the future of semiconductor industry - a foundry's · pdf filethe future of semiconductor...

TRANSCRIPT

Proprietary& Confidential

© 2007 TSMC, Ltd

The Future of Semiconductor Industry– A Foundry's Perspective –

Dr. F.C. TsengVice Chairman

TSMCJanuary 24, 2008

Proprietary& Confidential

© 2007 TSMC, Ltd

2

Outline

Semiconductor Market OutlookChallenges and Solutions

EconomicTechnology

Summary

Proprietary& Confidential

© 2007 TSMC, Ltd

3

Year

-40%

-20%

0%

20%

40%

60%

Gro

wth 16% 21%

5% ~8%

‘70 ‘75 ‘80 ‘85 ‘90 ‘95 ‘00 ‘05 ‘10 ‘15

Source: SIA

Year Growth

’07 +4%

’02 +1%

’03 +18%

’04 +28%

’05 +7%

’06 +9%

’08E +7~9%

Semiconductor Market Will Continue to Grow

Proprietary& Confidential

© 2007 TSMC, Ltd

4

12.6%

28.8%

18.8%

19.5%

20.9%

13.5%

27.2%

16.4%

16.3%

‘05 ‘10E

Increasing semiconductor penetration in electronics

ConsumerElectronics

Data Processing

Communications

‘01

Source: WSTS, IC Insights, TSMC estimates

Steady Market Expansion

Year

Proprietary& Confidential

© 2007 TSMC, Ltd

5

Increasing Semiconductor Content in Systems– Functionalities and performance

$77B$95B

?

HD

LCD

FHD

LCD

u LCD

$33B

$61B

?

2.5G

3G 4G?

$98B

Com

pact

Luxury

Intelligent

1.3x 1.8x 10x

LCD MobileHeadset

Automotive

Source: Gartner, iSuppli, Strategy Analytics

$1,025B

Proprietary& Confidential

© 2007 TSMC, Ltd

6

New Applications as Growth DriversU

nits

/ En

d U

ser

Year‘70 ‘80 ‘90 ‘00 ‘10

1

100

1/100

1/10000

Minicomputer

PC

Mainframe

ConsumerElectronics

(3C Convergence)

Proprietary& Confidential

© 2007 TSMC, Ltd

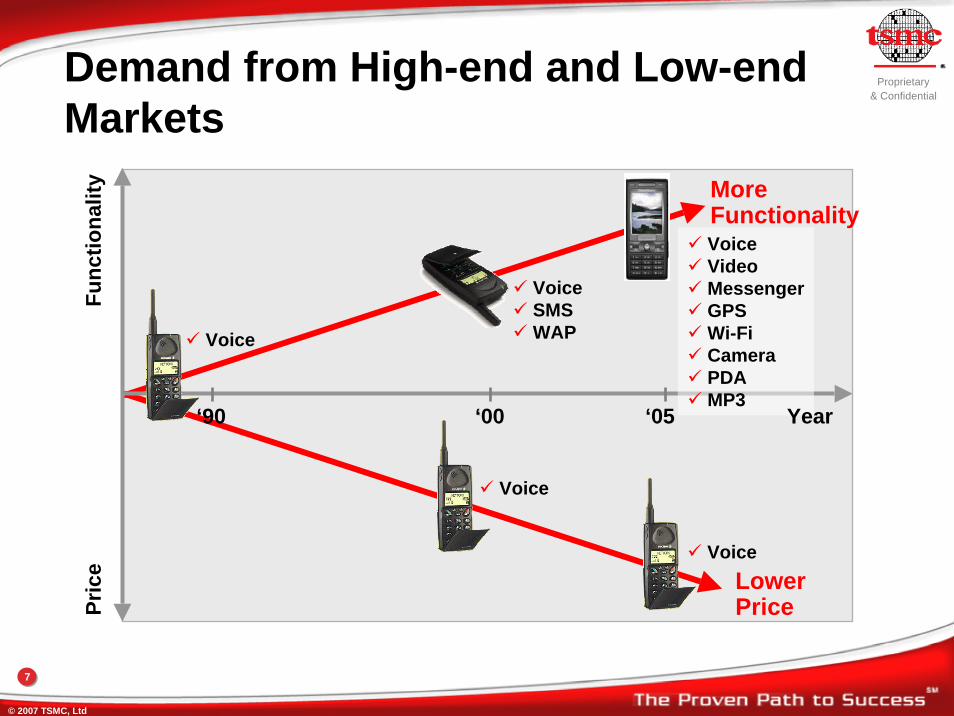

7

Func

tiona

lity

‘90 ‘‘00 ‘05

VoiceSMSWAPVoice

Pric

e

Voice

VoiceLowerPrice

Demand from High-end and Low-end Markets

VoiceVideoMessengerGPSWi-FiCameraPDAMP3

MoreFunctionality

Year

Proprietary& Confidential

© 2007 TSMC, Ltd

8

In Search of A PC to Serve “The Next Billion”

INTEL“ClassMate”

One Laptop Per Child“XO”

ASUS“Eee”

The low-cost PCs for the developing nations:

Proprietary& Confidential

© 2007 TSMC, Ltd

9

Growth Opportunities are Global

Source: “The fortune at the bottom of the pyramid” by C. K. Prahalad, and IMF

Developing(Base of the Pyramid)

Emerging

Population (millions)

800

1,500

4,000Basic functions

Feature-rich & connected

Product FocusPr

ice/ F

eatu

re/

Perfo

rman

ce

Spec

trum

Advanced

Proprietary& Confidential

© 2007 TSMC, Ltd

10

-5

5

15

25

35

45

55

65

Plenty of Opportunity Ahead

Source: US Census Bureau; IC-Insights; TSMC estimates

10

11

Wor

ld P

opul

atio

n (B

illio

n)

Sem

i $ /

Pers

on

5

6

7

8

9

‘80 ‘85 ‘90 ‘95 ‘00 ‘05 ‘10

US Semi / Person = ~$250245

255

265

China & India Semi / Person = ~$20

4

Worldwide average semiconductor $ per personWorld Population

Proprietary& Confidential

© 2007 TSMC, Ltd

11

Outline

Semiconductor Market OutlookChallenges and Solutions

EconomicTechnology

Summary

Proprietary& Confidential

© 2007 TSMC, Ltd

12

Challenges

Economic

1. Huge CapEx2. ROI Risk – Process3. ROI Risk – Product

Technology

4. Nanometer Manufacturing5. Nanometer Design6. Design Complexity

Proprietary& Confidential

© 2007 TSMC, Ltd

13

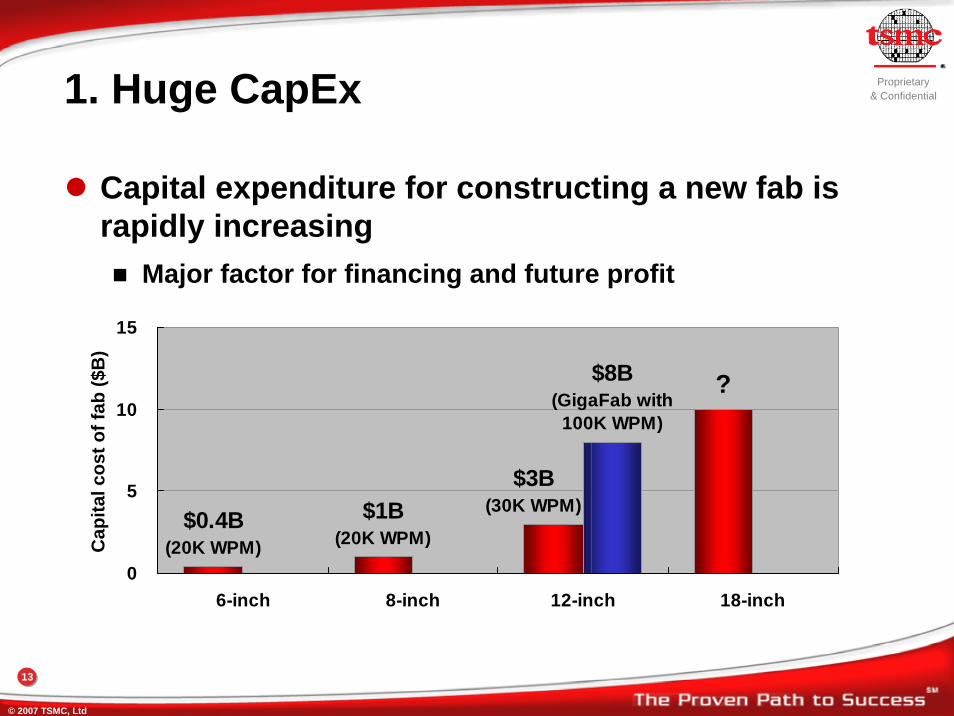

1. Huge CapEx

Capital expenditure for constructing a new fab is rapidly increasing

Major factor for financing and future profit

$0.4B(20K WPM)

$1B(20K WPM)

$3B(30K WPM)

?$8B(GigaFab with

100K WPM)

0

5

10

15

6-inch 8-inch 12-inch 18-inch

Cap

ital c

ost o

f fab

($B

)

Proprietary& Confidential

© 2007 TSMC, Ltd

14

PastPast

OEM

Distribution

Solution – Foundry Based Business Model

Many IDMs are changing to either fab-lite of fablessA wide variety of consolidation and collaboration are inevitable

FutureFuture

Assembly& Test

Design Service

IP Vendor Fabless

PresentPresent

Manufacturer

Product

Design Product Focused

IDM

IDM Getting Fab-lite Assembly

& Test

Foundry

IP Vendor

Fabless

Few IDMs

Few Foundries

Few IDMs & Foundries,Many Fabless

VerticallyIntegrated

IDMs in Transition,Fabless Getting Bigger

Proprietary& Confidential

© 2007 TSMC, Ltd

15

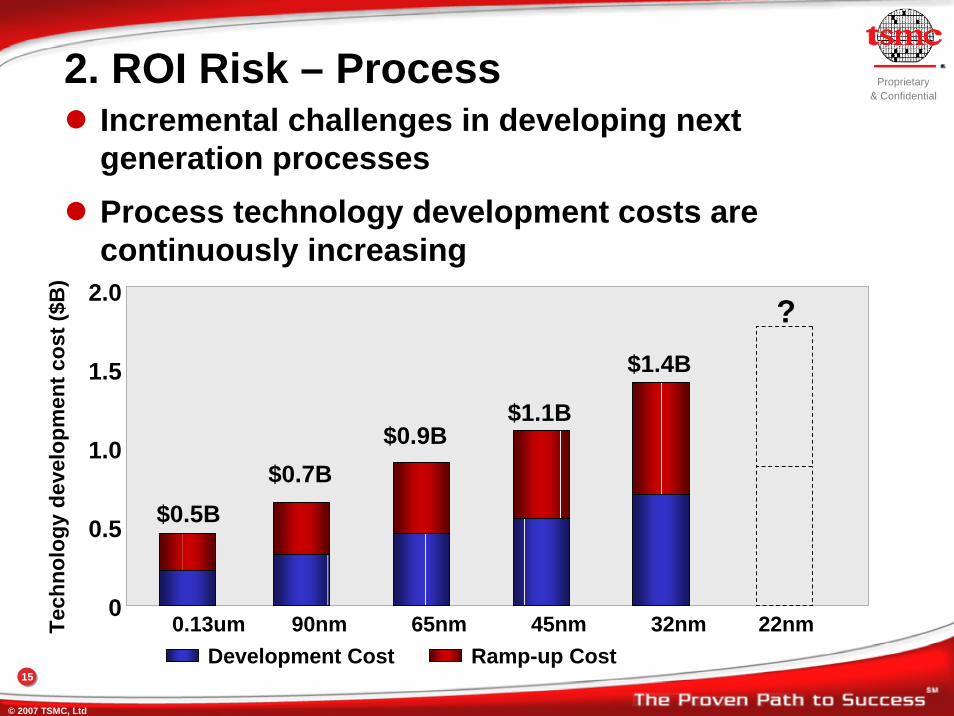

2. ROI Risk – ProcessIncremental challenges in developing next generation processesProcess technology development costs are continuously increasing

22nm0.13um 90nm

$0.5B$0.7B

65nm

$0.9B

45nm

$1.1B

32nm

$1.4B

Ramp-up CostDevelopment Cost

Tech

nolo

gy d

evel

opm

ent c

ost (

$B)

0.5

0

1.0

1.5

2.0 ?

Proprietary& Confidential

© 2007 TSMC, Ltd

16

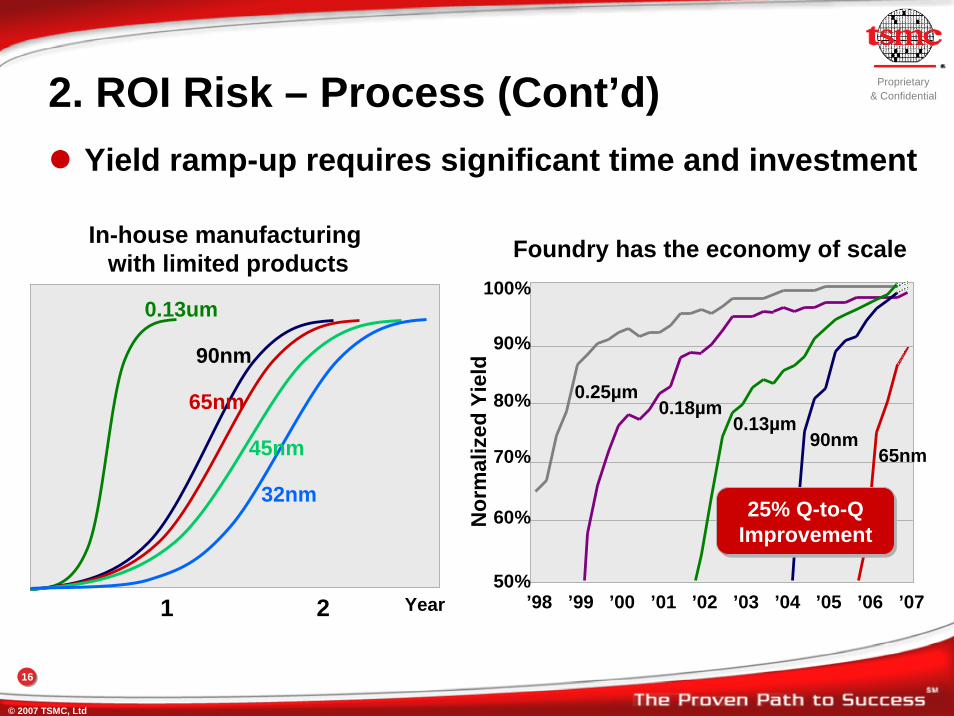

2. ROI Risk – Process (Cont’d)Yield ramp-up requires significant time and investment

50%

60%

70%

80%

90%

’98 ’99 ’00 ’01 ’02 ’03 ’04 ’05 ’06 ’07

Nor

mal

ized

Yie

ld

0.25µm0.18µm

0.13µm90nm

65nm

25% Q-to-QImprovement25% Q-to-Q

Improvement

100%

1 2 Year

0.13um

45nm

90nm

32nm

65nm

In-house manufacturing with limited products Foundry has the economy of scale

Proprietary& Confidential

© 2007 TSMC, Ltd

17

Solution I – Technology Alliance

Collaboration is required to overcame ever –increasing financial as well as technical challenges

IMEC

Matsushita

Proprietary& Confidential

© 2007 TSMC, Ltd

18

Solution II – Collaboration among Foundry, IP/EDA Vendors, And Design Service Suppliers

Standardization of IP & EDA tools

IDM

IP & EDADesign Service

Foundries

Proprietary& Confidential

© 2007 TSMC, Ltd

19

3. ROI Risks - ProductDesign complexity and cost increase rapidlyShort time to market

0.13um 90nm 65nm 45nm

10

20

30

40 80

60

40

209M$9.2M

16M

$18M

27M$48M

Gat

e C

ount

(M)

Des

ign

Cos

t ($M

)

Design CostGate Count

40M$70M

Proprietary& Confidential

© 2007 TSMC, Ltd

20

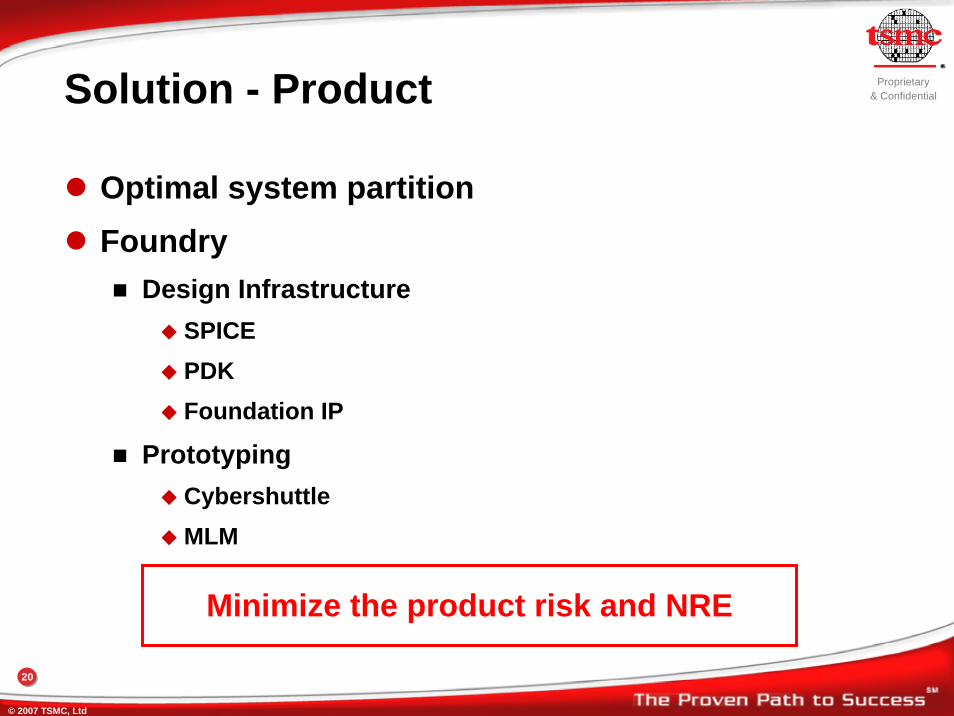

Solution - Product

Optimal system partitionFoundry

Design InfrastructureSPICEPDKFoundation IP

PrototypingCybershuttle MLM

Minimize the product risk and NRE

Proprietary& Confidential

© 2007 TSMC, Ltd

21

4. Nanometer Manufacturing

New materials and device structureHigh-K gate dielectric Metal gate3D FINFETLow-K Interconnect

New EDA solutions for technology modeling and advanced lithography

Proprietary& Confidential

© 2007 TSMC, Ltd

22

Solution – Technology Modeling / Advanced Lithography

Secure accurate SPICE modeling

Modeling in new material, 3D device and equipment / topographyPolarization, OPC, double exposure and mask 3D effects

Accuracy

Systematiceffect

Randomeffect

STIWPEStrained silicon effectOPC

Corner modelStatistical model

Collaborate with EDA vendors to achieve seamless interfacing hierarchy

Proprietary& Confidential

© 2007 TSMC, Ltd

23

5. Design for Nanometer

Increasing systematic / parameter / random yield loss due to process variation

Physical patterning effects, open and short, etc.Chemical and mechanical impact, planarity, antenna effect, and via opens, etc.Timing, signal integrity and voltage drop

Increasing leakage (quantity, source, variation)

Proprietary& Confidential

© 2007 TSMC, Ltd

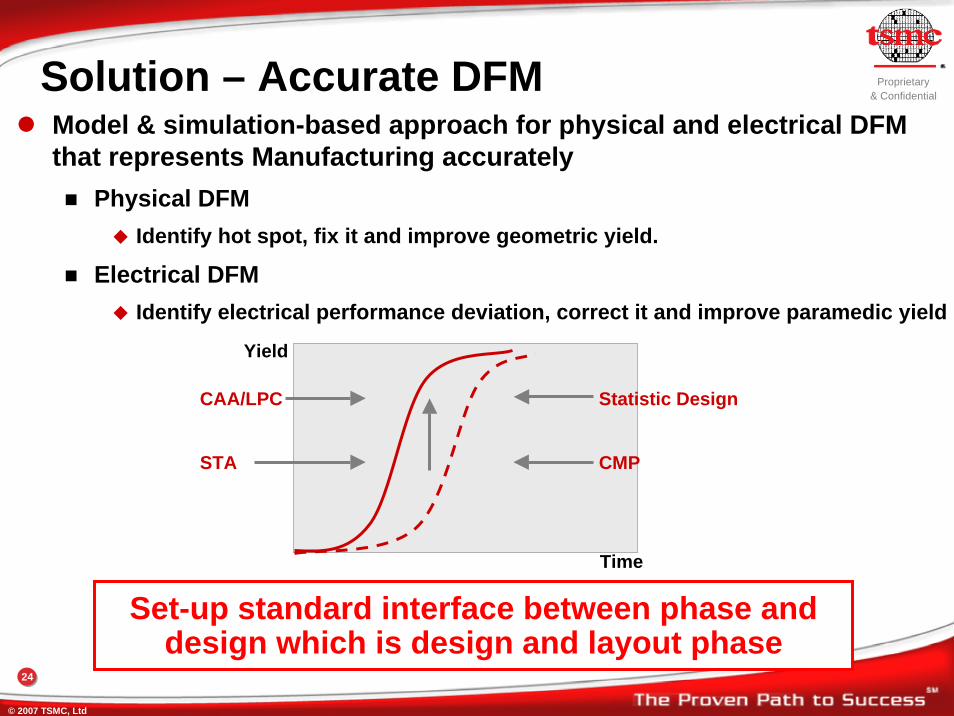

24

Solution – Accurate DFMModel & simulation-based approach for physical and electrical DFM that represents Manufacturing accurately

Physical DFMIdentify hot spot, fix it and improve geometric yield.

Electrical DFMIdentify electrical performance deviation, correct it and improve paramedic yield

Statistic Design

Time

CAA/LPC

STA CMP

Yield

Set-up standard interface between phase and design which is design and layout phase

Proprietary& Confidential

© 2007 TSMC, Ltd

25

Solution – DFM Ecosystem

Foundry to set up DFM ecosystem and open license DUF to reduce costStandard interface between the design infrastructure and manufacturing

EDA Alliance IP/Lib Alliance TSMC TSMC/GUC +DCA Alliance

TSMC DFM Compliance Initiative

Example:

Proprietary& Confidential

© 2007 TSMC, Ltd

26

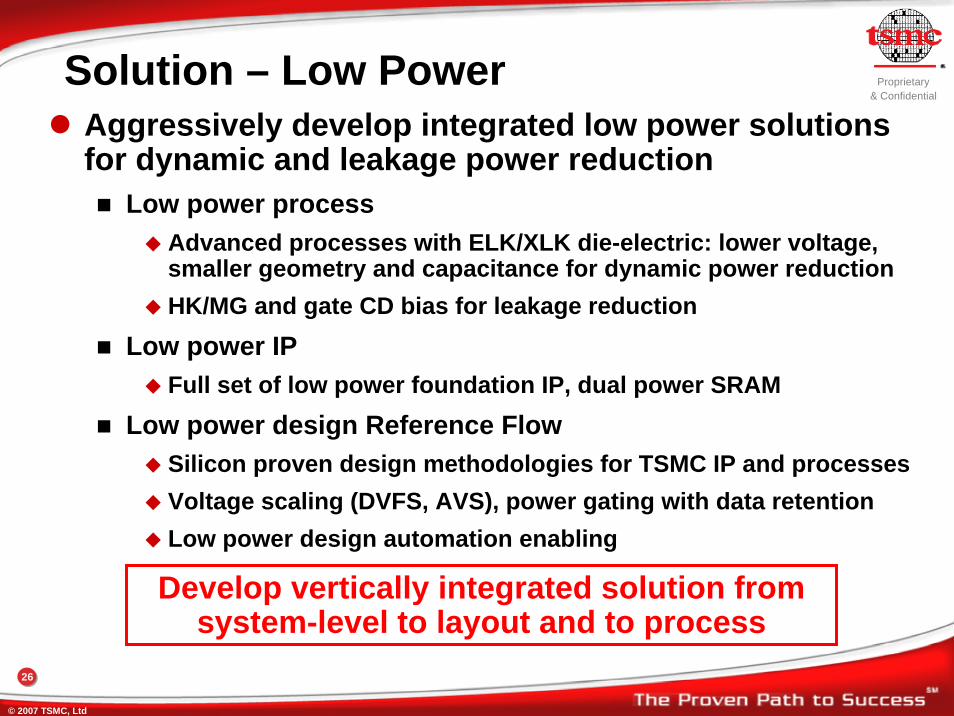

Solution – Low PowerAggressively develop integrated low power solutions for dynamic and leakage power reduction

Low power processAdvanced processes with ELK/XLK die-electric: lower voltage, smaller geometry and capacitance for dynamic power reductionHK/MG and gate CD bias for leakage reduction

Low power IPFull set of low power foundation IP, dual power SRAM

Low power design Reference Flow Silicon proven design methodologies for TSMC IP and processesVoltage scaling (DVFS, AVS), power gating with data retention Low power design automation enabling

Develop vertically integrated solution from system-level to layout and to process

Proprietary& Confidential

© 2007 TSMC, Ltd

27

6. Design ComplexityIncreased design complexity causes longer time-to-market and requires significant effort for verification and software design

‘95 ‘00 ‘05 ‘10 ‘15 ‘20

Moore’s Law

Mobile Multimedia DeviceCommunication Device

Current Design Productivity

VGA

D1

HD

Full HD

2G

3G

4G

Year

Com

plex

ity

Proprietary& Confidential

© 2007 TSMC, Ltd

28

ElectronicSystem Level (ESL)

Main Stream

ICE

AMBA Multi-layer AHBAMBA Multi-layer AHB

AMBA APBAMBA APB

APB BridgeAPB

Bridge

GPIOGPIOPWMPWM KBMOUSE

KBMOUSE WDTWDT I2CI2CDAI

(I2S)DAI (I2S) TimerTimer RTCRTC UARTUARTSSISSI

StaticMemory

Controller

StaticMemory

Controller

DirectMemoryAccess

DirectMemoryAccess

VectorInterrupt

Controller

VectorInterrupt

Controller

LocalMemory

Controller

LocalMemory

Controller

SDRAMController

(4-CH)

SDRAMController

(4-CH)

GPrimeGPrime PlatformPlatform

CPUCPU

Network

Architecture ExplorationSoftware ProfilingHardware ProfilingPower Estimation

Main Stream vs.ESL Co-development Environment

Proprietary& Confidential

© 2007 TSMC, Ltd

29

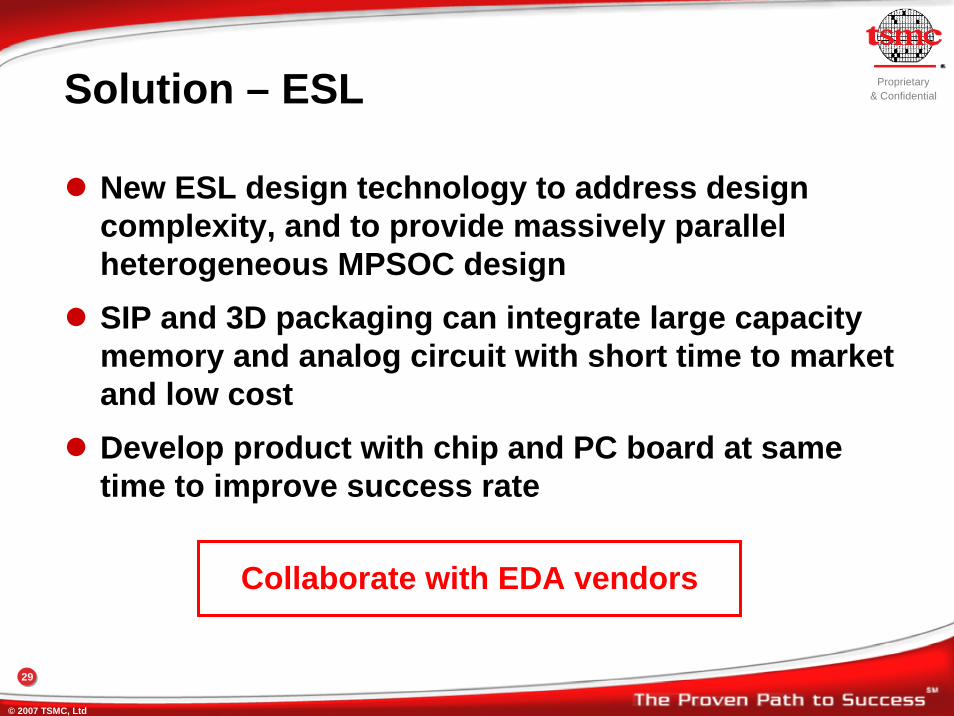

Solution – ESL

New ESL design technology to address design complexity, and to provide massively parallel heterogeneous MPSOC designSIP and 3D packaging can integrate large capacity memory and analog circuit with short time to market and low costDevelop product with chip and PC board at same time to improve success rate

Collaborate with EDA vendors

Proprietary& Confidential

© 2007 TSMC, Ltd

30

Summary

Semiconductor market growth will continue but moderate Future growth opportunities will be global but bifurcateHigh ROI risks in design, fab, and technology could be alleviated with the integrated foundry modelClose collaboration is required between EDA vendors, foundry and IC companies

Proprietary& Confidential

© 2007 TSMC, Ltd

www.tsmc.com

Thank You