the facilitation of lifelong financing for affordable housing in ksa full paper jfa

TRANSCRIPT

The facilitation of lifelong financing of the

affordable properties in the Kingdom of Saudi

Arabia

Bhzad Sidawi Department of Architecture, College of Architecture ad Planning, King

Faisal University

Abstract The demand for affordable housing has largely increased in

the past decades in Saudi Arabia due to the increase of population,

inflation and variation in income levels. Islamic banks and financial

organizations had emerged in Saudi Arabia as early as 1980’s and since

that time they have provided Islamic financing to the prospected home

buyers. The present financing system for buying properties seems

inflexible enough as it does not consider the user’s lifelong preferences

and requirements regarding the property such as: the future physical

alterations or improvements, partial or full transfer of the ownership and

the management of the property. It does not offer the necessary support to

the user to manage the changes that would affect the property during it’s’

lifecycle. These possible changes would have an impact on the property

value and leave the user/ owner unable to do improvements or alterations

or to properly manage or maintain the property. The owner has the right

of getting flexible lifelong financial support and management of the

property. The study argues that initial bank’s support to the buyer to

purchase of the property would not be sustainable unless it considers the

lifelong owner rights. The paper suggests an approach to lifelong

sustainable financing scheme that would support the owner to cope with

possible impacts on the property. This study should motivate banks,

charities, other financing organizations, investors and decision makers to

consider similar approach that provide lifelong financial benefits and

support to the owner.

Keywords: affordable housing, Islamic built law, owner’s lifelong rights, lifelong

sustainable financing, property management, user lifestyle

2

1 Introduction

The demand for affordable housing around the world – in general- and

particularly in Saudi Arabia Kingdom has increased in the past decades due a

number of factors such as: the variation of income levels, the increase of

population who do not have financial resources to buy a property from the

traditional market (Payne 1984). The demand for next few years will increase in

Kingdom of Saudi Arabia, and there is a concern that financial organizations did

not develop yet a feasible strategy and create flexible mechanisms to tackle the

problem. The present provision of funding by banks to prospected affordable

housing buyers consider a number of instant or purchase-moment factors,

meanwhile lifelong factors are not considered and the lifelong financial support

is absent.

The literature review and examination of online documents published by banks’

on their web sites found little evidence that governmental bodies, REDF (Real

Estate Development Fund), or banks support anything other than the purchase of

a property. The lifelong sustainable financial support to the owner is the support

that could meet the payment of the mortgage loan and meet the possible costs of

the following aspects:

lifelong environmental impacts on the property;

upgrading the property in response to the climate change;

lifelong maintenance and management of the property;

the property’s improvements in regards to user’s lifestyle; and

transfer of management and control, ownership and use/ utilization rights

Such support would be capable to reserve the value of property if does not

increase it. A survey has been undertaken on bank in Kingdom of Saudi Arabia

to find out the extent of banks’ support to the owner/user at present and their

future plans to provide lifelong support. The paper discusses the survey results

and suggests a methodology that could provide support to the property owner.

Two main themes that would affect the value of the property are discussed;

namely: the user/owner lifestyle; rights and responsibilities, and the

environmental impacts on the property.

This paper highlights the need to incorporate the factors that have a significant

impact on the property lifelong value such as the home owner and property

characteristics in the financing scheme. This may secure the property value

throughout it’s life. The owner characterises can be categorized broadly into: the

style of ownership, use, management; and control. The property characteristics

would include Building quality, adaptability and the energy efficiency. In the

following sections, this paper discusses the importance of various aspects of the

user’s and property characteristics.

2 Impacts on the property value

2.1 The owner/ user rights impact on property value

The ownership and control/ management rights of the home owner in Saudi

Arabia are partially and fragmentally addressed by built laws issued by the

government authorities (e.g. local municipalities). These set general guidelines in

regards to the home owner rights to build a property, to alter his/ her property. It

certifies what designers should do regarding the building setback distances,

distance between properties, block’s height restrictions and so on. It does not –

for instance- define how the property should be designed in regards to the local

lifestyle, traditions and norms or how the user should maintain the property.

These rights have been defined by the Islamic Sharria (Akbar 1992). Akbar

pointed out three broad types of these rights/ responsibilities of an individual (i.e.

the user or the owner), and these are: control and; management, ownership, and

use: this includes right of use and right of benefit.

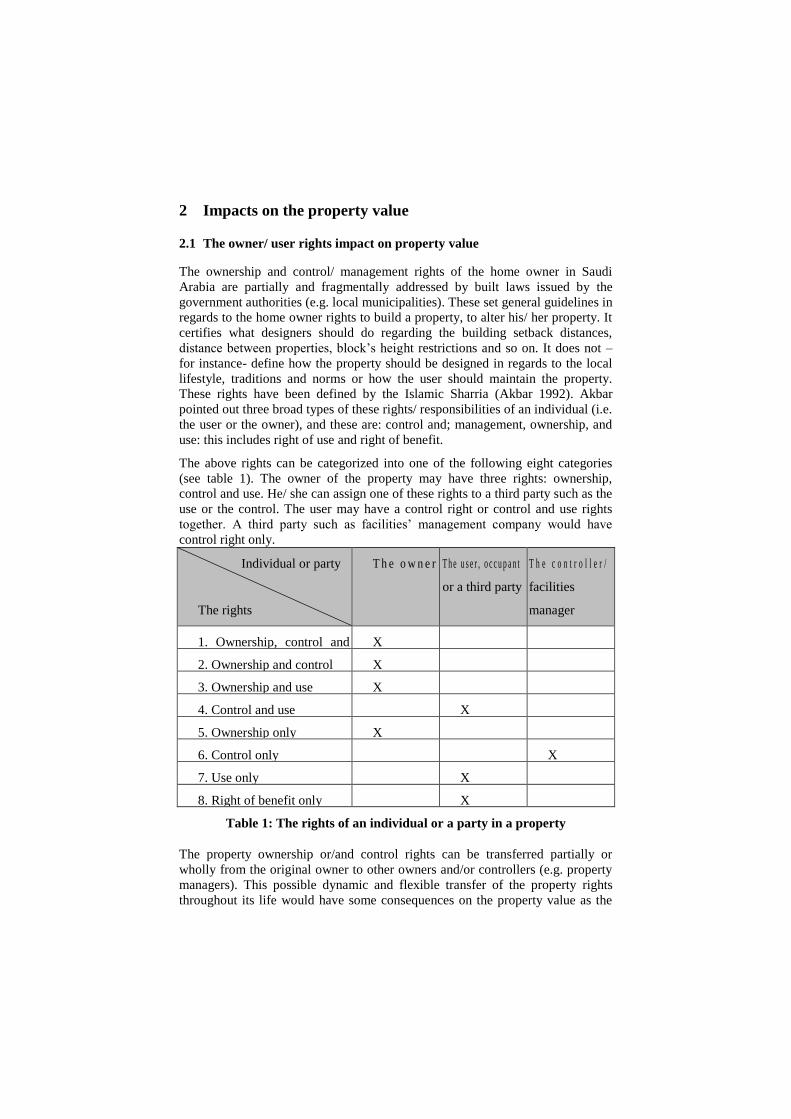

The above rights can be categorized into one of the following eight categories

(see table 1). The owner of the property may have three rights: ownership,

control and use. He/ she can assign one of these rights to a third party such as the

use or the control. The user may have a control right or control and use rights

together. A third party such as facilities’ management company would have

control right only.

Individual or party

The rights

T h e o w n e r T h e u s e r , o c c u p a n t

or a third party

T h e c o n t r o l l e r /

facilities

manager

1. Ownership, control and

use

X

2. Ownership and control X

3. Ownership and use X

4. Control and use X

5. Ownership only X

6. Control only X

7. Use only X

8. Right of benefit only X

Table 1: The rights of an individual or a party in a property

The property ownership or/and control rights can be transferred partially or

wholly from the original owner to other owners and/or controllers (e.g. property

managers). This possible dynamic and flexible transfer of the property rights

throughout its life would have some consequences on the property value as the

4

responsibility of use, maintenance or control would be exercised by a group of

people or an individual. This implicates responsibility of each one who would

have one of the above rights towards the property in terms what he/she should

do/not do and how it should be done. For instance, the home owner is

responsible to keep up the property in a good condition. In case he/she decides to

alter the property, he should do it without harming his neighbours and violating

their rights1. The user/ occupant is responsible to keep the property tidy and well

maintained and to report any problem to the owner. The property facilities’

manager should keep the property and its systems well maintained.

A number of research studies have highlighted the relation between the user

characteristics, housing design and use and pointed out the importance of

building up a knowledge that would be used in housing design to provide

tailored design solution to people needs, lifestyle and future preferences (Hillier

1984, 1996, Hojrup 2003, Habraken 2003, and Salama 2006). In KSA,

researchers mentioned that non-consideration of user needs such as: the need for

flexibility and adaptability in design has created an uncomfortable environment

to the user (Al-Kurdi 2002, Darweesh 2003). The absence of these aspects has

enforced the owner to carry out a number of changes to their properties which

are sometimes expensive and adapt it to suite the way he/ she would like to live.

Mahmud (2007) suggested that the transformation of properties can be

categorized under the following categories: slight adjustment, addition and

division, total conversion, and reconstruction. He mentioned some of the reasons

for the transformation of a property which would include:

the adoption of the some of the modern life features by the owner such as the

installation of new kitchen or bathroom;

the need to achieve a higher degree of privacy for some spaces;

to adapt the spaces to the owner lifestyle by –for example increasing the

number of rooms or changing the function of some spaces; and

to use a part of the property for commercial uses to generate an additional

income to support the family.

Therefore, the way that rights, responsibilities and lifestyle exercised by the

owner would affect the property and may bring down it’s value. Sayce (2004) –

for instance- highlighted a number of user characteristics that has an impact on

1 Ahmed and Parry highlighted how an owner/ user right should be practised without

violating the neighbours’ rights. They surveyed the low income housing in Cairo and

noticed that despite some disadvantages that exit in the low-income housing in Cairo,

residents corporate with their neighbours upon making decisions regarding alterations of

their properties or building new blocks. These residents were able to reach to the best

solution that would satisfy everyone. The researchers found that such corporation is

motivated by local people’s beliefs and principals such as ‘No Harm’ principal which is

derived from the Islamic values (Ahmed K G and Parry C M 2001, 2002)

the property value such as the impact of the occupier and the occupier’s

satisfaction with the property.

2.2 Environmental and property characteristics impacts on the property’s

value

Environmental impacts are due to the climate change which include rising global

temperatures, rising sea levels and increased frequency and intensity of extreme

weather. Extreme weather and natural disasters are expected to be more frequent

as well. In hot regions such as in KSA, the rise of temperature would enforce

people to use air conditioning more frequently and this would send more gases

into the air, cause more pollution and increase the annual energy bill. In the

future, properties may deteriorate faster and its’ systems may collapse or fail

quicker. The properties will be costive to run if they do not interact naturally

with the environment.

The incorporation of environmental impacts on the property value has been

researched by a number of researchers (Myers et al 2007). Sayce et al (2004)

suggested a link between the property value and sustainability indicators. The

target of this link is to attract several parties such as investors’, authorities and

occupiers attention to the importance of the sustainability and how the abandon

of sustainability would badly affect the property value. She created an appraisal

model that incorporates the sustainability indicators (i.e. building flexibility,

energy efficiency, transport, pollutants, location, occupier, ecology and design)

into calculations of property value. The impact of each indicator on property

value was done through changes in the allowances made for each of the property

appraisal criterions2. By linking each of the sustainability indicators with one or

more of these criterions it is possible to translate the sustainability of a property

into an impact on value (see table 2). She pointed out that a range of

sustainability issues should be considered by the investor or occupier who wishes

to mitigate the risks represented by increasingly stringent environmental

legislation, energy efficiency regulation and transport management policies

operating at local, regional and national levels.

2 Rental growth: the parameters developed for rental growth assume a direct

relationship between rent and occupier costs; any increase in occupier costs will reduce

the amount available for rent

Rental depreciation is commonly used by appraisers to reflect refurbishment costs.

Cashflow: in some instances a sustainability factor may impact directly through the

cashflow. This will normally be due to a requirement for a one off or series of cash

payments to insure against or mitigate a potential risk. Where this is the case, assuming

the cost can be accurately estimated, a figure can simply be deducted from the cashflow at

the appropriate point.

Risk: such as business and investment risk. These criterions are calculated over a

number of years (see Sayce 2003)

6

Sustainability

factor

Conduit (i.e. property appreciable criterion)

Building adaptability Risk premium, cash flow, rental growth, depreciation

Accessibility Rental growth, depreciation

Building quality Cash flow, rental growth, depreciation

Energy efficiency Risk premium, cash flow, rental growth, depreciation

Pollutants Risk premium, cash flow, rental growth, depreciation

Contextual fit Rental growth

Waste and water Cash flow, rental growth, depreciation

Occupier satisfaction Risk premium

Occupier impact Risk premium

TABLE 2: links between sustainability criteria and worth (source: Sayce

2004)

She highlighted that a building that can not be easily adapted to support the

changing needs of its user, compared with other buildings within its class, will

suffer relatively rapid depreciation; as utility falls willingness/ability to pay rent

will also fall. A building that is not sufficiently adaptable for its existing use type

(within use) may be sufficiently adaptable to move to another use (across use)

making it more sustainable than one which can not. In practical terms a building

without sufficient adaptability within use will require sooner - and potentially

more frequent- re-letting and refurbishment, and vice versa. This will reduce

cash flow by increasing voids and refurbishment costs. Increasing an occupants’

degree of control over their environment would increase the level of comfort and

perceived productivity. This increased tolerance, particularly when integrated

with other building fabric design strategies, can enhance the adaptive potential of

a building to climate change (Sayce et al 2004).

On the other hand, properties should be frequently maintained to prolong the life

of the property. Steemers (2003) pointed out that the absence of frequent

maintenance would create a situation where properties are in a desperate need for

maintenance. Struyk (2005) mentioned that a significant share of the housing stock in

Saudi Arabia would need replacement in the next 20–25 years and around 30% requires

improvement in the next 5 years.

As a conclusion, the property value would be affected by the following issues:

a. The owner/ user characteristics: these would include:

the lifestyle of the owner/ user that affect the way that he/ she uses and

manages the property;

the way the ownership, control and use rights are exercised by a party

or a number of parties and how each party conduct his responsibilities;

the characteristics of each party that has certain rights in the property;

and

the transfer of one of the rights to a third party

b. The property characteristics and these would include:

the adaptability, accessibility, and maintainability degree of the

property

the building quality of the property

the sustainability level of the property

3 Research objectives and methodology

The research has a set of objectives and these are:

to explore characteristics of the existing financing system and how far it

supports the lifelong owner’s lifestyle;

to find out which of the user lifestyle and environmental issues have

significant impact on the property value;

to make recommendations to banks and other financial organizations on

how to respond to people needs and aspirations and provides lifelong

support to them

To achieve these objectives, a survey questionnaire and discussion group tools

were used to assess the banks’ level of lifelong support to the user. A

questionnaire survey was used to target 11 Saudi banks and REDF. The

questionnaire was sent to banks in March 2008. Three banks including REDF

responded back. Afterwards, three remainders were sent but without any

response. The researcher contacted local branches of banks in the Eastern region

asking for an interview. After around two weeks, the researcher was able to

interview all real estate managers/ branch managers using the same

questionnaire. Simple statistic methods such as T-test, percentage and mean were

used to analyze the data as the sample number was too small. Bank managers

were invited to the College of Architecture to discuss the results of the

questionnaire and to find out banks’ future plans regarding the owner’s support.

Unfortunately, three banks managers were able to attend and the seminar was

chaired by an expertise in Islamic built laws from the College of architecture.

4 General results

Banks seem to have a very flexible policy regarding the alteration of the property

by the owner as all of them do not mind the owner to carry out any alterations.

Banks were divided over a number of issues regarding the owner rights and these

8

include his/ her right to grant the right of benefit to somebody else, to let the

property or part of it and to use the property for purposes other than residential.

Most banks (i.e. 10 out of 12) have no problem with the owner hiring a third

party to manage the property and they said that he/she has the right to sell the

property provided he/she paid the outstanding mortgage loan. Most of them (10

out of 12) were unhappy about the donation of the property or part of it by the

owner to somebody else and said he/she has no right to do so during the

repayment of the mortgage loan period.

Very few banks agreed to help the owner with transfer of right to benefit to a

third party, and to invest in the property i.e. to use a part of the property for other

uses. Banks were divided over supporting the owner regarding the following

issues: internal alteration, external alteration and management of the property by

third party. Many of them (i.e. 8 banks out of 12) said that they can help - in a

way or another- with transfer of the property to heirs (i.e. family and relatives)

and possible natural disaster. Some banks (i.e. 4- 5 out of 12) were unhappy to

address the following issues in their future plans: to give the borrower more

lifelong advantages and support, to extend the mortgage loan repayment period,

and to support the future needs of the client as such future alterations of the

property. Few banks (i.e. 2 out 12) are unhappy regarding the introduction of

smooth property registration, title transfer and to offer a flexible mortgage loan

package.

Banks were asked about the significance rank of a number of management

and ownership factors to the affordable property value during the repayment

period of the mortgage loan. Banks considered a number of factors would have a

weight above average (i.e. 5) and these are: building adaptability, the owner

occupant daily lifestyle activities, energy efficiency of the property, Internal and

external alterations carried out by the owner to suit his/her lifestyle, maintenance

and management practice style of the property by the owner, building quality and

other criterion (see table 1). Some of these factors (i.e. 5, 7, 11& 12, see table 1)

are found also by Sayce (2003) as significant factors that affect the property

value. It was not obvious at this stage whether and how banks consider these

issues in the initial mortgage scheme, in the re-mortgage scheme or provide other

means of financial support to the owner during the repayment of the mortgage

loan period. During the interviews, banks’ managers mentioned a number of

aspects which would affect the financing of affordable housing in KSA:

The slowness of REDF procedures;

Very few and weak links that exist between banks themselves, between

them and Joint-stock, other financial organizations including big

investors; and

The financial legislations regarding the real estate funding that do not

provide a secure environment to banks to operate

5 Cross tabulation results

In depth analysis (i.e. cross tabulation) has found links between banks

characteristics, their views about user rights and support to the user. Banks which

has high financial activity regarding the lending for property purchase during the

last year said:

it is the owner right to grant the right of benefit

to let the property to somebody

internal alteration expenses can be supported through other/ re-mortgage

loan arrangement

they are happy to support the future needs of clients

Property characterises and owner’s rights Weighting out of 10

1. Partial transfer of the ownership 0.17

2. The transfer of right to benefit to a third party 2.83

3. Commercial investment in the property by owner (i.e. use part of

the property for other uses such as commercial) 3.00

4. Management of the property by a third party 4.00

5. Building adaptability 5.27

6. The owner occupant daily lifestyle activities 5.33

7. Energy efficiency of the property 5.50

8. Internal alteration carried out by the owner to suit his lifestyle 5.83

9. Maintenance and management practice style of the property by

the owner 5.83

10. External alteration carried out by the owner to suit his lifestyle

(i.e. external extension) 6.36

11. Building quality 7.33

12. Other criterion (i.e. building location, age and area) 8.40

Table 3: The weight of each of property characteristics and owner rights

on the property value during the repayment period of the mortgage loan

(weight above average is in bold)

Banks with high financial activity since the start of their financing scheme

are happy that:

the owner has the right to grant the right of benefit

10

internal alteration expenses can be supported through other/ re-mortgage

loan arrangement

the owner can get financial support to transfer the right of benefit in a way

or another

the owner who likes to invest in the property, can get financial help

through a re-mortgage loan arrangement

Banks with low financial activity during last year said that it is possible to give

the borrower more lifelong advantages and support

All banks were happy with the following issues:

to have a very flexible policy towards the alteration of the property

to help the owner in some way to transfer of the property to heirs

to help the owner with possible natural disaster

Regardless of their financing history length, banks were divided over the

following issues:

the owner right to hire a third party to manage the property

the significance of the maintenance and management practice style carried

out by the owner to the property value

the building quality significance to the property value

Banks which consider providing financial support to the owner to carry out the

internal alteration said that the internal alteration has a significant weight on the

property value. The analysis of the questionnaire data had produced some useful

results but it raised some questions such as: why some banks are happy with an

issue or they said it is significant to the property value but they do not provide

support to the owner. The following section will discuss such questions with the

banker representatives to find possible explanations.

6 The discussion forum results

Banks’ representatives were invited to discuss the questionnaire results and

whether the factors that affect the property value that found in the initial survey

are really important. The output of the discussion revealed a number of

problematic factors that would affect the lifelong financial support to the home

owner.

The present financial legislations

A bank representative said that opportunities to provide financing in KSA are

low and there is high risk. He proceeds that it is better if the bank work with one

co-operate client and undertakes a low risk and gets less profit than working with

5000 customers and having problems in regards to the payments’ collection. He

regretted that rights of banks are not protected by present legislations. Banks are

willing to offer financing but they can not do it without protection. However, the

implementation of the Rahin Aqary (i.e. mortgage regulation system) would

provide protection to banks and regulates the relation between the borrower and

the lender. It would give banks the right to overtake the house if the borrower did

not make payments for a certain period. However, the system may contradict

with the some of the Islamic Shariah clauses which protect the homeowner

unless the system has the power to overcome this issue. This would give banks

bigger willingness to lend buyers because the system is capable to reserve the

banks’ rights. Banks have another problem as there are two systems in KSA; the

Grievance Board or Diwan al-Mazalim and the conventional judicial system and

each of them may give different verdict for the same case.

The Cultural issues

Another representative mentioned some of the cultural characteristics that affect

the lending process to the public. He said:”when the government announced the

property financing system, people imagine that it is free”. The Saudi Society

expects that everything is or should be free. Thus, when banks provide mortgage

loans, people have vague understanding of the mortgage loan terms and

conditions, whether it is free, halal (i.e. not prohibited by Islamic Shariah) or not.

This is why –as another banker said- banks initially went into Ijara scheme as

this would keep the property ownership with the bank.

The level of the financial knowledge of clients

A banker said that the customer should be educated about financing products and

process. He/she should understand he/she is entering into a business transaction

relation. The mortgage loan that the customer gets, will not be subsidized by the

government, it is a loan based on affordability and commitment to pay back.

The shortage of adequate mortgage loan package

One of the bank representatives pointed out that property financing scheme

should not be limited to the appraisal and financing issues but it should be

extended to include the property maintenance which is absent at present due to

the absence of high profile facilities’ management companies. On the other hand,

it is guaranteed that the tenant/ owner of a house/ villa would have full control on

the whole property but in case of a flat, the tenant/ owner would have full control

on the flat but he/she may not have control of the shared parts of the block. Thus,

this would affect the quality of maintenance of the whole block.

The problem of finding and creating Islamic financing mechanism

A banker said that if the bank feels that it needs to produce a new product (i.e.

mortgage loan), it will do it. The bank may have a product which another bank

does not have and does not want to have. It is related to the market demand and

what is offered. Banks has the ability and creativity to create and produce new

and excellent products.

This was rejected by another banker who said that creation of new products in

respect of the Islamic Shariah would be a problem as banks have to develop new

12

Islamic financing mechanisms. When a new Islamic mechanism is created, the

bank compares the effect of the new Islamic mechanism with the conventional

one in order to assess the potential risks. As an example, the bank has created an

Islamic mechanism for selling up a property on paper before construction. The

banker said: “we do it through Ijara Mawsofa Be-Zema which means that the

bank let the property to the client through a letting contract. The bank and client

signs Istisnaa contract in which the client instructs the bank to construct the

building for him/her. The bank instructs a building developer to construct the

building according to the client’s specifications”. Ijara Mawsofa Be-Zema has

its’ risk and the Istisnaa contract as well and these can not be put together back to

back as one contract because each one has its legal liabilities. The client and the

building developer will have no responsibility if any problem regarding the

building quality arises, and the bank will be the only one in trouble. Such

financial arrangement would constitute a high level of risk for the bank.

Therefore, when the bank is engaged in a relationship with a building developer,

the problem is to find the right Islamic mechanism that control such relationship

and provide the right product to the client. Another banker highlighted the

difficulty of the creation of some mortgage products as the government would

consider that it would conflict with the public rights and interest.

The mortgage loan product and lending process risks

One of bank representatives said that one of the issues that will stop the product

from being marketed is to be of a high risk. Banks are concern about risk/ reward

issue so since the bank own the property, it wants to be certain that it’s value will

not decline while it is under it’s custody until it is sold/ handed over to the

customer. At present, Saudi Credit Bureau (Saudi Credit Bureau 2008) have

credit history database for KSA citizens and this can be reached by banks which

incorporate it in pricing and assessing new mortgage loan products which would

reduce potential risks.

The weight of free land provision by government on property value

The discussion forum’s chairman pointed out to the importance of providing free

land plots to the low-income people. He stated that land plots should not be

given to influential individuals; instead the government should give it to highly

qualified giant companies and instruct them to set the infrastructure within an

assigned period. In case that they did not accomplish the work within the period,

the land would be given to somebody else. The land price which includes the

infrastructure costs would be cheaper.

7 Discussion and Conclusion

The study found a number of positive areas regarding the lifelong support of

banks to the owner. Banks seem to have a very flexible policy regarding the

alteration of the property by the owner as all of them do not mind the owner to

carry out any alterations. Most banks have no problem with the owner hiring a

third party to manage the property and they said that he/she has the right to sell

the property. Meanwhile, there was no overall agreement by banks regarding the

following owner rights:

his/her right to grant the right of benefit to somebody else;

to let the property or part of it and;

to use the property for purposes other than residential;

Banks were also divided over supporting the owner with the following issues:

internal alteration;

external alteration; and

management of the property by third party

Some banks were unhappy to address the following issues in their future plans:

to give the borrower more lifelong advantages and support;

to extend the mortgage loan repayment period; and

to support the future needs of the client as such future alterations of the

property.

Banks considered that a number of factors would have considerable weight

(above 6 out of 10) on the property value and these are: building quality and

other criterion (i.e. building location, age, area). Banks usually take into account

some of the property and user factors that would affect the property value but the

environmental and lifestyle factors are still absent from their agenda. These

potential factors should be incorporated in the calculation of the property lifelong

value to assure that future financial costs are met as much as possible.

In depth analysis showed that banks with long financing experience are happy to

consider some of the owner’s lifelong rights to support it such as: his/her right to

grant right of benefit and support the transfer of the right, to fund internal

alteration expenses, and support the owner who likes to use the property or part

of it for other uses such as commercial. However, all banks regardless of the

length of their financing experience were divided upon the significance of the

building management, quality and maintenance to the property value. The

interviews and discussion forum found that banks are well aware of the lifelong

needs of clients and they are happy to support some these needs but they are

incapable to do so due to a number of potential factors such as:

Insecure financial environment including legislations that hinder banks to

operate and flourish as they feel unprotected

the non-existence of building code that would control the building quality

in KSA;

the Cultural issues;

14

the level of the client’s education and knowledge regarding financial

issues;

the difficulty of finding and creating new Islamic financing mechanisms;

the financial risk of some of the new mortgage loan products; and

few and weak links with other financial organizations

Banks can develop new Islamic mortgage loan products such as the Istisnaa in

co-ordination with an expertise in Islamic financing law. On the environmental

side, lifelong financial support should address environmental impacts on the

property and how to meet it. On the owner/user’s lifestyle side, it may include

property development (i.e. design and construction), use/ownership, management

attributes or portions of each according to the client request. Mixing portions of

these attributes such as management and ownership or building development and

management would enable banks to produce multiple and flexible mortgage

packages. Through these packages, the bank would share some of the lifelong

ownership and management responsibilities with the owner.

The government should set clear and well defined financial legislations that

provide a secure financial environment to banks. Banks and the government have

the duty to provide basic financial education to the public. Future research would

investigate the present lifelong relationship between the bank and the owner and

test whether it is the right relationship that is capable to reserve the rights of both

sides while highlighting their responsibilities without contradicting Islamic

Financial laws. There should be also research on new methods that would

provide the lifelong financial support to the owner rather than the existing and

conventional financing ways which may exhaust the low-income owners.

Acknowledgements

The researcher would like to thank all banks and REDF in KSA for their

participation in the survey. Also, special thanks to the Dean and staff of College

of Architecture and Planning, King Faisal University for hosting and supporting

the discussion forum venue.

References

AHMED, K. G., PARRY, C. M. .(2002). Design for the poor in Egypt:

Satisfying User Needs or Achieving the Aspirations of Professionals?

the case of Mubarak National Housing Project for Youth, the Design

Research Society International Conference, Brunel University, London

AHMED, K. G., PARRY, C. M. . (2001). Towards a relevant framework for

participatory decision making processes in low-income neighbourhoods

in Cairo, Egypt: As an approach for socio-culturally responsive public

housing product. 1st International Postgraduate Research Conference on

the Built and Human Environment. University of Salford

AHMED, K.G., PARRY, C. M. (2001). Traditional Settlements, User

Participation and the ‘No-Harm’ Principle Towards a contemporary

participatory process in low-income public housing in Islamic cities.

IAPS Second International Symposium Traditional Environments in a

New Millennium: Defining Principles and Professional Practice.

Amasya, Turkey.

AKBAR, J. A. A. (1992). The Architecture of the earth in Islam (in Arabic)

KSA: Dar Al-Qebla.

ALDOSARY, A., ALSHUWAIKHAT, H., QUADRI, S. I., RAZIUDDIN., M.

(2007). Al Saedan Chair on Affordable Housing- revised report,

KFUPM, Volume I, determining affordable housing stocks in

administrative areas, Saudi Arabia Kingdom. April, 2007.

http://www.kfupm.edu.sa/crp/Saeedan/Volume%20One.pdf

AL-KURDI, F. (2002). (2002). The labor city in Dammam: an analysis of its

house forms. Advanced workshop ARAR 602. King Faisal University.

AL-KURDI, F. (2002) Lifestyle and house form: the case of Aramco houses

under home ownership in Dhahran. Unpublished graduate dissertation,

King Faisal University.

AL-SHAIKH, S. A., ALQATARI, M. A., MALICK, M. Y. (2000) Market

review and outlook: A weekly publication issued by the Economics

Department, NCB for the week ending 28th of April, 2000. Retrieved

May 2008 from

http://www.alahli.com/pdf/er2000/ncb_mro_28_04_2000.pdf

CHATFIELD, D. L. (2000). The challenges of affordable housing, APA

National planning conference, April 2000.

DEFRA. (2008). Climate change & energy. Retrieved July 2008 from

http://www.defra.gov.uk/Environment/climatechange/

DARWEESH, L. (2003) Dweller-initiated changes and transformations in Built

environment: the impact of building regulations. Unpublished MSC

thesis. King Faisal University.

DOUGLAS, M. (1996) Thought Styles: Critical Essays in Good Taste. London,

UK: Sage Publications.

HABRAKEN, J. (2003) Questions that will not go away: some Remarks on long

term trends in Architecture and their impact on Architectural education.

Keynote Speech: Proceedings of the Annual Conference of the

European Association of Architectural Education-EAAE. Hania, Crete,

Greece. pp. 32-42.

HILLIER, B. (1996) Space is the Machine. UK. Cambridge University Press.

HILLIER, B., HANSON, J. (1984) The Social logic of Space. UK. Cambridge

University Press. Hojrup., T. (2003) State, Culture, and Life Modes:

The Foundations of Life Mode Analysis. London, UK: Ashgate.

SHIHABUDDIN, MAHMUD. (2007). Identity crisis due to transformation of

16

home environment: the case for two Muslim cities, Dhaka and Hofuf,

METU JFA (24:2) 37-56.

MORSE, JANICE M. (ed.). (1991). Qualitative health research. Newbury Park,

Calif: Sage.

SAUDI CREDIT BUREAU. Retrieved July 2008 from http://www.simah.com

PAYNE G K. (1984). Low income housing in the developing world. Finance and

affordability, ed. Roger, T., Wily& sons Ltd.

PLYMOUTH CITY COUNCIL. (2008) Definition of Affordable Housing.

Retrieved October 2008 from

http://www.plymouth.gov.uk/homepage/environment/planning/planning

policy/affordablehousing/definitionofaffordablehousing.htm

SAIF SAUDI ARABIA INVESTMENT FUND. SAMBA, 1 quarter 2006. Saudi

Arabia and the real estate sector. Retrieved November 2007 from

http://www.samba.com/Content_Managers/SAIF_QTR_REP/files/Q1_2

006.pdf

SALAMA, A. M. (2006). A life style theories approach for affordable housing

research in Saudi Arabia. Emirates Journal for Engineering Research,

11 (1), 67-76. 2006.

SAYCE. S., ELLISON, L., SMITH, J. Incorporating sustainability in

commercial property appraisal: evidence from the UK. The 11th

European Real Estate Society Conference 2-5 June 2004. Milan, Italy.

(2004).

SAYCE, S. Integrating sustainability into the appraisal of property worth:

identifying appropriate indicators of sustainability. The American Real

Estate and Urban Economics Association conference. August 21 – 23,

2003, Skye, Scotland. (2003).

STEEMERS, KOEN. (2003). Establishing research directions in sustainable

building design, Tyndall Centre for Climate Change Research Technical

Report 5 September 2003. Retrieved December 2008from

http://www.tyndall.ac.uk/research/theme2/final_reports/it1_28.pdf.

STRUYK RAYMOND J.. Housing Policy Issues in a rich country with high

population growth: the case of Riyadh, Saudi Arabia, Review of Urban

& Regional Development Studies, Vol. 17, No. 2. pp. 140-161. (2005).

THE NATIONAL COMMERCIAL BANK NCB: Economics Department.

Market review and outlook, 15 June 2005, Volume 15, Issue 9,

Retrieved November 2008 from

http://www.alahli.com/pdf/er2005/15062005.pdf

WIKIPEDIA, Climate change, Retrieved June 2008 from

http://en.wikipedia.org/wiki/Climate_change#Examples_of_climate_ch

ange

Appendix A: Definition of terms

Al-Ijara: The bank owns high cost assets and assets that deal with

rapidly changing technology. After purchasing these assets, the bank then

rents them to the customer, giving him an option to either purchase them

during the rent period, or after its completion. It is the most efficient and

flexible way to utilize high cost assets and technology related products.

Al-Istinaa: An agreement suited for construction projects, whereby

the bank signs an agreement with the client for the construction of a site,

or a building, and then signs another agreement with the construction

company responsible for the development plan.

Diwan al-mazalim: A special tribunal that often resolves disputes

between citizens and government officials