the global outlook for the resources sector · 2006. 9. 27. · consensus economics, consensus...

TRANSCRIPT

economics@

Presentation to Presentation to

CPA Australia CPA Australia Western Resources ConventionWestern Resources Convention

The global outlook for the resources sector

The global outlook for The global outlook for the resources sectorthe resources sector

Saul EslakeSaul EslakeChief EconomistChief EconomistANZANZ

Duxton HotelDuxton HotelPerthPerth

2727thth September 2006September 2006

www.anz.com/go/economicswww.anz.com/go/economicswww.anz.com/go/economics

economics@2

Yet in fact the world economy is doing remarkably well, and likely to continue doing soYet in fact the world economy is doing remarkably Yet in fact the world economy is doing remarkably well, and likely to continue doing sowell, and likely to continue doing so

Global economic growth

0

1

2

3

4

5

6

7

8

70 74 78 82 86 90 94 98 02 06

Real % change from previous year

Long-term trend

Note: GDP is measured in US$ at purchasing power parities.Source: IMF; Economics@ANZ.

economics@3

Global growth is being increasingly driven by developing economies ….Global growth is being increasingly driven by Global growth is being increasingly driven by developing economies ….developing economies ….

0

1

2

3

4

5

6

7

70 74 78 82 86 90 94 98 02 06

Real % change from previous year

‘Advanced’ economies

‘Advanced’ economies comprise the US, Western Europe, Japan, Canada, Australia and New Zealand. Sources: IMF, World Economic Outlook September 2006 database; Economics@ANZ.

`

0

1

2

3

4

5

6

7

8

9

70 74 78 82 86 90 94 98 02 06

Real % change from previous year

‘Developing’ economies

Long-termtrend

Trend 1970-1991

Trend 1992-2006

Real GDP growth 1970-2008

economics@4

… which now account for just over 50% of world GDP … which now account for just over 50% of world … which now account for just over 50% of world GDP GDP

‘Advanced’ economies comprise the US, Western Europe, Japan, Canada, Australia and New Zealand Sources: IMF, World Economic Outlook; Angus Maddison, The World Economy: Historical Statistics; Economics@ANZ.

20

30

40

50

60

70

80

90

80 85 90 95 00 05 10

%

'Emerging' or'developing' economies

'Advanced'economies

Shares of world GDP growth

and over 60% of the growth in world GDPand over 60% of the and over 60% of the growthgrowth in world GDPin world GDP

35

40

45

50

55

60

65

50 60 70 80 90 00 10

%

'Emerging' or'developing' economies

'Advanced' economies

Shares of world GDP

economics@5

The world economy in ten years’ timeThe world economy in ten years’ time

13994Korea

17

1211=9=9

8=6=6

54321

Rank

630

1,0731,1051,5771,5761,6681,8301,8332,5223,6333,9119,412

12,278

US$bn

GDP in 2005

Canada

BrazilItalyFranceUnited Kingdom

Australia

Mexico

Russia

GermanyIndiaJapanChinaUnited States

Note: GDP figures are converted to US$ at purchasing power parities (PPPs), not market exchange rates. Forecasts are ‘consensus forecasts’ Sources: IMF, World Economic Outlook September 2006; Consensus Economics, Consensus Forecasts April 2006; ANZ.

14977Indonesia

=121,550

141,450

875

1,550

2,7002,2251,9502,2502,3002,9006,6004,600

20,65016,800

US$bn

GDP in 2015

=810=8

7

19

=12

6

53412

Rank

111,7504.6

3.3

3.72.75.53.61.52.12.31.56.51.68.03.1

GDP growth,

2006-2015 (f)

5.9

economics@6

China and India are reclaiming their historical position as the world’s largest economiesChina and India are reclaiming their historical China and India are reclaiming their historical position as the world’s largest economiesposition as the world’s largest economies

Shares of world GDP, 0 – 2015 AD

Source: Angus Maddison, The World Economy: A Millennial Perspective, OECD Development Centre, 2001; IMF, World Economic Outlook Database, September 2005; Consensus Economics, Consensus Forecasts, October 2005; Economics@ANZ.

0

5

10

15

20

25

30

35

40

0 1000 1500 1600 1700 1820 1870 1913 1950 1973 1998 2005 2015

%

China

Western Europe

US

India

economics@7

Oil prices have been at elevated levels for some time now, and seem likely to remain soOil prices have been at elevated levels for some Oil prices have been at elevated levels for some time now, and seem likely to remain sotime now, and seem likely to remain so

Nominal and real oil prices

0

10

20

30

40

50

60

70

80

90

100

70 75 80 85 90 95 00 05 10

US$ per barrel

Oil price incurrent dollars

Futurespricesas at

21 Sep2006

Oil price in2005 dollars

Note: Oil price is West Texas Intermediate. Shaded periods indicate ‘oil shocks’. Source: Thomson Financial Datastream; Bloomberg; US Bureau of Labor Statistics; Economics@ANZ.

economics@8

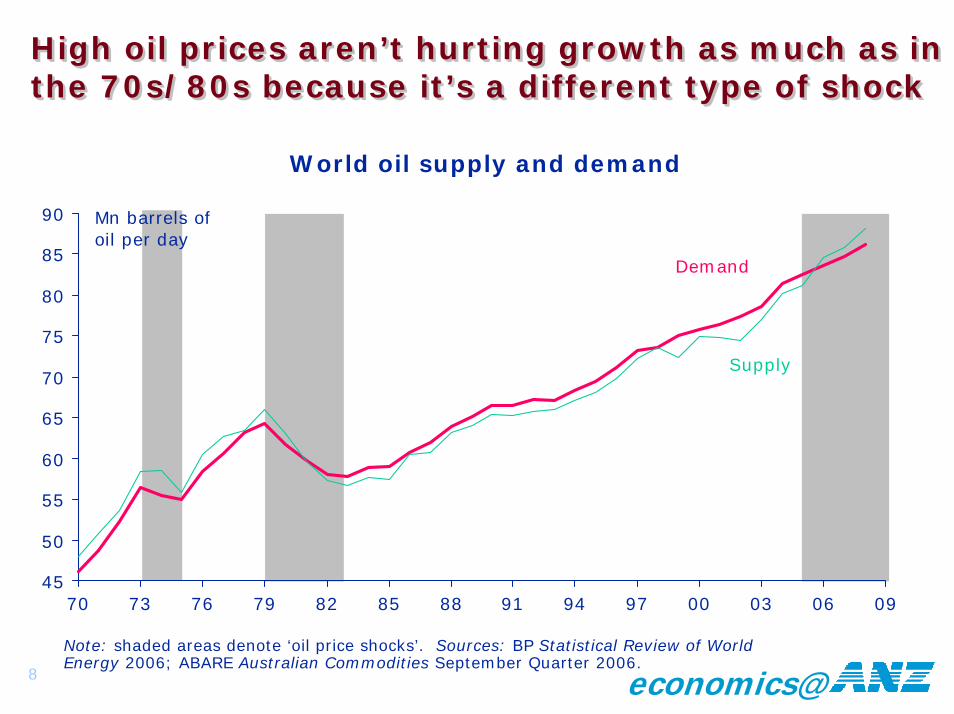

High oil prices aren’t hurting growth as much as in the 70s/80s because it’s a different type of shockHigh oil prices aren’t hurting growth as much as in High oil prices aren’t hurting growth as much as in the 70s/80s because it’s a different type of shockthe 70s/80s because it’s a different type of shock

World oil supply and demand

45

50

55

60

65

70

75

80

85

90

70 73 76 79 82 85 88 91 94 97 00 03 06 09

Mn barrels ofoil per day

Demand

Supply

Note: shaded areas denote ‘oil price shocks’. Sources: BP Statistical Review of World Energy 2006; ABARE Australian Commodities September Quarter 2006.

economics@9

Developing countries now account for over threeDeveloping countries now account for over three--quarters of world crude oil demand quarters of world crude oil demand

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

90 93 96 99 02 05

Developing economies

Advanced economies

Millions of barrels per day

Growth in worldoil demand

Oil consumption

15

20

25

30

35

40

45

70 75 80 85 90 95 00 05

Millions of barrels per day

'Advanced'economies

Developing oremerging economies

Note: ‘advanced economies’ are the US, Western Europe, Japan, Canada, Australia and New Zealand. Sources: BP Statistical Review of World Energy 2006; Economics@ANZ.

economics@10

Developing country demand for oil is likely to grow rapidly as incomes riseDeveloping country demand for oil is likely to Developing country demand for oil is likely to grow rapidly as incomes risegrow rapidly as incomes rise

Oil consumption and GDP per capita, 2005

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40 45

Barrels

GDP (at purchasing power parities) per capita

Oil

consu

mption p

er

capita

US$000

USCanada

Australia

Japan

Germany

Korea

UKFrance

Spain

Russia

Sth AfricaBrazil

Mexico

Argentina

Taiwan

ChinaIndia

Thailand Malaysia

Indonesia

Sources: The Economist ‘Survey of the World Economy’ 16 September 2006 p. 20; BP Statistical Review of World Energy 2005; IMF World Economic OutlookSeptember 2006; Economics@ANZ.

economics@11

Higher oil prices aren’t (thus far) leading to higher inflation and interest ratesHigher oil prices aren’t (thus far) leading to Higher oil prices aren’t (thus far) leading to higher inflation and interest rateshigher inflation and interest rates

Oil prices and inflation Oil prices and interest rates

0

10

20

30

40

50

60

70

80

90

100

70 74 78 82 86 90 94 98 02 060

2

4

6

8

10

12

14

16US$ per barrel(2005 prices)

Real oilprices

% per annum

G7 3-mth interest rates(right scale)

`

0

10

20

30

40

50

60

70

80

90

100

70 74 78 82 86 90 94 98 02 060

2

4

6

8

10

12

14

16US$ per barrel(2005 prices)

Real oil prices

% change fromyear earlier

G7 consumer prices (right scale)

Sources: Datastream; OECD; [email protected]: Shaded areas denote “oil price shocks”

economics@12

Metal prices are at record highs in nominal terms though below previous peaks in real termsMetal prices are at record highs in nominal terms Metal prices are at record highs in nominal terms though below previous peaks in real termsthough below previous peaks in real terms

Nominal and real metal prices

0

50

100

150

200

250

300

56 61 66 71 76 81 86 91 96 01 06

Index: 2000 = 100

Nominal terms

Deflated byUS CPI

Source: IMF International Financial Statistics;Economics@ANZ.

economics@13

China is now the major influence on global demand for base metals and steelChina is now the major influence on global China is now the major influence on global demand for base metals and steeldemand for base metals and steel

1993-2002 2002-2005

Contribution to growth (%) of

Contribution to growth (%) of

Other EMs* China

9

15

15

-11

11

16

10

48

51

110

87

54

86

113

World consum

-ption growth†

World consum

-ption growth† China

Other EMs*

Aluminium 3.8 38

43

42

12

38

34

42

7.6 9

Copper 3.5 3.8 41

Lead 3.0 4.3 -7

Nickel 4.4 3.6 -11

Steel 3.4 9.2 8

Tin 1.3 8.1 2

Zinc 3.4 3.8 7

† % pa * Emerging Markets (India, Russia, Brazil and Mexico)Source: IMF World Economic Outlook, September 2006 Table 5.3.

economics@14

Base metal consumption in developing countries is likely to grow strongly over timeBase metal consumption in developing Base metal consumption in developing countries is likely to grow strongly over timecountries is likely to grow strongly over time

Base metal consumption and GDP per capita, 2004

0

10

20

30

40

50

60

70

80

0 5 10 15 20 25 30 35 40

Tons

GDP (at purchasing power parities) per capita

Base

meta

l co

nsu

mption p

er

capita

US$000

US

Canada

Australia

Japan

Germany

Korea

UK

FranceSpain

Russia

Sth AfricaBrazil Mexico

Taiwan

China

India

Thai-land

Malaysia

Indo-nesia

Italy

Sources: ABARE Australian Commodities 2006; IMF World Economic OutlookSeptember 2006; Economics@ANZ.

economics@15

Per capita consumption of base metals and steel typically rises with income up to US$15-20,000 Per capita consumption of base metals and steel Per capita consumption of base metals and steel typically rises with income up to US$15typically rises with income up to US$15--20,000 20,000

China

Korea

EU

US

0

5

10

15

20

25

30

0 10 20 30 40

Kgs

Real GDP (at PPP) per capita

Alu

min

ium

con

sum

pti

on p

er c

apit

a

US$000Japan

Aluminium

China

Korea

EU

US

0

100

200

300

400

500

600

700

800

900

1000

0 10 20 30 40

Kgs

Real GDP (at PPP) per capita

Ste

el c

onsu

mpti

on p

er c

apit

a

US$000

Japan

Steel

Sources: IMF World Economic Outlook September 2006; (Figure 5.7); Economics@ANZ.

economics@16

Metal supply has responded more slowly to the acceleration in demand than in earlier cyclesMetal supply has responded more slowly to the Metal supply has responded more slowly to the acceleration in demand than in earlier cyclesacceleration in demand than in earlier cycles

Mining companies have to some extent been surprised at the strength of the upturn in demand

– industry views on the outlook for prices were generally pessimistic in the aftermath of the Asian economic crisis

The mining industry globally is more consolidated than in previous cycles

– companies are more conscious of the impact that an increase in their own production may have on prices

Mining companies now have alternative ways of spending windfall cash flows

– expanding exploration or production is no longer the first instinct

– takeovers, ‘special dividends’ and share buybacks are now much more common-place among mining companies

economics@17

Strong demand combined with muted supply increases have driven metal stocks to low levels Strong demand combined with muted supply Strong demand combined with muted supply increases have driven metal stocks to low levels increases have driven metal stocks to low levels

02468

10121416

65 75 85 95 05

Weeks' consumption

Aluminium

Copper

Nickel

Zinc

02468

101214

65 75 85 95 05

Weeks' consumption

0

5

10

15

20

85 95 05

Weeks' consumption

02468

101214

65 75 85 95 05

Weeks' consumption

Sources: ABARE; AME Mineral Economics; Economics@ANZ.

economics@18

Nickel and copper prices now very high relative to production costs – should prompt increased supplyNickel and copper prices now very high relative to Nickel and copper prices now very high relative to production costs production costs –– should prompt increased supplyshould prompt increased supply

Aluminium

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1985trough

1988peak

2002trough

2005up-turn

2006cur-rent

Ratio

Nickel

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1985trough

1988peak

2002trough

2005up-turn

2006cur-rent

Ratio

Copper

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1985trough

1989peak

2002trough

2005up-turn

2006cur-rent

Ratio

Ratio of price to cash operating cost of least efficient 10% of producers – selected base metals

Sources: Brooke Hunt Metal Consultants; International Monetary FundWorld Economic Outlook September 2006 Table 5.5.

economics@19

Modest increases in global production of most major mineral commodities now in prospectModest increases in global production of most Modest increases in global production of most major mineral commodities now in prospectmajor mineral commodities now in prospect

% change from previous year

1999-2004*

2005 (e)

2006 (f)

2007 (f)

Coal 5.0 7.4 2.2 2.2

Iron ore 5.9 10.3 11.7 9.2

Alumina 5.0 6.1 11.7 4.4

Copper 1.7 5.7 3.6 4.6

7.0

11.8

5.8

6.3

0.0

Aluminium 4.7 5.0 4.8

Lead 1.7 6.6 3.7

Nickel 3.3 4.7 3.0

Zinc 4.0 6.9 0.9

Gold (mine) -0.6 0.0 4.0

* Average annual rate. Sources: ABARE, Australian CommoditiesSeptember quarter 2006; Economics@ ANZ.

economics@20

200

400

600

800

1000

1200

1400

01020304050607080910

US¢/pound

LME

50

75

100

125

150

0102 0304050607 080910

US¢/pound

LME

2025303540455055

01 02 030405 06 070809 10

US$/tonne

NY Mercfutures

Futures markets expect metal and energy prices Futures markets expect metal and energy prices to remain strong by historical standardsto remain strong by historical standards

Thermal coal Gold

Copper

Aluminium

Zinc

50100150200250300350400

0102 0304050607 080910

US¢/pound

LME

Nickel

200

300

400

500

600

700

0102 0304050607 080910

US$/oz

Comex

25

50

75

100

125

150

175

0102 0304050607 080910

US¢/pound

LME

Note: Futures contract prices as at 21 September 2006.Source: Datastream; Bloomberg; Economics@ANZ.

economics@21

Leading indicators are giving a preliminary warning that the global cycle may have peakedLeading indicators are giving a preliminary Leading indicators are giving a preliminary warning that the global cycle may have peakedwarning that the global cycle may have peaked

World IP and the OECD leading indicator

World IP and the globalpurchasing managers index

-6

-4

-2

0

2

4

6

8

00 01 02 03 04 05 06

% change from year earlier

World industrialproduction (3-mthmoving average)

OECD compositeleading indicator,4 months forward

-6

-4

-2

0

2

4

6

8

00 01 02 03 04 05 0640

42

44

46

48

50

52

54

56

58

60% change from year earlier

World industrialproduction (3-mthmoving average)

Global purchasingmanagers' index,

3 mths forward(right scale)

Note: Global PMI based on PMIs for the US, Japan, Euro area, UK, Australia,Hong Kong and Singapore. Sources: OECD; national statistical agencies and purchasing managers’ associations; Economics@ NZ.

economics@22

It is becoming increasingly clear that the US housing market has peakedIt is becoming increasingly clear that the US It is becoming increasingly clear that the US housing market has peakedhousing market has peaked

Mortgage purchase applications

90100110120130140150160170

01 02 03 04 05 06

IndexTrend

Actual

Sources: Office of Federal Housing Enterprises Oversight; National Association of Realtors. Bureau of Economic Analysis; Mortgage Bankers’ Association.

Housing affordability

100

110

120

130

140

01 02 03 04 05 06

Index Lowest sinceAugust 1986

30-year mortgage rate

5.0

5.5

6.0

6.5

7.0

7.5

8.0

01 02 03 04 05 06

% paStill below average

of last 15 years (7½%)

0

4

8

12

16

01 02 03 04 05 06

% change from year earlier

OFHEO series

Nat'l Assocn of Realtorsexisting home sales prices

House prices

economics@23

Housing activity is clearly turning down – but there’s more to comeHousing activity is clearly turning down Housing activity is clearly turning down –– but but there’s more to comethere’s more to come

Sources: National Association of Housing Brokers; CommerceDepartment; National Association of Realtors.

Unsold new housing stock

3.03.54.04.55.05.56.06.57.0

01 02 03 04 05 06

Index (2000 = 100)

Trend

Actual

1.51.61.71.81.92.02.12.2

01 02 03 04 05 06

Index (2000 = 100)Trend

Actual

Housing starts

202530354045505560

01 02 03 04 05 06

Index

Lowest sinceJanuary 1991

New house ‘’buyer traffic’ Residential construction spending

-5

0

5

10

15

20

25

01 02 03 04 05 06

% change from year earlier

Trend

Actual

economics@24

End of the housing boom (and higher oil prices) will lead to slower growth in consumer spendingEnd of the housing boom (and higher oil prices) End of the housing boom (and higher oil prices) will lead to slower growth in consumer spendingwill lead to slower growth in consumer spending

-4

-2

0

2

4

01 02 03 04 05 06

% of disposable income

TrendActual

Personal saving Consumer spending

0

1

2

3

4

5

01 02 03 04 05 06

% change from year earlier

TrendActual

Mortgage refi applications

0

500

1000

1500

2000

01 02 03 04 05 06

Index

Trend

Actual

4.0

4.5

5.0

5.5

6.0

6.5

01 02 03 04 05 06

% of disposable income

Trend

Actual

Personal energy spending

Sources: Mortgage Bankers’ Association; US Bureau of Economic Analysis.

economics@25

The UK experience of the past few years provides a template for what may happen in the USThe UK experience of the past few years provides The UK experience of the past few years provides a template for what may happen in the USa template for what may happen in the US

Bank of England refi rate

Sources: Office of the Deputy Prime Minister; Halifax BoS; UK Office of National Statistics; Bank of England.

Unemployment

Consumer spending

0

5

10

15

20

25

30

35

01 02 03 04 05 06

% change from year earlier

ODPM series

HBOS series

House prices

0.00.51.01.52.02.53.03.54.04.5

01 02 03 04 05 06

% change from year earlier

2.50

2.75

3.00

3.25

3.50

01 02 03 04 05 06

% (claimant count series)

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

01 02 03 04 05 06

% paRatecut

economics@26

The euro zone economy is also picking up solidly –although tax hikes may slow the recovery in 2007The euro zone economy is also picking up solidly The euro zone economy is also picking up solidly ––although tax hikes may slow the recovery in 2007although tax hikes may slow the recovery in 2007

Sources: Eurostat; national purchasing managers’ associations.

Real GDP growth Purchasing managers’ indices

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

01 02 03 04 05 06

% change from year earlier

40

45

50

55

60

65

01 02 03 04 05 06

Net balance (%)Services

Manufactiring

7.5

8.0

8.5

9.0

01 02 03 04 05 06

% of the labour force

UnemploymentIndustrial production

-6

-4

-2

0

2

4

6

8

01 02 03 04 05 06

% change from year earlier(3-mth moving average)

economics@27

Japan’s recovery looks firmly entrenched even though the first half of 2006 was a little softJapan’s recovery looks firmly entrenched even Japan’s recovery looks firmly entrenched even though the first half of 2006 was a little softthough the first half of 2006 was a little soft

Sources: Economic & Social Research Institute; Bank of Japan; Home Ministry.

4.04.24.44.64.85.05.25.45.6

01 02 03 04 05 06

% of the labour force

Seas. adj. Trend

Lowest since May '98

UnemploymentConsumer confidence

Business confidence

-50-40-30-20-10

0102030

01 02 03 04 05 06

Net balance reportingbetter conditions (%)

Large

Smallcompanies

Bank lending

-6

-4

-2

0

2

4

01 02 03 04 05 06

% change from year earlier

30

35

40

45

50

55

01 02 03 04 05 06

%Tokyo

All Japan

economics@28

Japan’s corporate sector has worked off the ‘four excesses’ created by the 1980s ‘bubble’ …Japan’s corporate sector has worked off the ‘four Japan’s corporate sector has worked off the ‘four excesses’ created by the 1980s ‘bubble’ …excesses’ created by the 1980s ‘bubble’ …

Excess capacity

-15-10-505

10152025

90 94 98 02 06

Net balance (%) reporting 'excessive'

Large

Small

Source: Bank of Japan Tankan survey

Excess labour

-50-40-30-20-10

010203040

90 94 98 02 06

Net balance (%) reporting 'excessive'

Large

Small

Excess inventories

05

10152025303540

90 94 98 02 06

Net balance (%) reporting 'excessive'

Large

Small

Excess debt

-30

-20

-10

0

10

20

30

90 94 98 02 06

Net balance (%) reporting financialposition as 'satisfactory'

Large

Small

economics@29

… and is now in its strongest financial position since the mid-1980s… and is now in its strongest financial position … and is now in its strongest financial position since the midsince the mid--1980s1980s

Corporate profit share of GDP

1.0

1.5

2.0

2.5

3.0

81 86 91 96 01 06

% (4-qtr moving average)

Rate of return on assets

2.0

3.0

4.0

5.0

6.0

81 86 91 96 01 06

% (4-qtr moving average)

Bankruptcies

0.0

0.5

1.0

1.5

2.0

81 86 91 96 01 06

'000s (annual moving average)

Debt-equity ratio

200

250

300

350

400

450

500

81 86 91 96 01 06

% (4-qtr moving average)

Sources: Bank of Japan; Tokyo Shoko Research Company.

economics@30

China’s growth has accelerated in the first half of China’s growth has accelerated in the first half of 2006 despite official plans to slow it down2006 despite official plans to slow it down

Real GDP

Industrial production

7

8

9

10

11

12

00 01 02 03 04 05 06

% ch. from year earlier

0

5

10

15

20

25

00 01 02 03 04 05 06

% ch. from year earlierActual

6-mth moving average

Fixed asset investment

0

10

20

30

40

50

60

00 01 02 03 04 05 06

Cumulative % ch.from year earlier

Retail sales

0

5

10

15

20

25

30

00 01 02 03 04 05 06

% ch. from year earlierActual

6-mth moving average

Source: China National Statistics Bureau

economics@31

Modest tightening measures by the People’s Bank of China haven’t succeeded in reining in lendingModest tightening measures by the People’s Bank Modest tightening measures by the People’s Bank of China haven’t succeeded in reining in lendingof China haven’t succeeded in reining in lending

Money supply growth

0

5

10

15

20

25

01 02 03 04 05 06

% change from year earlierM2

M1

PBoCtarget

Interest rates

5.00

5.25

5.50

5.75

6.00

6.25

01 02 03 04 05 06

% change from year earlier

1 yr baselending rate

Construction loans

-20-10

0102030405060

01 02 03 04 05 06

% change from year earlier

Other

Construction

Bank lending

0

5

10

15

20

25

30

01 02 03 04 05 06

% change from year earlier

Source: People’s Bank of China.

economics@32

China’s rapid growth and industrialization is a particularly & uniquely ‘Good Thing’ for AustraliaChina’s rapid growth and industrialization is a China’s rapid growth and industrialization is a particularly & uniquely ‘Good Thing’ for Australiaparticularly & uniquely ‘Good Thing’ for Australia

Long-term price changes for Australian exports and imports

-6

-4

-2

0

2

4

6

8

1960s 1970s 1980s 1990s 2000s

Export prices

Import prices

% per annum (real US$ terms)

Ratio of Australian exportprices to import prices

60

70

80

90

100

110

120

130

140

150

160

170

50 55 60 65 70 75 80 85 90 95 00 05

2004-05 = 100

Korean Warwool boom

Mid-1970scommoditiesboom

Keating's'BananaRepublic'

Chinaboom

Note: the ‘terms of trade’ is the ratio of export to import prices; it is a measure of the international ‘purchasing power’ of Australia’sexports. Sources: ABS; US BEA; Economics@ANZ.

economics@33

‘Terms of trade’ gains since 1999 have been worth $2,844 pa to each Australian, on average‘Terms of trade’ gains since 1999 have been ‘Terms of trade’ gains since 1999 have been worth $2,844 pa to each Australian, on averageworth $2,844 pa to each Australian, on average

Note: Gross domestic income (GDI) is GDP adjusted for changes in the terms of trade (ratio of export to import prices). Sources: ABS; Economics@ANZ.

0

1

2

3

4

5

6

7

00 01 02 03 04 05 06

% change from year earlier(trend) Real gross

domestic income (GDI)

Real grossdomestic

product(GDP)

Real gross domestic productand income

38

39

40

41

42

43

44

45

46

47

00 01 02 03 04 05 06

A$ 000 (at annual rates;trend; 2004-05 prices)

GDI per capita

GDP per capita

-$1,783

$1,062

Real gross domestic productand income per capita

economics@34

Higher commodity prices have prompted a surge in resources-related investmentHigher commodity prices have prompted a surge Higher commodity prices have prompted a surge in resourcesin resources--related investmentrelated investment

Export-oriented infrastructure investment

Capital expenditure bythe mining industry

0.0

1.0

2.0

3.0

4.0

5.0

6.0

00 01 02 03 04 05 06

A$ bn (current prices,annualized rate)

Railways

Harbours

Electricity

0

2

4

6

8

10

12

14

16

18

20

00 01 02 03 04 05 06

A$ bn (constant prices,annualized rate)

Sources: ABS; Economics@ANZ.

economics@35

The ‘resources boom’ has arrived at a time when the economy is bumping into capacity constraintsThe ‘resources boom’ has arrived at a time when The ‘resources boom’ has arrived at a time when the economy is bumping into capacity constraintsthe economy is bumping into capacity constraints

4.5

5.0

5.5

6.0

6.5

7.0

7.5

00 01 02 03 04 05 06

% of the labour force

Actual

Trend

Lowest in30 years

Unemployment rate

Labour shortages

0

5

10

15

20

25

00 01 02 03 04 05 06

%

Businesses reporting labour shortages as aconstraint on output

Highest in historyof survey (since 1989)

`

CBD office vacancy rates

456789

101112

00 01 02 03 04 05 06

%Sydney

Rest of Australia

78

79

80

81

82

83

84

00 01 02 03 04 05 06

%

Actual (seas. adj. by ANZ)

Trend

Capacity utilization

Sources: ABS; National Australia Bank; PropertyCouncil of Australia.

economics@36

Labour costs and other ‘upstream’ prices have been accelerating for some timeLabour costs and other ‘upstream’ prices have Labour costs and other ‘upstream’ prices have been accelerating for some timebeen accelerating for some time

Private sector wage costs

2.5

3.0

3.5

4.0

4.5

00 01 02 03 04 05 06

% change from year earlier

Materials costs

-15-10-50

5101520

00 01 02 03 04 05 06

% change from year earlier

Producer prices - goods

0

1

2

3

4

5

6

00 01 02 03 04 05 06

% change from year earlier

(domestically-produced goods)

Producer prices - services

-1

0

1

2

3

4

5

00 01 02 03 04 05 06

% change from year earlier

Property& businessservices

Freight & storage

Source: ABS.

economics@37

Monetary policy isn’t yet really ‘tight’ by the standards of the ‘low inflation’ (post-1992) eraMonetary policy isn’t yet really ‘tight’ by the Monetary policy isn’t yet really ‘tight’ by the standards of the ‘low inflation’ (poststandards of the ‘low inflation’ (post--1992) era1992) era

Interest rates Real cash rate

4

5

6

7

8

9

10

11

12

13

14

93 94 95 96 97 98 99 00 01 02 03 04 05 06

% pa

Weighted average rate paid by small business

Cash rate

SVMR*

0

1

2

3

4

5

6

93 94 95 96 97 98 99 00 01 02 03 04 05 06

% pa

Cash rate deflated by4-qtr trailing 'underlying'inflation rate (simple average of RBA measures)

* Standard variable mortgage rate. Dotted lines show averages since 1993.Sources: RBA Statistical Bulletin; Economics@ANZ.

economics@38

Fiscal and monetary policy are now working at ‘cross purposes’Fiscal and monetary policy are now working at Fiscal and monetary policy are now working at ‘cross purposes’‘cross purposes’

Households have (as of 31 March) almost $1 trn of debt and just under $400bn of bank deposits and other interest-earning assets

– each ¼ pc point rise in interest rates costs households around $1¾ bn in aggregate (allowing for the fact that some deposits don’t attract interest)

– the combined impact of the May and August rate increases is thus to reduce household spending power by $3½ bn

The average household buys about 35 litres of petrol (or diesel/LPG) a week (or 1,820 litres per annum)

– so the roughly 14¢ per litre increase in petrol prices so far this year will cost Australia’s 7mn households about $1¾bn per annum (down from nearly $3bn pa at average August prices)

Against this, the personal income tax cuts which took effect on 1 July (including those foreshadowed in last year’s Budget) willboost household disposable incomes by around $9bn pa

So for Australian households in aggregate (if not for each individual household), tax cuts more than outweigh the impact of higher interest rates and petrol prices

economics@39

0

5

10

15

20

25

30

35

40

45

50

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10

'Parameter variations' 'Policy decisions'

$bn

Financial years

Cumulative impact of:

Net ‘bottom line’ impact of ‘parameter variations’vs ‘policy decision’ (tax cuts or spending increases)Net ‘bottom line’ impact of ‘parameter variations’

vs ‘policy decision’ (tax cuts or spending increases)

The Government has had a $263bn windfall over the past 4 Budgets – and ‘spent’ $248bn of itThe Government has had a $263bn windfall over The Government has had a $263bn windfall over the past 4 Budgets the past 4 Budgets –– and ‘spent’ $248bn of itand ‘spent’ $248bn of it

Sources: Budget Papers 2002-03 through 2006-07 andEconomics@ANZ calculations.

economics@40

The government is saving almost none of the windfall gains produced by the resources boom The government is saving almost none of the The government is saving almost none of the windfall gains produced by the resources boom windfall gains produced by the resources boom

-20

-15

-10

-5

0

5

10

15

20

70 75 80 85 90 95 00 05 10-5

-4

-3

-2

-1

0

1

2

3

4$bn

As a % of GDP(right scale)

$ bn(left scale)

%

Commonwealth ‘underlying’ cash balance

Forecast surpluses smaller as a % of GDP than at previous cyclical

and commodity price peaks

Sources: 2006-07 Budget Paper No. 1, Statement 13, Table 1(and previous issues).

economics@41

It’s likely that there will be at least one more rate increase before the middle of next yearIt’s likely that there will be at least one more rate It’s likely that there will be at least one more rate increase before the middle of next yearincrease before the middle of next year

4.0

4.5

5.0

5.5

6.0

6.5

01 02 03 04 05 06 07

% pa

90-daybill yield

Cash rate

Shaded areas denote forecasts.Sources: ABS; RBA; Economics@ANZ.

Interest rates In last week’s Statement on Monetary Policy, the Reserve Bank raised its forecast for ‘underlying’ inflation to 3% -the top of its ‘target range’It also raised its forecast for economic growth to 3½% - at the top of the range of estimates of Australia’s ‘potential’ growth rate, at a time when idle resources are becoming increasingly scarceWith another pre-election Budget likely next May, the clash between monetary and fiscal policy will continue …… creating a situation where further increase(s) in interest rates are likely

economics@42

The resources boom is keeping the A$ stronger than it otherwise would have beenThe resources boom is keeping the A$ stronger The resources boom is keeping the A$ stronger than it otherwise would have beenthan it otherwise would have been

Economic influences on the value of the A$

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

01 02 03 04 05 06-100

0

100

200

300

400

500US¢

Australia-US 90-day

interestrate spread,

forward 1 year(right scale)

Basis pointsA$-US$

(leftscale)

Interest rate spreads

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

01 02 03 04 05 0680

100

120

140

160

180

200

220US¢

RBA commodityprice index (in US$)(right scale)

2002-03 = 100

A$-US$(left scale)

Commodity prices

Sources: Datastream; Reserve Bank of Australia.

economics@43

Commodity prices and interest rate differentials have been working in opposite directions on the A$Commodity prices and interest rate differentials Commodity prices and interest rate differentials have been working in opposite directions on the A$have been working in opposite directions on the A$

If commodity priceshadn’t risen since June 2001

Alternative hypothetical scenarios for the A$

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

01 02 03 04 05 06

US¢ A$ predicted by model ifAustralia-US interest rate

spread had remained atJuly 2004 level

Actual

A$ as predictedby ANZ model

If the interest rate spread on the A$ hadn’t narrowed since July 2004

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

01 02 03 04 05 06

US¢

A$ predicted bymodel if commmodity

prices had remained atJune 2001 level

Actual

A$ as predictedby ANZ model

Sources: Datastream; Reserve Bank of Australia.

economics@44

The Australian resources sector is booming on all fronts except – surprisingly - outputThe Australian resources sector is booming on all The Australian resources sector is booming on all fronts except fronts except –– surprisingly surprisingly -- outputoutput

Employment

-10-505

10152025

00 01 02 03 04 05 06

% change from year earlier(4-qtr moving average)

Mining

Rest of the economy

Source: ABS.

Gross value added

Capital expenditures

-60-40-20

020406080

100

00 01 02 03 04 05 06

Real % change fromyear earlier Mining

Rest of theeconomy

Pre-tax profits

-50

0

50

100

150

00 01 02 03 04 05 06

% change from year earlier (4-qtrmoving average)

MiningRest of theeconomy

-10

-5

0

5

10

15

00 01 02 03 04 05 06

Real % change fromyear earlier

Mining

Rest ofthe economy

economics@45

It’s inevitable that different States will grow at different speedsIt’s inevitable that different States will grow at It’s inevitable that different States will grow at different speedsdifferent speeds

Mining and manufacturing as a share of State economies

0

5

10

15

20

25

NSW Vic Qld SA WA Tas NT

Mining Manufacturing% of gross State product, 2004-05

Sources: ABS; Economics@ANZ.

economics@46

0

2

4

6

8

10

12

14

80818283848586878889909192939495969798990001020304050607080910

p.c. points

Difference betweenfastest and slowestState GSP growth rates

State Budgetestimates &forecasts

Current differences between growth rates of different States are less than in previous cycles Current differences between growth rates of Current differences between growth rates of different States are less than in previous cycles different States are less than in previous cycles

Dispersion between fastest and slowest State economic growth rates

Sources: ABS State Accounts; State Budget Papers 2006-07;Economics@ANZ.

economics@47

Different growth rates across the States aren’t unusual: what is unusual is NSW coming last Different growth rates across the States aren’t Different growth rates across the States aren’t unusual: what is unusual is NSW coming last unusual: what is unusual is NSW coming last

Sources: ABS State Accounts; Economics@ ANZ.

-4

-2

0

2

4

6

8

80 85 90 95 00 05

% ch

New South Wales

Victoria

-4

-2

0

2

4

6

8

80 85 90 95 00 05

% ch

-4-202468

10

80 85 90 95 00 05

% ch

Queensland

Western Australia

-4-202468

1012

80 85 90 95 00 05

% ch

-4-202468

1012

80 85 90 95 00 05

% ch

South Australia

Tasmania

-6-4-202468

10

80 85 90 95 00 05

% ch

State and national real growth rates

economics@48

Different growth rates across the States aren’t unusual: what is unusual is NSW coming last Different growth rates across the States aren’t Different growth rates across the States aren’t unusual: what is unusual is NSW coming last unusual: what is unusual is NSW coming last

Sources: ABS State Accounts; Economics@ ANZ.

0.0

0.5

1.0

1.5

2.0

81 86 91 96 01 06

% ch

New South Wales

Victoria

Queensland

Western Australia

South Australia

Tasmania

State and national population growth rates

0.0

0.5

1.0

1.5

2.0

81 86 91 96 01 06

% ch

0.0

1.0

2.0

3.0

4.0

81 86 91 96 01 06

% ch

0.00.51.01.52.02.53.03.5

81 86 91 96 01 06

% ch

0.0

0.5

1.0

1.5

2.0

81 86 91 96 01 06

% ch

-0.5

0.0

0.5

1.0

1.5

2.0

81 86 91 96 01 06

% ch

economics@49

SummarySummarySummary

Global growth is now being driven by developing economies especially but not only China

Although commodity demand from advanced economies has begun to ease (with a slowing in the US), developing countries’ energy and metals demand is likely to continue growing strongly

The surge in energy and metals prices reflects the muted response of commodity supply to the rapid growth in demand

– in turn partly as a result of changes in the structure of the global resources industry

Prices of most resource commodities will ease from current highs but remain high by the standards of the past decade

The current ‘resources boom’ is allowing Australia to maintain reasonably strong economic growth in contrast to other countries where growth has been largely dependent on consumer spending fuelled by a now-passed housing boom

The ‘two-speed’ pattern of growth in the Australian economy is not unusual

– what is unusual (and behind the focus on this issue) is that New South Wales is at the bottom of the pack