the dollars and sense of student loans: the economics of ffel and private loans

DESCRIPTION

The Dollars and Sense of Student Loans: The Economics of FFEL and Private Loans. CASFAA Conference – December 6, 2008 Presenters: Thalassa Naylor, Sallie Mae Luke Downer, EdAmerica. Agenda. FFEL Economics – how FFEL lenders make money and finance FFEL loans in a healthy economy - PowerPoint PPT PresentationTRANSCRIPT

1

C A S FA A C O N F E R E N C E – D E C E M B E R 6 , 2 0 0 8P R E S E N T E R S :

T H A L A S S A N AY L O R , S A L L I E M A E L U K E D O W N E R , E D A M E R I C A

12/8/2008

The Dollars and Sense of Student Loans:The Economics of FFEL and Private Loans

2

Agenda

12/8/2008

1. FFEL Economics – how FFEL lenders make money and finance FFEL loans in a healthy economy

2. Private Loan Economics – how lenders make money and finance private loans in a healthy economy

3. Impact of Current Credit Markets on both FFEL and Private Loans – how this has changed the financial realities for lenders

4. ECASLA , TARP and TALF – the federal liquidity solutions and how this changes the traditional model

3

FFEL Economics – Healthy Economy

12/8/2008

Lenders primarily make money from interest paid over time.

Every loan dollar provided to a school is direct revenue for the school (or cash to the borrower)

For the lender, originating the loan is not revenue, it is an opportunity to earn interest over the life of the loan during repayment

Lenders are paid to originate, process, service and collect FFELP loans as well as provide the government with a balance sheet to hold the loans

4

FFEL Economics – Healthy Economy

12/8/2008

Student Loan Lifecycle

Student LoanApplication

FederalGuarantee or

Private Underwriting

LoanOrigination

LoanRepayment

Paid-in-Full

Delinquency DefaultCollection

3 - 4 Years in School 10 - 20 Years in Repayment

Servicing

5

FFEL Economics – Healthy Economy

12/8/2008

Key Factors that Influence Profitability

• ABI: average loan amount at time of purchase• Serialization: incremental loans to a current borrower’s account

• Premiums/Discounts: price paid above/below par

• Defaults: failure to repay a loan• Collection rate: post default collections• Interim / Repay Rate: The spread to index for a portfolio of loans• Servicing Costs: Vary by loan type, adjusted up for default

expectation

6

FFEL Economics – Healthy Economy

12/8/2008

Funding Sources in Stable Market ConditionsShort Term Funding

Asset Backed Commercial Paper Facilities Short and Medium Term Notes Bank Deposits

Long Term Funding Securitization

Lenders mitigate interest risk rate through asset/liability matching. Match fund asseets to liabilities so that the interest rate characteristics of

liabilities match the assets in terms and basis.

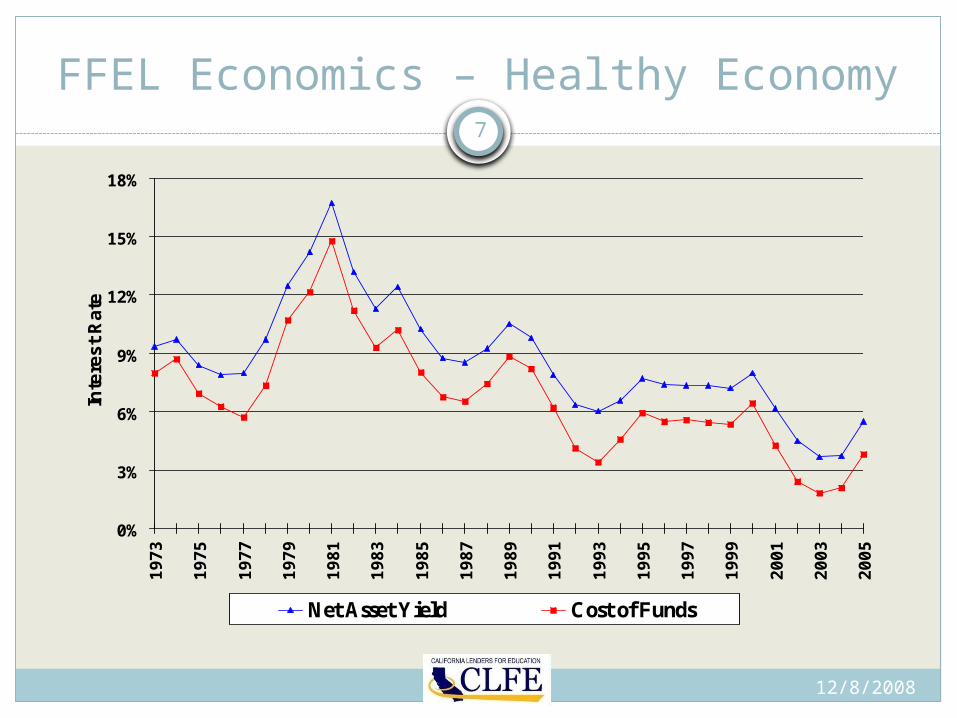

7

FFEL Economics – Healthy Economy

12/8/2008

0%

3%

6%

9%

12%

15%

18%

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

Inte

res

t R

ate

Net Asset Yield Cost of Funds

8

FFEL Economics – Healthy Economy

12/8/2008

For a school with $100 million in FFELP loans (15,000 borrowers), a lender should expect to earn enough income annually for origination, servicing and collection of these loans

$100M atCP plus COF

Borrower

School

Lender

Financial Markets

$100M

$100M atCP plus SAP

$100M

9

Private Loan Economics – Healthy Economy

12/8/2008

Lenders have a similar model for Private Loans with two major differences:

1. Default Risk Lenders must assume all risk of defaults Private student loans are similar to unsecured consumer finance loans

such as credit cards Lenders much manage lending to borrowers with acceptable credit to

manage losses

2. Interest Cap1. Unlike federal loans, where the government pays interest on behalf of

borrowers as loans exceed fixed raes, Private loan interst payments are the sole responsibility of the borrower.

10

Private Loan Economics

12/8/2008

School Type Traditional Non-Traditional Traditional Non-TraditionalCosigned Yes Yes No No

FICO Good Good Good GoodLife of Loan Charge-off 8%-10% 16%-18% 10%-12% 20%-25%

Annual Expense 1.00% 2.00% 1.50% 2.50%

FICO Excellent Excellent Excellent ExcellentLife of Loan Charge-off 4%-6% 12%-16% 8%-12% 16%-20%

Annual Expense 0.75% 1.75% 1.50% 2.00%

• School Type, Co-Borrowers and FICO have impact on life of loan Charge-Off rate and Provision cost

• Majority of Charge-offs are from loans with an original FICO of < 670 or No Score

*Data provided by Sallie Mae and other resources

Private Loan Default Charge-off Profiles

11

Private Loan Economics

12/8/2008

Graduated No Yes No YesCosigned Y Y N N

School Type Traditional Traditional Traditional TraditionalLife of Loan Charge-off 3% - 5% 2%-4% 8%-12% 4%-6%

Annual Expense 0.60% 0.40% 1.00% 0.75%

School Type Non-Traditional Non-Traditional Non-Traditional Non-TraditionalLife of Loan Charge-off 14% - 18% 10%-14% 20%- 25% 14%-18%

Annual Expense 1.75% 1.50% 2.50% 1.75%

Average Graduation RateTraditional 56%

Non-Traditional 34%

• School Type, Co-Borrowers and FICO have impact on life of loan charge-off rate and provision cost

• Over 50% of charge-offs are from borrowers that withdres or were less than half time.

12

Credit Crisis

12/8/2008

Headlines from MSNBC – December 4, 2008“1 in 10 US Homeowners in mortgage trouble”

Mortgage problems began about two years ago when adjustable rate mortgages reset to higher rates

“US Loses Most Jobs Since ’74” 533,000 jobs lost in November, national unemployment rate hits

6.7% (CA unemployment is about 2% higher!) Credit crunch continues to rise due to increased unemployment rates

Ongoing turbulance makes for extraordinarily challenging times for student lenders and the entire higher education community

13

Credit Crisis

12/8/2008

Mortgage industry driven Bad lending policies Brokers had no liability Fannie/Freddie allowed (even encouraged)risky paper

through system Financial institutions willing to take on risky paper Creative financing Government not paying attention

14

Credit Crisis Impact on Student Loans

12/8/2008

Inability to fund or fund at very high cost Investors are unwilling to fund assets until there is stability in

valuations/delinquency Investors want to see data to better understand risk

Inability to securitize Investors are less likely to fund longer term assets “Flight to Quality” – Short term Treasury rates have been driven down

to lowest rates in historyTightening of credit criteria (private loans)

Investors are more likely to fund assets with high credit qualityIncreased price of loans (private loans)

As funding spreads expand total cost of borrowing increases

15

Credit Crisis Impact on Student Loans

12/8/2008

Impact of Market Conditions Funding

Costs can fluctuate based on the liquidity of the credit markets Current costs are high due to limited liquidity (banks cutting back)

due in part to the fallout from the Mortgage industry activities

Securitization Long term financing of student loans Value has decreased to below face value levels

16

Credit Crisis Impact on Student Loans

12/8/2008

17

Credit Crisis Impact on Student Loans

12/8/2008

5 Year Credit Default Swaps

-

200

400

600

800

1,000

1,200

4/11

/07

5/11

/07

6/11

/07

7/11

/07

8/11

/07

9/11

/07

10/1

1/07

11/1

1/07

12/1

1/07

1/11

/08

2/11

/08

3/11

/08

4/11

/08

5/11

/08

Sp

read

to

Lib

or

18

Credit Crisis Impact on Student Loans

12/8/2008

More than 168 education lenders have exited or suspended their participation in all or part of the federally student loan program

More than 60 lenders have stopped making private loans. The remaining lenders have severely restricted access.

Hundreds of higher education institutions that regularly rely on the availability of reasonably priced credit to finance their day-to-day operations have also been unable to access critical funds.

19

Federal Solution – HR 5715

12/8/2008

HR 5715 – Injecting Liquidity for FFEL – “Ensuring Continued Access to Student Loans Act” (ECASLA)

H.R. 5715 gave the Secretary of Education authority to “purchase” student loans from FFELP lenders.

Under H.R. 5715 the Department of Education implemented a comprehensive solution to the credit crunch in the student loan capital markets for federal loans -- at no cost to taxpayers.

20

Federal Solution: HR 5715

12/8/2008

For lenders who need funds… Participation agreement or a short-term loan from the

government.

Lenders pay government Commercial Paper+50 basis points for funds after making first disbursements.

Still requires lenders to have enough initial short term liquidity to make the loans.

21

Federal Solution: HR 5715

12/8/2008

For lenders who have funds or can get funds… Ability to sell loans in order to make more loans (or improve

cost of funds) Private lenders who make new federal loans through AY 08-

09* can transfer ownership of loans to the Department for the principal value of the loan including accrued interest, a lender-paid loan origination fee rebate and a $75 payment per loan for the costs of servicing.

Standard benefits only (.25% IRR for ACH) on loans sold Called “Put”

* extended now through 09-10

22

Federal Solution: HR 5715

12/8/2008

The liquidity solution provides unlimited funding for student lenders to make loans through 2010.

Guarantees that any student that needs a federal loan for college will get one.

Lenders should have until 2010 to decide if they will sell loans to the Department (Awaiting implementation details of the extension from the Department).

Thus far, only one lender has decided to sell only $61 million in loans to the Department.

23

Federal Solution: HR 5715

12/8/2008

More than 800 lenders have enrolled to participate in the Department of Education’s program.

To date, the financing program has supported 40% of FFELP loans disbursed this year.

On 11/19/08 Dept of Ed announced it would purchase up to $6.5 B of loans made in 07-08. Program intended to bolster short term liquidity for private lenders.

24

Federal Solution: HR 5715

12/8/2008

Additional conduit funding programs have been approved but details are still forthcoming. Intent is to purchase and provide longer-term financing for FFELP

loans All fully-disbursed non-consolidation FFELP loans awarded between

October 1, 2003 and July 1, 2009 will be eligible for inclusion. Loans in the conduit will be financed with new issues of Asset Backed

Commercial Paper. Support will come from the Department of Education, which will enter into a forward commitment to purchase eligible student loans from the conduit in the future at a prearranged price.

Protect taxpayers by ensuring there is no net cost to the Federal government.

25

Federal Solution: HR 5715

12/8/2008

9/15/08 HR6889 Passed to extend HR 5715 an additional year through 7/01/10. This was signed by the President on November 8. ECASLA allows the Department to purchase FFELP loans first

disbursed on or after October 1, 2003, and before July 1, 2009. H.R. 6889 extends the Department's authority to purchase loans first disbursed through July 1, 2010.

The bill would extends other provisions in ECASLA that would allow schools to be eligible for institution-wide lender-of-last resort designation through June 30, 2010.

26

Federal Solution: HR 5715

12/8/2008

Changes to how lenders earn money on FFEL

Change from long term interest earnings to up front short term earnings (principal including accrued interest, and a $75 payment per loan for the costs of servicing)

Cost of funds for lenders to borrow from the Feds is at higher rates than what they used to get in the marketplace (but lower than what is currently available in the market)

27

Federal Solution: TARP (HR 1424)

12/8/2008

TARP – Troubled Asset Relief Program, or “The $700 Billion Bailout” Authorizes the US Treasury to provide the following:

Up to $250B for immediate use Requires the President to certify that an additional $100B in funds are needed final $350B are subject to Congressional approval.

As of November 12, $290B allocated, primarily to the Capital Purchase Program : $250B for bank equity infusions $40B for an equity infusion into insurer American International Group (AIG).

Secretary of the Treasury Paulson indicated that reviving the securitization market for consumer credit* would be a new priority in the second allotment, while legislators proposed loans to the struggling automobile industry. *potentially to include education private loans

28

Treasury Solution (Private Loans): TALF

12/8/2008

A component of TARP TALF - Term Asset-Backed Securities Loan FacilityTreasury Secretary Henry Paulson announced on 11/25/08 that

the Federal Reserve Board has created a facility that will help lenders meet the credit needs of households… by supporting the issuance of asset-backed securities (ABS) collateralized by student loans, etc…

TALF will help lenders raise enough money to continue offering private student loans to students

Note: Requires lender to be initially liquid enough to fund loans

29

Terms and Definitions: Loan Terms

12/8/2008

Borrower Rate Fixed for Life of Loan (Consolidation) Loans prior to 7/1/06 - Reset Annually every July 1st (Stafford,

PLUS) Effective 7/1/06, new disbursements (Stafford, PLUS & Consolidation) have a fixed

rateSpecial Allowance Payment (SAP) Rate

Index (CP, T-Bill), plus Legislated Spread (3.50% - 1.19%) Can change through Reauthorization

Lender Yield Lender’s yield is higher of the two For loans disbursed after 7/1/06, any floor income is rebated

back to government

30

Terms and Definitions: Financial Markets

12/8/2008

Liquidity The degree to which an asset or security can be bought or sold in the

market without affecting the asset's price. Liquidity is characterized by a high level of trading activity.

Leverage The use of various financial instruments or borrowed capital, such as

margin, to increase the potential return of an investment.

Asset Backed Securities/Securitization A financial security backed by a loan, lease or receivables against

assets other than real estate and mortgage-backed securities. For investors, asset-backed securities are an alternative to investing in corporate debt.

31

Terms and Definitions: Financial Markets

12/8/2008

Auction Rate Securities The interest rate that will be paid on a specific security as determined by an

auction process. The auctions take place at periodic intervals, and the interest rate is fixed until the next auction is held.

Risk Premium Compensation for investors who tolerate the extra risk, the riskier the asset the

higher the premiumPut

An option that gives the holder (Lender) the right to sell a certain quantity of an asset to the writer of the option (Dept of ED), at a specified price up to a specified date.

Participation An ownership interest on an Asset.

32

Terms and Definitions: Financial Markets

12/8/2008

Libor Rate London Inter-Bank Offer Rate. The rate that banks charge each other for loans. The

LIBOR is officially fixed once a day by a small group of large London banks, but the rate changes throughout the day.

Index Rate Mismatch The volatility that occurs when assets and liabilities are based on different indexes

(LIBOR vs. Commercial Paper). Recent events have created rate changes in one index vs. another causing volatility.

Credit Default Swaps A specific agreement which allows the transfer of risk from one party to the other.

One party is a lender and faces credit risk from a third party, and the counterparty agrees to insure this risk in exchange of regular payments (essentially an insurance premium).

33

Terms and Definitions: Profitability Measures

12/8/2008

Yield Average annual return on assets Sallie Mae receives from an investment or, the “Net Interest

Spread”

NPV Current present value of the stream of cash flows from Sallie Mae’s investment in an Asset,

discounted at the Cost of Funds.

NPVACC Current Present Value of the stream of cash flows from an investment in an Asset, less G&A and

cost of capital to compensate shareholders at a given minimum return. Adjust expected capital ratio to account for risk based pricing As portfolio risk increases, required capital increases

ROE Average annual return on equity a lender receives from an investment.

Average Life Average number of years that the original principal is outstanding.

34

References

12/8/2008

Default Swaps – The Monstor that Ate Wall Street http://www.newsweek.com/id/161199/page/2

What Caused the Credit Crisis? http://economistsview.typepad.com/economistsview/2008/10/what-caused-the.html http://economictimes.indiatimes.com/articleshow/3561424.cms

Index Rate Mismatch http://www.finaid.org/loans/indexratemismatch.phtml

HR 5715 (ECASLA) http://www.nasfaa.org/publications/2008/5715summary.html http://frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=110_cong_bills&docid=f:h5715enr.txt.pdf http://www.nasfaa.org/publications/2008/lnextend091608.html http://www.nasfaa.org/publications/2008/lnloans112108.html HR 6889 Extension of HR 5715

http://nasfaa.org/PDFs/2008/hr6889.pdf http://www.ed.gov/students/college/aid/ecasla-facts.html

TALF http://www.federalreserve.gov/newsevents/press/monetary/monetary20081125a1.pdf http://www.nasfaa.org/publications/2008/lnprivate112608.html http://www.federalreserve.gov/newsevents/press/monetary/20081125a.htm