the european economic crisis - carleton university · the european economic crisis patrick leblond...

TRANSCRIPT

© Patrick Leblond. 25 November 2013

The European Economic Crisis

Patrick Leblond

Teaching about the EU in the Classroom

Centre for European Studies

Carleton University, 25 November 2013

© Patrick Leblond. 25 November 2013

Outline

• Before the crisis

– European economic integration

– European monetary union

• The European economic crisis

• Conclusion

• Appendix: EU/Eurozone economic governance

© Patrick Leblond. 25 November 2013

EUROPEAN ECONOMIC INTEGRATION

3

© Patrick Leblond. 25 November 2013

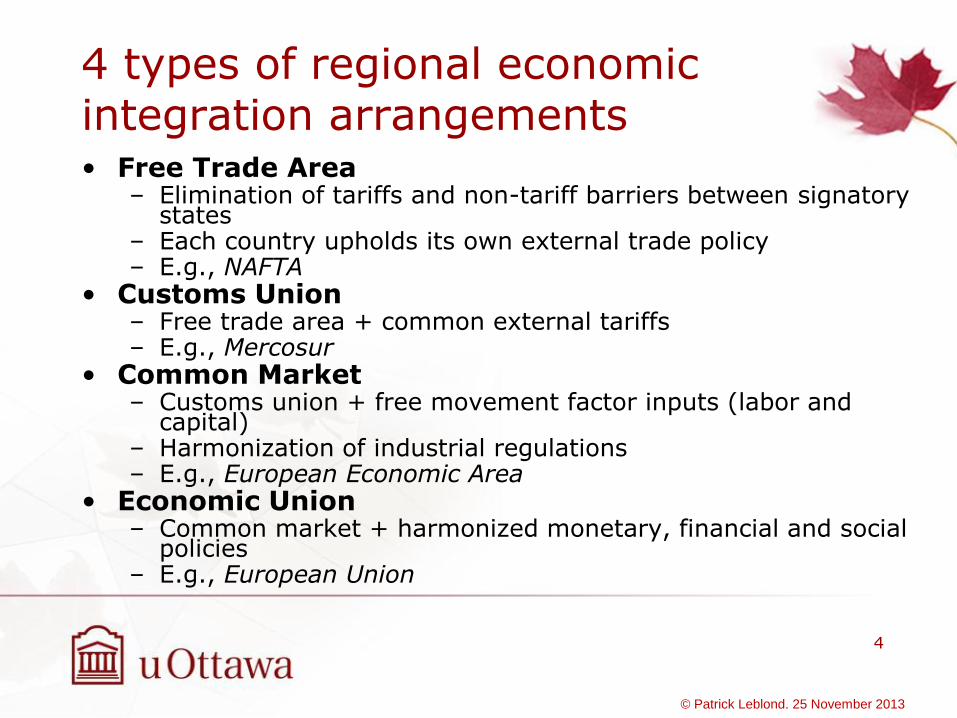

4 types of regional economic integration arrangements • Free Trade Area

– Elimination of tariffs and non-tariff barriers between signatory states

– Each country upholds its own external trade policy – E.g., NAFTA

• Customs Union – Free trade area + common external tariffs – E.g., Mercosur

• Common Market – Customs union + free movement factor inputs (labor and

capital) – Harmonization of industrial regulations – E.g., European Economic Area

• Economic Union – Common market + harmonized monetary, financial and social

policies – E.g., European Union

4

© Patrick Leblond. 25 November 2013

The four freedoms

• Goods

• Services

• Capital

• People

5

© Patrick Leblond. 25 November 2013

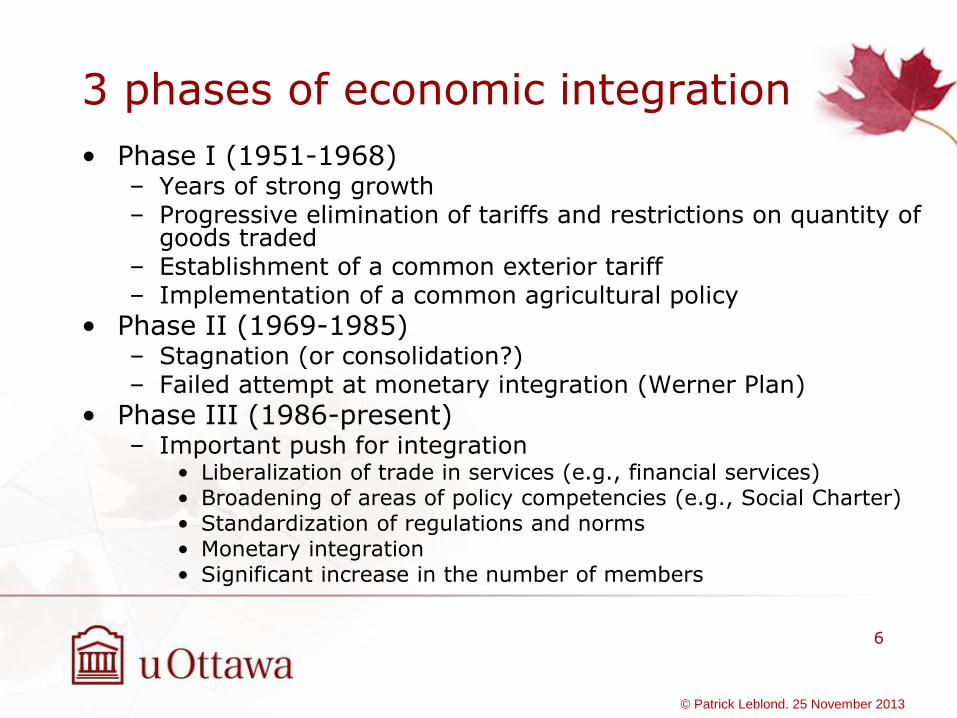

3 phases of economic integration

• Phase I (1951-1968) – Years of strong growth – Progressive elimination of tariffs and restrictions on quantity of

goods traded – Establishment of a common exterior tariff – Implementation of a common agricultural policy

• Phase II (1969-1985) – Stagnation (or consolidation?) – Failed attempt at monetary integration (Werner Plan)

• Phase III (1986-present) – Important push for integration

• Liberalization of trade in services (e.g., financial services) • Broadening of areas of policy competencies (e.g., Social Charter) • Standardization of regulations and norms • Monetary integration • Significant increase in the number of members

6

© Patrick Leblond. 25 November 2013

EUROPEAN MONETARY UNION

7

© Patrick Leblond. 25 November 2013

EMU timeline

• November 1, 1993 – Maastricht Treaty on European Union, signed in Feb. 1992 – Denmark and UK obtain a derogation

• January 1, 1994 – European Monetary Institute – European Commission

• January 1, 1999 – Birth of the euro – European Central Bank – 11 founding members

• January 1, 2002 – Euro notes and coins

• Today – 17 members (Latvia to join on January 1, 2014) – http://www.ecb.europa.eu/euro/intro/html/map.en.html

8

© Patrick Leblond. 25 November 2013

Economic rationale for EMU

• Next logical step after the Single Market • Benefits

– Lower transaction costs – Price stability – Lower interest rates – Lower economic volatility – Lower official reserves – International reserve currency

• Costs – Loss of monetary authority (but was already

very limited)

9

© Patrick Leblond. 25 November 2013

Political rationale for EMU

• France and Italy no longer wanted to follow Germany’s monetary policy leadership

• Provide a credible counterweight to the US dollar

• Bargain between France and Germany

• Anchor Germany more strongly into Europe

10

© Patrick Leblond. 25 November 2013

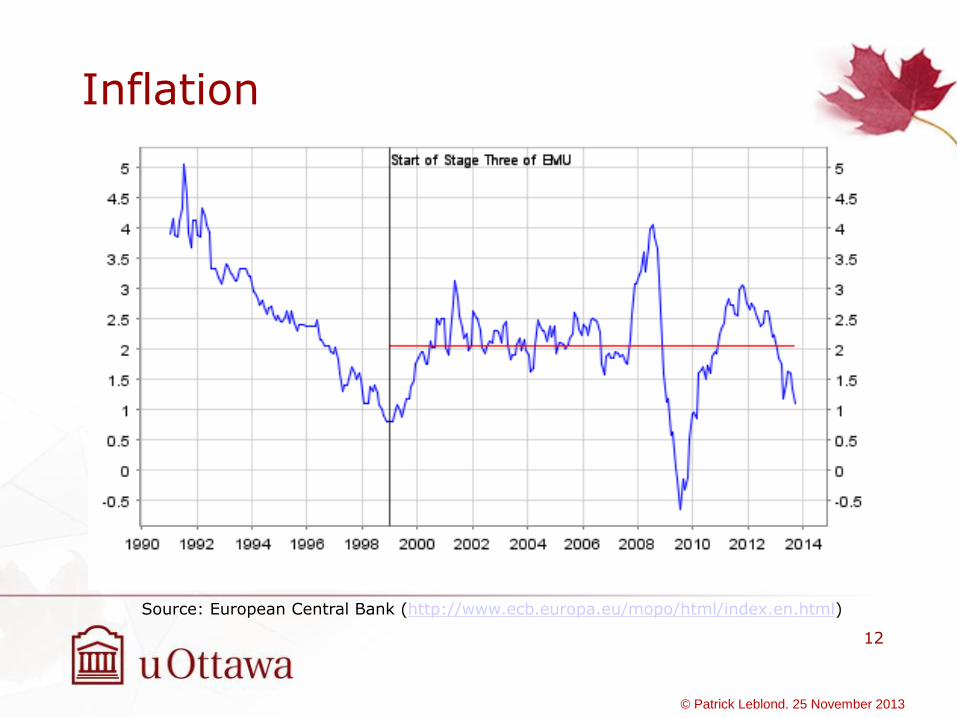

European Central Bank’s mandate

• The primary objective of the ECB’s monetary policy is to maintain price stability

• The ECB aims at inflation rates of below, but close to, 2% over the medium term

11

© Patrick Leblond. 25 November 2013

12

Source: European Central Bank (http://www.ecb.europa.eu/mopo/html/index.en.html)

Inflation

© Patrick Leblond. 25 November 2013

13

Real GDP Growth (by volume)

-5

-4

-3

-2

-1

0

1

2

3

4

5

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013f

%

EU-27 Euro-17

Source: Eurostat

13

Economic growth

© Patrick Leblond. 25 November 2013

14

Source: European Central Bank

14

The euro’s exchange rate vs. the US dollar

© Patrick Leblond. 25 November 2013

THE EUROPEAN ECONOMIC CRISIS

15

© Patrick Leblond. 25 November 2013

Kal’s Cartoon,The Economist, April 28th, 2012

How do we explain this?

16

© Patrick Leblond. 25 November 2013

Two crises, not one!

• The banking crisis

– Government rescue packages

– Monetary rescue by central banks

– Stimulus packages

• The debt crisis

– Market worry about mounting debts

– Panic in the markets

– Rescue operations (Greece and EFSF)

– ECB purchase of sovereign bonds

– Austerity packages

17

© Patrick Leblond. 25 November 2013

Sovereign Debt Crisis: Two Ways

18

Real Estate

Bubble

Bank

Leverage

Cheap

Credit

Bubble

Bursts

Bank

Failures

Bank

Bailouts

Sovereign

Debt Crisis

Fiscal

Deficits

Cheap

Credit

Sovereign

Debt Crisis

Low

Competitiveness

High Public

Debt

Ireland Spain Portugal Italy Greece

© Patrick Leblond. 25 November 2013

Banks & Sovereign Debt

19

Banks

Central

Banks

(ECB)

Member

States

Debt

© Patrick Leblond. 25 November 2013

The banking crisis led to fiscal deficits…

Source: Eurostat

© Patrick Leblond. 25 November 2013

So public debts went up! (But some had a head start…)

Source: Eurostat

21

© Patrick Leblond. 25 November 2013

Greece: A classic debt crisis

• Too much government borrowing in good times

• Fixed exchange rate regime

– Overvalued exchange rate: loss of competitiveness

• External shock

– The global financial crisis slows external demand

• Interest rates begin increasing

– Investors get nervous: higher risk premium

– Self-fulfilling prophecy?

• Debt financing becomes more and more expensive

• “Sudden Stop”: sovereign bond investors panic • EU/IMF bails out the government

22

© Patrick Leblond. 25 November 2013

Ireland: A classic banking crisis that became a debt crisis

• The economy grows very rapidly • Credit is cheap • Banks leverage themselves • People buy real estate and create a bubble • “Sudden stop” in credit • Economy slows down rapidly • Subprime mortgage defaults • Government bails out the banks and guarantees

all deposits • Sovereign bond investors panic • EU/IMF bails out the government

23

© Patrick Leblond. 25 November 2013

Who is to blame? Pretty much everyone!

• The obvious ones:

– Banking regulators in Ireland, Portugal and Spain

– Successive governments in Greece, Italy and Portugal

• But also the less obvious ones:

– Sovereign bond investors

– Germany and France

24

© Patrick Leblond. 25 November 2013

CONCLUSION

25

© Patrick Leblond. 25 November 2013

Market confidence has been improving, but for how long?

26 Source: European Central Bank

10-year sovereign bond yields

Failure of

Lehman Brothers

Greek Debt

Crisis Begins

© Patrick Leblond. 25 November 2013

Recovery takes time… sadly!

• That’s what history teaches us

• Fiscal consolidations are particularly painful when everyone is doing it at the same time

• It is even more difficult when the world economy is sluggish (e.g., China and the US)

• A lower euro might help a bit

© Patrick Leblond. 25 November 2013

The politics may have been messy but they have nevertheless worked

• Crisis management

– European Central Bank and the use of non-standard monetary policy instruments

– European Financial Stability Facility /European Stability Mechanism

• Sovereign (and soon bank) bailouts

• Crisis prevention

– Fiscal compact (completed)

– Banking union (in progress)

– Common bonds/fiscal union (?)

© Patrick Leblond. 25 November 2013

What does it mean for Canada?

• Canada has not been much affected by the euro area crisis

– Our banks had limited exposure to eurozone sovereign debt

– Our exports to the EU have remained relatively stable

• The real risk has been indirect

– Another global recession as a result of a freeze in the interbank credit market

• The dwindling of available AAA financial assets makes it cheap for the federal government to finance its growing debt

• A more economically stable and productive EU can only be good news for the Canadian economy

– Especially in light of the CETA

29

© Patrick Leblond. 25 November 2013

THANK YOU!

30

© Patrick Leblond. 25 November 2013

EU/EUROZONE ECONOMIC GOVERNANCE

APPENDIX

31

© Patrick Leblond. 25 November 2013

EU/Eurozone Economic Governance

• Banking

• Monetary

• Fiscal

32

© Patrick Leblond. 25 November 2013

Banking Governance

• EU-level coordination of national regulators

– European Banking Authority (EBA)

• Banking union for the eurozone (and participating member states)

– Single Supervisory Mechanism (ECB in 2014)

– Single Resolution Mechanism (in progress)

– Direct bank recapitalization by ESM (in progress)

– Single Deposit Guarantee Scheme (not yet)

• Conflicts between the EBA and the ECB?

33

© Patrick Leblond. 25 November 2013

Monetary Governance

• ECB has become a lender of last resort

• Outright Monetary Transactions (OMT)

– “Whatever it takes!” (Draghi, July 2012)

– Must be on an ESM program

– Not used until now (“probably the most successful monetary policy measure in recent times” [Draghi, June 2013])

34

© Patrick Leblond. 25 November 2013

Fiscal Governance (I)

• “Six-Pack”

– EU law (5 regulations and 1 directive)

– Fiscal surveillance (strengthen the Stability and Growth Pact)

– Macroeconomic imbalance surveillance

• Treaty on Stability, Coordination and Governance

– Intergovernmental treaty not part of EU law (17 eurozone members + 8 other EU members)

– “Fiscal Compact”

– Also includes reinforced surveillance of coordination of economic policies

35

© Patrick Leblond. 25 November 2013

Fiscal Governance (II)

• “Two-Pack”

– EU law (2 regulations)

– Euro area supplementary budgetary coordination and surveillance (beyond the Six-Pack)

– Enshrines parts of TSCG into EU law

• European Stability Mechanism (ESM)

– Permanent bailout fund for eurozone member states

• Eurobonds?

– Mutualization of eurozone sovereign bonds (in part or in whole)

– Only once the other fiscal governance measures have proved effective

36

© Patrick Leblond. 25 November 2013

Two-Pack

fits here

European Semester