the future of tax incentives in a changing … · incentive (no apas) o tax incentives aimed at...

TRANSCRIPT

THE FUTURE OF TAX INCENTIVES IN A CHANGING

POLITICAL AND ECONOMIC LANDSCAPE

Moderators: Lionel Nobre, Dell Computadores do Brasil Ltda., Rio Grande do Sul, Brazil Elinore J. Richardson, EMKDM Global Consultants Inc., Toronto, Canada Speakers: Sylvia Dikmans, Houthoff Buruma, Amsterdam,The Netherlands Andres Fuentes, Banamex-Citigroup, Mexico City, Mexico Randall Madriz, Pacheco Coto, San Jose, Costa Rica Javier Robalino, Ferrere, Quito, Ecuador Fernando Tonanni, Machado Meyer Advogados, Sao Paulo, Brazil 1

OVERVIEW

2

3

Overview

‘Tax incentive’ means any special tax provision granted by a country to qualified investment projects or firms that provides a favorable deviation from the general tax code

“Striking the right balance between an attractive tax regime for domestic and foreign investment, by using tax incentives and securing the necessary revenues for public spending, is a key policy dilemma.” (IMF, OECD, UN and World Bank, 2011)

Overview

4

Figure 2. Relative Importance of Tax Incentive Packages in Investor Location Survey 2010

(Left: Relative Rank; Right: Change in Rank since 2007) 0 1 2 3 4

-0.3

0.0 0.3

Economic stability 3.82 Political stability

Political stability 3.81 Local markets

Costs of raw materials 3.65 Availability of skilled labour

Local markets 3.63 Economic stability

Transparency of legal framework 3.51 Quality of life

Availability of skilled labour Transparency of legal framework 3.50

Labour costs Availability of local suppliers

3.46

0.06 Bilateral agreements and treaties Quality of life 3.32

0.00 Export market Availability of local suppliers 3.22

-0.01 Labour costs Bilateral agreements and treaties 3.05

-0.22 Costs of raw materials Incentives package 3.05

-0.26 Incentives package Export market 2.94

Source: UNIDO (2011)

0.28

0.24

0.15 0.12 0.10 0.09

0.31

Overview

Tax incentives have been used to pursue a variety of objectives The primary motivation is usually to stimulate investment and

attract foreign direct investment (FDI) FDI inflows are believed to not only bring capital and (high-wage)

jobs to a country, but also to spur competition and increase the efficiency of domestic markets more widely, thus contributing to a country’s overall economic development

Empirical growth regressions generally find positive correlations between inward FDI and economic growth, although conclusions about causality remain contentious

Tax incentive policies also often aim to promote specific economic sectors or types of activities as part of an industrial development

strategy or to address regional development needs 5

Overview

6

Figure 1. Prevalence of Income Tax Incentives around the World /1

/1 Figure shows the percent of countries in each of four income groups that have the indicated incentive. The sample size per income group is denoted between brackets. Source: Calculations based on James (2014)

Overview

Effectiveness varies between countries and sectors o In some countries, tax incentives seem to have played an important role in

attracting new investment and spurring economic growth, i.e. Korea and Singapore, where tax incentives—offered as part of a broader strategy to attract investment—seem to have encouraged rapid industrialization

o However, in many instances tax incentives have resulted in little or no new investment, For instance, FDI that is resource-seeking (to exploit the presence of natural resources), market-seeking (to penetrate a local market) or strategic asset-seeking (to exploit local know-how or technology) is generally found to be less responsive to tax than FDI that is efficiency- seeking (to exploit cost advantages in production for the world market)

o Tax incentives tend to have the greatest salience where investment is oriented toward exporting firms China is often quoted as an example of effective (tax) incentive policies. During its transition period between the mid-1980s and mid-2000s, it experimented with a wide range of industrial policy instruments, including tax incentives for special economic zones, reduced tax rates for FDI, and tax holidays for strategic industries. FDI inflows accelerated during this period and the country became a top destination for many multinationals. In a panel of 29 regions between 1985 to 1995, Chen and Kwan (2000) find, for instance, that special economic zones systematically boosted FDI inflows.

7

The effectiveness of incentives in attracting investment also depends on the international tax rules in place

Multinationals taxed on a “territorial” basis in their home country are able to retain the benefits of host country tax incentives, since there is no offsetting home country tax on the foreign source income

Multinationals might be subject to home country tax on foreign source income due to controlled foreign corporation (CFC) rules or tax upon repatriation under a ‘world- wide’ system—as used in e.g. the US, China and India

The tax incentive can then become ineffective, since the benefit will be taken away by increased tax payments in the multinational’s home country—although tax deferral until repatriation of income may where applicable effectively mitigate this result

Overview

8

Targets For Incentives

9

10

Brazil

Tax incentives in Brazil need to be approved by law and are granted on general basis to all taxpayers eligible for the incentive (no APAs)

o Tax incentives aimed at attracting FDI/portfolio investments o Shares, treasury bonds, infrastructure bonds and investment funds

o Tax incentives on exports o CAPEX Investment (PIS and COFINS suspension – converted into

0% rate) o Export revenues (PIS and COFINS immunity) o Cross-border export finance (0% WHT rate on interest) o Presumed credits on gross revenues derived from the export of

goods

11

Brazil

o Regional tax incentives o SUDAM – Amazon (75% corporate income tax reduction) o SUDENE – Northeaster States (75% corporate income tax

reduction)

o R&D o Corporate income tax, WHT and IPI reliefs

o Specific industries o Infrastructure (PIS/COFINS), semiconductor and digital

transmission (Corporate Income Tax, PIS/COFINS, IPI, Import Duty and CIDE), computer and IT (IPI), O&G (PIS/COFINS, IPI, Import Duty and State VAT), investment in port facilities (PIS/COFINS, IPI, Import Duty), automobile (IPI), etc.

Costa Rica

Costa Rica has focused on encouraging activities

within the free zone regime system and in tourism

12

Ecuador

The Organic Code of Production, Commerce and Investment (COPCI) enacted on December 29th, 2010 introduces general and specific incentives for local and foreign investments purposes, including tax reforms and new regulations on custom law

13

Biotechnology and applied

software

Logistics Services and foreign trade

Petrochemical Tourism

Production of fresh, frozen and

industrialized foodstuff

Forestry and agro forestry chain, and is manufactures

products

Sectors for strategic

substitution of imports (*)

Renewable energy, including

bio energy or energy bio mass

Metal Mechanical

PRIORITY ECONOMIC SECTORS

(*) SECTORS OF STRATEGIC SUBSTITUTION OF IMPORTS

Leather and shoes

Clothing products

Chemistry products

Ceramic products

Basic Chemistry substances

Radio. TVs and mobile devices

Domestic appliances

Detergents soaps, perfumes,

and bathroom products

Pesticides and agribusiness

products

10 year exemption from corporate income tax

Reimbursement of VAT paid in purchases destined to the PPP

Exemption from the 5% ORT related to foreign credit operations

Exemption from customs duties on imports directly related to the

PPP

Tax regimen stability during the term of the PPP

Income tax exemption for profits obtained from financial products

such as “commercial paper” of 360 days or more

Special Incentives for PPP Ventures

14

Mexico

At the Federal level there no specific tax incentives for foreign investment in Mexico and limited benefits for investors in general

Mexican incentives are aimed at

o IT - lump-sum depreciation on new fixed assets for 2016 and 2017, which is creditable for VAT purposes

o IT and VAT benefits for taxpayers that carry out innovative, technologic and scientific developments or activities pertaining to the agriculture industry in the “Special Economic Zones” in areas of poverty that are not developed

o Other limited benefits for the food and mining industries for VAT, IT and excise tax purposes

15

Mexico At the local level, there are no specific benefits for foreign

investment Subsidies are limited and differ in each State State incentives include

o Tax on ownership of cars o For new cars or cars that have a low value for taxpayers that were compliant in previous

years or for non-profit organizations

o Property tax o When the tax is paid annually in advance in one installment

o Wages tax o Where new jobs are created, for employment of elder workers, persons who are

employed for the first time, and of workers with disabilities; when tax is paid on a timely basis or is paid in one installment

o Capital gains tax from the sale of immovable property o Other incentives may be negotiated with the States such as for donation of

land

16

The Netherlands

Tax incentives specifically targeted at o R&D

o Innovation box o Additional deductions

o Maritime sector o Tonnage regime for shipping

o Environment o Accelerated depreciation o Additional deductions

17

Tax Holidays/ Tax Exemptions

18

19

Tax Holidays/ Tax Exemptions

Targeted to attract foreign investments in Brazilian Finance and Capital Markets

o Tax Exemptions o Gains arising from the sale of shares or other securities

within the Brazilian stock market o Real Estate Secured Bills (LIG) o Investment funds held by non-residents, the portfolio of

which is comprised exclusively of cash or assets that are exempt or subject to a zero tax rate

o Other tax exemptions only for foreign individuals (e.g. Real Estate Receivables Certificates – CRI)

20

Tax Holidays/ Tax Exemptions

Withholding tax exemptions applicable to

foreign investors on o Federal Government Bonds o Private equity funds o Infrastructure Private Equity Investment Funds o Infrastructure Receivables Investment Funds o Development and Innovation Investment Funds o Investment funds held only by non-residents, holding at least

98% federal government bonds o Infrastructure bonds or securities, publicly traded, issued by

private entities (non financial institutions)

Tax Holidays/ Tax Exemptions

Costa Rica does not grant tax holidays except through Free Zone status

Tax Exempted

o Cooperatives o Solidarity associations

Tax Exemptions

o Inheritances o Donations

21

Tax Holidays/ Tax Exemptions

Capital Gains are exempt unless

o Assets subject to depreciation o For – profit activity

Not subject to taxation due to a Territorial System

o Is income derived from

o Assets located o Services rendered o Capital invested

22

Costa Rica

Tax Exemptions under the Green House Gases

Compensation System

o For income derived from GHGCS o From real estate tax for land parcels involved in GHGCS

23

Sales Tax Exemption for supplies of

o Agricultural items o Medicines o Educational materials

24

Tax Holidays/ Tax Exemptions

The Netherlands does not grant tax holidays Tax Exemptions include

o Participation exemption on qualifying subsidiaries o Purports to avoid double taxation o Applies to subsidiaries that are not qualified as a low taxed portfolio investment o Subsidiaries benefitting from a tax holiday or tax exemption can qualify

o Exempt investment fund / fiscal investment fund o Pooling investors should not result in additional taxation - income taxed in hands

of investors

o Exemption from withholding tax on distributions to qualifying investors o Avoidance of double taxation

o 30% of the salary of employees recruited from outside the Netherlands may be paid tax exempt to cover relocation expenses

Tax Holidays/ Tax Exemptions

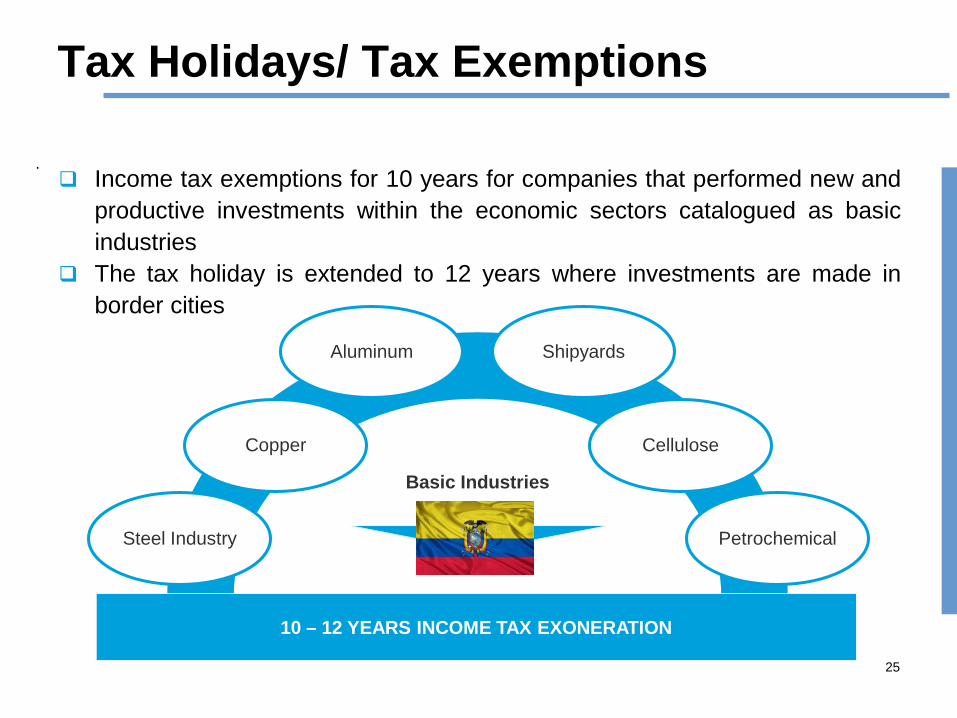

Income tax exemptions for 10 years for companies that performed new and productive investments within the economic sectors catalogued as basic industries

The tax holiday is extended to 12 years where investments are made in border cities

25

.

Basic Industries

Steel Industry

Copper

Aluminum

Petrochemical

Cellulose

Shipyards

10 – 12 YEARS INCOME TAX EXONERATION

Tax Holidays/ Tax Exemptions

100% ADDITIONAL DEPRECIATION ON NEW PRODUCTIVE ASSETS

Companies that acquire “new productive assets” can claim 100% additional depreciation as a deductible expense for income tax purposes

ANTICIPATED INCOME TAX PAYMENT EXONERATION

Companies with core business related with software development, with one year term development time

Companies with core business related with projects in agribusiness (agro-forestry and forestry)

26

Tax Holidays/ Tax Exemptions Companies set up after the inception of the COPCI as well as companies

already incorporated with the purpose of making new and productive investments will have a five year income tax holiday counted from the date when a new income is made on income that is solely and directly related to the new investment

Companies must be domiciled outside urban jurisdictions of Quito or Guayaquil

Only for investments within the Priority Economic Sector and/or Import Substitution Sectors

Exemption for 5 years from the Anticipated Income Tax Payment, only for new incorporated companies

The Anticipated Income Tax Payment will not apply to new investments that companies make that are intended to increase direct employment, raise salaries, asset acquisitions and incentive more productivity and innovation

Exemption from the Overseas Remittance Tax (ORT) of 5% on payments abroad for operations with external financing

27

Reduced Tax Rates

28

29

Reduced Tax Rates

Income Tax (applicable to Brazilian entities)

o Tax incentives for underdeveloped regions o SUDAM – Amazon (75% corporate income tax reduction) o SUDENE – Northeastern States (75% corporate income tax

reduction) o Tax incentive for IT activities: PADIS (0% corporate income tax

rate on the revenue derived from the sale of qualifying manufactured products - semiconductors)

30

Reduced Tax Rates

Other Taxes (applicable to Brazilian entities) o Selected sectors

o REIDI (infrastructure sectors), PADIS and PATVD (semiconductor and digital transmission industries), PPB (computer and IT), O&G tax incentives, REPORTO (investment in port facilities)

o Tax Incentives on Exports o REPES (software and IT services supply), RECAP

(CAPEX), REINTEGRA, export revenues and export finance

No Advanced Tax Ruling/ Advance Pricing Agreement are available in Brazil

31

Reduced Tax Rates

Netherlands grants Advance Tax Ruling / Advance Pricing Agreement (“ATR”/”APA”) to confirm tax position of taxpayer o Provided in line with the law o Not possible to agree to a reduced rate

A reduced rate of 20% applies to profits up to EUR 200,000

Dutch Tonnage tax regime for shipping o Taxable profit determined on basis of tonnage of vessels

Reduced Tax Rates

A progressive reduction of 3% points of Corporate Income Tax

(CIT), from 25% in 2010 to 22% in 2013 and for fiscal years ending before 2017

Benefits for companies opening their social capital for the benefit of their workers

Companies that reinvest their its annual profits will have a 10% reduction on the 22% CIT rate if the reinvestment is destined for the acquisition of new machinery and equipment

Additional Deductions for income tax purposes in certain circumstances

Payments facilities to custom taxes

32

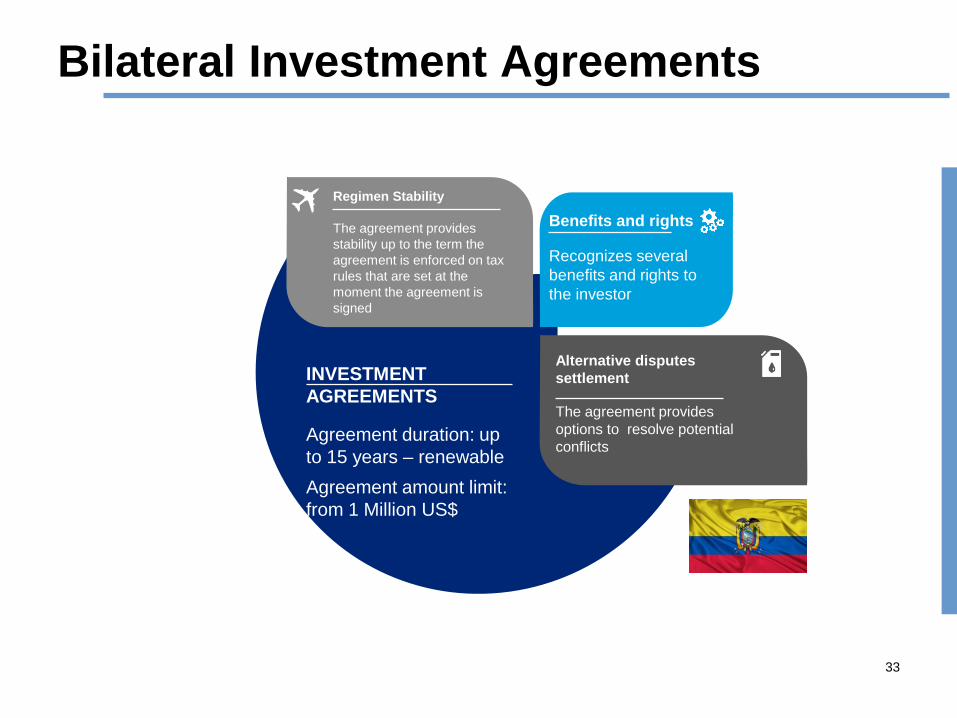

Bilateral Investment Agreements

33

INVESTMENT AGREEMENTS

Agreement duration: up to 15 years – renewable Agreement amount limit: from 1 Million US$

Regimen Stability

The agreement provides stability up to the term the agreement is enforced on tax rules that are set at the moment the agreement is signed

Benefits and rights

Recognizes several benefits and rights to the investor

Alternative disputes settlement

The agreement provides options to resolve potential conflicts

Reduced Tax Rates Investment Funds

o Money Market Funds o Subject to 5% corporate income tax o Distribution of benefits not subject to taxation even if the investors are

located abroad Costa Rica o Distributions of benefits could be subject to 15% withholding taxes but

the rule is unclear o Real Estate Funds and Real Estate Development Funds

o Regular income subject to 5% income tax on gross income o Capital gains are subject to 5% income tax o Distributions of benefits are not subject to taxation even if the investors

are located abroad

No Advanced Tax Rulings/ Advance Pricing Agreements are available in Costa Rica

34

Reduced Tax Rates

Special regulations prescribed income tax rates for small

businesses whose gross income does not exceed certain benchmarks

o 10% for companies with gross income up to US$96,000 approximately o 20% for companies with gross between US$96,000 and US$194,000

approximately

35

Reduced Tax Rates

Entities dealing exclusively in agricultural, livestock breeding, forestry or fishing activities (primary activities) are exempt from income tax when their gross revenues do not exceed 20 times the annual minimum wage for the geographic area in which the taxpayer is located for each partner and the aggregate does not exceed 200 times the annual minimum wage corresponding to the Mexico City area

Additionally, when the income exceeds the above threshold but does not exceed 423 times the annual minimum wage for the geographic area in which the taxpayer is located, a tax credit of 30% is granted to the tax payable as calculated in accordance with the corresponding articles

When the taxpayer’s income exceeds the mentioned limit, the tax payable is the standard corporate tax rate of 30%

Local tax on royalties ranges from 15% to 34% Depreciation allowances range from 5% to 25%, but can be up to 50% on pollution-

control equipment The value-added tax (VAT) rate is 16% throughout the country (a lower border rate

has been eliminated); food products and medicines remain exempt from VAT Additional changes to various tax regimes, which affect conglomerates and maquila

(domestic assembly for re-export) firms have also come into effect

36

Investment Allowances/ Tax Credits

37

38

Investment Allowances/ Tax Credits

Brazilian Equity investment allowances o Interest on Net Equity (IOE)

o Hybrid form of capital remuneration o 34% deduction and WHT at a 15% rate o Trend to restrict IOE tax benefit by eliminating the

possibility to pay IOE o Goodwill tax amortization in M&A transactions

between non-related parties Brazilian debt investment allowances

o Withholding tax exemption on interest payable on cross-border export finance

39

Investment Allowances/ Tax Credits

Other taxes o REINTEGRA – 3% tax credit calculated on the gross

revenues derived from the export of goods o Tax credits also granted as investment allowances at

the state level

40

Investment Allowances/ Tax Credits

Dutch national law includes tax measures as incentives for R&D

Tax Sparing Provisions in Double Tax Treaties o Brazil – NL: tax sparing credit for dividends, interest & royalties

o Limited or absent taxation in the Netherlands on royalties and interest

o Dividends (i) exempt under participation exemption or (ii) application of tax sparing credit

41

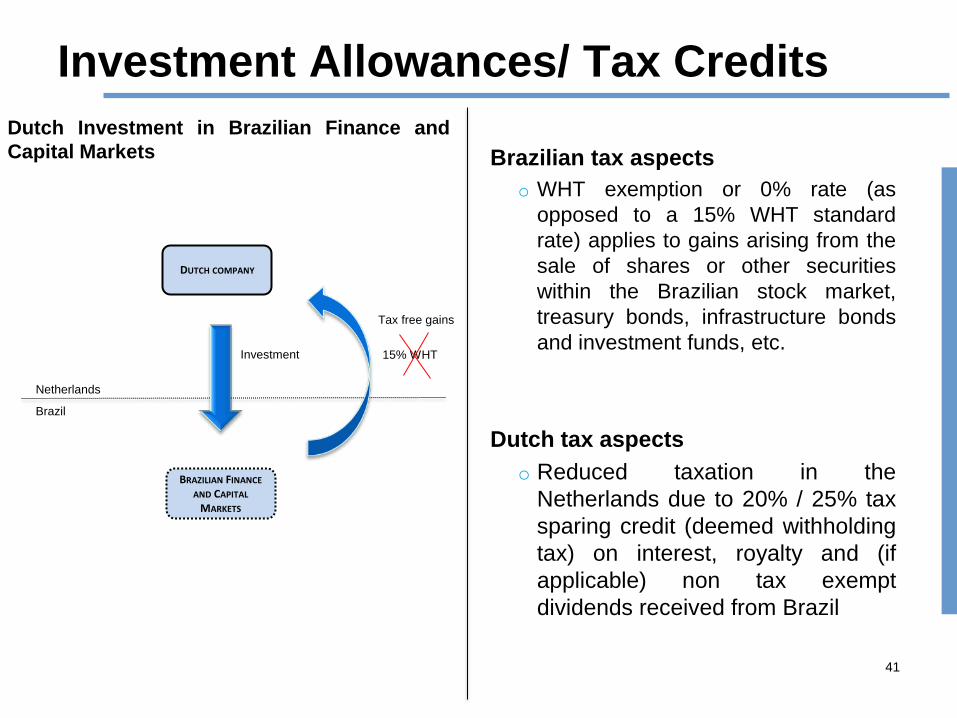

Investment Allowances/ Tax Credits

DUTCH COMPANY

Netherlands

Brazil

Tax free gains

15% WHT

Dutch Investment in Brazilian Finance and Capital Markets

BRAZILIAN FINANCE AND CAPITAL

MARKETS

Investment

Brazilian tax aspects o WHT exemption or 0% rate (as

opposed to a 15% WHT standard rate) applies to gains arising from the sale of shares or other securities within the Brazilian stock market, treasury bonds, infrastructure bonds and investment funds, etc.

Dutch tax aspects

o Reduced taxation in the Netherlands due to 20% / 25% tax sparing credit (deemed withholding tax) on interest, royalty and (if applicable) non tax exempt dividends received from Brazil

42

Investment Allowances/ Tax Credits

DUTCH COMPANY

Netherlands

Brazil

Equity/debt investment

BR ENTITY

Return on equity IOE

Interest under debt

In Brazil: 34% deduction on the payment of IOE and interest

Cross border finance and equity Investments in Brazil by Dutch entities

In Netherlands: Participation exemption /

tax sparing credits

Dutch tax aspects

o Reduced taxation in the Netherlands due to tax sparing credit for interest (20 / 25%).

o Participation exemption not applicable as IOE is deductible in Brazil. Due to tax sparing credit full / significant reduction of Dutch taxation

Brazilian tax aspects

o IOE (return on equity) – 15% WHT rate o Interest (return on debt) – 15% WHT rate o Tax deduction in both cases (34% benefit)

Investment Allowances/ Tax Credits

The tax incentives have been granted, in general terms, in the form of tax credits or deductions applicable to federal taxes; however some of the above require special authorization from the tax authorities

They include: Tax benefits for trusts engaged in the construction or acquisition of real properties (Mexican

REITs Deduction of land cost by real - estate developers Tax incentive for investment projects and distribution in domestic cinematographic and

theatre productions Incentive for venture-capital investments in Mexico Deduction of special taxes paid in the acquisition of diesel, for use in machinery different to

motor vehicles Deduction of special taxes paid in the acquisition of diesel for motor vehicles that were

intended only for public and private transport of people or goods Deduction of toll roads for those which render public and private transport of people or goods

43

Investment Allowances/ Tax Credits

Generally the application of specific allowances or subsidies has its origin in the intention of States or municipalities to attain social goals by attracting investments, or to encourage (for different reasons) growth of activities or areas in different industries

These subsidies or incentives are generally negotiated directly with the State or municipality where the investment will be made and their importance depends on the size of the investment, whether there is land purchase, number of jobs to be created over a certain timeframe and other similar factors

These may include o Discount on the purchase price of land o Reduction in state taxes (real estate acquisition tax, property tax, payroll tax) for

a determined period of time o Reimbursement of training fees

44

Investment Allowances/ Tax Credits

45

DUTCH COMPANY

Netherlands

Mexico

100% Equity investment

MEX ENTITY

Dutch tax aspects o Participation exemption on

dividends received from and capital gains realized on MEX entity are exempt from Dutch taxation

Mexican tax aspects o No withholding tax on dividends

due to tax treaty (provided the participation exemption applies in the Netherlands)

Dutch Equity Investments in Mexican entities

Investment Allowances/ Tax Credits

Special depreciation allowances o Administrative resolution 17 - 2002

o Limited to technological assets o Limited to manufacturing companies o Accelerated sum of digit method o Does not require previous approval

o Tourism Incentives Law 6990

o Limited to certain assets o Requires previous approval

Custom duties concessions o Tourism Incentives Law 6990

o Items to be incorporated in buildings and premises engaged in tourism

46

R&D Tax Incentives/ Patent Box Regimes

47

48

R&D Tax Incentives/ Patent Box Regimes

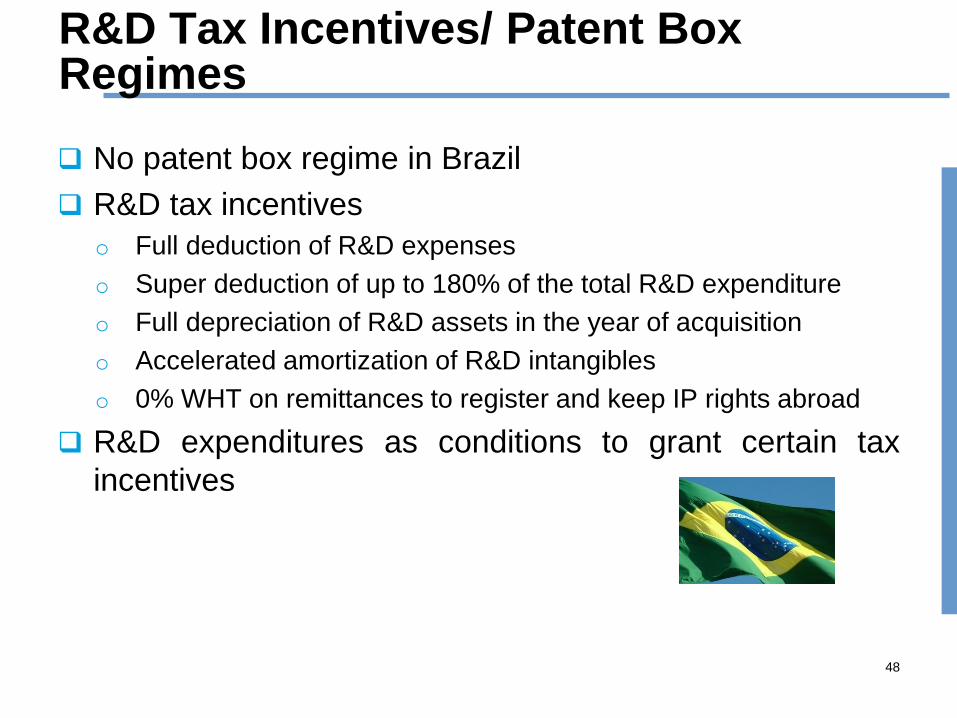

No patent box regime in Brazil R&D tax incentives

o Full deduction of R&D expenses o Super deduction of up to 180% of the total R&D expenditure o Full depreciation of R&D assets in the year of acquisition o Accelerated amortization of R&D intangibles o 0% WHT on remittances to register and keep IP rights abroad

R&D expenditures as conditions to grant certain tax incentives

49

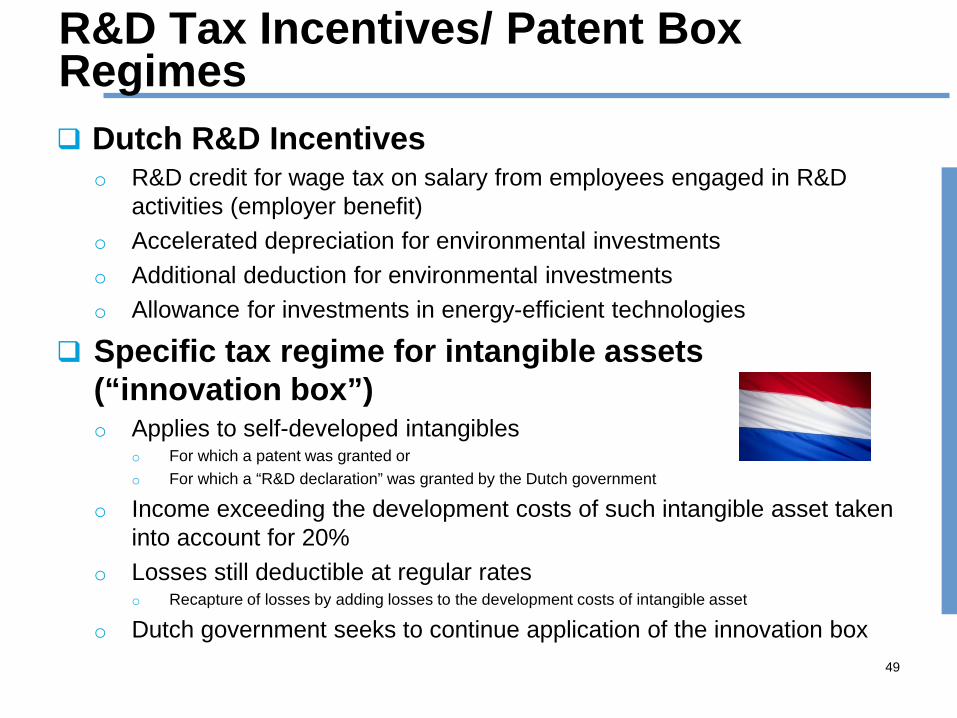

R&D Tax Incentives/ Patent Box Regimes Dutch R&D Incentives

o R&D credit for wage tax on salary from employees engaged in R&D activities (employer benefit)

o Accelerated depreciation for environmental investments o Additional deduction for environmental investments o Allowance for investments in energy-efficient technologies

Specific tax regime for intangible assets (“innovation box”) o Applies to self-developed intangibles

o For which a patent was granted or o For which a “R&D declaration” was granted by the Dutch government

o Income exceeding the development costs of such intangible asset taken into account for 20%

o Losses still deductible at regular rates o Recapture of losses by adding losses to the development costs of intangible asset

o Dutch government seeks to continue application of the innovation box

R&D Tax Incentives/ Patent Box Regimes

No R&D Tax Incentives in Costa Rica

No Patent Box Regime in Costa Rica

50

Super Deductions

51

52

Super Deductions

Super deduction of up to 180% of total R&D expenditure

(as previously mentioned)

Accelerated depreciation of fixed assets applicable to R&D activities and companies within SUDAM/SEDENE regions

53

Super Deductions

Dutch fiscal unities for VAT or CIT purposes o Full consolidation o Ignores intercompany transactions between entities o Applies to Dutch resident entities / PE’s of qualifying non-Dutch

resident entities o Legislation has been proposed to bring regime in line with recent

ECJ case law - scope will be broadened o Case law pending on non-discrimination clauses in tax treaties -

relevant for non-EU countries with Dutch resident group companies

Super Deductions

54

Technical assistance and market share/competitiveness

analysis; Technical assistance in processes’ implementation,

adaptation and design; industry-related new software

Technical coaching aimed at the investigation and

development of technology innovation

Travel expenses and commercial promotion to

access international markets, business meetings and

international conventions

Small and medium sized enterprises can claim an additional 100% deduction on expenses related with the following activities

Super Deductions

Companies that acquire merchandise, equipment and technology with environmental benefits are entitle to an additional 100% deduction on the cost of those goods

Conditions:

55

Goods acquired since the enactment of the COPCI

Goods destined to “cleaner” mechanisms of production

Goods to be used in renewable energy processes; or in reducing the environmental impact of productive activity

Super Deductions

Taxpayers may deduct twice the wages paid to employees with disabilities

56

SEZ/Free Zones/ EPZ/Freeport

57

SEZ/Free Zones/ EPZ/Freeport

Companies operating under the Free Trade Zone Regime that are located in the Great Extended Metropolitan Area (GEMA) benefit from an income tax exemption of 100% for the first eight years and of 50% for the next four years

Companies located outside the GEMA benefit from an income tax exemption of 100% for the first 12 years and of 50% for the next 6 years.

The Ministry of National Planning and Economic Policy specifies which areas are considered part of the GEMA.

On 22 January 2010, the executive branch of the Costa Rican government published Law 8794 which amends and adds certain sections to the Free Trade Zone Regime Law No. 7210

This law created a new category of companies that produce or process goods, regardless of whether the goods are for exportation, that can apply for the Free Trade Zone Regime

Companies in this category are subject to income tax at reduced rates (0%, 5%, 6% or 15%) for a specified number of years depending on whether the company is located inside or outside the GEMA or depending on the amount of the investment

58

59

SEZ/Free Zones/ EPZ/Freeport

Brazil provides for typical free zones EPZs were created but are not in force

o The model is not widely adopted in Brazil o There are 2 EPZ (Acre and Ceará) and 22 pre-operational

EPZ

Free Trade Zones Creation not directly linked with FDI and its benefits are

mainly linked to indirect taxes o Was adopted in order to enhance the less developed

regions of Brazil (Manaus Free Trade Zone - ZFM) o Allows an industrial facility located there to benefit from

SUDAM tax reduction

60

SEZ/Free Zones/ EPZ/Freeport

The Netherlands does not provide for a typical free zone Some countries that form part of the former Netherlands

Antilles do provide for such free zones o Aruba o Curacao

SEZ/Free Zones/ EPZ/Freeport

61

ZEDES

Income Tax Rate: 17%

Custom duties exemption for all goods to be entered to the ZEDES

VAT 0% rate on goods import exclusively destined to the ZEDES or for any productive process develop at the ZEDES

Tax credit for the paid VAT in purchase of raw materials and services from local market to be incorporated into productive process

ORT 5% exoneration on imports of goods and services related with the activity of the ZEDES

ORT 5% exoneration on payments abroad related with foreign credit operations

ZEDES is a custom designation in specific determined space within the national territory, for setting up new investment, that will have exclusive tax incentives.

Conclusions/ Future

62

Conclusions/ Future

Empirical evidence finds that taxes matter for investment, although most likely less so in developing countries Empirical studies on the relationship between effective tax burdens and FDI

generally conclude that host country taxation significantly affects investment Most of this evidence, however, refers to advanced economies Recent studies report similar results for developing countries, although the

effects tend to be somewhat smaller on average many developing countries do not offer attractive general investment conditions for most

multinational companies, due to for instance poor infrastructure, macroeconomic instability, unclear property rights, and weak governance or judicial systems

In these circumstances, tax incentives do not effectively counterbalance such poor conditions and are largely ineffective

At the same time, however, tax incentives might be one of the few (albeit second-best) instruments for developing countries to offset disadvantaged circumstances, address regional disparities and mitigate market failures, such as lack of financial access

63

64

Conclusions/Future - Brazil

Tax incentives targeted at foreign investors (FDI and portfolio) o The tax incentives applicable to Brazilian finance and capital markets

are viewed as an efficient mechanism with positive results in terms of investment flow

Tax incentives targeted at specific industries o Since 2011, the Brazilian Government is adopting a policy of granting

tax incentives to selected industries - apply to Brazilian based companies and are targeted mainly at VAT taxes (PIS/COFINS, IPI, ICMS)

Trends for the future o Since 2014, Brazil has been going through an economic downturn and

as a consequence, several tax incentives targeted at specific industries have been recently reduced or eliminated

65

Conclusions/Future - Brazil

o The following Brazilian tax incentives were challenged before the WTO (challenges brought by the EU and Japan, US and Argentina requested participation in the consultation phase of the WTO dispute) o INOVAR-AUTO o Tax incentives related to electronic products and related sectors (PPB, PADIS,

PATVD and PID) o ZFM and other free trade zones o Tax incentives for export (RECAP and other incentives targeted at companies

primarily exporters)

o The WTO dispute occurs in 4 phases: (i) consultations (negotiation between the parties), (ii) panel (appointment of 3 experts to judge the dispute), (iii) appellate body (hears appeals from reports issued by panels in disputes) and (iv) implementation (several procedures aiming at the enforcement of the decision upheld)

o Possible outcomes of WTO dispute o Favorable decision to Brazil and settlement of the dispute. o Partial or entire favorable decision to EU which would permit reasonable time for

the elimination or modification of the tax incentive (usually 2 years) - WTO disputes are never enforced on retroactive basis

66

Conclusions/Future – The Netherlands

The Netherlands general tax code includes various tax incentives

Specific incentives apply to most predominantly R&D and environmental investments

The Dutch government position is that the Dutch tax system is in line with recent EU and OECD developments o Only specific investigation with respect to Starbucks APA o Changes to innovation box on the basis of level paying field

Conclusions/Future – Ecuador

67

01

100% additional deduction of the cost of contracting new employees

02 All other general and

sectorial incentives

Tax incentives rules seeks to equalize territorial development, prioritizing investments in Economical Depressed Zones

Variables taken into consideration for the determination of Economically Depressed Zones: - high indexes of unsatisfied needs based on statistics available to the government

Conclusions/Future – Costa Rica

The Ministry of Finance estimates that income not received in 2015 due to the existence of exemptions and special tax regimes was equivalent to 5.8% of GDP, of which 3.68% corresponds to general sales tax, 1.82% to income tax and 0.3% for other taxes

Due to poor legislative and management procedures there exist many exemptions which benefit even specific taxpayers

Currently the Costa Rican fiscal deficit is equivalent to 5.9% of GDP In the near future it is expected that many of these tax benefits will

be removed

68

Conclusions/Future – Mexico

Mexico offers foreign investors a relatively stable and secure business environment, a large internal market and an extensive network of free-trade agreements (FTAs) with investment-protection components, factors that have put the country among the more attractive investment locations in Latin America

A number of improvements have simplified foreign investment procedures in recent years, including less red tape, higher ceilings for foreign capital, fewer local-content requirements and better intellectual-property legislation

The United States has traditionally been the leading source of foreign investment into Mexico, and since the 1994 implementation of the North American Free-Trade Agreement (NAFTA), the Mexican manufacturing sector is deeply integrated with US production and distributions systems

69

70

Thank you!

Lionel Nobre Dell Computadores do Brasil Ltda., RioGrande do Sol, Braszil Email: [email protected] Elinore J. Richardson EMKDM Global Consultants Inc., Toronto, Canada Email: [email protected] Sylvia Dikmans Houthoff Buruma, Amsterdam, The Netherlands Email: [email protected] Andres Fuentes Banamex-Citigroup, Santa Fe, Mexico City, Mexico Email: [email protected] Randall Madriz Pacheco Coto, San Jose, Costa Rica Email: [email protected] Javiere Robalino Orellano Ferrere, Quito, Ecuador Email: [email protected] Fernando Tonanni Machado Meyer Sendacz & Opice Advogados, Sao Paulo, Brazil

Email: fernando [email protected]