the emergence of china: opportunities and challenges for latin america and the caribbean...

TRANSCRIPT

The Emergence of China: Opportunities and Challenges for Latin America and the Caribbean

Coordinators:

Robert Devlin, Deputy Manager (INT)

Antoni Estevadeordal, Principal Economist (INT)

Andrés Rodríguez (RES)

Inter-American Development BankInter-American Development Bank Integration and Regional Programs Department (INT)Integration and Regional Programs Department (INT)

Research Department (RES)Research Department (RES)

An increasing importance in world trade…

0

20

40

60

80

100

120

140

160

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Year

China Exports China Imports World ExportsSource: IMF.

Growth of Trade: China vs. World(1970 = 1)

Liberalization of China’s Trade Policy Regime

MFN Tariff Liberalization (unweighted averages)

CHINA WTO ACCESSION

0

5

10

15

20

25

30

35

40

45

50

Per

cent

China Latin America

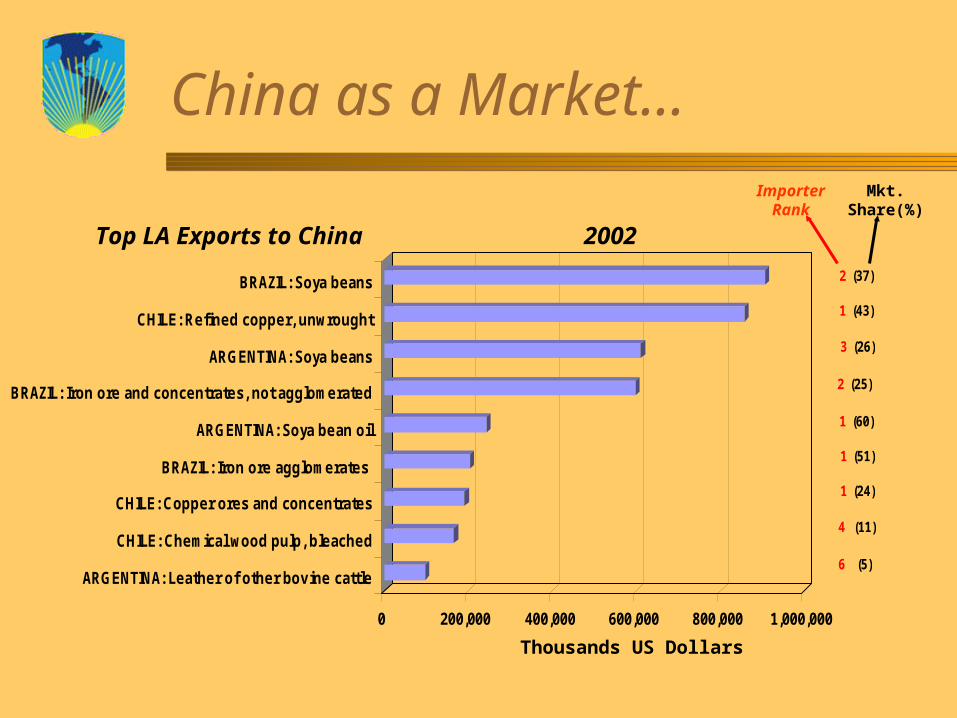

China as a Market…

6 (5)

4 (11)

1 (24)

1 (51)

1 (60)

2 (25)

3 (26)

1 (43)

2 (37)

0 200,000 400,000 600,000 800,000 1,000,000

BRAZIL: Soya beans

CHILE: Refined copper, unwrought

ARGENTINA: Soya beans

BRAZIL: Iron ore and concentrates, not agglomerated

ARGENTINA: Soya bean oil

BRAZIL: Iron ore agglomerates

CHILE: Copper ores and concentrates

CHILE: Chemical wood pulp, bleached

ARGENTINA: Leather of other bovine cattle

Top LA Exports to China

Thousands US Dollars

2002

Mkt. Share(%)

Importer Rank

Competing with China in Global Trade

A highly diversified export basket

0

100

200

300

400

500

600

700

800

OECD United States LAC Mexico Argentina Chile China

20022002

Export Concentration Index

Comparing Chinese and LAC Export Structure by Technological Content

0% 20% 40% 60% 80% 100%

China 1987

China 2002

LAC 1987

LAC 2002

Primary prod. Resource-based manuf.Low-tech manuf. Medium- and high-tech manuf.Other

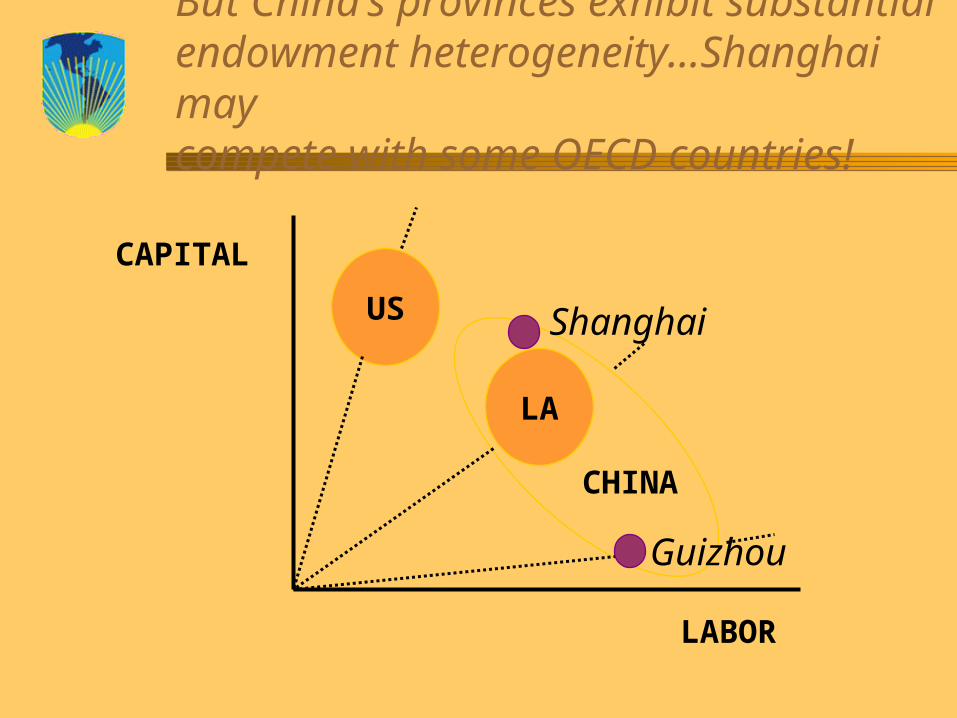

China as a whole is extremely labor abundant…it should compete with the world’s lowest wage countries

CHINA

LA

US

LABOR

CAPITAL

But China’s provinces exhibit substantial endowment heterogeneity…Shanghai may compete with some OECD countries!

LA

US

LABOR

CAPITAL

Shanghai

CHINA

Guizhou

Market Share in the US (Manufacturing)

0

10

20

30

40

50

60

70

80

90

100

1972 1981 1991 2001

OECD Latin America Asia (incl. China)

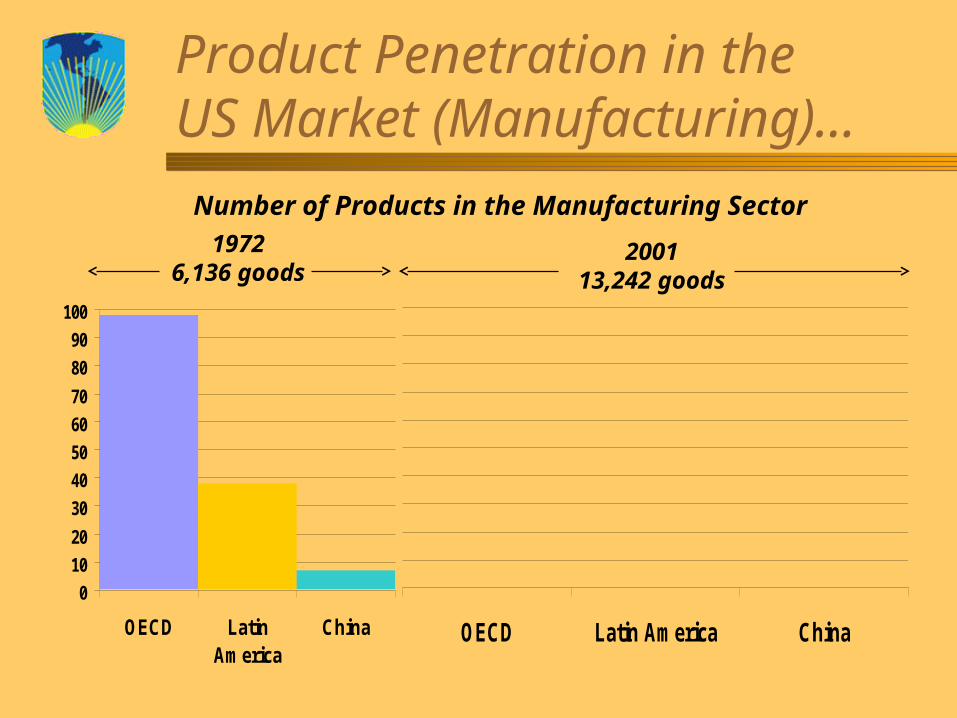

Product Penetration in the US Market (Manufacturing)…

0

10

20

30

40

50

60

70

80

90

100

OECD LatinAmerica

China OECD Latin America China

Number of Products in the Manufacturing Sector

19726,136 goods

200113,242 goods

Product Penetration in the US Market (Manufacturing)…

0

10

20

30

40

50

60

70

80

90

100

OECD LatinAmerica

China OECD Latin America China

Number of Products in the Manufacturing Sector

19726,136 goods

200113,242 goods

Product Penetration in the US Market (Manufacturing)…

0

10

20

30

40

50

60

70

80

90

100

OECD LatinAmerica

China OECD Latin America China

Number of Products in the Manufacturing Sector

19726,136 goods

200113,242 goods

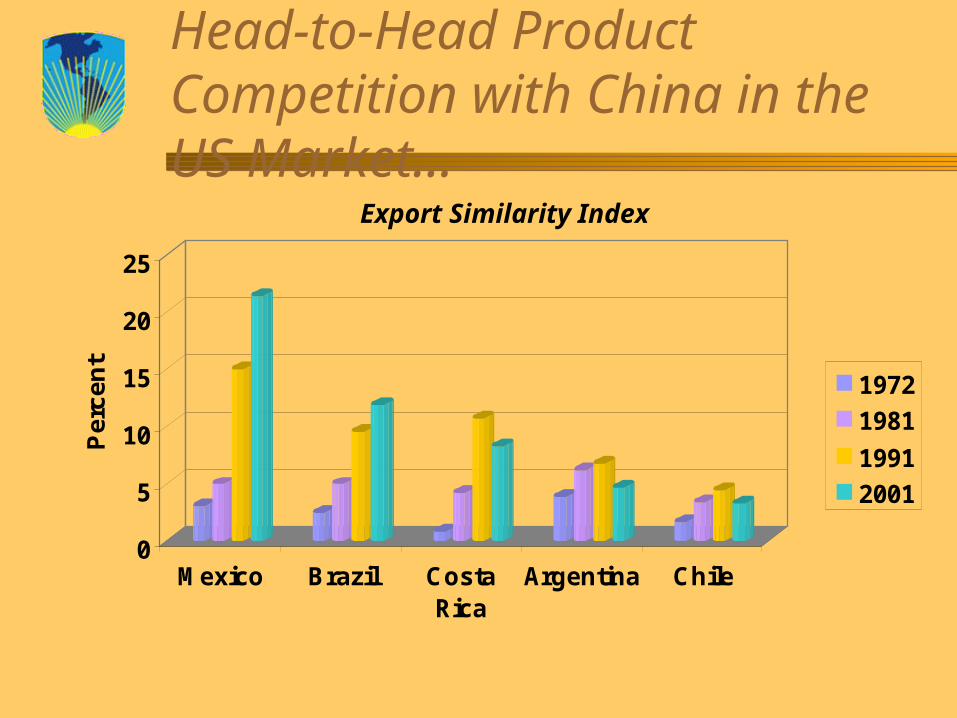

Head-to-Head Product Competition with China in the US Market…

0

5

10

15

20

25

30

OECD S.E. Asia Latin America

1972

1981

1991

2001

Export Similarity Index

Head-to-Head Product Competition with China in the US Market…

0

5

10

15

20

25

Pe

rce

nt

Mexico Brazil CostaRica

Argentina Chile

1972

1981

1991

2001

Export Similarity Index

FDI Competition?

The Surge of FDI to China

There is a surge of FDI to ChinaThis due to China’s clear competitive

advantages and recent reforms, most recently WTO accession

Should Latin America be concerned?

Should Latin America be Concerned?

Conceptually, reforms that allow FDI in a country such as China could divert investment…

But magnitudes would be small… at most 4% reduction in FDI flows to the region

But it could be that some countries are affected more than others…

Are Some Countries More Likely to be Affected?

FDI competition may be stronger across countries with same FDI sources

It may also be stronger across countries that get FDI in the same sectors…

… especially if these are traded sectors

FDI sources differ greatly

A comparison of sources of FDI in Latin America and China reveals large differences:– FDI to China is predominantly from Asia– FDI to Latin America is predominantly from U.S. and

EuropeThe reduction in investment flows from general

FDI competition is thus likely to be even lower than the 4% mentioned earlier…… Asian countries (e.g., Korea, India) have much more to worry!

FDI sector coincidence varies greatly across countries

A Case Study

Are multinationals in L.A. moving to China?A survey in Costa Rica: representative sample of

41 MNCs out of a total of 100 in the EPZ systemTwo MNCs said they were moving to ChinaThe threat is in sectors that rely on cheap labor

and inputs coming from AsiaCountries whose main advantage in attracting

FDI is low wages should be most concerned

Summing Up

Overall FDI competition is modestMain competition is for countries in AsiaL.A. countries that will be more affected

are those specializing in exports dependent on cheap labor (e.g., Mexico, Central America)

The Future of Textiles in Latin America

Several countries in L.A. have experienced high growth in exports of textiles and apparel to U.S.

This has been one of the main sources of new formal jobs in several countries in CA

Unfortunately, this growth was a result of preferential access to the U.S. market that is about to be considerably weakened

January 2005: elimination of remaining U.S. MFA quotas on textiles and apparel

What will happen? What should be done?

A Snapshot of the Current Situation

“The region” (Mexico, CA, DR) is heavily oriented towards the U.S., and is based on maquila (little vertical integration) and low wages

China is tremendously competitive: it has much lower wages and is vertically integrated (cluster)

When U.S. has removed quotas on some items recently, China’s share of the market has boomed

Advantages and Opportunities

The region has two advantages: geography and market access

But NAFTA and CAFTA are not enough: tariff preference is small compared to cost gap with China

Differential transport costs represent a small advantage

The best opportunity is a large difference in the time it takes to ship the product to the U.S.– Specialize in product lines where “speed to market” is

critical

Policies

Avoid protective measures and allow market to come up with solutions that take advantage of region’s advantages (geography, market access)

Policies (may require sub-regional cooperation):– Customs facilitation with U.S. and within region– Infrastructure (roads, ports, electricity)– Long term capital– Specialized human resources (engineering, design,

marketing, procurement, etc.) In addition, promote export diversification

Conclusions

China The Market: Opportunities for Latin America

Systemic Factors– New Stimulus to Growth of World Economy in Face

of Sluggish or Uncertain OECD Growth

– Openness and X M

– Cost Effective Supply Finished Goods and Inputs

– Savings Finance U.S. Treasury Bonds and Help Keep International Interest Rates in Check

China The Market: Opportunities for Latin America

Latin America Specific– Bouyant World Commodity Prices– 1.3 Billion Consumers; Demand for

• Agriculture and processed foods• Raw and processed materials• Services, especially tourism

– FDI• Host (e.g. Embraer)• Source (e.g. Shanghai Bao Steel)

– Cooperation• Support for multilateralism (e.g. G-20)• Policy best practices• Interchange (education, sciences and technology, etc.)

China The Competitor Endowments Give China Competitive Edge in Low, Medium and

High-Tech Manufactures Long-Term Policy Drivers of Competitiveness

– Education• Small surplus in “predicted” secondary enrollment (L.A. has big deficit)• Like L.A., deficit in terciary but

– Extremely high per student expenditure ratio for terciary education– Scale: 1.3 million graduates of higher education– 45% in science and engineering– World competitive test scores

– Innovation• R & D researchers and patent applications in U.S. > L.A.• R & D expenditures % GDP > 1% (> L.A.)• Absolute R & D expenditures South Korea

– Investment (incl. Infraestructure)

Coping with Chinese Competition

Coping with Chinese Competition

China’s (and S.E. Asia) Success Raises Anxiety over Current and/or Future Competition– Intensify Criticisms of Washington Consensus?– Risk Protectionist Backlash?

A Better Response: Treat China as a “Wake-up Call” to Rethink Development Policy

L.A. Does Not Face Challenge Unarmed– During Reforms Acquired or Reinforced Assets to Compete– Must Strategically Combine Existing Assets and Create New

Ones to Become More Offensive Player in Global Economy

Towards a Policy Framework to Compete

A Public-Private AllianceNational Social ProcessHorizontal and Vertical Policies

A Public-Private Alliance

Goal: A Constructive Partnership Between Public Sector and Private Sector

A Requirement: A Government with a Capacity to Engage the Private Sector in Pursuit of Policies to Compete– Long-Term Strategic Focus (strengths and weaknesses)– Experimentation– Learning– Development of Capacities

Focus: Identifying and Overcoming Market Failures that are a Binding Constraint

A Public-Private Alliance

Bottom Line– China and East Asia Successes not based on purely

market forces– Few Economic Success Stories are Entirely a Market

Phenomenon– No Formulas for Proactive Policy –local creativity and

adaptations– But a Strong State with Focus on Support of Industrial

Diversification and Upgrading has been Important in China and East Asia Generally

– Don’t Forget Services

Strategic National Social Process

Strategic National Social Process

Start a National Social Process– Create Space for Active Collaboration Between Public and Private

Sectors– Work Towards Forward Looking and Focused National Policy

Framework to Compete Globally– Process Must Allow for Competition of Interests, Visions and

Capacities in the Private Sector (broadly defined)– Government Must Ultimately Arbitrate with:

• Predictability• Transparency• Accountability• Technical Criteria• Test of the International Market Place

Strategic National Social Process

– For Longer Term Focus Governments Need More Fiscal Space, Public Savings and Strengthening Public Sector Human Resources

– Gradualism• All Governments Have Some Capacity to Engage in Intervention and

Alliance Building• Try Pilot Programs First that Allow for Tests Against the Marketplace,

Learning and Adaptation. • The Weaker Government Capacity, the Fewer and Simpler the

Interventions Should be Until Capacity Develops

– Beware of Unproductive Rent Seeking and Corruption– But Risks of Rent Seeking Lower than Past When

• Protectionism much higher• Competition minimal• Little or no democracy• Little government accountability

Horizontal and Vertical Policies

Horizontal and Vertical Policies

Horizontal Enabling Policies not Controversial

Vertical Policies are More Controversial Because of the need for Selectivity– Governments cannot intervene in all sectors– Fiscal resources are scarce– Public sector human resources limited

Horizontal and Vertical Policies

Choosing Sectors for Support – Some Considerations– Support investment in activities that are

socially very beneficial but unlikely to happen without public action

– Selection of sectors not “picked” by government – must emerge from national social process

Horizontal and Vertical Policies

– Requirement: Cooperation from private sector Associations which have market based knowledge and experience

– Sunset and performance clauses for support programs

Some Policy Areas to Support Industrial and Services Upgrading and Competitiveness

Dealing with the Dutch Disease

What is it?– A market failure

– Happens when high commodity prices push economy away from more knowledge-based non-traditional agriculture and manufacturing

What to do?– When systemic could tax commodity to finance

support for diversification• Chile proposal: tax copper and use for an “Innovation Fund

for Competitiveness”

Provision Public Goods

Intervene to Overcome Classic Coordination Problems in Supply of Public Goods and Services Critical for Growth of Sectors– Overcoming free riding problems – Infrastructure– Identifying and supporting strong

complementarities (e.g. hotel-airports)

Education

Recent Emphasis: Primary EducationMore Emphasis: Secondary and Higher Education

– China’s advantage in low wage labor raises skill premium in Latin America

– More focus on secondary and higher education deficits for supply of skilled professionals and development of R & D capacities

– Upgrade curriculums (math, science and engineering)– Collaboration between universities and private sector for

curriculums and research– More Equality of access

Export Development and Investment

Need more than macro stability, financial deepening, property rights, etc.– Specific support for discovery/investment/activities where social

benefits of spillovers > benefits to single entrepreneur

– Mechanisms = market credit, grants, specialized promotion agencies and programs for discovery of export markets, investment, and attraction FDI

– Competitive real exchange rate

– Predictable rules of the game for investors – role of investment contracts

– Transport systems and infrastructure (scale, hub & spokes, etc)

Innovation

Innovation activities generate substantial externalities and are under-produced by market

Horizontal policies like IPR and across the board corporate tax breaks not enough– Shift attention from traditional improvement of supply

capacities to promoting demand driven innovation– Make supply relevant to demand– Focus support in universities and research centers on

existing industry groups with comparative advantage– Support public-private collaborative innovation in

potential cluster areas

Role of Economic Integration

Regional Integration: Subregional; Latin America; Interregional FTAs (FTAA, EU, U.S., Japan).

Regional Markets facilitate– Scale – Agglomeration– FDI Attraction– Reduce distance (tariffs and preferences, transport and search costs)– Cooperation (education, R & D, X promotion, clusters, joint negotiation,

etc.)– But be careful of overly restrictive rules of origin

Role of WTO: Leveling Playing Field with China– Market Opening– Rules– Dispute Settlement