the evolving economics of ethanol, and the outlook for policy change and industry investment dermot...

Post on 21-Dec-2015

215 views

TRANSCRIPT

The Evolving Economics of Ethanol, and the Outlook for Policy Change and Industry Investment

Dermot Hayes

Pioneer Hi-Bred Chair in Agribusiness

Iowa State University

Informa Economics

December 13th Roundtable Meeting

Outline

Based on the CARD studies “Emerging Biofuels: Outlook of Effects on U.S. Grain, Oilseed, and Livestock Markets” and Implied Objectives of Biofuels Subsidies: What are we trying to accomplish?

http://www.card.iastate.edu/publications/synopsis.aspx?id=1050

The objective was to estimate: how large the biofuels sector in the U.S. could become the impact of the biofuels sector on crops markets, trade, and on

livestock markets the response of world agricultural markets What the current level of subsidies suggests about our goals How we should subsidize to achieve our goals

Outline of the first study

After establishing a baseline, we ran a number of scenarios including: high crude oil price with no bottleneck high crude oil price with bottleneck drought with an ethanol mandate removal of CRP land for ethanol production removal of tax credit and import tariff

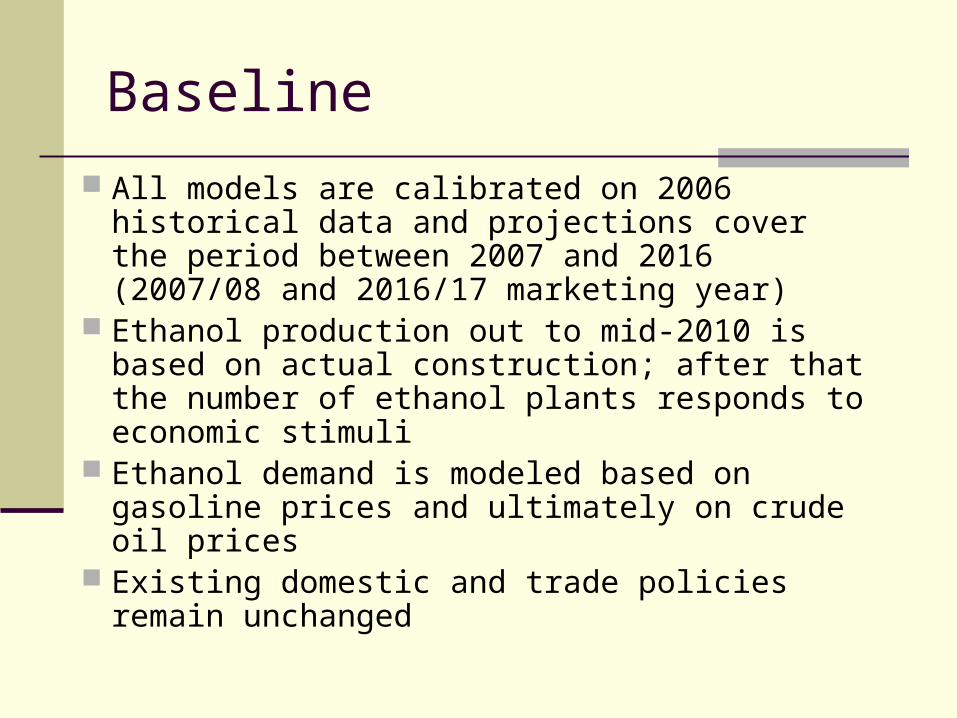

Baseline

All models are calibrated on 2006 historical data and projections cover the period between 2007 and 2016 (2007/08 and 2016/17 marketing year)

Ethanol production out to mid-2010 is based on actual construction; after that the number of ethanol plants responds to economic stimuli

Ethanol demand is modeled based on gasoline prices and ultimately on crude oil prices

Existing domestic and trade policies remain unchanged

Crude Prices are Critical

We used approximately $65 crude in the baseline and $75 crude in the high oil scenario

As of October 16th the NYMEX light sweet crude was almost exactly at the $75 for 2015 delivery

We had anticipated the current ethanol bottleneck and expect retail ethanol to sell at or below its 0.66 energy value for the projection period

Baseline Wholesale Gasoline and Ethanol Prices

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

2006 2008 2010 2012 2014 2016

US$/gallon

Unleaded Gasoline Ethanol

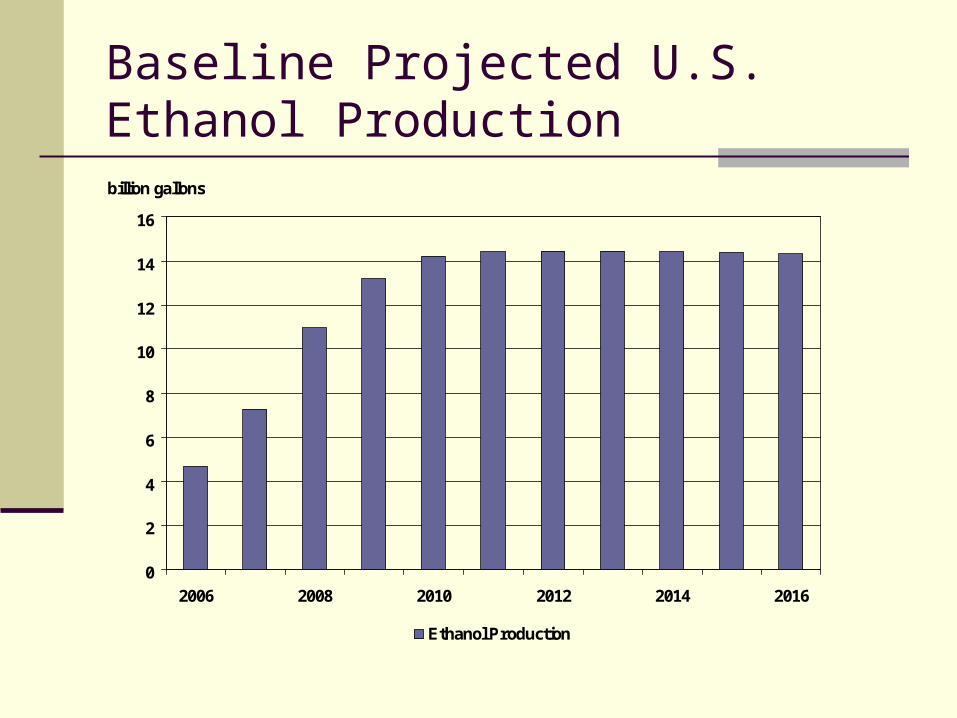

Baseline Projected U.S. Ethanol Production

0

2

4

6

8

10

12

14

16

2006 2008 2010 2012 2014 2016

billion gallons

Ethanol Production

Baseline Projected U.S. Corn Planted Area

70

75

80

85

90

95

2006 2008 2010 2012 2014 2016

million acres

Corn Planted Area

Baseline Projected Utilization of Corn

0

1000

2000

3000

4000

5000

6000

7000

2006 2007 2008 2009 2010 2016

million bushels

Feed Fuel HFCS Seed Food, Other Exports

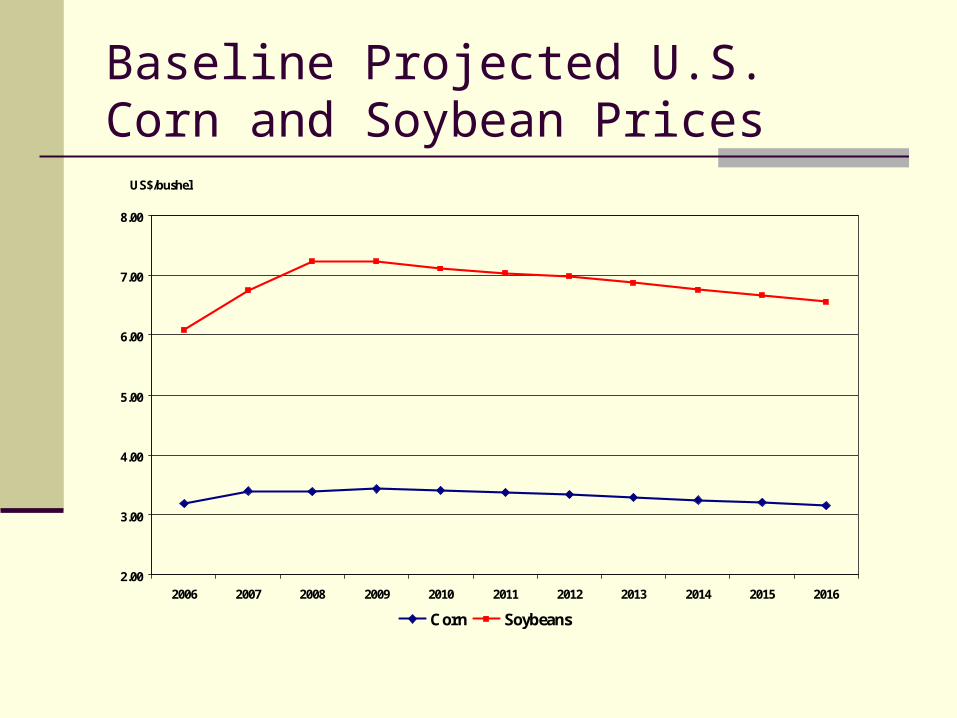

Baseline Projected U.S. Corn and Soybean Prices

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US$/bushel

Corn Soybeans

Baseline Brazilian and Argentine Soybean Planted Area

50.00

60.00

70.00

80.00

90.00

100.00

110.00

120.00

130.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

million acres

Soybean Area

Impact of Higher Crude Oil Price

Increased crude oil price by $10/barrel over the projection Margins on ethanol plants increase New incentive to invest in added capacity for ethanol

production Eventually, a new equilibrium reached where there is no

incentive to invest in or exit the ethanol industry Will demand for ethanol be enough?

E-10 market will saturate around 15 billion gallons Drop in ethanol price will eventually encourage increase in

demand for the flex-fuel cars

Corn Market

Baseline (2016) Long-Run Percentage Change

Corn Price

($/bushel)

3.16 4.43 40.2%

Corn Area

(million acres)

92.5 112.3 21.4%

Corn Production

(million bushels)

14,750 18,038 22.3%

Corn Use in Ethanol (million bushels)

5,046 10,765 113.3%

Corn Feed Use

(million bushels)

5,746 4,914 -14.5%

Corn Exports

(million bushels)

2,451 911 -62.8%

Ethanol and Distillers Grains Markets

Baseline (2016) Long-Run Percentage Change

Ethanol Production from Corn (million gallons)

14,568 29,063 99.5%

Ethanol Consumption

(million gallons)

15,244 29,934 96.4%

Ethanol Wholesale Price (US$/gallon)

1.57 1.91 21.7%

Ethanol Net Imports

(million gallons)

314 337 7.3%

Distillers Grains Production

(thousand tons)

39,758 87,614 120.4

Distillers Grains Price

(US$/ton)

105.81 143.94 36.0%

Distillers Grains Domestic Use (thousand tons)

37,280 63,658 70.8%

Livestock Market

Baseline (2016) Long-Run Percentage Change

Beef Retail Price

(US$/pound)

4.52 4.71 4.2%

Pork Retail Price

(US$/pound)

3.30 3.44 4.2%

Broiler Retail Price

(US¢/pound)

196.07 205.32 4.7%

Turkey Retail Price

(US¢/pound)

126.28 136.96 8.5%

Egg Retail Price

(US¢/dozen)

162.98 177.07 8.6%

Milk Retail Price

(US$/cwt)

14.65 15.44 5.4%

Impact of Short Crop Scenario

Drought in 2012 similar to 1988 Regional yields of corn, soybeans and wheat

changed from trend levels Yields fell by 25% for corn, 18% for soybeans,

11% for wheat Ethanol mandate for 2012 assumed to be 14.7

billion gallons

Corn, Soybean and Ethanol Markets

Corn price increases by 42% above baseline levels Soybean price rises by 22% Corn exports and stock levels decline by more

than 60% Corn exports from South America, China, etc. fill

part of the gap from decline in U.S. corn exports The southern hemisphere gets the “message” in

late July and produces enough to get the world through to the following year

Corn feed use declines by 15%

Other Biofuels

Cellulosic ethanol is not competitive under current policy incentives

The costs associated with baling and hauling stover make it uncompetitive so long as corn is less that $4.80 per bushel

Switchgrass has an additional problem in that an acre of crop ground must be used, the higher the energy price the greater the value of this acre

Biodiesel does not make economic sense under current policy

Why does corn ethanol dominate?

Table 7. Assumptions to obtain the amount of biofuels produced by acre of land and

the payments that would result under the current scheme.

Yields Biofuel production

gal/acre

Current Subsidy*

$/acre

Corn (bu/acre) 153 428 218.5

Soybean (bu/acre) 45 63.1 63.1

Corn Stover (kg/acre) 1600 112 57.1

Switchgrass (kg/acre) 5,000 350 178.5

Well to Wheels petroleum energy use of various fuels in Btus per million btus of fuel produced and used, and associated reduction in fossil energy consumption relative to

gasoline or diesel.

Fuel Technology/ Feedstock

WTP PTW WTW Reduction

Btu/mbtu Btu/mbtu Btu/mbtu

vs. gas./diesel

Gasoline Current 110,000 1,000,000 1,110,000 -

Future 110,000 1,000,000 1,110,000 -

Avg. EtoH Current 100,000 0 100,000 91.0%

Future 90,000 0 90,000 91.9%

New EtoH NG-DDGS 85,000 0 85,000 92.3%

NG-WDGS 85,000 0 85,000 92.3%

Coal-DDGS 90,000 0 90,000 91.9%

Coal-WDGS 90,000 0 90,000 91.9%

Cellulosic EtoH Switchgrass 70,000 0 70,000 93.7%

Corn Stover* 66,600 0 66,600 94.0%

Diesel** 112,196 1,000,000 1,112,196 -

Biodiesel Soybean oil** 129,377 0 129,377 88.4%

GHG emissions of various fuels in CO2-equivalent grams per million btus of fuel produced and used, and percent reduction compared to current gasoline

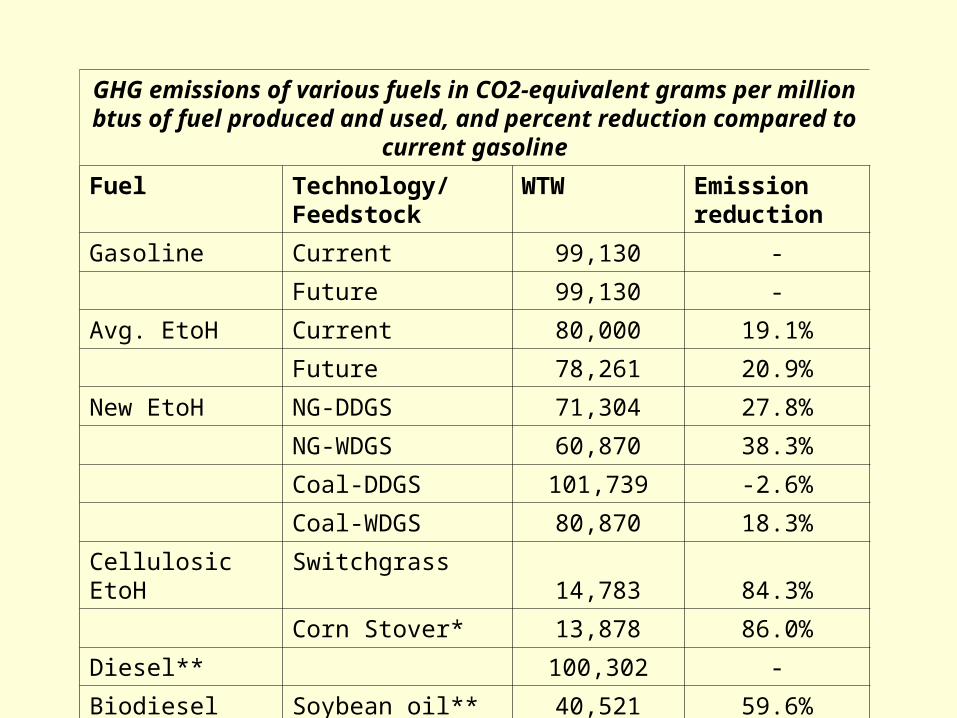

Fuel Technology/ Feedstock

WTW Emission reduction

Gasoline Current 99,130 -

Future 99,130 -

Avg. EtoH Current 80,000 19.1%

Future 78,261 20.9%

New EtoH NG-DDGS 71,304 27.8%

NG-WDGS 60,870 38.3%

Coal-DDGS 101,739 -2.6%

Coal-WDGS 80,870 18.3%

Cellulosic EtoH Switchgrass 14,783 84.3%

Corn Stover* 13,878 86.0%

Diesel** 100,302 -

Biodiesel Soybean oil** 40,521 59.6%

Per gallon compensation needed to provide equivalent subsidies relative to current for based ethanol

FuelTechnology/ feedstock

Fossil Energy

Petroleum Energy

GHG

Avg. EtoH Current 1.000 1.000 1.000

Coal-DDGS 0.865 1.010 -0.136

Cellulosic EtoH Switchgrass 2.461 1.030 4.409

Corn Stover 2.444 1.033 4.456

Sugarcane EtoH Sugarcane** 2.347 1.007 3.697

Biodiesel Soybean oil 2.473 1.588 5.099

Current subsidies for the externalities provided by biofuelsFuel Technology/

FeedstockFossil Energy Reduction

Petroleum Energy Reduction

GHG Emission Reduction

$/mbtu $/mbtu $/ton

Avg. EtoH Current 14.7 6.6 350.8

Future14.5 6.6 321.5

New EtoH NG-DDGS 13.5 6.5 241.2

NG-WDGS 10.4 6.5 175.4

Coal-DDGS 17.0 6.6 -*

Coal-WDGS 11.4 6.6 367.5

Cellulosic EtoH

Switchgrass6.0 6.5 79.6

Corn Stover 6.0 6.4 78.7

Biodiesel Soybean oil 11.7 8.2 134.9

Bottom Line

Crude oil prices will drive ethanol production and ethanol production will drive corn and soybean prices

If crude stays strong, ethanol will continue to grow and will continue to displace animal feed and exports

Whenever corn falls below a breakeven price we will build ethanol facilities to drive it back to that price

We do not expect to see cheap DDGs over the long run Cellulosic ethanol is not ready for commercialization Biodiesel is an industry that is waiting for high crude oil

prices and cheap soybean oil prices this will not happen so long as farmers can chose between corn and soybean production

The current subsidy structure appears designed to foster corn based ethanol

Thank You