the croatian tax reform

DESCRIPTION

The tax system of any country depends on its economic, political and social system. Therefore, the changes in these systems are inevitably followed by changes in the composition of the taxation system. Major changes that impact that system are considered as a tax reform. On July 1st 2013, Croatia is to experience a monumental change in its system, as it is to become the 28th Member of the European Union. Because of this, the Croatian Government is obliged to bring about certain tax reforms in order to comply with the regulations that govern the Member States of the EU.TRANSCRIPT

The Croatian tax reform

Sarajevo, May 2013.

Table of Contents

1. Introduction....................................................................................................................3

2. Value added tax – changes in the Croatian rates............................................................4

2.1...............................................................Changes entered into force on March 1st 20126

2.2.............................................................Changes entered into force on January 1st 20137

2.3...............................................................Changes entered into force on March 7th 20137

3. Corporate Income Tax Act – perceived changes.............................................................9

4. Personal Income Tax Act and Contributions Act...........................................................11

4.1. Changes entered into force on March 1st 2012..........................................................13

5. Croatian excise duties...................................................................................................15

5.1...........................................................Excise duties on alcohol and alcoholic beverages16

5.2..................................................................................Excise duties on tobacco products18

5.3............................................................Excise duties on energy products and electricity20

6. Conclusion.....................................................................................................................23

7. References.................................................................................................................... 24

2

1. Introduction

The tax system of any country depends on its economic, political and social system.

Therefore, the changes in these systems are inevitably followed by changes in the

composition of the taxation system. Major changes that impact that system are considered

as a tax reform. On July 1st 2013, Croatia is to experience a monumental change in its system,

as it is to become the 28th Member of the European Union. Because of this, the Croatian

Government is obliged to bring about certain tax reforms in order to comply with the

regulations that govern the Member States of the EU.

This paper will provide an overview of the most important changes in the Croatian taxation

system with regard to:

Value added tax – where an increase in the VAT rate is introduced;

Corporate Income Tax Act – where taxation of dividends is introduced and the

reinvested profit is exempt from taxation; and

Personal Income Tax Act and Contributions Act – where changes in taxation of

personal income and state mandatory health insurance contributions are presented.

In addition to this, I will also explain the most important changes in the Croatian Excise

Duties Act regarding the excise rates for product affected by them, mainly: alcohol and

alcoholic beverages, tobacco products and energy products and electricity.

Due to the fact that considerable changes have been introduced at such short notice and

amidst an economic crisis that continues to grip this country the consequences (although yet

indiscernible) are worth examining, as they are sure to be felt by the public and economy

sectors as well as the citizens of the country.

3

2. Value added tax – changes in the Croatian rates

Value added tax (VAT) is typically described as a tax on consumer spending. In more detail, it

is defined as “a type of consumption tax that is placed on a product whenever value is added

at a stage of production and at final sale” (Investopedia 2013b). Having this in mind, those

taxable under the value added tax include legal entities, individuals operating a registered

business and other individuals who typically make taxable supplies of goods and services and

imports of goods. According to the Croatian VAT law, a company that supplies goods or

services in the Croatian territory and does not have a head office or some other type of

residence will be treated as a VAT taxpayer unless the service recipient is liable to self-

assessment and VAT payment or when a foreign company buys goods in Croatia and makes

further deliveries in Croatia (Expat Croatia 2013). In addition to this is necessary to

emphasize that non-residents are obliged to register for VAT if they perform a taxable

business activity in Croatia, the registration of which is around HRK 85.000.

VAT itself has been applied in over 150 countries (due to its neutrality and the general revues

it provides), and is most often used in the European Union. In EU, VAT is applied in each

member state according to a common legal framework, although member states do enjoy

derogations from the General VAT Directive that allows for some flexibility (Revenue.ie

2013).

The Croatian value added taxation system incurred significant changes in early 2012 (the

most important of which was the increase in the general rate from 23% to 25%) and

continued to change in 2013 because of the “rapid” fiscal effect of VAT, as well as due to the

need for further compliance and alignment of the Croatian legislation with that of the

European Union (Bratic 2013). This increase in the general VAT rate by 2% was done in an

4

effort to increase tax revenues in 2012. An overview of the Croatian tax revenues for the

period 2008-2012 is given in table 2.1.

Table 2.1. Croatian tax revenues, 2008-2012

2008 2009 2010 2011 2012

Total state budget revenue (excluding

contributions in million HRK)

115.77

3

110.258 107.466 107.052 108.649

VAT revenues (in million HRK) 41.308 37.050 37.689 39.314 40.522

Share of VAT revenues in total tax

revenues (%)

35.8 33.0 35.7 36.2 37.0

Source: Kulis (2012)

Although this action was put in place, it should be taken into account that simply raising the

VAT rate in itself won’t always lead to an increase in tax revenues, because apart from the

rates they depend on a number of other factors. An example of this can be seen in 2009,

when as of August 2009, the VAT rate went up from 21% to 23%, but VAT revenues

decreased significantly from July. As a result VAT revenues for 2009 were almost 10% lower

than in the previous year. The Croatian Ministry of Finance justified such an occurrence by

stating that the drop in VAT revenues was due to an economic downturn, particular in

personal consumption, that affected not only Croatia but also other European countries and

the world at large.

It is therefore noted that the decision to lower or increase the general tax rate must be taken

with care not only because it affects tax revenues, but also the quantities and prices of goods

and services and, indirectly, the income, consumption, competitiveness in the market and

living standards of citizens (Kulis 2012).

If the Croatian general VAT rate is compared to other European countries, the following

results, represented in figure 2.1 emerge.

5

Figure 2.1. General VAT rates in EU and Croatia, early 2013 (%)

Source: European Commission (2013)

The results indicate that Croatia has the second highest VAT rate in Europe, after Hungary,

which is equal to that of Sweden and Denmark.

2.1. Changes entered into force on March 1st 2012

The 2012 amendments to the Value Added Tax Act included the following measures

(Ernst&Young 2012b) to be put into force:

An increase in the general VAT rate from 23% to 25%;

Introduction of the reduced 10% rate on:

Edible oils and fats of both animal and vegetable origin;

Baby food and processed cereal-based foods for infants and toddlers;

6

Delivery of water except for that which is marketed in bottles or other

containers;

White sugar from the sugar cane or beet.

Abolition of input VAT deduction for the procurement and maintenance of vessels,

planes, personal motor vehicles and other personal modes of transportation;

Abolition of input VAT deduction for the procurement of goods and services for

entertainment purposes;

Increase in the VAT registration threshold and;

Changes in penal provisions.

2.2. Changes entered into force on January 1st 2013

The early 2013 changes to the Croatian value added taxation system included measures

(Bratic 2013) such as:

A reduced rate of 10% applied to supplies of food, non-alcoholic drinks and wine and

beer in catering facilities;

A replaced zero-rate by a reduced rate of 5% on goods and services such as: all kinds

of bread and milk; medicines, scientific journals, devices surgically implanted into the

human body, cinema tickets, books with professional, scientific, cultural, art and

educational contents etc.

A new 5% rate introduced on vessels for sport and leisure which were previously

under temporary admission procedure and are to be put into the customs procedure

of free circulation by May 31st of 2013.

2.3. Changes entered into force on March 7th 2013

The new Croatian VAT Act, based on a proposal submitted to their Parliament on March 7th

of this year and its subsequent adoption, is set to pave the way for further harmonization

7

with the VAT regulations of the European Union, which Croatia is set to enter on July 1 st

2013.

Changes envisioned by this act include changes such as (Bratic 2013):

Inclusion of free zones in the Croatian territory;

Abolition of VAT exemption for the import of passenger cars and equipment for the

performance of business activities by Croatian war veterans;

Abolition of VAT exemption for the import of goods received by religious

organizations from foreign religious organizations and other natural individuals used

for the purpose of performing some type of a religious activity;

Abolition of VAT exemption for freelance artists;

Abolition of VAT exemption for the purchase of fuel for ships sailing on high seas;

The introduction of value added tax on building land as of January 1st 2015.

Regarding this new Croatian VAT Act it is also important to mention that according to

estimates from the Croatian Minister of Finance Slavko Linic, such actions may lead to a drop

in the state budget revenues by about HRK 500 million in 2013 (or by approximately HRK 1

billion in the upcoming years), but it is also expected to facilitate operations of Croatian

companies exporting to EU countries and to ensure greater liquidity (Radio.net 2013).

Related to this matter, the Croatian Prime Minister Zoran Milanovic emphasized that

although the VAT tax for tourism was reduced from 23% to 10% (applicable from January 1 st

2012) because of the great importance of the tourism sector to the Croatian economy

(Bradbury 2011), a similar type of reduction in the publishing industry could not be

performed. He added that amendments the new Croatian VAT Act do plan to reduce the VAT

tax on daily newspapers form 10% to 5% as of July 1 st 2013 (when Croatia enters the

European Union and becomes the official 28th member), but otherwise publishers must

unfortunately fend for themselves and find new ways of becoming competitive in the market

place until more appropriate solutions can be envisioned for this sector (Radio.net 2013).

8

3. Corporate Income Tax Act – perceived changes

Corporate taxes are defined as “taxes against profits earned by businesses during a given

taxable period, generally applied to a company’s operating earnings after expenses and

depreciation have been deducted from revenues” (Investopedia 2013a). Corporate taxes and

laws that govern them differ significantly around the world, and in Croatia the corporate

income tax (CIT) is based on the consumption concept. This means that the tax burden is

targeted toward those parts of income that are intended for consumption, whereas parts of

the income intended for reinvestment and savings are considered more favorably or are in

fact entirely exempt from taxation.

The corporate income tax must be paid by (Expat Croatia 2013):

Companies and other legal entities residing in Croatia who continuously provide

action for profit;

Non-residents in Croatia, for the profit made during business operations via a

permanent subsidiary or business unit located in the Croatian territory;

A natural person who drives income under the income tax regulations if it is stated

that the person in question wants to pay corporate income tax instead of paying

personal tax; and

An entrepreneur who derives income from a small business if:

Total revenue in the preceding tax period exceeded HRK 2.000.000; or

Total income in the preceding tax period exceeded HRK 4.000.000; or

The value of long-term assets exceeds HRK 2.000.000.

The Croatian CIT rate is currently 20%. Figure 3.1 provides a comparison between the

Croatian CIT rate and other European countries.

9

Figure 3.1. CIT rates in Croatia and other European countries (%)

Source: Simovic (2009)

The comparison indicates that Croatia has a low CIT rate, which is well below the EU-27

average. And unlike other EU countries that have changed their CIT rates, Croatia has a

relatively long period of CIT rate application of 20% (the rate has not been modified since its

application in 2001). However, due to the fact that Croatia is on it’s way to becoming a

Member State of the EU, the Government has added amendments to the Corporate Income

Tax Act (Ernst&Young 2012b) as follows:

Withholding tax at 12% applies on dividends and shares in profits paid to foreign legal

entities after March 1st 2012;

Once Croatia becomes an EU Member, no withholding tax should apply on dividend

payments to shareholders in other EU countries, provided that the shareholder has

held at least a 10% equity stake in the company paying the dividends for an

uninterrupted period of 24 months;

10

The CIT base may be decreased for the profit that is for investment purposes used for

share capital increase;

In line with the amendments to the OECD Transfer Pricing Guidelines, the

comparable uncontrolled price method is no longer preferred over other methods;

As of March 1st 2012, the period after which the cost of value adjustment of

receivables may be recognized as tax deductible is reduced from a 120 days to 60

days.

Under the previous bylaws of the Corporate Income Tax Act all profits were taxed in Croatia,

irrespective of whether they were paid out to the stakeholders or reinvested into new

ventures. The latest proposed reform states that if profit is reinvested into the company’s

share capital in the first six months of the following fiscal year, the reinvested amount will be

exempt from taxation. What is also interesting is that the dividends are now a part of taxable

income, although the dividends up to HRK 12.000 annually will be exempt from taxation if

they are paid to private local individuals.

4. Personal Income Tax Act and Contributions Act

Personal income tax is defined as “a tax paid on one’s personal income as distinct from the

tax paid on a firm’s earnings” (Business Dictionary 2013). Under this act, those who are

taxable are either:

A taxable natural person that derives income from his or her activities; or

A natural successor.

Typical sources of taxable income include sources such as: income derived form

employment, income gained from property and other property rights, income that comes as

a result of performing individual activities, income that comes about as a result of

investment making etc.

11

The tax rate on personal income in Croatia has a progressive rate (persons with higher

income pay higher taxes) and it goes from 12% to 40%. If we take a look at the Croatian

personal income tax rate for the last five years and compare it to some other countries in

Western and Southern Europe, it can be noticed that the Croatian rates were equal to those

find in Spain in 2008-2010, Greece in 2010, and Switzerland in 2011-2012.

Figure 4.1. Personal income tax rates in Croatia and other select European countries (%)

Source: KPGM (2012a)

It should be also taken into account that the minimum monthly gross salary in Croatia for full

time employment (40 working hours a week) in the period from June 1 st 2011 to May 31st

2012 was equal to HRK 2.814.

12

4.1. Changes entered into force on March 1st 2012

In March of 2012, Croatia has entered several changes into the Personal Income Tax Act

because of its subsequent entry into the European Union. These changes include the

following mandates (Ernst&Young 2012a):

Monthly personal income has increased from HRK 1.800 to HRK 2.200 (for retirees

from HRK 3.200 to HRK 3.400 per month).

The tax rate schedule is also changed meaning that new tax brackets now apply on a

new tax base (gross salary reduced by obligatory contributions from salaries and

personal allowances) and they are as follows:

o Monthly tax brackets:

The 12% rate applies to income up to HRK 2.200;

The 25% rate applies to income between HRK 2.200 and HRK 8.800; and

The 40% rate applies to income exceeding HRK 8.800.

o Annual tax brackets: These are generally determined as being 12 times the

monthly brackets, however is should be taken into account that there was an

exception in 2012, when the annual brackets were averaged over the whole

year due to their change in March of the same year.

Pensions income received from abroad by Croatian residents is taxable at the same

progressive tax rates as the employment income, and are subject to the provisions of

an effective double tax treaty, with the right to utilize basic personal allowances up to

HRK 3.400. Tax payments, such as this are required to be paid by the taxpayer within

eight days from the recipient of income.

Additional changes to the Personal Income Tax Act stipulate that, unless specifically exempt,

all non-cash salary items (benefits) are generally taxable according to the market value

(including 25% VAT). Typical non-cash salary items include items such as private use of

company available cars, housing and rental reimbursements, meals, loans with an interest

13

rate that is below 3% etc. An example of how non-cash salary item are taxes is provided

below for the private use of a company car.

EXAMPLE: Tax value for the private use of a company car

The taxable value of this type of non-cash salary item is calculated in one of three ways:

a) Based on the number of actual driven kilometers for private use in a month’s time;

b) Tax value is equal to 1% of the purchase price (including 25% VAT of the company car

per month for those purchased); or

c) Tax value is equal to 20% of the monthly lease installment including again 25% VAT.

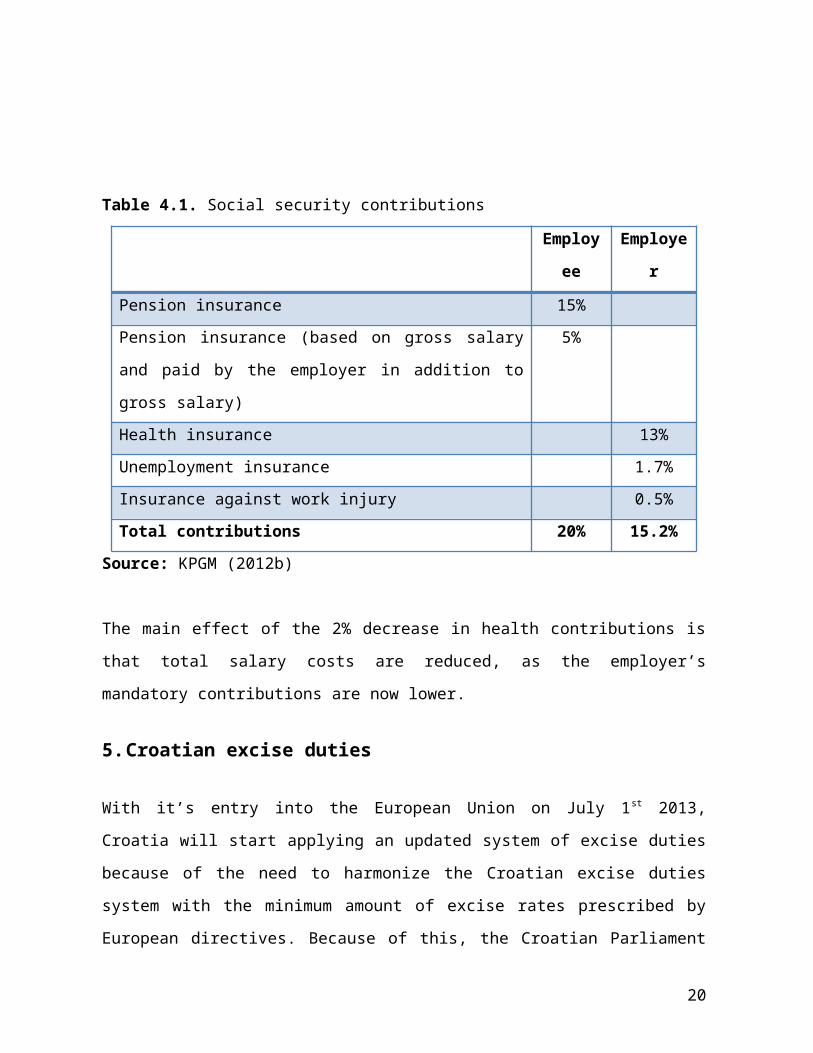

Mandatory Contributions Act

The Act on Mandatory Contributions primarily concerns health insurance contributions and

social security contributions, which are typically deducted from income and paychecks.

The two most prominent changes in the Act on Mandatory Contributions include

(Ernst&Young 2012b):

A decrease in health insurance contributions from 15% to 13%. This mandate applies

to all salaries from April 30th 2012;

The procedure for offsetting outstanding employer contribution liabilities against its

claims toward the Croatian Institute for Health Insurance is introduced in May of

2012.

These proposed changes in the contributions act contemplate the possibility that the

Government will make changes in the payment mechanisms for social contributions. If we

take a closer look at these social security contributions, the following results emerge:

14

Table 4.1. Social security contributions

Employee Employer

Pension insurance 15%

Pension insurance (based on gross salary and paid by the

employer in addition to gross salary)

5%

Health insurance 13%

Unemployment insurance 1.7%

Insurance against work injury 0.5%

Total contributions 20% 15.2%

Source: KPGM (2012b)

The main effect of the 2% decrease in health contributions is that total salary costs are

reduced, as the employer’s mandatory contributions are now lower.

5. Croatian excise duties

With it’s entry into the European Union on July 1st 2013, Croatia will start applying an

updated system of excise duties because of the need to harmonize the Croatian excise duties

system with the minimum amount of excise rates prescribed by European directives.

Because of this, the Croatian Parliament has recently adopted a new Excise Duties Act, which

stipulates the excise tariffs for the products that are subject to this type of duty. The three

types of products subject to excise duty are:

a) Alcohol and alcoholic beverages (including beer, wine and other beverages obtained

by fermenting, intermediate products and ethyl alcohol);

b) Tobacco products (cigarettes, cigars, cigarillos and smoking tobacco);

c) Energy products (motor fuel or heating fuel, or electricity).

15

5.1. Excise duties on alcohol and alcoholic beverages

The 2013 Excise Duties Act does not stipulate any changes in how alcohol and alcoholic

beverages are taxed. As can be seen in table 5.1 the Croatian excise rates for these types of

products are at a rate higher than those currently prescribed in the European Union.

Table 5.1. Excise duties rates on alcohol and alcoholic beverages in Croatia and EU

Excise product Amount of excise in Croatia Minimum excise duty in EU

Beer HRK 40.00 HRK 13.89

Still wines HRK 0.00 HRK 0.00

Sparkling wines HRK 0.00 HRK 0.00

Other alcoholic beverages HRK 0.00 HRK 0.00

Intermediate products

HRK 500.00

containing

less than 15%

vol. of pure

alcohol

HRK 800.00

containing

15% vol. of

pure alcohol

or more

HRK 334.15

Ethyl alcohol HRK 5.300.00 HRK 4.084.03

Source: Tax Administration of RC (2013)

The difference in excise duty rates between Croatia and the EU is primarily due to the fact

that in Croatia every alcoholic product is taxed at a single rate, while in the European Union

there are typically one or more standard or reduced rates for all categories of goods.

On accession to the European Union some of the changes in the Croatian Excise Duties Act

that will come into force include (Kulis 2013):

The volume restrictions for commercial restriction outside the system of suspended

payment for excise duties are to be lifted;

16

Producers who produce beer, intermediate products and other alcoholic beverages

for commercial purposes will be able to operate outside the excise warehouse;

In the production and processing of non-food products, an exempt user of excise

goods will not be required to pay an excise duty on ethyl alcohol partially denatured

by regulation preparations.

To demonstrate the difference in excise duty rates between Croatia and other EU Member

States, standard rates in the case of beer are taken as an example. In the new Croatian Law

on Excise Duties (Article 60) beer is taxed at HRK 40.00 for 1% of actual alcoholic strength in

a hectoliter of finished product (Croatian Parliament 2013), while in the EU the rates on beer

relate to the malt concentration or the proportion of alcohol in beer. Figure 5.1 indicates the

amount of excise duty rates on beer according to the criteria of malt concentration and the

proportion of alcohol.

Figure 5.1. Rates of excise duties on beer in Croatia and EU countries 20012/2013 (€)

Source: Kulis (2013)

17

The figure indicates that the highest rates are applied in the UK and Finland, where the rate

of excise duty is measured according to the proportion of alcohol, while in comparison the

rate in Croatia is lowest for beer is taxed only according to a single rate.

5.2. Excise duties on tobacco products

When it comes to the excise duty rates applied to tobacco products, the biggest change in

the new Law is with regard to how the reference value and base for measuring the

percentage of the share of a specific excise in the total tax burden is introduced. Article 75 of

this Law stipulates that instead of a retail price of cigarettes the new value base is the

weighted average price (WAP) of cigarettes released for consumption is used (Croatian

Parliament 2013).

A comparison in excise duty rates between Croatia and other EU countries based on the

percentage of the weighted average retail price of cigarettes is provided in figure 5.2.

Figure 5.2. Rates of excise duties on cigarettes in Croatia and EU countries January 1st 2013

Source: Kulis (2013)

18

The figure indicates that the lowest rates on tobacco are found in Croatia. This means that a

significant amount of time will have to pass, for these rates to be harmonized with the

Directives of the European Union. However during negotiation for Croatian accession into

the EU, it was announced that Croatia can keep its lower excise rates on cigarettes until

December 31st 2017 when harmonization with EU Directives must be completed (Delegation

of the EU to RC 2013).

Until that time, some of the obligations before the Croatian Parliament with regard to excise

duties on Croatia are as follows (Kulis 2013):

July 1st, 2013 – Total excise must come to at least 57% of the average weighted retail

price of cigarettes released for consumption and 64 euro per 1.000 cigarettes.

Currently that percentage is about 52.2% and 62.25 euro per 1.000 cigarettes.

January 1st, 2014 – Weighted average price of cigarettes should be 77 euro per 1,000

cigarettes released for consumption.

December 31st, 2017 – Price of cigarettes should be 90 euro per 1,000 cigarettes, in

conjunction with a minimal 60% of the average weighted retail price of cigarettes

released for consumption.

Current excise prices on all tobacco products are shown in table 5.2.

Table 5.2. Excise duties rates on tobacco products in Croatia and EU

Excise product

Amount of excise in Croatia

Minimum excise duty in EUBefore EU

accession

After EU

accession

Cigarettes

HRK 180.00

per 1000

items

HRK 475.00

per 1000

items

HRK 475.00 per 1000 items

Cigars

HRK 1.100.00

per 1000

items

HRK 600.00

per 1000

items

HRK 89.00 per 1000 items

19

Cigarillos

HRK 220.00

per 1000

items

HRK 600.00

per 1000

items

HRK 89.00 per 1000 items

Fine-cut tobacco

HRK 325.00

per kg of

product

HRK 351.00

per kg of

product

HRK 349.00 per kg of product

Other smoking tobacco

HRK 146.00

per 1000

items

HRK 296.00

per 1000

items

HRK 163.00 per 1000 items

Source: Tax administration of RC (2013); Kulis (2013)

5.3. Excise duties on energy products and electricity

When it comes to the 2013 Croatian Excise Duties Act, the biggest changes are with regard to

the duties regarding energy products and electricity. More specifically, the Law (article 84)

states that in addition to an increase in rates, taxation will now be extended to natural gas,

coal, coke and electricity.

The rates for these products are listed in table 5.3.

Table 5.3. Excise duties rates on energy products and electricity

Excise product Amount of excise in

Croatia

Minimum excise duty in EU

Petrol used as motor fuel:

(1) Leaded; (2) Unleaded

(1) HRK 3.801.00 per 1000 l

(2) HRK 3.151.00 per 1000 l

(1) HRK 3.126.00 per 1000 l

(2) HRK 2.666.00 per 1000 l

Gas oil:

(1) For motor fuels;

(2) For heating

(1) HRK 2.450.50 per 1000 l

(2) HRK 343.00 per 1000 l

(1) HRK 2.450.50 per 1000 l

(2) HRK 156.00 per 1000 l

Kerosene:

(1) For motor fuels; (1) HRK 2.450.50 per 1000 l (1) HRK 2.450.50 per 1000 l

20

(2) For heating (2) HRK 1.752.00 per 1000 l (2) HRK 0.00 per 1000 l

Liquid petroleum gas:

(1) For motor fuels;

(2) For heating

(1) HRK 100.00 per 1000 kg

(2) HRK 100.00 per 1000 kg

(1) HRK 928.00 per 1000 kg

(2) HRK 0.00 per 1000 kg

Heavy fuel oil HRK 160.00 per 1000 kg HRK 111.00 per 1000 kg

Natural gas:

(1) For motor fuels;

(2) For heating (business use)

(3) For heating (non-business

use)

(1) HRK 0.00 per MWh

(2) HRK 4.05 per MWh

(3) HRK 8.10 per MWh

(1) HRK 19.00 per Gj

(2) HRK 1.11 per Gj

(3) HRK 2.23 per Gj

Coal and coke:

(1) For business use

(2) For non-business use

(1) HRK 2.30 per Gj

(2) HRK 2.30 per Gj

(1) HRK 1.11 per Gj

(2) HRK 2.23 per Gj

Electricity:

(1) For business use

(2) For non-business use

(1) HRK 3.75 per MWh

(2) HRK 7.50 per MWh

(1) HRK 3.71 per MWh

(2) HRK 7.43 per MWh

Bio-fuels HRK 0.00 HRK 0.00

Source: Croatian parliament (2013); Kulis (2013)

As can be seen in the table above, excise duty rates in Croatian aren’t that different than

those found in the European Union. The only exceptions to this, where rates aren’t

compliant with the minimally prescribed EU rates, are with regard to excise duty rates for

liquid petroleum gas and kerosene.

A comparison in excise duty rates between Croatia and other EU countries for petrol (both

leaded and unleaded) is provided below in figure 5.2.

Figure 5.2. Rates of excise duties on petrol in Croatia and EU countries

21

Source: Kulis (2013)

The figure indicates that the highest rates for both leaded and unleaded petrol can be found

in Netherlands, while four countries namely Russia, Bulgaria, Latvia and Estonia have lower

rates on leaded petrol than Croatia. On the other hand, it can also be noted that the use of

leaded petrol is prohibited in Poland and Finland.

22

6. Conclusion

In response to the need for fiscal consolidation and financial adjustment of the Croatian

taxation system with that of the Member States of the European Union, it is clear that

Croatia has made some obvious and commendable changes. With regard to its Value Added

Tax system, the most noticeable change is that it first increased its general VAT rate (from

23% to 25%) in 2012, and then abolished the zero rate in early 2013. Such changes in VAT

rates are expected to increase tax revenues, provided that there are no economic activity

reductions or other reduction in personal consumption of Croatian citizens. The Croatian

Corporate Income Tax Act, also introduced some changes to its mandates, and these

primarily concern the introduction of the withholding tax and the taxation of dividends,

while reinvested profit now becomes exempt from taxation. When it comes to the changes

in the Personal Income Tax and Mandatory Contributions Act these primarily concern

increases in the amount of monthly personal income and decreases in health insurance

contributions. Finally, with regard the new Croatian Excise Duties Act the changes are not

that distinctive. This act is mostly harmonized with the minimal rates prescribed in the

European Directives, although the exception are the excise duties on tobacco products,

where increases in rates and price are expected to be preformed until December 31 st 2017

upon which time they should be fully harmonized with those found in EU Member States.

23

7. References

Bradbury, P., 2011. New Croatian Prime Minister Zoran Milanovic reduces tourism VAT. Available at: http://www.digitaljournal.com/article/316617 [Accessed May 27, 2013].

Bratic, V., 2013. Value Added Tax: Changes in Rates in Croatia and Trends in the European Union.

Business Dictionary, 2013. What is personal income tax? BusinessDictionary.com. Available at: http://www.businessdictionary.com/definition/personal-income-tax.html [Accessed May 26, 2013].

Croatian Parliament, 2013. Croatian Excise Duties Act. Narodne novine. Available at: http://narodne-novine.nn.hr/clanci/sluzbeni/2013_02_22_357.html [Accessed May 29, 2013].

Delegation of the EU to RC, 2013. Croatia and EU - prejudices and realities. Delegation of the European Union to the Republic of Croatia. Available at: http://www.delhrv.ec.europa.eu/?lang=en&content=61 [Accessed May 29, 2013].

Ernst&Young, 2012a. HR and tax alert.

Ernst&Young, 2012b. The Croatian Tax Package.

European Commission, 2013. VAT rates Applied in the Member States of the European Union, European Commission. Available at: http://ec.europa.eu/taxation_customs/taxation/vat/how_vat_works/rates/ [Accessed May 24, 2013].

Expat Croatia, 2013. Important taxes. Expat Croatia. Available at: http://www.expatcroatia.net/once-youre-here/banking-a-finance/5141-important-taxes [Accessed May 26, 2013].

Investopedia, 2013a. Corporate Tax Definition. Investopedia. Available at: http://www.investopedia.com/terms/c/corporatetax.asp [Accessed May 25, 2013].

Investopedia, 2013b. Value-Added Tax (VAT) Definition. Investopedia. Available at: http://www.investopedia.com/terms/v/valueaddedtax.asp [Accessed May 24, 2013].

KPGM, 2012a. Individual Income Tax and Social Security Rate Srvey, KPGM International.

KPGM, 2012b. Tax Card 2012.

Kulis, D., 2012. Changes in the Value Added Tax System.

24

Kulis, D., 2013. Excise duties system in Croatia closer to the European system.

Radio.net, 2013. Government adopts VAT Bill. Daily tprtal.hr. Available at: http://daily.tportal.hr/247759/Gov-t-adopts-VAT-Bill.html [Accessed May 27, 2013].

Revenue.ie, 2013. EU VAT Issues. Revenue.ie. Available at: http://www.revenue.ie/en/tax/vat/vat-issues.html [Accessed May 24, 2013].

Simovic, H., 2009. Effective Corporate Income Tax Burden in Croatia. Working Paper Series. Zagreb: Faculty of Economics and Business.

Tax Administration of RC, 2013. The Croatian Tax system. Republic of Croatia Ministry of Finance. Available at: http://www.porezna-uprava.hr/en/porezi/v_poreza.asp?id=b01d1#1.1_VALUE_ADDED_TAX [Accessed May 29, 2013].

25