the geography of aps in a goods exporting economy: the case of west germany

TRANSCRIPT

CHAPTER 4

The Geography of APS in a Goods Exporting Economy: The Case of West Germany

E. W. Schamp

4 . 1 . I N T R O D U C T I O N : A M A N U F A C T U R I N G - D R I V E N A P S G E O G R A P H Y

German advanced producer services firms are rather rare on the global scene. In fact, Germany has long been a net importer of services. Although the balance of payments is heavily weighted by travel expenditures given the fact that German private households enthusiastically travel to other countries, fees and expenditures for patents and licences, for advertising and fairs and for business services such as consultancy all cause a negative balance in services trade as well. We do not know from these balance of payments figures who participates in international trade in services, whether they are specialised services firms or other actors. But these figures clearly point to the fact that the economic base of the German economy is not in services. Germany has long been one of the leading exporters of manufactured goods. The share of manufactured goods in the international trade of Germany is very large, such as 92% in 1992. The trade balance in manufactured goods has always been positive during the last decade, outrunning by far the balance in services trade. The balance of net exports reached a maximum of 135 bn DM in 1989 and had a minimum of 22 bn DM in 1991 whereas the balance in services oscillated from a negative balance of 8 bn DM in 1988 to a positive one of 8.5 bn in 1989 but dropped away to a negative 24 bn DM in 1992. Even engineering and other technical services, which was a net exporter during the 1980s, became a net importer in 1993 (Deutsche Bundesbank, 1993). Furthermore, a recent pilot study on producer services in Germany came to the conclusion that 95% of sales of German services firms were oriented to domestic clients (Reim, 1992: p. 725).

Hence, the economic base of Germany's competitiveness on the world market is still manufacturing. It is far too early to think of Germany as a services exporting economy, despite the quickening deindustrialisation process which accelerated after unification. In what follows only the Western part of contemporary Germany

155

156 Progress in Planning

will be dealt with, while the Eastern part will be analysed by W. Gaebe, in this volume. Differences between the transformation of post-socialist and formerly highly industrialised Eastern economic structures and market oriented Western economic structures are too large. Whereas there was an almost complete lack of producer services firms in the East, combined with a sudden deindustrialisation, tendencies for rationalisation in manufacturing combined with a more or less well developed producer services sector in thc West gave rise to a new geography of APS over the last decade.

As far as West Germany is concerned, it might be assumed that the service sector remains largely derivative of goods production, this holding even true for advanced producer services. Admittedly, the share of the manufacturing sector has steadily declined to 40% of the GDP whereas the share of the service sector rose to 58.7% in 1991 (Statistisches Bundesamt, 1992). The residual category of 'other services' in official statistics, which includes producer services, proved to be the fastest growing sub-sector although it remained small compared to the consumer services sector. The share of the service sector as a whole in the domestic economy has also been growing for decades in terms of employment. According to Jost (1991), employment in services increased by 42% whereas employment in manufacturing industries decreased by 17% between 1970 to 1987. This, however, is a very general statement, since sectoral classifications no longer reflect the kind of activities undertaken. Obviously, tertiarisation of manufacturing activities remained hidden behind the sectoral classifications. In analysing the development of services in West Germany from 1939 to 1987 both in sectoral and functional terms Bade et al. (1990) pointed to two different phases in the economic development of West Germany after World War II. During the 1950s employment in manufacturing grew faster than in services; this has been called the reconstruction phase of the West German manufacturing economy (Abelshauser, 1983), and it ended by the mid-1960s, at the latest in a first (minor) crisis in 1967. Since then, employment - - in functional terms - - decreased in manufacturing activities, while it increased in service activities to reach 65% of total employment in 1987. Most of the growth of service activities, however, must have occurred within manufacturing firms, since only at the end of the 1970s did employment in the tertiary sector overtake that in the secondary sector.

During recent decades, several shifts occurred. While employment in trade and transport remained relatively constant over nearly 30 years, employment in financial as well as public services grew particularly fast just after the reconstruction phase (1960 to 1973); but from 1973 onwards, employment in the health sector as well as in 'other' services w which actually means business services - - increased considerably (Bade et a l . , 1990). These statistics, however, do not unambigously differentiate between services offered to private households or to business firms. Taking into account the current increasing rationalisation in

The Geography of Advanced Producer Services in Europe 157

the commercial, transport and financial Sectoi~s and the cutback Of public activities given long-term deficits in state budgets, as well as national insurance budgets it may be expected that in the future intermediary services such as business services will be the only ones to contribute to the growth in service employment.

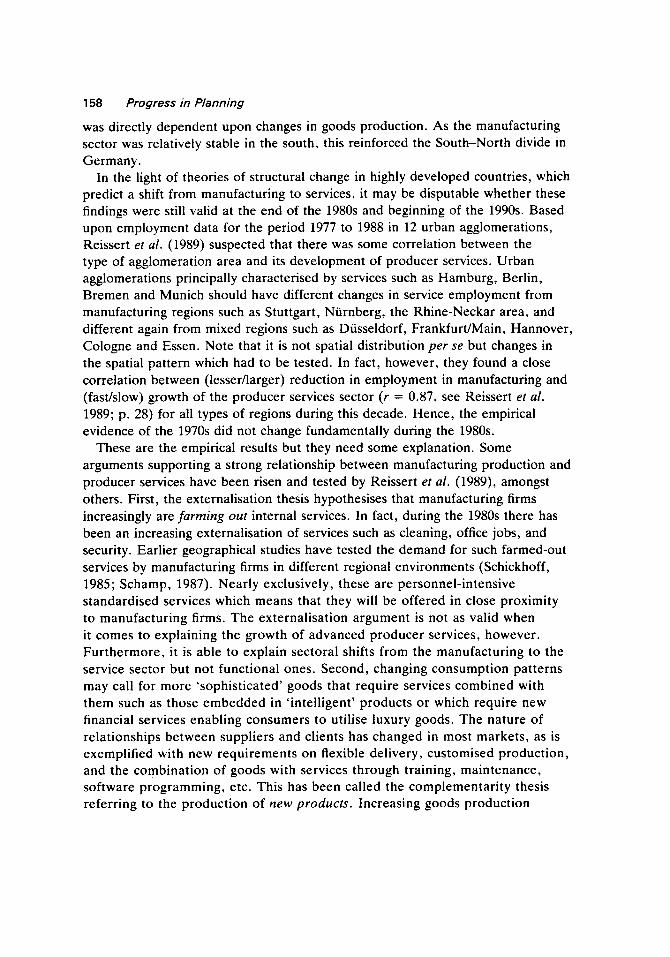

The question remains, however, whether recent growth has been independent from changes in manufacturing. Demonstration of the close interrelationship of services and manufacturing is statistically difficult. In fact, statistics in input-output-tables do not differentiate sub-sectors of services in such a way that producer services can be precisely identified, let alone advanced producer services. Table 4.1, however, clearly shows the importance of the manufacturing sector as a user of intermediate services (so-called 'other market determined services') as input in the national income accounts.

TABLE 4.1. Users of intermediate services (domestic plus imports) as inputs in 1988

Sector Mill. DM In (%)

Manufacturing 119,835 42.6 Construction 18,751 6.7 Retail, wholesale, transport 27,697 9.8 Finance, renting, catering, education and media 43,118 15.3 Own demand 44,126 15.7 Others 28,122 9.9

Total 281,649 100

Source: Statistisches Bundesamt 1990a*. Note: *Including services such as brokerage, laundry and cleaning, legal and consultancy services,

architecture and engineering, advertising, real estate services, renting of vehicles.

Anyway, where producer services are delivered to other producer service sectors, such as tax consultancy to advertising, it would be better to know the final demand for those services and hence follow a filidre approach in order to know the driving forces behind service demand. Empirical evidence of this kind is scarce and only infrequently available on the regional level. Nevertheless, Table 4.1 confirms that APS are manufacturing driven in the German economy.

The question arises, however, as to whether this interrelationship holds true in spatial terms as well. As the locational pattern of services firms is presumed to be mainly bound to the urban system, some recent studies have looked more closely at the regional-scale interrelationship between changes in manufacturing and growth of the service sector in the major German urban agglomerations. An earlier investigation of changes in value added and employment from 1970 to 1980 revealed a close correlation between the two sectors: Producer services grew faster where manufacturing remained relatively strong. According to K6ppei (1983, p. 219) the expansion of producer services had not developed autonomously but

158 Progress in Planning

was directly dependent upon changes in goods production. As the manufacturing sector was relatively stable in the south, this reinforced the South-North divide in Germany.

In the light of theories of structural change in highly developed countries, which predict a shift from manufacturing to services, it may be disputable whether these findings were still valid at the end of the 1980s and beginning of the 1990s. Based upon employment data for the period 1977 to 1988 in 12 urban agglomerations, Reissert et al. (1989) suspected that there was some correlation between the type of agglomeration area and its development of producer services. Urban agglomerations principally characterised by services such as Hamburg, Berlin, Bremen and Munich should have different changes in service employment from manufacturing regions such as Stuttgart, Ntirnberg, the Rhine-Neckar area, and different again from mixed regions such as Diisseldorf, Frankfurt/Main, Hannover, Cologne and Essen. Note that it is not spatial distribution per se but changes in the spatial pattern which had to be tested. In fact, however, they found a close correlation between (lesser/larger) reduction in employment in manufacturing and (fast/slow) growth of the producer services sector (r = 0.87, see Reissert et al.

1989; p. 28) for all types of regions during this decade. Hence, the empirical evidence of the 1970s did not change fundamentally during the 1980s.

These are the empirical results but they need some explanation. Some arguments supporting a strong relationship between manufacturing production and producer services have been risen and tested by Reissert et al. (1989), amongst others. First, the externalisation thesis hypothesises that manufacturing firms increasingly are farming out internal services. In fact, during the 1980s there has been an increasing externalisation of services such as cleaning, office jobs, and security. Earlier geographical studies have tested the demand for such farmed-out services by manufacturing firms in different regional environments (Schickhoff, 1985; Schamp, 1987). Nearly exclusively, these are personnel-intensive standardised services which means that they will be offered in close proximity to manufacturing firms. The externalisation argument is not as valid when it comes to explaining the growth of advanced producer services, however. Furthermore, it is able to explain sectoral shifts from the manufacturing to the service sector but not functional ones. Second, changing consumption patterns may call for more 'sophisticated' goods that require services combined with them such as those embedded in 'intelligent' products or which require new financial services enabling consumers to utilise luxury goods. The nature of relationships between suppliers and clients has changed in most markets, as is exemplified with new requirements on flexible delivery, customised production, and the combination of goods with services through training, maintenance, software programming, etc. This has been called the complementarity thesis referring to the production of new products . Increasing goods production

The Geography of Advanced Producer Services in Europe 159

and the need for backward and forward services such as those mentioned or finance and insurance foster the overall growth of the service sector. It may be questioned, however, whether the complementarity thesis really will be able to explain the regional coincidence of manufacturing and (advanced) producer services, given the fact that, for instance, financial services have been largely decoupled Iocationally from manufacturing production (see Schamp et al., 1993). Finally, restructuring o f production in the manufacturing sector increasingly makes use of new information and communication technologies. As a result, innovation in organisation, administration and production has arisen, and an increasing division of labour has emerged through growing interaction within the producer services sector itself. This has been called the interaction thesis by Reissert et al. (1989). They are supported by the argument of Gruhler (1990) concerning an increasing 'scientification' of manufacturing production due to increasing use of micro-electronics as a cross-section technique which influences production as well as organisation and products and, thus, requires an increasing need for knowledge-intensive services in management, consultancy and R & D. A further argument for the growing necessity for producer services, however, is the increase in state regulations covering industrial law, work council law, company law, tax law, consumer law and environmental law, which increasingly require the use of external specialists (Gruhler, 1990, p. 84). The considerable growth in accountancy services is but one example.

When they looked at some interactive services such as engineering, legal services, consultancy and advertising, Reissert et al. (1989) found that the growth of such services was highest where increasing tertiarisation of manufacturing firms took place. This was mainly the case in Southern Germany. Linking this empirical evidence to the interaction hypothesis they came to the conclusion that "the key for the explanation of the 'little employment miracle' in the South is due to interactive services, i.e. to the increasing networking of goods production and firms offering 'intelligent' (knowledge based) services" (Reissert et al., 1989, p. 97).

4 . 2 . ' A D V A N C E D ' P R O D U C E R S E R V I C E S IN T H E S T A T I S T I C S

One peculiarity of studies on the service sector is the fact of ever changing statistical data bases and incompatible classification schemes. Statistical sources are very different in classifications, dates and objects of investigation. This affects all kinds of studies of the service sector but principally those on producer services and their regional pattern (Statistisches Bundesamt, 1990b; Gaebe et al., 1993). Hence, empirical evidence is rather scattered and only of limited comparability. There are not yet regularly produced statistics on producer services in Germany. The census of workplaces (Arbeitssti~ttenziihlung) is precise in location and is

160 Progress in Planning

highly disaggregated up to the 4-digit-level, but it suffers from being carried out only once a decade (1970 and 1987, re.spectively). Furthermore. its classification of activities neither fits into NACE (i,e. the European classification) on the NUTS-3 level nor is it compatible with employment statistics created by the Federal Bureau of Labour (BfA: Bundesanstah far Arbeit). In 1991/2, the Federal Bureau of Statistics made a pilot study of producer services, testing NACE adaptation of its classification in order to make some suggestions for future regular surveys on producer services (Reim, 1992). But apart from some interesting facts about the structure of the sector, first results have to be interpreted very carefully, and, fur thermore, do not provide regional-level information.

In order to get a first insight into the geography of producer services in Germany and its recent changes, only employment statistics from the Federal Bureau of Labour are - - to a limited extent - - useful. Their disadvantage is that they only encompass those persons in the service sector who are obliged to contribute to the national insurance system. This means that self-employed persons, civil servants, independent businessmen, managers as well as participating family members are not recorded. One could easily imagine problems for scientific analysis in activities such as legal services, software services or consultancy which are characterised by a large number of small-scale independent businesses.

Fur thermore , classification of activities is not compatible with other official statistics. This holds particularly true for data processing which is a 4-digit class of activities in the census of 1987 (no. 7892) while it is embodied in three different classes of the BfA data. BfA statistics, however, make possible further differentiation of service activities according both to sectors - - although possibly using another elassifactory system than the census - - and the kind of activities carried out. They will be used further on. A word seems necessary to explain the spatial level chosen in this chapter. The NUTS-3 level which actually is equal to the district (Kreis) in Germany provides information which is spatially more precise but not detailed. The NUTS-2 level which is the primary administrative division of a Land (Regierungsbezirk) might give more detailed information but is geographically meaningless. We should draw attention to the fact that the statistical unit registered on NUTS-3 level is the plant (Betriebsstiitte); in consequence, local service units of manufacturing firms will be treated as services. The NUTS-3 level is better suited to describing changes in urban agglomeration areas, of which no general definition can be given (hence, different studies have used different boundaries).

Additionally, the meaning of producer services is far from clear. As has been suggested earlier, financial services will be excluded here (see introduction to this special issue). Even if there were general agreement on what producer services means, a further differentiation between routinised and knowledge-intensive 'advanced' producer services proves to be necessary as only the latter have a particular significance for the competitiveness of manufacturing industries on

The Geography of Advanced Producer Services in Europe 161

a global scale. Knowledge for managerial purposes will be created in services such as legal advice and consultancy, for technical purposes in engineer's offices and laboratories. Hence only certain sub-sectors of producer services could be called 'advanced'. In the following section, the sub-sectors of (1) legal services, (2) consultancy and accountancy, (3) architecture and technical consultancy, (4) chemical laboratories, and (5) advertising, based on BfA statistics, will represent advanced producer services. There are two caveats: first, not all of these service firms are knowledge-intensive and oriented towards export-oriented manufacturing sectors, sometimes they are more embedded in local economic circuits. Second, this classification only superficially fits into the NACE classification of legal services (835), accountancy (836), technical services (837), advertising (838) and other business services (839).

4 . 3 . T H E S P A T I A L P A T T E R N O F A P S

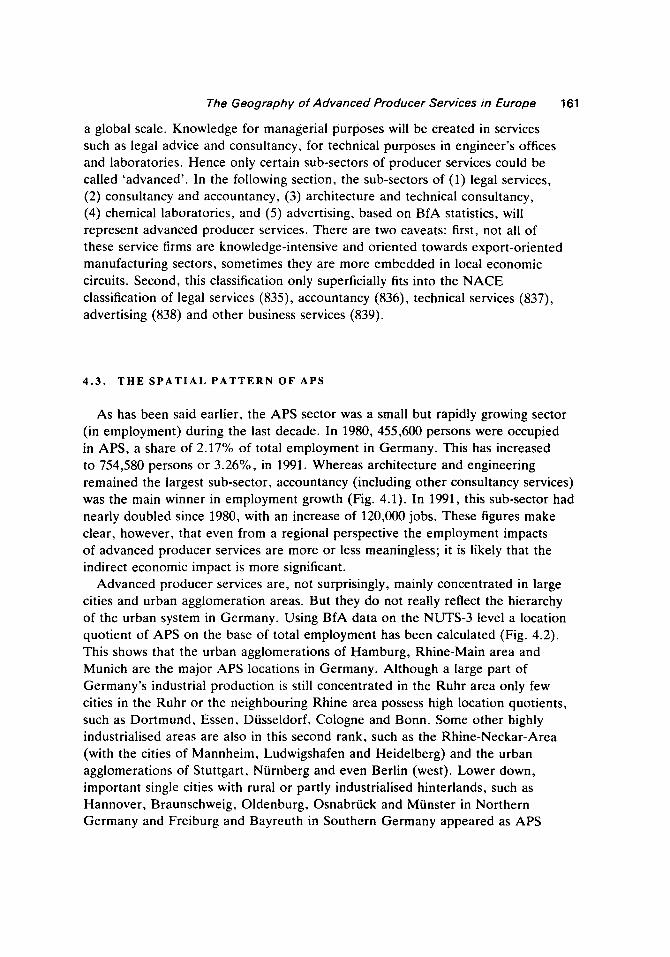

As has been said earlier, the APS sector was a small but rapidly growing sector (in employment) during the last decade. In 1980, 455,600 persons were occupied in APS, a share of 2.17% of total employment in Germany. This has increased to 754,580 persons or 3.26%, in 1991. Whereas architecture and engineering remained the largest sub-sector, accountancy (including other consultancy services) was the main winner in employment growth (Fig. 4.1). In 1991, this sub-sector had nearly doubled since 1980, with an increase of 120,000 jobs. These figures make clear, however, that even from a regional perspective the employment impacts of advanced producer services are more or less meaningless; it is likely that the indirect economic impact is more significant.

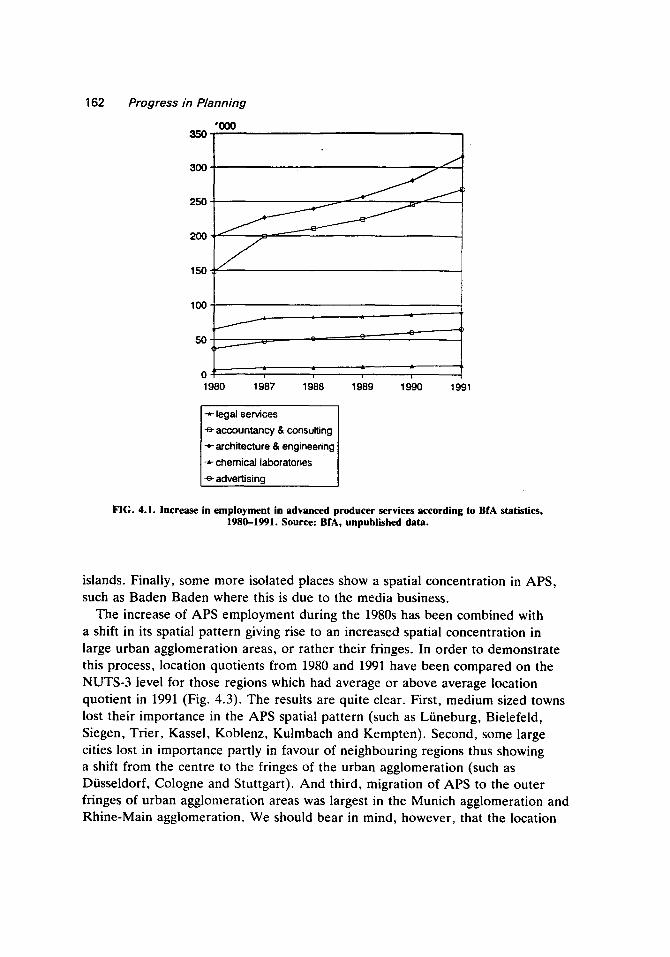

Advanced producer services are, not surprisingly, mainly concentrated in large cities and urban agglomeration areas. But they do not really reflect the hierarchy of the urban system in Germany. Using BfA data on the NUTS-3 level a location quotient of APS on the base of total employment has been calculated (Fig. 4.2). This shows that the urban agglomerations of Hamburg, Rhine-Main area and Munich are the major APS locations in Germany. Although a large part of Germany's industrial production is still concentrated in the Ruhr area only few cities in the Ruhr or the neighbouring Rhine area possess high location quotients, such as Dortmund, Essen, Dtisseldorf, Cologne and Bonn. Some other highly industrialised areas are also in this second rank, such as the Rhine-Neckar-Area (with the cities of Mannheim, Ludwigshafen and Heidelberg) and the urban agglomerations of Stuttgart, N/irnberg and even Berlin (west). Lower down, important single cities with rural or partly industrialised hinterlands, such as Hannover, Braunschweig, Oldenburg, Osnabriick and MOnster in Northern Germany and Freiburg and Bayreuth in Southern Germany appeared as APS

162 Progress in Planning

35O

300

250

"000

2 0 0 / - - J

lOO

f

JL

o 1980 1987

J. , t ,L

1988 1 9 1990 1991

I --,- legal services

-e- accountancy & consulting

--*-architecture & engineering

-*- chemical laboratories

-6- advertising

FIG. 4.1. Increase in employment in advanced producer services according to BfA statistics, 1980-1991. Source: BfA, unpublished data.

islands. Finally, some more isolated places show a spatial concentration in APS, such as Baden Baden where this is due to the media business.

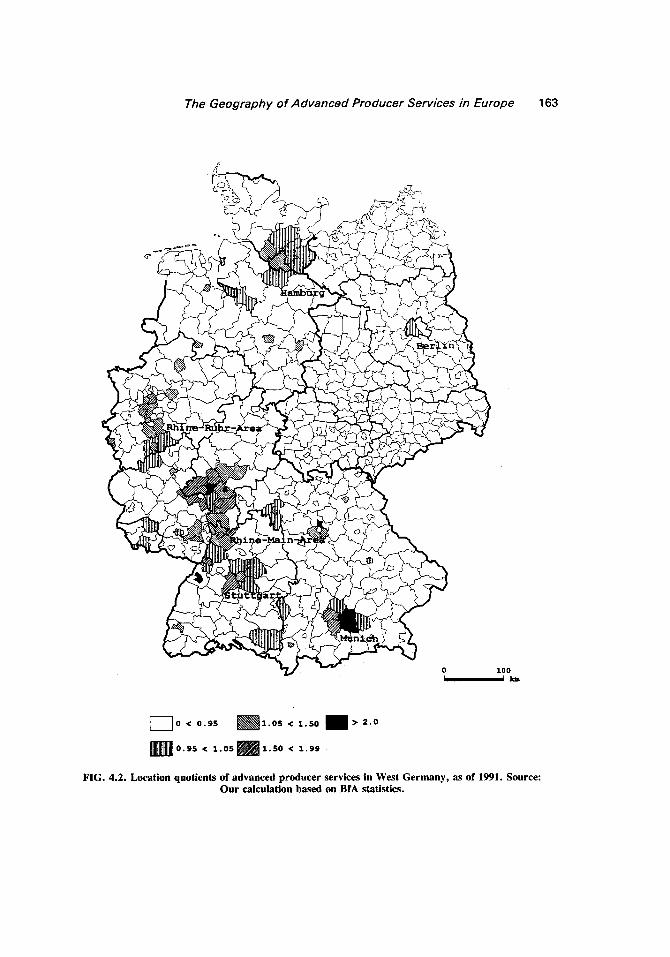

The increase of APS employment during the 1980s has been combined with a shift in its spatial pattern giving rise to an increased spatial concentration in large urban agglomeration areas, or rather their fringes. In order to demonstrate this process, location quotients from 1980 and 1991 have been compared on the NUTS-3 level for those regions which had average or above average location quotient in 1991 (Fig. 4.3). The results are quite clear. First, medium sized towns lost their importance in the APS spatial pattern (such as Lfineburg, Bielefeld, Siegen, Trier, Kassel, Koblenz, Kulmbach and Kempten). Second, some large cities lost in importance partly in favour of neighbouring regions thus showing a shift from the centre to the fringes of the urban agglomeration (such as Diisse|dorf, Cologne and Stuttgart). And third, migration of APS to the outer fringes of urban agglomeration areas was largest in the Munich agglomeration and Rhine-Main agglomeration. We should bear in mind, however, that the location

The Geography of Advanced Producer Services in Europe 163

100 I I ~

~-~o< o,ss ~ l . o s < l . s o I > 2 . o

~ o . s s < 1 . O S ~ l . S O < 1.99

FIG. 4.2. Location quotients of advanced producer services in West Germany, as of 1991. Source: Our calculation based on BfA statistics.

164 Progress in Planning

< 0 ~ 0.I < 0.3 ~ 0.5 < 1.0

~o<o.I ~ o.3 < o.5 l>l.O

FIG. 4.3. Changes in location quotients of APS in Germany, 1980-1991.

l O O

The Geography of Advanced Producer Services in Europe 165

quotient is calculated on relative figures, thus leading to a larger shift in the location quotient where absolute figures were previously low.

This general consideration of all APS subsectors covers over a tendency of increasing specialisation of certain urban agglomeration areas, in particular producer services. For this purpose we made a rough comparison of location quotients for particular services with those for all APS services. The major differences appeared in the Rhine-Main area where accountancy and consultancy services clustered at the Western fringe. Advertising was highly concentrated: first, in Hamburg and the neighbouring district Pinneberg; second, in Diisseldorf; and, third, in Frankfurt city as well as some neighbouring districts. Finally, architecture and engineering services, apart from showing an above average concentration in Essen or the medium sized town of Aachen where one of the famous technical universities is located, mainly cluster in some districts of the Rhine-Main area, particularly south of Frankfurt/Main, in and around Munich and in Erlangen and Fiirth (which may be due to the Siemens research laboratories). Hence, obviously Hamburg and Diisseldorf seem to be specialised in advertising, Munich, in engineering whereas Frankfurt and its surroundings show a broader spectrum of APS.

It is quite obvious from Fig. 4.3 that APS firms increasingly tend to locate on the fringes of large urban agglomeration areas. Although the city of Frankfurt and the city of Munich remained focal points in the spatial pattern of APS, they only grew at the national average rate from 1980 to 1991. A much above average increase and specialisation occurred in suburban NUTS-3 regions with attractive residential areas such as the Rheingau-Taunus district West of Frankfurt/Main which is famous in the world for its Rhine wines. As has been mentioned before, there is a lack of precise information about the location of particular advanced producer services. In the following sections, therefore, the spatial patterns of two particular advanced producer services will be analysed using further sources.

4 . 4 . T H E G E O G R A P H Y O F A C C O U N T A N C Y F I R M S

One of those advanced producer services which exists mainly because of state regulations is accountancy. Auditing of annual statements of accounts has been obligatory in Germany for joint stock companies since the banking and economic crisis at the beginning of the 1930s. Changes in law in 1985 took into account the emerging common EC law and extended the circle of firms with obligatory inspection to companies with limited liability. The demand for auditing, hence, is increasing considerably, while the supply of accountants is restricted to about 6340 (in 1989) due to a rigorous training and selection system determined by the Ministries of Economics in the different L~inder. In what follows we mainly draw upon a recent survey on the long-term development of this subsector which

166 Progress in Planning

was based largely upon data from the national register of accountants (de Eange, 1993).

Accountants perform different activities, but mainly auditing, tax consultancy and general consultancy. The supply of auditing is highly segmented. In the first place, most accountants are free-lance, either having an office of their own or joining a partnership with other auditors, lawyers or tax experts. In general, these are small offices which are mainly oriented to giving tax consultancy. In consequence, they are largely offering services to local business which means that they could be interpreted as services for local demand only. This interpretation is confirmed by the fact that accountants are located in most central places of a higher order and even some middle order central places in Germany. In the second place, few firms employ a large number of accountants; de Lange (1993), counted 11 accountancy companies with more than five employees giving employment to 177 accountants in total in DiJsseldorf, in 1980, and only six companies with 63 accountants in Munich. It is this segment of large accountancy firms which is spatially concentrated in a few cities. The activities of such firms differ considerably from those of the smaller professionals as only large companies are able to carry out auditing of large (multinational) companies.

Considering the spatial distribution of employed (rather than self-employed) accountants only, i.e. of larger accountancy firms, Frankfurt/Main is at the top of the list, followed by Diisseidorf, Hamburg and Stuttgart. De Lange (1993, p. 29) did not find, however, a close correlation between this spatial pattern and the regional distribution of headquarters of large firms (of all sectors). Obviously the ties between large manufacturing firms and APS are loosening giving rise to a new hierarchy of APS centres. What has been said for the spatial pattern of total employment in APS obviously does not hold true for this particular advanced producer service.

In the long-run, however, accountants seem to be a good indicator of the fundamental reorganisation of the German city system which took place after World War II and before unification (de Lange, 1993). While Berlin was unchallenged at the top in 1939, followed at a large distance by Hamburg, Leipzig, Munich and K61n, from the 1960s onwards Frankfurt/Main and Dtisseldorf took the lead. Although Berlin and some other East German places experience the location of new accountants, a return to the old geography of the sector is hardly to be expected after unification, as there are few headquarters of larger firms in East Germany.

4 . 5 . T H E G E O G R A P H Y O F S O F T W A R E P R O D U C T I O N IN W E S T G E R M A N Y

Given the increasing penetration of all economic sectors by information technology, software production has emerged as one of the most important

The Geography of Advanced Producer Services in Europe 167

knowledge intensive service sectors. During the 1980s, the software market in Germany grew annually by 19% while the hardware market only increased by 9% (Buschmann et al. , 1989, p. 20). Technical flexibility, which is identified as one characteristic of the modern economy, is mainly achieved by software in production, organisation, distribution and, not least, in finance. Only relatively small productivity gains have been achieved in software production so far, which means that the sector is very intensive in personnel. Standardised solutions are hardly possible in a context of customised problem solving. Compared to other countries, German software production is extremely expensive, partly due to the preponderance of small software houses. Recent studies, therefore, identify a significant threat of relocation by software production to low wage countries (Weber, 1992).

Software production in Germany is still mainly a matter of activities internal to user companies, however. In 1989, software expenditures by enterprises were estimated at 32,200 million DM, of which only 37% were purchased externally (Buschmann et al . , 1989, p. 20). Technological change in large firms in traditional major industrial sectors such as steel making, car manufacturing and machine tool production has been promoted more via internal software departments than by purchase of software services. These firms are thought to be in a better position to produce customised software solutions, and, more importantly, to cover the long-term maintenance of software in view of the often short life-spans among the predominantly small software houses in Germany.

Public statistics on software houses are as inadequate as those on other advanced producer services. One of the reasons for this is that there exists no unambigous definition of the software sector. This sector covers, first, different activities such as systems specification, systems design, implementation, testing and maintenance both of standardised and customised software products; second, software production has long been combined with hardware production; and, third, since the implementation of software is often a cross-sectional technique it is often necessary to maintain close connection to other advanced producer services such as consultancy. Furthermore, the four-digit classification of data processing used in the recent census of workplaces in Germany (1987) included both advanced and routine producer services (the latter involving such as book-keeping, secretarial works and computing). Software production in its proper sense only accounted for a small but unknown share of this sector. According to this census, there were 20,280 establishments with 100,590 employees in this sector in Germany in 1987. In calculating another location quotient it can be stated that the sector is mainly located in Southern Germany. Data processing is spatially concentrated in a few urban agglomeration areas, first Munich, followed by Frankfurt, Stuttgart and Hamburg. In the Munich case, concentration of data processing can be mainly explained as a phenomenon of what is called 'Isar

168 Progress in Planning

valley': the unique concentration of space, aircraft and defence industries (Haas, 1988) and of the central research lab of Siemens and other microelcctronics firms. In the Rhine-Main area both incubator organisations such as the technical university of Darmstadt with its highly respected computer science department and four other research labs working in fields such as graphic interactive systems, telecommunications and media technology on the one hand, and local demand in the financial and distribution sectors of Frankfurt , on the other hand, influence the spatial concentration of data processing. As can be observed for other advanced producer services as well, the Ruhr area is poorly equipped with data processing units; some spatial concentration can be found in DiJsseldorf and Cologne. But more evident are the clusters of data processing around large manufacturing locations such as Stuttgart, Ludwigshafen or Niirnberg - - in the latter case due to the nearby Siemens research labs in Erlagen.

Sound market reports, however, tell another story about the far smaller number of software houses in Germany. In 1989, the Buschmann report estimated the number of larger software houses, i.e. those with more than 10 employees, at 850 to 900 firms, and that of small firms at under 1500. It is, however, extremely difficult to get a close overview of this sector in Germany. During the rapid growth of the software sector in recent decades, it is mostly small firms that have been created, and this has caused an extreme fluctuation among firms and gave rise to only a few large enterprises.

4 . 6 . P R E S E N T A N D F U T U R E T R E N D S I N T H E W E S T G E R M A N

G E O G R A P H Y O F A P S

Obviously, there is a paradox emerging from this very short overview of the geography of advanced producer services in West Germany: first, as has been said before, there exists a close relationship between the regional growth of APS and the survival of firms in the manufacturing sector; but second, the specialisation of some large urban agglomeration areas in APS is further intensified. More anecdotal information points to the fact that the Rhine-Main urban agglomeration, i.e. Frankfurt/Main and its surroundings, has emerged as the major centre for subsidiaries of foreign APS firms and of large domestic firms in services such as advertising, business lawyers, accountants. For instance, among the 10 largest 'law factories' in 1989, four were in Frankfurt but only two in D~isseldorf and one in Hamburg; for the 10 largest accountancy firms Frankfurt ranked first with five firms, accounting for 66% of total turnover; out of the 10 largest advertising firms two are located in the urban agglomeration of Hamburg, three in DiJsseldorf and four in Frankfurt/Main (Handelsblatt 43, 3 March 1993, p. 20); finally, the Rhine-Main area ranked highest with regard to the top twenty firms in information technology consultancy (Brake, 1991).

The Geography of Advanced Producer Services in Europe 169

Across all advanced producer services in Germany, most of which are small-sized firms or free-lancers, concentration is taking place, in combination with the increasing arrival of foreign subsidiaries. With the increasing necessity for large German manufacturing firms to promote international sales activities, demand for advertising is shifting from small domestic firms to foreign subsidiaries, with the latter taking the first 10 places in this business. In consequence, concentration is increasing rapidly. The same holds true for business lawyers since 1987, when the Federal Constitutional Court first allowed mergers of free-lance lawyers. A further example is the software sector. As might be expected from the small size of most software firms and the particular medium-sized structure of user firms in Germany the software market has largely remained domestic. In 1989, only 11% of larger software firms (more than 10 employees) had a foreign subsidiary, mostly in neighbouring German speaking Switzerland and Austria but only rarely in other EC countries and the U.S.A. On the other hand, 34% of all larger software firms in Germany were subsidiaries of, or joint ventures with, foreign firms, particularly American and French ones (Buschmann et al. , 1989, p. 89). The market, however, is quickly changing. First, in the current economic crisis many large hardware and user firms such as banks and manufacturing enterprises, are farming out their own software departments, giving risc to a growing number of large software firms; second, a significant concentration trend is emerging, mainly affecting medium-sized software firms. While the number of foreign software firms are increasing in the German market, which remains the largest national market in Europe - - boosted by the creation of the Single European Market - - (e.g. Pawar and Driva, 1992), large German firms are starting to go international. This process is not without difficulties, however; for instance, Daimler-Benz AG, through its subsidiary Debis, GmbH, bought a share in Europe's largest software house, the French Cap Gemini Sogeti, but did not manage to obtain majority control. Software AG from Darmstadt, which is the largest German firm in the sector, still achieves about 64% of its annual turnover in Europe, while the second largest firm (SAP) achieved 58% of its turnover on the domestic market in 1990.

The APS-sector in Germany is subject to rapid change. Trends towards concentration and Europeanisation are accelerating. Given the small-size of most firms in the sector, both trends are bound to involve leading foreign firms. At the same time, however, the manufacturing base of the German economy, so strong for so long, has entered into a serious crisis. Formerly prosperous manufacturing regions, such as Baden-Wiirttemberg, the Munich area, or the Rhine-Main area, are facing increasing deindustrialisation and rising unemployment rates. It may be argued that manufacturing had postponed reorganisation pressures during the recent prosperous decade and is now being forced into a precipitate restructuring process which is affecting the labour force not only on the shopfloor but in administration and management as well. This may contribute to a further

JPP 43-Z/3-F

170 Progress in Planning

decoupling of manufacturing and APS activities on the regional level in the future But it will not shift the economic base. of Germany towards the service sector.

4 . 7 . R E F E R E N C E S

ABELSHAUSER, W. (1983) Wirtschaftsgeschichte der Bundesrepublik Deutschland, 1945-1980. Economic History of the Federal Republic of Germany, 1945-1980, Frankfurt/Main, edition Suhrkamp 1241.

BADE, Fr. J., MIDDELMANN, U. and SCHULER, M. (1990) Expansion und regionale Ausbreitung der Dienstleistungen. Expansion and regional distribution of services, ILS Schriften 42, Dortmund.

BRAKE, KI. (1991) Dienstleistungen und r~umliche Entwicklung Frankfurt, Strukturveriinderungen in Stadt und Region. Services and spatial development Frankfurt. Structural changes in the city and the region. Universit~it Oldenburg, Dortmund.

BUSCHMANN, E. et al. (1989) Der Software-Markt in der Bundesrepublik Deutschland. The Software Market in the Federal Republic of Germany, St Augustin, Gesellschaft fiir Matbematik und Datenverarbeitung mbH.

DEUTSCHE BUNDESBANK (1993) Zahlungsbilanzstatistik. Statistics on the balance of payments. Monatsberichte Reihe 3, Nov. 1993.

GAEBE, W., STRAMBACH, S., WOOD, P. and MOULAERT, F. (1993) Employment in business related services ~ An intercountry comparison of Germany, the United Kingdom and France. Unpublished Report for the Commission of the European Community, Stuttgart.

GRUHLER, W. (1990) Dienstleitungsbestimmter Strukturwandel in deutschen lndustrieunternehmen. Service-led Structural Change in German Manufacturing Enterprises, KOln, Deutscher Instituts-Verlag.

HAAS, H. D. (1988) The German armament industry with specific regard to military air and space crafts, Zeitschriflfar Wirtschaflsgeographie 32(3), 192-208.

JOST, P. (1991) Die r~iumliche Ordnung auf dem Weg in die Dienstleistungsgesellschaft [The spatial organisation on the way to the service society], Raumforschung und Raumordnung 49(4), 237-246.

KOPPEL, M. (1983) Zur Bedeutung der Dienstleistungssektoren fiir die regionale Entwicklung in der Bundesrepublik. On the significance of service sectors for regional development in the Federal Republic. Mitteilungen des Rheinisch-Westfiilischen lnstituts far Wirtschaftsforschung, 34, 205-27.

LANGE, De. N. (1993) Standorte unternehmensbezogener Dienstleistungsfunktionen in Deutschland. Das Beispiel der Wirtschaftsprtifer [Locations of business services in Germany. The case of accountants. Geographische Zeitschrift, 81, 18-34.

PAWAR, K. S. and DRIVA, H. (1992) An investigation of British computing services firms exporting to Germany. European Business Review 92(4), 35-43.

REIM, U. (1992) Piloterhebung im Dienstleistungsbereich [pilot survey in the realm of services]. Wirtschaft und Statistik, 10, 718-27.

REISSERT, B., SCHMIDT, G. and JAHN, J. (1989) Mehr Arbeitspliitze dutch Dienstleistungen? Ein Vergleich der Beschi~ftigungsentwicklung in den Ballungsregionen der BRD. More employment through services? A comparison of employment development in the urban agglomerations of the Federal Republic of Germany, Wissenschaftszentrum disc. paper FS I 89-14, Berlin.

SCHAMP, E. W. (1987) Business services for manufacturers: demand behaviour by enterprises in Lower Saxony, in F. E. I. Hamilton (ed), Industrial Change in Advanced Economies, pp. 270--291. Croom Helm, London.

SCHAMP, E. W., Linge, G. J. R. and Rogerson. Ch. (eds) (1993) Finance, Institutions and Industrial Change: Spatial Perspectives, de Gruyter, Berlin.

SCHICKHOFF, 1. (1985) Dienstleistungen ftir lndustrieunternehmen: Einfliisse yon Unternehmens- und Standorteigenschaften auf die Reichweite ausgew~ihlter industrieller Dienstleistungsverflechtungen. Services for manufacturing firms: Impact of factors of enterprise and location on the range of selected service linkages. Erdkunde, 39, 73--84.

STATISTISCHES BUNDESAMT (1990a) Input-Output Tabellen 1985 bis 1988. Volkswirtschaftliche Gesamtrechnungen, Fachserie 18 Reihe 2, Wiesbaden.

The Geography of Advanced Producer Services in Europe

STATISTISCHES BUNDESAMT (1990b) Zum Datenangebot iiber Dienstleistungen in der Bundesstatistik. On the data offer about services in the Federal Statistics. Wiesbaden, Schriftenreihe Ausgew~hlte Arbeitsunterlagen zur Bundesstatistik 3.

STATISTISCHES BUNDESAMT (1992), Statistisches, Jahrbuch 1992, Stuttgart. WEBER, H. (1992) Die Software-Krise und ihre Macher [The software crisis and its men of action].

Springer, Berlin.

171