the dfsa sourcebookdfsa.complinet.com/net_file_store/new_rulebooks/d/f/dfsa1547_10906... ·...

TRANSCRIPT

The DFSA Sourcebook

Prudential Returns Module

(PRU)

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Contents

The contents of this module are divided into the following chapters, sections and forms:

1 INSTRUCTIONAL GUIDELINES FOR PIB RETURNS 1.1 Form B10 Statement of Financial Position 1.2 Form B10 Appendix 1 Detail of Non-Trading Book Assets 1.3 Form B10 Appendix 2 Detail of Non-Market Risk in the Trading Book 1.4 Form B10 Appendix 3 Market Risk in the Trading Book 1.5 Form B10 Appendix 4 Calculation of the DCR 1.6 Form B20 Statement of Financial Position – Islamic Financial

Institutions 1.7 Form B20 Appendix 1 Detail of Non-Trading Book Assets - Self-Financed 1.8 Form B20 Appendix 2 Detail of Non-Trading Book Assets - PSIA Unrestricted

(PSIAU). 1.9 Form B20 Appendix 3 Detail of Non-Trading Book Assets - PSIA Restricted (PSIAR) 1.10 Form B20 Appendix 4 Detail of Non-Market Risk in Trading Book - Self-Financed 1.11 Form B20 Appendix 5 Detail of Non-Market Risk in Trading Book - PSIA Unrestricted

(PSIAU) 1.12 Form B20 Appendix 6 Detail of Non-Market Risk in Trading Book - PSIA Restricted

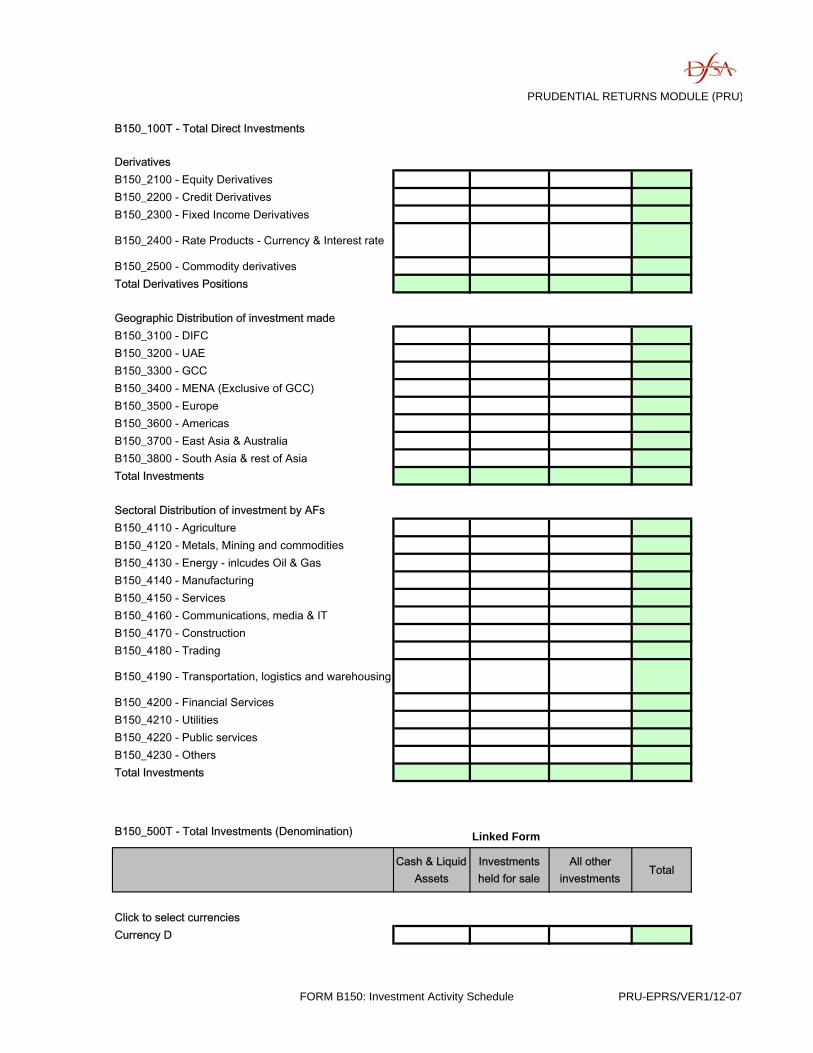

(PSIAR) 1.13 Form B20 Appendix 7 Detail of Market Risk in the Trading Book 1.14 Form B20 Appendix 8 Calculation of the Displaced Commercial Risk (DCR) 1.15 Form B20 Appendix 9 Analysis of Reserves Movement 1.16 Form B30 Income Statement 1.17 Form B40 Income Statement - Islamic Financial Institutions 1.18 Form B50 Expenditure Based Capital Minimum 1.19 Form B60 Capital Adequacy Schedule 1.20 Form B70 Large Exposures Schedule 1.21 Form B80 Liquidity Schedule – Maturity Mismatch 1.22 Form B90 Branch Return 1.23 Form B90 Appendix 1 Large Exposures - Branch 1.24 Form B120 Geographical Distribution of Assets and Liabilities 1.25 Form B130 Provisions for Impairment 1.26 Form B140 Exposures in Arrears 1.27 Form B150 Investment Activity Schedule 1.28 Form B160 Credit Activity Schedule 1.29 Form B170 Acceptance of Deposits Schedule 1.30 Form B180 Wealth Management Activity 1.31 Form B190 Asset Management, Custody & Trust Services 1.32 Form B200 Brokerage Activity 1.33 Form B210 Outward Remittances 1.34 Form B220 Inward Remittances 1.35 Form B230 Domestic Fund Activity 1.36 Form B240 Balances due from and due to Head Office, Own

Branches & Other Banks

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

1.37 Form B260 Acting as a Trustee of a Fund and Fund Administration Activity

1.38 Form B270 Related Party Transactions 1.39 Form B280 Financial Group Capital Adequacy Report

2 PIB FORMS

Form B10 Statement of Financial Position Form B10 Appendix 1 Detail of Non-Trading Book Assets Form B10 Appendix 2 Detail of Non-Market Risk in the Trading Book Form B10 Appendix 3 Market Risk in the Trading Book Form B10 Appendix 4 Calculation of the DCR Form B20 Statement of Financial Position – Islamic Financial Institutions Form B20 Appendix 1 Detail of Non-Trading Book Assets - Self-Financed Form B20 Appendix 2 Detail of Non-Trading Book Assets - PSIA Unrestricted (PSIAU). Form B20 Appendix 3 Detail of Non-Trading Book Assets - PSIA Restricted (PSIAR) Form B20 Appendix 4 Detail of Non-Market Risk in Trading Book - Self-Financed Form B20 Appendix 5 Detail of Non-Market Risk in Trading Book - PSIA Unrestricted (PSIAU) Form B20 Appendix 6 Detail of Non-Market Risk in Trading Book - PSIA Restricted (PSIAR) Form B20 Appendix 7 Detail of Market Risk in the Trading Book Form B20 Appendix 8 Calculation of the Displaced Commercial Risk (DCR) Form B20 Appendix 9 Analysis of Reserves Movement Form B30 Income Statement Form B40 Income Statement - Islamic Financial Institutions Form B50 Expenditure Based Capital Minimum Form B60 Capital Adequacy Schedule Form B70 Large Exposures Schedule Form B70 Appendix 1 Detail of Largest 25 Exposures Arising from Islamic Contracts Form B80 Liquidity Schedule – Maturity Mismatch Form B90 Branch Return Form B90 Appendix 1 Large Exposures - Branch Form B100 Declaration by Authorised Firm Form B120 Geographical Distribution of Assets and Liabilities Form B130 Provisions for Impairment Form B140 Exposures in Arrears Form B150 Investment Activity Schedule Form B160 Credit Activity Schedule Form B170 Acceptance of Deposits Schedule Form B180 Wealth Management Activity Form B190 Asset Management, Custody & Trust Services Form B200 Brokerage Activity Form B210 Outward Remittances Form B220 Inward Remittances Form B230 Domestic Fund Activity Form B240 Balances due from and due to Head Office, Own Branches &

Other Banks Form B260 Acting as a Trustee of a Fund and Fund Administration Activity Form B270 Related Party Transactions Form B280 Financial Group Capital Adequacy Report

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

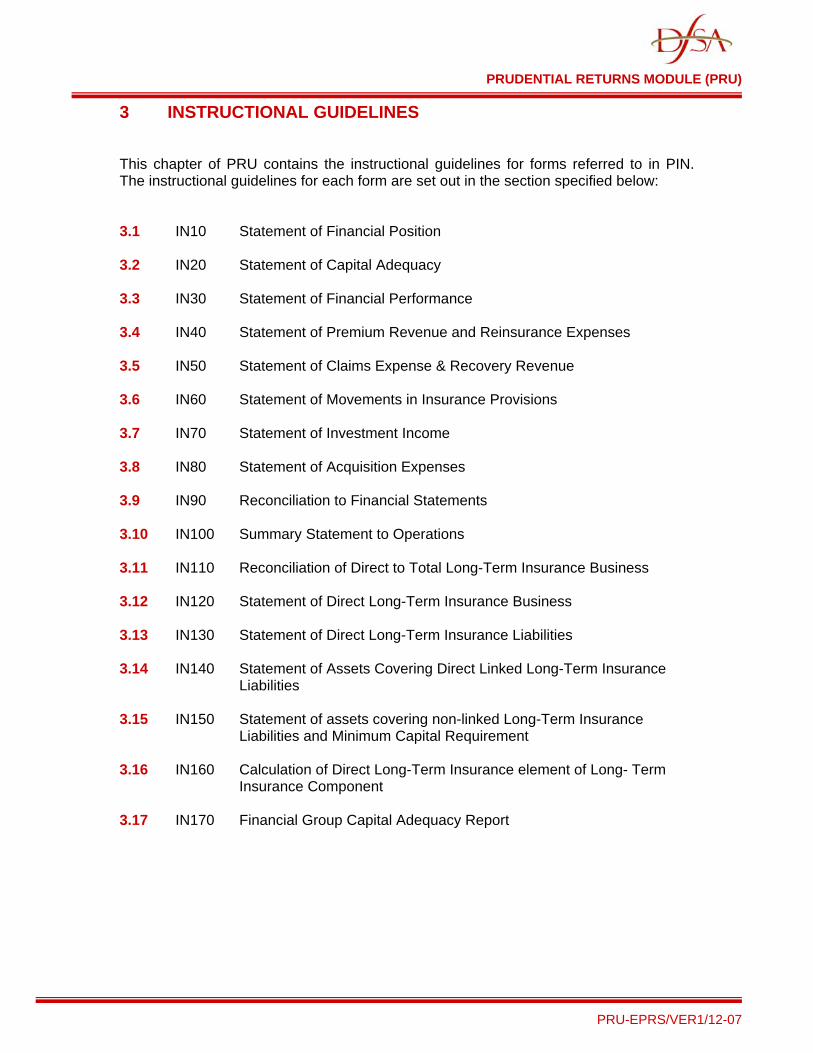

3 INSTRUCTIONAL GUIDELINES 3.1 Form IN10 – Statement of Financial Position 3.2 Form IN20 – Statement of Capital Adequacy 3.3 Form IN30 – Statement of Financial Performance 3.4 Form IN40 – Statement of Premium Revenue and Reinsurance Expenses 3.5 Form IN50 – Statement of Claims Expense & Recovery Revenue 3.6 Form IN60 – Statement of Movements in Insurance Provisions 3.7 Form IN70 – Statement of Investment Income 3.8 Form IN80 – Statement of Acquisition Expenses 3.9 Form IN90 – Reconciliation to Financial Statements 3.10 Form IN100 – Summary Statement to Operations 3.11 Form IN110 – Reconciliation of Direct to Total Long-Term Insurance Business 3.12 Form IN120 – Statement of Direct Long-Term Insurance Business 3.13 Form IN130 – Statement of Direct Long-Term Insurance Liabilities 3.14 Form IN140 – Statement of Assets Covering Direct Linked Long-Term

Insurance Liabilities 3.15 Form IN150 – Statement of Assets Covering Non-Linked Long-Term Insurance

Liabilities and Minimum Capital Requirement 3.16 Form IN160 – Calculation of Direct Long-Term Insurance Element of Long-

Term Insurance Component 3.17 Form IN170 – Financial Group Capital Adequacy Report

4 PIN FORMS IN10 Statement of Financial Position IN20 Statement of Capital Adequacy IN30 Statement of Financial Performance IN40 Statement of Premium Revenue and Reinsurance Expenses IN50 Statement of Claims Expense & Recovery Revenue IN60 Statement of Movements in Insurance Provisions IN70 Statement of Investment Income IN80 Statement of Acquisition Expenses IN90 Reconciliation to Financial Statements IN100 Summary Statement to Operations IN110 Reconciliation of Direct to Total Long-Term Insurance Business IN120 Statement of Direct Long-Term Insurance Business IN130 Statement of Direct Long-Term Insurance Liabilities IN140 Statement of Assets Covering Direct Linked Long-Term Insurance Liabilities IN150 Statement of Assets Covering Non-Linked Long-Term Insurance Liabilities

and Minimum Capital Requirement IN160 Calculation of Direct Long-Term Insurance Element of Long- Term Insurance

Component IN170 Financial Group Capital Adequacy Report

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

INTRODUCTION

Application

Guidance

1. This Sourcebook (PRU) is relevant to a Person to whom PIB or PIN applies.

2. Chapter 1 contains instructional guidelines in respect of the forms in Chapter 2. 3. Chapter 2 contains the forms referred to in PIB. 4. Chapter 3 contains instructional guidelines in respect of the forms in Chapter 4. 5. Chapter 4 contains the forms referred to in PIN.

Defined terms

Guidance 1. Defined terms are identified throughout the forms by the capitalisation of the initial letter of a word

or each word of a phrase and are defined in the Glossary module (GLO) of the DFSA’s Rulebook. Unless the context otherwise requires, where capitalisation of the initial letter is not used, an expression has its natural meaning. Within this module the term EPRS has the meaning of the DFSA’s electronic prudential reporting system.

2. Notwithstanding the use of capitalisation for identifying defined terms, capitalisation is also used

when reference is made to sections and items in the forms by quoting the title of the section or the name of the item. Take note that some of these words or phases are not also defined terms and, therefore, will not be defined in GLO, PIB or PIN.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

1 INSTRUCTIONAL GUIDELINES This chapter of PRU contains instructional guidelines for forms referred to in PIB. The instructional guidelines for each form are set out in the sections specified below:

1.1 Form B10 Statement of Financial Position 1.2 Form B10 Appendix 1 Detail of Non-Trading Book Assets 1.3 Form B10 Appendix 2 Detail of Non-Market Risk in the Trading Book 1.4 Form B10 Appendix 3 Market Risk in the Trading Book 1.5 Form B10 Appendix 4 Calculation of the DCR 1.6 Form B20 Statement of Financial Position – Islamic Financial Institutions 1.7 Form B20 Appendix 1 Detail of Non-Trading Book Assets - Self-Financed 1.8 Form B20 Appendix 2 Detail of Non-Trading Book Assets - PSIA Unrestricted

(PSIAU). 1.9 Form B20 Appendix 3 Detail of Non-Trading Book Assets - PSIA Restricted (PSIAR) 1.10 Form B20 Appendix 4 Detail of Non-Market Risk in Trading Book - Self-Financed 1.11 Form B20 Appendix 5 Detail of Non-Market Risk in Trading Book - PSIA Unrestricted

(PSIAU) 1.12 Form B20 Appendix 6 Detail of Non-Market Risk in Trading Book - PSIA Restricted

(PSIAR) 1.13 Form B20 Appendix 7 Detail of Market Risk in the Trading Book 1.14 Form B20 Appendix 8 Calculation of the Displaced Commercial Risk (DCR) 1.15 Form B20 Appendix 9 Analysis of Reserves Movement 1.16 Form B30 Income Statement 1.17 Form B40 Income Statement - Islamic Financial Institutions 1.18 Form B50 Expenditure Based Capital Minimum 1.19 Form B60 Capital Adequacy Schedule 1.20 Form B70 Large Exposures Schedule 1.21 Form B80 Liquidity Schedule – Maturity Mismatch 1.22 Form B90 Branch Return 1.23 Form B90 Appendix 1 Large Exposures - Branch 1.24 Form B120 Geographical Distribution of Assets and Liabilities 1.25 Form B130 Provisions for Impairment 1.26 Form B140 Exposures in Arrears 1.27 Form B150 Investment Activity Schedule 1.28 Form B160 Credit Activity Schedule 1.29 Form B170 Acceptance of Deposits Schedule 1.30 Form B180 Wealth Management Activity 1.31 Form B190 Asset Management, Custody & Trust Services 1.32 Form B200 Brokerage Activity 1.33 Form B210 Outward Remittances 1.34 Form B220 Inward Remittances 1.35 Form B230 Domestic Fund Activity 1.36 Form B240 Balances due from and due to Head Office, Own Branches &

Other Banks 1.37 Form B260 Acting as a Trustee of a Fund and Fund Administration Activity 1.38 Form B270 Related Party Transactions 1.39 Form B280 Financial Group Capital Adequacy Report

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

1 INSTRUCTIONAL GUIDELINES FOR PIB RETURNS 1.1 Instructional Guidelines – Form B10 – Statement of Financial

Position

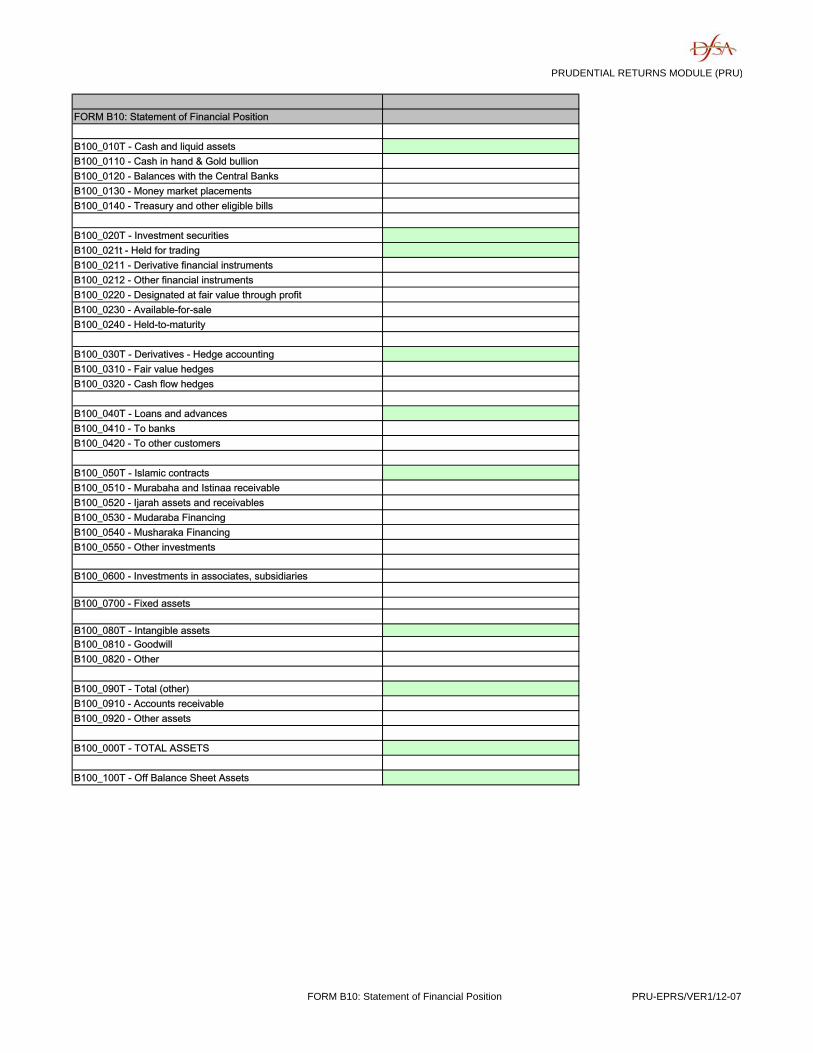

Purpose Form B10 – Balance sheet is intended to reflect the financial position of an Authorised Firm at the end of the reporting period. Applicability This form is applicable to the Authorised Firms categorised under prudential categories 1, 2, 3 and 4, except for Authorised Firms in these categories involved in managing PSIAs. This form is not applicable to Islamic Financial Institutions (IFI), Authorised Firms operating through branches in the DIFC and Authorised Firms managing PSIAs. Instead, IFIs and Authorised Firms managing PSIAs should use the form B20 and branches should use the form B90 along with the respective appendices. Content The form is designed to capture information pertaining to the Authorised Firm’s on-balance sheet and off-balance sheet assets, liabilities and shareholders’ equity at a given point in time. Structure of the form in EPRS B10 is presented as a single form. Instructional Guidelines

Item/ Section

No. Item/ Section Instructional Guidelines

On Balance sheet items B100_0110 Cash in hand &

Gold bullion Include, for example, the following amounts:

• Notes and coins; • Long positions in Gold bullion (including Tola Bars);

B100_0120 Balances with the Central Banks

Amounts placed with central banks including funds required to be placed on deposit with central banks and monetary authorities.

B100_0130 Money market placements

Include deposits at call and other money market placements with banks or other money market participants.

B100_0140 Treasury bills and other eligible bills

Treasury bills issued by the national governments or by the Central banks on behalf of the governments. Also include bills issued by other entities, which are eligible for rediscounting with the central bank.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_0211 Derivative financial

instruments The assets reported here should include, but are not limited to, positions representing the following instruments, recorded at fair value:

• Forward and Futures contracts in currencies, interest rates and other financial assets

• Forward rate agreements • Currency and interest rate swaps • Credit derivatives • Option contracts on currency, interest rate and other financial

assets. These derivatives include both the exchange-traded and over-the-counter versions. Derivatives held for hedging purposes should be included under section B100_030T.

B100_0212 Other Financial instruments (held for trading)

Include investments acquired principally for the purpose of selling or repurchasing them in the near term for short-term-profit-taking. This would include but not limited to, debt, equity and hybrid instruments

B100_0220 Other financial instruments – Designated at fair value through profit and loss

Include all financial instruments which are, upon initial recognition, designated by the entity as financial assets to be measured at fair value through profit or loss other than the trading securities included in B100_0211 and B100_0212.

B100_0230 Available-for-sale Include non-derivative financial assets that are designated as available for sale by the firm or that have not been classified under any of the other categories of investments.

B100_02401101.2.5

Held-to-maturity Include non-derivative financial assets with fixed or determinable payments and fixed maturity that the firm has positive intention and ability to hold to maturity.

B100_0310 and B100_0320

Derivatives – Hedge accounting -Fair value hedges -Cash flow hedges

Include all the derivative instruments held for the purposes of hedging. Derivatives held for trading should be accounted for under B100_0211.

B100_040T Loans and advances Under this section include the amounts arising from, for example: • Revolving credit facilities; • Credit cards outstanding balances; • Housing loans (both variable and fixed rates); • Term loans (both variable and fixed rates); • The book value of assets leased out under finance lease agreements; • Loans made under conditional hire purchase contracts; • Advances purchased by or assigned to the reporting institutions,

factoring or similar arrangements • Other loans and advances.

The items listed above are indicative examples and are not exhaustive universe of items to be reported under this item.

The amounts reported should be gross of provisions (as specific and general provisions should be reported in the Liabilities section of the balance sheet) and net of interest receivable.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_0510 Murabaha and Istisna’a receivables

Report here all receivables relating to Murabaha and Istisna’a contracts. Refer to FAS 2 and FAS 10 of AAOIFI respectively.

B100_0520 Ijarah assets and receivables

Include Ijarah assets net of depreciation/ amortisation and Ijarah receivables. Refer to FAS 8 of AAOIFI.

B100_0530 Mudaraba Financing Financing provided on a Mudaraba basis should be reported here. Refer to FAS 3 of AAOIFI.

B100_0540 Musharaka Financing

Report financing provided on a Musharaka basis. Refer to FAS 4 of AAOIFI. Investment in the share capital of another company should be reported under “Other investments”, under B100_0550.

B100_0550 Other investments Include any other investments undertaken through Islamic contracts, including Parallel Istisna’a assets (refer FAS 10 of AAOIFI) and capital provided on Salam contracts (refer FAS 7 AAOIFI).

B100_0700 Fixed assets Include, for example, the value of the following: • Plant and equipment, the residual value of items leased out under an

operating lease (excluding balances relating to named Ijarah assets which should be included separately under B100_0520);

• Own premises being occupied or developed for occupation by the Authorised Firm, property (excluding property acquired / held available for sale which should be included in “Other Assets”, B100_0920).

The amounts reported here should be net of accumulated depreciation and amortisation.

B100_0810 Goodwill Include amounts relating to any purchased goodwill. B100_0820 Other intangible

assets Items to be included, for example, but are not limited to:

• Capitalised development costs • Brand names, trademarks and similar rights • Licences and exchange seats which may be held as part of the

Authorised Firm’s trading requirement. Off Balance sheet items

B100_1010 Direct credit substitutes

These relate to the financial requirements of Counterparty where the risk of loss to the Authorised Firm on the transaction is equivalent to that arising from a direct claim on the Counterparty. The indicative examples of items to be Included here are • Guarantees of a financial nature to stand behind the current obligations

of customers (e.g. loan guarantees); • Guarantees of leasing operations; • Letters of Credit and Stand-by Letters of Credit to the extent that they

do not qualify for inclusion in item B100_1030 “Trade related contingents” below;

• Guarantees of a capital nature such as undertakings given to a non-bank financial company which are considered as capital by the appropriate regulatory body. Guarantees given to a company not connected to the reporting institution should be risk weighted at 100% and those for connected companies should be deducted from the reporting institution’s capital base.

• Acceptances granted and risk participation in bankers’ acceptances. Where the Authorised Firm’s own acceptances have been discounted by that institution the nominal value of the bills held should be deducted from the nominal amount of the bills issued under the facility and a corresponding on-balance sheet entry made.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_1020 Transaction related

contingents These exposures relate to the on-going trading activities of a Counterparty where the risk of loss to the Authorised Firm depends on the likelihood of a future event which is independent of the creditworthiness of the Counterparty. They are essentially guarantees that support particular non financial obligations rather than a customer’s financial obligations. Include here: • Advance payment guarantees • Performance bonds including bid or tender bonds, warranties and

indemnities (indemnities given for lost share certificates or bills of lading and guarantees of the validity of papers rather than of payment under certain conditions should be reported here);

Stand-by Letters of Credit relating to a particular contract or to non-financial transactions (including arrangements backing, inter alia, subcontractors’ and supplier’s performance, labour and materials, contracts and construction tenders/bids).

B100_1030 Trade related contingents

Report short term self-liquidating trade related items such as documentary letters of credit issued by the Authorised Firm that are collateralised by the underlying shipment i.e. the credit provides for the Authorised Firm to retain title to the underlying shipment. L/C’s issued without provision for the Authorised Firm to retain title to the underlying shipment should be reported under direct credit substitutes above.

B100_1040 Sale and Repurchase Agreements

In this item, report only the sale and repurchase agreements where the asset sold is not reported on the balance sheet. Where the asset is off-balance sheet, the appropriate Counterparty weighting is determined by the issuer of the security and not according to the Counterparty with whom the transaction has been undertaken.

B100_1050 Forward Assets Purchases

The appropriate Counterparty weighting should be determined by the asset to be purchased and not the Counterparty with whom the contract has been entered into. Include commitments for loans and other on-balance sheet items with definitive drawdown schedules. Exclude foreign currency spot deposits with value date of up to two business days after trade date.

B100_1060 Forward Deposits Placed

Relates to agreements between two parties whereby one will pay and the other receive an agreed rate of interest on a deposit to be placed by one with the other at some pre-determined rate in the future. Exclude foreign currency spot deposits with value date of up to two business days after trade date.

B100_1070 Uncalled partly- paid shares and securities

Include under this item calls with specific dates. If there is no specific date for a call, the item should be included as a long term commitment under item no. B100_1122 “Other Commitments”.

B100_1080 NIF’s and RUF’s Note issuance and revolving underwriting facilities should include the Authorised Firm’s underwriting obligations of any maturity. Where the facility has been drawn down by the borrower and the notes are held by someone other than the Authorised Firm, the underwriting obligation should continue to be reported at the nominal amount.

B100_1090 Endorsement of Bills These should be reported at the full nominal amount, less any amount for bills which the Authorised Firm currently holds but had previously endorsed.

B100_1111 & B100_1122

Other commitments All other undrawn commitments are to be reported here, divided into commitments of maturity, under and over one year.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_1110 Assets funded by restricted PSIAs

The methodology for calculating exposures financed by PSIAs are, in principle, no different to calculating exposures for a reporting institution’s self financed assets. All the Instructional Guidelines above apply in their entirety unless stated otherwise.

B100_210T Deposits In this section, identify and report deposits due to banks and financial institutions in item no B100_2110. All other deposits are to be reported as deposits due to other customers - item no B100_2120.

B100_2310 Provisions for bad and doubtful debts

All specific and general provisions in respect of all assets, including loans and advances and other receivables should be reported under this section. Exclude provisions against Islamic contracts which should be reported in item no B100_2640.

B100_2400 Derivative financial instruments – held for trading

The indicative examples of liabilities to be included under this item, but are not limited to, liabilities arising out of positions representing the following instruments, recorded at fair value:

• Forward and Futures contracts in currencies, interest rates and other financial assets

• Forward rate agreements • Currency and interest rate swaps • Credit derivatives • Option contracts on currency, interest rate and other financial

assets. These derivatives include both the exchange-traded and over-the-counter versions. Also include under this item other trading liabilities.

B100_260T Liabilities arising from Islamic contracts

Liabilities arising from Islamic contracts include advances received against Salam contracts (defined in Para 3 and 19 of FAS 7 issued by AAOIFI and Ijarah investment payables (refer to FAS 8 of AAOIFI). Report any provisions against Islamic contracts in item B100_2640.

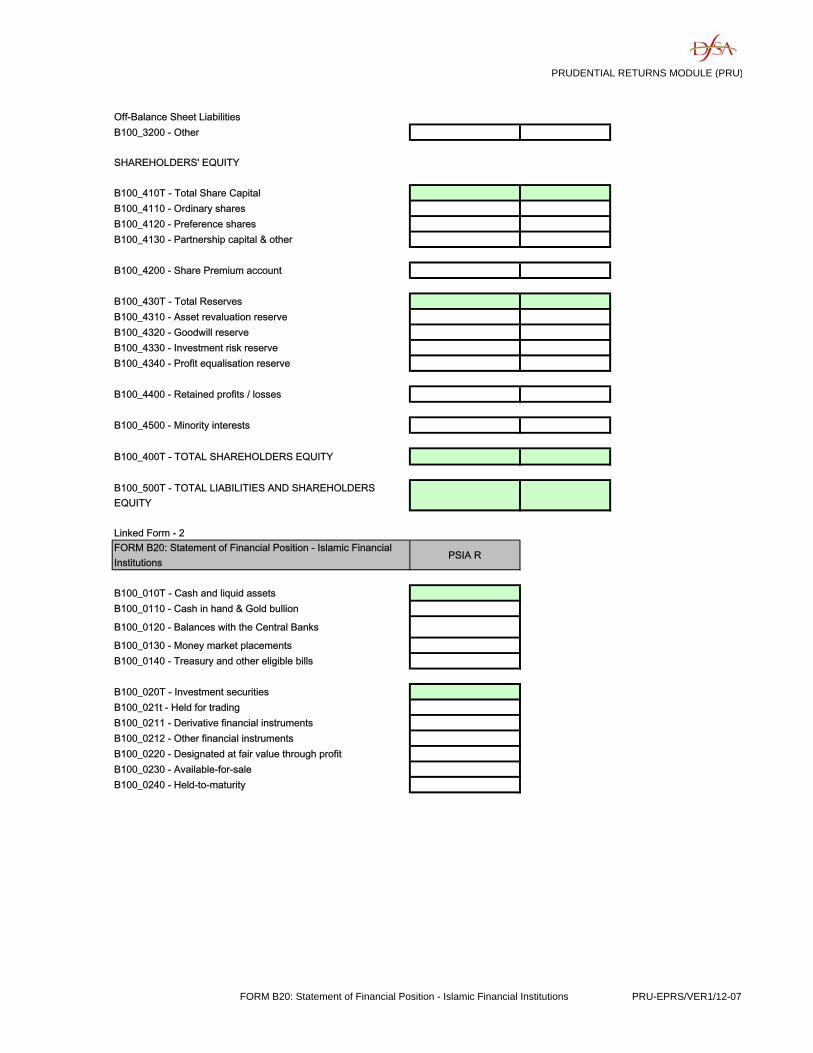

B100_3100 Liabilities relating to Restricted PSIA

Include under this section, off-balance sheet liabilities related to restricted PSIA investments.

B100_4110 Ordinary Shares Include in respect of this item the amount of ordinary share capital issued, reported at nominal paid up value. Do not report the unpaid element of partly paid shares or authorised but unissued share capital. Authorised Firms should exclude holdings in their own shares.

B100_4120 Preference Shares Report the value of the preference shares issued, which rank above ordinary shares in the event of liquidation.

B100_4130 Partnership Capital and other

Include here other types of equity which have the same properties of permanent share capital. This could include partnership capital accounts, capital items for unincorporated associations etc.

B100_4200 Share premium account

Any amounts received by the Authorised Firm in excess of the nominal paid up value.

B100_4310 Asset revaluation reserve

Include in this item, reserves arising from the revaluation of assets for which it has been necessary to set up this reserve.

B100_4320 Goodwill reserve Include reserves arising from purchased goodwill or other situations for which it has been necessary to set up this or any other reserve.

B100_4330 Investment Risk reserve

Prudential category 5 Authorised Firms should include in respect of this item the amount that is appropriated out of the income of investment account holders, after allocating the Mudarib share, in order to meet future losses attributable to investment account holders. Refer also to FAS 11 of AAOIFI.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_4340 Profit Equalisation Reserve

Prudential category 5 Authorised Firms should include in respect of this item the amount appropriated out of the Mudaraba income, before allocating the Mudarib share, in order to maintain a certain level of investment returns for investment account holders and to increase owners’ equity. Refer also to FAS 11 of AAOIFI.

B100_4350 General Reserve Include here all the reserves which have not been reported under any of the above categories in the section “Reserves” – B100_430T.

B100_430T Total Reserves This is calculated by EPRS and is calculated by adding the items. B100_4310 + B100_4320 + B100_4330 + B100_4340+ B100_4350.

B100_4500 Minority Interests Report amounts attributable to minority shareholders from the overall equity figure.

B100_400T Total shareholders’ equity

This is calculated by EPRS as the sum of items B100_430T, B100_410T, B100_4200 and B100_4400 less B100_4500.

B100_500T Total liabilities and shareholders’ equity

This is calculated by the EPRS as the sum of items B100_200T and B100_400T.

1.2 Instructional Guidelines – Form B10 – Appendix 1 – Detail of Non-Trading Book Assets Purpose Form B10A1 is intended to capture the information regarding the calculation of risk weighted assets in the Non-Trading Book of an Authorised Firm. Applicability This form is applicable to the Authorised Firms which are Domestic Firms, and are categorised under prudential categories 1, 2, and 3. This form is not applicable to the Authorised Firms operating through branches in the DIFC. Content The form is designed to capture the details regarding the risk weighted assets on the Non-Trading Book of an Authorised Firm and calculate the applicable capital charge. Structure of the form in EPRS B10A1 consists of three linked forms namely, “On Balance Sheet items”, “Off Balance sheet items” and “OTC derivative contracts”. Accordingly, all the on-balance sheet items should be analysed in the first linked form and the off balance sheet items in the second linked form. The OTC derivative contracts are analysed in the third linked form. The main form has the links to the three linked forms and also displays the result of each of the linked forms – the NTB risk-weighted assets calculated by each of the linked forms. The main form also calculates the total NTB risk-weighted assets and the CRCOM applicable to the Authorised Firm.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Instructional Guidelines:

1. Authorised Firms are referred to PIB Chapter 4 and Appendix 4 to understand the rationale behind risk weighting of assets in the Non-Trading Book and the relevant rules for risk weighting. In particular, PIB Section A4.3 contains detailed rules on classifying exposures in the appropriate risk weight categories. If an Authorised Firm is uncertain as to where to classify a particular exposure, it should contact DFSA to obtain this clarity. Particular care should be taken for exposures classified in anything other than the 100% risk weight category.

2. Among other things, risk weights may be reduced on Non-Trading Book items by

obtaining a guarantee from a third party or a party connected to the Authorised Firm (the “guarantor”). Provided the conditions laid out in PIB Rules A4.3.1 to A4.3.4 are met, the Authorised Firm may opt to use the Counterparty risk weight of the guarantor where this risk weight is less than that for the underlying Counterparty.

3. In respect of Counterparty weightings for exposures in the Non-Trading Book relating to

the Islamic contracts, Authorised Firms are referred PIB Rules 3.5.1 to 3.5.5. In particular, attention is drawn to the weightings referred to in table 2 by Islamic contract type

4. On-balance sheet items: Analyse each of the on-balance sheet items and classify them

into various risk weight categories as per applicable PIB rules referred above. The applicable risk weight categories are listed for each of the asset groups. The total value of assets classified into a particular risk weight category should be entered in the second column – titled “Non_Trading – Amount”, against the respective risk weight percentages. Amount of assets classified as forming part of the Trading Book under each of the major asset groups should be entered in the column titled –“Trading Book Amount”. However, Trading Book Amounts are captured primarily to ensure completeness and are not analysed across various risk weights.

5. Off-balance sheet items: All the off-balance sheet items should be analysed and

classified on the basis of the Credit Conversion factors applicable to them. Details of Credit Conversion Factors are set out in PIB Rules A4.3.10 to A4.3.14. These are then analysed and classified further into various risk weights as per rules in PIB Section A4.3. The second linked form which deals with off-balance sheet items provides for entry of the aggregate amount of off-balance sheet items classified into categories representing a specific credit conversion factor. Each credit conversion factor is dealt with in a separate table. For each credit conversion factor, the items are to be classified and aggregated into trading book and Non-Trading Book amounts. The aggregate Non-Trading Book amount for that particular credit conversion factor is then classified in to those pertaining to different risk weight categories. The total amount of items which deserve a specific risk weight should be entered in the respective row under the column titled “Non_Trading Amount”.

6. Specifically, guarantees given to a company not connected to the reporting institution

should be risk weighted at 100% and those for connected companies should be deducted from the reporting institution’s capital base.

7. Sale and Repurchase Agreements: Attention is drawn to PIB Rules A4.3.15 to 4.3.17

which note that the Counterparty weight of a repo agreement is by reference to the issuer of the asset subject to the agreement and not to the Counterparty to the repurchase agreement. The weight on a reverse repo is determined as if it were a collateralised loan to a Counterparty

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

8. Forward deposits placed: The risk weight should be determined according to the Counterparty with whom the deposit will be placed.

9. Endorsement of bills: Exposures arising out of endorsed bills not accepted by banks will

attract the Counterparty risk weighting of the issuer. If it has been endorsed by another bank, a reduced risk weighting applies.

10. Other commitments: Authorised Firms are referred to the detail of PIB Rules A4.4.1 to A

4.4.7 in respect of determining the maturity of commitments where they have been renegotiated or are linked commitments.

11. OTC derivative contracts: In the third linked form provide details regarding the OTC

derivative contracts. The calculation of the Credit Equivalent Amount is set out in PIB Rule A4.5.12. Authorised Firms are referred to the table in PIB Rule A4.5.14 which sets out the calculation of Potential Future Credit Exposures with detailed rules on how to net them being set out in PIB Rule A4.9.1.

12. Capital charge on the Non-Trading Book assets (i.e. CRCOM) is derived by multiplying

the sum of risk weighted assets from the Non-Trading Book by 8%. The main form of B10A1 indicates the Total Non-Trading Book risk weighted assets and the resultant CRCOM. CRCOM thus calculated is used in Form B60 for the purposes of calculating capital adequacy.

1.3 Instructional Guidelines – Form B10 – Appendix 2 – Detail of

Non-Market Risk in the Trading Book Purpose Form B10A2 is intended to capture the details regarding the non-market risk in the Trading Book of an Authorised Firm. Applicability This form is applicable to Authorised Firms which are Domestic Firms, and are categorised under prudential categories 1, 2, and 3. This form is not applicable to Authorised Firms operating through branches in the DIFC, IFIs and Authorised Firms managing PSIAs. Content The form is designed to capture the data on Counterparty credit risk exposures arising from unsettled transactions on markets, OTC derivative trades, repos and reverse repo transactions and deferred settlement transactions. included in the Trading Book of an Authorised Firm. The form also enables the calculation of amount at risk, weighted amount and applicable capital charge i.e. CPCOM.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Structure of the form in EPRS B10A2 consists of five linked forms covering the five main sections of this form dealing with “Counterparty risk on unsettled transactions”, “OTC Derivatives Capital Charge”, “Repos capital charge”, “Reverse repos capital charge” and “Deferred Settlement Transactions”. In each of the linked forms, the amount of potential loss and other information required to calculate the Potential Future Exposure are to be provided in the respective columns and the weighted amounts are calculated as per the applicable risk weights. The total capital charge for Counterparty risk reported in the linked forms will be displayed as a result on the main form. Instructional Guidelines The details for calculating the exposures on these risks is set out in PIB Section A4.5 which is the Appendix relating to Credit Risk.

Item Instructional Guidelines OTC derivatives For OTC derivatives, attention is drawn to PIB Rule A4.5.3 which

states that the maximum weighting is limited to 50%.

Repos and Reverse Repos For the Counterparty weights on Repos and Reverse Repos, attention is drawn to the Instruction Instructional Guidelines relating to Form B10, Item No. B100_1040.

Total Counterparty risk requirement for non market risk in the Trading Book

The total Counterparty risk requirement for non-market risk in the trading book (“CPCOM”) is the sum of the capital charges arising from Delivery Versus Payment transactions, Free Deliveries, OTC Derivatives, Repos, Reverse Repos and Deferred Settlement Transactions. CPCOM thus calculated is used in Form B60 for the purposes of calculating capital adequacy.

1.4 Instructional Guidelines – Form B10 – Appendix 3 – Market Risk in the Trading Book Purpose Form B10A3 is intended to capture the data on capital charges applicable to market risk exposures in the Trading Book of an Authorised Firm. Applicability This form is applicable to the Authorised Firms which are Domestic Firms categorised under prudential categories 1 and 2. This form is not applicable to the Authorised Firms operating through branches in the DIFC, IFIs and Authorised Firms managing PSIAs.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Content The form is designed to enable Authorised Firms to report the capital charges applicable to the various elements of market risk exposures in their Trading Book and the resultant capital charge for market risk i.e. Market Risk Capital Requirement (MRCOM). Structure of the form in EPRS B10A3 is presented as a single form in the EPRS.

Instructional Guidelines 1. DFSA acknowledges that even for Authorised Firms with relatively straightforward

exposures on the trading books, the underlying calculations for various market risks can be detailed and complex. DFSA requires Authorised Firms to report only the summary capital charge for various elements of market risk recognised in the rules under PIB Chapter 5 of the DFSA Rulebook. However, DFSA expects Authorised Firms to maintain detailed audit trails that substantiate the capital charges reported in this form. Authorised Firms are also reminded that they should make this information available for review as and when required.

2. In the event of any uncertainty, Authorised Firms are advised to contact their supervisor

for clarity. Authorised Firms are expected to review the material set out Appendix 5 of the PIB module with care given the multiplicity of methods that can be used to calculate the capital requirement on Interest Rate Risk, Equity Risk, FX Risk, Commodities Risk Options Risk and Securities Underwriting Risk.

3. Where Authorised Firms intend to use internally developed market risk models for the

purposes of valuing positions and calculating capital requirements, particular attention is drawn to PIB Section A5.8 and the qualitative criteria.

Item No. Item Instructional Guidelines B103_1100, B103_1200, B103_1400, B103_1500, B103_1600

Various risk requirements

An Authorised Firm’s total Trading Book capital requirement is as defined in PIB Rule 2.8.3. With the exception of the foreign exchange risk requirement, the total risk requirements as calculated for Interest rate, Equity, Commodities, Options and Securities Underwriting transactions are transferred to Form B60 under the section titled Trading Book Capital requirement (item nos. B103_1100 to B103_1600).

B103_1300

Foreign exchange risk requirement

The Foreign Exchange risk capital requirement is included in the Form B60 under the Non Trading Book Capital requirement and is transferred to item no. B103_1300 (refer PIB Rule 2.8.3).

B103_000T Total Trading Book capital requirement

The total Trading Book Capital requirement calculated in this form is transferred to the Form B 60, item no B600_141T.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

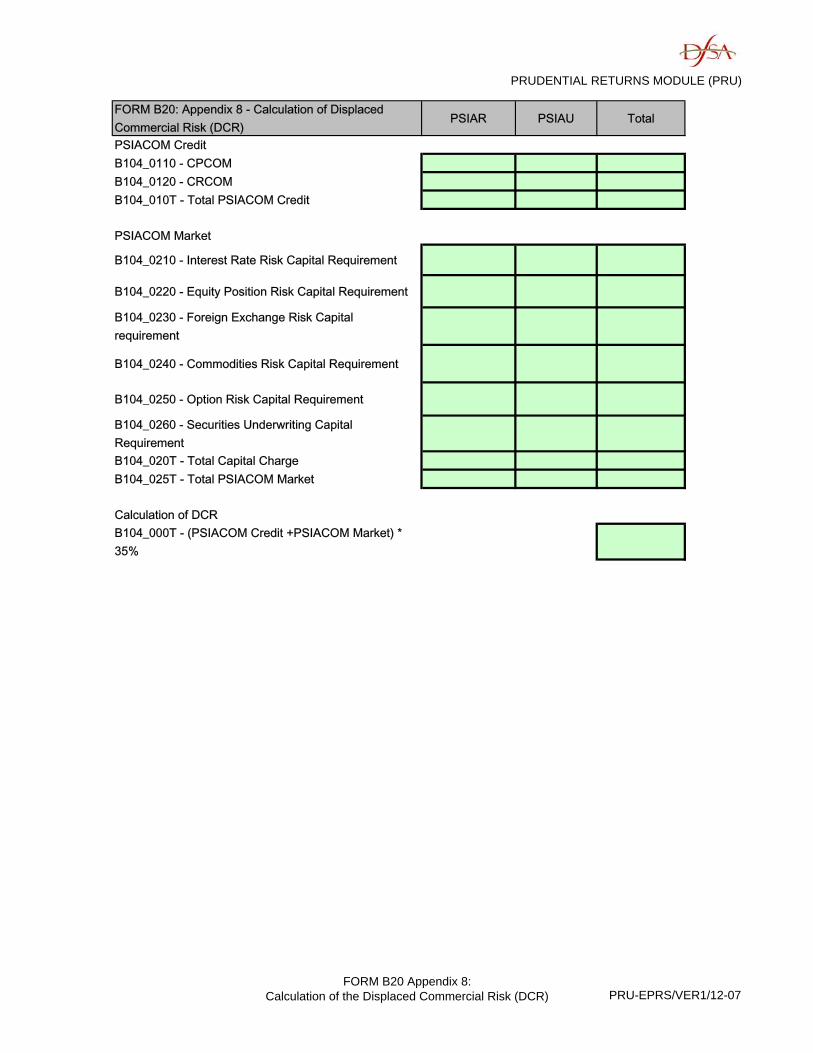

1.5 Instructional Guidelines – Form B10 – Appendix 4 – Calculation of the DCR

Purpose Form B10A4 is intended to reflect the data on different elements of the Displaced Commercial Risk Capital Requirement faced by Authorised Firms. Applicability This form is applicable to Authorised Firms falling under prudential categories 1, 2, or 3 and operating an Islamic window to manage PSIAs. Note that the DCR only applies in respect of restricted and unrestricted PSIA accounts. Content The form is designed to capture the credit and market risk capital requirements pertaining to the assets of both PSIA restricted and PSIA unrestricted accounts and calculate the Displaced Commercial Risk capital charge in respect of the PSIAs managed by an Authorised Firm as per applicable PIB rules. Structure of the form in EPRS The form does no allow any manual data entry. The values required for completion of this form are directly sourced from the detailed appendices relating to CRCOM, CPCOM and MRCOM pertaining to the PSIA restricted and unrestricted businesses (Appendices B20A2, B20A3, B20A5, B20A6 and B20A7 respectively) that precede this form. So, Authorised Firms are advised to complete the appendices referred above before attempting to complete this form.

Instructional Guidelines DCR is defined in PIB Section 3.4. Authorised Firms are advised to refer to that Section to understand why DCR arises and how it is calculated. Authorised Firms are reminded that DCR only applies in respect of PSIA assets of both the restricted and unrestricted type. As noted earlier, this Appendix aggregates totals from the detailed appendices that precede this form.

Item No. Item Instructional Guidelines B104_010T PSIACOM Credit PSIACOM Credit comprised CRCOM and CPCOM calculated on

PSIA assets. It is the sum of item nos. [B104_0110 and B104_0120] below.

B104_0110 CPCOM CPCOM for PSIAu comes from Form B20A5, and for PSIAR from Form B20A6.

B104_0120 CRCOM CRCOM for PSIAu comes from Form B20A2, and for PSIAR from Form B20A3.

B104_025T PSIACOM Market The figures for PSIACOM Market are all derived from Form B20A7.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B104_000T Calculation of DCR DCR represents (PSIACOM Credit +PSIACOM Market) * 35%. This figure is transferred to Form B60, item no B104_000T.

1.6 Instructional Guidelines – Form B20 – Statement of Financial Position – Islamic Financial Institutions Purpose Form B20 – Balance sheet is intended to capture the financial position of an Islamic Financial Institution (IFI) at the end of the reporting period. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categorised 1, 2, 3 and managing PSIAs within an Islamic Window . Content The form is designed to capture information pertaining to the Authorised Firm’s on-balance sheet and off-balance sheet assets, liabilities and shareholders’ equity at a given point in time. The form enables reporting of assets and liabilities pertaining to the Restricted and Unrestricted PSIA accounts separately, apart from presenting the balance sheet of the IFI. Structure of the form in EPRS The form is split into two linked forms. The first linked form is intended to capture information pertaining to assets and liabilities on the Authorised Firm’s own balance sheet which are its self-financed business and the assets and liabilities of Unrestricted PSIAs managed by the Authorised Firm. The second linked form is designed to capture information pertaining to the assets and liabilities of Restricted PSIAs managed by the Authorised Firm. Instructional Guidelines The form enables effectively three sets of returns on balance sheet information for Authorised Firms using this form. Whilst AAOIFI permits unrestricted PSIA assets to be commingled with self financed assets for balance sheet reporting purposes, the need to maintain separate records for each asset class is paramount. Restricted PSIA assets and liabilities cannot be commingled with the former and should be reported off balance sheet. In the event of any uncertainty, Authorised Firms are required to consult with DFSA to obtain the necessary clarity.

Item No Item Instructional Guidelines

B100_0110 Cash in hand & Gold bullion

Include, for example, the following amounts: • Notes and coins; • Long positions in Gold bullion (including Tola Bars);

B100_0120 Balances with the Central Banks

Amounts placed with central banks including funds required to be placed on deposit with central banks and monetary authorities.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_0130 Money market placements

Include deposits at call and other money market placements with banks or other money market participants.

B100_0140 Treasury bills and other eligible bills

Treasury bills issued by the national governments or by the Central banks on behalf of the governments. Also include bills issued by other entities, which are eligible for rediscounting with the central bank.

B100_0211 Derivative financial instruments

The assets reported here should include, but are not limited to, positions representing the following instruments, recorded at fair value:

• Forward and Futures contracts in currencies, interest rates and other financial assets

• Forward rate agreements • Currency and interest rate swaps • Credit derivatives • Option contracts on currency, interest rate and other financial

assets. These derivatives include both the exchange-traded and over-the-counter versions. Derivatives held for hedging purposes should be included under section B100_030T.

B100_0212 Other financial instruments (held for trading)

Include investments acquired principally for the purpose of selling or repurchasing them in the near term for short-term-profit-taking. This would include but not limited to, debt, equity and hybrid instruments

B100_0220 Other financial instruments designated at fair value through profit and loss

Include all financial instruments which are, upon initial recognition, designated by the entity as financial assets to be measured at fair value through profit or loss other than the trading securities included in B100_0211 and B100_0212.

B100_0230 Available-for-sale Include non-derivative financial assets that are designated as available for sale by the firm or that have not been classified under any of the other categories of investments.

B100_0240 Held-to-maturity Include non-derivative financial assets with fixed or determinable payments and fixed maturity that the firm has positive intention and ability to hold to maturity.

B100_040T Loans and advances Under this section include the amounts arising from, for example: • Revolving credit facilities; • Credit cards outstanding balances; • Housing loans (both variable and fixed rates); • Term loans (both variable and fixed rates); • The book value of assets leased out under finance lease agreements; • Loans made under conditional hire purchase contracts; • Advances purchased by or assigned to the reporting institutions,

factoring or similar arrangements • Other loans and advances.

The items listed above are indicative examples and are not exhaustive universe of items to be reported under this item.

The amounts reported should be gross of provisions (as specific and general provisions should be reported in the Liabilities section of the balance sheet) and net of interest receivable.

B100_0510 Murabaha and Report here all receivables relating to Murabaha and Istisna’a contracts.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Istisna’a receivables Refer to FAS 2 and FAS 10 of AAOIFI respectively. B100_0520 Ijarah assets and

receivables Include Ijarah assets net of depreciation/ amortisation and Ijarah receivables. Refer to FAS 8 of AAOIFI.

B100_0530 Mudaraba Financing Financing provided on a Mudaraba basis should be reported here. Refer to FAS 3 of AAOIFI.

B100_0540 Musharaka Financing

Report financing provided on a Musharaka basis. Refer to FAS 4 of AAOIFI. Investment in the share capital of another company should be reported under “Other investments”, under B100_0550.

B200_0550 Salam Financing provided on Salam contract should be reported here. Refer to FAS 7 of AAOIFI.

B200_0560 Parallel Istisna’a Parallel Istisna’a receivables/assets should be reported here. Refer to FAS 10 of AAOFI.

B100_0550 Other investments Include any other investments undertaken through Islamic contracts, including Parallel Istisna’a assets (refer FAS 10 of AAOIFI) and capital provided on Salam contracts (refer FAS 7 AAOIFI).

B100_0700 Fixed assets Include, for example, the value of the following: • Plant and equipment, the residual value of items leased out under an

operating lease (excluding balances relating to named Ijarah assets which should be included separately under B100_0520);

• Own premises being occupied or developed for occupation by the Authorised Firm, property (excluding property acquired / held available for sale which should be included in “Other Assets”, B100_0920).

The amounts reported here should be net of accumulated depreciation and amortisation.

B100_0810 Goodwill Include amounts relating to any purchased goodwill. B100_0820 Other intangible

assets Items to be included, for example, but are not limited to:

• Capitalised development costs • Brand names, trademarks and similar rights • Licences and exchange seats which may be held as part of the

Authorised Firm’s trading requirement. Off Balance sheet items

B100_1010 Direct credit substitutes

These relate to the financial requirements of Counterparty where the risk of loss to the Authorised Firm on the transaction is equivalent to that arising from a direct claim on the Counterparty. The indicative examples of items to be Included here are • Guarantees of a financial nature to stand behind the current obligations

of customers (e.g. loan guarantees); • Guarantees of leasing operations; • Letters of Credit and Stand-by Letters of Credit to the extent that they

do not qualify for inclusion in item B100_1030 “Trade related contingents” below;

• Guarantees of a capital nature such as undertakings given to a non-bank financial company which are considered as capital by the appropriate regulatory body. Guarantees given to a company not connected to the reporting institution should be risk weighted at 100% and those for connected companies should be deducted from the reporting institution’s capital base.

• Acceptances granted and risk participation in bankers’ acceptances. Where the Authorised Firm’s own acceptances have been discounted by that institution the nominal value of the bills held should be

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

deducted from the nominal amount of the bills issued under the facility and a corresponding on-balance sheet entry made.

B100_1020 Transaction related contingents

These exposures relate to the on-going trading activities of a Counterparty where the risk of loss to the Authorised Firm depends on the likelihood of a future event which is independent of the creditworthiness of the Counterparty. They are essentially guarantees that support particular non financial obligations rather than a customer’s financial obligations. Include here: • Advance payment guarantees • Performance bonds including bid or tender bonds, warranties and

indemnities (indemnities given for lost share certificates or bills of lading and guarantees of the validity of papers rather than of payment under certain conditions should be reported here);

Stand-by Letters of Credit relating to a particular contract or to non-financial transactions (including arrangements backing, inter alia, subcontractors’ and supplier’s performance, labour and materials, contracts and construction tenders/bids).

B100_1030 Trade related contingents

Report short term self-liquidating trade related items such as documentary letters of credit issued by the Authorised Firm that are collateralised by the underlying shipment i.e. the credit provides for the Authorised Firm to retain title to the underlying shipment. L/C’s issued without provision for the Authorised Firm to retain title to the underlying shipment should be reported under direct credit substitutes above.

B100_1040 Sale and Repurchase Agreements

In this item, report only the sale and repurchase agreements where the asset sold is not reported on the balance sheet. Where the asset is off-balance sheet, the appropriate Counterparty weighting is determined by the issuer of the security and not according to the Counterparty with whom the transaction has been undertaken.

B100_1050 Forward Assets Purchases

The appropriate Counterparty weighting should be determined by the asset to be purchased and not the Counterparty with whom the contract has been entered into. Include commitments for loans and other on-balance sheet items with definitive drawdown schedules. Exclude foreign currency spot deposits with value date of up to two business days after trade date.

B100_1060 Forward Deposits Placed

Relates to agreements between two parties whereby one will pay and the other receive an agreed rate of interest on a deposit to be placed by one with the other at some pre-determined rate in the future. Exclude foreign currency spot deposits with value date of up to two business days after trade date.

B100_1070 Uncalled partly- paid shares and securities

Only include here if there is a specific date for a call. If there is no specific date for a call, the item should be included as a long term commitment under item no. B100_1122 “Other Commitments”.

B100_1080 NIF’s and RUF’s Note issuance and revolving underwriting facilities should include the Authorised Firm’s underwriting obligations of any maturity. Where the facility has been drawn down by the borrower and the notes are held by someone other than the Authorised Firm, the underwriting obligation should continue to be reported at the nominal amount.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_1090 Endorsement of Bills These should be reported at the full nominal amount, less any amount for

bills which the Authorised Firm currently holds but had previously endorsed.

B100_1111 & B100_1122

Other Commitments All other undrawn commitments are reportable here, divided into commitments under and over one year.

B100_000T to B100_100T

Assets funded by restricted PSIAs

The methodology for calculating exposures financed by PSIAs are, in principle, no different to calculating exposures for a reporting institution’s self financed assets. All the Instructional Guidelines above apply in their entirety unless stated otherwise.

B100_210T Deposits In this section, identify and report deposits due to banks and financial institutions in item no B100_2110. All other deposits are to be reported as deposits due to other customers - item no B100_2120.

B100_230T Provisions All specific and general provisions in respect of all assets, including loans and advances and other receivables should be reported under this section. Exclude provisions against Islamic contracts which should be reported in item no B100_2640.

B100_260T Liabilities arising from Islamic contracts

Liabilities arising from Islamic contracts include advances received against Salam contracts (defined in Para 3 and 19 of FAS 7 issued by AAOIFI and Ijarah investment payables (refer to FAS 8 of AAOIFI). Report any provisions against Islamic contracts in item B100_2640.

Off balance sheet liabilities

Liabilities relating to Restricted PSIA

Include under this section, off-balance sheet liabilities related to restricted PSIA investments.

B100_4110 Ordinary Shares Include in respect of this item the amount of ordinary share capital issued, reported at nominal paid up value. Do not report the unpaid element of partly paid shares or authorised but unissued share capital. Authorised Firms should exclude holdings in their own shares.

B100_4120 Preference Shares Report the value of the preference shares issued, which rank above ordinary shares in the event of liquidation.

B100_4130 Partnership Capital and other

Include here other types of equity which have the same properties of permanent share capital. This could include partnership capital accounts, capital items for unincorporated associations etc.

B100_4200 Share premium account

Any amounts received by the authorised institution in excess of the nominal paid up value.

B100_4310 Asset revaluation reserve

Include in this item, reserves arising from the revaluation of assets for which it has been necessary to set up this reserve.

B100_4320 Goodwill reserve Include reserves arising from purchased goodwill or other situations for which it has been necessary to set up this or any other reserve.

B100_4330 Investment Risk reserve

Prudential category 5 Authorised Firms should include in respect of this item the amount that is appropriated out of the income of investment account holders, after allocating the Mudarib share, in order to meet future losses attributable to investment account holders. Refer also to FAS 11 of AAOIFI.

B100_4340 Profit Equalisation reserve

Category 5 Authorised Firms should include in respect of this item the amount appropriated out of the Mudaraba income, before allocating the Mudarib share, in order to maintain a certain level of investment returns for investment account holders and to increase owners’ equity. Refer also to FAS 11 of AAOIFI.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

B100_430T Total Reserves This is calculated by the EPRS and is calculated by adding the items. B100_4310 + B100_4320 + B100_4330 + B100_4340+ B100_4350.

B100_4500 Minority Interests Report amounts attributable to minority shareholders from the overall equity figure.

B100_400T Total shareholders’ equity

This is calculated by the EPRS as the sum of items B100_430T, B100_410T, B100_4200 and B100_4400 less B100_4500.

B100_500T Total liabilities and shareholders’ equity

This is calculated by the EPRS as the sum of items B100_200T and B100_400T.

1.7 Instructional Guidelines – Form B20 – Appendix 1 – Detail of Non-Trading Book Assets - self-financed Purpose Form B20A1 is intended to capture the details regarding the calculation of risk weighted assets in respect of the self-financed assets in the Non-Trading Book of an Authorised Firm. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categories 1,2,3 which are also involved in managing PSIAs within an Islamic Window . Content The form is designed to capture the details regarding the risk weighted assets on the Non-Trading Book and the applicable capital charge. Structure of the form in EPRS B20A1 consists of three linked forms namely, “On Balance Sheet items”, “Off Balance sheet items” and “OTC derivative contracts”. Accordingly, all the on balance sheet items should be analysed in the first linked form and the off balance sheet items in the second linked form. The OTC derivative contracts are analysed in the third linked form. The main form has the links to the three linked forms and also displays the result of each of the linked forms – the NTB risk-weighted assets calculated by each of the linked forms. The main form also calculates the total NTB risk-weighted assets and the CRCOM applicable to the Authorised Firm.

Instructional Guidelines

1. This form is meant for entry of data on exposures relating to self financed assets or

assets on the balance sheet of the Authorised Firm. 2. Authorised Firms are referred to PIB Chapter 4 and Appendix 4 to understand the

rationale behind risk weighting of assets in the Non-Trading Book and the relevant rules

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

for risk weighting. In particular, PIB Section A4.3 contains detailed rules on classifying exposures in the appropriate risk weight categories. If an Authorised Firm is uncertain as to where to classify a particular exposure, it should contact DFSA to obtain this clarity. Particular care should be taken for exposures classified in anything other than the 100% risk weight category.

3. Among other things, risk weights may be reduced on Non-Trading Book items by

obtaining a guarantee from a third party or a party connected to the Authorised Firm (the “guarantor”). Provided the conditions laid out in PIB Rules A4.3.1 to A4.3.4 are met, the Authorised Firm may opt to use the Counterparty risk weight of the guarantor where this risk weight is less than that for the underlying Counterparty.

4. In respect of Counterparty weightings for exposures in the Non-Trading Book relating to

the Islamic contracts, Authorised Firms are referred PIB Rules 3.5.1 to 3.5.5. In particular, attention is drawn to the weightings referred to in table 2 by Islamic contract type.

5. On balance sheet items: Analyse each of the on-balance sheet items and classify them

into various risk weight categories as per applicable PIB Rules referred above. The applicable risk weight categories are listed for each of the asset groups. The total value of assets classified into a particular risk weight category should be entered in the second column – titled “Non_Trading – Amount”, against the respective risk weight percentages. Amount of assets classified as forming part of the Trading Book under each of the major asset groups should be entered in the column titled –“Trading Book Amount”. However, Trading Book Amounts are captured primarily to ensure completeness and are not analysed across various risk weights.

6. Off-balance sheet items: All the off-balance sheet items should be analysed and

classified on the basis of the Credit Conversion factors applicable to them. Details of Credit Conversion Factors are set out in PIB Rules A4.3.10 to A4.3.14. These are then analysed and classified further into various risk weights as per rules in PIB Section A4.3. The second linked form which deals with off-balance sheet items provides for entry of the aggregate amount of off-balance sheet items classified into categories representing a specific credit conversion factor. Each credit conversion factor is dealt with in a separate table. For each credit conversion factor, the items are to be classified and aggregated into trading book and Non-Trading Book amounts. The aggregate Non-Trading Book amount for that particular credit conversion factor is then classified in to those pertaining to different risk weight categories. The total amount of items which deserve a specific risk weight should be entered in the respective row under the column titled “Non_Trading Amount”.

7. Specifically, guarantees given to a company not connected to the reporting institution

should be risk weighted at 100% and those for connected companies should be deducted from the reporting institution’s capital base.

8. Sale and Repurchase Agreements: Attention is drawn to PIB Rules A4.3.15 to 4.3.17

which note that the Counterparty weight of a repo agreement is by reference to the issuer of the asset subject to the agreement and not to the Counterparty to the repurchase agreement. The weight on a reverse repo is determined as if it were a collateralised loan to a Counterparty

9. Forward deposits placed: The risk weight should be determined according to the

Counterparty with whom the deposit will be placed.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

10. Endorsement of bills: Exposures arising out of endorsed bills not accepted by banks will attract the Counterparty risk weighting of the issuer. If it has been endorsed by another bank, a reduced risk weighting applies.

11. Other commitments: Authorised Firms are referred to the detail of PIB Rules A4.4.1 to A

4.4.7 in respect of determining the maturity of commitments where they have been renegotiated or are linked commitments.

12. OTC derivative contracts: In the third linked form provide details regarding the OTC

derivative contracts. The calculation of the Credit Equivalent Amount is set out in PIB Rule A4.5.12. Authorised Firms are referred to the table in PIB Rule A4.5.14 which sets out the calculation of Potential Future Credit Exposures with detailed rules on how to net them being set out in PIB Rule A4.9.1.

13. Capital charge on the Non-Trading Book assets (i.e. CRCOM) is derived by multiplying

the sum of risk weighted assets from the Non-Trading Book by 8%. The main form of B10A1 indicates the Total Non-Trading Book risk weighted assets and the resultant CRCOM. CRCOM thus calculated is used in Form B60 for the purposes of calculating capital adequacy.

1.8 Instructional Guidelines – Form B20 – Appendix 2 – Detail of

Non-Trading Book Assets - PSIA Unrestricted (PSIAU).

Purpose Form B20A2 is intended to capture the details regarding the calculation of risk weighted assets in respect of the PSIAU assets in the Non-Trading Book of an Authorised Firm. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and to Authorised Firms classified under categories 1, 2, 3 and involved in managing PSIAs within an Islamic Window. Content The form is designed to capture the details regarding the risk weighted assets on the Non-Trading Book and the applicable capital charge which is essential for calculation of the DCR capital requirement. Structure of the form in EPRS This form is identical to the form B20A1 in EPRS.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Instructional Guidelines 1. All the Instructional Guidelines provided for form B20A1 are applicable to this form

also. However, this form is meant only for exposures relating to assets funded by the PSIAU investments.

2. Note that the total CRCOM (i.e. the capital charge) figure as calculated in this form and

reported on the main form is transferred to Form B20A8, item no B104_0120.

1.9 Instructional Guidelines – Form B20 – Appendix 3 – Detail of Non-Trading Book Assets - PSIA Restricted (PSIAR) Purpose Form B20A3 is intended to capture the details regarding the calculation of risk weighted assets in respect of the PSIAR assets in the Non-Trading Book of an Authorised Firm. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and to Authorised Firms classified under categories 1, 2, 3 and involved in managing PSIAs within an Islamic Window. Content The form is designed to capture the details regarding the risk weighted assets on the Non-Trading Book and the applicable capital charge which is essential for calculation of the DCR capital requirement. Structure of the form in EPRS This form is identical to the form B20A1 in EPRS.

Instructional Guidelines

1. All the Instructional Guidelines provided for form B20A1 are applicable to this form

also. However, this form is meant only for exposures relating to assets funded by the PSIAR investments.

2. Note that the total CRCOM (i.e. the capital charge) figure as calculated in this form and

reported on the main form is transferred to Form B20A8, item no B104_0120.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

1.10 Instructional Guidelines – Form B20 – Appendix 4 – Detail of Non-Market Risk in Trading Book - Self-financed

Purpose Form B20A4 is intended to capture the details regarding the non-market risk in the Trading Book of an Authorised Firm, particularly those arising from exposures self-financed by the firm. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categories 1, 2, 3 and managing PSIAs within an Islamic Window. Content The form is designed to capture the data on Counterparty credit risk exposures arising from unsettled transactions on markets, OTC derivative trades, repos and reverse repo transactions and deferred settlement transactions included in the Trading Book of an Authorised Firm. The form also enables the calculation of amount at risk, weighted amount and applicable capital charge i.e. CPCOM. Structure of the form in EPRS B20A4 consists of five linked forms covering the five main sections of this form dealing with “Counterparty risk on unsettled transactions”, “OTC Derivatives Capital Charge”, “Repos capital charge”, “Reverse repos capital charge” and “Deferred Settlement Transactions”. In each of the linked forms, the amount of potential loss and other information required to calculate the Potential Future Exposure are to be provided in the respective columns and the weighted amounts are calculated as per the applicable risk weights. The total capital charge for Counterparty risk reported in the linked forms will be displayed as a result on the main form.

Instructional Guidelines This form is restricted to calculating the risk weighted capital charge for self financed assets only. The details for calculating the exposures on these risks is set out in PIB Section A4.5 of the DFSA Rulebook.

Item Instructional Guidelines OTC derivatives For OTC derivatives, attention is drawn to PIB Rule A4.5.3 which

states that the maximum weighting is limited to 50%.

Repos and Reverse Repos For the Counterparty weights on Repos and Reverse Repos, attention is drawn to the Instructional Guidelines relating to Form B20, Item No. B100_1040.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Total Counterparty risk requirement for non market risk in the Trading Book

The total Counterparty risk requirement for non-market risk in the trading book (“CPCOM”) is the sum of the capital charges arising from Delivery Versus Payment transactions, Free Deliveries, OTC Derivatives, Repos, Reverse Repos and Deferred Settlement Transactions. CPCOM thus calculated is used in Form B60 for the purposes of calculating capital adequacy.

1.11 Instructional Guidelines – Form B20 – Appendix 5 – Detail of

Non-Market Risk in Trading Book - PSIA Unrestricted (PSIAU)

Purpose Form B20A5 is intended to capture the details regarding the non-market risk in the Trading Book of an Authorised Firm, particularly those arising from exposures funded by the PSIAU funds. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categorised 1, 2, 3 and managing PSIAs within an Islamic Window. Content & Structure of the form in EPRS This form is identical to the form B20A4 in respect of its content and structure in EPRS. Instructional Guidelines All the Instructional Guidelines provided for form B20A4 are applicable to this form also. However, this form is meant only for exposures relating to assets funded by the PSIAU investments. Note that the total CPCOM (i.e. the capital charge) figure as calculated in this form and reported on the main form is transferred to Form B20A8, item no B104_0110.

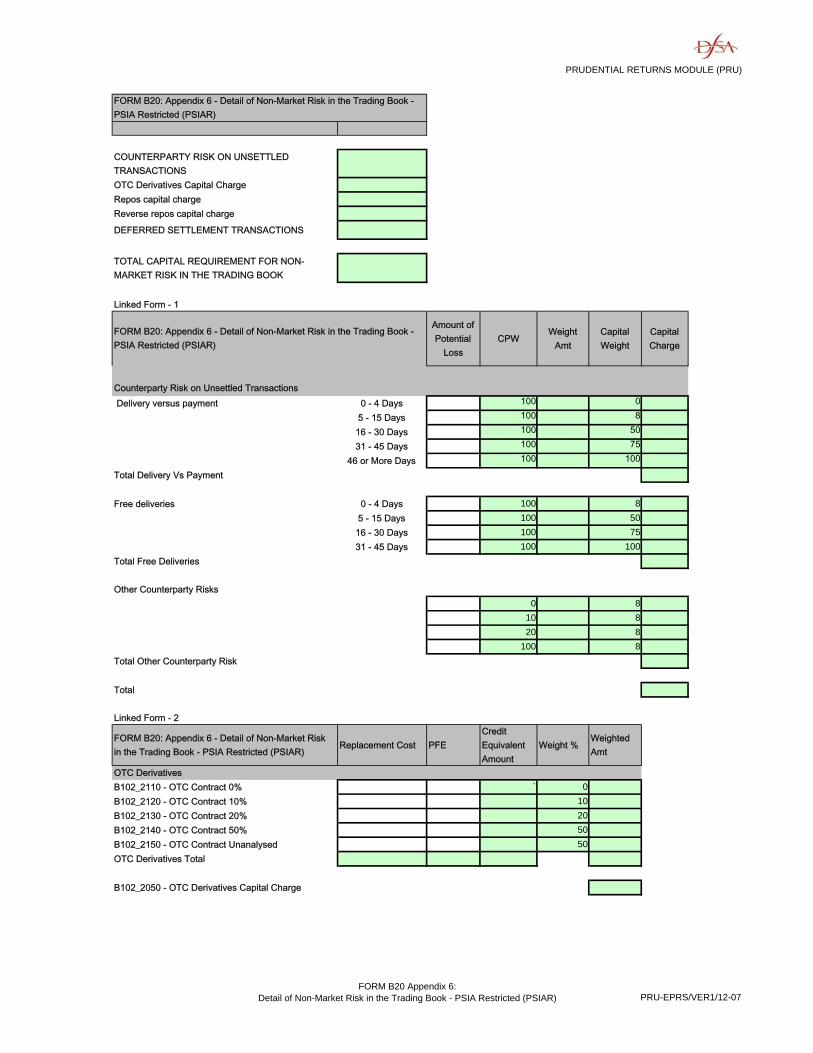

1.12 Instructional Guidelines – Form B20 – Appendix 6 – Detail of

Non-Market Risk in Trading Book - PSIA Restricted (PSIAR)

Purpose Form B20A6 is intended to capture the details regarding the non-market risk in the Trading Book of an Authorised Firm, particularly those arising from exposures funded by the PSIAR.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categories 1, 2, 3 and managing PSIAs within an Islamic Window. Content & Structure of the form in EPRS This form is identical to the form B20A4 in respect of its content and structure in EPRS.

Instructional Guidelines

All the Instructional Guidelines provided for form B20A4 are applicable to this form also. However, this form is meant only for exposures relating to assets funded by the PSIAR investments. Note that the total CPCOM (i.e. the capital charge) figure as calculated in this form and reported on the main form is transferred to Form B20A8, item no B104_0110.

1.13 Instructional Guidelines – Form B20 – Appendix 7 – Detail of

Market Risk in the Trading Book

Purpose Form B20A7 is intended to capture the details regarding the market risk in the Trading Book of an Authorised Firm. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categories 1,2,3 and managing PSIAs within an Islamic Window . Content The form is designed to enable Authorised Firms to report the capital charges applicable to the various elements of market risk exposures in their Trading Book and the resultant capital charge for market risk i.e. MRCOM. Structure of the form in EPRS The form is split into two linked forms namely, “Interest Rate Risk Capital Requirement” and “All Other Risks”.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

Instructional Guidelines

1. The first linked form (“Interest Rate Risk Capital Requirement”) enables the calculation of the Interest Rate Risk Capital Requirement. Note that the relevant amounts have to be entered in respect of self financed, PSIA Unrestricted and PSIA Restricted businesses, separately in the respective columns provided.

2. In the second linked (“All Other Risk”) form summary amounts of all other components

of market risk capital requirement such as Equity Risk, Foreign Exchange Risk, Commodities Risk, Options Risk and Securities Underwriting Risk are required to be entered. The relevant amounts should be provided for self financed, PSIA Unrestricted and PSIA Restricted business separately in the respective columns provided.

3. Authorised Firms are asked to review the rules set out PIB Appendix 5 with care given

the multiplicity of methods that can be used to calculate the capital requirement on Interest Rate Risk, Equity Risk, FX Risk, Commodities Risk Options Risk and Securities Underwriting Risk.

4. DFSA acknowledges that even for Authorised Firms with relatively straightforward

exposures on the trading books, the underlying calculations for various market risks can be detailed and complex. DFSA requires only the summary numbers to be reported but expects Authorised Firms to maintain detailed audit trails that substantiate the risk requirements. Authorised Firms are also reminded that they should make this information available for review as and when required.

5. In the event of any uncertainty, Authorised Firms are advised to contact their supervisor

for clarity. 6. Where Authorised Firms intend to use internally developed market risk models for the

purposes of valuing positions and calculating capital requirements, particular attention is drawn to PIB Section A5.8 and the qualitative criteria.

Item No. Item Instructional Guidelines B103_1100, B103_1200, B103_1400, B103_1500, B103_1600

Various risk requirements

The total capital requirements for interest rate, equity position risk, Commodities, Options and Securities Underwriting exposures in respect of self financed assets is transferred to Form B60 (item nos. B103_1100 to B103_1600). The capital requirements for PSIA funded assets (both unrestricted and restricted), including the Foreign exchange risk requirement is transferred to Form B20A8 for the calculation of the Displaced Commercial Risk Charge.

B103_1300

Foreign exchange risk requirement

The FX risk capital requirement arising from self financed assets is transferred to Form B60 under Non-Trading Book Capital requirement to item no. B103_1300 (refer PIB Rule 2.8.3).

B103_000T Total Trading Book Capital Requirement

The total Trading Book Capital requirement (i.e. MRCOM) here is transferred to the Form B60, item no B600_141T.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

1.14 Instructional Guidelines – Form B20 – Appendix 8 – Calculation of the Displaced Commercial Risk (DCR) Purpose Form B20A8 is intended to capture the details regarding the Displaced Commercial Risk charge. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categories 1,2,3 and managing PSIAs within an Islamic Window. Note that the DCR only applies in respect of PSIA assets for both the restricted and unrestricted categories. Content The form is designed to capture the details regarding the Displaced Commercial Risk charge in respect of Islamic Finance Business. Structure of the form in EPRS The form does no allow any manual data entry. The values in this form are directly transferred by EPRS from the detailed forms relating to the calculation of CRCOM, CPCOM and MRCOM in respect of PSIAR and PSIAU businesses (Appendices B20A2, B20A3, B20A5, B20A6 and B20A7 respectively) that precede it. So, Authorised Firms are advised to complete the appendices referred above before attempting to complete this form.

Instructional Guidelines

DCR is defined in PIB Section 3.4. Authorised Firms are advised to refer to that Section to understand why DCR arises and how it is calculated. Authorised Firms are reminded that DCR only applies in respect of PSIA assets of both the restricted and unrestricted type. As noted earlier, this Appendix aggregates totals from the detailed appendices that precede this form.

Item No. Item Instructional Guidelines B104_010T PSIACOM Credit PSIACOM Credit is comprised of CRCOM and CPCOM and is

calculated on PSIA assets. It is the sum of item nos. [B104_0110 and B104_0120] below.

B104_0110 CPCOM CPCOM for PSIAu comes from Form B20A5, and for PSIAR from Form B20A6.

B104_0120 CRCOM CRCOM for PSIAu comes from Form B20A2, and for PSIAR from Form B20A3.

B104_025T PSIACOM Market The figures for PSIACOM Market are all derived from Form B20A7. B104_000T Calculation of DCR DCR represents (PSIACOM Credit +PSIACOM Market) * 35%. This

figure is transferred to Form B60, item no B104_000T.

PRUDENTIAL RETURNS MODULE (PRU)

PRU-EPRS/VER1/12-07

1.15 Instructional Guidelines – Form B20 – Appendix 9 – Analysis of Reserves Movement Purpose Form B20A9 is intended to capture the details regarding the changes in the reserves pertaining to the Islamic Finance Business. Applicability This form is applicable to the Authorised Firms categorised under prudential category 5 and Authorised Firms classified under categorised 1,2,3 and managing PSIAs within an Islamic Window. Note that the DCR only applies in respect of PSIA assets for both he restricted and unrestricted categories. Content The form is designed to capture the details regarding the details regarding the changes in the reserves pertaining to the Islamic Finance Business. The form provides two separate columns for data to be input in respect of both PSIA Unrestricted and Restricted businesses.

Instructional Guidelines

Item No. Item Instructional Guidelines B290_1010 Capital invested Report here the total amount of capital invested by PSIAU account

holders (on balance sheet) gross of provisions. Report similar amounts relating to funds provided by PSIAR account holders (off balance sheet).