the emerging investment opportunity in ... emerging investment opportunity in fundamental resource...

TRANSCRIPT

THE EMERGING INVESTMENT OPPORTUNITY IN FUNDAMENTAL

RESOURCE SECTORSCA P I TA L I Z I N G O N T H E S H I F T TO D I ST R I B U T E D I N F R AST RU CT U R E

FA L L 20 16

PAG E 2

TABLE OF CONTENTS

E X ECU T I V E SU M M A RY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

The convergence of physical, economic, and technological trends is driving a major paradigm shift in how resources are used and managed—creating unprecedented opportunities for investors.

CO N V E RG I N G T R E N DS D R I V I N G M A J O R PA RA D I G M S H I F T . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Converging Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Long-Term Resource Needs

Resource Resilience Needs

Technological Capabilities

Distributed Models for Resource Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Efficiency: Doing More with Less

Reuse: Converting Waste Streams to Value

Reaching Price Parity Across Sectors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Agriculture

Energy

Water

Waste

CREATING UNPRECEDENTED OPPORTUNITIES FOR INVESTORS . . . . . . . . . . . . . . . . . . . . . . 15

High Impacts = High Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Long-Term Stewardship of Increasingly High-Value Resources

Capital-Ready Projects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Project Models

Experienced Developers

Emerging Investor Access . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Real Assets

Project Finance

CONCLUSIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

PAG E 3

EXECUTIVE SUMMARY

The convergence of physical resource limitations, economic value, and technological innovation is driving a paradigm shift toward the more

efficient and localized use of natural resources—providing an unprecedented opportunity for investors. Within the critical resource sectors of food, water, energy, and waste, firms are innovating new, distributed models for resource management . These innovations have reached (or will soon reach) price parity with the incumbent, centralized resource delivery systems across these sectors . This shift presents an unprecedented opportunity for investors, who can finance and accelerate the transition to localized resources while realizing exceptional risk-

adjusted returns on such investments . Financial innovation is opening investor access to these opportunities through new real asset project finance products .

The objective of this paper is to identify this emerging opportunity for investors. It demonstrates why distributed resource management models make economic sense and outlines the subsequent investment opportunity . It further details how a new class of innovative investment products is emerging to link institutional capital to sustainable real asset projects .

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION4 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

20

40

20

50

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (Million)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE

MODEL

DISTRIBUTED/SUSTAINABLE

MODEL

fresh water used for soil-based farming 50-80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method of farming

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE

• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSSLOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

LOSS

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewelry, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, consumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES ATZINC

(galvanizing)

LEAD

(lead pipes, batteries)

SILVER

( jewelry, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewelry, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(t(tttttt(t(t((( rrrrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN APRIL 2007

301 MILLIONU.S. POPULATION IN APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODITIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

POPULATION

TROPICAL FOREST LOSS

ENERGY USE WATER USE

TEMPERATURE CHANGECARBON DIOXIDE EMISSIONS

Wo

rld

po

pu

lati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

A. POPULATION

I. TROPICAL FOREST LOSS

D. ENERGY USE D. WATER USE

M. TEMPERATURE CHANGEL. CARBON DIOXIDE EMISSIONS

Wo

rld

pu

pilati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

2040

2050

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (Million)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE MODEL

DISTRIBUTED/REGENERATIVEMODELDISTRIBUTETR D//D REGENERATIVEG TE E

fresh water used for soil-based farming, 50–80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSS

LOSS

LOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewellery, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, comsumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/

2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES AT..ZINC

(galvanising)

LEAD

(lead pipes, batteries)

SILVER

( jewellery, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewellery, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(tttt(t(( rrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN

APRIL 2007

301 MILLIONU.S. POPULATION IN

APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODITIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

Incomes are rising in developing economies faster—and on a greater scale—than at any previous point in history

World Population: 1950–2050

Fig. 1. Global population is projected to grow by over 30% in

the next quarter-century.

Source: US Census Bureau.

Fig. 2. Three billion more consumers will enter the global middle class by 2030. This shift represents an unprecedented rate and scale of wealth creation and resource consumption.

Source: McKinsey & Company.

PAG E 4

CONVERGING TRENDS DRIVING MAJOR PARADIGM SHIFTTHE CONVERGING TRENDS

Critical resources are facing increasing demand, accelerating scarcity, and rapid environmental change—creating crucial sustainability and

resilience challenges . Technological innovation is simultaneously enabling new, more efficient decentralized infrastructure to help alleviate resource constraints in a more affordable, reliable and sustainable way .

Long-Term Resource NeedsThe global population is projected to grow by over thirty percent before the middle of this century1, with three billion more consumers expected to enter the global middle class by 20302 (Fig . 1, Fig . 2) . These trends are driving unprecedented rates of consumption, dramatically increasing demand for natural resources and exacerbating the need to deliver sustainability

Resource Resilience NeedsHuman activities are also dramatically altering the Earth’s natural systems that support and sustain life at unprecedented rates and scales (Fig . 3) . 3 4 These trends are driving rapid global environmental change, underpinning the need to deliver resilience solutions at scale .

Fig. 3. Human activities have drastically and rapidly altered the Earth’s natural systems in recent decades.

Source: Rockefeller Foundation and Lancet Commission.

1 World Population Projected to Reach 9.7 Billion by 2050. 2015. United Nations Department of Economic and Social Affairs.2 Dobbs, Richard, Jeremy Oppenheim, Fraser Thompson, Marcel Brinkman, and Marc Zornes. Resource Revolution: Meeting the World’s Energy, Materials, Food, and Water Needs.

November 2011. McKinsey & Company.3 Ecosystems and Human Well-Being: Synthesis Report. 2005. Millennium Ecosystem Assessment. Washington, DC: Island Press.4 Whitmee, Sarah et al. 2015. Safeguarding Human Health in the Anthropocene Epoch: Report of the Rockefeller Foundation-Lancet Commission on Planetary Health.

The Lancet Commissions.

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION4 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

20

40

20

50

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (Million)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE

MODEL

DISTRIBUTED/SUSTAINABLE

MODEL

fresh water used for soil-based farming 50-80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method of farming

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE

• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSSLOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

LOSS

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewelry, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, consumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES ATZINC

(galvanizing)

LEAD

(lead pipes, batteries)

SILVER

( jewelry, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewelry, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(t(tttttt(t(t((( rrrrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN APRIL 2007

301 MILLIONU.S. POPULATION IN APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODITIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

POPULATION

TROPICAL FOREST LOSS

ENERGY USE WATER USE

TEMPERATURE CHANGECARBON DIOXIDE EMISSIONS

Wo

rld

po

pu

lati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

PAG E 5

Technological CapabilitiesInnovation is driving new resource capabilities through a new generation of decentralized infrastructure that is cost-effective at scales substantially smaller than those of conventional infrastructure . These technological advancements—and the consequent feasibility of decentralized infrastructure—result in increased resource efficiency and opportunities for lowering the cost and price volatility of natural resources.5 6 7

Take the energy sector, for example . Most electricity is generated at large, centralized power plants, inefficiently distributing to customers hundreds of miles away . Today, however, technological advances in renewable energy generation and storage are driving a shift toward more decentralized energy production . We now see greater diversity in energy generation sources (including solar, natural gas, and wind), greater efficiency across a distributed infrastructure system (less lengthy transmission and transit costs as generation is closer to both fuel supply and load), and greater resilience

(as the distributed infrastructure is not as vulnerable to outside shocks, such as natural disasters, as incumbent centralized systems) .

This trend can be seen at an economy-wide level, where the shift to more efficient and sustainable production is already underway . This is illustrated by the decoupling of GDP and CO2 emissions: the economy is growing while we are using natural resources more efficiently . 2014 was the first year that global GDP decoupled from carbon emissions8; in 2015, this was the reality for twenty-one national economies .9 The United States is the largest country to experience multiple consecutive years of economic growth decoupled from CO2 emissions, and projections indicate that the nation’s shift to a cleaner electricity system after 2020 will sustain this trend (Fig . 4)10 .

Fig. 4. Shifts to cleaner technologies are driving more efficient economic output in the US.

Source: World Resources Institute.

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

A. POPULATION

I. TROPICAL FOREST LOSS

D. ENERGY USE D. WATER USE

M. TEMPERATURE CHANGEL. CARBON DIOXIDE EMISSIONS

Wo

rld

pu

pilati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

2040

2050

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (millions)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE

MODEL

DISTRIBUTED/SUSTAINABLE

MODEL

fresh water used for soil-based farming 50-80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method of farming

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE

• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSSLOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

LOSS

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewellery, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, comsumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/

2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES AT..ZINC

(galvanising)

LEAD

(lead pipes, batteries)

SILVER

( jewellery, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewellery, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(tttt(t(( rrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN

APRIL 2007

301 MILLIONU.S. POPULATION IN

APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODOTIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

$1.40

$1.20

$1.00

$0.80

$0.60

$0.40

$0.20

$0

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050

NY

2026CA

2031

KY

2047

TX

2047

HI

PRE-2014

SOLAR-PLUS BATTERY LEVELIZED COST OF ELECTRICITY (LCOE) VS. UTILITY RETAIL PRICE PROJECTIONSCOMERCIAL - BASE CASE {Y-AXIS $/kWh}

Louisville, KY

Westchester, NY

San Antonio, TX

Los Angeles, CA

Honolulu, HI

LCOE Retail Price

100

80

60

40

20

0

Mainstream

Direct

Intermediated

Portland, OR

Blueberries

Sacramento, CA

Spring mix

Twin Cities, MN

Beef

DC area

Milk

ea

d te

Pe

rce

nt

of

reta

il p

rice

Syracuse, NY

Apples

$ T

rillio

ns

(US

D)

1995

Total volume of sustainable investments nearly doubled from 2012 to 2014

20031999 20071997 20052001 2010 2012 2014

$3.47 Trillion

$6.57 Trillion7

6

5

4

3

2

1

0

2

1950 1970 19951955 1975 2000 20151960 1980 2005 20201965 19901985 2010 2025

HISTORICAL FORECAST

CO2

GDP

$24,000

$20,000

$16,000

$12,000

$8,000

$4,000

$0

6,000

5,000

4,000

3,000

2,000

1,000

0

U.S. CO2 Emissions and GDP, 1950–2025

5 Heck, Dr. Stefan. 2015. Resource Revolution: Investor Opportunities in the New Climate. Stanford University.6 Heck, Stefan and Matt Rogers. 2014. Resource Revolution: How to Capture the Biggest Business Opportunity in a Century. New York: Melcher Media.7 Distributed Systems: A Design Model for Sustainable and Resilient Infrastructure. 2010. Victorian Eco Innovation Lab at the University of Melbourne.8 Global Energy-Related Emissions of CO2 Stalled in 2014: IEA Data Point to Emissions Decoupling from Economic Growth for First Time in 40 Years. 2015. International Energy Agency.9 Aden, Nate. 2016. The Roads to Decoupling: 21 Countries are Reducing Carbon Emissions While Growing GDP. World Resources Institute.10 Aden, Nate. 2016. The Roads to Decoupling: 21 Countries are Reducing Carbon Emissions While Growing GDP. World Resources Institute.

Tota

l Ene

rgy-

Rel

ated

Car

bon

Dio

xide

Em

issi

ons

(Mt

CO

2)

GD

P (B

illions of Chained 20

09

Dollars)

PAG E 6

RESOURCE MANAGEMENT AND PLANNING NEED TO TRANSITION FROM

THE PAST MODEL THAT PLACED VALUE PRIMARILY ON EXTRACTING

NATURAL RESOURCES, TO A NEW MODEL THAT VALUES PROJECTS WITH

CONNECTED BENEFITS AND SUSTAINABLE OUTCOMES.”11 ‘‘

DISTRIBUTED MODELS FOR RESOURCE UTILIZATION

The convergence of these global mega-trends represents “an opportunity to achieve a resource productivity revolution comparable with the progress made on labor productivity during the 20th century”12 through innovative, highly-resilient distributed resource utilization models . Just as networked computers and mobile devices replaced mainframe computers and redefined how we work, consume, and live, critical resource sectors are undergoing a radical transformation toward distributed infrastructure . This creates new standards of efficiency and reduces vulnerability to shocks that would otherwise devastate incumbent centralized systems .

These distributed models for sustainable resource management are marked by efficiency (the ability to do more with less resources) and reuse (the ability to convert waste into value) .

Efficiency: Doing More with LessIn order to achieve growth in the face of increased resource demand, a revolution of production efficiency—the ability to do more with less—is needed .13 By stimulating and deploying technological innovation and establishing new methods of organization and management, radical improvements in efficiency will drive enhanced productivity across the food, energy, water, and waste sectors .14 15

Reuse: Converting Waste Streams to ValueReuse can be thought of as converting waste streams into value that can then be utilized again, a concept that is critical to achieving sustainable economic development in the twenty-first century .16 By applying proven technologies to current waste streams, new opportunities to create sellable commodities from previously discarded materials will drive more reuse, and reduce waste, across critical resource sectors .

11 Dobbs, Richard, Jeremy Oppenheim, Fraser Thompson, Marcel Brinkman, and Marc Zornes. Resource Revolution: Meeting the World’s Energy, Materials, Food, and Water Needs. November 2011. McKinsey & Company.

12 From Crisis to Connectivity: Renewed Thinking About Managing California’s Water & Food Supply. 2014. California Roundtable on Agriculture and the Environment. Prepared by Ag Innovations Network.

13 Borza, Mioara. 2014. The Connection between Efficiency and Sustainability: A Theoretical Approach. Proceddia Economics and Finance. Volume 15: pp. 1355–1363.14 Heck, Stefan and Matt Rogers. 2014. Resource Revolution: How to Capture the Biggest Business Opportunity in a Century. New York: Melcher Media.15 Borza, Mioara. 2014. The Connection between Efficiency and Sustainability: A Theoretical Approach. Proceddia Economics and Finance. Volume 15: pp. 1355–1363.16 Mohanty, C.R.C. 2011. Reduce, Reuse, Recycle and Resource Efficiency as the Basis for Sustainable Waste Management. United Nations Centre for Regional Development.17 Distributed Systems: A Design Model for Sustainable and Resilient Infrastructure. 2010. Victorian Eco Innovation Lab at the University of Melbourne.

OVER THE NEXT FEW DECADES, THE WAY PEOPLE OBTAIN THEIR FOOD,

WATER, AND ENERGY WILL UNDERGO A MAJOR EVOLUTION. PEOPLE

WILL NO LONGER RELY ON INDUSTRIAL PRODUCTION UNITS HUNDREDS

OR THOUSANDS OF KILOMETERS AWAY. INSTEAD THEY WILL SOURCE

A GREATER PROPORTION OF ESSENTIAL RESOURCES, GOODS, AND

SERVICES FROM WITHIN THEIR ‘NEIGHBORHOOD’.”17

‘‘

PAG E 7

REACHING PRICE PARITY ACROSS SECTORS

The transition to distributed systems in critical resource sectors is no longer a question of if, but when. Across agriculture, energy, water, and waste systems, new business models are rapidly approaching price parity with traditional centralized systems—some have even exceeded parity and are now the low-cost option . This shifting economic landscape will enable distributed resource utilization through new technologies in the very near future .

AgricultureSustainability & Resilience Challenges

By 2050, it is anticipated that two-thirds of the global population will live in urban areas and there will be 80 million new mouths to feed each year . Global food production will need to rise by 70% in order to feed these individuals .18 By 2030, nourishment needs are projected to require up to 220 million hectares of additional cropland globally .19

The world’s existing agricultural lands are, however, already experiencing degradation . Soil degradation alone is driving the loss of between one and twelve million hectares of agricultural land per year—the equivalent of 20 million tons of grain annually .20 At the same time,

roughly one-third of the food produced globally goes to waste21—either at points of production in developing markets or points of consumption in developed economies .

Today’s centralized agricultural systems are also facing increased vulnerability to outside shocks . Climate change is already affecting the quality and quantity of food production globally, a trend that is anticipated to worsen in coming decades . The Intergovernmental Panel on Climate Change has concluded that direct impacts from climate change (such as extreme weather and precipitation trends) will reduce crop yields by 0–2% per decade for the remainder of the century, while indirect impacts (such as increased plant diseases) could reduce annual crop yields by up to 16% .22

Technological Innovation & Price Parity

Innovation is currently driving new, distributed agricultural production models that sustainably produces affordable, nutritious, and resilient food23 . Emerging technologies drive this shift and operate across the agricultural supply chain; examples include indoor localized food production, precision irrigation farming, and protein synthesis . These projects consolidate to create agricultural systems and markets that are sophisticated, replicable, and scalable .24 Recent research indicates that 90% of Americans could now be fed entirely by localized food systems within 100 miles of their homes.25

In light of these trends, it is no surprise that incumbent centralized agricultural systems are beginning to make less economic sense than more efficient, resilient, distributed models . Vertical farming, characterized by the production of food in vertically stacked layers using controlled-environment agriculture technologies, uses up to 95% less fresh water than traditional agriculture (Fig . 5) .26 In the United States, localized agricultural supply chains now create more value for producers than mainstream models, with “agricultural producers’ share of revenues generally decreasing with distance to market and number of intermediaries involved in the traditional [supply] chain” (Fig . 6) .27 Through greater economic efficiencies, many of these projects can achieve higher returns than their conventional competition .

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

A. POPULATION

I. TROPICAL FOREST LOSS

D. ENERGY USE D. WATER USE

M. TEMPERATURE CHANGEL. CARBON DIOXIDE EMISSIONS

Wo

rld

pu

pilati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

2040

2050

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (Million)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE MODEL

DISTRIBUTED/REGENERATIVEMODELDISTRIBUTETR D//D REGENERATIVEG TE E

fresh water used for soil-based farming, 50–80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSS

LOSS

LOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewellery, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, comsumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/

2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES AT..ZINC

(galvanising)

LEAD

(lead pipes, batteries)

SILVER

( jewellery, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewellery, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(tttt(t(( rrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN

APRIL 2007

301 MILLIONU.S. POPULATION IN

APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODITIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

Accelerating economics of distributed regenerative models

18 Jenkyn-Jones, Bryce. 2012. Resource Scarcity and the Efficiency Revolution. Impax Asset Management.19 Dobbs, Richard, Jeremy Oppenheim, Fraser Thompson, Marcel Brinkman, and Marc Zornes. Resource Revolution: Meeting the World’s Energy, Materials, Food, and Water Needs.

November 2011. McKinsey & Company.20 Whitmee, Sarah et al. 2015. Safeguarding Human Health in the Anthropocene Epoch: Report of the Rockefeller Foundation-Lancet Commission on Planetary Health. The Lancet

Commissions.21 Lipinski, Brian et al. 2013. Reducing Food Loss and Waste. World Resources Institute.22 Turn Down the Heat: Confronting the New Climate Normal. 2014. World Bank.23 Cleaner Technologies: Evolving Towards a Sustainable End-State. 2012. Deutsche Bank.24 Goedde, Lutz et al. 2015. Pursuing the Global Opportunity in Food and Agribusiness. McKinsey & Company.25 Zumkehr, Andrew and J. Elliott Campbell. 2015. The Potential for Local Croplands to Meet US Food Demand. Frontiers in Ecology and the Environment. Volume 13, Issue 5. P. 244-248.26 Vertical Farming Infographics. 2016. Association for Vertical Farming.27 Comparing the Structure, Size, and Performance of Local and Mainstream Food Supply Chains. 2010. Economic Research Service of the United States Department of Agriculture.

PAG E 8

EnergySustainability & Resilience Challenges

The costs of relying on centralized fossil fuel energy systems are becoming more apparent by the day.28 As the world continues to meet rapidly increasing energy demand with fossil fuel combustion, anthropogenic carbon emissions have reached unprecedented levels at an unprecedented rate . The last time the Earth’s atmosphere reached the levels of CO2 seen today (in the Pliocene epoch, 2 .6 million years ago), our planet was much

warmer, with a climate and sea level very different from those in which modern human civilizations have developed and thrived .29 The consequences of climate change are already being observed and experienced around the world; even at current (relatively low) levels, there are more frequent occurrences of “extreme heat and extreme precipitation, drying trends in drought-prone regions, and increased tropical cyclone activity .”30

Percent of retail prices received by producers net of marketing and processing costs, by place and supply chain type

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

A. POPULATION

I. TROPICAL FOREST LOSS

D. ENERGY USE D. WATER USE

M. TEMPERATURE CHANGEL. CARBON DIOXIDE EMISSIONS

Wo

rld

pu

pilati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

2040

2050

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (Million)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE MODEL

DISTRIBUTED/REGENERATIVEMODELDISTRIBUTETR D//D REGENERATIVEG TE E

fresh water used for soil-based farming, 50–80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSS

LOSS

LOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewellery, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, comsumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/

2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES AT..ZINC

(galvanising)

LEAD

(lead pipes, batteries)

SILVER

( jewellery, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewellery, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(tttt(t(( rrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN

APRIL 2007

301 MILLIONU.S. POPULATION IN

APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODITIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

Fig. 5. Vertical farming is more energy and water-efficient than traditional

agricultural methods.

Source: Association for Vertical Farming.

28 Disruptive Technologies: Advances that Will Transform Life, Business, and the Global Economy. 2013. McKinsey Global Institute.29 Kunzig, Robert. 2013. Climate Milestone: Earth’s CO2 Level Passes 400ppm. National Geographic. 30 Turn Down the Heat: Confronting the New Climate Normal. 2014. World Bank.

Traditional Farming Vertical Farming

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

A. POPULATION

I. TROPICAL FOREST LOSS

D. ENERGY USE D. WATER USE

M. TEMPERATURE CHANGEL. CARBON DIOXIDE EMISSIONS

Wo

rld

pu

pilati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

2040

2050

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (millions)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE

MODEL

DISTRIBUTED/SUSTAINABLE

MODEL

fresh water used for soil-based farming 50-80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method of farming

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE

• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSSLOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

LOSS

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewellery, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, comsumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/

2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES AT..ZINC

(galvanising)

LEAD

(lead pipes, batteries)

SILVER

( jewellery, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewellery, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(tttt(t(( rrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN

APRIL 2007

301 MILLIONU.S. POPULATION IN

APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODOTIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

$1.40

$1.20

$1.00

$0.80

$0.60

$0.40

$0.20

$0

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050

NY

2026CA

2031

KY

2047

TX

2047

HI

PRE-2014

SOLAR-PLUS BATTERY LEVELIZED COST OF ELECTRICITY (LCOE) VS. UTILITY RETAIL PRICE PROJECTIONSCOMERCIAL - BASE CASE {Y-AXIS $/kWh}

Louisville, KY

Westchester, NY

San Antonio, TX

Los Angeles, CA

Honolulu, HI

LCOE Retail Price

100

80

60

40

20

0

Mainstream

Direct

Intermediated

Portland, OR

Blueberries

Sacramento, CA

Spring mix

Twin Cities, MN

Beef

DC area

Milk

ea

d te

Pe

rce

nt

of

reta

il p

rice

Syracuse, NY

Apples

$ T

rillio

ns

(US

D)

1995

Total volume of sustainable investments nearly doubled from 2012 to 2014

20031999 20071997 20052001 2010 2012 2014

$3.47 Trillion

$6.57 Trillion7

6

5

4

3

2

1

0

2

1950 1970 19951955 1975 2000 20151960 1980 2005 20201965 19901985 2010 2025

HISTORICAL FORECAST

CO2

GDP

$24,000

$20,000

$16,000

$12,000

$8,000

$4,000

$0

6,000

5,000

4,000

3,000

2,000

1,000

0

Perc

ent

of r

etai

l pri

ce

Fig. 6. Agricultural producers’ share of revenue

decreases with distance to market, helping drive

price parity for distributed agricultural systems.

Source: US Department of Agriculture.

PAG E 9

Centralized fossil fuel systems are also extremely inefficient and inequitable . In the United States, we waste more energy than we use—an issue that has increased since 1970 .31 Globally, one out of every five people still lacks access to electricity, and twice as many (nearly three billion people) use wood, coal, charcoal, animal waste, or other biomass to cook their meals and heat their homes . This lack of modern energy access not only inhibits global economic development, but also leads to the deaths of nearly two million people per year from indoor air pollution .32

Technological Innovation & Price Parity

Fortunately, clean energy technologies are increasingly efficient and cost-effective . The cost of renewable, energy generation has dropped dramatically over the past decade and is poised for further reduction .33 34 Additionally, new distributed energy storage technologies are rapidly advancing in capability and cost (Fig . 7) . The combination of these distributed generation and storage tech-nologies are anticipated to disrupt centralized energy systems to the extent that developed markets will move to an off-grid approach while developing markets will leapfrog traditional centralized infrastructure altogether .35 36

Fig. 7. Distributed energy storage technologies are achieving rapid performance improvements and cost reductions, disrupting centralized energy systems to drive more sustainable, distributed energy infrastructure

in developed and emerging markets.

Source: Goldman Sachs.

7

6

5

4

3

2

1

0

40

30

20

10

0

600

500

400

300

200

100

0

0-50

0-25

0

0-25

0-50

400

350

300

250

18001800 18501850 19001900 19501950 20002000

4

3

2

1

0

A. POPULATION

I. TROPICAL FOREST LOSS

D. ENERGY USE D. WATER USE

M. TEMPERATURE CHANGEL. CARBON DIOXIDE EMISSIONS

Wo

rld

pu

pilati

on

(b

illio

ns)

Glo

bal tr

op

ical fo

rest

lo

ss

co

mp

are

d w

ith

170

0 b

ase

lin

e (

%)

Wo

rld

pri

mary

en

erg

y u

se(E

J)

Glo

bal w

ate

r u

se (

tho

usa

nd

km

2)

Me

an

glo

bal te

mp

era

ture

ch

an

ge

(oC

)

Atm

osp

he

ric c

on

ce

ntr

ati

on

of

CO

2 (

pp

m)

Source: U.S. Census Bureau, International Database, July

2015 Update

Fig. 1. Global population is projected to grow by over 40% in

the next quarter-century.

Source: US Census Bureau

WORLD POPULATION:

1950 - 2050

3 BILLION

196

0

1970

198

0

199

0

20

00

20

10

20

20

20

30

2040

2050

10

9

8

7

6

5

4

3

2

1

0

5 BILLION6 BILLION

7 BILLION

8 BILLION

9 BILLION

UNITED KINGDOM

COUNTRYPOPULATION AT THE START OF THE GROWTH PERIOD (Million)YEARS TO DOUBLE PER CAPITA GDP1

YEAR

1700 1800 1900 2000

53

65

33

16

12

16 822

1,023

22

48

28

10

9154

UNITED STATES

GERMANY

JAPAN

SOUTH KOREA

INDIA

CHINA

CO

ST

TIME

PRICE PARITY

CENTRALIZED/EXTRACTIVE MODEL

DISTRIBUTED/REGENERATIVEMODELDISTRIBUTETR D//D REGENERATIVEG TE E

fresh water used for soil-based farming, 50–80% of which is lost to evaporation

70% GLOBAL

1500 MILES

70-95% LESS

LOCALon average, food travels 1500 to 2500 miles on its way to our plate

fresh water used for vertical farming utilizing the aquaponics or aeroponics method

vertical farming reduces the need for long-distance transport diminishing the use of fossil fuel and ensuring quality

TRADITIONAL FARMING VERTICAL FARMING

$14,250

250 KG

120 KG

20 kWh

160 KM

275 KM

+72%

30 kWh

$5,250

-63%

-52%

+50%

5

2015

BATTERY COST (1000$) BATTERY WEIGHT (10s of KG) BATTERY RANGE (10s of KM)

BATTERY CAPACITY (kWh)

2015 2015 20152020E 2020E 2020E 2020E

10

15

20

25

30

35

40

• EFFICIENCY

• REUSE• SOURCE OF DIVERSIFICATIONAA

SOURCE SOURCE SOURCE SOURCE

WASTE

TREATMENT USE

THE FUTURE: WATER CULTIVATION

USE

LOSS

LOSS

LOSS

LOSS

• INEFFICIENCY

• DISPOSABILITY

• HOMOGENOUS SUPPLYLL

SOURCE

WASTE

TREATMENT

TODAY: WATER HUNTING

TIN

(cans, solder)

GOLD

( jewellery, dental)

PHOSPHORUS

(fertil izer, animal blades)

ALUMINUM

(transport, electric, comsumer durables)

Today’s global consumption rate

Half the U.S. consumption rate

Reverse base

Annual global consumption

reverse base

(assuming global

consumption =

global production)

World population1/

2 U.S. per capita

consumption in

2006

X

If the demand grows, some key resources will be exhausted more quicky if predicted technologies appear and the population grows

HOW MANY YEARS LEFT IF THE WORLD CONSUMES AT..ZINC

(galvanising)

LEAD

(lead pipes, batteries)

SILVER

( jewellery, catalytic converters)

CHROMIUM

(chrome plating, paint)

INDIUM

(LCDs)

PLATINUM

( jewellery, catalysts, fuel cells)

ANTIMONY

(drugs)

URANIUM

(weapons, power stations)

NICKEL

(batteries, turbine blades)

TITANIUM

(cellphones, camera lenses)

COPPER

(wire, coins, plumbing)

48

9

13

42

29

1317

19

30

59

(t(t(tttt(t(( rrrr

4

20

34

36

38

40

42

57

142

510

116

46

45

61

143

360

90

345

1027

40

6.58 BILLIONWORLD POPULATION IN

APRIL 2007

301 MILLIONU.S. POPULATION IN

APRIL 2007

POPULATION COMPARISON

PLATINUM

0%

PHOSPHORUS

0%

GALLIUM

0%

URANIUM

0%

INDIUM

0%

COPPER

31%

NICKEL

35%

SILVER

16%

TITANIUM

20%

LEAD

72%

GOLD

43%

ALUMINUM

49%

ZINC

26%

TIN

26%

GERMANIUM

35%

CHROMIUM

25%

HOW LONG WILL IT LAST

PROPORTION OF CONSUMPTION MET BY RECYCLED MATERIALS

RE

TU

RN

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

BONDS

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18%

REAL ESTATE

AGRICULTURE

TIMBER

EQUITIES

PRIVATE EQUITY

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% OF RESPONDENTS INCREASING IN THE PAST THREE YEARS/NEXT 18 MONTHS

REAL ESTATE

(n=192)

INFRASTRUCTURE

(n=132)

COMMODITIES

(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months

Increased over the past three years

Source: Blackrock and The Economist Intelligence Unit, 31 October 2014.

Low carbon technologies achieve rapid performance improvements and cost reductionsBattery cost reduction/performance improvements

31 Heck, Dr. Stefan. 2015. Resource Revolution: Investor Opportunities in the New Climate. Stanford University.32 Secretary-General Ban Ki-moon. 2011. Sustainable Energy for All: A Vision Statement. United Nations.33 Net Energy Metering, Zero Net Energy, and the Distributed Energy Resource Future: Adapting Electric Utility Business Models for the 21st Century. 2012. Rocky Mountain Institute.34 The Low Carbon Economy: Investor’s Guide to a Low-Carbon World, 2015–2025. 2015. Goldman Sachs.35 Solar Power & Energy Storage: Policy Factors vs. Improving Economics. 2014. Morgan Stanley.36 Disruptive Technologies: Advances that Will Transform Life, Business, and the Global Economy. 2013. McKinsey Global Institute.37 Solar Power & Energy Storage: Policy Factors vs. Improving Economics. 2014. Morgan Stanley.

ENERGY STORAGE, WHEN COMBINED WITH SOLAR POWER, COULD

DISRUPT UTILITIES TO THE EXTENT THAT CUSTOMERS MOVE TO AN

OFF-GRID APPROACH.”37‘‘

PAG E 10

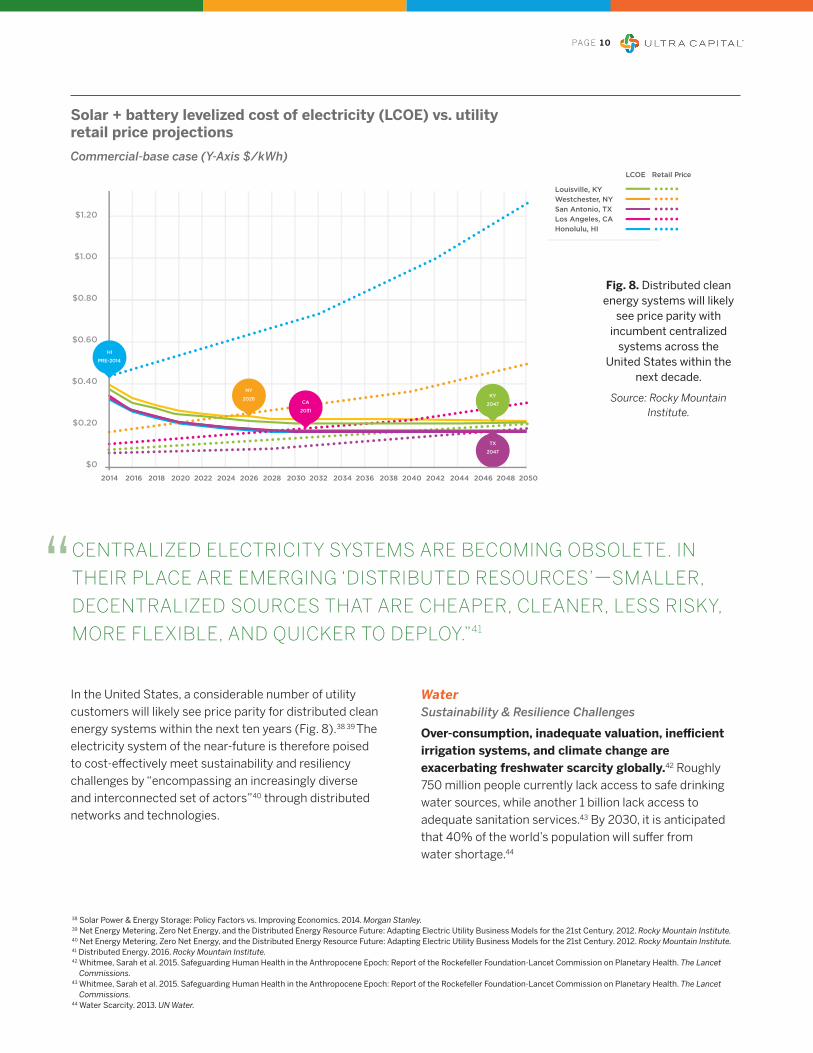

In the United States, a considerable number of utility customers will likely see price parity for distributed clean energy systems within the next ten years (Fig . 8) .38 39 The electricity system of the near-future is therefore poised to cost-effectively meet sustainability and resiliency challenges by “encompassing an increasingly diverse and interconnected set of actors”40 through distributed networks and technologies .

WaterSustainability & Resilience Challenges

Over-consumption, inadequate valuation, inefficient irrigation systems, and climate change are exacerbating freshwater scarcity globally.42 Roughly 750 million people currently lack access to safe drinking water sources, while another 1 billion lack access to adequate sanitation services .43 By 2030, it is anticipated that 40% of the world’s population will suffer from water shortage .44

Fig. 8. Distributed clean energy systems will likely

see price parity with incumbent centralized

systems across the United States within the

next decade.

Source: Rocky Mountain Institute.

Solar + battery levelized cost of electricity (LCOE) vs. utility retail price projectionsCommercial-base case (Y-Axis $/kWh)

38 Solar Power & Energy Storage: Policy Factors vs. Improving Economics. 2014. Morgan Stanley.39 Net Energy Metering, Zero Net Energy, and the Distributed Energy Resource Future: Adapting Electric Utility Business Models for the 21st Century. 2012. Rocky Mountain Institute.40 Net Energy Metering, Zero Net Energy, and the Distributed Energy Resource Future: Adapting Electric Utility Business Models for the 21st Century. 2012. Rocky Mountain Institute.41 Distributed Energy. 2016. Rocky Mountain Institute.42 Whitmee, Sarah et al. 2015. Safeguarding Human Health in the Anthropocene Epoch: Report of the Rockefeller Foundation-Lancet Commission on Planetary Health. The Lancet

Commissions.43 Whitmee, Sarah et al. 2015. Safeguarding Human Health in the Anthropocene Epoch: Report of the Rockefeller Foundation-Lancet Commission on Planetary Health. The Lancet

Commissions.44 Water Scarcity. 2013. UN Water.

CENTRALIZED ELECTRICITY SYSTEMS ARE BECOMING OBSOLETE. IN