the european 3pl market a brief analysis of...

TRANSCRIPT

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

1

The European 3PL Market A brief analysis of eyefortransport’s recent survey

September 2008

For further details please contact: Chris Saynor - eyefortransport Email: [email protected] Telephone: +44 20 7375 7529 US Toll Free: 1 800 814 3459 ext 209

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

2

Table of Contents

I Introduction .....................................................................................3

II Survey overview..............................................................................4

III Profile of respondents .....................................................................4

IV Impact of the economic downturn ...................................................5

V Combating the global economic crisis.............................................7

VI Potential growth per geographic region ..........................................9

VII How are 3PLs shaping up? ...........................................................10

VIII Choosing a new 3PL .....................................................................12

IX Contract renewal ...........................................................................13

X How green is your 3PL?................................................................14

XI 6th eyefortransport European 3PL Summit 2006..........................16

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

3

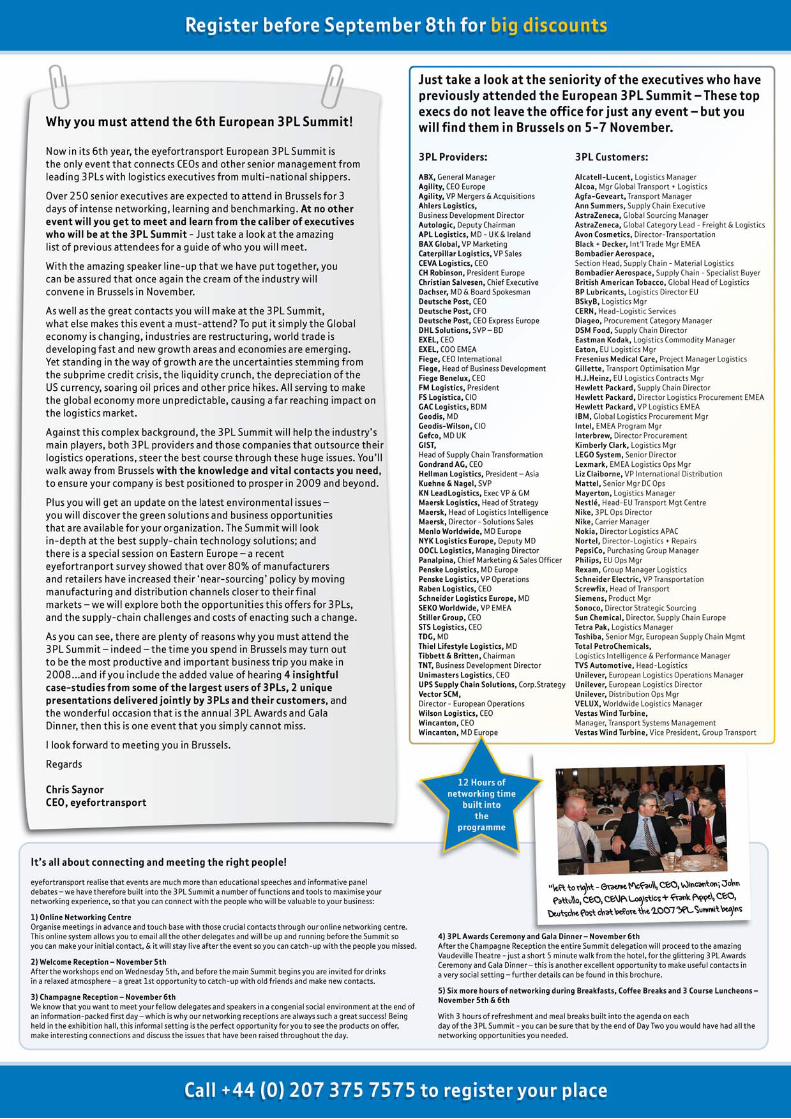

I Introduction There have been inevitable shifts in perceptions and predications relating to the 3PL industry since our European survey of two years ago, but the broad picture remains essentially the same. Issues that players in the industry considered to be of the greatest importance in 2006 are still regarded as the important issues of today. This report expands on the 2006 report by analysing new areas of concern for 3PLs and their customers in Europe, and the differences between the 3PL’s perspective and that of the client. The 3PL industry continues to evolve, and trends continue to validate the role of the 3PL in all aspects of logistics. As businesses diversify and their supply chains become increasingly complex and fragile, more and more of them are outsourcing their logistics in order to ensure economical, reliable and efficient deliveries from their suppliers and to their markets. It has become almost a maxim of commerce that a 3PL should be not merely a contractor, but in many senses also a business partner. Merely validating the role of 3PLs does not imply that they will be successful. Competition among 3PLs has become intense. Many have resorted to consolidation so that they can expand their capabilities across sectors and regions. Consolidation may help the larger 3PLs to overcome fragmentation and claim a bigger slice of the market. For smaller companies, consolidation may be crucial to their very survival. Mergers and acquisitions remain high on the agendas of 3PLs. However, consolidation can be a doubled-edge sword; while it may strengthen a company’s position, it can also turn that company into a target. The hard truth of evolution applies as much in business as it does in nature – survival of the fittest. In an effort to establish the nature of the current challenges faced by the European 3PL industry, eyefortransport conducted the European 3PL Market Survey during July-September 2008. Much of the data gathered in the survey will be discussed and debated at the 6th eyefortransport European 3PL Summit 2008, which takes place on November 6-7 Brussels. For more information on the eyefortransport survey results or the conference, contact Chris Saynor: email [email protected] or call +44 (0) 207 375 7529 (or US Toll Free on 1 800 814 3459 ext 209).

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

4

II Survey overview The survey was conducted via the Internet, with responses solicited by targeted e-mail lists, select trade association memberships, various related-industry databases and other targeted methods. No individual responses were analysed, but rather all responses were consolidated. The aim of the survey was to identify the main challenges for European 3PLs, as well as the best potential opportunities in the different geographical regions and the impact on operations of the current global economic downturn. Respondents were asked a number of questions to establish the key criteria for choosing a 3PL as well as the main reasons for non-renewal of 3PL contracts. It is interesting to see the difference between what is important to the client and what the 3PL thinks are the client’s priorities.

III Profile of respondents participating in the survey More than 400 logistics professionals from 3PLs, freight forwarders, carriers, warehouse operators, shippers, consultants and technology providers responded to the survey.

Primary business of respondents

3%2%2%2%1%

1%

2%

4%

83%

Automotive FoodChemicals Healthcare / pharmaceuticalHi-tech / electronics / telecoms RetailConsumer packaged goods / FMCG Other industrial3PL

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

5

IV The impact of the economic downturn

Respondents were asked whether their business operations have been negatively impacted by the current economic slowdown, and whether the global economic downturn will affect their business growth over the next twelve months.

40% of the respondents said that their business operations have already been negatively affected by the economic slowdown. Almost half of these companies report annual revenues of more than €1 billion.

Respondents' annual revenues

39%

9% 12%

40%

Less than €50m €50m - €250m €250m - €1bn More than €1bn

Business operations impacted by economic slowdown

40%

30%

30%

Yes No Not yet

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

6

More than half of the respondents said they expect their companies’ growth to be slower than originally forecast, and 12% said they don’t expect to show any growth at all.

Interestingly, the companies least concerned about the immediate future are those with annual revenues of more than €1 billion, with only 7% saying their growth will either remain static or decline.

Overall, the global economy is expected to start recovering sometime in 2009, according to just over half of the respondents, and in 2010 according to a third.

Effects of economic downturn in next 12 months

28%

55%

12%

5%

Our growth will be as strong aspreviously predicted

Our growth will be slower than originallypredicted

We are unlikely to show any growth

We expect our revenues to decline

Expected global economic turnaround

5%

23%

32%

32%

8%

By end-2008

By mid-2009

By end-2009

During 2010

2011 and beyond

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

7

V Combating the global economic crisis When asked what measures they are taking to combat the challenging global economic conditions, more than half of the 3PLs said they are terminating existing unprofitable accounts and being very selective with new customer accounts. Less than half of the 3PLs are focusing on core markets, while just over one-third are diversifying their product offerings. 20% of the 3PL respondents said they are reducing planned expansions. In fact, 14% are outsourcing company-owned warehouse space and 13% are reducing staff levels. Almost one-third of 3PLs are looking for strategic mergers and acquisitions. While one-third of the 3PLs say they are negotiating lower prices with contractors, less than 10% are cutting prices for their customers. Contrary to the growing trend of sourcing from or outsourcing to low-cost countries, 80% of 3PLs surveyed said that their customers are moving production and sourcing closer to their home markets.

3PLs' measures to combat economic conditions

9%

13%

14%

20%

32%

33%38%

43%

54%

51%

74%

6%

Reducing costs through other internal efficiencies

Terminate existing unprofitable accounts

Being selective with new customer accounts

Focusing on core markets

Diversifying product offering

Negotiating lower prices with contractors

Looking for strategic mergers and acquisitions

Reducing expansion plans

Outsourcing company owned warehousing space

Staff reductions

Cutting prices for our customers

Other, please specify

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

8

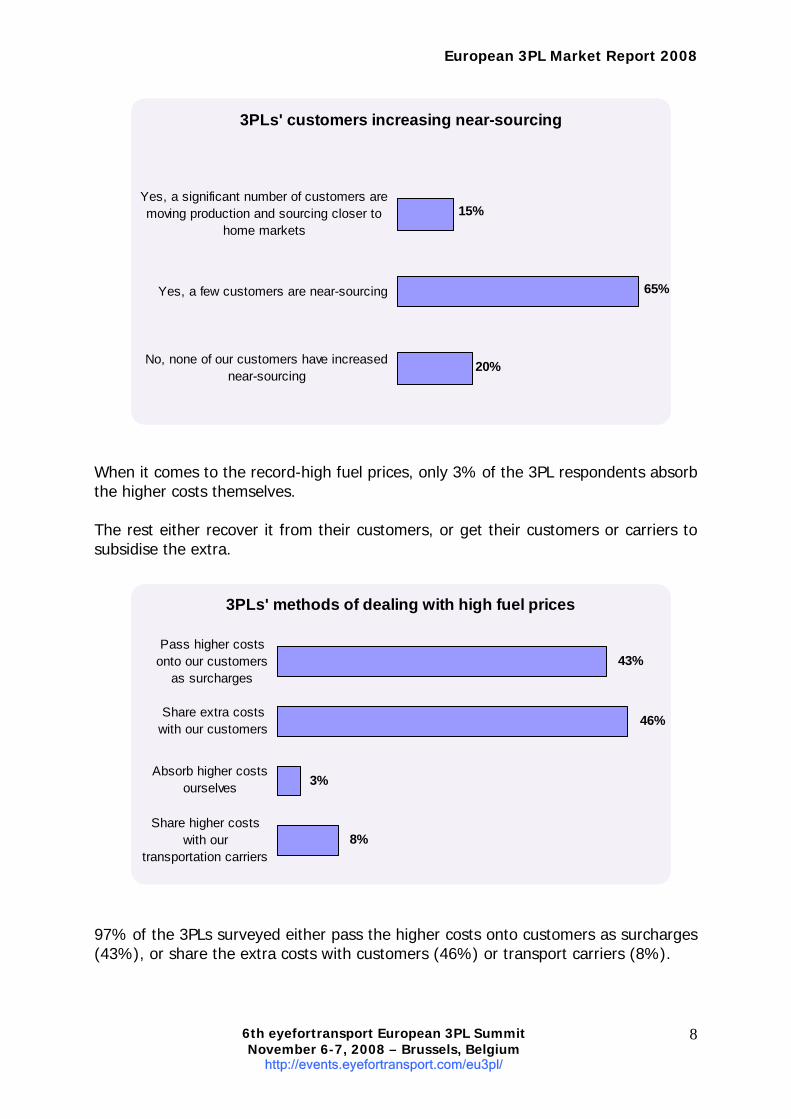

When it comes to the record-high fuel prices, only 3% of the 3PL respondents absorb the higher costs themselves. The rest either recover it from their customers, or get their customers or carriers to subsidise the extra. 97% of the 3PLs surveyed either pass the higher costs onto customers as surcharges (43%), or share the extra costs with customers (46%) or transport carriers (8%).

3PLs' methods of dealing with high fuel prices

8%

3%

46%

43%Pass higher costs

onto our customersas surcharges

Share extra costswith our customers

Absorb higher costsourselves

Share higher costswith our

transportation carriers

3PLs' customers increasing near-sourcing

20%

65%

15%Yes, a significant number of customers aremoving production and sourcing closer to

home markets

Yes, a few customers are near-sourcing

No, none of our customers have increasednear-sourcing

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

9

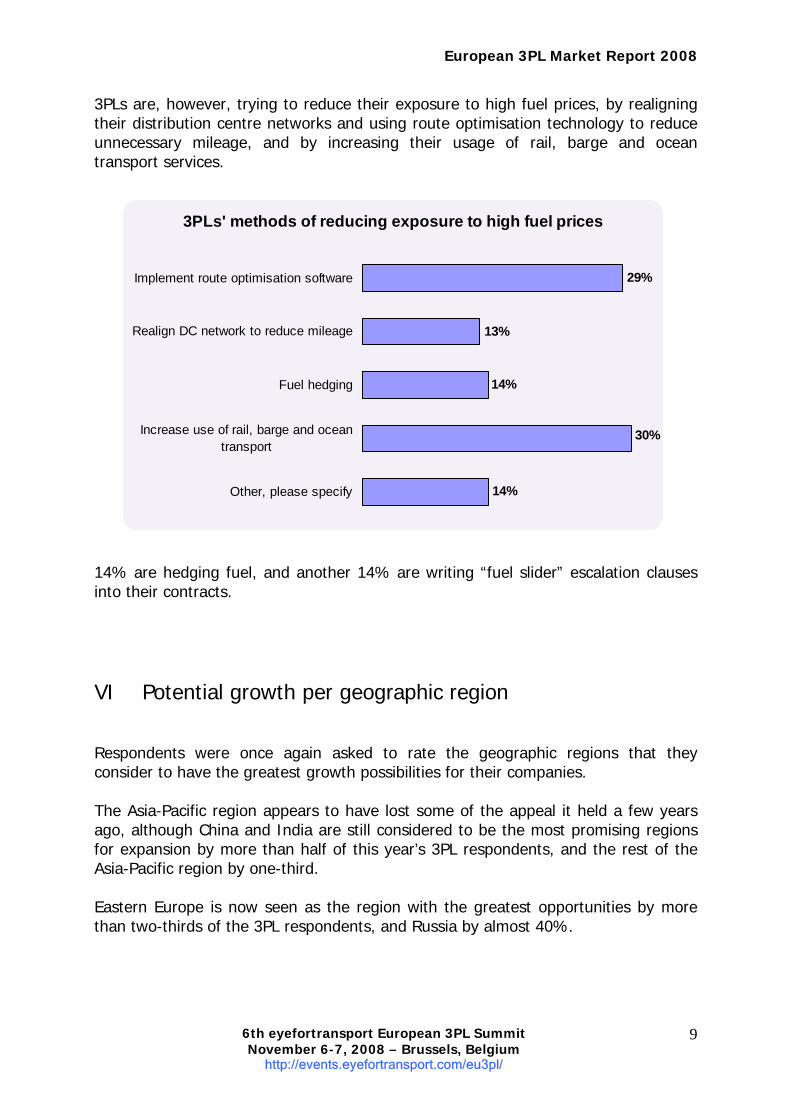

3PLs are, however, trying to reduce their exposure to high fuel prices, by realigning their distribution centre networks and using route optimisation technology to reduce unnecessary mileage, and by increasing their usage of rail, barge and ocean transport services. 14% are hedging fuel, and another 14% are writing “fuel slider” escalation clauses into their contracts.

VI Potential growth per geographic region Respondents were once again asked to rate the geographic regions that they consider to have the greatest growth possibilities for their companies. The Asia-Pacific region appears to have lost some of the appeal it held a few years ago, although China and India are still considered to be the most promising regions for expansion by more than half of this year’s 3PL respondents, and the rest of the Asia-Pacific region by one-third. Eastern Europe is now seen as the region with the greatest opportunities by more than two-thirds of the 3PL respondents, and Russia by almost 40%.

3PLs' methods of reducing exposure to high fuel prices

14%

29%

13%

14%

30%

Implement route optimisation software

Realign DC network to reduce mileage

Fuel hedging

Increase use of rail, barge and oceantransport

Other, please specify

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

10

South America, Western Europe and Africa are considered to have limited potential, but North America and its collapsing economy has dropped to the bottom of the list.

VII How are 3PLs shaping up? Only 17% of the survey respondents use the services of a 4PL.

Regions with greatest opportunities for 3PLs

61%

55%

32%

67%

39%

17%

6%

22%

14%

China

India

Asia-Pacific (not China or India)

Eastern Europe

Russia

Western Europe

North America

South America

Africa

Clients using the services of a 4PL

17%

83%

Yes No

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

11

More than half of the 3PL clients who responded to the survey use the services of four or more 3PLs, and almost one-quarter spread their business amongst more than eleven different 3PLs. Almost three-quarters of the respondents rated their 3PLs’ performance as “good”, and 8% said performance levels are higher than expected. However, a full 20% of respondents are receiving service that does not meet their expectations.

Different 3PLs used

7%

44%22%

27%

1-3 4-6 7-10 More than 11

Clients' rating of 3PLs' performance

72%

20%8%

Higher than expected Good Lower than expected

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

12

Despite this, 95% of the respondents said they are likely or very likely to increase their usage of 3PL services.

VIII Choosing a new 3PL All the survey respondents were asked to rate a number of criteria that shippers use when making the decision to choose a new 3PL. Roughly one-quarter of the 3PLs believe that contracts are awarded to the 3PL who offers (a) the best service, (b) the lowest price, and (c) has the relevant sector expertise.

Criteria for choosing a new 3PL - The 3PLs' perspective

27%

26%

25%

9%

6%

17%

26%

17%

11%

23%

18%

25%

14%

14%

29%

15%

15%

14%

12%

25%

7%

13%

26%

13%

12%

7%

26%

19%

20%

10%

12%

18%

24%

16%5%

4%Best quality service

Lowest price

Sector expertise

Size and scope of 3PL

Geographic expertise

Reputation / testimonials

1 Most important 2 3 4 5 6 Least important

Clients who will increase usage of 3PL services

5%

45%50%

Very likely Possibly Unlikely

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

13

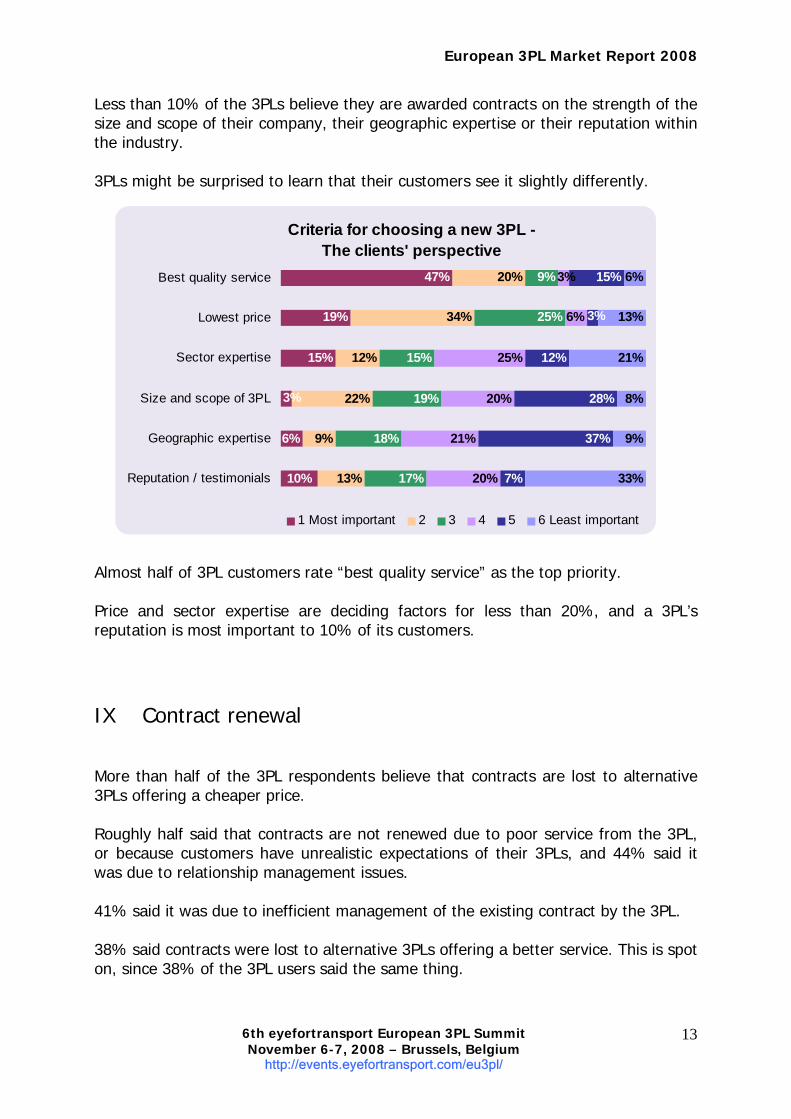

Less than 10% of the 3PLs believe they are awarded contracts on the strength of the size and scope of their company, their geographic expertise or their reputation within the industry. 3PLs might be surprised to learn that their customers see it slightly differently.

Almost half of 3PL customers rate “best quality service” as the top priority. Price and sector expertise are deciding factors for less than 20%, and a 3PL’s reputation is most important to 10% of its customers.

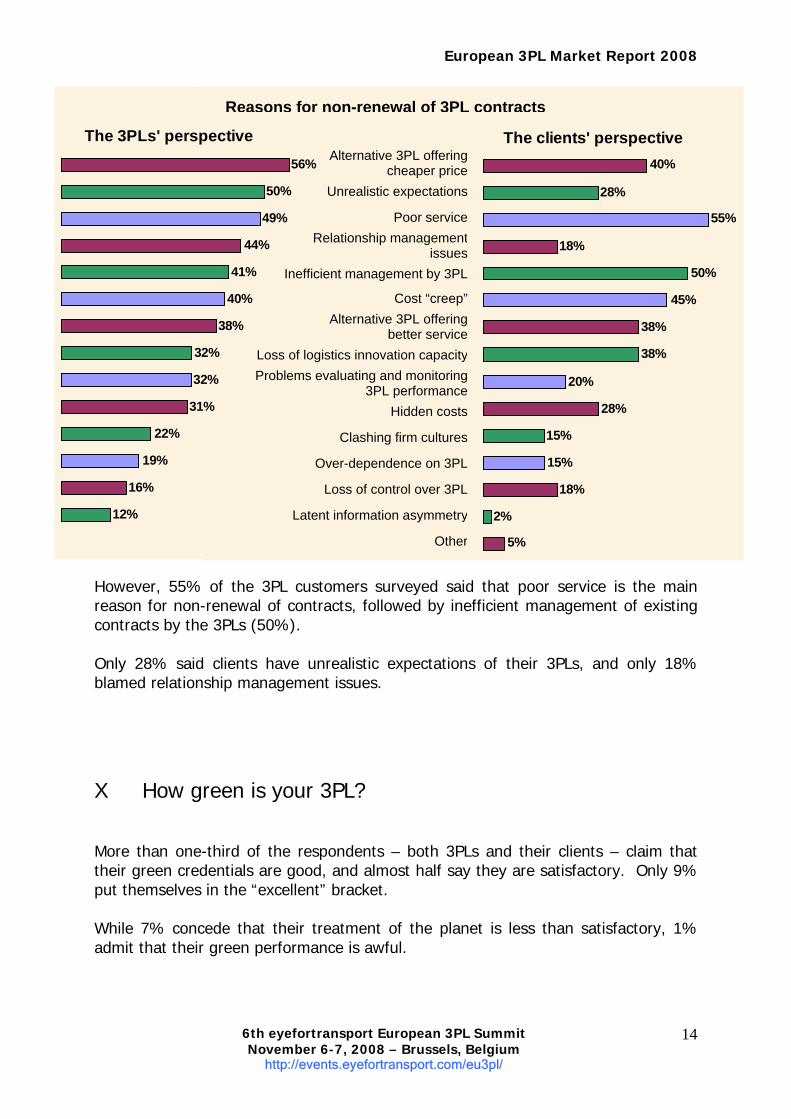

IX Contract renewal More than half of the 3PL respondents believe that contracts are lost to alternative 3PLs offering a cheaper price. Roughly half said that contracts are not renewed due to poor service from the 3PL, or because customers have unrealistic expectations of their 3PLs, and 44% said it was due to relationship management issues. 41% said it was due to inefficient management of the existing contract by the 3PL. 38% said contracts were lost to alternative 3PLs offering a better service. This is spot on, since 38% of the 3PL users said the same thing.

Criteria for choosing a new 3PL -The clients' perspective

47%

19%

15%

6%

20%

34%

12%

22%

9%

13%

9%

25%

15%

19%

18%

17%

6%

25%

20%

21%

20%

15%

12%

28%

37%

7%

13%

21%

8%

9%

33%

3%

10%

3%

3%

6%Best quality service

Lowest price

Sector expertise

Size and scope of 3PL

Geographic expertise

Reputation / testimonials

1 Most important 2 3 4 5 6 Least important

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

14

However, 55% of the 3PL customers surveyed said that poor service is the main reason for non-renewal of contracts, followed by inefficient management of existing contracts by the 3PLs (50%). Only 28% said clients have unrealistic expectations of their 3PLs, and only 18% blamed relationship management issues.

X How green is your 3PL? More than one-third of the respondents – both 3PLs and their clients – claim that their green credentials are good, and almost half say they are satisfactory. Only 9% put themselves in the “excellent” bracket. While 7% concede that their treatment of the planet is less than satisfactory, 1% admit that their green performance is awful.

The clients' perspective

2%

18%

15%

15%

28%

20%

38%

38%

45%

50%

18%

55%

28%

40%

5%

Alternative 3PL offering cheaper price

Initial unrealistic expectations

Poor service

Relationship management issues

Inefficient management by 3PL

Cost “creep”

Alternative 3PL offering better service

Loss of logistics innovation capacityProblems evaluating and monitoring 3PL

performanceHidden costs

Clashing firm cultures

Over-dependence on 3PL

Loss of control over 3PL

Latent information asymmetry

Other, please specify

The 3PLs' perspective56%

50%

49%

44%

41%

40%

38%

32%

32%

31%

22%

19%

16%

12%

Reasons for non-renewal of 3PL contracts

Alternative 3PL offeringcheaper price

Unrealistic expectations

Poor serviceRelationship management

issuesInefficient management by 3PL

Cost “creep”Alternative 3PL offering

better serviceLoss of logistics innovation capacityProblems evaluating and monitoring

3PL performanceHidden costs

Clashing firm cultures

Over-dependence on 3PL

Loss of control over 3PL

Latent information asymmetry

Other

European 3PL Market Report 2008

6th eyefortransport European 3PL Summit November 6-7, 2008 – Brussels, Belgium

http://events.eyefortransport.com/eu3pl/

15

Having said that, the majority of the respondents do have green initiatives in place, with more than two-thirds making an effort to improve energy efficiency. Almost half of the respondents are actively measuring emissions and/or reducing their carbon footprint, with one-quarter monitoring emissions data from suppliers and/or carriers. “Other” initiatives include the use of onsite renewable technologies, low-energy lighting and solar power in facilities, eliminating paper-based transactions, the use of telematics solutions for route optimisation, and adopting a policy of using ONLY green carriers and suppliers.

Current green performance

1%7%

45%38%

9%

Awful Below Average Satisfactory Good Excellent

Green initiatives in place

14%

23%

28%

35%

38%

40%

40%

46%

69%Improving energy efficiency

Measuring/reducing emissions/carbon footprint

Strategic location of warehouse/distribution facilities

Switching to more fuel-efficient modes of transport

Vehicle re-routing to reduce miles

Switching to more fuel-efficient road vehicles

Requesting emissions data / scorecards from suppliers /carriers

Trialling / using alternative fuels

Other, please specify