

ndash nearly 40

bull Al-Husseini [believes] Aramcos reserves are overstated by as much

as 300bn barrels In his view once 50 of original proven reserves has

been reached hellip a steady output in decline will ensue and no amount of

effort will be able to stop it He believes that what will result is a plateau in

total output that will last approximately 15 years followed by decreasing

outputldquo

bull ldquoClearly they [Saudi] can drive prices up but we question whether they

any longer have the power to drive prices down for a prolonged periodrdquo

Source US Embassy cables to Washington 2007-2009 The Guardian 8 February 2010

Sadad al-Husseini a geologist and former head of exploration at the Saudi oil monopoly Aramco met the US

consul general in Riyadh in November 2007

18

United States

Russia

Iran

Qatar

Other OPEC

Rest of World

100

yearslsquo

US

supply

05

10

15

20

25

30

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

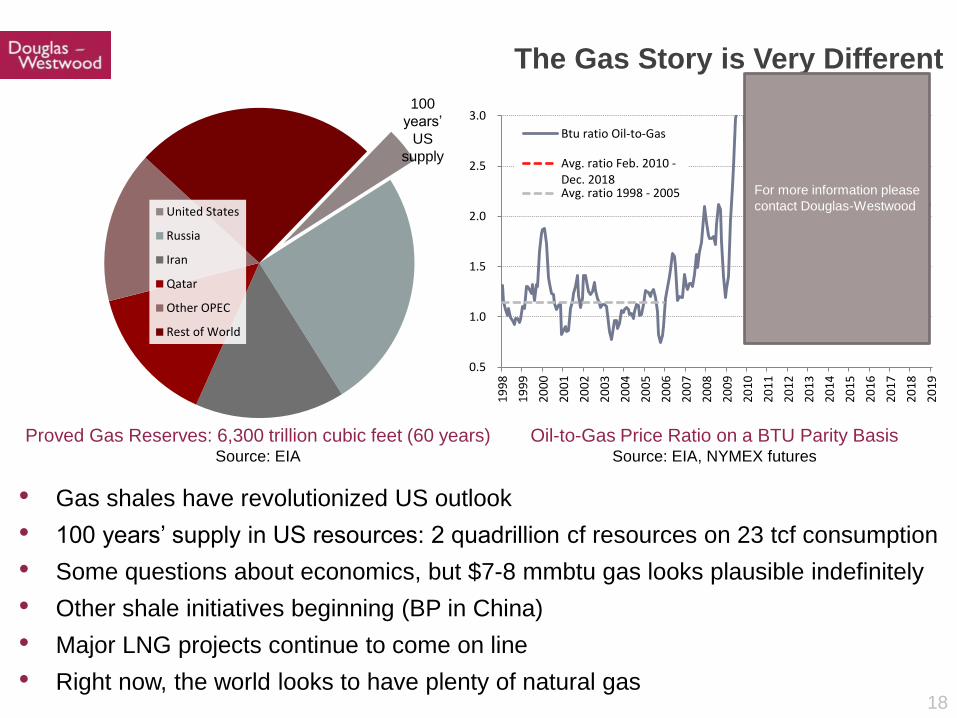

Btu ratio Oil-to-Gas

Avg ratio Feb 2010 -Dec 2018Avg ratio 1998 - 2005

Oil-to-Gas Price Ratio on a BTU Parity Basis Source EIA NYMEX futures

Proved Gas Reserves 6300 trillion cubic feet (60 years) Source EIA

bull Gas shales have revolutionized US outlook

bull 100 yearslsquo supply in US resources 2 quadrillion cf resources on 23 tcf consumption

bull Some questions about economics but $7-8 mmbtu gas looks plausible indefinitely

bull Other shale initiatives beginning (BP in China)

bull Major LNG projects continue to come on line

bull Right now the world looks to have plenty of natural gas

The Gas Story is Very Different

For more information please

contact Douglas-Westwood

19 SUT London ndash February 2011

bull Dominated by E Europe amp FSU but others to see significant growth

bull Deepwater gas and LNG to be of growing importance

bull Impact of shale gas on North America (amp other markets)

bull But local supply issues eg Europe to import gt73 by 2020

Natural gas production and use to soar

Source Energyfiles

0

10

20

30

40

50

60

70

80

90

100

1930 1937 1944 1951 1958 1965 1972 1979 1986 1993 2000 2007 2014 2021

million b

arr

els

of o

il eq

uiv

ale

nt p

er d

ay

Africa

Asia

Australasia

Eastern Europe amp FSU

Latin America

Middle East

North America

Western Europe

ME

FSU

NA

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

20 SUT London ndash February 2011

10

2428

31

3941

47 48

5356

60

0

1

2

3

4

5

6

Capex ($ m

llion m

W)

Source EIA Nov 2010

Gas ndash lowest Capex for power plants

21 SUT London ndash February 2011

Gas ndash FLNG in prospect

bull Liquefaction ndash $20 bn spend by 2017

bull Australasia to account for 60

bull Woodside has raised the prospect of FLNG for its Greater Sunrise project

bull Inpex (Japan) considering FLNG at its $196 billion Abadi field in Indonesia

bull GDF Suez and Australias Santos set up a joint venture to develop a floating

LNG project off northwest Australia

Picture Shell

Source The World FLNG Report Douglas-Westwood

0

1

2

3

4

5

6

7

8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Exp

en

ditur

e ($ b

illio

n)

Africa

Asia

Australasia

Latin America

Middle East

North America

0

1

2

3

4

5

6

7

8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Exp

en

ditur

e ($ b

illio

n)

Africa

Asia

Australasia

Latin America

Middle East

North America

$67bn

For more information please

contact Douglas-Westwood

22 SUT London ndash February 2011

$0

$100

$200

$300

$400

$500

$600

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

US

Do

llar

Bil

lio

ns

Outside North America

Canada

United States

bull Recovery in 2010 up 10 to $442 bn

bull Continued growth in 2011 to $490 bn up 11 a new peak

bull US spend up 8 Canada up 5 international up 12

bull Spend up $48 bn in 2011 of which 82 is international

Recovery and growth in global EampP spend

Source Jim Crandell Barclaylsquos EampP Spending Survey December 2010

Global EampP Spend

+10 -15 +11

23 SUT London ndash February 2011

0

10

20

30

40

50

60

70

80

90

100

$70 $75 $80 $85 $90 $95 $100

Cu

mu

lati

ve P

erc

en

t o

f R

esp

on

de

nts

0

10

20

30

40

50

60

70

80

90

100

$35 $40 $45 $50 $55 $60 $65 $70 $75

Cu

mu

lati

ve P

erc

en

t o

f R

esp

on

de

nts

bull EampP companies prepared budgets assuming $77 oil on average

up from $70 last year

bull Expect capex to materially decrease in the industry if oil prices fall

much below $60

bull Expect capex to increase materially if oil prices sustain above $90

up from $85 last year

Source Barclays Capital EampP Spending Survey Dec2010

Oil Price Threshold for Reducing Capex Oil Price Threshold for Increasing Capex

Source Barclays Capital EampP Spending Survey Dec2010

Percent of Respondents Decreasing Capex at a Given Oil Price

Percent of Respondents Increasing Capex at a Given Oil Price

2011 ndash EampP Spend Sensitivity to Oil Prices

24 SUT London ndash February 2011

Offshore Oil amp Gas

Nowhere else left for big finds

Strong Capex growth

Importance of deepwater

The beauty of Opex

25 SUT London ndash February 2011

Global offshore oil amp gas production amp spend to grow

Source Datamonitor

bull Global Capex fell in lsquo0910 but Opex grew

bull Both Capex amp Opex to grow strongly in the years ahead

bull 28 new rigs ordered since October + 8 options 10-15 more in 2011

bull Deepwater Capex to exceed $205 billion

0

20

40

60

80

100

120

140

160

180

200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ex

pe

nd

itu

re ($

bill

ion

s)

AfricaAsiaAustralasiaEastern Europe and FSULatin AmericaMiddle EastNorth AmericaWestern Europe For more information please

contact Douglas-Westwood

26 SUT London ndash February 2011

OPTIONS

ORDERS

The next rig cycle begins

27 SUT London ndash February 2011

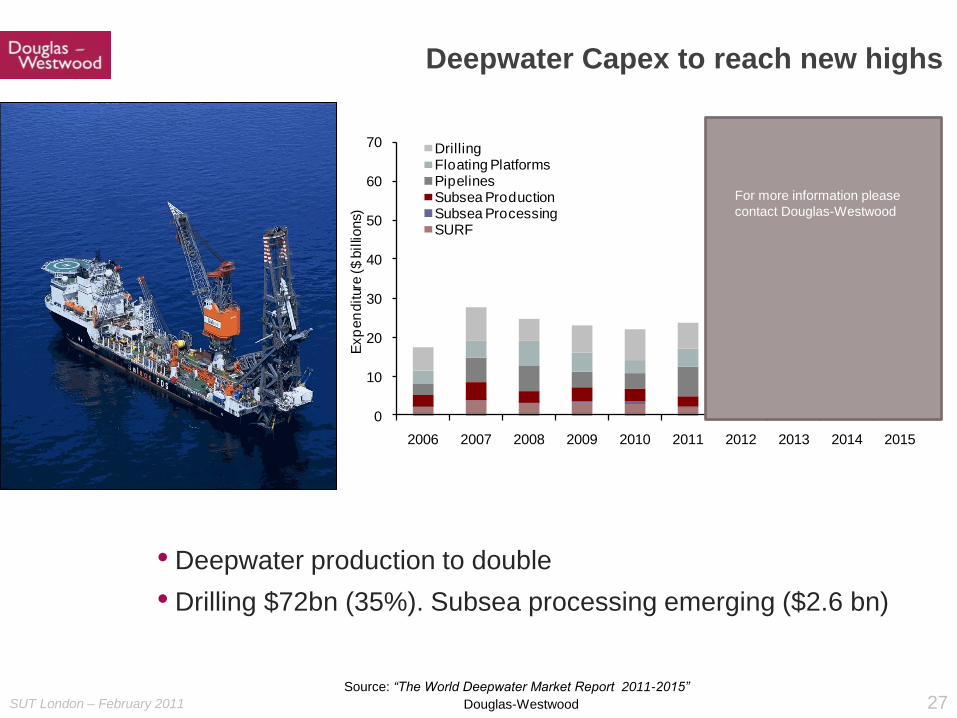

Deepwater Capex to reach new highs

bull Deepwater production to double

bull Drilling $72bn (35) Subsea processing emerging ($26 bn)

Source ldquoThe World Deepwater Market Report 2011-2015rdquo

Douglas-Westwood

0

10

20

30

40

50

60

70

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e ($ b

illio

ns)

DrillingFloating PlatformsPipelinesSubsea ProductionSubsea ProcessingSURF

For more information please

contact Douglas-Westwood

28 SUT London ndash February 2011

Deepwater ndash Africa amp Brazil to lead spend

bull Brazil amp W Africa to total $126bn (62)

bull But much more Brazil spend to come

Source ldquoThe World Deepwater Market Report 2011-2015rdquo

Douglas-Westwood

0

10

20

30

40

50

60

70

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e ($ b

illio

ns)

AfricaAsiaAustralasiaEastern Europe and FSULatin AmericaMiddle EastNorth AmericaWestern Europe

For more information please

contact Douglas-Westwood

29 SUT London ndash February 2011

Brazil ndash Petrobrasrsquos pre-salt deepwater lsquoshopping listrsquo

50 bn boe reserves 2 million production bpd by 2020

By 2018

bull Includes 58 new drilling rigs

By 2020

bull 72 VLCCs

bull 146 supply amp service vessels

bull 45 production platforms

bull Plus subsea hardware

Finance

bull 2010 $70bn stock offering

bull 2011 $6bn corporate bond

bull Next 4 years $30-40bn debt raising

bull Capex of $224bn by 2014

bull Capex amp Opex to total $1 trillion

Tupi Discovery Source CGG Veritas

30 SUT London ndash February 2011

Floating production recovery expected

Global Floating Production Expenditure Source Douglas-Westwood

bull Material decrease in orders in 2009 but market bottomed in 2010

bull Increasing share of market to leased FPSOs Consolidation likely

bull Deepwater Horizon unlikely to impact GoM small part of the market

bull Long term gt200 prospects exist and growth will return

bull Market to reach $16 billion in 2014

0

2

4

6

8

10

12

14

16

18

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e ($ b

illio

ns)

AfricaAsiaAustralasiaEE amp FSULatin AmericaMiddle EastNorth AmericaWestern Europe

For more information please

contact Douglas-Westwood

31 SUT London ndash February 2011

Subsea

Hardware

Operational Demands

Inspection Maintenance Repair

Well intervention

ROV AUV and Subsea Vessels

Operations Market

32 SUT London ndash February 2011

Subsea technology is vital to offshore production

bull Unlocking deepwater reserves

bull Improving economics of marginal fields in shallow waters

bull Tie-backs of small reservoirs into existing facilities

Subsea ndash long term outlook is sound

0

5

10

15

20

25

30

35

40

45

50

0

10

20

30

40

50

60

70

80

2001 2004 2007 2010 2013 2016 2019 2022 2025

Mill

ion B

oep

d

Topside ProductionSubsea Production Subsea Production

Offshore Production 2000-2025 Source Datamonitor

For more information please

contact Douglas-Westwood

33 SUT London ndash February 2011

$0

$5

$10

$15

$20

$25

$30

$35

$40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e $

bn

Africa AsiaAustralasia Eastern Europe amp FSULatin America Middle EastNorth America NorwayRoWE UK

bull $135 billion forecast for next five years

bull Pipelines to account for half of forecast expenditure

bull Major pipeline projects in Eastern Europe amp FSU Asia and the Middle

East

bull Subsea production hardware SURF and subsea processing driven by

deepwater regions

Source FMC Technologies

Subsea Hardware

For more information please

contact Douglas-Westwood

34 SUT London ndash February 2011

0

10

20

30

40

50

60

70

80

Mill

ion B

oepd

Incremental ProductionLost through DeclineProduction Base

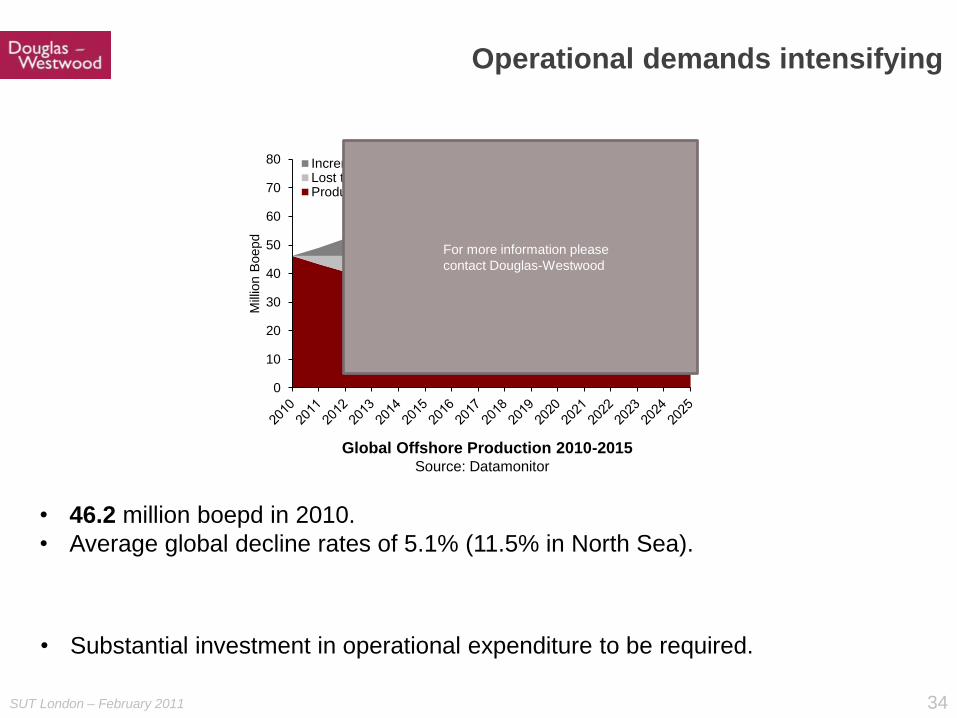

Global Offshore Production 2010-2015 Source Datamonitor

bull 462 million boepd in 2010

bull Average global decline rates of 51 (115 in North Sea)

bull Substantial investment in operational expenditure to be required

Operational demands intensifying

For more information please

contact Douglas-Westwood

35 SUT London ndash February 2011

Offshore ops amp maint spend to see good growth

Source ldquoThe World Offshore Operations amp Maintenance Market Report 2010-14rdquo

Douglas-Westwood

$0

$10

$20

$30

$40

$50

$60

$70

$80

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$bill

ions

AfricaAsia-PacificEastern Europe amp FSULatin AmericaMiddle EastNorth AmericaNorwayUKRest of Europe

bull gt7000 fixed amp gt200 floating platforms

bull Plus demand for major modifications

Fo

r more

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

36 SUT London ndash February 2011

Subsea IRM Expenditure 2004-2015 Source Douglas-Westwood

bull Over 7000 production platforms 190000km of pipeline currently installed

bull $28 billion of expenditure in Subsea IRM in 2010

bull Nearly $20 billion of further investment expected over the next five years

bull 55 forecast expenditure expected in the North Sea amp Gulf of Mexico

bull Less exposure to market cyclicality

00

10

20

30

40

50

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$m

illio

ns

Others

Western Europe

North America

Latin America

Asia-Pacific

Africa

Subsea Inspection Repair amp Maintenance

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

37 SUT London ndash February 2011

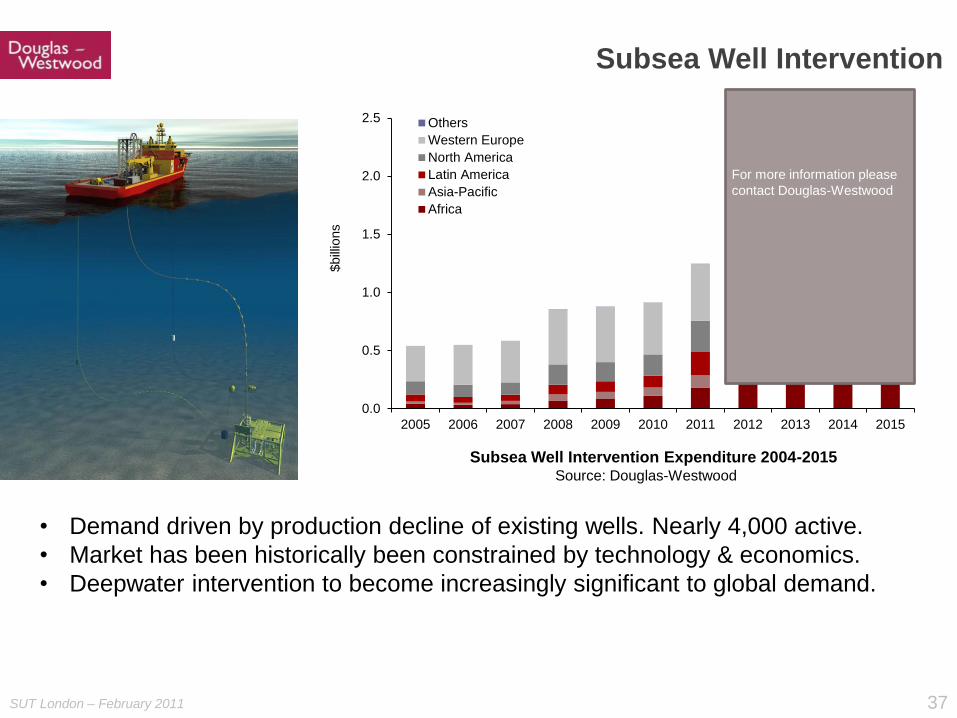

Subsea Well Intervention Expenditure 2004-2015 Source Douglas-Westwood

bull Demand driven by production decline of existing wells Nearly 4000 active

bull Market has been historically been constrained by technology amp economics

bull Deepwater intervention to become increasingly significant to global demand

00

05

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$bill

ions

Others

Western Europe

North America

Latin America

Asia-Pacific

Africa

Subsea Well Intervention

For more information please

contact Douglas-Westwood

38 SUT London ndash February 2011

320

370

420

470

520

570

620

$00

$05

$10

$15

$20

$25

$30

$35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Ac

tiv

e R

OV

s

Ex

pe

nd

itu

re ($

billio

ns

)

Africa

Asia Pacific

E EuropeFSU

Latin America

Middle East

North America

Western Europe

Active ROVs

The World Work Class ROV Operations Market 2005-2014

(Oil amp Gas) Source ―The World ROV Report 2010-2014 ndash Douglas-Westwood

ROV Paces the Growth of Deepwater

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

39 SUT London ndash February 2011

bull Self-guided under water survey and inspection vessels

bull From 1 to 5 meters long

bull Priced from $150000 to $7 million

bull Very hot topic recentlymdashmilitary contractors looking for commercial

applications

bull Greater acceptance for not only deep but shallow water oil and gas

survey

bull But a small market

Hugin 1000 MR AUV Courtesy Kongsberg Marine

AUV ndash Autonomous Underwater Vehicles

40 SUT London ndash February 2011

Subsea Vessel Operations Market

Subsea Operation Vessel Demand by Workscope Source Douglas-Westwood

bull Current IRM market demand for around 92 vessels

bull Field development market still depressed ndash upturn in 2012 amp beyond

bull Well intervention and PampA to see substantial growth

-

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

V

essels

Intervention amp PampA

Field Development

Inspection Repair amp Maintenance

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

41 SUT London ndash February 2011

Macondo ndash a $40 billion tragedy

bull 11 dead

bull Environmental amp PR disaster

bull Blamed on ldquoa failure of

managementrdquo

bull ldquoThe costs of getting it wrong

have gone up a lotrdquo Ceres

bull Will liabilities of deepwater

mean that only the majors can

participate in US

bull Regulatory change bringing

US standards in line with best

practise

bull But US dependence on

deepwater is clear

bull Little long-term impact

elsewhere

US Gulf of Mexico Oil Production ( 2010 view)

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1993 1995 1997 1999 2001 2003 2005 2007 2009F 2011F 2013F 2015F

Barr

els

per

day (

000s)

Additional Deepwater Potential

Deepwater Oil

Shallow Water Oil

Deepwater

42 SUT London ndash February 2011

The next last offshore frontier

43 SUT London ndash February 2011

The Arctic

Credit Hugo Ahlenius UNEPGRID-Arendal

bull Over 400 fields discovered with

approx 240 bn Bboe

bull Further 412 bn Boe yet

undiscovered (USGS) technically

recoverable resources

bull Approx 84 offshore

bull 90 billion barrels (13) of the

worlds undiscovered oil reserves

and 30 of the gas resources

according to USGS

bull But USGS recently reduced

Alaska oil resources by 90

44 SUT London ndash February 2011

Some arctic projects

Norway - Goliat bull Predominantly oil

bull Extended shutdown now back on line

Cairn bull Two drilling rigs off coast of Greenland

bull Modestly promising results to date

Hebron ndash ExxonMobil bull East Canada

bull Fourth Newfoundland field

bull 400 ndash 700 m barrels 92 meters

bull First oil 2017

Shell bull Chukchi and Beaufort seas

bull Permits pulled

bull One year delay

bull Macondo will cast a long shadow

Goliat Source Eni Norge

Sevan 1000 Source Sevan

45 SUT London ndash February 2011

Lifecycle Opportunities

The easy oil goes first

NOCs need to internationalise

And local OFS companies

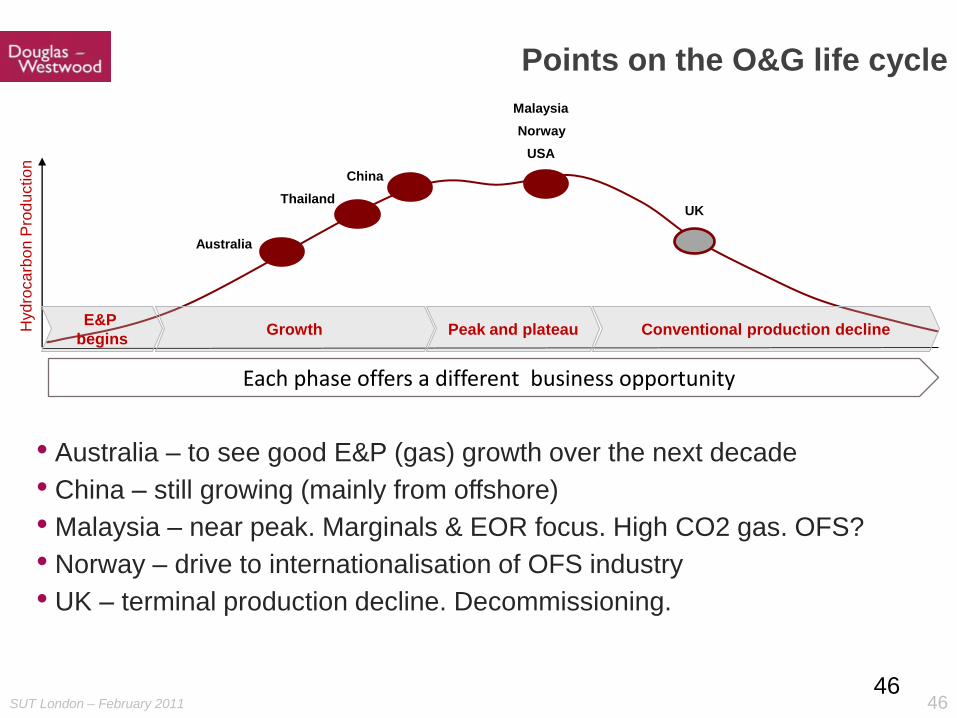

46 SUT London ndash February 2011

Hyd

roca

rbo

n P

rod

uctio

n

Australia

UK

China

Norway

Thailand

Malaysia

USA

46

Points on the OampG life cycle

bull Australia ndash to see good EampP (gas) growth over the next decade

bull China ndash still growing (mainly from offshore)

bull Malaysia ndash near peak Marginals amp EOR focus High CO2 gas OFS

bull Norway ndash drive to internationalisation of OFS industry

bull UK ndash terminal production decline Decommissioning

Growth Peak and plateau EampP

begins Conventional production decline

Each phase offers a different business opportunity

47 SUT London ndash February 2011

The significance of the national oil company

bull NOCs can be tasked with building a local supply chain

bull and building a knowledge base

bull Examples include

bull Petrobras ndash massive drive to build Brazilian OFS industry

bull Statoil ndash major RampD focus aids Norwegian companies

bull Petronas ndash a heavy focus on local needs

bull But ultimately local OampG production declines

bull Then NOCs need to access other countrieslsquo reserves

bull local OFS companies have to gain business in world markets

bull Then need to upscale and gain external investment

48 SUT London ndash February 2011

Conclusions

49 SUT London ndash February 2011

Conclusions

bull Global economic growth has resumed

bull Oil supply outlook remains restrained

bull Will OPEC answer the call for its nominal spare capacity

bull Oil prices are high but few visible drivers to push them down

bull OFS pricing competition should remain pronounced in 2011

bull Spare capacity in offshore sector rigs equipment services

bull High oil prices and restrained cost pressures should encourage

operators to bring projects forward ndash activity levels should pick up

bull Market players appear to be anticipating the next cycle

bull A good future for the Subsea IRM sector

50 SUT London ndash February 2011

Thank you

2 SUT London ndash February 2011

wwwdw-1com

Our Business

LNG

offshore

onshore

downstream

power

LNG

renewables

History and Locations

bull Established 1990

bull Aberdeen New York amp Canterbury

Setting up in Singapore

Activities amp Service Lines

bull Market research amp analysis

bull Commercial due-diligence

bull Business strategy amp advisory

bull Published market studies

Industry Sector Coverage

bull Oil amp Gas

bull Renewables

bull Power

Large Diversified Client Base

bull 650 projects 400 clients 70 countries

bull Leading global corporates

bull Energy majors and their suppliers

bull Investment banks amp PE firms

bull Government agencies

copy Douglas-Westwood Limited 2011

3 SUT London ndash February 2011

Financial Transaction Credentials Includehellip

Market amp commercial due diligence as part of financial transactions

is one of our largest activities

Further information at wwwdw-1com

copy Douglas-Westwood Limited 2009

euro670 acquisition by

Ferd Private Equity

Fund-raising for rig

newbuild programme

Acquisition by Cable

Solutions Group Inc pound319 million IPO

$768 million IPO Arcapita completes

acquisition of Roxar

Perry Slingsby Systems

capital acquired by Triton

Group Holdings pound535m finance facility

Songa Drilling

pound29 million

Refinancing

pound345 million Rovtech

acquired by Fugro

Acquisition Growth and

Working Capital Facilities

pound15 million MBO of

Motherwell Bridge

Expro Group $675m

acquisition of Powerwell

Services

Inflexion Private Equity

Backs pound22m MBO of

Viking Moorings

pound50 million credit facility

for Sovereigns

acquisition of Forfab

Investor syndicate

$925m acquisition of

ABB Oil amp Gas

$280m acquisition of

KBR Production

Services

pound130m debt facility

to finance the

construction of two

specialist vessels

Epcon Offshore AS

acquisition by M-I

SWACO

Serimer Holdings

acquisition of the UMAX

group

UMAX Ltd

Recapitalisation

pound755 million MBO $719 million IPO AGT Energy acquisition of

50 share of Oilflow

Solutions from Vienco

Management buyout of ESS

Steel Holdings

$305 million project

financing of FPSO RJS-409

(Espadarte Sul)

$180 million project

financing of FSO Cidade de

Macae MV15

Acquisition by

Inflexion Private

Equity

pound142m

acquisition by

Close Brothers

Private Equity

Sale of Motherwell

Bridge to Kuwait Finance

House

NOK 43 billion

joint acquisition

by First Reserve

amp DOF

Acquisition of

APAC division

by Champ

Ventures

Borets Group $150

million debt facility led

by EBRD

MBO backed by

HSBC Private

Equity

Acquisition by SCF

Partners

Acquisition of Anson by

NOV

Acquisition of ASEP by

NOV

Equity investments in

Advantec

4 SUT London ndash February 2011

Energy Macro Factors

Offshore Oil amp Gas

Lifecycle Opportunities

Conclusions

5 SUT London ndash February 2011

Energy Macro Factors

A global drive for energy that is

Sustainable

Secure

Affordable

A growing demand driven by

Population growth

GDP growth

6 SUT London ndash February 2011

The Importance of Oil

Oil is the fuel of

transportation

Demand is growing

Supplies are limited

Prices will rise

Other energy prices often

linked to oil

7 SUT London ndash February 2011 Source Financial Times London 5 January 2011

Source BP

Energy Consumption 1965-2009

00

05

10

15

20

25

30

35

40

45

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

Bill

ion to

nnes o

f o

il eq

uiv

ele

nt

North America

S amp Cent America

Europe amp Eurasia

Middle East

Africa

Asia Pacif ic

Energy Demand Growth ndash Historic amp Outlook

bull Energy demand growth outpaces population growth (95 v 55)

bull Close correlation between GDP growth and energy consumption

bull Recently driven by growth in China and India

8

bull Spring 08 ndash Spring 09 dramatic

drop in consumption of 5mbpd

from gt87mbpd

bull Strengthening recovery to new

peaks in consumption 876

bull Forecast for 2011 up 12 mbpd

compared to Jan 2010 forecast

bull OECD up modestly in 2010

bull US up 200k

bull EU up 200k

bull Japan down -150k

bull China up 6 +500k

bull Global consumption up 18

mbpd over last year

Source EIA STEO Jan 2010 and Jan 2011

EIA World Oil Consumption Actual and Forecast

million barrels per day (3 mma)

83

84

85

86

87

88

89

Mar

-07

Jul-

07

No

v-0

7

Mar

-08

Jul-

08

No

v-0

8

Mar

-09

Jul-

09

No

v-0

9

Mar

-10

Jul-

10

No

v-1

0

Mar

-11

Jul-

11

No

v-1

1

Actual

Jan 2010 Forecast

Jan 2011 Forecast

Short-term Outlook

9

bull Worldlsquos second largest economy 10 GDP growth

bull ―Astonishing oil demand growth

bull 18 million light vehicle sales vs 136 million prior year (126 m for US in 2010)

bull 120 million new cars by 2015 = all passenger vehicles UK + France + Germany

bull In 2010 China was 13 of total global oil demand growth (less than other Asia and

non-OECD)

bull Chinalsquos foreign oil dependence rises from 1 in 2 bbls to potentially 9 in 10 by 2030

Source EIA Douglas-Westwood Analysis

China Crude Oil Production and Constrained Demand

0

2

4

6

8

10

12

14

16

18

20

Mill

ions o

f barr

els

per

Day

Onshore oil production

Offshore oil production

Oil consumption

5

10

15

20

25

30

35

40

45

50

55

mill

ion b

arr

els

per

day

China as Japan(1960-1973)

China as Korea(1976-1996)

China - EIA IEO2010

Source EIA Douglas-Westwood Analysis

China Unconstrained Demand

Longer Term Outlook China Chinaand Others

For more information please

contact Douglas-Westwood

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

10

bull North Sea and Mexico continue

decline

bull Canada flat

bull Brazil underperforms

bull FSUmdashmostly Azerbaijanmdash

doing well

bull China and USA at front of the

pack

bull OPEC NGLs are leading the

way

bull Total world supply up 20 mbpd

half is NGLs

bull EIA expects 2011 largely flat

Source EIA STEO Jan 2011

World Liquids Production Growth 2010

million barrels per day

(600)

(400)

(200)

-

200

400

600

800

1000

Liquids Supply in 2010

11 SUT London ndash February 2011

bull Iraq

bull Output up 300 kbpd to 27 mbpd

bull Potential to increase by 05 mbpd per year to 6-7 mbpd

bull Bakken

bull Output up 80 kpbd to 380000 bpd

bull Potential to add 80 kbpd year potentially to greater than 1 mpbd or more

bull Like gas shales production is front-loaded

bull More to come from other sources

Supply Risks Iraq and Bakken

12

$50

$60

$70

$80

$90

$100

$110

$120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WTI

Cru

de

Oil

Spo

t P

rice

- A

nn

ual

B

asis

- C

urr

en

t D

olla

rs

Actual WTI

EIA - Reference Case

DWL - Base Case

bull We assume supply is flat to modestly increasing

bull Historically US could not add oil consumption at more than 4 of

GDPmdashequals $86

bull In last three months of 2010 US up 230 kbpd at average $85

bull US up 700 kbpd in December at $89

bull WTI at $92mdashabove our expectation of mid-to-high $80s for 2011

bull If US can reset to a higher tolerance for oil prices a substantial oil

price rally could be in store

Source EIA AEO ( adjusted RACC + $150) Douglas-Westwood

Annual WTI Spot Oil Price Forecasts EIA Douglas-Westwood

bull

Current oil price

Medium Term Oil Price Outlook

For more information please

contact Douglas-Westwood

13

0

20

40

60

80

100

Year 2030

Uppsala University

IEA EIA IOClsquos

Douglas-Westwood

Total Production Capacity

Current Production

Only material difference between

Uppsala and IEA is depletion rates

on fields to be discovered and

developed to 2030

Range of Global Oil Supply Forecasts ndash 2030 ndash All

Liquids Source various

bull Petroleum liquids

supply forecasts from

75 ndash 105 mbpd for

2030

bull All are essentially

peak oil forecasts

bull Quiet consensus has

emergedmdash

disagreements are

increasingly narrow

and specific

Long-term Outlook A Narrowing of Views

14

Oil Production ndash The Importance of Offshore

There is an increasing reliance on offshore and deepwater production

bull Offshore oil 25 of global production in 1990 31 in 2000 33 in 2010

and 34 by 2020

bull Deepwater 0 in 1990 2 in 2000 9 in 2010 13 by 2020

Global Oil Production 1950-2025

0

10

20

30

40

50

60

70

80

90

100

1930 1937 1944 1951 1958 1965 1972 1979 1986 1993 2000 2007 2014 2021

mill

ion b

arr

els

of

oil

per

day

Bitumen and Oil Sands

Offshore Deep

Offshore Shallow

Conventional Onshore

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

15

Peak Oil is a Reality

Data Petroleum Review May 2010

bull With most of the easy oillsquo in the hands of the NOCs

majors are scrambling to replace reserves and off-

set production decline

bull They are moving to harsh environments ndash offshore

deepwater politically difficult geographically remote

Peak Year

2002 2003 2004 2005 2006 2007 2008 2009

ExxonMobil 2496 2516 2571 2523 2681 2616 2404 2387

BP 2018 2121 2531 2562 2475 2414 2410 2535

PetroChina 2109 2119 2233 2270 2276 2312 2380 2311

Shell 2359 2379 2253 2093 2030 1899 1771 1680

Petrobras 1533 1701 1661 1847 1908 1920 1996 2103

Chevron 1897 1823 1737 1701 1759 1783 1676 1872

Total 1589 1661 1695 1621 1506 1509 1456 1381

ConocoPhillips 891 1237 1242 1447 1698 1644 1367 1615

ENI 921 981 1034 1111 1079 1020 1026 1007

StatoilHydro 1112 1132 1135 1102 1058 1054 1056 1067

Source Offshore Technology

NOCs (limited equity access )

78

NOCs (equity access)

10

New Russian Companies

6

Full IOC access6

Restricted access to oil reserves

16 SUT London ndash February 2011

85

86

87

88

89

90

91

92

93

94

95

2009 2010 2011 2012 2013

mill

ion

bar

rels

pe

r d

ay

Demand Growth as 2002-2005

Demand Growth as 1976-1979

IEA Supply Demand Forecast

Effective Global Liquids Production Capacity

Medium term outlook risks of oil shock growing

bull Adequate spare capacity today ndash

but frac34 of it is in Saudi

bull IEA sees demand rising slowly

less than 14 mbpd year in 2011

bull Previous recoveries saw strong

demand growth during first three

years

bull After 2002 77 mbpd

bull After 1976 73 mbpd

bull If previous patterns hold true a

possible supply crunch in

20122013

bull What will Saudi do Source IEA Douglas-Westwood analysis

Oil Demand under Three Scenarios and Global

Liquids Production Capacity

Oil shock

IEA forecast (2010)

Surplus Capacity

bull Dec 2010 demand

Spare Capacity at Saudi 10 mbpd limit

bull Jan 2011 forecast

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

17 SUT London ndash February 2011

The WikiLeaks Saudi cables

Crude oil reserves may have been overstated by as much as 300bn barrels

ndash nearly 40

bull Al-Husseini [believes] Aramcos reserves are overstated by as much

as 300bn barrels In his view once 50 of original proven reserves has

been reached hellip a steady output in decline will ensue and no amount of

effort will be able to stop it He believes that what will result is a plateau in

total output that will last approximately 15 years followed by decreasing

outputldquo

bull ldquoClearly they [Saudi] can drive prices up but we question whether they

any longer have the power to drive prices down for a prolonged periodrdquo

Source US Embassy cables to Washington 2007-2009 The Guardian 8 February 2010

Sadad al-Husseini a geologist and former head of exploration at the Saudi oil monopoly Aramco met the US

consul general in Riyadh in November 2007

18

United States

Russia

Iran

Qatar

Other OPEC

Rest of World

100

yearslsquo

US

supply

05

10

15

20

25

30

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Btu ratio Oil-to-Gas

Avg ratio Feb 2010 -Dec 2018Avg ratio 1998 - 2005

Oil-to-Gas Price Ratio on a BTU Parity Basis Source EIA NYMEX futures

Proved Gas Reserves 6300 trillion cubic feet (60 years) Source EIA

bull Gas shales have revolutionized US outlook

bull 100 yearslsquo supply in US resources 2 quadrillion cf resources on 23 tcf consumption

bull Some questions about economics but $7-8 mmbtu gas looks plausible indefinitely

bull Other shale initiatives beginning (BP in China)

bull Major LNG projects continue to come on line

bull Right now the world looks to have plenty of natural gas

The Gas Story is Very Different

For more information please

contact Douglas-Westwood

19 SUT London ndash February 2011

bull Dominated by E Europe amp FSU but others to see significant growth

bull Deepwater gas and LNG to be of growing importance

bull Impact of shale gas on North America (amp other markets)

bull But local supply issues eg Europe to import gt73 by 2020

Natural gas production and use to soar

Source Energyfiles

0

10

20

30

40

50

60

70

80

90

100

1930 1937 1944 1951 1958 1965 1972 1979 1986 1993 2000 2007 2014 2021

million b

arr

els

of o

il eq

uiv

ale

nt p

er d

ay

Africa

Asia

Australasia

Eastern Europe amp FSU

Latin America

Middle East

North America

Western Europe

ME

FSU

NA

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

20 SUT London ndash February 2011

10

2428

31

3941

47 48

5356

60

0

1

2

3

4

5

6

Capex ($ m

llion m

W)

Source EIA Nov 2010

Gas ndash lowest Capex for power plants

21 SUT London ndash February 2011

Gas ndash FLNG in prospect

bull Liquefaction ndash $20 bn spend by 2017

bull Australasia to account for 60

bull Woodside has raised the prospect of FLNG for its Greater Sunrise project

bull Inpex (Japan) considering FLNG at its $196 billion Abadi field in Indonesia

bull GDF Suez and Australias Santos set up a joint venture to develop a floating

LNG project off northwest Australia

Picture Shell

Source The World FLNG Report Douglas-Westwood

0

1

2

3

4

5

6

7

8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Exp

en

ditur

e ($ b

illio

n)

Africa

Asia

Australasia

Latin America

Middle East

North America

0

1

2

3

4

5

6

7

8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Exp

en

ditur

e ($ b

illio

n)

Africa

Asia

Australasia

Latin America

Middle East

North America

$67bn

For more information please

contact Douglas-Westwood

22 SUT London ndash February 2011

$0

$100

$200

$300

$400

$500

$600

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

US

Do

llar

Bil

lio

ns

Outside North America

Canada

United States

bull Recovery in 2010 up 10 to $442 bn

bull Continued growth in 2011 to $490 bn up 11 a new peak

bull US spend up 8 Canada up 5 international up 12

bull Spend up $48 bn in 2011 of which 82 is international

Recovery and growth in global EampP spend

Source Jim Crandell Barclaylsquos EampP Spending Survey December 2010

Global EampP Spend

+10 -15 +11

23 SUT London ndash February 2011

0

10

20

30

40

50

60

70

80

90

100

$70 $75 $80 $85 $90 $95 $100

Cu

mu

lati

ve P

erc

en

t o

f R

esp

on

de

nts

0

10

20

30

40

50

60

70

80

90

100

$35 $40 $45 $50 $55 $60 $65 $70 $75

Cu

mu

lati

ve P

erc

en

t o

f R

esp

on

de

nts

bull EampP companies prepared budgets assuming $77 oil on average

up from $70 last year

bull Expect capex to materially decrease in the industry if oil prices fall

much below $60

bull Expect capex to increase materially if oil prices sustain above $90

up from $85 last year

Source Barclays Capital EampP Spending Survey Dec2010

Oil Price Threshold for Reducing Capex Oil Price Threshold for Increasing Capex

Source Barclays Capital EampP Spending Survey Dec2010

Percent of Respondents Decreasing Capex at a Given Oil Price

Percent of Respondents Increasing Capex at a Given Oil Price

2011 ndash EampP Spend Sensitivity to Oil Prices

24 SUT London ndash February 2011

Offshore Oil amp Gas

Nowhere else left for big finds

Strong Capex growth

Importance of deepwater

The beauty of Opex

25 SUT London ndash February 2011

Global offshore oil amp gas production amp spend to grow

Source Datamonitor

bull Global Capex fell in lsquo0910 but Opex grew

bull Both Capex amp Opex to grow strongly in the years ahead

bull 28 new rigs ordered since October + 8 options 10-15 more in 2011

bull Deepwater Capex to exceed $205 billion

0

20

40

60

80

100

120

140

160

180

200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ex

pe

nd

itu

re ($

bill

ion

s)

AfricaAsiaAustralasiaEastern Europe and FSULatin AmericaMiddle EastNorth AmericaWestern Europe For more information please

contact Douglas-Westwood

26 SUT London ndash February 2011

OPTIONS

ORDERS

The next rig cycle begins

27 SUT London ndash February 2011

Deepwater Capex to reach new highs

bull Deepwater production to double

bull Drilling $72bn (35) Subsea processing emerging ($26 bn)

Source ldquoThe World Deepwater Market Report 2011-2015rdquo

Douglas-Westwood

0

10

20

30

40

50

60

70

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e ($ b

illio

ns)

DrillingFloating PlatformsPipelinesSubsea ProductionSubsea ProcessingSURF

For more information please

contact Douglas-Westwood

28 SUT London ndash February 2011

Deepwater ndash Africa amp Brazil to lead spend

bull Brazil amp W Africa to total $126bn (62)

bull But much more Brazil spend to come

Source ldquoThe World Deepwater Market Report 2011-2015rdquo

Douglas-Westwood

0

10

20

30

40

50

60

70

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e ($ b

illio

ns)

AfricaAsiaAustralasiaEastern Europe and FSULatin AmericaMiddle EastNorth AmericaWestern Europe

For more information please

contact Douglas-Westwood

29 SUT London ndash February 2011

Brazil ndash Petrobrasrsquos pre-salt deepwater lsquoshopping listrsquo

50 bn boe reserves 2 million production bpd by 2020

By 2018

bull Includes 58 new drilling rigs

By 2020

bull 72 VLCCs

bull 146 supply amp service vessels

bull 45 production platforms

bull Plus subsea hardware

Finance

bull 2010 $70bn stock offering

bull 2011 $6bn corporate bond

bull Next 4 years $30-40bn debt raising

bull Capex of $224bn by 2014

bull Capex amp Opex to total $1 trillion

Tupi Discovery Source CGG Veritas

30 SUT London ndash February 2011

Floating production recovery expected

Global Floating Production Expenditure Source Douglas-Westwood

bull Material decrease in orders in 2009 but market bottomed in 2010

bull Increasing share of market to leased FPSOs Consolidation likely

bull Deepwater Horizon unlikely to impact GoM small part of the market

bull Long term gt200 prospects exist and growth will return

bull Market to reach $16 billion in 2014

0

2

4

6

8

10

12

14

16

18

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e ($ b

illio

ns)

AfricaAsiaAustralasiaEE amp FSULatin AmericaMiddle EastNorth AmericaWestern Europe

For more information please

contact Douglas-Westwood

31 SUT London ndash February 2011

Subsea

Hardware

Operational Demands

Inspection Maintenance Repair

Well intervention

ROV AUV and Subsea Vessels

Operations Market

32 SUT London ndash February 2011

Subsea technology is vital to offshore production

bull Unlocking deepwater reserves

bull Improving economics of marginal fields in shallow waters

bull Tie-backs of small reservoirs into existing facilities

Subsea ndash long term outlook is sound

0

5

10

15

20

25

30

35

40

45

50

0

10

20

30

40

50

60

70

80

2001 2004 2007 2010 2013 2016 2019 2022 2025

Mill

ion B

oep

d

Topside ProductionSubsea Production Subsea Production

Offshore Production 2000-2025 Source Datamonitor

For more information please

contact Douglas-Westwood

33 SUT London ndash February 2011

$0

$5

$10

$15

$20

$25

$30

$35

$40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exp

en

ditur

e $

bn

Africa AsiaAustralasia Eastern Europe amp FSULatin America Middle EastNorth America NorwayRoWE UK

bull $135 billion forecast for next five years

bull Pipelines to account for half of forecast expenditure

bull Major pipeline projects in Eastern Europe amp FSU Asia and the Middle

East

bull Subsea production hardware SURF and subsea processing driven by

deepwater regions

Source FMC Technologies

Subsea Hardware

For more information please

contact Douglas-Westwood

34 SUT London ndash February 2011

0

10

20

30

40

50

60

70

80

Mill

ion B

oepd

Incremental ProductionLost through DeclineProduction Base

Global Offshore Production 2010-2015 Source Datamonitor

bull 462 million boepd in 2010

bull Average global decline rates of 51 (115 in North Sea)

bull Substantial investment in operational expenditure to be required

Operational demands intensifying

For more information please

contact Douglas-Westwood

35 SUT London ndash February 2011

Offshore ops amp maint spend to see good growth

Source ldquoThe World Offshore Operations amp Maintenance Market Report 2010-14rdquo

Douglas-Westwood

$0

$10

$20

$30

$40

$50

$60

$70

$80

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$bill

ions

AfricaAsia-PacificEastern Europe amp FSULatin AmericaMiddle EastNorth AmericaNorwayUKRest of Europe

bull gt7000 fixed amp gt200 floating platforms

bull Plus demand for major modifications

Fo

r more

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

36 SUT London ndash February 2011

Subsea IRM Expenditure 2004-2015 Source Douglas-Westwood

bull Over 7000 production platforms 190000km of pipeline currently installed

bull $28 billion of expenditure in Subsea IRM in 2010

bull Nearly $20 billion of further investment expected over the next five years

bull 55 forecast expenditure expected in the North Sea amp Gulf of Mexico

bull Less exposure to market cyclicality

00

10

20

30

40

50

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$m

illio

ns

Others

Western Europe

North America

Latin America

Asia-Pacific

Africa

Subsea Inspection Repair amp Maintenance

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

37 SUT London ndash February 2011

Subsea Well Intervention Expenditure 2004-2015 Source Douglas-Westwood

bull Demand driven by production decline of existing wells Nearly 4000 active

bull Market has been historically been constrained by technology amp economics

bull Deepwater intervention to become increasingly significant to global demand

00

05

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$bill

ions

Others

Western Europe

North America

Latin America

Asia-Pacific

Africa

Subsea Well Intervention

For more information please

contact Douglas-Westwood

38 SUT London ndash February 2011

320

370

420

470

520

570

620

$00

$05

$10

$15

$20

$25

$30

$35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Ac

tiv

e R

OV

s

Ex

pe

nd

itu

re ($

billio

ns

)

Africa

Asia Pacific

E EuropeFSU

Latin America

Middle East

North America

Western Europe

Active ROVs

The World Work Class ROV Operations Market 2005-2014

(Oil amp Gas) Source ―The World ROV Report 2010-2014 ndash Douglas-Westwood

ROV Paces the Growth of Deepwater

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

39 SUT London ndash February 2011

bull Self-guided under water survey and inspection vessels

bull From 1 to 5 meters long

bull Priced from $150000 to $7 million

bull Very hot topic recentlymdashmilitary contractors looking for commercial

applications

bull Greater acceptance for not only deep but shallow water oil and gas

survey

bull But a small market

Hugin 1000 MR AUV Courtesy Kongsberg Marine

AUV ndash Autonomous Underwater Vehicles

40 SUT London ndash February 2011

Subsea Vessel Operations Market

Subsea Operation Vessel Demand by Workscope Source Douglas-Westwood

bull Current IRM market demand for around 92 vessels

bull Field development market still depressed ndash upturn in 2012 amp beyond

bull Well intervention and PampA to see substantial growth

-

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

V

essels

Intervention amp PampA

Field Development

Inspection Repair amp Maintenance

For m

ore

info

rmatio

n p

lease

conta

ct D

ougla

s-W

estw

ood

41 SUT London ndash February 2011

Macondo ndash a $40 billion tragedy

bull 11 dead

bull Environmental amp PR disaster

bull Blamed on ldquoa failure of

managementrdquo

bull ldquoThe costs of getting it wrong

have gone up a lotrdquo Ceres

bull Will liabilities of deepwater

mean that only the majors can

participate in US

bull Regulatory change bringing

US standards in line with best

practise

bull But US dependence on

deepwater is clear

bull Little long-term impact

elsewhere

US Gulf of Mexico Oil Production ( 2010 view)

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1993 1995 1997 1999 2001 2003 2005 2007 2009F 2011F 2013F 2015F

Barr

els

per

day (

000s)

Additional Deepwater Potential

Deepwater Oil

Shallow Water Oil

Deepwater

42 SUT London ndash February 2011

The next last offshore frontier

43 SUT London ndash February 2011

The Arctic

Credit Hugo Ahlenius UNEPGRID-Arendal

bull Over 400 fields discovered with

approx 240 bn Bboe

bull Further 412 bn Boe yet

undiscovered (USGS) technically

recoverable resources

bull Approx 84 offshore

bull 90 billion barrels (13) of the

worlds undiscovered oil reserves

and 30 of the gas resources

according to USGS

bull But USGS recently reduced

Alaska oil resources by 90

44 SUT London ndash February 2011

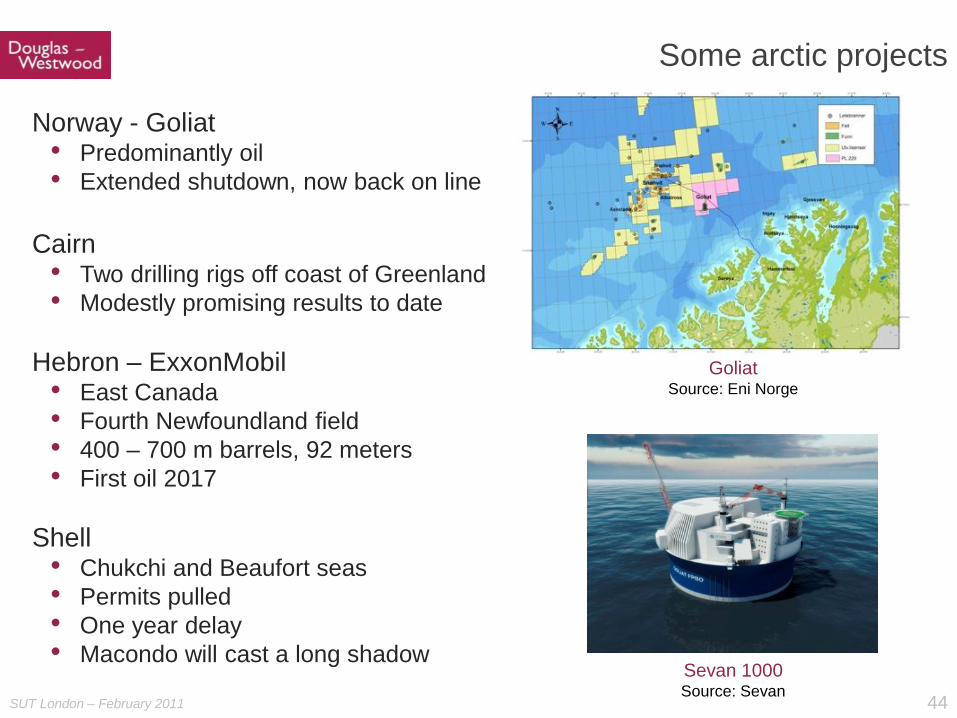

Some arctic projects

Norway - Goliat bull Predominantly oil

bull Extended shutdown now back on line

Cairn bull Two drilling rigs off coast of Greenland

bull Modestly promising results to date

Hebron ndash ExxonMobil bull East Canada

bull Fourth Newfoundland field

bull 400 ndash 700 m barrels 92 meters

bull First oil 2017

Shell bull Chukchi and Beaufort seas

bull Permits pulled

bull One year delay

bull Macondo will cast a long shadow

Goliat Source Eni Norge

Sevan 1000 Source Sevan

45 SUT London ndash February 2011

Lifecycle Opportunities

The easy oil goes first

NOCs need to internationalise

And local OFS companies

46 SUT London ndash February 2011

Hyd

roca

rbo

n P

rod

uctio

n

Australia

UK

China

Norway

Thailand

Malaysia

USA

46

Points on the OampG life cycle

bull Australia ndash to see good EampP (gas) growth over the next decade

bull China ndash still growing (mainly from offshore)

bull Malaysia ndash near peak Marginals amp EOR focus High CO2 gas OFS

bull Norway ndash drive to internationalisation of OFS industry

bull UK ndash terminal production decline Decommissioning

Growth Peak and plateau EampP

begins Conventional production decline

Each phase offers a different business opportunity

47 SUT London ndash February 2011

The significance of the national oil company

bull NOCs can be tasked with building a local supply chain

bull and building a knowledge base

bull Examples include

bull Petrobras ndash massive drive to build Brazilian OFS industry

bull Statoil ndash major RampD focus aids Norwegian companies

bull Petronas ndash a heavy focus on local needs

bull But ultimately local OampG production declines

bull Then NOCs need to access other countrieslsquo reserves

bull local OFS companies have to gain business in world markets

bull Then need to upscale and gain external investment

48 SUT London ndash February 2011

Conclusions

49 SUT London ndash February 2011

Conclusions

bull Global economic growth has resumed

bull Oil supply outlook remains restrained

bull Will OPEC answer the call for its nominal spare capacity

bull Oil prices are high but few visible drivers to push them down

bull OFS pricing competition should remain pronounced in 2011

bull Spare capacity in offshore sector rigs equipment services

bull High oil prices and restrained cost pressures should encourage

operators to bring projects forward ndash activity levels should pick up

bull Market players appear to be anticipating the next cycle

bull A good future for the Subsea IRM sector

50 SUT London ndash February 2011

Thank you

3 SUT London ndash February 2011

Financial Transaction Credentials Includehellip

Market amp commercial due diligence as part of financial transactions

is one of our largest activities

Further information at wwwdw-1com

copy Douglas-Westwood Limited 2009

euro670 acquisition by

Ferd Private Equity

Fund-raising for rig

newbuild programme

Acquisition by Cable

Solutions Group Inc pound319 million IPO

$768 million IPO Arcapita completes

acquisition of Roxar

Perry Slingsby Systems

capital acquired by Triton

Group Holdings pound535m finance facility

Songa Drilling

pound29 million

Refinancing

pound345 million Rovtech

acquired by Fugro

Acquisition Growth and

Working Capital Facilities

pound15 million MBO of

Motherwell Bridge

Expro Group $675m

acquisition of Powerwell

Services

Inflexion Private Equity

Backs pound22m MBO of

Viking Moorings

pound50 million credit facility

for Sovereigns

acquisition of Forfab

Investor syndicate

$925m acquisition of

ABB Oil amp Gas

$280m acquisition of

KBR Production

Services

pound130m debt facility

to finance the

construction of two

specialist vessels

Epcon Offshore AS

acquisition by M-I

SWACO

Serimer Holdings

acquisition of the UMAX

group

UMAX Ltd

Recapitalisation

pound755 million MBO $719 million IPO AGT Energy acquisition of

50 share of Oilflow

Solutions from Vienco

Management buyout of ESS

Steel Holdings

$305 million project

financing of FPSO RJS-409

(Espadarte Sul)

$180 million project

financing of FSO Cidade de

Macae MV15

Acquisition by

Inflexion Private

Equity

pound142m

acquisition by

Close Brothers

Private Equity

Sale of Motherwell

Bridge to Kuwait Finance

House

NOK 43 billion

joint acquisition

by First Reserve

amp DOF

Acquisition of

APAC division

by Champ

Ventures

Borets Group $150

million debt facility led

by EBRD

MBO backed by

HSBC Private

Equity

Acquisition by SCF

Partners

Acquisition of Anson by

NOV

Acquisition of ASEP by

NOV

Equity investments in

Advantec

4 SUT London ndash February 2011

Energy Macro Factors

Offshore Oil amp Gas

Lifecycle Opportunities

Conclusions

5 SUT London ndash February 2011

Energy Macro Factors

A global drive for energy that is

Sustainable

Secure

Affordable

A growing demand driven by

Population growth

GDP growth

6 SUT London ndash February 2011

The Importance of Oil

Oil is the fuel of

transportation

Demand is growing

Supplies are limited

Prices will rise

Other energy prices often

linked to oil

7 SUT London ndash February 2011 Source Financial Times London 5 January 2011

Source BP

Energy Consumption 1965-2009

00

05

10

15

20

25

30

35

40

45

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

Bill

ion to

nnes o

f o

il eq

uiv

ele

nt

North America

S amp Cent America

Europe amp Eurasia

Middle East

Africa

Asia Pacif ic

Energy Demand Growth ndash Historic amp Outlook

bull Energy demand growth outpaces population growth (95 v 55)

bull Close correlation between GDP growth and energy consumption

bull Recently driven by growth in China and India

8

bull Spring 08 ndash Spring 09 dramatic

drop in consumption of 5mbpd

from gt87mbpd

bull Strengthening recovery to new

peaks in consumption 876

bull Forecast for 2011 up 12 mbpd

compared to Jan 2010 forecast

bull OECD up modestly in 2010

bull US up 200k

bull EU up 200k

bull Japan down -150k

bull China up 6 +500k

bull Global consumption up 18

mbpd over last year

Source EIA STEO Jan 2010 and Jan 2011

EIA World Oil Consumption Actual and Forecast

million barrels per day (3 mma)

83

84

85

86

87

88

89

Mar

-07

Jul-

07

No

v-0

7

Mar

-08

Jul-

08

No

v-0

8

Mar

-09

Jul-

09

No

v-0

9

Mar

-10

Jul-

10

No

v-1

0

Mar

-11

Jul-

11

No

v-1

1

Actual

Jan 2010 Forecast

Jan 2011 Forecast

Short-term Outlook

9

bull Worldlsquos second largest economy 10 GDP growth

bull ―Astonishing oil demand growth

bull 18 million light vehicle sales vs 136 million prior year (126 m for US in 2010)

bull 120 million new cars by 2015 = all passenger vehicles UK + France + Germany

bull In 2010 China was 13 of total global oil demand growth (less than other Asia and

non-OECD)

bull Chinalsquos foreign oil dependence rises from 1 in 2 bbls to potentially 9 in 10 by 2030

Source EIA Douglas-Westwood Analysis

China Crude Oil Production and Constrained Demand

0

2

4

6

8

10

12

14

16

18

20

Mill

ions o

f barr

els

per

Day

Onshore oil production

Offshore oil production

Oil consumption

5

10

15

20

25

30

35

40

45

50

55

mill

ion b

arr

els

per

day

China as Japan(1960-1973)

China as Korea(1976-1996)

China - EIA IEO2010

Source EIA Douglas-Westwood Analysis

China Unconstrained Demand

Longer Term Outlook China Chinaand Others