the evolution of tax structures

TRANSCRIPT

The Evolution of Tax StructuresAuthor(s): James E. AltSource: Public Choice, Vol. 41, No. 1 (1983), pp. 181-222Published by: SpringerStable URL: http://www.jstor.org/stable/30024041 .

Accessed: 14/06/2014 08:46

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Springer is collaborating with JSTOR to digitize, preserve and extend access to Public Choice.

http://www.jstor.org

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

Public Choice 41: 181-222 (1983) b 1983 Martinus Nijhoff Publishers, The Hague. Printed in the Netherlands

The evolution of tax structures*

JAMES E. ALT **

1. Introduction

Variations in nations' tax structures result from their different economic and political

structures. The first part of this paper establishes a context for studying tax structures.

The next part describes the differences in tax structures which need to be explained. The

idea that a tax structure is at least partly the result of political choice is not especially

controversial. However, there is little agreement on how to account for the choices made

or what the main structural constraints on choice are. The four main sections of this paper

discuss important ideas to which the existing literature pays too little attention. These

include (1) the imperative of redistribution as the motive force in tax reform, and the role

of taxpayer resistance to redistribution; (2) the constraint of administrative costs of

collection and the effect this has on the distribution of direct taxes between households

and business; (3) the relationship between costs of administration and costs of compliance,

and how this affects the choice of tax instruments; and (4) the relationship between fiscal

* I would like to thank my colleagues Randy Calvert, Art Denzau, and Barry Weingast for their advice and criticism. Research for this paper was assisted by the National Science Foundation under grant SES80-06488.

** Department of Political Science, Washington University, St. Louis.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

182

illusion and the inherent uncertainty of incidence of tax structure changes. The argument

is that within the household sector, the demand for redistribution through the tax system

gives rise to resistance which raises the costs of collection of direct taxes. It has become

increasingly easy to collect taxes from organized business rather than from individual

households. Reduced costs of administration raise costs of compliance, in some cases (for

instance, the VAT) by a great deal. Finally, tax expenditures exemplify the way in which

politicians exploit the uncertain incidence of tax innovation. These ideas provide a

framework for the analysis of national differences in taxation in which a major role is

played by the interaction of narrow sectoral interests and public administrative costs, in a

context of uncertainty surrounding the actual effects of major tax reforms.

2. Framework for analysis

To begin with, here is a straightforward view of tax structure evolution:

"Our tax system has evolved historically through a series of compromises and reforms which have attempted, on the one hand, to achieve some level of efficiency and equity while raising a given revenue and, on the

other, have reflected important political forces embodied in special interest groups. But the underlying economic forces which determine the desirability of specific features of our tax laws have changed markedly through time. ...Each of these changes in the economy...put innumerable

pressures on our tax system to change in a direction that increases its

efficiency and equity." (Boskin, 1978, p. 25)

The politics of taxation

The politics of taxation needs more of a framework than disembodied "political forces."

It must incorporate both overt political decisions and behavioral adjustments of individuals

and firms to the tax system. Moreover, efficiency and equity are not obviously the sources

of demand for tax-system changes. Efficiency considerations are important in the sense

that, ceteris paribus, people seek to minimize their share of the deadweight loss caused

by the tax structure. Equity, however, is an ethical constraint on the effects of the most

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

183

common political demand in taxation policy, a desire to shift the burden of a tax onto

someone else. Indeed, this is the purpose of the political activities of special interests.

Taxes always have distributive effects, even if the purpose of taxation varies. Tax-

ation is used as a deliberate instrument for the generation of selective investment incentives,

as in France. Some tax legislation is explicitly used as a deliberate instrument for the redistri-

bution of incomes between broadly defined classes, as in the Swedish tax reform of 1970.

Usually taxes simply finance benefits in the form of expenditures. But one thing is every-

where true: taxation always involves redistribution. That is, tax reform always has some

effect on the distribution of income and wealth.

Therefore, some things will be true of tax politics everywhere. Taxation always

involves conflict. Political institutions adapt to contain conflict. In the United States until

the mid-1970s, the House Ways and Means Committee had broad discretionary powers to

write tax law, and its decisions were as bipartisan as possible (Manley, 1970). The House of

Representatives considered tax bills under a closed rule to prevent the sort of amending for

special interests that happened in the Senate (Reese, 1979). In Sweden, the desire of coa-

lition governments to create supporting majorities led them into policy compromises from

the doctrinaire stances of their principal supporting organizations (Elvander, 1972). Most

decisions about taxes are taken independently of decisions about the expenditures they

finance, that is, in the context of benefits assumed to be unaffected by the actual choice

of taxes. Tax policy is thus a matter of inducing taxpayers to pay more than they otherwise

might wish to pay. Taxation remains a "bad," and so the best thing a politician can do is

to keep the decision out of sight. Any way of distributing tax costs broadly to make them

appear less significant will seem politically desirable. The distribution of taxes is the result

of the pursuit of narrowly perceived interests by special interest groups (Herring, 1938).

Surrey (1971; also Surrey and McDaniel, 1980; McDaniel, 1978) argues that the complexity

of the tax structure arises from the multitude of political actors involved in any legislative

process.

All that suggests that tax structure evolution is in general the outcome of many

small adjustments and narrow reforms. Nevertheless, there are times when major changes

occur in tax structures. New taxes are adopted, old taxes are eliminated or replaced, and

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

184

major changes are made in the administration and collection of taxes. Legislative scholars

have commented on the tendency of tax-structure innovations to coincide with points of

realignment in the party system and occasions when single parties control governorships

and legislatures simultaneously (Hansen, 1978; Portney, 1980). Outside the United States,

the same reasoning suggests that the predominant coalition governments and disciplined

party systems of different European countries produce tax structures which are different

from that produced by the logrolling and interest-group pacification of the American system.

Consequently, the anblyst's basic choice is whether to look at big changes or small

ones. Feldstein (1976) distinguishes between decisions about creation of tax structures

ab initio and decisions about changes in existing structures.1 Big changes like the intro-

duction of a new tax are characterized by increased uncertainty of effect, the activities of

broad coalitions, and the major extra cost of creating a collection bureaucracy. Small

changes are more common. Their politics are dominated by the activity of groups with

narrow perception of interests. Small changes are individually dwarfed in the overall evo-

lution of tax structures by nonpolitical adjustment decisions of individual firms. These

unobservable adjustment decisions are present in the aggregate process of tax structure

evolution. The structure of decision will have common elements in all cases. Saying what

they are requires a close look at two problems: the relationship between taxes and property

rights, and the difference between the politics of taxation and expenditures.

Taxation and property rights

The tax structure of a state is part of what economists call "property rights," the legal

foundations which govern obtainable rates of return from ownership of commodities (see

North, 1981). The structure of taxes is an institution whose existence creates the structure

of opportunities within the economy and, thus, society. A tax is both a claim to ownership

and an extraction of value.2 Nevertheless, a tax must be distinguished from the sort of

1. The importance of Feldstein's elaboration of the theory of second-best is that the optimal move from an existing structure will not necessarily be to - or even in the direction of - what would be the optimal arrangement if there were no pre-existing structure. This is because optimality depends on net costs which involve adjustment to the new tax structure from no structure in the ab initi-o case and a structure to which the economy had adjusted in the reform case, and there is no reason to believe these net costs will be the same, or even distributed similarly, in the two cases. 2. I had thought the roots of the word "tax" lay, like those of "taxonomy," in the Greek "taxis," or "arrangement." Indeed, they do not: the word is derived, via Old French and Middle English, from the Latin "tangere," which means "to touch." Thus, a modern idiomatic rendering of the roots of "to tax" would be "to put the touch upon."

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

185

tributes extracted by the conquerors from the conquered, or, on a note closer to home,

from an act of confiscation. There are three differences between taxation and other forms

of extraction.

First, as historians are fond of pointing out, taxation is inseparable from the ex-

istence of a state. Indeed, it is the price of having a state, whether the resulting society is

civilized or not. The legitimacy of a tax is that of the state that levies and collects it. A

tribute is not a tax because it is not legitimized. Does this mean that no tax can be illegiti-

mate? Not exactly: it means that the answer to the question "Why have a tax?" is the same

as that to the question "Why have a state?" The answer lies in the benefits received by

citizens. This is the second important point about taxes. Taxation is a cost and taxes set

prices. Any calculation about taxation is a calculation about costs incurred and benefits

received. Taxation is implicitly bound up with a conception of exchange. That is, taxation

is a sort of property right exchanged for the promise of some other benefit. The position of

an individual vis-a-vis a tax cannot be considered independent of the benefits the tax is

buying.

Finally, taxation is unlike extraction because it is not arbitrary. It has at its roots, as

Brennan and Buchanan (1980) discuss at length, specific notions of bases and rates. This

legal dimension means that those who pay a tax have clear expectations about consistency

of its application. But some modern usages confuse the issue. Inflation is not a tax (though

it may be a transfer or have effects like those of a tax) precisely because it lacks the legiti-

macy, exchange, and specificity of rates and base which are fundamental to taxes. Similarly,

there is no notion of "taxable income" which has any authority more fundamental than the

present tax code, something often forgotten when people debate the legitimacy of various

"tax expenditures." Uncritical use of the phrase "erosion of the tax base" ignores the fact

that the tax base is an institution underwritten by the law and represents the outcome of

political and social conflict. Whether a limited tax base is eroded or reflects a safely secured

property right is, as in many other matters, a matter of point of view.

Taxes, expenditures, and uncertainty

While there is a long literature on the politics of spending, there is far less on the politics

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

186

of taxation. How do the politics of taxing and spending differ? Since taxes are property

rights, they create a structure of opportunities and are bound up with questions of en-

titlement. This alone makes tax politics different from expenditure politics. Some public

expenditures (especially defense, or at a higher level of abstraction, the enforceability of

contracts) are public goods, indivisible and nonexcludable, and therefore property rights

considerations do not apply. Nevertheless, some expenditures do involve the creation of

opportunities (building roads affects location decisions, etc.). Social entitlement expendi-

tures (for instance, age-related pensions) do not necessarily encourage adjustment, since

one cannot change one's age. Lump-sum taxes are the taxes most like public consumption

expenditures, and entitlement expenditures are the expenditures most like taxation.

The benefits and costs of a tax structure change are uncertain. They are only partially

realized immediately, and more so after a period of adjustment in which one person's bene-

fit depends upon the uncontrollable decisions of others. Of course, expenditures also induce

adjustments. If money is appropriated to build a park, some property values will change,

people will be induced to move, and so on. However, the value of all ultimate adjustments

will be fairly clear at the outset, and the initial capitalization of the benefit will use most

of the ultimate capitalization. A credit against taxes for parks or a tax on the absence of

park land in neighborhoods may result in a park here, or a bigger park somewhere else,

or many small parks, or no parks. Moreover, unlike the expenditure, the tax or credit

becomes part of the law and does not terminate after a few years, so the adjustments

continue. This increases the role of uncertainty and economic adjustment in the evolution

of tax structures.

The imposition of a tax cannot be studied without considering its incidence. At the

time of imposition, however, the incidence is uncertain. The uncertainty is not in what

people want and like, but in who will do what. The class or group advantaged by the tax

may be described, but who actually is in that class may not be absolute. In general, an

innovation will have some immediate effects and more contingent subsequent individual

adjustments to the new structure. These will not be known or anticipatable at the time the

decision is taken. Each person's ultimate costs and benefits depend on others' subsequent

actions, but individuals cannot affect each other's adjustments. The narrower the change in

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

187

tax policy, the more predictable the effects and the less uncertainty matters. However, the

narrower the change, the greater is the gap between it and the broader evolution of differ-

ences in tax structures.

The more uncertain costs and benefits will be more heavily discounted at the time a

decision is taken. Therefore, precisely at the time new taxes are imposed, it is inappropriate

to assume that if one understands the fully adjusted, long-run, ex post incidence of a tax,

one also understands ex ante the demand for that tax. Rather, one should seek to elucidate

how uncertain guesses about subsequent behavior might affect or distort political choices

of tax structure. Indeed, this is precisely the role of political institutions in tax policy.

Political institutions constrain tax decisions in the way the distribution of information

about the inherent uncertainty of tax change effects is capitalized by various policy actors.

3. Analysis of tax structures

What exactly are the differences between the tax structures of various countries? The

concept of tax structure is ambiguously defined. There are at least five ways in which tax

structures can vary. These are:

(1) level of revenue extracted, usually measured as the share of national income or

product taken by public revenues;

(2) shares of total revenue raised by different sorts of taxes, for which a wide variety

of classifications may be used;

(3) centralization of administration, the extent to which revenues are collected by

central or other levels of government;

(4) amount of redistribution achieved by the tax system, measured by comparing the

distributions of pre-tax and post-tax incomes; and

(5) the complexity of the tax system, the different sorts and rates of taxes, and the

range of exemptions from them.

The problem lies in the political differences underlying each of these aspects. There may be

relationships among them. For instance, Cameron (1978) argues that the countries where

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

188

the tax share of national income has grown most rapidly are those which achieve greatest

post-tax equilization of incomes. But redistribution may be achieved by benefits rather

than taxes, regardless of the magnitude of public revenues.

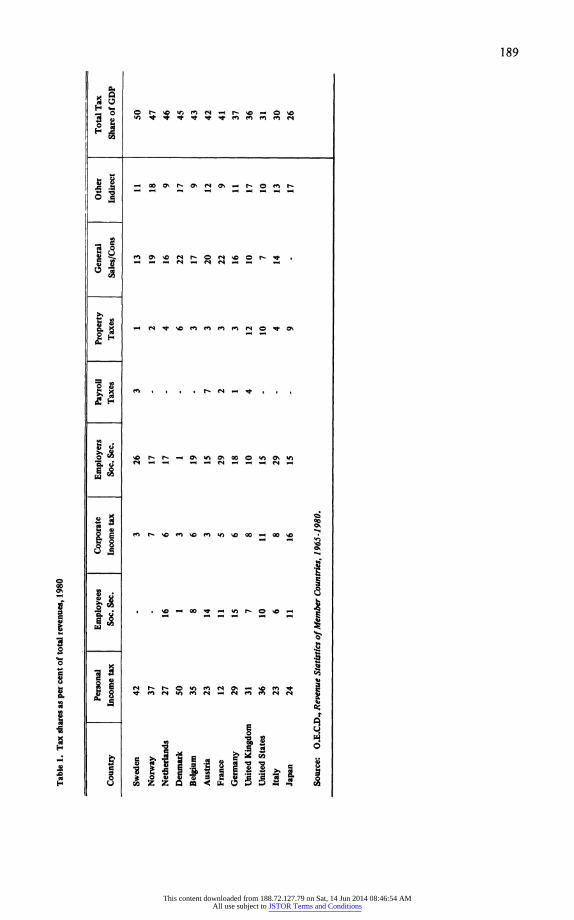

The last century of tax structure evolution has involved trends toward direct taxes

and centralization of revenue collection, with national variation around the trend. Table I

gives the current tax shares of twelve industrial countries, arranged in descending order of

the level of total revenues. The order of these countries has hardly changed since 1970.

The share of GDP taken by tax revenues has grown in nearly all these countries in that

decade. This growth is enlarged by the decline in real economic growth rates. The overall

tax share is also affected by deficits, which in some cases have become substantial.3 One can

observe in the data a slight tendency for the share of personal income tax to be highest

where the overall tax share of GDP is largest, and conversely for the share of corporate

income tax to be highest where the overall tax share is lowest.

Similar countries

One way to simplify the data is to examine correlations among shares to see if clusters of

similar countries appear. Peters (1981, also 1979) does this for seventeen OECD countries

and arrives at four "clusters" of countries.4 The clusters include those countries marked by

"high redistributive effort" (for which read large share of income tax and no employees'

social security contributions), including Sweden and Norway; "large-scale avoidance"

(presuming that administrative difficulties of collection are reflected in a large share of

indirect taxes), including France and Italy; "decentralized systems" (large share of property

tax), including Britain and the United States; and "corporatist systems" (equal shares of

many sorts of taxes), including Austria, Belgium, Germany, and the Netherlands.

Evolution of direct and indirect shares

While this approach captures similarities between countries at one particular time, tax

3. Denmark and Norway trade places and Britain moves from fifth to ninth. In the latter case, the fall in tax revenues is accompanied by a large and sustained increase in government deficits rather than by a fall in expenditures. In both Belgium and Italy, the general government financial deficit for 1980 was over 8 per cent of GDP. Norwegian government had a surplus of over 5 per cent of GDP. 4. Like most cluster analyses, there is no clear criterion to determine the optimal number of clusters to select, and no statistics are provided to assess the internal homogeneity of the clusters.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

189

Table

1. Tax

shares

as per

cent

of total

revenues,

1980

Personal

Employees

Corporate

Employers

Payroll

Property

General

Other

Total

Tax

Country

Income

tax

Soc.

Sec.

Income

tax

Soc.

Sec.

Taxes

Taxes

Sales/Cons

Indirect

Share

of GDP

Sweden

42

-

3

26

3

1

13

11

50

Norway

37

7

17

-

2

19

18

47

Netherlands

27

16

6

17

-

4

16

9

46

Denmark

50

1

3

1

-

6

22

17

45

Belgium

35

8

6

19

-

3

17

9

43

Austria

23

14

3

15

7

3

20

12

42

France

12

11

5

29

2

3

22

9

41

Germany

29

15

6

18

1

3

16

11

37

United

Kingdom

31

7

8

10

4

12

10

17

36

United

States

36

10

11

15

-

10

7

10

31

Italy

23

6

8

29

-

4

14

13

30

Japan

24

11

16

15

9

17

26

Source:

O.E.C.D,

Revenue

Statistics

of Member

Countries,

1965-1980.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

190

structures are rooted in economic and administrative institutions and evolve slowly. Detailed

data on tax shares in a number of countries from Seebohm's (1976) meticulous ten-country,

century-long study are summarized in Table 2. In general, the share of indirect taxes has

been falling over the last century. This trend is clearer if social security contributions are

included as direct taxes. The rates at which this change has taken place vary among

countries. Seebohm argues that there are three separate patterns of tax share evolution.

First, there is the most common European pattern. This involves a sharp rise in indirect

taxation in the later nineteenth century, with a general drift toward direct taxation since

the end of World War I. Sweden, Norway, Netherlands, Austria, Belgium, and Finland

are examples of this pattern, but it is not so clearly evident in the Table. Second, there are

the countries which developed earlier (United Kingdom, Germany). Here the share of

indirect taxes is already as high in 1850 as it would get and it falls steadily after 1890.

Finally, there are France and Italy, where the share of indirect taxes remains consistently

high until quite recently. Increases in direct taxation occur only after World War II.

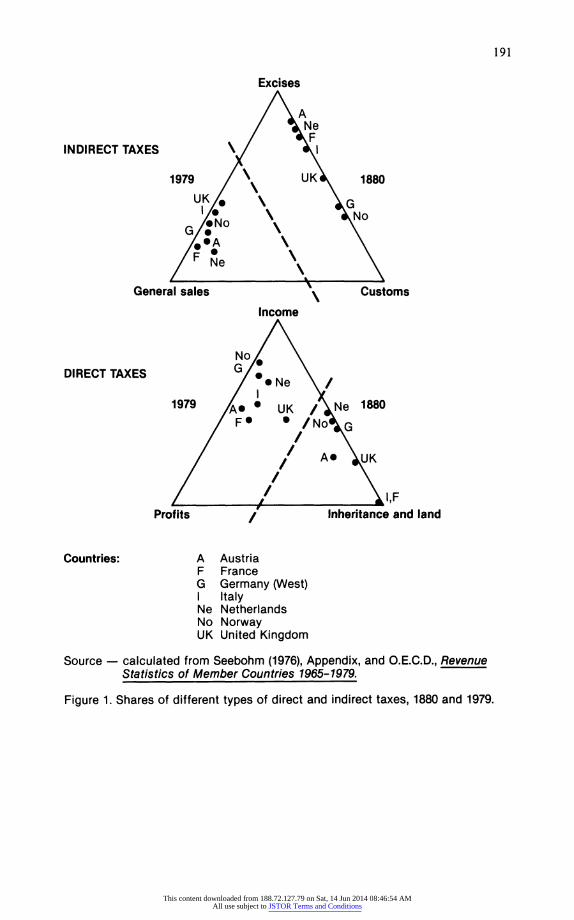

Figure 1 summarizes long-run developments within each type of tax. The main indirect

taxes are customs, excise, and general sales taxes. A century ago, there were only the taxes

on specific commodities, and countries ranged from nearly exclusive dependence on excises

(Austria, Netherlands, France) to heavy dependence on customs (Norway, Germany). The

differences cannot be attributed directly to economic structure. The open economies of

the Netherlands and Austria had excise taxes like the relatively closed economies of France

and Italy. The United Kingdom economy was more open than either Germany or Norway.

A century later, only the most open (the Netherlands) still derives more than a tiny pro-

portion of indirect taxes from customs. The variation in shares between specific excises

and general sales taxes is small. All countries depend more on broader-based, less elastic

general sales taxes.

Direct taxes a century ago were levied on either inheritance or land exclusively (Italy,

France) or largely (all the others). The Netherlands, Norway, and Germany had nearly

reached the point of raising as much revenue from individual income taxes as from the

more traditional sources. Only Austria taxed profits. A century later they all depend princi-

pally on individual income taxes, and all except Britain raise more revenue from taxing

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

191

Excises

A Ne \F

INDIRECT TAXES I

1979 UK 1880 UK G I No No G

A F Ne

General sales Customs

Income

No DIRECT TAXES G

Ne I

1979 1880 A UK Ne F /No G

A UK

SI,F Profits Inheritance and land

Countries: A Austria F France G Germany (West) I Italy Ne Netherlands No Norway UK United Kingdom

Source - calculated from Seebohm (1976), Appendix, and O.E.C.D., Revenue Statistics of Member Countries 1965-1979.

Figure 1. Shares of different types of direct and indirect taxes, 1880 and 1979.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

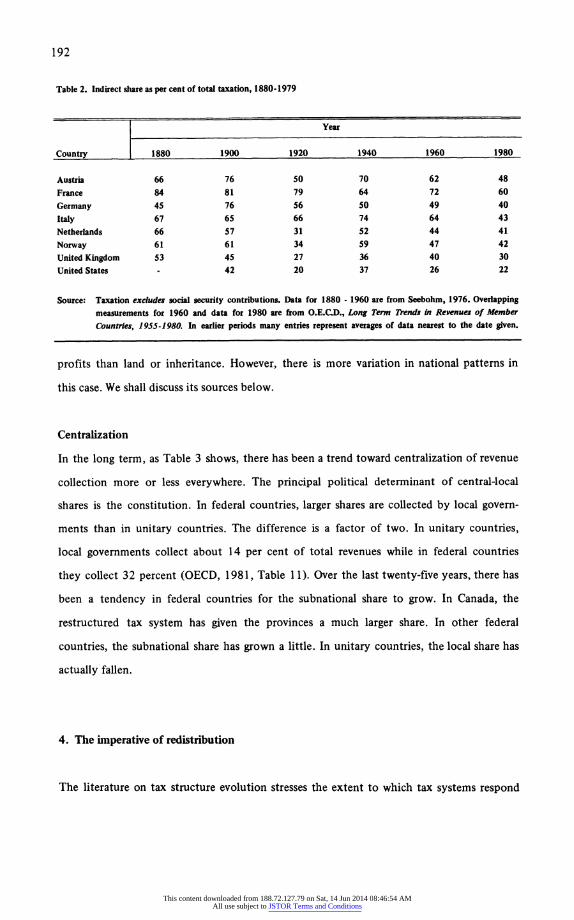

192

Table 2. Indirect share as per cent of total taxation, 1880-1979

Year

Country 1880 1900 1920 1940 1960 1980

Austria 66 76 50 70 62 48

France 84 81 79 64 72 60

Germany 45 76 56 50 49 40

Italy 67 65 66 74 64 43

Netherlands 66 57 31 52 44 41

Norway 61 61 34 59 47 42

United Kingdom 53 45 27 36 40 30

United States - 42 20 37 26 22

Source: Taxation excludes social security contributions. Data for 1880 - 1960 are from Seebohm, 1976. Overlapping measurements for 1960 and data for 1980 are from O.E.C.D., Long Term Trends In Revenues of Member

Countries, 1955-1980. In earlier periods many entries represent averages of data nearest to the date given.

profits than land or inheritance. However, there is more variation in national patterns in

this case. We shall discuss its sources below.

Centralization

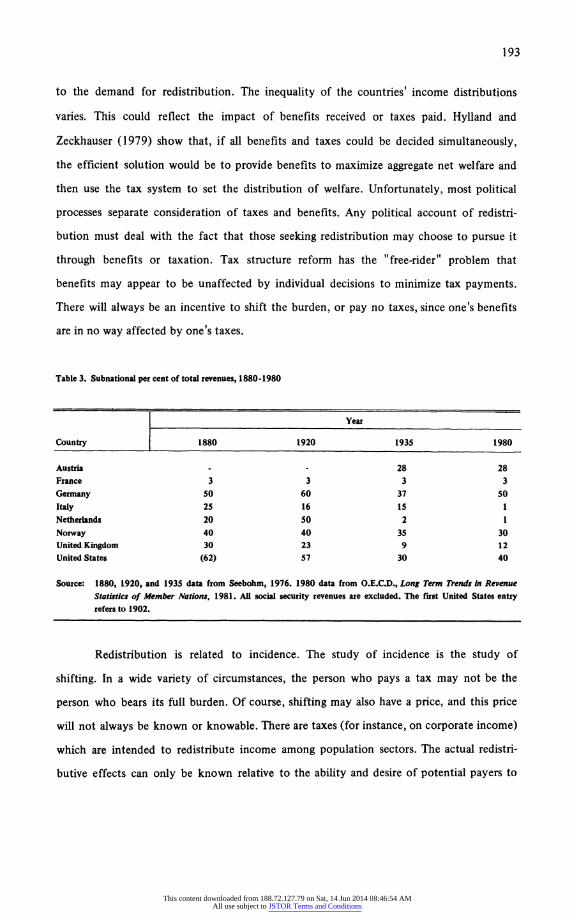

In the long term, as Table 3 shows, there has been a trend toward centralization of revenue

collection more or less everywhere. The principal political determinant of central-local

shares is the constitution. In federal countries, larger shares are collected by local govern-

ments than in unitary countries. The difference is a factor of two. In unitary countries,

local governments collect about 14 per cent of total revenues while in federal countries

they collect 32 percent (OECD, 1981, Table 11). Over the last twenty-five years, there has

been a tendency in federal countries for the subnational share to grow. In Canada, the

restructured tax system has given the provinces a much larger share. In other federal

countries, the subnational share has grown a little. In unitary countries, the local share has

actually fallen.

4. The imperative of redistribution

The literature on tax structure evolution stresses the extent to which tax systems respond

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

193

to the demand for redistribution. The inequality of the countries' income distributions

varies. This could reflect the impact of benefits received or taxes paid. Hylland and

Zeckhauser (1979) show that, if all benefits and taxes could be decided simultaneously,

the efficient solution would be to provide benefits to maximize aggregate net welfare and

then use the tax system to set the distribution of welfare. Unfortunately, most political

processes separate consideration of taxes and benefits. Any political account of redistri-

bution must deal with the fact that those seeking redistribution may choose to pursue it

through benefits or taxation. Tax structure reform has the "free-rider" problem that

benefits may appear to be unaffected by individual decisions to minimize tax payments.

There will always be an incentive to shift the burden, or pay no taxes, since one's benefits

are in no way affected by one's taxes.

Table 3. Subnational per cent of total revenues, 1880-1980

Year

Country 1880 1920 1935 1980

Austria - - 28 28 France 3 3 3 3

Germany 50 60 37 50

Italy 25 16 15 1 Netherlands 20 50 2 1

Norway 40 40 35 30 United Kingdom 30 23 9 12 United States (62) 57 30 40

Source: 1880, 1920, and 1935 data from Seebohm, 1976. 1980 data from O.E.C.D., Long Term Trends in Revenue Statistics of Member Nations, 1981. All social security revenues are excluded. The first United States entry refers to 1902.

Redistribution is related to incidence. The study of incidence is the study of

shifting. In a wide variety of circumstances, the person who pays a tax may not be the

person who bears its full burden. Of course, shifting may also have a price, and this price

will not always be known or knowable. There are taxes (for instance, on corporate income)

which are intended to redistribute income among population sectors. The actual redistri-

butive effects can only be known relative to the ability and desire of potential payers to

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

194

shift the burden of the tax. The desire to shift the burden will depend on the relative costs

of the original burden, shifting, and avoidance.5

If the demand for tax reform is "Don't tax you, don't tax me, tax that fellow

behind the tree," then the demand for redistribution is just "Don't tax me." One cannot

read the history of taxation without being struck by how common the theme was of shifting

the tax burden onto someone else. If the demand for redistribution arises from the distri-

bution of votes being more egalitarian than the distribution of incomes (Meltzer and

Richard, 1981), what tax structure would be created by direct democracy? Unfortunately,

history is not full of examples, but 5th-century B.C. Athens is one such case. The citizens of

Athens voted to pay no direct taxes. They taxed foreigners, they taxed slaves - indeed,

they taxed themselves indirectly, at proportional rates, on consumption and for religious

observances - but no direct taxes (Andreades, 1933). The Prussian aristocrats of the 18th

century paid proportionately little in class tax, compared with the contribution of peasants

and other lower orders. This result owed more to the distribution of power than to the

tastes of the median Junker. Where benefits are not earmarked, "somebody else should

pay" is always a powerful motivation in tax policy.

If taxes were set by simple majority rule and people were confident of their likely

incomes, 50% - 1 taxpayers would find themselves footing the entire tax bill. Indeed, the

history of progressive income taxation is often written in terms of the use of income tax to

fund redistributive social policy.6 The demand for progressivity and the power to make it

stick are two different things, because the existence of representative institutions presents

opportunities for those paying most under progressive taxation to invest in rewriting the

tax structure. Consider a simple system in which taxes are used to provide public goods

which are consumed in proportion to income, but taxes are progressive. The situation is

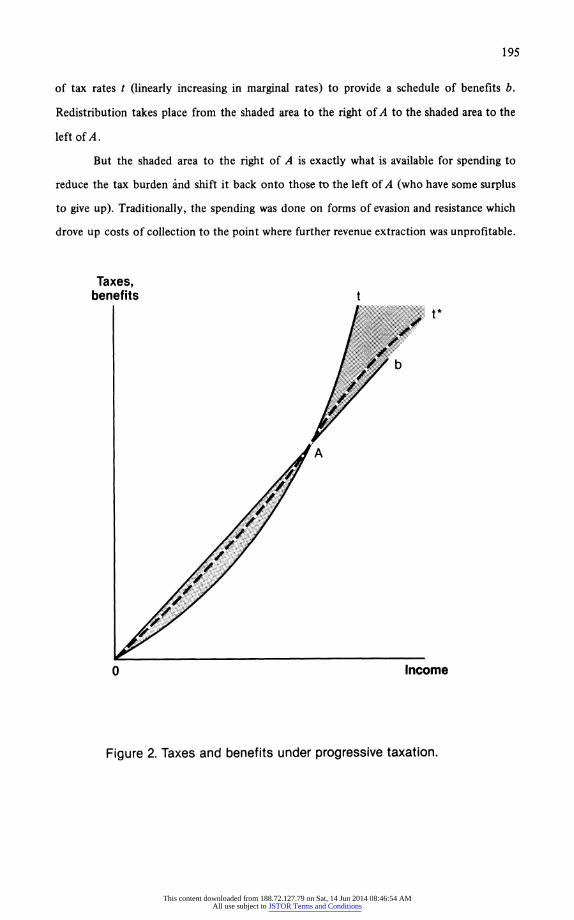

shown in Figure 2. A bare majority of voters lie to the left of point A, and set a structure

5. The demand for redistribution and considerations of equalizing the distribution of incomes are related to the concern of public finance scholars for equity, though equity and equality are by no means the same thing. An equitable tax system treats equals equally, whether the equality is in terms of source or level of incomes. The link between redistri- bution and equity is dissolved by Feldstein (1976), who offers as a redefinition of an equitable tax one which preserves post-tax the pre-tax ordering of incomes or utilities. While this definition speaks commendably to the common idea that the tax system should squeeze rather than re-order incomes (and the problems of measurement are probably not as great as he makes out), the idea that equity means that the most harshly you can treat the second-worst off member of a society is bounded only by the harshness of the treatment of the worstoff is unlikely to find much favor. 6. The US. income tax had progressive rates by 1864, long before any social reform programs.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

195

of tax rates t (linearly increasing in marginal rates) to provide a schedule of benefits b.

Redistribution takes place from the shaded area to the right of A to the shaded area to the

left of A.

But the shaded area to the right of A is exactly what is available for spending to

reduce the tax burden and shift it back onto those to the left of A (who have some surplus

to give up). Traditionally, the spending was done on forms of evasion and resistance which

drove up costs of collection to the point where further revenue extraction was unprofitable.

Taxes, benefits t

t*

b

A

0 Income

Figure 2. Taxes and benefits under progressive taxation.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

196

In the modern world, the resistance takes the form either of structural adjustment or

interest-group activity.7 Its effects can be observed in aggregate data. For instance, Musgrave

(1980) provides a table which shows that in successive decades after major increases in the

progressivity of the American income tax, extra increments of taxation have tended to

return asymptotically to the underlying distribution of income, or proportionality.

But how redistributive are different nations' tax systems, and how is this affected by

resistance? The model requires data on the share of income actually paid in taxes at differ-

ent levels of income in different countries. Define the marginal progressivity p of a tax

system as the rate at which the share of income actually paid in taxes is changing, at some

level of income. For example, at the level of the average production worker's income w,

the taxes paid are t, and the share of income paid in taxes is tw/w.

The marginal pro-

gressivity of the tax system at income w is p, and can be defined as Pw+k/Pw for some

increment of income k, or (tw+klw+k)/(tw/w). The marginal progressivity of the tax

system is determined by the extent to which demands for redistribution are offset by

resistance of those who pay most.

Since political activity requires organization and intervention, it involves fixed costs

as well as returns proportional to activity. If so, the incentive to shift taxes back down the

income scale increases with increasing levels of state activity, or increasing average tax take.

Where the average tax share is low, taxes will increase sharply above the median income.

Where the average tax share is high, ceteris paribus, the potential for resistance is greater,

and marginal progressivity around an average income should be lower. The highest marginal

progressivity at average incomes should exist where the average share is lowest. Moreover,

at lower tax shares the marginal progressivity at average incomes should be high but should

decline sharply at higher income levels. At higher tax shares, the marginal progressivity will

no longer increase above average incomes. These patterns are consistent with the idea of

the best-off investing in forcing a bulge like t* back down the income distribution in Figure

2. If the idea is correct, then those nations with lower tax shares at average incomes should

7. The idea that there is some resistance frequently appears in economic approaches to the politics of taxation. Aumann and Kurz (1977) employ a model in which people can destroy some of their initial endowments as resistance, thus producing a lower aggregate outcome. Frey (1981) provides a model in which high tax rates induce a preference for working in the black or untaxed economy rather than the usual "preference for leisure." Foley (1967) gives examples of tax outcomes in this context which are stable under majority rule decision processes.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

197

display high but decreasing marginal progressivity at that income level. Where tax shares at

average income are higher, the expected pattern is lower but nonincreasing marginal pro-

gressivity.

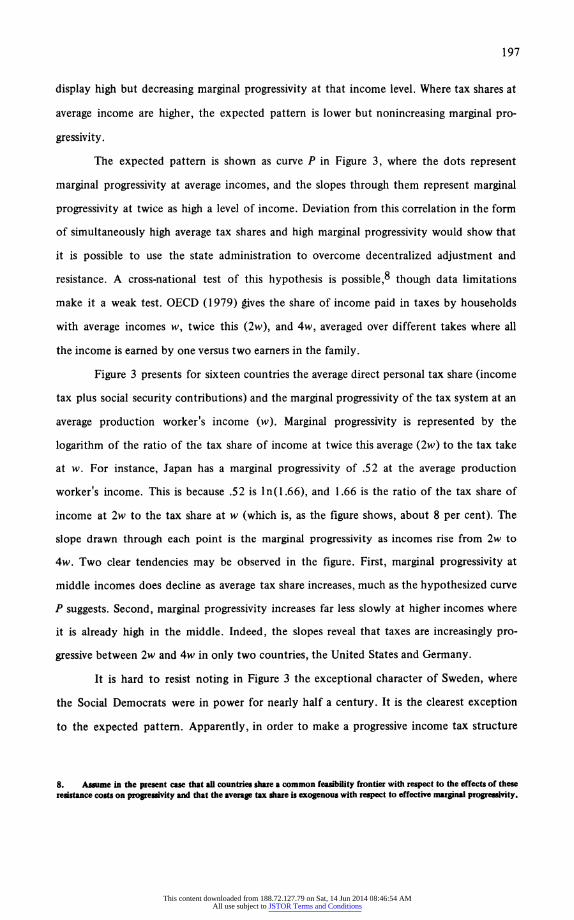

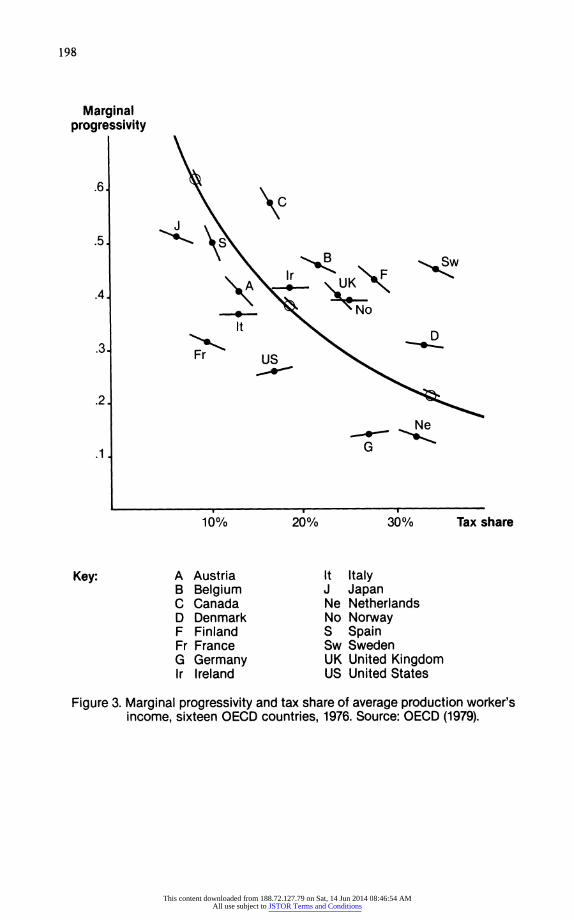

The expected pattern is shown as curve P in Figure 3, where the dots represent

marginal progressivity at average incomes, and the slopes through them represent marginal

progressivity at twice as high a level of income. Deviation from this correlation in the form

of simultaneously high average tax shares and high marginal progressivity would show that

it is possible to use the state administration to overcome decentralized adjustment and

resistance. A cross-national test of this hypothesis is possible,8 though data limitations

make it a weak test. OECD (1979) gives the share of income paid in taxes by households

with average incomes w, twice this (2w), and 4w, averaged over different takes where all

the income is earned by one versus two earners in the family.

Figure 3 presents for sixteen countries the average direct personal tax share (income

tax plus social security contributions) and the marginal progressivity of the tax system at an

average production worker's income (w). Marginal progressivity is represented by the

logarithm of the ratio of the tax share of income at twice this average (2w) to the tax take

at w. For instance, Japan has a marginal progressivity of .52 at the average production

worker's income. This is because .52 is ln(1.66), and 1.66 is the ratio of the tax share of

income at 2w to the tax share at w (which is, as the figure shows, about 8 per cent). The

slope drawn through each point is the marginal progressivity as incomes rise from 2w to

4w. Two clear tendencies may be observed in the figure. First, marginal progressivity at

middle incomes does decline as average tax share increases, much as the hypothesized curve

P suggests. Second, marginal progressivity increases far less slowly at higher incomes where

it is already high in the middle. Indeed, the slopes reveal that taxes are increasingly pro-

gressive between 2w and 4w in only two countries, the United States and Germany.

It is hard to resist noting in Figure 3 the exceptional character of Sweden, where

the Social Democrats were in power for nearly half a century. It is the clearest exception

to the expected pattern. Apparently, in order to make a progressive income tax structure

8. Assume in the present case that all countries share a common feasibility frontier with respect to the effects of these resistance costs on progressivity and that the average tax share is exogenous with respect to effective marginal progressivity.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

198

Marginal progressivity

.6 C

.5 S J

B Sw Ir F

.4 A UK

No

It D

.3 Fr US

.2

Ne

G .1

10% 20% 30% Tax share

Key: A Austria It Italy B Belgium J Japan C Canada Ne Netherlands D Denmark No Norway F Finland S Spain Fr France Sw Sweden G Germany UK United Kingdom Ir Ireland US United States

Figure 3. Marginal progressivity and tax share of average production worker's income, sixteen OECD countries, 1976. Source: OECD (1979).

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

199

stick, a party committed to it must be in continuous control of government for a long

period of time and undertake periodic tax reforms aimed at restoring progressivity. Other-

wise, the idea that progressivity creates the incentive for resistance, subject to the fixed

costs of organized activity, appears to be a universal characteristic of tax politics.

5. Collection costs

The public finance approach

Political Science has concentrated on. the demand for redistribution. In addition, public

finance economists have treated taxation as a problem of collection. The costs of collection

change with the economic development of a country. Thus, the level, structure, and central-

ization of revenues depend on available tax instruments, which are constrained by the

level of social and economic development of a country:

If the availability of tax handles places a constraint on total expenditures in low income countries, it may be expected to do so even more with

regard to the tax structure mix. This constraint again loosens as per capita income rises, and in high income countries the composition of the revenue structure becomes a free policy choice. (Musgrave, 1969, p. 147)

Hinrichs (1966) argues that revenues rise in traditional societies as foreign trade develops,

due to ease of collection. Further domestic development of trade produces excises and

other indirect taxes. Direct taxes follow at high levels of development. Historians of 18th-

century Europe (Ardant, 1975; Braun, 1975) claim that the construction of a state appa-

ratus required the opportunity to reduce costs of collecting taxes which arose through the

growth of internal and external trade in previous subsistence economies. The same pattern,

income and payroll taxes following tariffs and indirect taxes, may be viewed as a drift

toward administrative complexity in taxation (Musgrave, 1969). This literature treats the

growth of direct taxes in the twentieth century as the natural outcome of technological

development.

A major source of demand for revenue growth is the impact of war, which appears

to create a structural break in the processes of fiscal decisionmaking. Peacock and Wiseman

(1961, p. xxxiv) argue

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

200

This displacement effect has two aspects. People will accept, in times of crisis, methods of raising revenue formerly thought intolerable, and the acceptance of new tax levels remains when the disturbance has dis-

appeared. ... At the same time, social upheavals impose new and con-

tinuing obligations on governments both as the aftermath of functions assumed in wartime (e.g., payments of war pensions, debt...) and as the result of changes in social ideas.

However, new methods need not entail higher levels of revenue and may or may not survive

the war. Wars need not coincide with changes in social ideas. A war presents the opportunity

for a state to offer taxpayers a public good (defense) which comprises a benefit whose

magnitude is highly uncertain but most probably large. Moreover, the two instances in

which wars created major and sustained increases in revenues relative to national income

(the United States after World War II and Britain after World War I) owe as much to the

promises of postwar benefits ("a land fit for heroes") to raise a large civilian army to fight

overseas as to any proximate change in social ideas.9

Given sufficient demand for revenues, money will be raised from wherever it is

most readily available. This depends on the resistance of taxpayers, which determines the

administrative costs of collecting the tax. Taxpayer resistance is low when taxes are placed

on essential commodities. In such cases as the salt levy in France (Ardant, 1975), it may be

profitable for the state to erect a large and powerful bureaucratic operation to collect the

tax. This argument explains the taxing of other price-inelastic commodities. The demand

can be imposed by the urgent need to fund a war, as in Napoleon's raising of revenues via

a tax on alcohol (Emerson wrote, "He got five millions from the tax on brandy, and wished

to know which of the virtues would have served him as well"). It can also come from the

need for raising a particular amount in the political context of fine-tuning. The British

government repeatedly undertook deflation in budgets between 1960 and 1974 by raising

excise taxes on alcohol, tobacco, and gasoline while undertaking reflation by reducing

income tax. 10

Moreover, people did not just pay up, as the literature on the evolution of taxes

9. In the aftermath of a war, the probability of another war must increase the amount people want to spend on de- fense. It is clear that more than defense spending increased in these cases. 10. Table 4.2 of Blackaby (1978) lists the budget measures undertaken by British governments between 1960 and 1974. On seven occasions between 1961 and 1974 serious deflation was undertaken with excise tax rates. Four major reflations were carried out, all with income tax, none with excise taxes.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

201

seems to imply. Ardant (1975) describes clearly how the creation of the cadastre system

(local land offices and inspectors who estimated the value of farms and thereby levied direct

taxes on land) led to widespread abandonment of farms where the taxes exceeded the

available profits from farming. Many of the 19th-century American state income and other

direct taxes raised less revenue than they cost to administer (Melichar, 1963) and were

consequently abandoned.11 Their corrupt administration shows how taxpayers in decentral-

ized settings reduce tax outlays by bribes, which tax collectors' agents may accept, lacking

incentives to do otherwise.

Contemporary aspects of collection costs

In terms of the shares of taxes in Table 1, the share of taxes paid by business is now the

largest single source of variation in the tax structures of industrial countries. The growth of

the business share of direct taxes is the most striking feature of Figure 1. The actual burden

of certain taxes paid by businesses can be shifted. However, the tax has to be paid long

before the actual cost net of the shifted burden is known, and there is enough risk involved

in shifting to motivate business resistance to increased tax collection.12

Interest-group theory makes predictions about business participation in tax structure

decisions. Salamon and Siegfried (1977; Coolidge and Tullock, 1980) provide a test of

business tax avoidance which by and large is consistent with the sort of reasoning that

arises from Olson's (1965) predictions about group activity. Their measure of avoidance is

effective tax rates: that is, taxes paid as a fraction of original income. They find greater

avoidance (lower effective rates) in sectors marked by a high degree of concentration of

the median firm. Independent of this, it is reduced in large and decentralized industrial

11. Moreover, the very uncertainty of incidence surrounding a new tax (the American income tax of 1861 is an ex-

ample) can make it attractive as a compromise or "even-split" solution when need for revenues is urgent, but existing taxes have burdens out of proportion to the share of benefits extra taxes can provide. 12. Tax payments are certain while shifting is risky. Employers' social security contributions are made first. Then the

supply and demand of labor, price elasticity of demand for the product, and the possibility of leakage through inter- national competition have their effects on the firm. One can be more confident about the ultimate shifting of employers' contributions (Brittain, 1972) than the corporate income tax (Byrne and Sato, 1976). Shifting corporate tax requires assumptions about elasticities of demand for products, substitution effects, and more. There are also incentives for govern- ments to farm out the collection of taxes to business, provided that the costs to business are matched by incentives to collect the taxes. These include the ability to invest the collected revenues for short periods. These are discussed in the

next two parts of the paper.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

202

sectors. These findings are consistent with the greater ease of organization and excludability

of benefit among concentrated firms in concentrated industries.

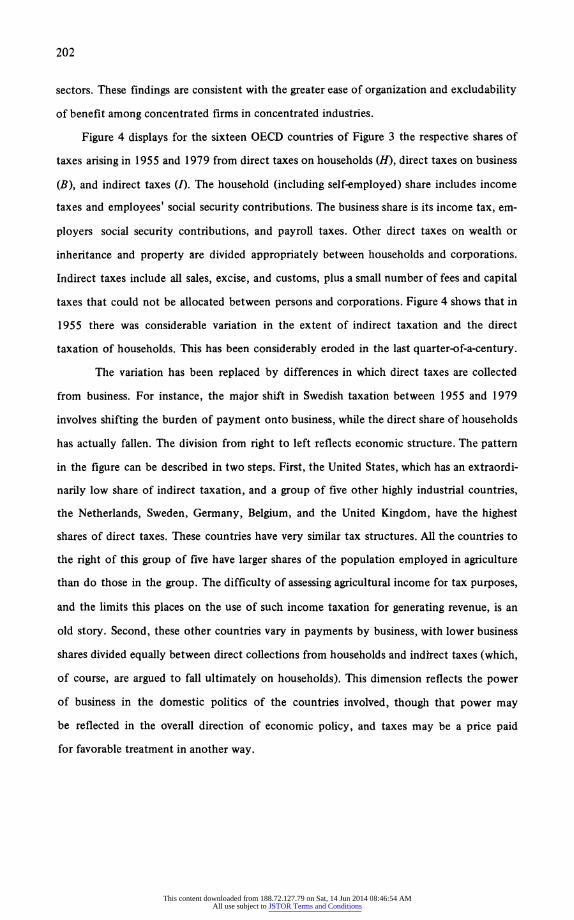

Figure 4 displays for the sixteen OECD countries of Figure 3 the respective shares of

taxes arising in 1955 and 1979 from direct taxes on households (H), direct taxes on business

(B), and indirect taxes (I). The household (including self-employed) share includes income

taxes and employees' social security contributions. The business share is its income tax, em-

ployers social security contributions, and payroll taxes. Other direct taxes on wealth or

inheritance and property are divided appropriately between households and corporations.

Indirect taxes include all sales, excise, and customs, plus a small number of fees and capital

taxes that could not be allocated between persons and corporations. Figure 4 shows that in

1955 there was considerable variation in the extent of indirect taxation and the direct

taxation of households. This has been considerably eroded in the last quarter-of-a-century.

The variation has been replaced by differences in which direct taxes are collected

from business. For instance, the major shift in Swedish taxation between 1955 and 1979

involves shifting the burden of payment onto business, while the direct share of households

has actually fallen. The division from right to left reflects economic structure. The pattern

in the figure can be described in two steps. First, the United States, which has an extraordi-

narily low share of indirect taxation, and a group of five other highly industrial countries,

the Netherlands, Sweden, Germany, Belgium, and the United Kingdom, have the highest

shares of direct taxes. These countries have very similar tax structures. All the countries to

the right of this group of five have larger shares of the population employed in agriculture

than do those in the group. The difficulty of assessing agricultural income for tax purposes,

and the limits this places on the use of such income taxation for generating revenue, is an

old story. Second, these other countries vary in payments by business, with lower business

shares divided equally between direct collections from households and indirect taxes (which,

of course, are argued to fall ultimately on households). This dimension reflects the power

of business in the domestic politics of the countries involved, though that power may

be reflected in the overall direction of economic policy, and taxes may be a price paid

for favorable treatment in another way.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

203

B = Direct Taxes on Business

1955

US UK Ne It

G B J A F C Sw

Ne Ir

D

H = 1= Direct Taxes on Households Indirect Taxes

B

1979 S Fr

US Sw t j

G UK Ne No B A C Ir F

D

H l

Figure 4. Tax shares in OECD countries (key as Figure 3). Source: OECD, 1981a.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

204

6. Administration and compliance

A model of administration and complianice costs

A major trend toward taxation of. business and indeed toward the use of businesses as

collection agents suggests that the costs of collection determine tax system evolution.

Within costs of collection it is possible to distinguish costs of administration and costs of

compliance. While the discussion in general deals only with taxpayers and collectors, ex-

amples will provide specific applications. Under any tax system with well-defined rates,

base, and rules x, each taxpayer chooses a taxpaying strategy y. Each taxpayer then has a

level of outlays Oi(x, y) associated with the tax system and his strategy. He has a level

of costs Ci(x, y) associated with tax system compliance. These costs are actual time and

money spent in either obeying the law or evading taxes. They include costs of keeping

records, paying private tax assistance, and the cost of evading, discounted by the probability

of being caught. There is also a set of costs Li(x, y) associated with the aggregate deadweight

loss caused by the tax structure. This loss may be thought of in a static model as the devi-

ation from an "ideal" tax (disincentive effects, distortions) inherent in the present structure,

and in a dynamic model as both that sort of loss plus the costs of adjustment to the new

system. Any tax structure imposes such costs on taxpayers. The i-th taxpayer's problem is

to make himself as well off as possible by finding the optimal outlay Oi(x, y*), where

y*i = min (Oi(x, y) + Ci(x, y) + Li(x, y)). y

A payer's share of total C and L is not equal to his share of total revenue.

From the point of view of the tax collector there are gross receipts R(x) (identically

equal to O(x, y*) summed over all payers) and costs of administering the tax structure

A(x). The collectors' problem is to maximize net revenues N(x):

N(x) = max (R(x) -A(x).

subject to R(x) = Y Oi(x, y) i

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

205

The maximization assumption may be inappropriate, but the increase in public revenue

shares of national income over the last century suggests that in most concrete situations

the collectors will at least be trying to increase N(x). National differences in tax systems

have often been discussed in terms of mechanisms and costs of compliance and adminis-

tration, although economists less commonly discuss these matters explicitly in considering

tax reform proposals. Every tax has different effects on the distribution of A and C, as well

as on 0 or R and L. In general, we can treat C and A as directly related, while 0 and C are

inversely related.

Administrative costs are the ones which can be directly controlled. There are two

parts to the outlays of government in administering the tax system. One covers the me-

chanics of collecting the revenues. The other makes credible the penalties for tax avoidance

and thus encourages payment. If net revenues are to be maximized, there is an incentive

to shift administrative costs wherever possible, either by farming out collection13 or by

inducing compliance. Usually, taxes which increase costs of compliance also increase costs

of administration, due to increased resistance.

Tax collectors try to maximize (increase) revenue net of the cost of collecting it

(R - A). Clearly, if administrative costs are not directly proportional to revenues, the opti-

mal tax in the presence of administrative costs will not be the same as the optimal tax

without these costs, and need not even be efficient (Heller and Shell, 1974). Any tax other

than a lump-sum tax will be subject to diminishing marginal returns at higher rates, due

partially to distortions and disincentive effects. Similarly, any specific tax will have marginal

costs of administration which increase with tax rates, simply because higher tax rates induce

higher propensity to tax evasion via entry into the underground economy. While in general

average costs of administration are small compared to average revenues, marginal adminis-

trative costs and marginal revenues will meet.14 The costs a payer will bear are a function

of benefits received and the legally prescribed penalties for noncompliance, discounted by

13. The difficulties of administering a new and unfamiliar tax is clearly revealed in the offer made in the American 1861 income tax of a 15% discount in the required contribution to any state that would take over the administration

and collection of the tax. 14. It is useful to note that while the average administrative cost of the American I.R.S. is low relative to income tax

revenues, at the margin the I.R.S. is sometimes unwilling to guarantee that extra administrative expenditure will be self-

financing.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

206

the probability of detection, envorcement, and so on. The corresponding equilibrium for

the payer is when the marginal savings on outlays balance marginal costs of compliance.

Administration and compliance in practice

It is often possible to offset administrative and compliance costs at a profit to the authori-

ties, if the loss in outlays from increased compliance costs is less than the saving in ad-

ministrative costs. This is cited in support of self-assessment in income tax, though it may or

may not be true.15 Countries differ in the degree to which administrative costs are under-

taken. The administrative cost of the German income tax is 4-6 times higher as a proportion

of revenue than in the United States. The money buys closer scrutiny of individual returns,

higher levels of periodic auditing, and a much greater level and tenacity of prosecution for

evasion. The French also underwrite a higher level of bureaucratic activity and intense

personal scrutiny by inspectors, each of whom may have as few as 300 personal payers and

400 corporate payers assigned to him (Heidenheimer et al., 1983). The French system of

allowing small businesses and professionals (about 5 per cent of the work force) to bargain

(without records) with the inspectors over what constitutes their incomes is a case where

marginal administrative costs balance marginal outlays from the point of view of the col-

lectors. The payers accept a reduction in compliance costs in return for a particular level

of outlay.

One of the most remarkable stories of modern tax structure evolution is the wide-

spread and rapid adoption of value-added taxation among European countries. Unused

twenty years ago, it is now a major source of revenue in over a dozen countries. Some

academic discussions of VAT in America find it efficient compared to a corporate income

tax and see it as the basis of a comprehensive expenditure tax. The VAT, however, also

contains an unusual tradeoff between administrative and compliance costs.

The VAT imposes compliance costs without raising administrative costs, through

incentives for self-policing. Each stage in production is liable for taxation on its sales, but

the liability is rebated with respect to the tax incurred in its purchases. Those in the middle

15. The Anglo-American literature confounds the cost of keeping records, borne by the payer even in those systems without selfasessment, with the arithmetic of calculating taxes, which in simple cases even the American authorities will do.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

207

of a production process have an incentive to turn in complete returns of purchases, thereby

policing those who sold to them, since full disclosure reduces their liability regarding sales.

Except retailers, all those who under-report sales bear the cost of being caught if someone

turns them in. The best evidence of the presence of this incentive outside final stage sectors

is Pedone's (1981) data. This shows that the highest rates of evasion of Italian VAT (perhaps

in excess of 50 per cent) are in the heavily retail sectors of "trade" and "construction,"

and the lowest rates of evasion are in "energy" and "manufacturing."16

The compliance costs of VAT are by no means equally distributed. Sandford et al.

(1981) suggest that average costs of complying with the requirements of VAT amount to

about two per cent of total turnover, when time costs of administrative visits are included.

More important, there is an enormous advantage attached to concentration for reducing

compliance costs. It appears that compliance costs increase proportionally to the square or

cube root of turnover. Moreover, costs exceed revenues for traders up to a turnover of about

$100,000, but fall to 2 per cent of revenues for firms with turnovers greater than $2 million.

Multiple rates of VAT further increase compliance costs. Moreover, vertically integrated

firms who control production from beginning to end act as their own policemen.

When the VAT was first adopted in France, it replaced a complex set of business

taxes, so the increase in compliance costs may have been small. The Germans, who had to

be persuaded to accept the VAT as the basis of a harmonized EEC tax system, used it to

replace a complex turnover-based company tax system which also gave advantages to

concentrated, vertically integrated firms (Aaron, 1981). The VAT was sold to much of the

rest of Europe as the price of entry into the EEC. In the early 1970s, political resistance,

especially among the self-employed, arising from compliance costs was overcome with

promises of growth in larger markets available within an enlarged EEC. Elvander (1972)

ascribes the existence of VAT in Sweden to the influence of big business, without further

discussion. Norway does not have the same representation of big business organizations in

politics. It adopted a VAT as the price of joining the EEC, but then turned down the EEC

in a referendum. There has been a campaign since then to abolish VAT, largely led by

16. Hemming and Kay (1981) ignore the probability of detection when they argue that self-policing effects are illusory: "The buyer has an incentive to ensure that an invoice is issued but none to ensure that tax is indeed paid." Nevertheless, they concede, "compliance is high...."

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

208

representatives of small businesses and the self-employed. (Of course, having set up a tax

system, the costs of doing away with it may exceed the benefits, even if it would have

been better never to have set it up at all.) The one country where a VAT has made no

headway at all is the United States, where it is considered that business organizations are

relatively sectorally oriented and decentralized, reducing the overall influence of large

companies vis-a-vis smaller companies in national politics.

7. Fiscal illusion, uncertainty, and tax expenditures

Fiscal illusion and unrest

Are tax structures imposed by collectors in such a way as to minimize popular discontent

among the payers? The history of taxation is to some extent the history of riots, uprising,

and revolution. Of course, in a world restricted to material well-being, rational expectations,

and unbiased, objective perceptions, there is no difference between unrest potential and

the excess burden. Nevertheless, there has always been a tendency to psychologize the

perception of costs (Schmolders, 1970; Lewis, 1982). Fiscal illusion, which causes payers

to underestimate the burden of their tax shares and to exaggerate their share of benefits

received from taxation, is the wellspring of this tradition.

Fiscal illusion is often invoked to explain voluntary compliance with unrewarding

tax systems. But most devices which are argued to produce fiscal illusion merely produce

uncertainty about burden, with no systematic bias towards underestimation.17 But which

institutional forms promote fiscal illusion? Pommerehne and Schneider (1978) suggest

timing, complexity, and visibility. People are unable to assess the future tax costs of debt

and consequently accept a higher burden via debt financing than via taxation. But this is

not illusion. Under any (local) system of producing public goods the possibility of (moving

and) death means that a payer should rationally prefer any capital good, whose costs must

be paid now but which is not consumed all at once, to be financed by debt. The "illusion"

17. There is an enormous literature which one can consult, all cited in Pommerehne and Schneider (1978). To their sources one can add Ordeshook (1979). In more or less all cases it was easier to explain systematic miscalculation and exaggeration of burden than underestimation.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

209

of debt finance is merely the egoistic preference to let someone else pay for the good if

one is not there to enjoy it.18

Fiscal illusion studies often invoke a "law of small numbers" which asserts that

people faced with a number of small tax payments are more likely to underestimate the

total than if they paid one large sum. Information costs might lead to adoption of a rule of

thumb to estimate total costs. But this rule of thumb could as well round up and exaggerate

as underestimate. The argument that fiscal illusion will be present in complex tax systems

is one of the few to find empirical support (Pommerehne and Schneider, 1978; Wagner,

1976). However, both these studies achieve their results by assuming that complexity of

the tax structure is exogeneous with respect to the level of expenditures provided. This

assumption cannot be sustained in view of marginal administrative costs. If ceteris paribus

higher rates of any specific tax produce decreasing marginal returns and increasing marginal

administrative costs, then any social process which (exogenously) produces a higher level

of demand for public expenditure simultaneously produces the possibility of new taxes

and a more diversified tax system.19

Contemporary sociological accounts of tax revolts assert that invisible taxes cause

fiscal illusion. Wilensky (1975) claims that resistance to social reform is higher where taxes

are more visible, and Hanneman (1982) investigates long-run trends toward the use of

invisible taxes. These studies all assume that direct taxes are visible and indirect taxes are

invisible. A receipt with 15-17 per cent VAT added does not make indirect taxes invisible.

The argument that what you do not see does not hurt has face validity, if what one can

and cannot see is clearly specified. A sales tax included in quoted price is relatively invisible.

The general invisibility of indirect taxes rests on the further assertion of the law of small

numbers. Income tax is visible, but income tax withheld at source, like social security

contributions, is not.

Then why do governments which require withholding of income tax not require

prices to be displayed gross of tax? Prices in the United States are always displayed net of

18. Several points are omitted from this discussion that should be developed. First, preferences depend on individual beliefs about the probability of dying or moving. Second, there is the problem that choice of debt or tax finance can be

capitalized. Moreover, note that the illusion is present if the goods provided are currently consumed. 19. The possibility of fixed political and administrative costs in the creation of new taxes makes this an oversimplifi- cation. The demand for expenditure could produce complex taxes as much as the illusion in complex structures produced the demand for excess expenditures.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

210

state sales taxes, though state income taxes are withheld. Federal excise taxes are sometimes

included in prices (gasoline, liquor) and sometimes not (tires, cars). In Europe, VAT is

sometimes included and sometimes not. The preference for price displays net/gross of tax

depends on the structure of the retail trade. If all sectors behave and are taxed alike and we

ignore political boundaries, then retailers incur a small compliance cost in displaying prices

net of tax which may be offset by the fear of losing trade (via superficial comparison of

advertised prices if they displayed gross) to another retailer displaying net. Within a com-

petitive retail sector the stable outcome is probably where all do the same. If all display

gross price, there is a small compliance cost gain to all. However, there will be an incentive

to defect from this situation to capture the extra trade from being the one who displays

net price when others display gross. This could well produce the outcome in which all

display net. The aggregate loss from that outcome means that some amount is available for

a political campaign to require gross display, though the difficulties of organizing a de-

centralized and competitive retail sector may outweigh this gain. The small compliance gain

will outweigh the competitive gain and all will display gross only in monopolistic, concen-

trated, or price-inelastic markets.

The growth of tax expenditures

Fiscal illusion should not require people to make costly errors. However, the uncertainty-

inherent in the incidence of tax reforms allows a sort of fiscal illusion to persist. The

currently fashionable topic of tax expenditures ia a good example of how the political

process determines the way in which uncertainty inherent in tax reform is capitalized. Tax

expenditures now amount to about 30 per cent of the annual American budget and are

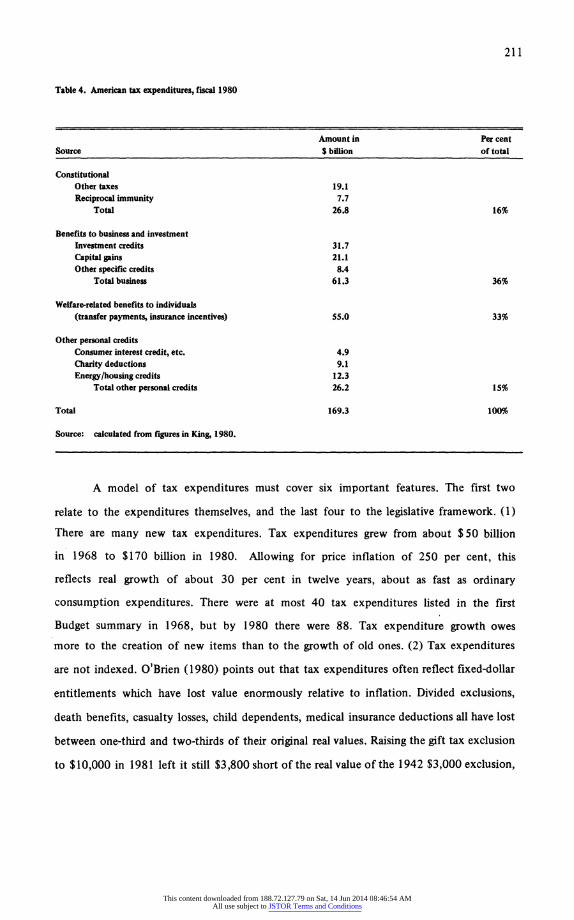

the growth industry of American tax law. Table 4 describes recent American tax expendi-

tures.20

20. Some see tax expenditures as a major source of "uncontrollables" in an out-of-control budget process. Others see them as the hidden hand of corporate power or as the source of unwarranted complexity in the American tax system. Kane (1981) points out that whether one styles them as tax expenditures, loopholes, preferences, subsidies, or incentives is a matter of point of view. What constitutes a tax expenditure is arbitrary. Exclusion of income earned abroad is a tax ex- penditure but credits for taxes on the same income are not, even though individual payers have the choice of which treatment to accept. Tax expenditures as calculated in the Budget ignore second-order effects and thus do not reflect the revenues that would have been collected if the "loopholes" did not exist.

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

211

Table 4. American tax expenditures, fiscal 1980

Amount in Per cent Source $ billion of total

Constitutional Other taxes 19.1 Reciprocal immunity 7.7

Total 26.8 16%

Benefits to business and investment Investment credits 31.7 Capital gains 21.1 Other specific credits 8.4

Total business 61.3 36%

Welfare-related benefits to individuals (transfer payments, insurance incentives) 55.0 33%

Other personal credits Consumer interest credit, etc. 4.9 Charity deductions 9.1 Energy/housing credits 12.3

Total other personal credits 26.2 15%

Total 169.3 100%

Source: calculated from figures in King, 1980.

A model of tax expenditures must cover six important features. The first two

relate to the expenditures themselves, and the last four to the legislative framework. (1)

There are many new tax expenditures. Tax expenditures grew from about $50 billion

in 1968 to $170 billion in 1980. Allowing for price inflation of 250 per cent, this

reflects real growth of about 30 per cent in twelve years, about as fast as ordinary

consumption expenditures. There were at most 40 tax expenditures listed in the first

Budget summary in 1968, but by 1980 there were 88. Tax expenditure growth owes

more to the creation of new items than to the growth of old ones. (2) Tax expenditures

are not indexed. O'Brien (1980) points out that tax expenditures often reflect fixed-dollar

entitlements which have lost value enormously relative to inflation. Divided exclusions,

death benefits, casualty losses, child dependents, medical insurance deductions all have lost

between one-third and two-thirds of their original real values. Raising the gift tax exclusion

to $10,000 in 1981 left it still $3,800 short of the real value of the 1942 $3,000 exclusion,

This content downloaded from 188.72.127.79 on Sat, 14 Jun 2014 08:46:54 AMAll use subject to JSTOR Terms and Conditions

212

which in turn was worth only half of the real value of the original (1932) $5,000 exclusion.

In a world in which there is no shortage of demand for security against inflation in the form

of indexing all sorts of entitlement expenditures and even tax rates, it seems strange that

so many tax expenditures should lose value so fast.

(3) Many of the biggest tax expenditures listed in Table 4 reflect broad entitlements.

Tax expenditures like the investment tax credit were written around broad classes of eligi-

bility. They provide opportunities to many rather than highly specific benefits. This is

inconsistent with the excludability preference of interest groups and suggests the need to

consider models of legislative supply of tax expenditures. (4) However, tax expenditures

are not generally the product of bills like omnibus appropriations legislation. There are

indeed tax relief bills, but they are not commonly packaged into surplus-coalition-type

omnibus measures of the sort discussed by Fiorina and Noll (1978). (5) Many tax ex-

penditures lack the geographic specificity of pork-barrel projects discussed by Shepsle and

Weingast (1981). For instance, Reese's (1979) example of a highly specific tax expenditure

for interstate transit companies turned out upon examination not to have passed the

Congress. (6) Finally, bureaucrats' incentives conflict. The facilitation of bureaucratic

growth argument has less applicability in the case of taxes than benefits. Bureaucrats are

normally styled as wanting to maximize tax receipts, but in the legislator's support calculus

they would be required to assist in the reduction of taxes. Indeed, the tax avoidance indus-

try grows in the private sector, but the public tax bureaucracy is larger where extraction is

more intense.

Assume that in the political context of tax bills, the benefits that will be provided

through public expenditures are fixed and the political cost of extracting the level of

revenue necessary to provide those expenditures is exogenous. Legislators first decide

expenditures, then the level of revenue, and, given that level, how to raise it. Why would a

legislator who could achieve the same final level of revenue choose to do so by offering

broadbased tax expenditures and a higher rate of taxation rather than a lower rate of