the global financial and economic crisis: implications...

TRANSCRIPT

3/26/2009

1

The Global Financial and

Economic Crisis: Implications for

SADC Economies and

Development Finance Institutions

Keith Jefferis

Econsult Botswana/USAID Southern African Trade Hub

March 26, 2009

Structure of Presentation

� The Global Financial and Economic Crisis�Origins of the crisis

� Unfolding of the crisis

� Impact of the Crisis on Developing Countries

� Implications for SADC Economies� Exports

� Balance of payments & financing

� Fiscal position

� The Bright Side!

� Implications for DFIs

3/26/2009

2

Global Financial & Economic Crisis

Global Growth Slowdown

� World economy now in deep recession

� Global growth forecasts for 2009 revised down from 3.9% to 0.5% (IMF)

� Developed country growth forecasts slashed to -2.0%

� Emerging / developing faster growth at 3.3%, but still affected

� Trend of downward revision of forecasts not yet over

� IMF forecasts the most optimistic, e.g. JP Morgan -2.6% for 2009

-3-2-10123456789

%

IMF Growth Forecasts, 2009 (July 2008 & Jan 2009)

3/26/2009

3

Global Growth Slowdown

� News snippets – this week� EIU – 30% chance of global depression (developed country growth <1% to 2013)

� SA new vehicle sales est. at 385 000 in 2009, down by almost 50% from 714 000 in 2006

� Sony Ericsson handset sales down by 50% from 2008Q4 to 2009Q1

� Japanese vehicle exports down 70% in February 2009 compared to a year earlier, and total exports down 49%

� Premium air travel down 25% in January on a year earlier

Global Growth Slowdown

-8

-6

-4

-2

0

2

4

6

8

Annualised real GDP growth, qoq

World Developed Emerging markets

Source: JP Morgan

� Depths of recession –4Q2008 and 1Q2009

� Now widely acknowledged to be worst recession since 1930s

� Stronger growth in emerging markets, but still big drop

� Weak recovery projected towards end of 2009

� Sluggish but positive growth in 2010

� Robust world growth (>3%) only likely in 2011

3/26/2009

4

Global Growth Slowdown - Advanced economies

-16

-14

-12

-10

-8

-6

-4

-2

0

2

42Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

Annualised real GDP growth, qoq

USA Euro Japan

Source: JP Morgan

� Four quarters of negative growth, with total decline in GDP of:

� USA – 3.4%

� Euro zone – 3.7%

� Japan – 8.3%

� Even when recovery starts, there will be a long “catching up” process

� 2008-9 recession likely to be deeper than slowdowns of 2001, 1991 & 1981

Origins of the Crisis

� The global financial economic crisis has its origin in three interconnected areas:

� Financial Sector Issues

�Global macroeconomic imbalances

� Commodity Prices

3/26/2009

5

Financial sector

� Sub-prime mortgage lending� New models of financial behaviour (originate-to-distribute -> off balance sheet)

� Complex new financial instruments (CDOs)

� Misaligned incentives (selling of loans not repayments; determination of bonuses)

� Credit explosion� Lax monetary policy� Asset price bubbles (housing, equities)� Defective risk assessment (rating agencies)� Weak regulation

Global imbalances

� Mismatch between surplus and deficit nations

X – M = S - I

� Surplus nations:� high savings (> investment)

� = current account surpluses

� capital exports to RoW

� Fx reserve accumulation

� Deficit nations:� low savings (< investment)

� = current account deficits

� capital imports from RoW

� debt accumulation

� Two sides of the same coin� Capital outflows from surplus nations financed deficits in low-savings nations, contributed to low interest rates and credit expansion

� e.g. China, oil exporters buying US T-bills and bonds

� Exchange rate inflexibility :� Asian currencies (managed) undervalued

� US dollar overvalued

� EUR-USD rate bears burden of adjustment

3/26/2009

6

Commodity price bubble

� Commodity prices at historically high levels by 2007/early-2008:� Oil

� Metals

� Foodstuffs

� Structural change effects –e.g. Rapid growth and infrastructure investment in China

� Long growth upswing

� Credit-induced spending

� Supply inelasticity

� Accentuated global imbalances, e.g. raised savings by commodity exporters

How the crisis unfolded - 1

� Financial Sector� Sub-prime defaults, triggered defaults on wide range of financial instruments

� Risk exposure and risk mis-pricing apparent

� Credit ratings inaccurate

� Uncertainty in markets

� Inter-linkages between institutions amplified problems

� Credit crunch, collapse of financial institutions, rescues, de-capitalisation

3/26/2009

7

How the crisis unfolded - 2

� Global imbalances� Rising savings in deficit nations:

� rebuilding HH and corporate balance sheets

� reduced consumption, lower demand

� Desire to accumulate reserves� perceived as economic strength

� but we can’t all run surpluses!

� Imbalances will have to be unwound:� exchange rate misalignments must be corrected (but flight to quality has led to strengthening dollar);

� needs rising consumption in high savings nations

How the crisis unfolded - 3

� Commodity Prices

� Rising inflation

� Declining real income in oil-consuming countries, hence reduced real expenditure

� E.g. on automobiles

� Tighter monetary policy (higher interest rates exacerbated credit problems)

3/26/2009

8

Impact of the Crisis

� Three phases

� Financial crisis (systemic)

� International financial flows/risk aversion

� Economic crisis (collapse in real growth rates, trade flows)

Systemic

banking

crisis

Cross-

border

financial

flows

Growth &

trade

effects

Advanced

countries

I III

Emerging

markets

II III

Less-

developed

countries

II III

Financial Contagion - Markets

� Aversion to emerging market (EM) risk + liquidity calls

� Capital flow reversals as foreign investors withdraw

� Falling equity markets

� Pressure on exchange rates (weaker)

� Rollover risks for existing borrowers (corporate and sovereign)

� Higher cost of funds (EM spreads)

� Trade finance scarce

� Inflows of FDI much reduced

� IIF estimates net private capital flows to EMs to fall sharply� $930bn in 2007

� $467 bn in 2008

� $165 bn in 2009

� EMs that used commercial finance to fund CADs esp. vulnerable

� In Africa, small but growing

� Ghana & Kenya� postponed planned international

bond offerings

� SA, Nigeria� external financing for companies,

banks scarce & expensive (higher interest rates)

3/26/2009

9

Financial Contagion – Other Flows

� Of particular importance to LDCs� ODA flows under pressure� Donor country budgets under pressure

� Commitments to increase ODA now doubtful

� Remittances falling sharply� Falling employment and real incomes in advanced economies

� Greater reliance on MFIs � IMF

� World Bank

� IFC

� AfDB

Trade & Growth Effects

� Reduced prices and volumes for major commodity exports

� Major ToT deterioration for commodity exporters (reduced real incomes)

� General reduction in trade flows worldwide

� World trade expected to decline in 2009� First time since 1982� Largest fall for 80 years� 2008Q4 saw major falls in exports in many countries

� Compounded by drying up of trade finance

� Risk of protectionism & slow progress on DDA negotiations

3/26/2009

10

Minerals prices way down....

$0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000

$10,000

Source: LME

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

Source: LME

Copper ($/tonne) Nickel ($/tonne)

Trade & Growth Effects - Africa

� SS Africa growth forecast to remain positive in 2009 (IMF 3.5%)

� but much reduced from 2007 levels

� Changing employment patterns

� from dynamic export sectors to lower productivity sectors

� reversal of urban-rural migration

� Higher poverty due to:

� reduced employment

� lower wages

� lower remittances

� Concern about fragile states (Zim, DRC, Burundi, Guinea-Bissau, Liberia)

� Reduced availability of finance will inhibit investment in infrastructure & human capital

-4

-2

0

2

4

6

8

10

2007 2008 2009 2010

%

Real GDP Growth (IMF)

SS Africa Developing

Advanced

3/26/2009

11

Global Growth Slowdown – Key risks & uncertainties

� Depth and duration of recession� - how long and how deep?

� V-shape or L-shape?

� Shape of Financial Sector� Institutions?� Regulation?� Public/private ownership?

� Impact on international trade� Reversion to protectionism?

� Prospects for DDA?

� Macroeconomic Impact� Monetary expansion -> inflation

� Fiscal stability & future taxes

� Exchange rate realignment

� Unemployment

Implications for SADC Economies

3/26/2009

12

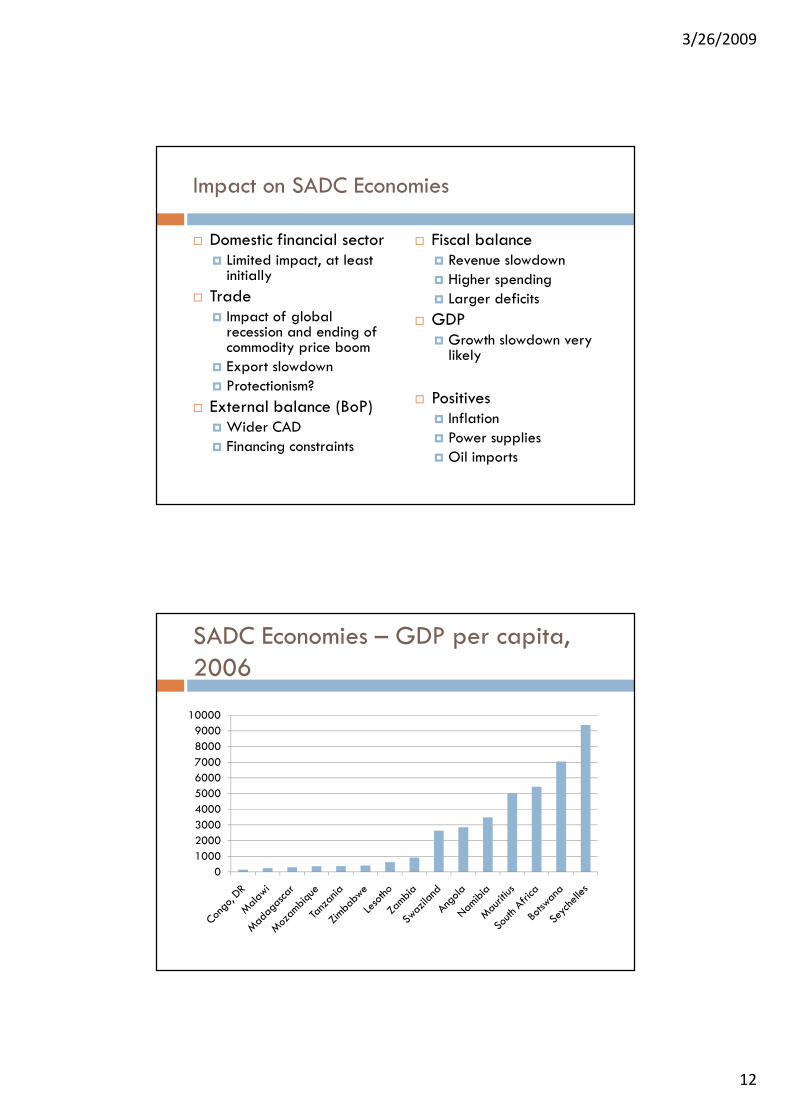

Impact on SADC Economies

� Domestic financial sector� Limited impact, at least initially

� Trade� Impact of global recession and ending of commodity price boom

� Export slowdown� Protectionism?

� External balance (BoP)� Wider CAD� Financing constraints

� Fiscal balance� Revenue slowdown� Higher spending� Larger deficits

� GDP � Growth slowdown very likely

� Positives� Inflation� Power supplies� Oil imports

SADC Economies – GDP per capita, 2006

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

3/26/2009

13

Export Slowdown

� Main impact on mineral producers

� Huge declines in:� Oil prices (-70%)

� Base metal prices (copper, -70%; nickel, -80%)

� Diamond sales volumes, to a lesser extent prices

� Slow recovery forecast in commodities markets, but no return to 2007/8 peaks

� E.g. Stanchart f’casts2009 avg. vs. end-2008� Nickel +0%

� Copper +18%

� Oil +56%

� Lower than 2008 avgprices

Export Slowdown

Country Commodity % of exports

Angola Oil, diamonds 99%

Botswana Diamonds, copper, nickel 90%

Congo DR Diamonds, oil 64%

Mozambique Aluminium, gas 74%

Namibia Diamonds, copper, uranium 59%

South Africa Gold, platinum, coal <50%

Zambia Copper, cobalt 77%

Mineral Exporters

3/26/2009

14

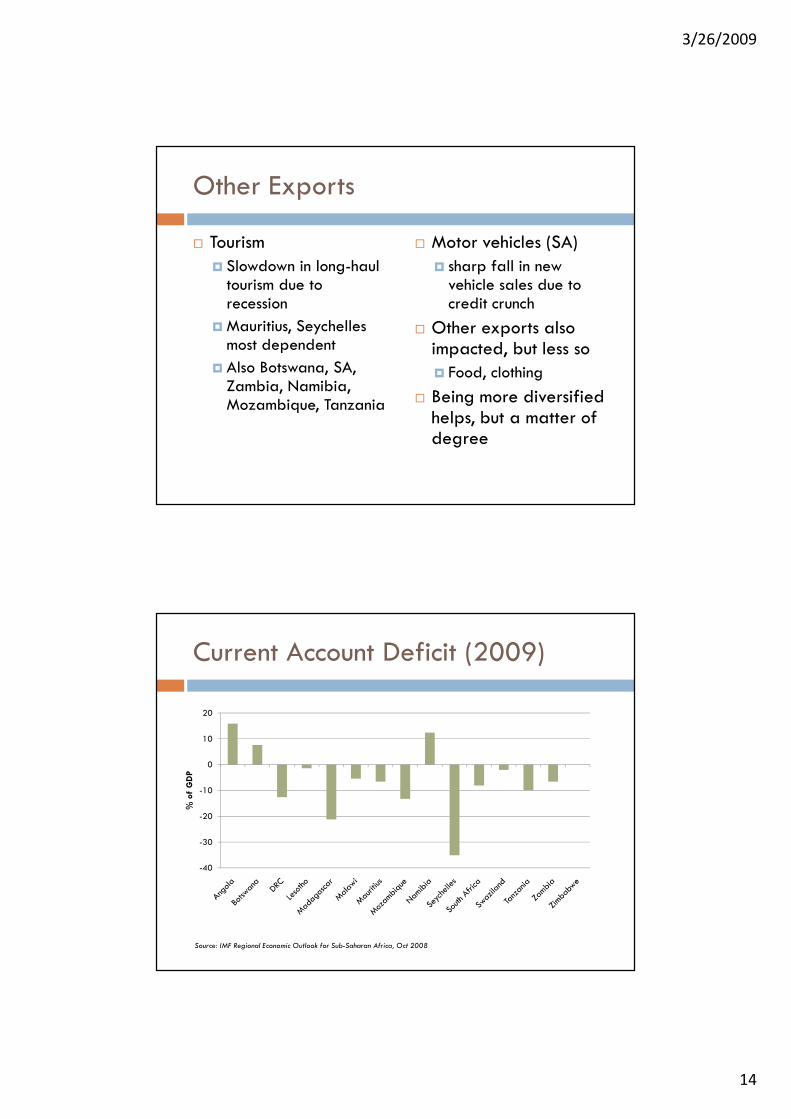

Other Exports

� Tourism� Slowdown in long-haul tourism due to recession

�Mauritius, Seychelles most dependent

� Also Botswana, SA, Zambia, Namibia, Mozambique, Tanzania

� Motor vehicles (SA)� sharp fall in new vehicle sales due to credit crunch

� Other exports also impacted, but less so� Food, clothing

� Being more diversified helps, but a matter of degree

Current Account Deficit (2009)

-40

-30

-20

-10

0

10

20

% of GDP

Source: IMF Regional Economic Outlook for Sub-Saharan Africa, Oct 2008

3/26/2009

15

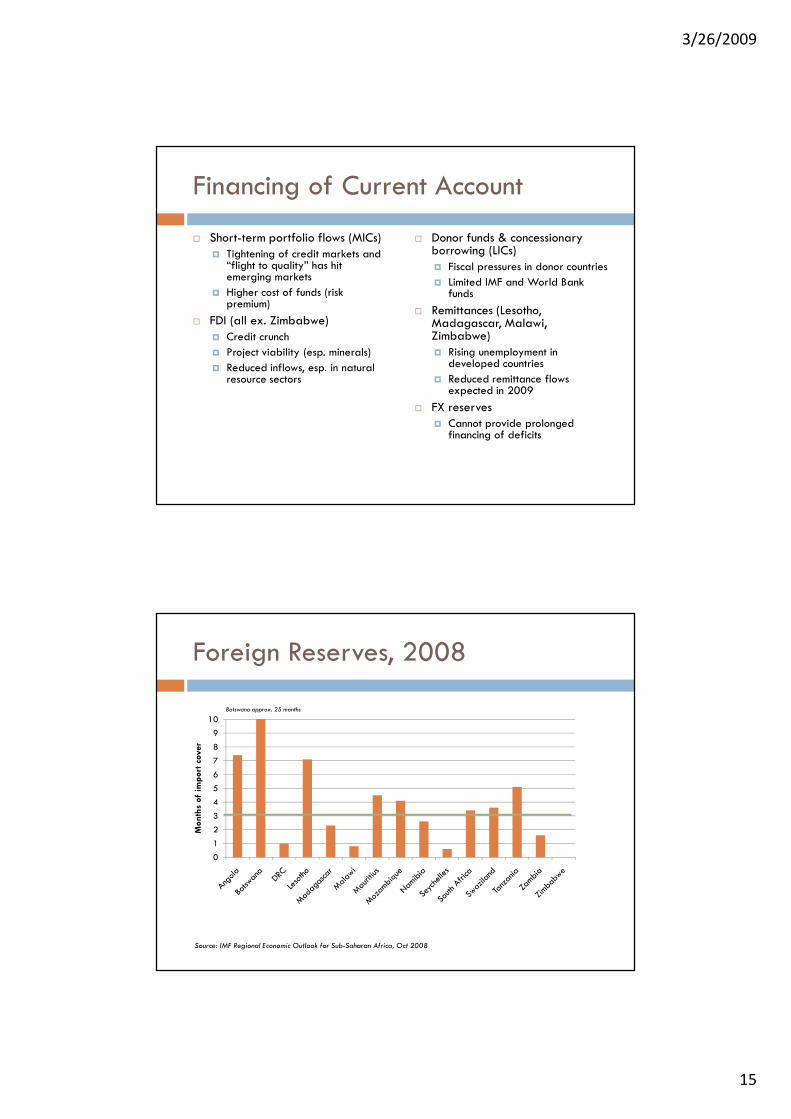

Financing of Current Account

� Short-term portfolio flows (MICs)� Tightening of credit markets and

“flight to quality” has hit emerging markets

� Higher cost of funds (risk premium)

� FDI (all ex. Zimbabwe)� Credit crunch

� Project viability (esp. minerals)

� Reduced inflows, esp. in natural resource sectors

� Donor funds & concessionary borrowing (LICs)� Fiscal pressures in donor countries

� Limited IMF and World Bank funds

� Remittances (Lesotho, Madagascar, Malawi, Zimbabwe)� Rising unemployment in

developed countries

� Reduced remittance flows expected in 2009

� FX reserves� Cannot provide prolonged

financing of deficits

Foreign Reserves, 2008

0

1

2

3

4

5

6

7

8

9

10

Months of import cover

Botswana approx. 25 months

Source: IMF Regional Economic Outlook for Sub-Saharan Africa, Oct 2008

3/26/2009

16

Fiscal Balance (2007)

-10 -5 0 5 10 15

Zambia

Tanzania

Swaziland

South Africa

Seychelles

Namibia

Mozambique

Mauritius

Malawi

Madagascar

Lesotho

DRC

Botswana

Angola � Initial fiscal position reasonable:� Several countries with surpluses

� Deficits mostly manageable

� Benefits of ongoing fiscal reforms

Fiscal Balance & Financing

� Lower revenues likely due to reduced trade and growth

� Higher spending, e.g. social safety nets

� Vulnerabilities:� Commodity-revenue dependence

� Donor dependence

� Existing budget deficits

� High debts

� SACU revenues

� Deficit financing may be a problem� Access to international capital markets (eurobond issues) limited

� Domestic financing capacity –varies from country to country

� Banks – depends on many other factors

� Bond markets - generally underdeveloped – but now may be a good time to develop

� Danger of crowding out of private sector

3/26/2009

17

Donor dependence

� Donor funds of great importance to low-income SADC countries:� Malawi, Lesotho, Mozambique, Madagascar, Zambia, Tanzania

� Funding of budget, BoP, crucial for development projects

� Previous commitments to increase donor funding now questionable

� Need for donor funding rising

� Need for effective lobbying to – at a minimum –preserve donor funding levels

Role of MFIs

� MFIs have a crucial role given adverse markets

� Source of concessional finance for LICs

� Less risk-averse than banks

� WB & AfDB for infrastructure finance, but slow

� IMF more flexible and can provide budget and BoP support� Exogenous shocks facility

� Under-funded; need for recapitalisation

� G20 Agreement to increase IMF funding

� Still issues over “voice” and US veto

� Conditionality issues – esp. in the context of exogenous shocks

3/26/2009

18

Summary of negative impacts

� Slower / negative GDP growth

� Reduced investment� Increased current account deficits; financing constraints

� Exchange rate weakness� Fiscal deficits; financing constraints

� Rising unemployment & poverty

� Uncertainty over depth and duration of crisis

� Risks mostly on the downside

The Bright Side

3/26/2009

19

Financial Sectors

� Mostly untouched by first round of crisis:

� commercial banks sound

� much improved regulation and supervision

� limited cross-border banking linkages

� limited exposure to complex financial products

� deposit-funded lending

� money markets functioning normally

� Vulnerability - protracted downturn elevates risk:

� falling incomes, borrowers less able to service debts

� sectoral concentration of bank portfolios

� market volatility if banks have lent for investment in stock markets

� withdrawal of funds from parent banks

� equity markets following global trends

Inflation Forecasts

0

5

10

15

20

25

30

35

%

2008 2009

Source: IMF REO for SSA (October

2008)

� Inflation will fall due to:� Lower oil prices

� Lower food prices

� Sharply declining global inflation

� Will lead to lower interest rates

3/26/2009

20

Electricity

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

MW

Reserve Net capacity Peak Demand

� Reserve margin rapidly eroded

� Eskom now expects no growth in demand in 2008-2009

� New capacity of 40000MW needed over next decade (almost doubling)

� Slowdown provides breathing space

� But commercial financial markets currently closed

Import Bills

� Lower commodity prices:

� All except Angola & DRC net oil importers

� Fuel approx 20% of total imports on average

� Will help CAD

� Mainly oil, but also other commodity-related imports (e.g. steel)

� Net food importers also aided by lower world food prices

3/26/2009

21

Summary of Country ImpactsANG BWA DRC LES MAD MAL MAU MOZ NAM SEY SA SWZ TAN ZAM ZIM

Exports

Minerals XX XX XX X XX X XX

Tourism X X XX X X XX X X X

Finance

CAD XX XX X X XX XX X X XX X

FDI X X X X X X X X X X X X X X

Remittan-

ces

X X X X

Donors X X X X

Reserves X X X X X X X

Positives

Inflation � � � �

Power � � � � �

Oil

Imports

� � � � � � � � � � � � �

Summary of Impacts

� All countries will be hit, but impact will vary from country to country, depending on:� trade structure, fx reserves, fiscal position

� Impact less if:� sound policies in place� good reserves & low debt� more diversified

� Vulnerability from previous high inflation and CADs

� Most vulnerable are mineral exporters with high dependence on foreign capital

3/26/2009

22

Policy Responses - 1

� Internationally, lobby for:

� No protectionism!

� Resume DDA

� Additional resources for IMF/WB, that can be disbursed quickly and flexibly

� Preservation of donor funding commitments

� Fair treatment for migrant workers

Policy Responses - 2

� Domestically:� Exchange rate flexibility – to support adjustment

� Use monetary policy to support growth when inflation is low

� Fiscal policy – can be expansionary s.t. sustainability constraints

� Ensure quality of government budgeting & spending

� Renewed focus on financial sector supervision & regulation – banks & non-banks

� Need for high quality, timely economic and financial data

� Contingency planning & monitoring of evolving conditions

� Sustain reforms

3/26/2009

23

Implications for DFIs

A very different environment ....

� Constrained access to international financial markets increases demands on domestic sources of finance

� Domestic banking systems vary in ability to provide additional funds (liquidity, risk appetite, parent co’s)

� E.g. infrastructure projects, power projects

� Provides new opportunities for:� DFI finance

� SMMEs� MLS private sector projects

� Infrastructure

� Domestic bond markets

3/26/2009

24

Availability of finance for DFIs?

� DFIs also face reduced access to int’l markets� Scarce & expensive

� Govts also tapping debt markets

� DFI reliance on gov’tfinance may also be a problem:� Competing demands on public funds

� Limits on public sector debt/guarantees

� Most SADC countries have savings shortage (S<I)� Dependent on foreign finance to bridge gap

� Only a few countries with high savings (S>I) � Botswana, Namibia, Angola (?)

How can DFIs strengthen their ability of raise finance?

� Improve ability credit standing & ability to compete:� Strengthen balance sheets

� Consider credit rating

� Tap domestic bond markets

� Talk to governments

� Improve project selection� Increased demand and possibly reduced supply of finance puts pressure on ability to select projects� Sound projects

�Minimise risks

� Contribute to LT economic growth

3/26/2009

25

Thank You