the gatehouse bank islamic finance consumer report 2019

TRANSCRIPT

The Gatehouse Bank Islamic Finance Consumer Report 2019

Contents

The UK Muslim Consumer

Who is the UK Muslim consumer?

Islamic FinanceConsumer Profiles

AwarenessPerception

UseExperience

Advocacy

Conclusions and Recommendations

Mapping the Consumer Journey

Looking Ahead

2

Introduction by Charles HaresnapeChief Executive Officer of Gatehouse Bank

Welcome to the first Islamic Finance Consumer Report, commissioned by Gatehouse Bank.

The UK is recognised as a leading Western centre for Islamic Finance and a growing number of providers are now offering Shariah-compliant products and services to individuals and businesses.

However, as a relatively new member of the Islamic Finance community, I have been amazed how little research has been carried out amongst UK Muslim consumers. This is why I was eager for Gatehouse Bank to commission this study.

In order to ensure the Islamic Finance market continues to offer attractive services, it is important to understand how it is viewed by existing and potential customers and how the industry can better engage and provide the support they need to help them realise their dreams and aspirations.

This report, which we believe is the first of its kind, highlights a number of areas where Islamic Finance is having a positive impact. It also reveals barriers that Muslim consumers feel they face when considering the best financial solution for their individual needs.

I hope that this document will help interested parties to understand the views of the UK Muslim community and prove useful for those looking to engage and provide attractive services. At Gatehouse Bank, a growing UK bank offering Shariah-compliant financial services, we are eager to understand more about the banking needs of UK Muslims and will be utilising the insight this report provides to develop new and innovative propositions and services.

3

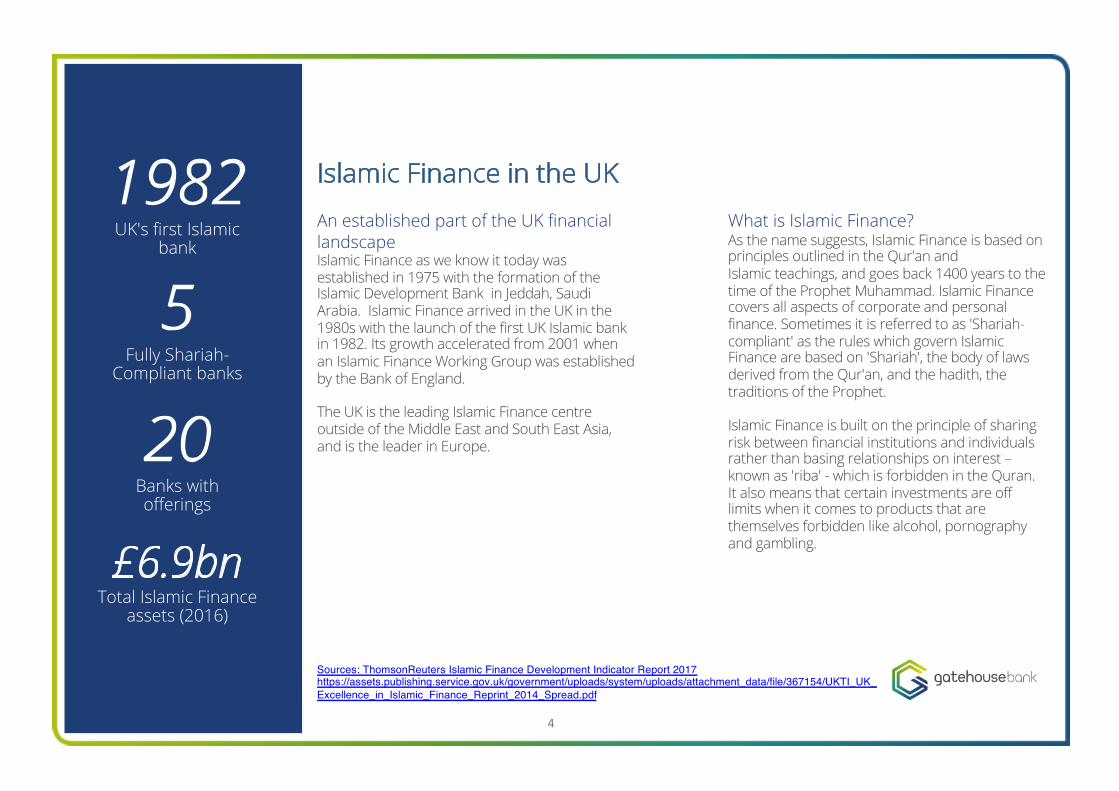

1982UK's first Islamic

bank

5Fully Shariah-

Compliant banks

20Banks with offerings

£6.9bnTotal Islamic Finance

assets (2016)

Islamic Finance in the UK

An established part of the UK financial landscapeIslamic Finance as we know it today was established in 1975 with the formation of the Islamic Development Bank in Jeddah, Saudi Arabia. Islamic Finance arrived in the UK in the 1980s with the launch of the first UK Islamic bank in 1982. Its growth accelerated from 2001 when an Islamic Finance Working Group was established by the Bank of England.

The UK is the leading Islamic Finance centreoutside of the Middle East and South East Asia, and is the leader in Europe.

What is Islamic Finance?As the name suggests, Islamic Finance is based on principles outlined in the Qur'an and Islamic teachings, and goes back 1400 years to the time of the Prophet Muhammad. Islamic Financecovers all aspects of corporate and personal finance. Sometimes it is referred to as 'Shariah-compliant' as the rules which govern Islamic Finance are based on 'Shariah', the body of laws derived from the Qur'an, and the hadith, the traditions of the Prophet.

Islamic Finance is built on the principle of sharing risk between financial institutions and individuals rather than basing relationships on interest –known as 'riba' - which is forbidden in the Quran. It also means that certain investments are off limits when it comes to products that are themselves forbidden like alcohol, pornography and gambling.

Sources: ThomsonReuters Islamic Finance Development Indicator Report 2017https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/367154/UKTI_UK_Excellence_in_Islamic_Finance_Reprint_2014_Spread.pdf

4

Executive Summary5

Whilst the Islamic Finance industry in the UK has been established since 1982, relatively little insight is available on the opinions of Muslim consumers, what they know about the industry and how they interact with it.

This first-of-its-kind study aims to address these questions so that the industry can create stronger engagement at every stage of the consumer journey from awareness and perception through to use, experience and advocacy. In particular the study addresses the profiles of existing users, those who are interested and those who currently say that they are not interested. It also identifies key drivers and barriers for users in deciding whether to purchase Islamic Finance products and services.

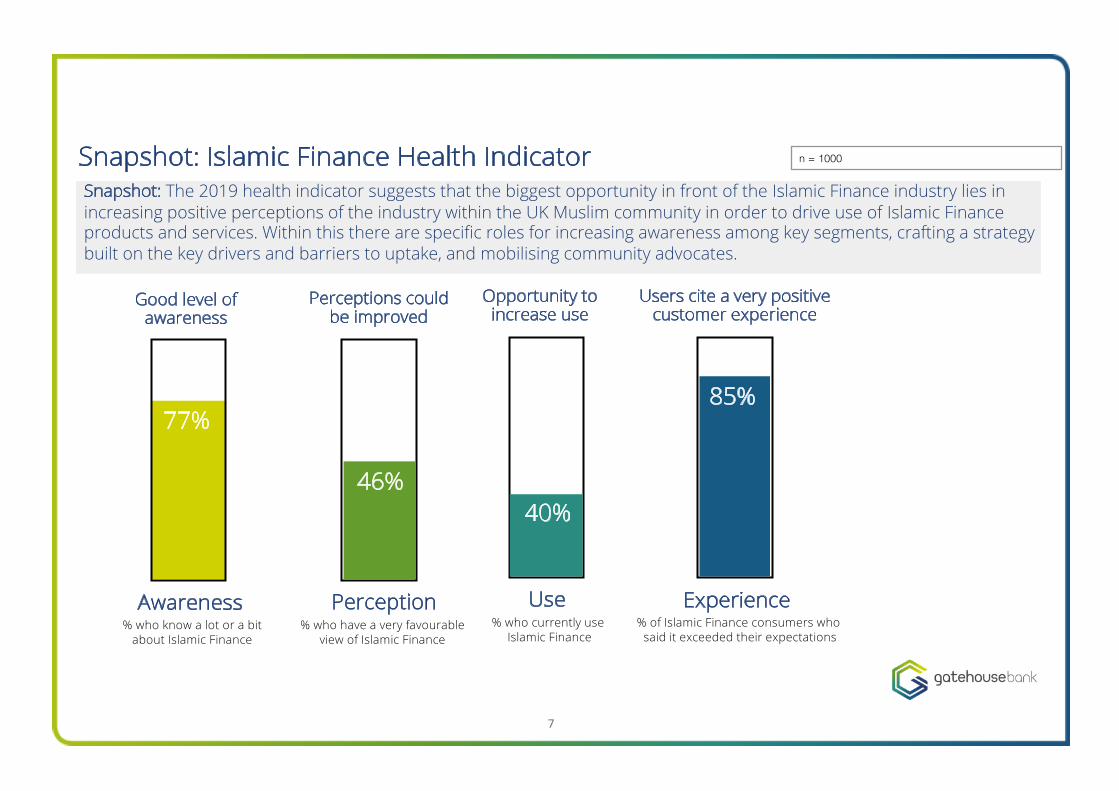

The report introduces an Islamic Finance HealthIndicator as a snapshot which measures the current state of the industry across the consumer journey. At each stage of the consumer experience we investigate the responses of Muslim consumers, and highlight where the biggest areas of focus should be.

Understanding UK Muslim consumer attitudes to Islamic Finance

AWARENESS PERCEPTION USE EXPERIENCE

6

Snapshot: Islamic Finance Health Indicator

77%

46% 40%

85%

Good level of awareness

Perceptions could be improved

Users cite a very positive customer experience

Opportunity to increase use

Awareness Perception Use Experience% who know a lot or a bit

about Islamic Finance% who have a very favourable

view of Islamic Finance% who currently use

Islamic Finance% of Islamic Finance consumers who

said it exceeded their expectations

n = 1000

Snapshot: The 2019 health indicator suggests that the biggest opportunity in front of the Islamic Finance industry lies inincreasing positive perceptions of the industry within the UK Muslim community in order to drive use of Islamic Financeproducts and services. Within this there are specific roles for increasing awareness among key segments, crafting a strategy built on the key drivers and barriers to uptake, and mobilising community advocates.

7

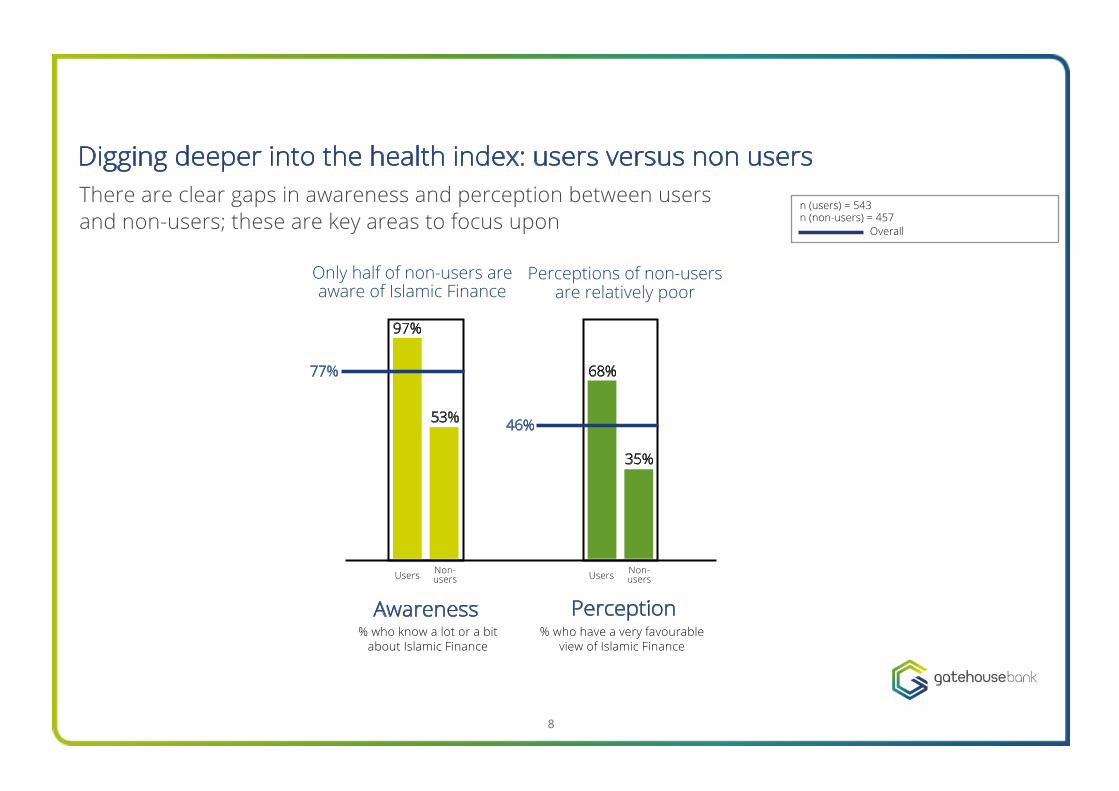

Only half of non-users are aware of Islamic Finance

Perceptions of non-users are relatively poor

Digging deeper into the health index: users versus non users

Awareness Perception% who know a lot or a bit

about Islamic Finance

Users Non-users Users Non-

users

97%

68%

53%

35%

77%

46%

n (users) = 543n (non-users) = 457

% who have a very favourableview of Islamic Finance

Overall

There are clear gaps in awareness and perception between users and non-users; these are key areas to focus upon

8

Awareness Perception% who know a lot or a bit

about Islamic Finance

Users Non-users Users Non-

users

97%

68%

53%

35%

77%

46%

This is even clearer when looking in depth at users, those interested and those not interested, showing again that awareness and perception are the key areas where efforts need to be focused

n (users) = 543n (interested) = 248n (not interested) = 209

3%

36%

Not interested

Overall

% who have a very favourableview of Islamic Finance

Not interested

9

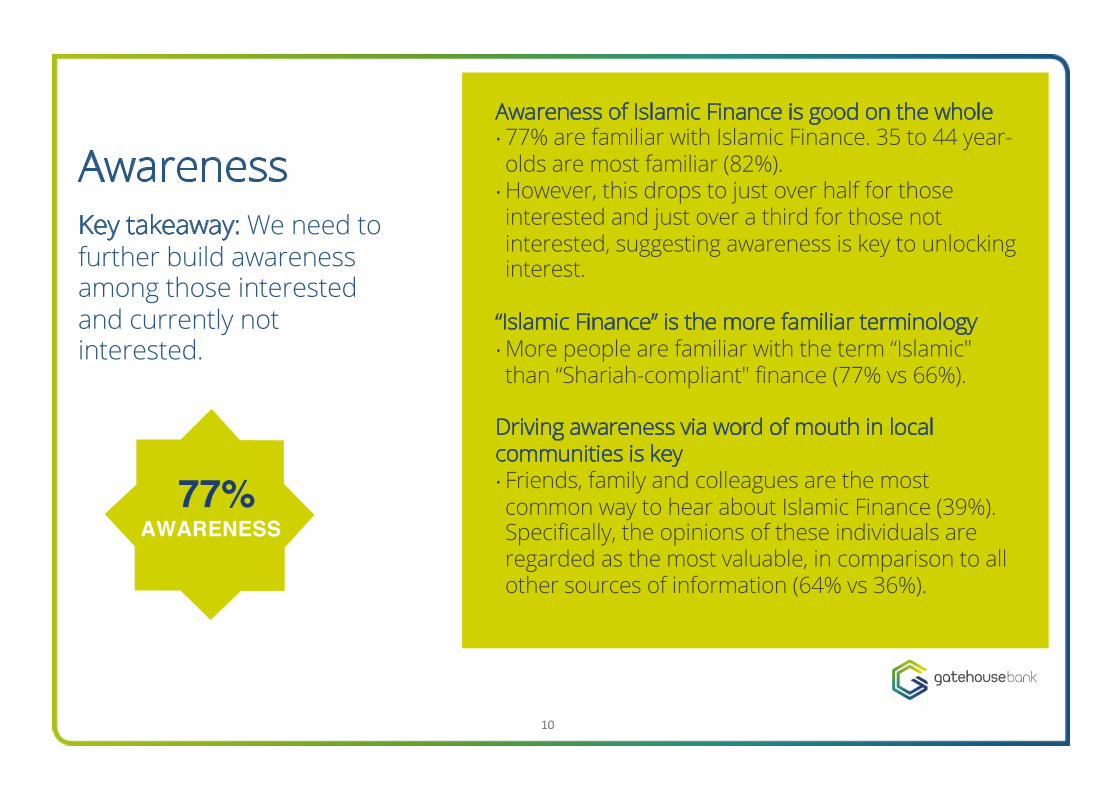

AwarenessAwareness of Islamic Finance is good on the whole• 77% are familiar with Islamic Finance. 35 to 44 year-olds are most familiar (82%).

• However, this drops to just over half for thoseinterested and just over a third for those not interested, suggesting awareness is key to unlocking interest.

“Islamic Finance” is the more familiar terminology• More people are familiar with the term “Islamic"than “Shariah-compliant" finance (77% vs 66%).

Driving awareness via word of mouth in local communities is key• Friends, family and colleagues are the mostcommon way to hear about Islamic Finance (39%). Specifically, the opinions of these individuals are regarded as the most valuable, in comparison to all other sources of information (64% vs 36%).

AWARENESS77%

10

Key takeaway: We need to further build awareness among those interested and currently not interested.

Perceptions of Islamic Finance are more positive amongst current users with significant work to do among non-users• 68% of current users vs 21% of non-users viewed Islamic Finance very

favourably.

Experience with Islamic Finance boosts perceptions of the wider financial industry • The whole financial industry is viewed more favourably by current Islamic

Finance users (59% very favourable) compared to non-users (19% veryfavourable).

Islamic Finance is perceived as having a strong sense of community• People believe Islamic Finance is dedicated to the interests of the community

(71%) and works hard to better serve its customers (61%), suggesting thatbuilding on this sense of community could be a powerful universal driver of use.

Some scepticism about how Islamic the products truly are• Some people felt that they didn’t know how certain Shariah–compliant products

really were (61%), suggesting more work needs to be done to increase the clarityand understanding of Islamic Finance products and services.

Seen as ethical, trustworthy and a good service but difficult to purchase• Most people felt that Islamic Finance aligned with their values and beliefs (72%),

was trustworthy and ethical (71%), and offered a good service (71%), but wasdifficult to purchase (60%) and that it was difficult to compare options (62%).This suggests more work needs to be done to make it more accessible andeasier to obtain.

Perception

PERCEPTION46%

11

Key takeaway: This is the main area of focus as significant challenges exist with perception overall but particularly among non-users. This is the key to unlocking growth.

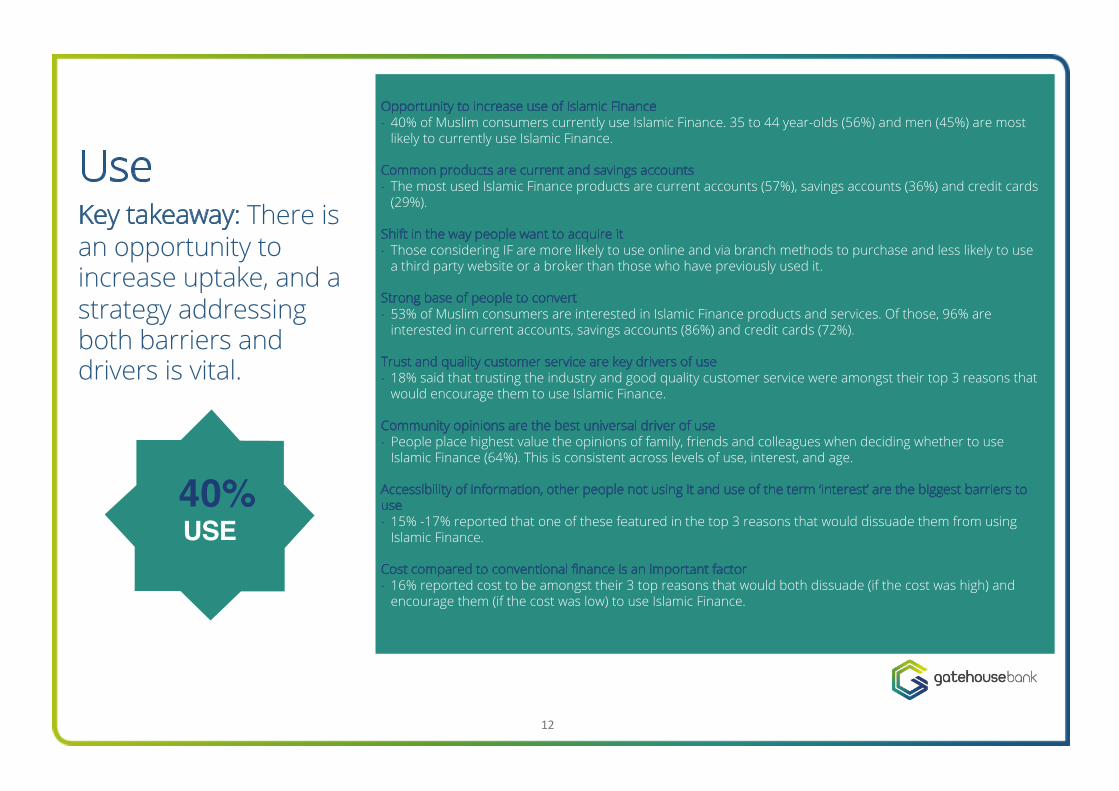

Opportunity to increase use of Islamic Finance• 40% of Muslim consumers currently use Islamic Finance. 35 to 44 year-olds (56%) and men (45%) are most

likely to currently use Islamic Finance.

Common products are current and savings accounts • The most used Islamic Finance products are current accounts (57%), savings accounts (36%) and credit cards

(29%).

Shift in the way people want to acquire it • Those considering IF are more likely to use online and via branch methods to purchase and less likely to use

a third party website or a broker than those who have previously used it.

Strong base of people to convert• 53% of Muslim consumers are interested in Islamic Finance products and services. Of those, 96% are

interested in current accounts, savings accounts (86%) and credit cards (72%).

Trust and quality customer service are key drivers of use • 18% said that trusting the industry and good quality customer service were amongst their top 3 reasons that

would encourage them to use Islamic Finance.

Community opinions are the best universal driver of use • People place highest value the opinions of family, friends and colleagues when deciding whether to use

Islamic Finance (64%). This is consistent across levels of use, interest, and age.

Accessibility of information, other people not using it and use of the term ‘interest’ are the biggest barriers to use • 15% -17% reported that one of these featured in the top 3 reasons that would dissuade them from using

Islamic Finance.

Cost compared to conventional finance is an important factor • 16% reported cost to be amongst their 3 top reasons that would both dissuade (if the cost was high) and

encourage them (if the cost was low) to use Islamic Finance.

Use

USE40%

12

Key takeaway: There is an opportunity to increase uptake, and a strategy addressing both barriers and drivers is vital.

Experience of Islamic Finance exceeds expectations• 85% of Islamic Finance users said it exceeded theirexpectations. This was especially true for 35 to 44year-olds (93%).

Ideal advocates of Islamic Finance are aged 35-44• 46% of Islamic Finance users would highlyrecommend it to others.

• 35-44 year olds are most likely to recommend itwith 62% highly recommending it.

Strong opportunity to mobilise community advocates• The Islamic Finance Industry has a good NetPromoter Score (+18) but this could be improvedconsidering the extent to which this industry isdriven by a strong sense of community.

EXPERIENCE

Experience andAdvocacy

85%

13

Key takeaway: When people actually use Islamic Finance it exceeds their expectations. The Islamic Finance Industry should use consumer advocates to promote it.

The Islamic Finance category may boost positive perceptions of the finance industry as a whole.Islamic Finance users tend to view wider financial services more generally in a more positive light than non-users.

There is high emotional importance placed on financialproducts and services aligning with values and ethics.Muslims polled extremely highly that they would like their financial services to align with their values and ethics. This builds on previous findings that religion is a strong determinant of identity for Muslims in the UK.

Although perceptions are mixed, when people douse Islamic Finance, they are pleased.Those who use Islamic Finance products have a high opinion of it, thinking of it as having good customer service, reasonable costs and being beneficial to the community. They are highly likely to recommend it. Their experience of it is better than they expect.

Notable findings

14

Islamic Finance is a community movement, and it needs to be grown as such.Islamic Finance is a growing social movement within the Muslim community, with green shoots waiting to be nurtured. Other people’s opinions are most influential in making decisions about whether to purchase Islamic Finance products; people are affected by how many of their peers use it, and how highly the industry is regarded by their peers. Users of Islamic Finance feel that it serves the needs of the community, that it is innovative and does good.

The UK Muslim Consumer and Islamic Finance15

2.8mMuslims in the UK

Sources: The Muslim Pound, Muslim Council of Britain 2013, ONS census 2011

The UK Muslim consumer is young, urban and wields significant spending power

76% of Muslims live in Greater London, the West Midlands, the North West and Yorkshire and Humberside. Muslims make up 12.4% of London’s population

Muslims in the UK are much younger than the average

person, and have larger than average household sizes

16

UK Muslims make a contribution of £31bn to the UK economy, with a

spending power of £20.5bn

n = 1000Q. How important is it to you that the finance products you purchase fit with the values and ethics of your life? (94%)

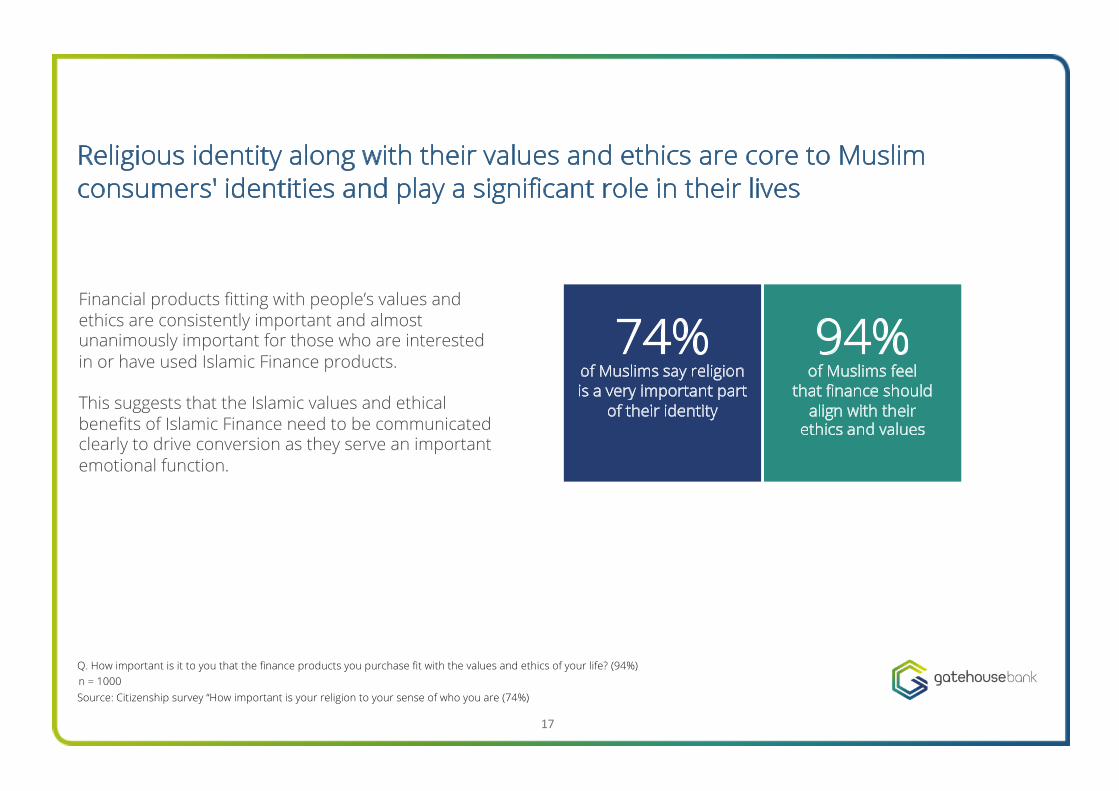

Financial products fitting with people’s values and ethics are consistently important and almost unanimously important for those who are interested in or have used Islamic Finance products.

This suggests that the Islamic values and ethical benefits of Islamic Finance need to be communicated clearly to drive conversion as they serve an important emotional function.

Religious identity along with their values and ethics are core to Muslim consumers' identities and play a significant role in their lives

74%of Muslims say religion is a very important part

of their identity

94%of Muslims feel

that finance should align with their

ethics and values

Source: Citizenship survey “How important is your religion to your sense of who you are (74%)

17

Muslim Consumer Profile: Existing Islamic Finance User

97%

68% 85%

Awareness Perception Experience(% who know a lot

or a bit about Islamic Finance)

(% who have a very favourable view of

Islamic Finance)

(% of Islamic Finance consumers who said it exceeded their

expectations)

Good quality customer service (19%*)KEY DRIVER

KEY BARRIER High costs and mention of interest (17%*)

*% of people who selected as one of their top 3 reasonsn = 543

45% 35%

40% 14% 46%Currently use

Islamic FinanceHave used Islamic Finance in the past

Have never used Islamic Finance

Age: 18-24

25-34

35-44

45+

24%

41%

56%

15%

18

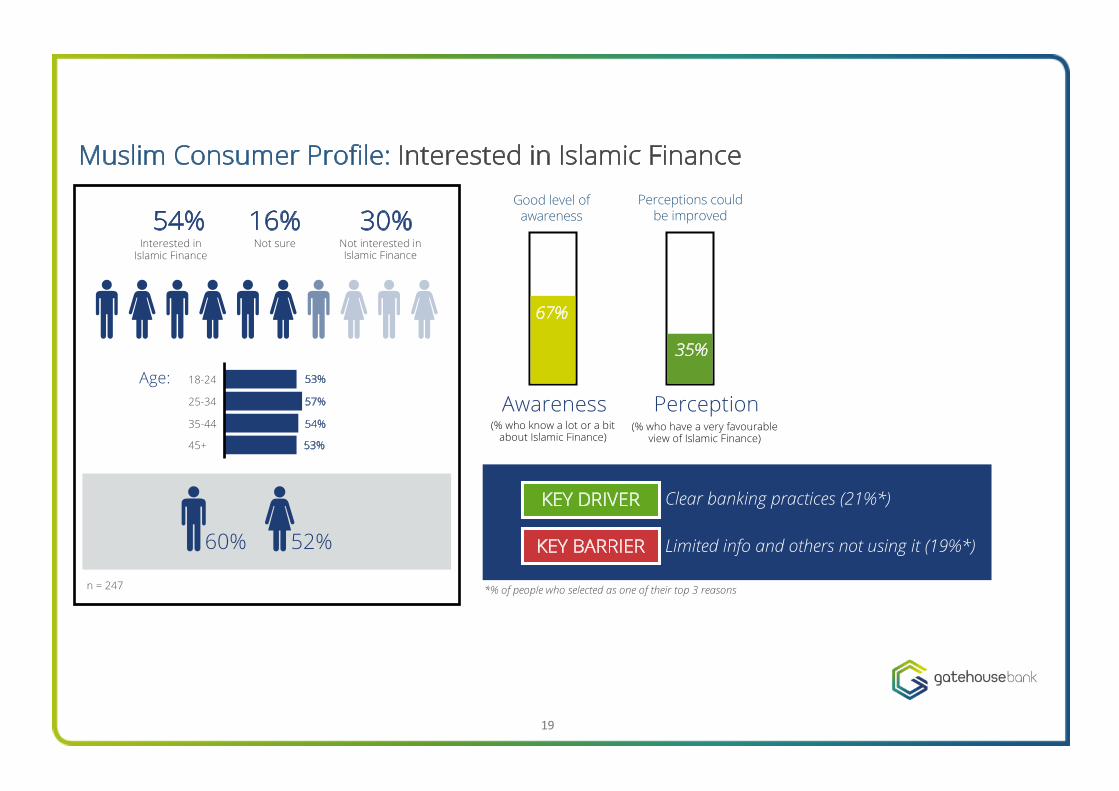

Very high level of awareness

Good perceptions

Very positive customer experience

67%

35%

Awareness Perception(% who know a lot or a bit

about Islamic Finance)(% who have a very favourable

view of Islamic Finance)

Clear banking practices (21%*)

Limited info and others not using it (19%*)

*% of people who selected as one of their top 3 reasonsn = 247

60% 52%

54% 16% 30%Interested in

Islamic FinanceNot sure Not interested in

Islamic Finance

Age: 18-24

25-34

35-44

45+

53%

57%

54%

53%

Muslim Consumer Profile: Interested in Islamic Finance

KEY DRIVER

KEY BARRIER

19

Good level of awareness

Perceptions could be improved

36% 3%

Awareness Perception(% who know a lot or a bit about

Islamic Finance)(% who have a very favourable view

of Islamic Finance)

Nothing would encourage them (28%*)

Others they know not using it (34%*)

*% of people who selected as one of their top 3 reasonsn = 133

29% 30%

Age: 18-24

25-34

35-44

45+

31%

25%

31%

29%

Muslim Consumer Profile: Not currently interested in Islamic Finance

KEY DRIVER

KEY BARRIER

20

54% 16% 30%Interested in

Islamic FinanceNot sure Not interested in

Islamic Finance

Low level of awareness

Perceptions need to be improved

Mapping the Consumer Journey21

In this section we explore the journey that the Muslim consumer undertakes from learning of Islamic Finance and their perceptions of the industry to what products are relevant for them and how they purchase those products. Ultimately, for those who do become consumers, we

look at what experience they have of using Islamic Finance.

AWARENESS PERCEPTION USE EXPERIENCE

Mapping the consumer journey

22

AWARENESS

23

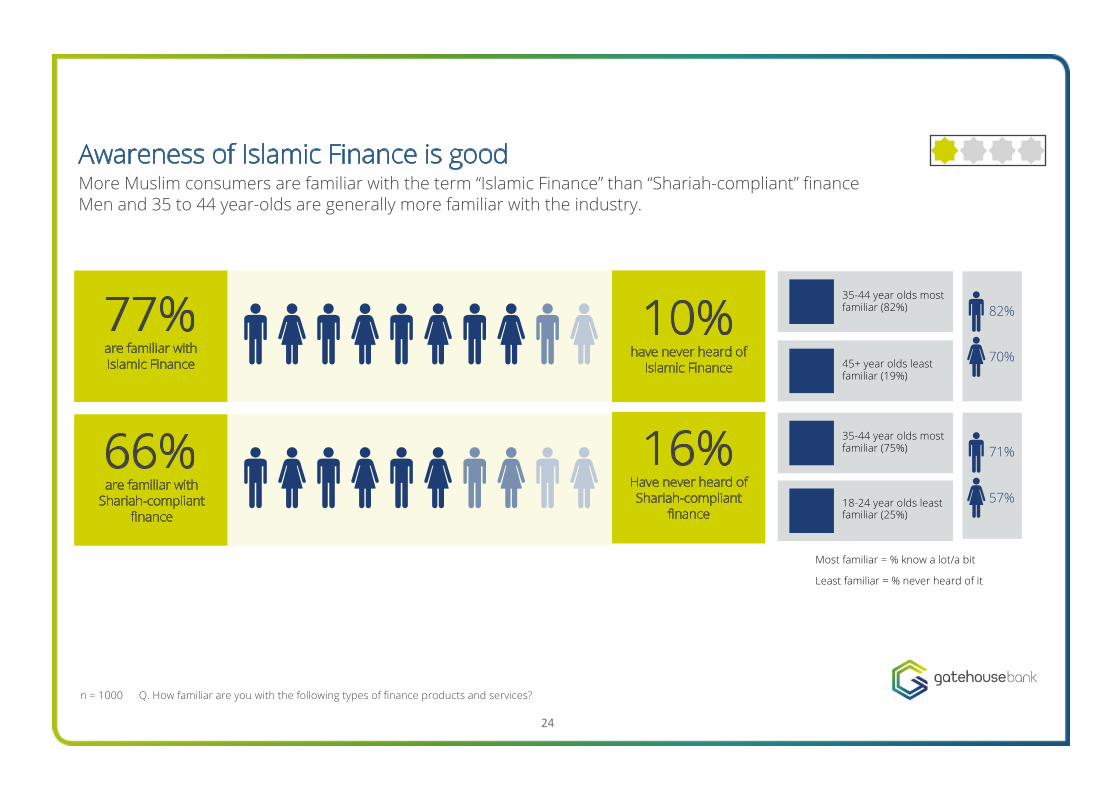

45+ year olds least familiar (19%)

35-44 year olds mostfamiliar (82%)

n = 1000 Q. How familiar are you with the following types of finance products and services?

Awareness of Islamic Finance is good

Most familiar = % know a lot/a bit

Least familiar = % never heard of it

82%

70%

More Muslim consumers are familiar with the term “Islamic Finance” than “Shariah-compliant” financeMen and 35 to 44 year-olds are generally more familiar with the industry.

77%are familiar with Islamic Finance

66%are familiar with

Shariah-compliant finance

10%have never heard of

Islamic Finance

16%Have never heard of Shariah-compliant

finance

71%

57%18-24 year olds leastfamiliar (25%)

35-44 year olds mostfamiliar (75%)

24

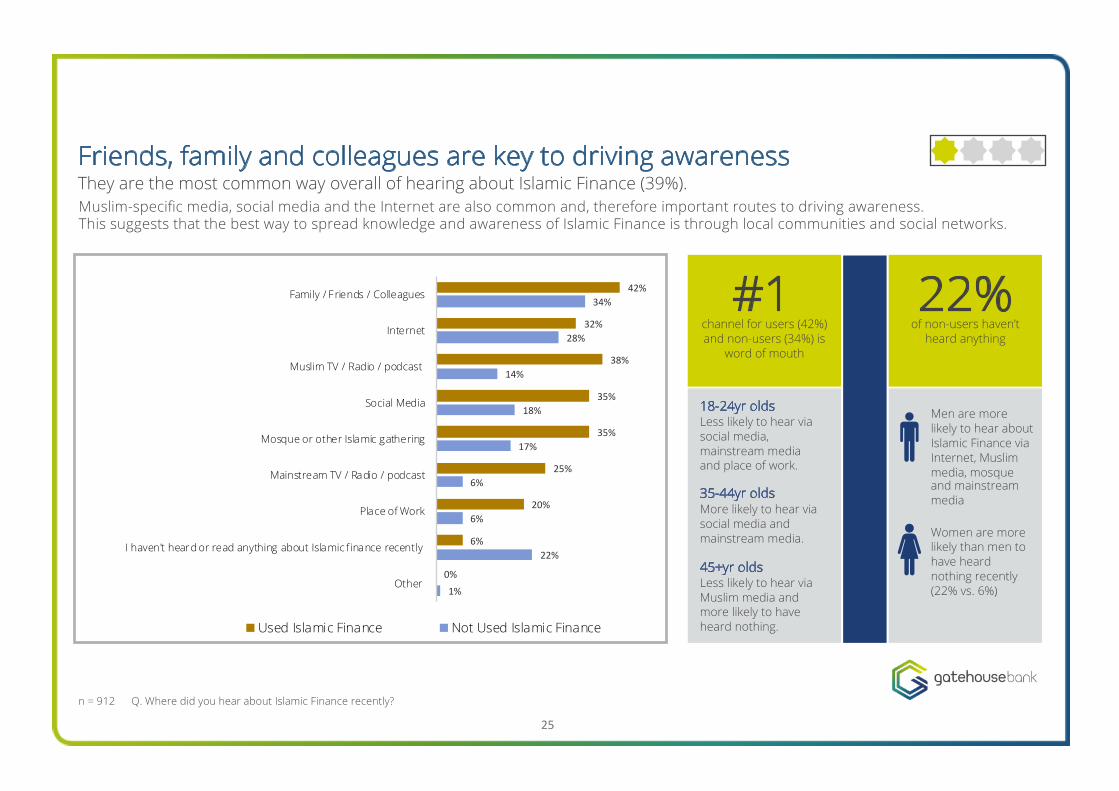

Friends, family and colleagues are key to driving awareness They are the most common way overall of hearing about Islamic Finance (39%).

n = 912 Q. Where did you hear about Islamic Finance recently?

Muslim-specific media, social media and the Internet are also common and, therefore important routes to driving awareness. This suggests that the best way to spread knowledge and awareness of Islamic Finance is through local communities and social networks.

channel for users (42%) and non-users (34%) is

word of mouth

42%

32%

38%

35%

35%

25%

20%

6%

0%

34%

28%

14%

18%

17%

6%

6%

22%

1%

Family / F riends / Colleagues

Internet

Muslim TV / Radio / podcast

Social Media

Mosque or other Islamic gathering

Mainstream TV / Radio / podcast

Place of Work

I haven't heard or read anything about Islamic finance recently

Other

Used Islamic Finance Not Used Islamic Finance

Men are more likely to hear about Islamic Finance via Internet, Muslim media, mosqueand mainstreammedia

Women are more likely than men to have heard nothing recently (22% vs. 6%)

Less likely to hear viasocial media,mainstream mediaand place of work.

18-24yr olds

More likely to hear viasocial media andmainstream media.

35-44yr olds

Less likely to hear via Muslim media andmore likely to have heard nothing.

45+yr olds

#1 22%of non-users haven’t

heard anything

25

PERCEPTIONS

26

Islamic Finance is viewed more favourably than the wider finance industry in general

n = 1000 Q. What is your view of the financial services industry? Q. What is your view of Islamic Finance?

41%

28%

21%

7%

3%

46%

29%

6%3%

17%

Veryfavourable

Somewhatfavourable

Neutral Somewhatunfavourable

Veryunfavourable

Financial service industry Islamic finance

of IF users have a very favourable view of Islamic

Finance

This is particularly the case among Islamic Finance users (68% vs 59% very favourable).People have strong feelings about Islamic Finance.

People are also less likely to have neutral views about Islamic Finance than finance generally and more likely to have very unfavourable views towards Islamic Finance than the whole financial services industry.

This might be fuelled by a lack of consistent knowledge and awareness.

68%

21%of non-IF users

have a very favourable view of

Islamic Finance

27

Perceptions of financial services industry vs. Islamic Finance

n (used) = 543n (not used) = 457 Q3. What is your view of the financial services industry?

Experience with Islamic Finance is associated with a more positive perception of financial services generallyIslamic Finance consumers view the whole financial services industry more favourably compared to non-Islamic Finance consumers (85% of Islamic Finance users had a favourable view vs. 50% amongst non-Islamic Finance users).

This suggests that those who use Islamic Finance also have improved perceptions of financial services more generally.

59%

26%

10%

3% 2%

19%

31%34%

12%

4%

Very favourable Somewhatfavourable

Neutral Somewhatunfavourable

Very unfavourable

Used Islamic Finance Not used Islamic Finance

What is your view of the financial services industry?

28

People believe Islamic Finance has a strong sense of community and is customer centricHowever, they have concerns over accessibility and the extent to which it is truly Islamic.

n = 1000 Q. How well do these describe your view of the Islamic Finance industry?

% Agree

71%

68%

68%

67%

66%

56%

55%

It’s dedicated to the interests of the communities it serves

Islamic banks aren’t very accessible compared to conventional banks

It works hard to improve its business and better serveits customers

It’s an innovator in the banking industry

I’m not sure how Islamic or Shariah-compliant providers really are

It’s banking practices are unclear and not very transparent

It’s only suitable for Muslim consumers

% Agree

positives

negatives

Perceptions of Islamic Finance having a strong sense of community are high among all those questioned, suggesting that this is a powerful universal driver of conversion. Notions of Islamic Financebeing customer centric are highestamong those who have used it (84%)

Those who are interested in using Islamic finance also have a high opinion of this(70%), suggesting that this is a key benefit that should be communicated to others.

Scepticism about how Islamic the products truly are is most prominent in those who are not interested in Islamic Finance (61%).This suggests more work needs to be done to increase the clarity and transparency of Islamic Financeproducts/services.

Interested

Not Interested

IF users

29

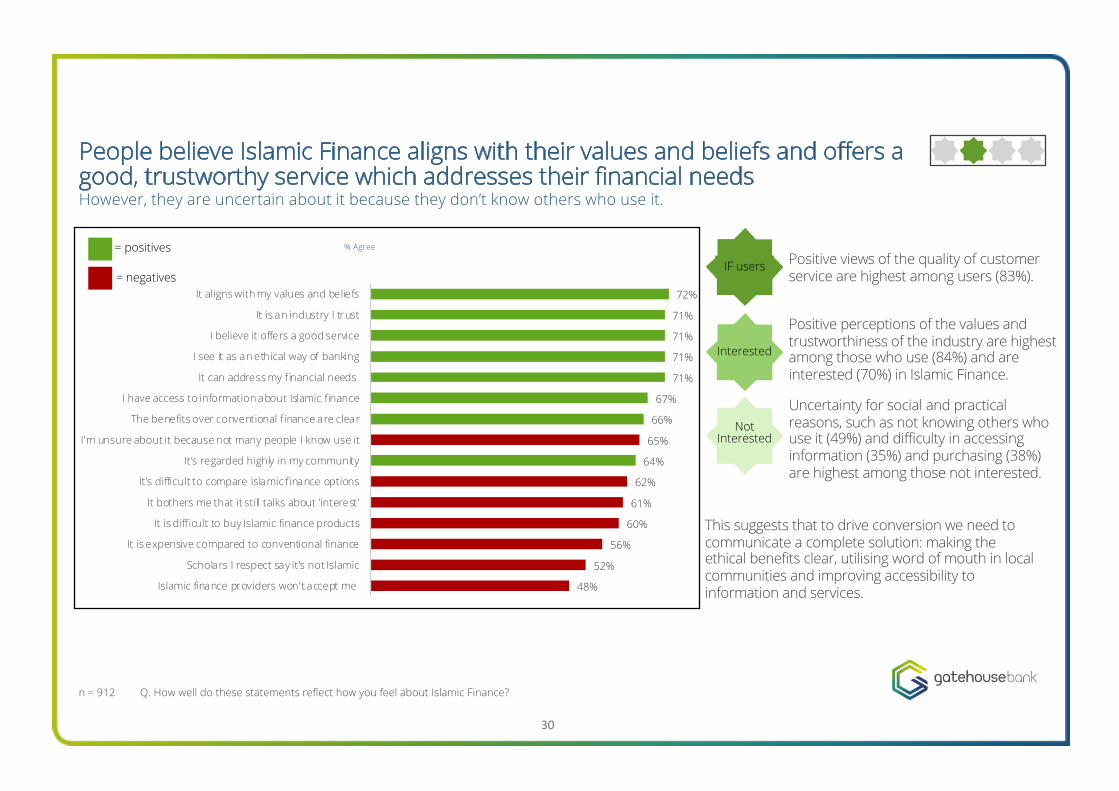

People believe Islamic Finance aligns with their values and beliefs and offers a good, trustworthy service which addresses their financial needs However, they are uncertain about it because they don’t know others who use it.

n = 912 Q. How well do these statements reflect how you feel about Islamic Finance?

Positive views of the quality of customer service are highest among users (83%).

Positive perceptions of the values and trustworthiness of the industry are highest among those who use (84%) and are interested (70%) in Islamic Finance.

Uncertainty for social and practical reasons, such as not knowing others who use it (49%) and difficulty in accessing information (35%) and purchasing (38%) are highest among those not interested.

This suggests that to drive conversion we need to communicate a complete solution: making the ethical benefits clear, utilising word of mouth in local communities and improving accessibility to information and services.

= positives

= negatives72%

71%

71%

71%

71%

67%

66%

65%

64%

62%

61%

60%

56%

52%

48%

It aligns with my values and beliefs

It is an industry I trust

I believe it offers a good service

I see it as an ethical way of banking

It can address my financial needs

I have access to information about Islamic finance

The benefits over conventional finance are clear

I'm unsure about it because not many people I know use it

It's regarded highly in my community

It's difficult to compare Islamic finance options

It bothers me that it still talks about 'interest'

It is difficult to buy Islamic finance products

It is expensive compared to conventional finance

Scholars I respect say it's not Islamic

Islamic finance providers won't accept me

IF users

Interested

Not Interested

% Agree

30

USE

31

n = 1000n = 543

Q. Have you ever used Islamic Finance products?Q. You’ve indicated that you use the following products.Please indicate if any of these products were provided by an Islamic/Shariah-compliant finance provider.

40% of Muslim consumers currently use Islamic Finance46% have never used Islamic Finance

40% 14% 46%Currently use

Islamic FinanceHave used Islamic Finance in the past

Have never used Islamic Finance

32

n = 543 Q. You’ve indicated that you use the following products.Please indicate if any of these products were provided by an Islamic/Shariah-compliant finance provider.

57%

36%

29%

15%

11%

9%

9%

8%

7%

6%

6%

5%

5%

4%

4%

1%

Current accounts

Savings accounts

Credit cards

Mortgages/HPPs

Investment services

Financial planning

Buy-to-let

Personal loans

Int'l money transfer

Home equity loans

Wills & tax affairs

Certificates of deposit

Children's savings

Wakala deposits

None

Student finance

Current accounts, savings accounts and credit cards are the most popular Islamic Finance products

33

n = 1000 Q. Have you ever used Islamic Finance products?

35 to 44 year-olds are most likely to use Islamic Finance45+ years old are least likely to have used Islamic FinanceMen are more likely to use or have used Islamic Finance than women

24%

41%

56%

15%

22%

17%

9%

9%

55%

42%

35%

76%

18-24

25-34

35-44

45+

Yes, I use Islamic finance products currentlyYes, I have used Islamic finance products in the pastNo, I have never used I slamic finance products

45%Currently use

39%Have never used

35%Currently use

53%Have never used

34

Online is the most popular channel for buying Islamic Finance

n = 543n = 227

Q. You previously indicated you have taken out an Islamic Finance product. How did you arrange this?Q. You previously indicated that you might consider buying an Islamic Finance product. How would you be most likely to arrange this?

53%

43%

40%

35%

1%

62%

57%

19%

8%

0%

Online

Via a branch

Online via a third party website such as a comparisonwebsite)

Via a broker

Other

Previously used Islamic Finance Consider using Islamic Finance

Those considering Islamic Finance say they are more likely to use online or purchase via a branch and less likely to use a third-party website or a broker than those who have previously used it. This suggests a shift in the way people want to acquire Islamic Finance products and services.

35

n = 457n = 791

Q. You’ve indicated that you have never used Islamic Finance products.To what extent would you be interested in these types of products in the future?Q. In the future, how likely would you be to consider the following products if they were provided by an Islamic Finance provider.

Similar across ages

54% are interested in using Islamic FinanceThe majority of potential consumers are interested in current and savings accounts, credit cards and insurance.

The products people aware of Islamic Finance are interested in are:Current accounts (96%), savings accounts (86%), credit cards (72%), insurance (70%), children’s savings (70%), international money transfers (68%), personal loans (68%), Mortgages/HPPs (68%), wills and tax affairs (67%), Investment services (67%), Financial Planning (66%), certificates of deposit (62%), home equity loans (62%), buy to let (62%).

60% interested

52% interested

54% 16% 30%Interested in

Islamic FinanceNot sure Not interested in

Islamic Finance

36

Trust is the main driver to using Islamic Finance, whilst accessibility of information is the main barrier

n = 1000

Other factors that influenced purchase revealed smaller differences, suggesting they were considered nearly equally as drivers (D) and barriers (B).These factors were: opinions of scholars (D = 9%; B = 11%) , ease/difficulty of comparing options (D = 12%; B = 10%), likelihood of being accepted (D = 11%; B = 10%), opinion of the community (D = 11%; B = 10%), clarity of the benefits over conventional finance (D = 12%; B = 13%), alignment with values and beliefs (D = 12%; B = 10%), ease/difficulty of purchasing Islamic Finance products (D = 12%; B = 10%), accessibility compared to conventional banks (D = 13%; B = 15%) and clarity of banking practices (D = 12%; B = 13%).

Q. Which of the following are most likely to encourage you to use or consider Islamic Finance?Q. Which of the following are most likely to dissuade you from using or considering Islamic Finance?

Trust, good quality customer service, Shariah-compliance and addressing financial needs are the main drivers towards Islamic Finance.

Limited information, other people not using it and mentions of ‘interest’ are the biggest barriers to use.

Costs compared to conventional finance arealso an important factor. Low costs drive use, whilst high costs are a key barrier.

These findings suggest more work needs to be done to increase accessibility and clarity of information on Islamic Finance. Work also needs also to be done to drive its presence in local communities by ensuring people know others who use the services.

18%

18%

14%

14%

12%

11%

11%

9%

12%

9%

9%

15%

16%

17%

Trust of the industry

Quality of customer service

Extent to which Islamic / Shariah-compliant

Extent to which it addresses financial needs

Mention/no mention of "interest"

Other people you know using / not using it

Accessibility of information

High cost was a strong barrier (16%) Low cost was a strong driver (16%)% of people who selected statement as one of their top 3 barriers and drivers to use

37

Current consumers are motivated by service, but dissuaded by high costsIslamic Finance consumers are most motivated by a good competitive service but would be most dissuaded by high costs and mentions of interest.

n = 543 Q. Which of the following are most likely to encourage you to use or consider Islamic Finance?Q. Which of the following are most likely to dissuade you from using or considering Islamic Finance?

Islamic FinanceConsumers

17%Trust of the

industry

16%Good costs

19%Good quality

customer service

16%Limited

information

17%High costs

and mention of interest

15%Poor

customer service

% = % of people who selected as one of their top 3 reasons

KEY DRIVER KEY BARRIER

38

Interested consumers are motivated by clear practices, but dissuaded by limited informationInterested consumers are most motivated by clear banking practices and would be most dissuaded by limited information and others they know not using it.

n = 248 Q. Which of the following are most likely to encourage you to use or consider Islamic Finance?Q. Which of the following are most likely to dissuade you from using or considering Islamic Finance?

21%Clear banking

practices

20%Trust of the

industry

18%Good

customerservice

19%Limited

informationand others not using it

16%Mentions of

'interest'

17%High costs

and low accessibility

% = % of people who selected as one of their top 3 reasons

KEY DRIVER KEY BARRIER

39

Interested Consumers

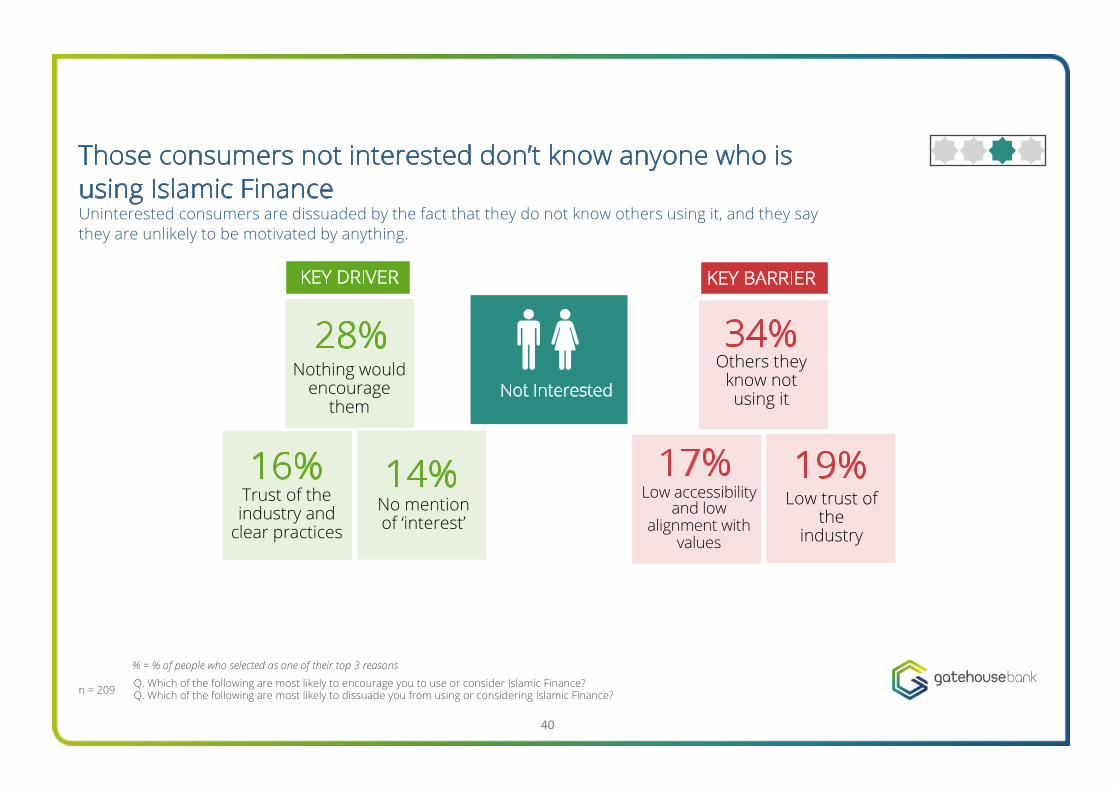

Those consumers not interested don’t know anyone who is using Islamic FinanceUninterested consumers are dissuaded by the fact that they do not know others using it, and they say they are unlikely to be motivated by anything.

n = 209 Q. Which of the following are most likely to encourage you to use or consider Islamic Finance?Q. Which of the following are most likely to dissuade you from using or considering Islamic Finance?

Not Interested

28%Nothing would

encourage them

16%Trust of the industry and

clear practices

14%No mention of ‘interest’

34%Others they

know not using it

17%Low accessibility

and low alignment with

values

19%Low trust of

the industry

% = % of people who selected as one of their top 3 reasons

KEY DRIVER KEY BARRIER

40

Current and interested consumers are focused on practical concerns such as customer service andcosts.

Non-users are focused on social factors such as whether others they know anyone who uses Islamic Finance.

Limited information is the biggest barrier for those who are interested.

Conversion is driven by community engagementThe biggest opportunity to drive conversion is to build a stronger Islamic Finance community to share information, and to promote its customer service, trustworthiness and attractive costs

n = 1000 Q. Which of the following are most likely to encourage you to use or consider Islamic Finance?Q. Which of the following are most likely to dissuade you from using or considering Islamic Finance?

Not Interested

Interested Consumers

Islamic FinanceConsumers

Low trust and lack of alignment with values and beliefs are key barriers to

those who aren’t interested; which may make

this group difficult to convert.

Key drivers: Good customer service

TrustworthinessGood costs

Clear banking practice is the biggest driver for interested

consumers.

Limited information is the biggest barrier.

This suggests more clarity and transparency of services is key

to converting this group.

Key barriers for those who don’t currently use Islamic Finance:Not knowing people who use Islamic Finance

Low accessibility of services Work needs to be done to spread word of mouth

in communities and to make more accessible.

These positive elements of the service should be communicated

to those who are interested.

41

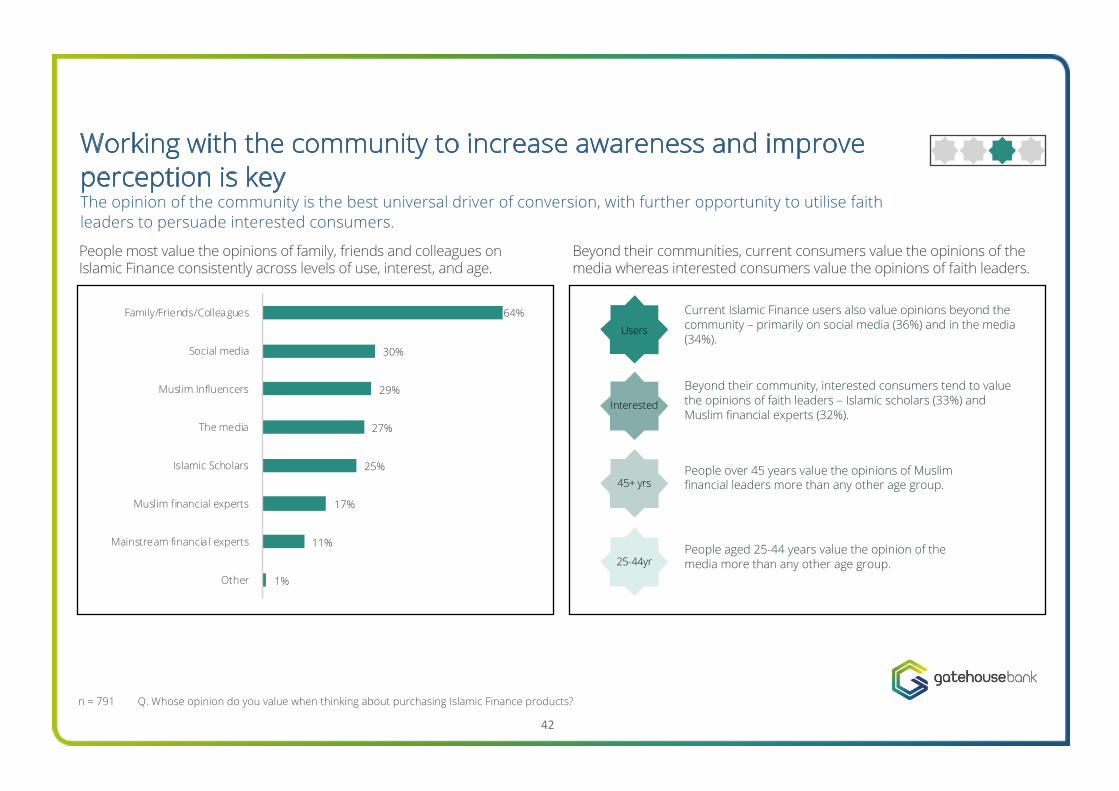

People most value the opinions of family, friends and colleagues on Islamic Finance consistently across levels of use, interest, and age.

n = 791 Q. Whose opinion do you value when thinking about purchasing Islamic Finance products?

64%

30%

29%

27%

25%

17%

11%

1%

Family/Friends/Colleagues

Social media

Muslim Influencers

The media

Islamic Scholars

Muslim financial experts

Mainstream financial experts

Other

Current Islamic Finance users also value opinions beyond the community – primarily on social media (36%) and in the media (34%).

Beyond their communities, current consumers value the opinions of the media whereas interested consumers value the opinions of faith leaders.

Beyond their community, interested consumers tend to value the opinions of faith leaders – Islamic scholars (33%) and Muslim financial experts (32%).

People over 45 years value the opinions of Muslim financial leaders more than any other age group.

People aged 25-44 years value the opinion of the media more than any other age group.

Users

Interested

45+ yrs

25-44yr

Working with the community to increase awareness and improve perception is key The opinion of the community is the best universal driver of conversion, with further opportunity to utilise faith leaders to persuade interested consumers.

42

EXPERIENCE AND

ADVOCACY

43

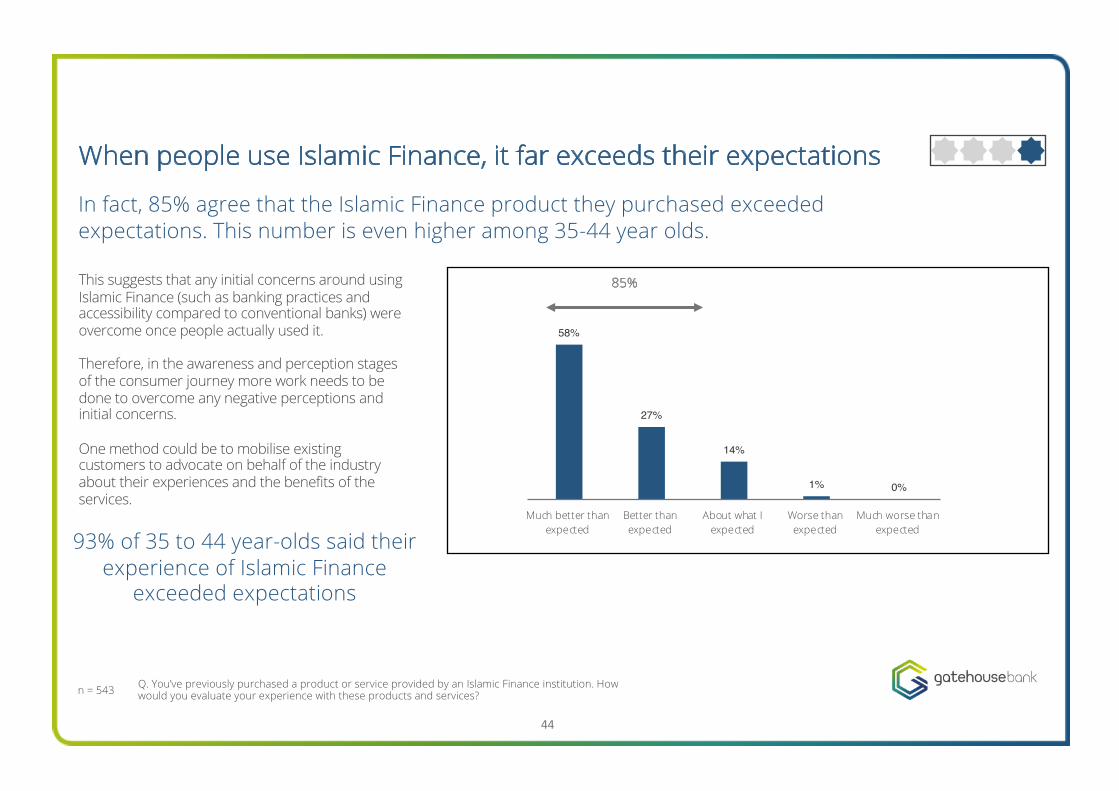

58%

27%

14%

1% 0%

Much better thanexpected

Better thanexpected

About what Iexpected

Worse thanexpected

Much worse thanexpected

When people use Islamic Finance, it far exceeds their expectations

n = 543 Q. You’ve previously purchased a product or service provided by an Islamic Finance institution. Howwould you evaluate your experience with these products and services?

In fact, 85% agree that the Islamic Finance product they purchased exceeded expectations. This number is even higher among 35-44 year olds.

85%This suggests that any initial concerns around using Islamic Finance (such as banking practices and accessibility compared to conventional banks) were overcome once people actually used it.

Therefore, in the awareness and perception stages of the consumer journey more work needs to be done to overcome any negative perceptions and initial concerns.

One method could be to mobilise existing customers to advocate on behalf of the industry about their experiences and the benefits of the services.

44

93% of 35 to 44 year-olds said their experience of Islamic Finance

exceeded expectations

46% of Islamic Finance users would highly recommend it to others

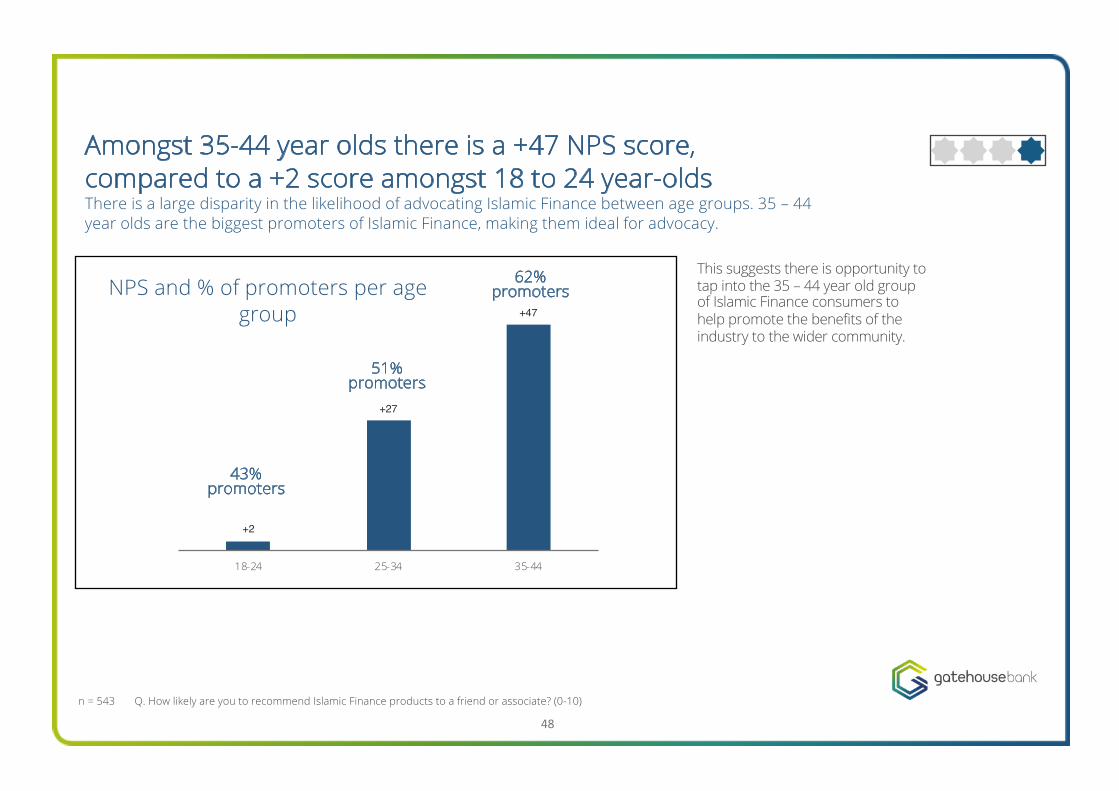

n = 543 Q. How likely are you to recommend Islamic Finance products to a friend or associate? (0-10)

Detractors Passive Promoters

28% 26% 46%Unlikely to

recommend(0-6)

Neutral about recommending

(7-8)

Highly likely to recommend

(9-10)

45

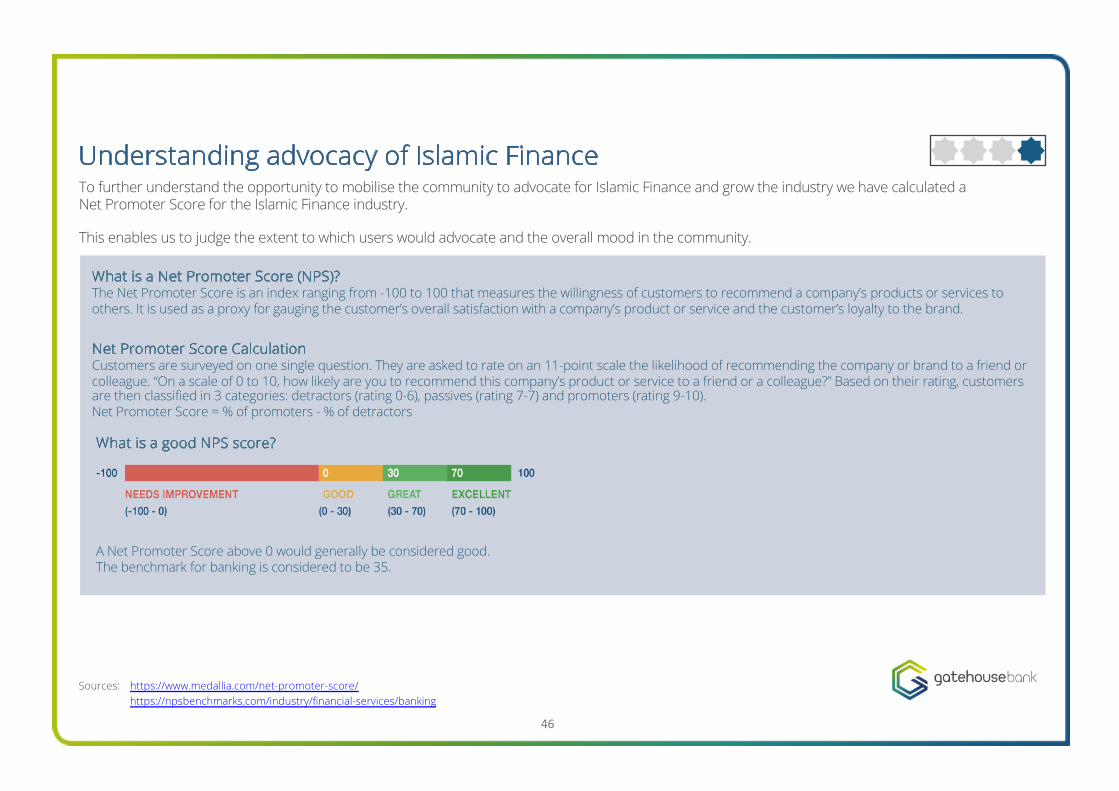

Understanding advocacy of Islamic FinanceTo further understand the opportunity to mobilise the community to advocate for Islamic Finance and grow the industry we have calculated a Net Promoter Score for the Islamic Finance industry.

This enables us to judge the extent to which users would advocate and the overall mood in the community.

https://www.medallia.com/net-promoter-score/Sources:https://npsbenchmarks.com/industry/financial-services/banking

What is a Net Promoter Score (NPS)?The Net Promoter Score is an index ranging from -100 to 100 that measures the willingness of customers to recommend a company’s products or services to others. It is used as a proxy for gauging the customer’s overall satisfaction with a company’s product or service and the customer’s loyalty to the brand.

Net Promoter Score CalculationCustomers are surveyed on one single question. They are asked to rate on an 11-point scale the likelihood of recommending the company or brand to a friend or colleague. “On a scale of 0 to 10, how likely are you to recommend this company’s product or service to a friend or a colleague?” Based on their rating, customers are then classified in 3 categories: detractors (rating 0-6), passives (rating 7-7) and promoters (rating 9-10).Net Promoter Score = % of promoters - % of detractors

A Net Promoter Score above 0 would generally be considered good. The benchmark for banking is considered to be 35.

What is a good NPS score?

46

The overall net promoter score for Islamic Finance is +18Although the Net Promoter Score falls in the ‘good’ range, it is at the lower end of the scale and could be improved. This is particularly important given how highly both users and non-users value the opinions of their peers and the regard in which others do or don’t hold the industry, and the importance of community.

n = 543 Q. How likely are you to recommend Islamic Finance products to a friend or associate? (0-10)

Net Promoter Score

This suggests there is much more to do to engage the community and that there is an opportunity for the community to mobilise its community advocates.

Detractors Passive Promoters

28% 26%

+18Unlikely to

recommend(0-6)

Neutral about recommending

(7-8)

Highly likely to recommend

(9-10)

47

46%

Q. How likely are you to recommend Islamic Finance products to a friend or associate? (0-10)n = 543

+2

+27

+47

18-24 25-34 35-44

NPS and % of promoters per age group

43% promoters

51% promoters

62% promoters

This suggests there is opportunity to tap into the 35 – 44 year old group of Islamic Finance consumers to help promote the benefits of the industry to the wider community.

Amongst 35-44 year olds there is a +47 NPS score, compared to a +2 score amongst 18 to 24 year-olds There is a large disparity in the likelihood of advocating Islamic Finance between age groups. 35 – 44 year olds are the biggest promoters of Islamic Finance, making them ideal for advocacy.

48

Looking Ahead: Conclusions and Recommendations

49

Snapshot: Islamic Finance Health Indicator

77%

46% 40%

85%

Good level of awareness

Perceptions could be improved

Users cite a very positive customer experience

Opportunity to increase use

Awareness Perception Use Experience% who know a lot or a bit

about Islamic Finance% who have a very favourable

view of Islamic Finance% who currently use

Islamic Finance% of Islamic Finance consumers who said it exceeded their expectations

n = 1000

Snapshot:The 2019 health indicator suggests that the biggest opportunity ahead of the Islamic Finance industry is to increase positive perceptions of the industry within the UK Muslim community in order to drive use of Islamic Finance products and services. Within this there are specific roles for increasing awareness among key segments, crafting a strategy built on the key drivers and barriers to uptake, and mobilisingcommunity advocates.

50

Communicate a complete solution

UK Muslim consumers are motivated by both emotional and rational factors when it comes to Islamic Finance, suggesting we need to communicate a complete solution to their needs.

The strong majority of UK Muslims feel that finance should align with their ethics and values which suggests that clearly communicating the ethical benefits of Islamic Finance is key.

However, consumers also want a good quality service which competes with conventional finance on customer service, costs, and accessibility. This suggests that these benefits need to be equally apparent to encourage interested consumers and grow the industry.

A community movement

The power of the community’s opinions towards Islamic Finance is the most significant factor in building on the momentum that already exists.

With UK Muslims valuing the opinions of their friends, family and colleagues the most when it comes to making decisions about Islamic Finance, driving word of mouth in local communities is key to growing the industry.

To boost perceptions of the industry we need to mobilise our community advocates, primarily 35 to 44 year-old Islamic Financeconsumers, with further opportunities to utilise faith leaders (Islamic scholars and Muslim financial experts) to convert interested consumers.

Increase clarity and understanding

Work needs to be done to increase the clarity and understanding of Islamic Finance products and services.

There is currently a high level of scepticism about how Islamic the products truly are. This is further fuelled by a lack of clear and accessible information about what providers offer and confusion over banking practices.

Looking ahead: Recommendations for the industry

51

Awareness, perception and uptake were particularly low among 18 to 24 year-olds. This is a key growing demographic, and early engagement is important.

The industry should think about how to build relationships in this early stage.

Women also show lower awareness and engagement with Islamic Finance. More investigation is required into why this might be the case, and whether it fits into similar, wider financial consumer trends. This could be a particularly rich area of investigation.

Increase awareness and knowledge

Looking ahead: More work to be done

Our research suggests that mobilising our community advocates to boost perceptions of the industry by advocating its ethical and practical benefits is key.

However, more work needs to be done to determine the most effective message and channel to reach our potential consumers.

Further investigation is also required to assess levels of awareness and knowledge around Islamic Finance.

Effective messaging

Our research suggests that awareness and use of Islamic Finance vary quite considerably across age groups, with 35 to 44 year-olds being considerably more likely to both know about and use it than any other age group.

Further research should be conducted to uncover the reasons behind differences in awareness and opinions amongst age groups to help tailor effective messaging.

Understanding perceptions across age

52

Appendix1. Survey methodology and sample2. About Gatehouse Bank3. Partners and acknowledgements

53

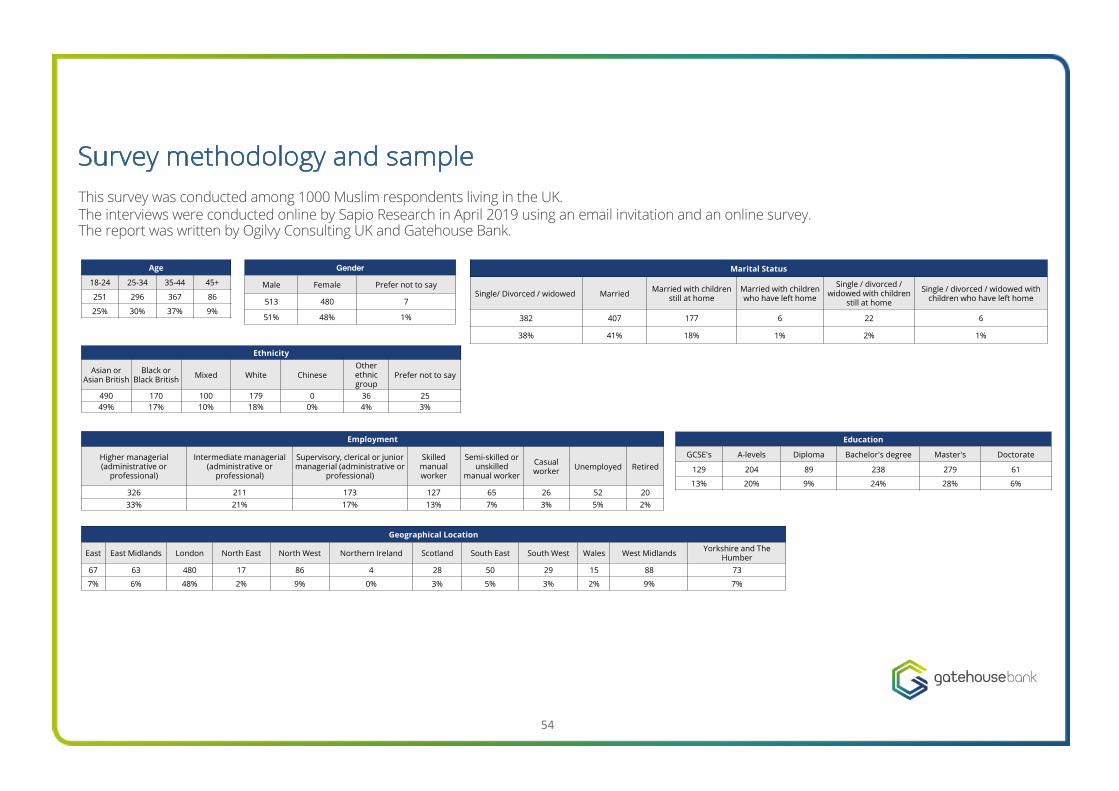

Survey methodology and sampleThis survey was conducted among 1000 Muslim respondents living in the UK.The interviews were conducted online by Sapio Research in April 2019 using an email invitation and an online survey.The report was written by Ogilvy Consulting UK and Gatehouse Bank.

Marital Status

Single/ Divorced / widowed Married Married with children still at home

Married with children who have left home

Single / divorced / widowed with children

still at home

Single / divorced / widowed with children who have left home

382 407 177 6 22 6

38% 41% 18% 1% 2% 1%

Ethnicity

Asian or Asian British

Black or Black British Mixed White Chinese

Other ethnic group

Prefer not to say

490 170 100 179 0 36 2549% 17% 10% 18% 0% 4% 3%

Gender

Male Female Prefer not to say

513 480 7

51% 48% 1%

Age

18-24 25-34 35-44 45+

251 296 367 86

25% 30% 37% 9%

Employment

Higher managerial (administrative or

professional)

Intermediate managerial (administrative or

professional)

Supervisory, clerical or junior managerial (administrative or

professional)

Skilled manual worker

Semi-skilled or unskilled

manual worker

Casual worker Unemployed Retired

326 211 173 127 65 26 52 2033% 21% 17% 13% 7% 3% 5% 2%

Education

GCSE's A-levels Diploma Bachelor's degree Master's Doctorate

129 204 89 238 279 61

13% 20% 9% 24% 28% 6%

Geographical Location

East East Midlands London North East North West Northern Ireland Scotland South East South West Wales West Midlands Yorkshire and The Humber

67 63 480 17 86 4 28 50 29 15 88 73

7% 6% 48% 2% 9% 0% 3% 5% 3% 2% 9% 7%

54

Gatehouse Bank plc is a Shariah-compliant bank based in London and is a subsidiary of Gatehouse Financial Group Limited.

It is authorised by the Prudential Regulation Authority (PRA) and regulated by the Prudential Regulation Authority and the Financial Conduct Authority (FCA).

Founded in 2007, Gatehouse Bank supports savvy savers looking for a better return, aspiring homeowners and businesses driving for growth. We offer a genuine alternative to conventional banks, with products that are transparent, fair and socially responsible.

About Gatehouse Bank

55

Fair. Transparent. Socially responsible.

Try banking a different way.

ResponsibleWe believe in a transparent, fair and socially responsible system of finance, based on Shariah principles. Through the sharing of both risk and reward in an equitable way, we offer an alternative, balanced approach to banking for our customers.

OpenWe encourage an open and transparent dialogue with our customers and colleagues, welcoming different ideas and perspectives. We recognise the value of listening and the progress that comes from freedom of thought and permission to fail.

Can-doWe embrace opportunity and are resourceful in the face of challenge. By looking beyond accepted conventions, being willing to adapt, and always working as a team, we move forward where others stand still. Our attitude is refreshingly can-do.

Our Values

This report was made possible through our partners at Ogilvy Consulting, led by Shelina Janmohamed, Vice President of Islamic Marketing at Ogilvy UK, in partnership with their Behavioural Science Practice and the market research partner Sapio Research.

Built within the worldwide Ogilvy network, Ogilvy Consulting is a strategy and innovation consulting group that brings the deep analytical rigour and business focus of the management consultancies together with the brand, customer and creative focus of a world-leading creative agency.

Acknowledgements

SHELINA JANMOHAMEDVice President, Islamic Marketing

MADELEINE CROUCHERSenior Consultant, Behavioural Science

WILLIAM FERNANDEZConsultant, Behavioural Science

CHLOE HUTCHINGS HAYAnalyst, Behavioural Science

OgilvyConsulting

56

Thank youFor any questions please contact:

Andy Homer, Director of Communications, Gatehouse [email protected]

Rachael Snelling,Head of External Communications, Gatehouse [email protected]

57

58