the competitive advantage of greece: moving to the … files/caon_greece_2003.05...athens, greece 8...

TRANSCRIPT

1 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

The Competitive Advantage of Greece:Moving to the Next Level

Professor Michael E. PorterInstitute for Strategy and Competitiveness

Harvard Business School

Athens, Greece8 May, 2003

This presentation draws on ideas from Professor Porter’s articles and books, in particular, The Competitive Advantage of Nations (The Free Press, 1990), “Building the Microeconomic Foundations of Competitiveness,” in The Global Competitiveness Report 2002, (World Economic Forum, 2002), “Clusters and the New Competitive Agenda for Companies and Governments” in On Competition (Harvard Business School Press, 1998), and ongoing research on clusters and competitiveness. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means - electronic, mechanical, photocopying, recording, or otherwise - without the permission of Michael E. Porter.Further information on Professor Porter’s work and the Institute for Strategy and Competitiveness is available at www.isc.hbs.edu

2 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

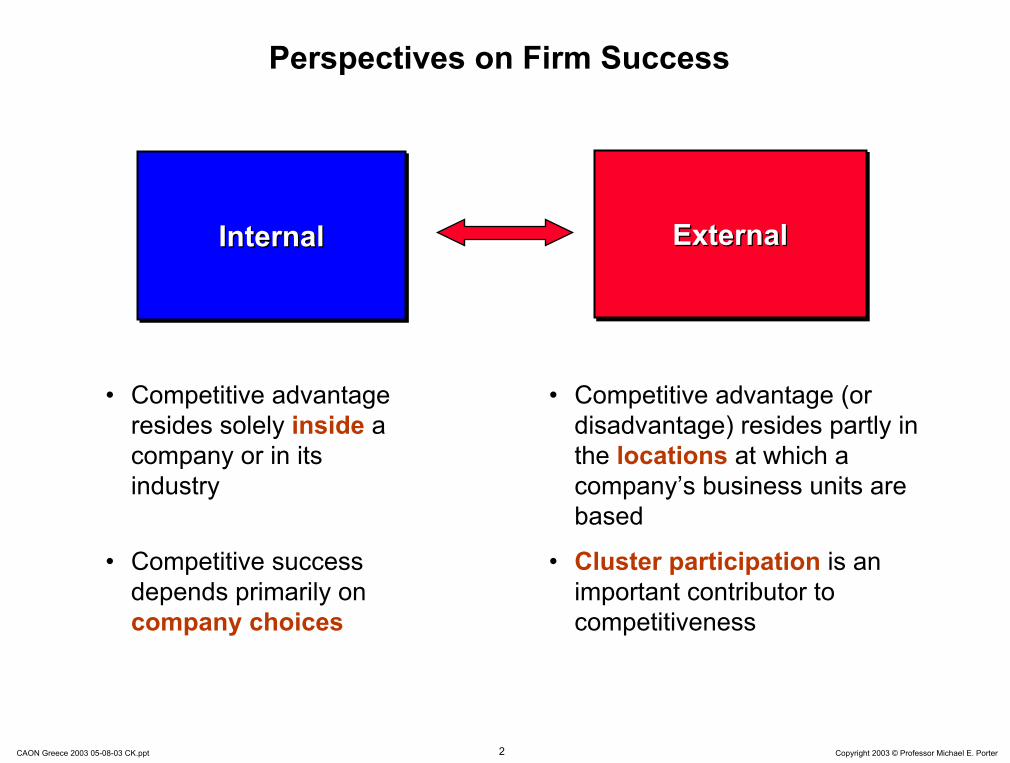

Perspectives on Firm Success

InternalInternalInternal ExternalExternalExternal

• Competitive advantage resides solely inside a company or in its industry

• Competitive success depends primarily on company choices

• Competitive advantage (or disadvantage) resides partly in the locations at which a company’s business units are based

• Cluster participation is an important contributor to competitiveness

3 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

What is Competitiveness?

• Competitiveness is determined by the productivity with which a nation uses its human, capital, and natural resources. Productivity sets a nation’s or region’s standard of living (wages, returns to capital, returns to natural resource endowments)

– Productivity depends both on the value of products and services (e.g. uniqueness, quality) as well as the efficiency with which they are produced.

– It is not what industries a nation competes in that matters for prosperity, but howfirms compete in those industries

– Productivity in a nation is a reflection of what both domestic and foreign firms choose to do in that location. The location of ownership is secondary for national prosperity.

– The productivity of “local” industries is of fundamental importance to competitiveness, not just that of traded industries

– Devaluation does not make a country more competitive

• Nations compete in offering the most productive environment for business

• The public and private sectors play different but interrelated roles in creating a productive economy

4 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Innovation and Competitiveness

ProductivityProductivity

Innovative CapacityInnovative CapacityInnovative Capacity

Competitiveness

• Innovation is more than just scientific discovery• There are no low-tech industries, only low-tech firms

ProsperityProsperityProsperity

5 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

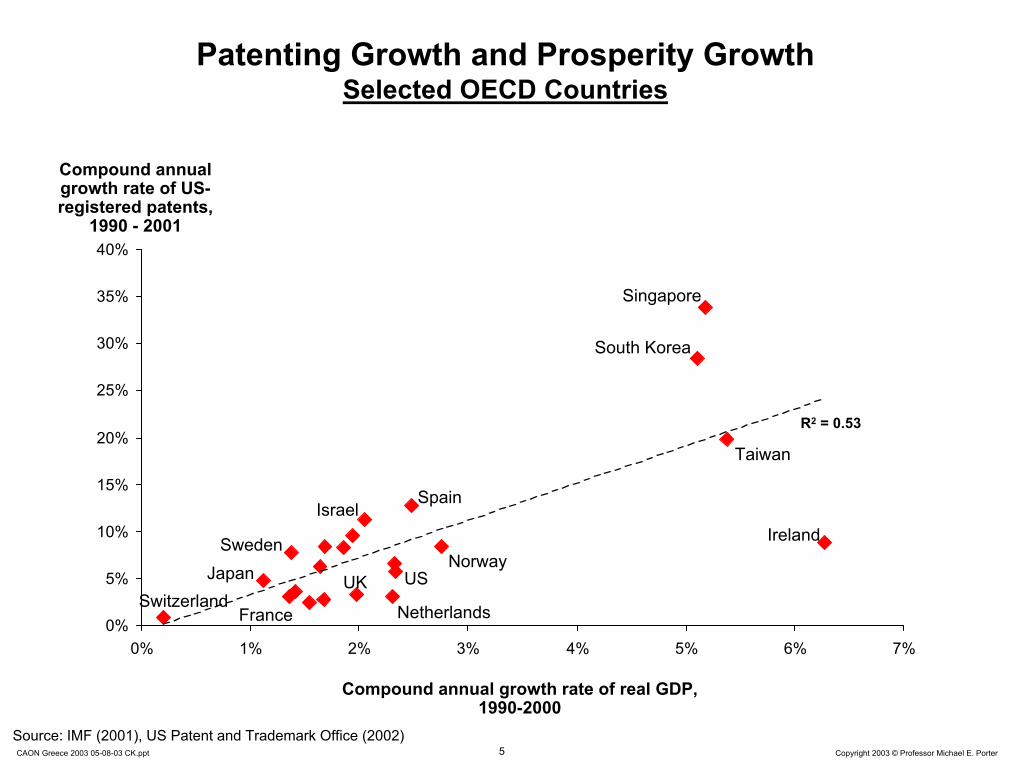

Patenting Growth and Prosperity GrowthSelected OECD Countries

0%

5%

10%

15%

20%

25%

30%

35%

40%

0% 1% 2% 3% 4% 5% 6% 7%

Ireland

Compound annual growth rate of US-registered patents,

1990 - 2001

Compound annual growth rate of real GDP, 1990-2000

USUKJapan

Spain

France Netherlands

Israel

Singapore

Norway

Source: IMF (2001), US Patent and Trademark Office (2002)

R2 = 0.53

Taiwan

Switzerland

Sweden

South Korea

6 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

The Greek Economic Situation in 2003

• Greece has been among the leading European Union member countries in terms of GDP growth in the last five years

• Macroeconomic progress has been considerable, and Greece successfully entered the European Monetary Union in the first wave

However

• Much of the recent growth has been fueled by low interest ratesafter entry into the EMU and access to EU structural funds

• Despite some recent progress, Greece is still lagging behind the reforms other countries started much earlier

• Greece will receive reduced EU funding after 2006 and faces increasingly intense competition from EU accession countries in Eastern Europe

• Greece has significant competitiveness challenges that must be addressed if prosperity growth is to be sustainable

7 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

GreeceSpainAustriaItalyPortugal

Comparative Economic PerformanceGrowth Rate of Real GDP, Selected Economies

Annual Growth Rate of Real GDP

Source: EIU (2002)

8 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

30%

40%

50%

60%

70%

80%

90%

100%

-2.0% -1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0%

UK

United States

Comparative Economic PerformanceProsperity, Selected Economies

Korea

Netherlands FinlandGermanyJapan

Source: World Development Indicators 2002

Switzerland

GDP per Capita, 2001, US=100

CAGR of GDP per Capita Relative to the US, 1995-2001

Slovenia

Taiwan

France

New Zealand

Italy

Canada

Israel

Hungary

Hong Kong

Argentina

Portugal

Denmark

Greece

Sweden

Spain

Slovak Republic

Singapore

Norway

Czech Republic

BelgiumAustria Australia

9 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

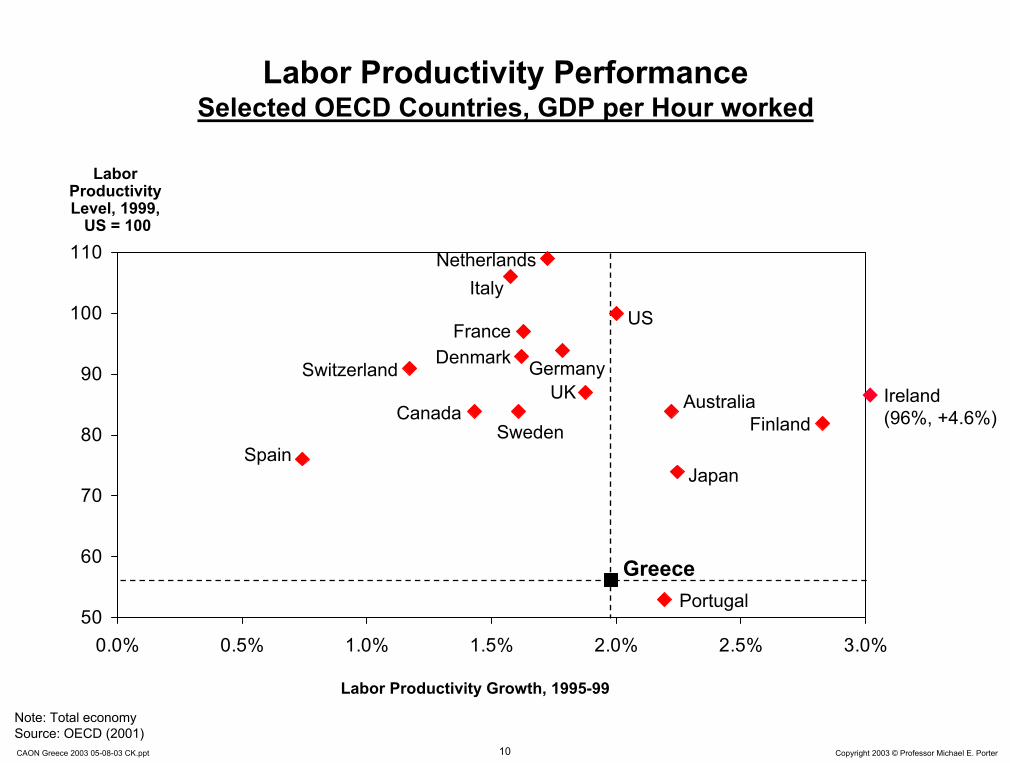

Greek Microeconomic Performance

• Greece has registered solid labor productivity growth in the last few years

However

• The overall level of labor productivity is still low

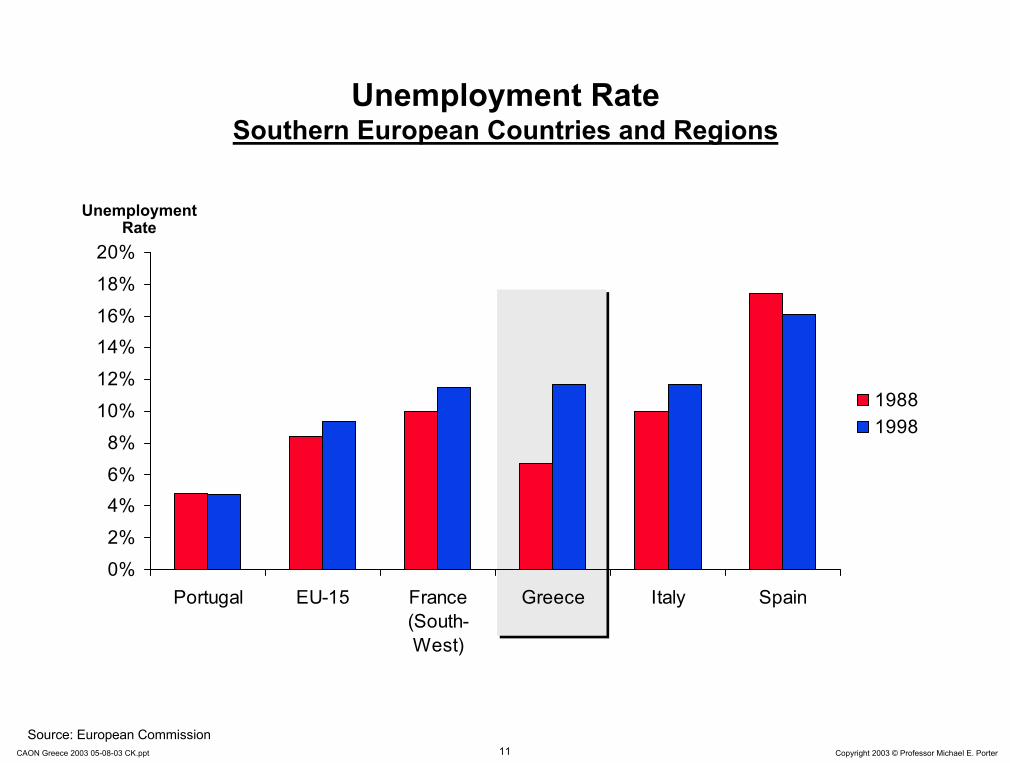

• Greece has a been one of the few middle to high-income countries with increasing unemployment since 1995– The effects of corporate restructuring, labor force inflows from

agriculture, higher participation of women, and immigrants have outweighed positive job creation

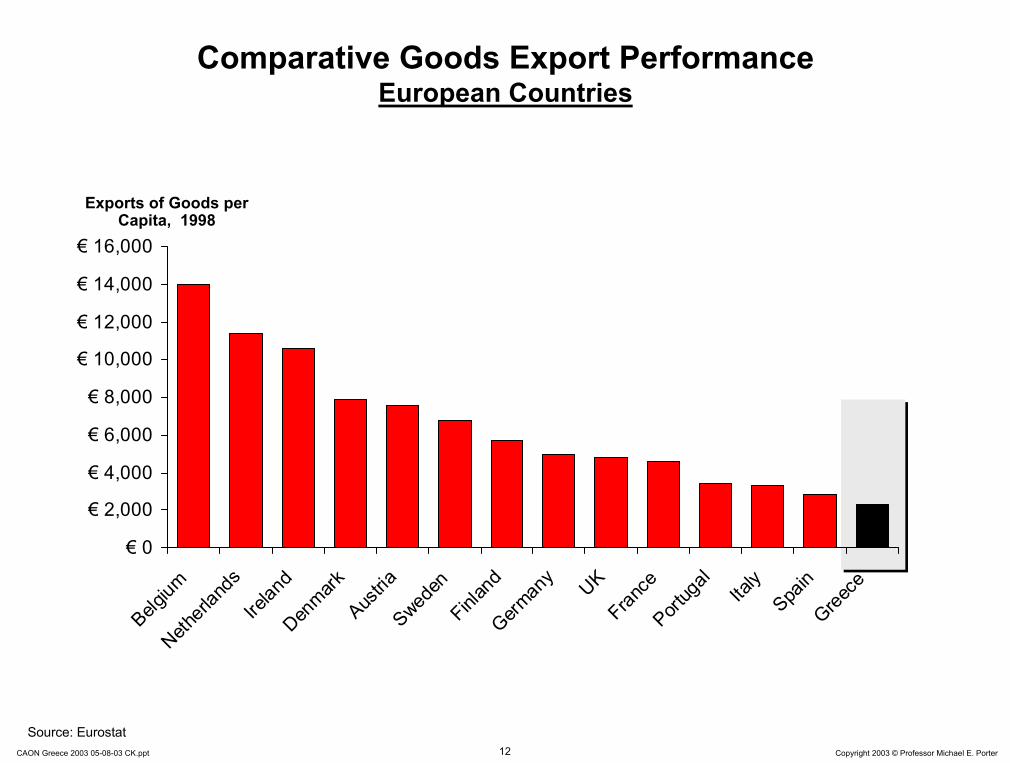

• Greece has a weak position in exports. Performance is better in service exports such as tourism and shipping

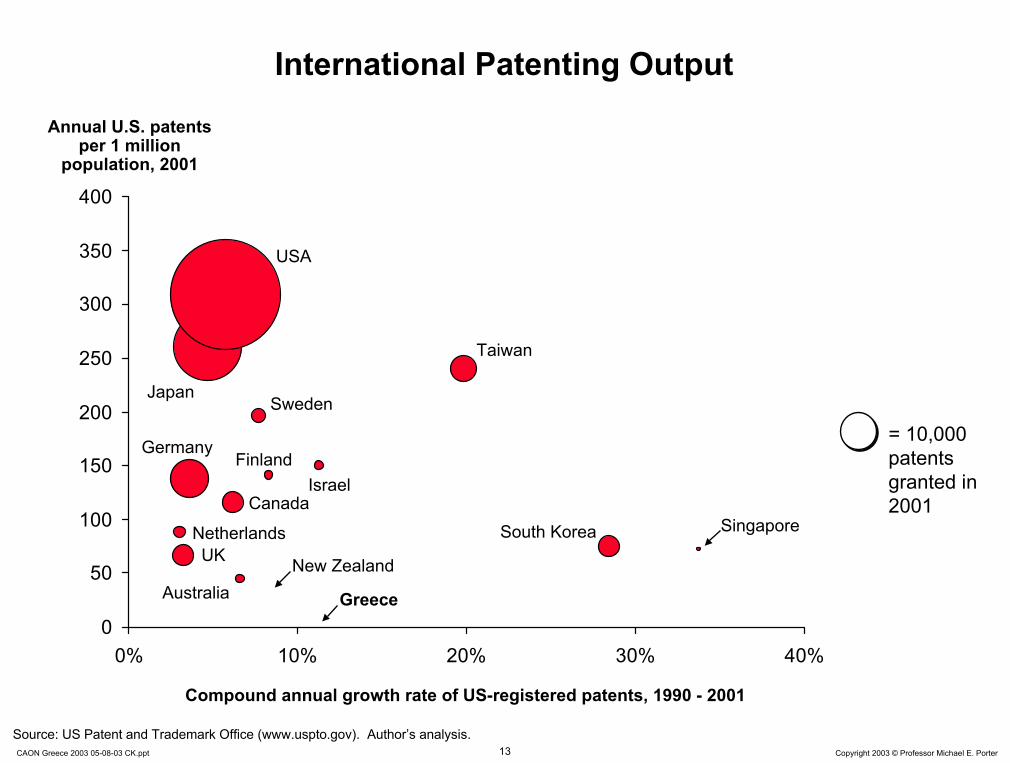

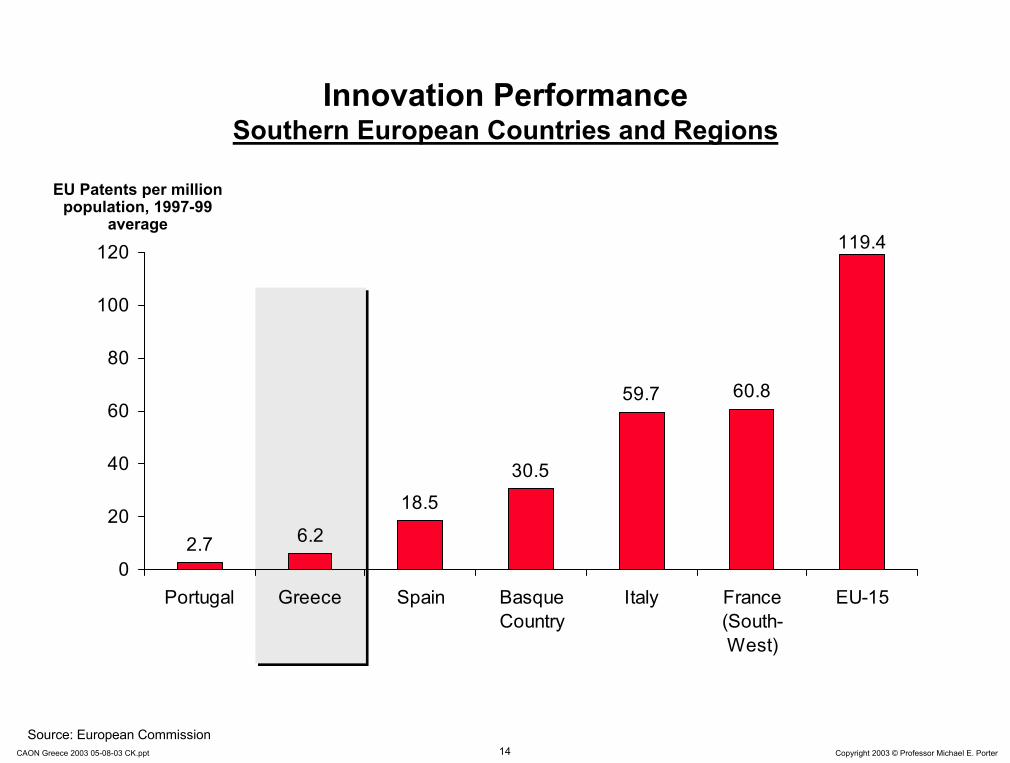

• Greece innovation performance lags all other EU member countries with the exception of Portugal

10 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Labor Productivity PerformanceSelected OECD Countries, GDP per Hour worked

50

60

70

80

90

100

110

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0%

Labor Productivity Level, 1999,

US = 100

Labor Productivity Growth, 1995-99

AustraliaFinland

US

GermanyUK

JapanSpain

Canada

France

NetherlandsItaly

Denmark

Note: Total economySource: OECD (2001)

Switzerland

Sweden

Ireland(96%, +4.6%)

GreecePortugal

11 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Unemployment RateSouthern European Countries and Regions

0%2%4%6%8%

10%12%14%16%18%20%

Portugal EU-15 France(South-West)

Greece Italy Spain

19881998

Unemployment Rate

Source: European Commission

12 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

€ 0

€ 2,000

€ 4,000

€ 6,000

€ 8,000

€ 10,000

€ 12,000

€ 14,000

€ 16,000

Belgium

Netherl

ands

Irelan

dDen

markAus

triaSwed

enFinl

and

German

y UKFran

cePort

ugal

Italy

Spain

Greece

Comparative Goods Export PerformanceEuropean Countries

Exports of Goods per Capita, 1998

Source: Eurostat

13 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Source: US Patent and Trademark Office (www.uspto.gov). Author’s analysis.

Annual U.S. patents per 1 million

population, 2001

Compound annual growth rate of US-registered patents, 1990 - 2001

International Patenting Output

0

50

100

150

200

250

300

350

400

0% 10% 20% 30% 40%

Australia

Canada

Germany

Japan

South Korea

New Zealand

Singapore

Sweden

Taiwan

UK

Israel

= 10,000 patents granted in 2001

USA

Finland

Netherlands

Greece

14 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Innovation PerformanceSouthern European Countries and Regions

2.7 6.2

18.530.5

59.7 60.8

119.4

0

20

40

60

80

100

120

Portugal Greece Spain BasqueCountry

Italy France(South-West)

EU-15

EU Patents per million population, 1997-99

average

Source: European Commission

15 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Microeconomic Foundations of DevelopmentMicroeconomic Foundations of Development

Quality of the Microeconomic

BusinessEnvironment

Quality of the Quality of the MicroeconomicMicroeconomic

BusinessBusinessEnvironmentEnvironment

Sophisticationof Company

Operations andStrategy

SophisticationSophisticationof Companyof Company

Operations andOperations andStrategyStrategy

Determinants of Productivity and Productivity Growth

Macroeconomic, Political, Legal, and Social Context for Development

Macroeconomic, Political, Legal, and Social Macroeconomic, Political, Legal, and Social Context for DevelopmentContext for Development

• A sound macroeconomic, political, legal, and social context creates the potential for competitiveness, but is not sufficient

• Competitiveness ultimately depends on improving the microeconomic capability of the economy and the sophistication of local companies and local competition

16 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

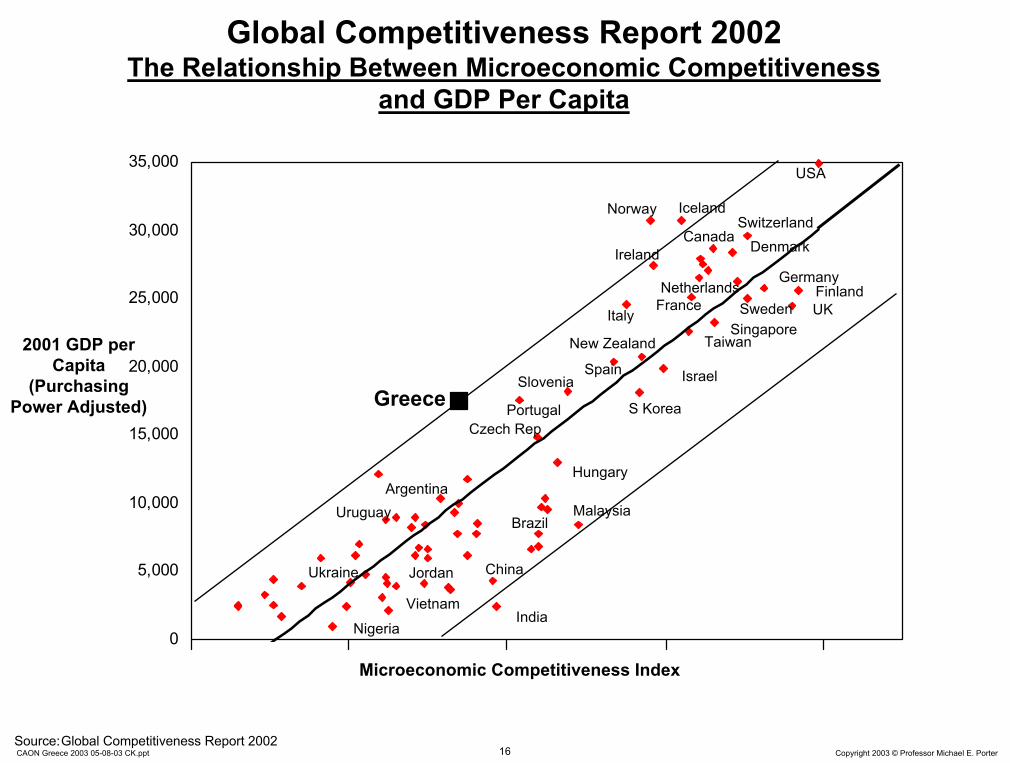

Global Competitiveness Report 2002The Relationship Between Microeconomic Competitiveness

and GDP Per Capita

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000USA

FinlandNetherlandsSweden

Switzerland

Germany

UK

Denmark

SingaporeNew Zealand Taiwan

Norway Iceland

Ireland

GreeceIsrael

Italy

S Korea

Hungary

India

France

Canada

Spain

Czech Rep

Slovenia

Portugal

Microeconomic Competitiveness Index

2001 GDP per Capita

(Purchasing Power Adjusted)

BrazilMalaysia

China

Argentina

Ukraine

Vietnam

Jordan

Uruguay

Nigeria

Source:Global Competitiveness Report 2002

17 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

Productivity, Innovation, and the Business Environment

• Successful economic development is a process of successive economic upgrading, in which the business environment in a nation evolves to support and encourage increasingly sophisticated ways of competing

Sophisticated and demandinglocal customer(s)Local customer needs that anticipate those elsewhereUnusual local demand in specialized segments that can be served nationally and globally

Presence of high quality, specialized inputs available to firms

–Human resources–Capital resources–Physical infrastructure–Administrative infrastructure–Information infrastructure–Scientific and technological

infrastructure–Natural resources

Access to capable, locally based suppliersand firms in related fieldsPresence of clusters instead of isolated industries

A local context and rules that encourage investment and sustained upgrading

–e.g., Intellectual property protection

Meritocratic incentive system across institutionsOpen and vigorous competition among locally based rivals

18 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

The California Wine Cluster

Educational, Research, & Trade Organizations (e.g. Wine Institute,

UC Davis, Culinary Institutes)

Educational, Research, & Trade Organizations (e.g. Wine Institute,

UC Davis, Culinary Institutes)

Growers/VineyardsGrowers/Vineyards

Sources: California Wine Institute, Internet search, California State Legislature. Based on research by MBA 1997 students R. Alexander, R. Arney, N. Black, E. Frost, and A. Shivananda.

Wineries/ProcessingFacilities

Wineries/ProcessingFacilities

GrapestockGrapestock

Fertilizer, Pesticides, Herbicides

Fertilizer, Pesticides, Herbicides

Grape Harvesting Equipment

Grape Harvesting Equipment

Irrigation TechnologyIrrigation Technology

Winemaking Equipment

Winemaking Equipment

BarrelsBarrels

LabelsLabels

BottlesBottles

Caps and CorksCaps and Corks

Public Relations and Advertising

Public Relations and Advertising

Specialized Publications (e.g., Wine Spectator,

Trade Journal)

Specialized Publications (e.g., Wine Spectator,

Trade Journal)

Food ClusterFood Cluster

Tourism ClusterTourism ClusterCalifornia Agricultural Cluster

California Agricultural Cluster

State Government Agencies(e.g., Select Committee on Wine

Production and Economy)

19 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

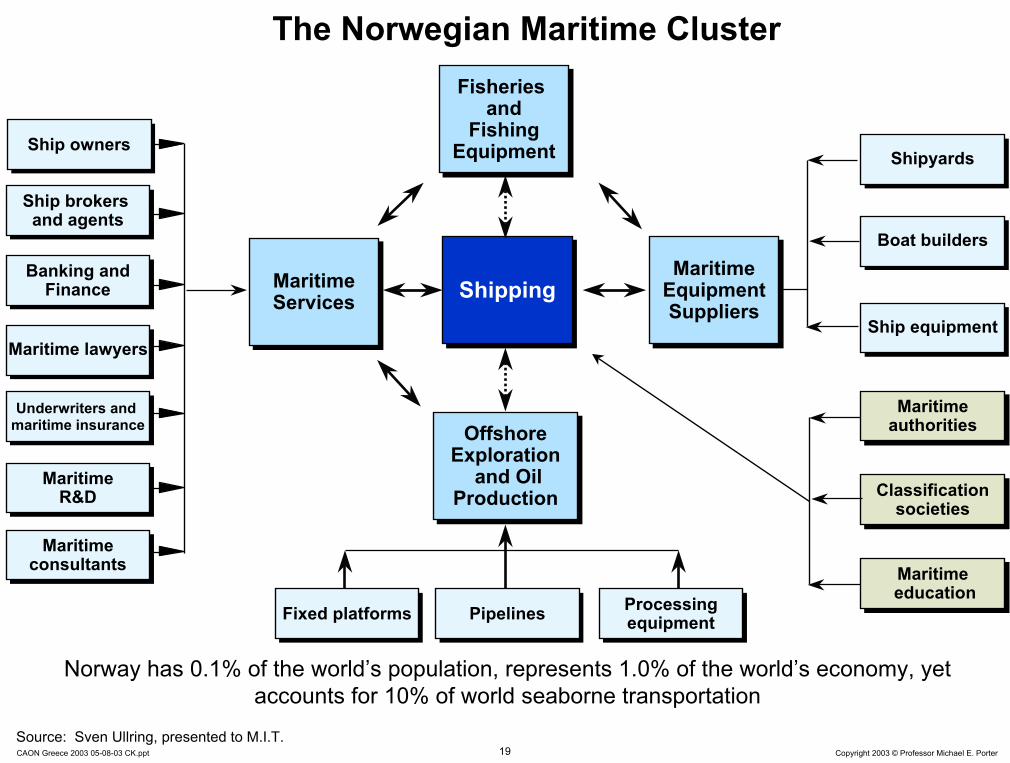

The Norwegian Maritime Cluster

Norway has 0.1% of the world’s population, represents 1.0% of the world’s economy, yet accounts for 10% of world seaborne transportation

MaritimeEquipmentSuppliers

MaritimeEquipmentSuppliers

ShippingShippingMaritimeServicesMaritimeServices

OffshoreExploration

and OilProduction

OffshoreExploration

and OilProduction

ShipyardsShipyards

Boat buildersBoat builders

Ship equipmentShip equipment

Fixed platformsFixed platforms PipelinesPipelines Processingequipment

Processingequipment

Fisheries and

FishingEquipment

Fisheries and

FishingEquipment

Ship brokers and agents

Ship brokers and agents

Banking andFinance

Banking andFinance

MaritimeeducationMaritimeeducation

Underwriters and maritime insuranceUnderwriters and

maritime insurance

Maritime lawyersMaritime lawyers

Classificationsocieties

Classificationsocieties

MaritimeR&D

MaritimeR&D

MaritimeconsultantsMaritime

consultants

Ship ownersShip owners

MaritimeauthoritiesMaritime

authorities

Source: Sven Ullring, presented to M.I.T.

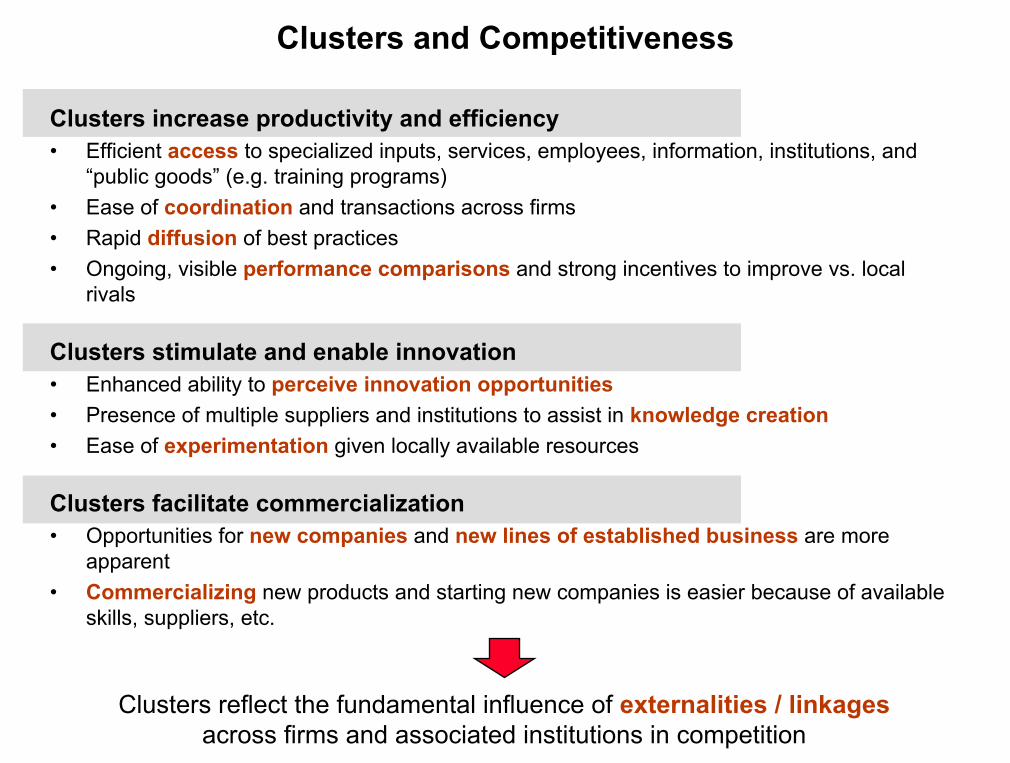

Clusters and Competitiveness

Clusters increase productivity and efficiency• Efficient access to specialized inputs, services, employees, information, institutions, and

“public goods” (e.g. training programs)• Ease of coordination and transactions across firms• Rapid diffusion of best practices• Ongoing, visible performance comparisons and strong incentives to improve vs. local

rivals

Clusters stimulate and enable innovation • Enhanced ability to perceive innovation opportunities• Presence of multiple suppliers and institutions to assist in knowledge creation• Ease of experimentation given locally available resources

Clusters facilitate commercialization• Opportunities for new companies and new lines of established business are more

apparent• Commercializing new products and starting new companies is easier because of available

skills, suppliers, etc.

Clusters reflect the fundamental influence of externalities / linkagesacross firms and associated institutions in competition

21 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

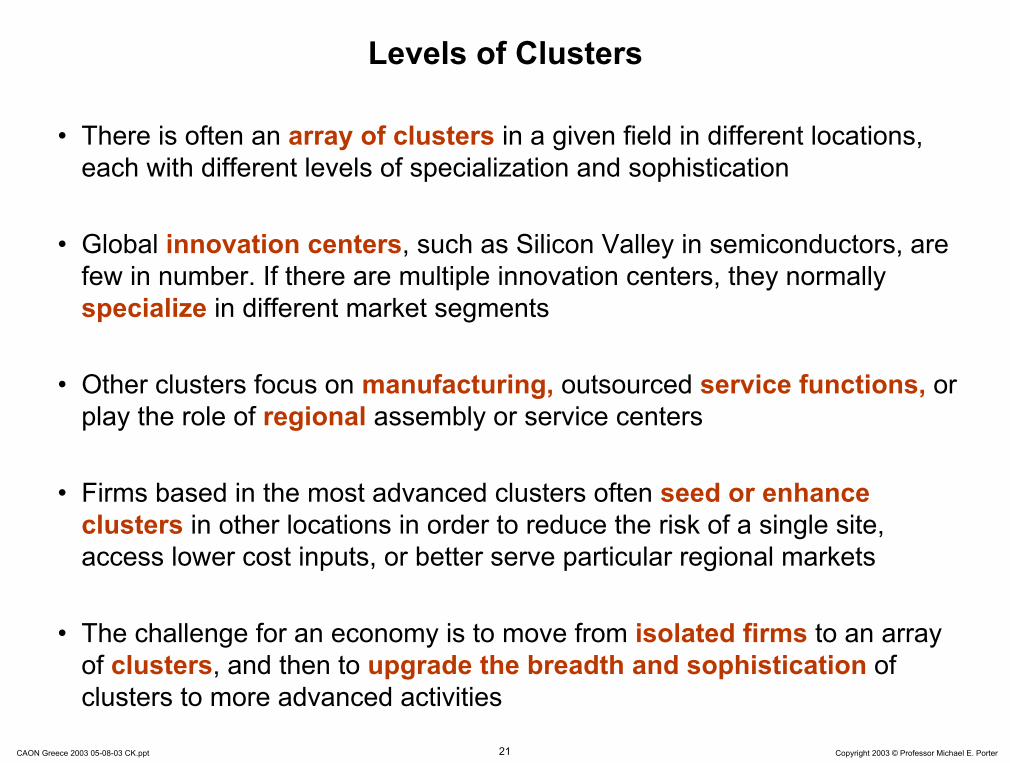

Levels of Clusters

• There is often an array of clusters in a given field in different locations, each with different levels of specialization and sophistication

• Global innovation centers, such as Silicon Valley in semiconductors, are few in number. If there are multiple innovation centers, they normally specialize in different market segments

• Other clusters focus on manufacturing, outsourced service functions, or play the role of regional assembly or service centers

• Firms based in the most advanced clusters often seed or enhance clusters in other locations in order to reduce the risk of a single site, access lower cost inputs, or better serve particular regional markets

• The challenge for an economy is to move from isolated firms to an array of clusters, and then to upgrade the breadth and sophistication of clusters to more advanced activities

22 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

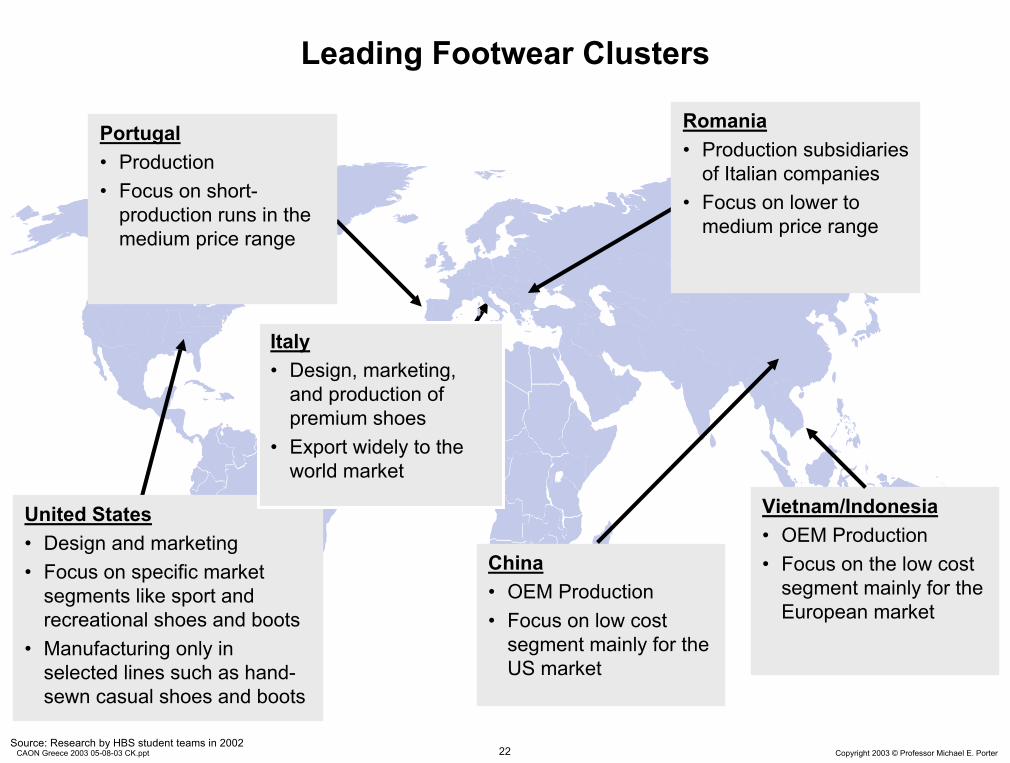

Leading Footwear Clusters

Vietnam/Indonesia• OEM Production • Focus on the low cost

segment mainly for the European market

China• OEM Production• Focus on low cost

segment mainly for the US market

Portugal• Production • Focus on short-

production runs in the medium price range

Romania• Production subsidiaries

of Italian companies• Focus on lower to

medium price range

United States• Design and marketing • Focus on specific market

segments like sport and recreational shoes and boots

• Manufacturing only in selected lines such as hand-sewn casual shoes and boots

Source: Research by HBS student teams in 2002

Italy• Design, marketing,

and production of premium shoes

• Export widely to the world market

23 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

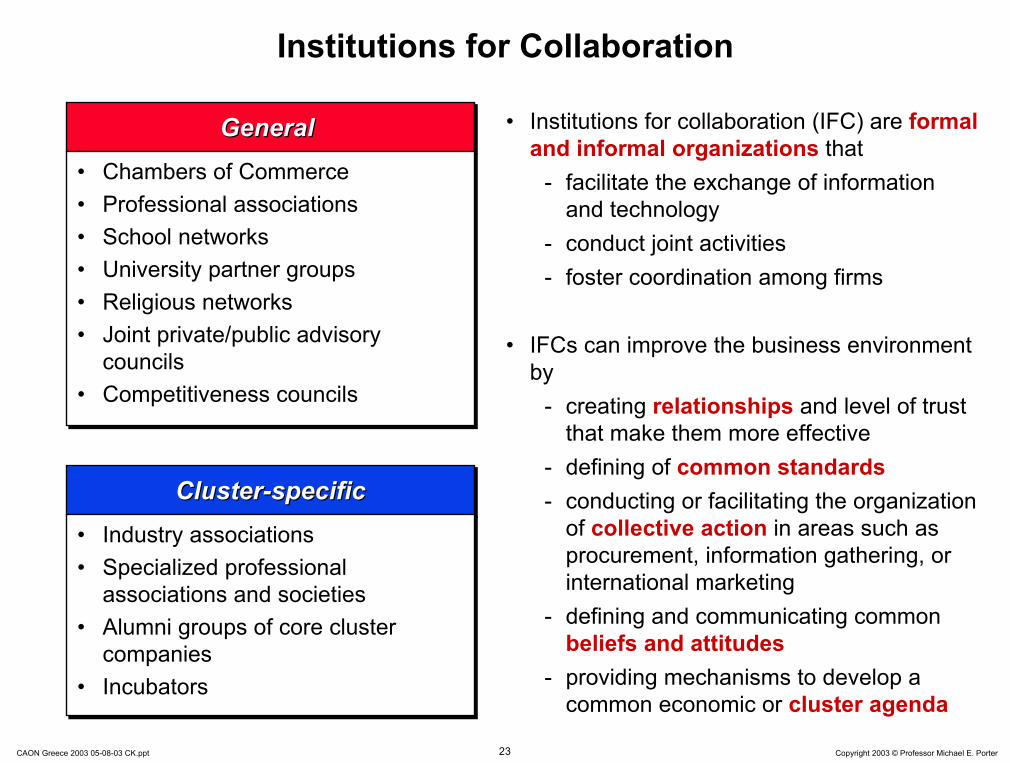

General General General

• Chambers of Commerce• Professional associations• School networks • University partner groups• Religious networks• Joint private/public advisory

councils• Competitiveness councils

• Chambers of Commerce• Professional associations• School networks • University partner groups• Religious networks• Joint private/public advisory

councils• Competitiveness councils

Cluster-specificClusterCluster--specificspecific

• Industry associations• Specialized professional

associations and societies• Alumni groups of core cluster

companies• Incubators

• Industry associations• Specialized professional

associations and societies• Alumni groups of core cluster

companies• Incubators

Institutions for Collaboration

• Institutions for collaboration (IFC) are formal and informal organizations that

- facilitate the exchange of information and technology

- conduct joint activities- foster coordination among firms

• IFCs can improve the business environment by

- creating relationships and level of trust that make them more effective

- defining of common standards- conducting or facilitating the organization

of collective action in areas such as procurement, information gathering, or international marketing

- defining and communicating common beliefs and attitudes

- providing mechanisms to develop a common economic or cluster agenda

Institutions for CollaborationSelected Institutions for Collaboration, San Diego

Source: Clusters of Innovation project (www.compete.org)

GeneralGeneral

San Diego Chamber of Commerce

San Diego MIT Enterprise Forum

Corporate Director’s Forum

San Diego Dialogue

Service Corps of Retired Executives, San Diego

San Diego Regional Economic Development Corporation

Center for Applied Competitive Technologies

San Diego World Trade Center

UCSD Alumni

San Diego Regional Technology Alliance

San Diego Science and Technology Council

Office of Trade and Business Development

San Diego Chamber of Commerce

San Diego MIT Enterprise Forum

Corporate Director’s Forum

San Diego Dialogue

Service Corps of Retired Executives, San Diego

San Diego Regional Economic Development Corporation

Center for Applied Competitive Technologies

San Diego World Trade Center

UCSD Alumni

San Diego Regional Technology Alliance

San Diego Science and Technology Council

Office of Trade and Business Development

Cluster-SpecificCluster-Specific

Telecommunication

Linkabit Alumni

Biotech

Hybritech Alumni

Scripps Research Institute Alumni

BIOCOMM

UCSD Connect

Telecommunication

Linkabit Alumni

Biotech

Hybritech Alumni

Scripps Research Institute Alumni

BIOCOMM

UCSD Connect

25 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Stages Of Competitive Development

Factor-Driven Economy

FactorFactor--Driven Driven EconomyEconomy

Investment-Driven Economy

InvestmentInvestment--Driven EconomyDriven Economy

Innovation-Driven Economy

InnovationInnovation--Driven EconomyDriven Economy

Source: Porter, Michael E., The Competitive Advantage of Nations, The Free Press: New York (1990)

Low InputCost

Efficiency Through Heavy Investment

Unique Value

26 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Greece’s Competitiveness Agenda 2003

• Continue the macroeconomic progress

• Upgrade the business environment

• Foster cluster development

• Create a regional strategy for Southeast Europe

• Shift the roles of government and business in economic development

27 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

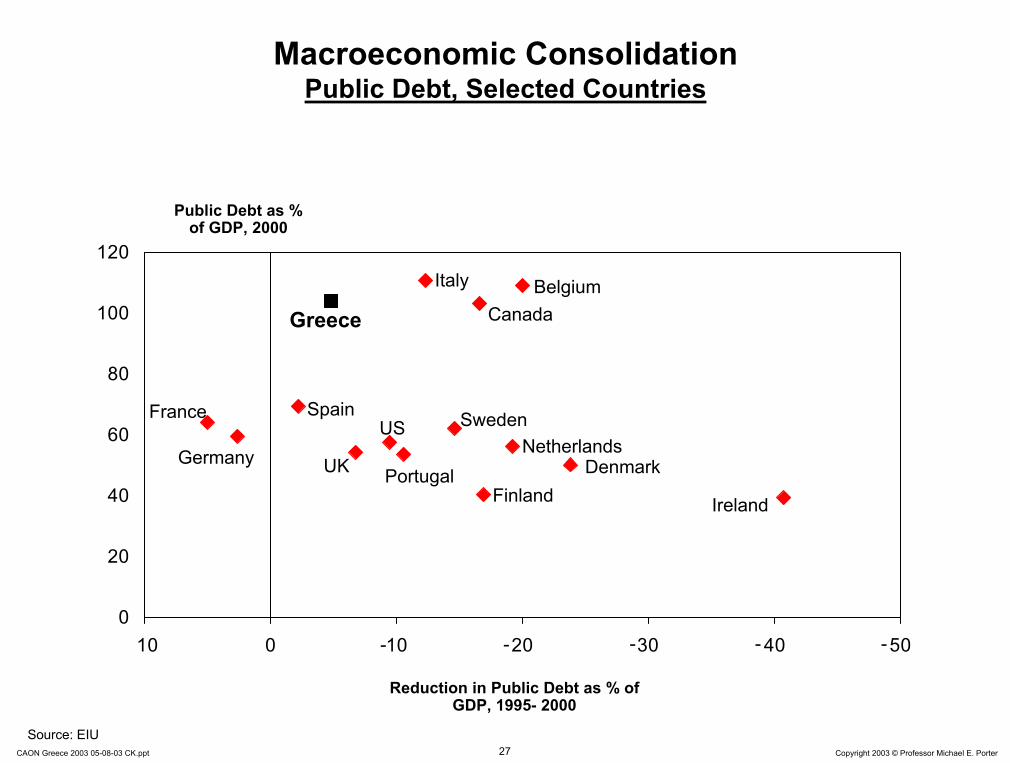

Macroeconomic ConsolidationPublic Debt, Selected Countries

0

20

40

60

80

100

120

-10 0 10 20 30 40 50

Public Debt as % of GDP, 2000

Reduction in Public Debt as % of GDP, 1995- 2000

Portugal

Source: EIU

Ireland

CanadaBelgium

Greece

Italy

SpainFrance SwedenUSGermany Denmark

NetherlandsUK

Finland

- - - - -

28 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

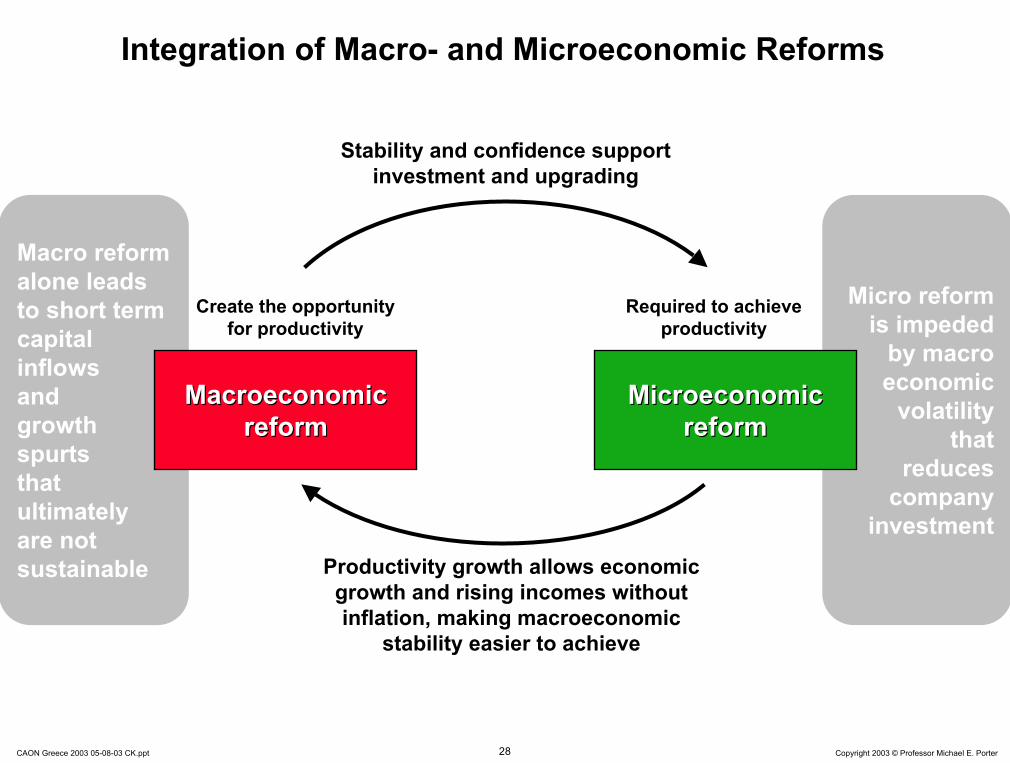

Micro reform is impeded

by macro economic

volatility that

reduces company

investment

Macro reform alone leads to short term capital inflows and growth spurts that ultimately are not sustainable

Integration of Macro- and Microeconomic Reforms

Macroeconomic Macroeconomic reformreform

Microeconomic Microeconomic reformreform

Create the opportunityfor productivity

Required to achieveproductivity

Productivity growth allows economic growth and rising incomes without inflation, making macroeconomic

stability easier to achieve

Stability and confidence support investment and upgrading

29 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Greece’s Competitiveness Agenda 2003

• Continue the macroeconomic progress

• Upgrade the business environment

• Foster cluster development

• Create a regional strategy for Southeast Europe

• Shift the roles of government and business in economic development

30 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Factor (Input) ConditionsGreece’s Relative Position

Factor(Input)

Conditions

Factor(Input)

Conditions

Availability of Scientists and Engineers 21

Ease of Access to Loans 31

University/Industry Research Collaboration 34

Judicial Independence 36

Local Equity Market Access 36

Telephone/Fax Infrastructure Quality 38

Venture Capital Availability 38

Financial Market Sophistication 40

Extent of Bureaucratic Red Tape 41

Intellectual Property Protection 41

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Quality of Management Schools 62

Administrative Burden for Start-Ups 61

Quality of Public Schools 52

Quality of Scientific Research Institutions 51

Electricity Supply Quality 49

Overall Infrastructure Quality 48

Port Infrastructure Quality 48

Railroad Infrastructure Quality 48

Police Protection of Businesses 47

Adequacy of Public Sector Legal Recourse43

Air Transport Infrastructure Quality 43

Quality of Math and Science Education 42

Note: Rank by countries; overall Greece ranks 43 out of 80 countries (41 on National Business Environment, 28 on GDP pc 2001)Source: Global Competitiveness Report 2002

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

31 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Educational AttainmentSouthern European Countries and Regions

32% 36%49% 52% 54%

62%78%

46% 43%33%

18%

36% 16%

12%22% 21% 18%

30%

10%22%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

France(South-West)

EU-15 Greece Basque Italy Spain Portugal

HighMediumLow

Share of 25-59 year old by level of educational attainment

Source: European Commission

Factor(Input)

Conditions

Factor(Input)

Conditions

32 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

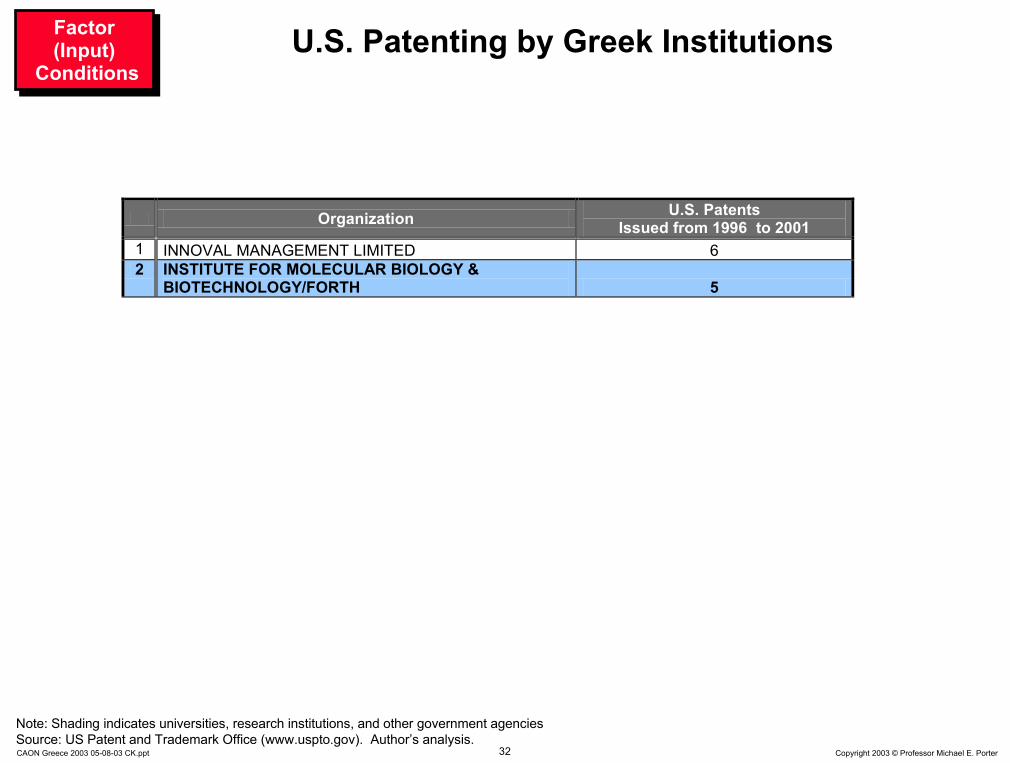

U.S. Patenting by Greek Institutions

Organization U.S. Patents Issued from 1996 to 2001

1 INNOVAL MANAGEMENT LIMITED 6 2 INSTITUTE FOR MOLECULAR BIOLOGY &

BIOTECHNOLOGY/FORTH 5

Note: Shading indicates universities, research institutions, and other government agencies Source: US Patent and Trademark Office (www.uspto.gov). Author’s analysis.

Factor(Input)

Conditions

Factor(Input)

Conditions

33 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Patents by OrganizationCommonwealth of Massachusetts

Organization Patents Issued from 1997 to 2001 1 MASSACHUSETTS INSTITUTE OF TECHNOLOGY 518 2 GENERAL HOSPITAL CORPORATION 296 3 EMC CORPORATION 269 4 DIGITAL EQUIPMENT CORPORATION 261 5 POLAROID CORPORATION 213 6 ANALOG DEVICES, INC. 167 7 MILLENNIUM PHARMACEUTICALS, INC. 165 8 HARVARD UNIVERSITY 150 9 COMPAQ COMPUTER CORPORATION, INC. 147 10 SUN MICROSYSTEMS, INC. 143 11 BOSTON SCIENTIFIC CORPORATION 135 12 ACUSHNET COMPANY 130 13 GENETICS INSTITUTE, INC. 127 14 GILLETTE COMPANY 112 15 BRIGHAM AND WOMEN'S HOSPITAL 107 16 RAYTHEON COMPANY 101 17 GENERAL ELECTRIC COMPANY 99 18 HEWLETT-PACKARD COMPANY 96 19 CHILDREN'S MEDICAL CENTER CORPORATION 93 20 QUANTUM CORP. (CA) 93 21 COGNEX CORPORATION 90 22 DANA-FARBER CANCER INSTITUTE 90 23 JOHNSON & JOHNSON PROFESSIONAL INC. 90 24 BOSTON UNIVERSITY 84 25 SEPRACOR INC. 84

Note: Shading indicates universities, research institutions, and other government agencies Source: US Patent and Trademark Office (www.uspto.gov). Author’s analysis.

34 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Public R&D Spending as % of GDP, 2001 (or last available)

Source: EU Scoreboard

Government R&D Spending Selected European Countries

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

-10% -5% 0% 5% 10% 15%

Change of Public R&D Spending as % of GDP, last three years

Germany Denmark

Sweden

UK

France

Finland

Netherlands

Slovakia

Greece

LatviaIreland

BulgariaSpain Hungary

Poland

Estonia ItalyLithuania

Czech Rep.Belgium

PortugalSlovenia

Factor(Input)

Conditions

Factor(Input)

Conditions

35 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

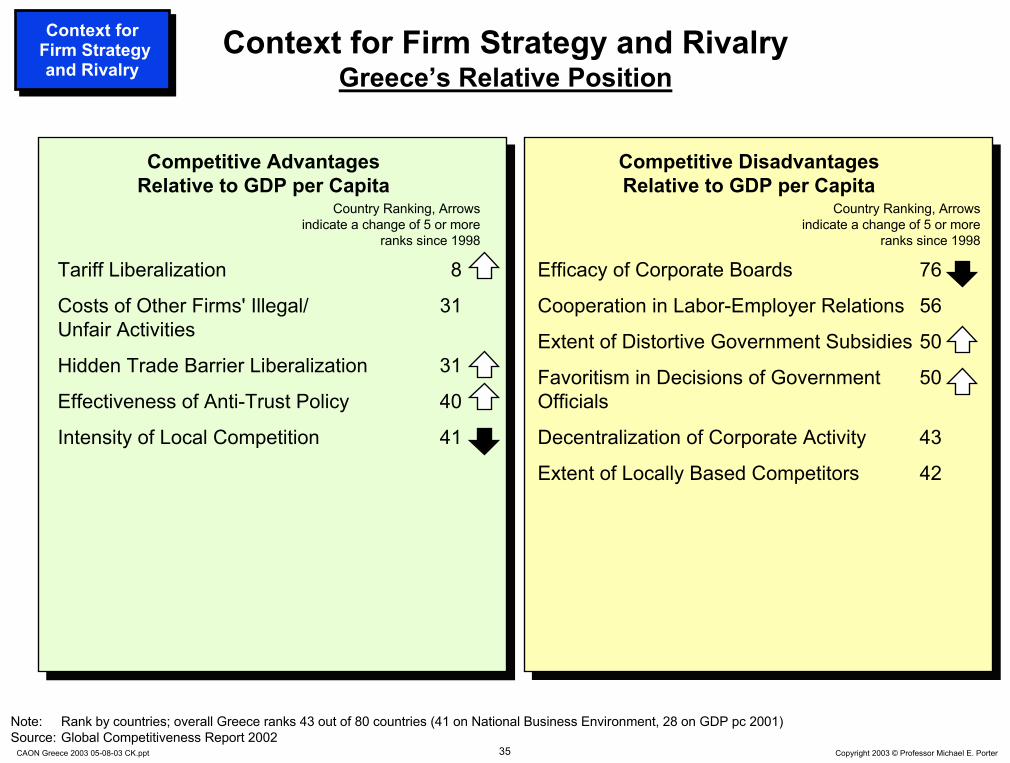

Context for Firm Strategy and RivalryGreece’s Relative Position

Tariff Liberalization 8

Costs of Other Firms' Illegal/ 31Unfair Activities

Hidden Trade Barrier Liberalization 31

Effectiveness of Anti-Trust Policy 40

Intensity of Local Competition 41

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Efficacy of Corporate Boards 76

Cooperation in Labor-Employer Relations 56

Extent of Distortive Government Subsidies 50

Favoritism in Decisions of Government 50 Officials

Decentralization of Corporate Activity 43

Extent of Locally Based Competitors 42

Context for Firm Strategy and Rivalry

Context for Firm Strategy and Rivalry

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Note: Rank by countries; overall Greece ranks 43 out of 80 countries (41 on National Business Environment, 28 on GDP pc 2001)Source: Global Competitiveness Report 2002

36 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

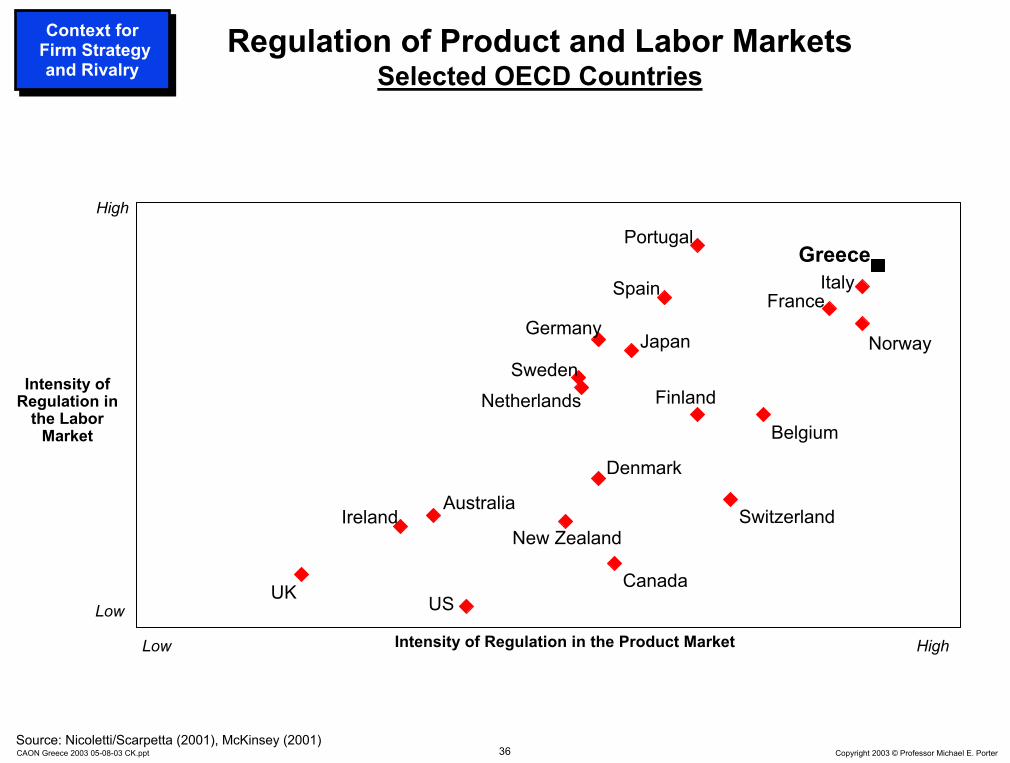

Spain France

Australia

New ZealandIreland

Sweden

UK CanadaUS

Finland

Regulation of Product and Labor MarketsSelected OECD Countries

Denmark

Germany

GreeceItaly

Japan

Netherlands

Norway

Portugal

Switzerland

Intensity of Regulation in the Product Market

Intensity of Regulation in

the Labor Market

Low

Low

High

High

Source: Nicoletti/Scarpetta (2001), McKinsey (2001)

Belgium

Context for Firm Strategy and Rivalry

Context for Firm Strategy and Rivalry

37 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

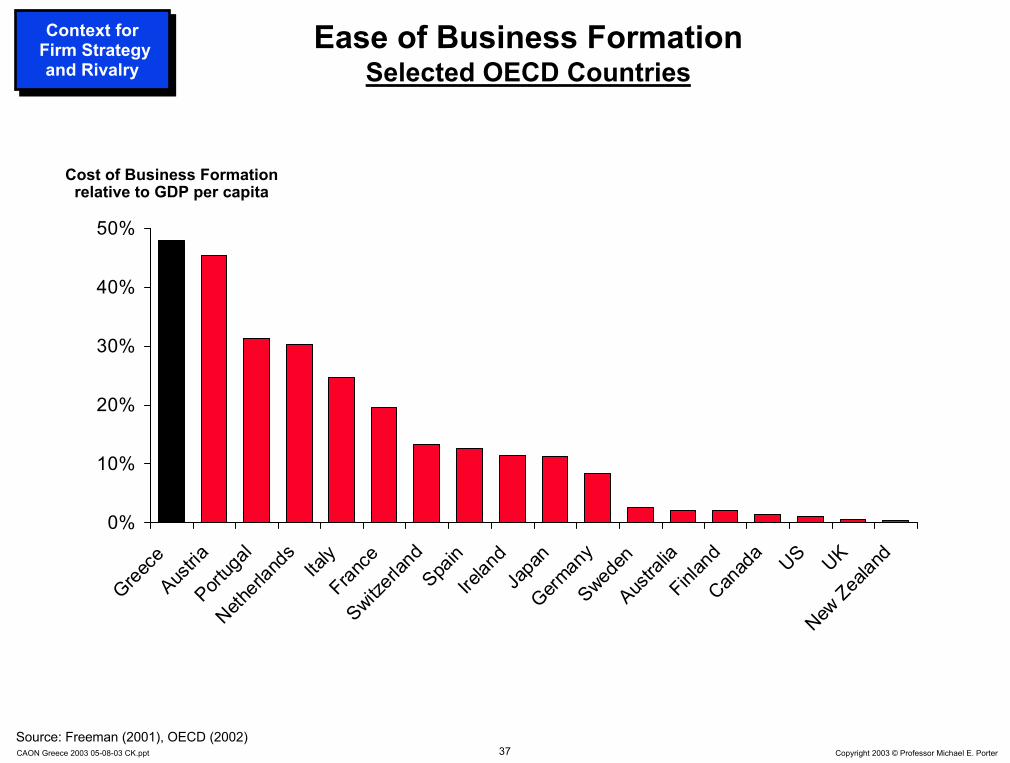

Ease of Business FormationSelected OECD Countries

0%

10%

20%

30%

40%

50%

Greece

Austria

Portug

alNeth

erlan

ds Italy

France

Switzerl

and

Spain

Irelan

dJa

pan

German

ySwed

enAus

tralia

Finlan

dCan

ada US UK

New Zea

land

Cost of Business Formation relative to GDP per capita

Source: Freeman (2001), OECD (2002)

Context for Firm Strategy and Rivalry

Context for Firm Strategy and Rivalry

38 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Demand ConditionsGreece’s Relative Position

Buyer Sophistication 37

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Laws Relating to Information Technology 67

Government Procurement of Advanced 56 Technology Products

Consumer Adoption of Latest Products 52

Stringency of Environmental Regulations 50

Demand ConditionsDemand

Conditions

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Note: Rank by countries; overall Greece ranks 43 out of 80 countries (41 on National Business Environment, 28 on GDP pc 2001)Source: Global Competitiveness Report 2002

39 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Related and Supporting IndustriesGreece’s Relative Position

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Related and Supporting Industries

Related and Supporting Industries

State of Cluster Development 67

Extent of Product and Process 65 Collaboration

Local Availability of Components 60and Parts

Local Availability of Specialized 57 Research and Training Services

Local Availability of Process Machinery 54

Local Supplier Quality 49

Local Supplier Quantity 47

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Note: Rank by countries; overall Greece ranks 43 out of 80 countries (41 on National Business Environment, 28 on GDP pc 2001)Source: Global Competitiveness Report 2002

40 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Company Operations and StrategyGreece’s Relative Position 2002

Extent of Marketing 30

Control of International Distribution 38

Value Chain Presence 40

Production Process Sophistication 42

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Note: Rank by countries; overall the Greece ranks 43 out of 80 countries (47 on Company Operations and Strategy, 28 on GDP pc 2001)Source: Global Competitiveness Report 2002

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Reliance on Professional Management 67

Willingness to Delegate Authority 63

Capacity for Innovation 57

Extent of Staff Training 57

Company Spending on R&D 56

Breadth of International Markets 47

Extent of Branding 47

Extent of Incentive Compensation 47

Degree of Customer Orientation 44

41 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

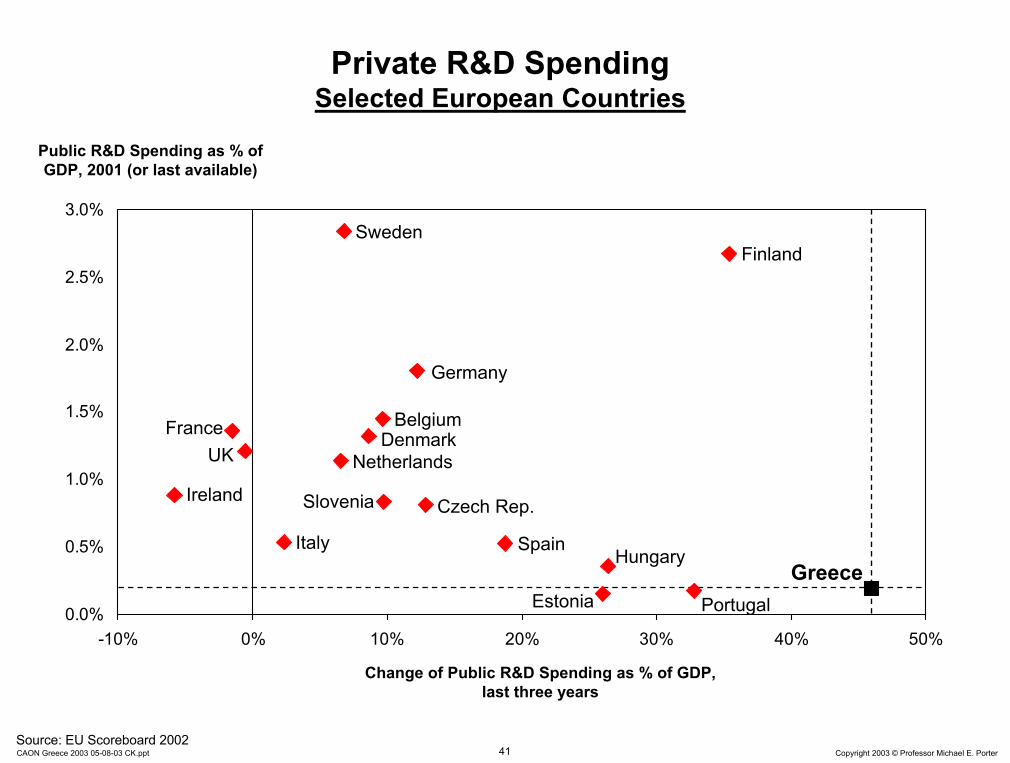

Public R&D Spending as % of GDP, 2001 (or last available)

Source: EU Scoreboard 2002

Private R&D Spending Selected European Countries

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

-10% 0% 10% 20% 30% 40% 50%

Change of Public R&D Spending as % of GDP, last three years

Germany

Denmark

Sweden

UKFrance

Finland

Netherlands

Greece

Ireland

SpainHungary

Estonia

Italy

Czech Rep.

Belgium

Portugal

Slovenia

42 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Greece’s Competitiveness Agenda 2003

• Continue the macroeconomic progress

• Upgrade the business environment

• Foster cluster development

• Create a regional strategy for Southeast Europe

• Shift the roles of government and business in economic development

43 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Greece’s average change in world goods export share:

- 0.03%

Greece’s average goods export share: 0.19%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

-0.3% -0.2% -0.1% 0.0% 0.1% 0.2%

Source: UNCTAD Trade Data. Author’s analysis.

Change in Greece’s World Export Share, 1995 - 2000

Greek Export Performance By Broad Sector1995-2000

Power Health Care

Food/Beverages

EntertainmentOffice

Personal

Textiles/Apparel

Transportation

Multiple Business

DD = $500 million export volume in 2000

+

Petroleum/Chemicals

Materials/Metals

+

World Export Share, 2000

Housing/Household

• Greece is loosing position in some of its largest export clusters

Information Technology

Telecommunications

44 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

-15% -10% -5% 0% 5% 10% 15%

Source: World Tourism Organization

Change in %CAGR of Tourism Receipts per Capita, 1997-2000

Tourism Cluster Performance

+++

Tourism Receipts per Capita, 2000

• Greece has a strong tourism cluster that increased revenues per tourists in the last few years

Switzerland

Australia

Germany

United States

France

GreeceItaly

Hong Kong

Turkey

Mexico

UKSpain

China

CanadaAustria

= 2.5% World Market Share

45 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

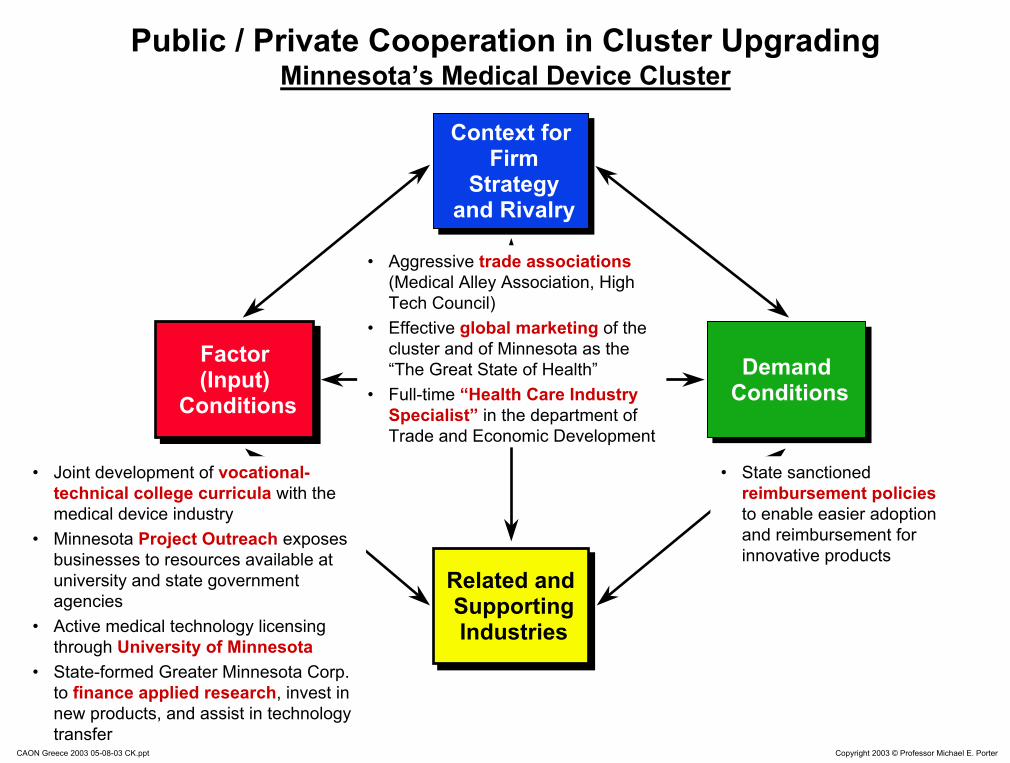

Public / Private Cooperation in Cluster UpgradingMinnesota’s Medical Device Cluster

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

• Joint development of vocational-technical college curricula with the medical device industry

• Minnesota Project Outreach exposes businesses to resources available at university and state government agencies

• Active medical technology licensing through University of Minnesota

• State-formed Greater Minnesota Corp. to finance applied research, invest in new products, and assist in technology transfer

• State sanctioned reimbursement policiesto enable easier adoption and reimbursement for innovative products

• Aggressive trade associations(Medical Alley Association, High Tech Council)

• Effective global marketing of the cluster and of Minnesota as the “The Great State of Health”

• Full-time “Health Care Industry Specialist” in the department of Trade and Economic Development

46 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1995 1996 1997 1998 1999 20000%

1%

2%

3%

4%

5%

6%

7%

8%

ValueMarket Share

The Australian Wine ClusterTrade Performance

Source: UN Trade Statistics

Australian Wine Exports in million US

DollarsAustralian Wine

World Export Market Share

47 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

The Australian Wine ClusterHistory

1955

Australian Wine Research Institute founded

1970

Winemaking school at Charles Sturt University founded

1980

Australian Wine and Brandy Corporation established

1965

Australian Wine Bureau established

1930

First oenology course at Roseworthy Agricultural College

1950s

Import of European winery technology

1960s

Recruiting of experienced foreign investors, e.g. Wolf Bass

1990s

Surge in exports and international acquisitions

1980s

Creation of large number of new wineries

1970s

Continued inflow of foreign capital and management

1990

Winemaker’s Federation of Australia established

1991 to 1998

New organizations created for education, research, market information, and export promotions

Source: Michael E. Porter and Örjan Sölvell, The Australian Wine Cluster – Supplement, Harvard Business School Case Study, 2002

48 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

The Australian Wine ClusterRecently founded Institutions for Collaboration

Wine Industry National Education and Training Council

Wine Industry National Wine Industry National Education and Training CouncilEducation and Training Council

Established in 1995

Focus: Coordination, integration, and standard maintenance for vocational training and education

Funding: Government; other cluster organizations

Established in 1995

Focus: Coordination, integration, and standard maintenance for vocational training and education

Funding: Government; other cluster organizations

Cooperative Centre for ViticultureCooperative Cooperative Centre Centre for Viticulturefor Viticulture

Established in 1991

Focus: Coordination of research and education policy in viticulture

Funding: other cluster organizations

Established in 1991

Focus: Coordination of research and education policy in viticulture

Funding: other cluster organizations

Australian Wine Export CouncilAustralian Wine Export CouncilAustralian Wine Export Council

Established in 1992

Focus: Wine export promotion through international offices in London and San Francisco

Funding: Government; cluster organizations

Established in 1992

Focus: Wine export promotion through international offices in London and San Francisco

Funding: Government; cluster organizations

Winemakers’ Federation of AustraliaWinemakers’ Federation of AustraliaWinemakers’ Federation of Australia

Established in 1990

Focus: Public policy representation of companies in the wine cluster

Funding: Member companies

Established in 1990

Focus: Public policy representation of companies in the wine cluster

Funding: Member companies

Grape and Wine R&D CorporationGrape and Wine R&D CorporationGrape and Wine R&D Corporation

Established in 1991 as statutory body

Focus: Funding of research and development activities

Funding: Government; statutory levy

Established in 1991 as statutory body

Focus: Funding of research and development activities

Funding: Government; statutory levy

Wine Industry Information ServiceWine Industry Information ServiceWine Industry Information Service

Established in 1998

Focus: Information collection, organization, and dissemination

Funding: Cluster organizations

Established in 1998

Focus: Information collection, organization, and dissemination

Funding: Cluster organizations

Source: Michael E. Porter and Örjan Sölvell, The Australian Wine Cluster – Supplement, Harvard Business School Case Study, 2002

49 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Appropriate Roles of Government in Cluster Development

• A successful cluster policy builds on sound overall economic policies

• Government should support the development of all clusters, not choose among them

• Government policy should reinforce established and emerging clusters rather than attempt to create entirely new ones

• Government’s role in cluster initiatives is as facilitator and participant. The most successful cluster initiatives are a public-private partnership

50 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Cluster Policy versus Industrial Policy

Industrial Policy

Industrial Industrial PolicyPolicy

Cluster-basedPolicy

ClusterCluster--basedbasedPolicyPolicy

• Target desirable industries / sectors

• Focus on domestic companies

• Intervene in competition (e.g., protection, industry promotion, subsidies)

• Centralizes decisions at the national level

• All clusters can contribute to prosperity

• Domestic and foreign companies both enhance productivity

• Relax impediments and constraints to productivity

• Emphasize cross-industry linkages / complementarities

• Encourage initiative at the state and local level

Distort competition Enhance competition

51 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Greece’s Competitiveness Agenda 2003

• Continue the macroeconomic progress

• Upgrade the business environment

• Foster cluster development

• Create a regional strategy for Southeast Europe

• Shift the roles of government and business in economic development

52 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Influences on CompetitivenessMultiple Geographic Levels

Broad Economic AreasBroad Economic Areas

Groups of Neighboring Groups of Neighboring NationsNations

States, ProvincesStates, Provinces

Cities, Metropolitan Cities, Metropolitan AreasAreas

NationsNations

World EconomyWorld Economy

53 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Cross-National Regions and Economic StrategyTraditional Views• Regions as free trade zones; regions as economic unions (e.g., United States,

European Union)

New View• A regional strategy as a powerful tool to enhance competitiveness in autonomous

countries• Internal trade and investment

– Gains from internal trade and investmentAND

• Company operations and strategy– Enhancing the competitive capability of firms– Expanding trade in non-traditional export industries

• Business environment– Mutual benefits to the productivity of the business environment through policy coordination

that captures external economies and the benefits of specialization in institutions and infrastructure across borders

• Cluster development– Cross-border cluster specialization and integration

• Foreign investment– Enhancing interest and investment in the region by the international community

• Economic policy process– Improving economic policy formulation and implementation at the national level

54 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Cross-National Economic CoordinationAlternate Geographic Levels

Broad Economic AreasBroad Economic Areas

Groups of Neighboring Groups of Neighboring NationsNations

States, ProvincesStates, Provinces

Cities, Metropolitan Cities, Metropolitan AreasAreas

NationsNations

World EconomyWorld Economy

e.g. European Union

e.g. South-Eastern Europe

e.g. Greece

55 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

• Coordinate macroecono-mic policies

• Eliminate trade and investmentbarriers within the region

• Simplify cross-borderregulations and paperwork

• Guarantee minimum basic investor protections

• Set minimum environmentalstandards

• Set minimum safety standards

• Establish reciprocal consumer protection laws

• Agree on foreign investment promotion guidelines to limit forms of investment promotion that do not enhance productivity

• Coordinatedcompetition policy

• Improve regional transportation infrastructure

• Create an efficient energy network

• Upgrade/link regional communications

• Upgrade/linkfinancial markets

• Upgrade higher education through facilitating specialization and student exchanges

• Expand cross-border business and financial information access and sharing

• Coordinate activities to ensure personal safety

• Establish ongoing upgrading process in clusters that cross national borders, e.g.

– Tourism

– Agribusiness

– Textiles and Apparel

– Information Technology

• Share best practices in government operations

• Improve regional institutions

– Regional development bank

– Dispute resolution mechanisms

– Policy coordination body

• Develop a regional marketing strategy

Factor (Input)

Conditions

Factor Factor (Input)(Input)

ConditionsConditionsRegional

GovernanceRegional

GovernanceContext for

Strategy and Rivalry

Context for Context for Strategy Strategy

and Rivalryand Rivalry

Related and Supporting Industries

Related and Supporting Industries

Demand ConditionsDemand Demand

ConditionsConditions

Cross-National Economic Coordination Illustrative Policy Areas

56 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Greece’s Competitiveness Agenda 2003

• Continue the macroeconomic progress

• Upgrade the business environment

• Foster cluster development

• Create a regional strategy for Southeast Europe

• Shift the roles of government and business in economic development

57 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Shifting Responsibilities for Economic Development

Old ModelOld ModelOld Model

• Government drives economic development through policy decisions and incentives

• Government drives economic development through policy decisions and incentives

New ModelNew ModelNew Model

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

58 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

• Macroeconomic, political, legal, and social context– Establish a stable and predictable macroeconomic, legal, and political

environment – Improve the social conditions of citizens

• General microeconomic business environment– Improve the availability, quality, and efficiency of cross-cutting or

general purpose inputs, infrastructure, and institutions– Set overall rules and incentives governing competition that encourage

productivity growth

• Clusters– Facilitate cluster development and upgrading

• Process of Economic Change– Create institutions and processes for upgrading competitiveness that

inform citizens and mobilize the private sector, government at all levels, educational and other institutions, and civil society to take action

Roles of Government in Economic Development

59 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Role of the Private Sector in Economic Development

• A company’s competitive advantage is partly the result of the local environment

• Company membership in a cluster offers collective benefits• Private investment in “public goods” is justified

• Take an active role in upgrading the local infrastructure• Nurture local suppliers and attract new supplier investments • Work closely with local educational and research institutions to

upgrade quality and create specialized programs addressing cluster needs

• Provide government with information and substantive input on regulatory issues and constraints bearing on cluster development

• Focus corporate philanthropy on enhancing the local business environment

• An important role for trade associations– Greater influence – Cost sharing

60 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Selected References• The Competitive Advantage of Nations, New York: The Free Press, 1990

• “Clusters and the New Competitive Agenda for Companies and Governments” in On Competition, Boston: Harvard Business School Press, 1998

• “The Microeconomic Foundations of Economic Development,” in The Global Competitiveness Report 1998-99, (World Economic Forum, 1998)

• “The Current Competitiveness Index: Measuring the Microeconomic Foundations of Prosperity” in The Global Competitiveness Report 2000-01, New York: Oxford University Press, 2000

• “Enhancing the Microeconomic Foundations of Prosperity: The Current Competitiveness Index” in The Global Competitiveness Report 2001-02, New York: Oxford University Press, 2001

• “Building the Microeconomic Foundations of Prosperity: Findings from the Microeconomic Competitiveness Index” in The Global Competitiveness Report 2002-03, New York: Oxford University Press, forthcoming 2002

• “Location, Competition, and Economic Development: Local Clusters in a Global Economy,” (Economic Development Quarterly, February 2000, 15-34)

• “Locations, Clusters, and Company Strategy” in The Oxford Handbook of Economic Geography, (G. L. Clark, M.P. Feldman, and M.S. Gertler, eds.), New York: Oxford University Press, 2000

• “Attitudes, Values, Beliefs and the Microeconomics of Prosperity,” in Culture Matters: How Values Shape Human Progress, (L.E. Harrison, S.P. Huntington, eds.), New York: Basic Books, 2000

61 Copyright 2003 © Professor Michael E. PorterCAON Greece 2003 05-08-03 CK.ppt

Web resources

• Institute for Strategy and Competitiveness www.isc.hbs.edu

• ISC Cluster Mapping Data (US) data.isc.hbs.edu/isc/index.jsp

• Cluster of Innovation Initiative– Council on Competitiveness www.compete.org– Monitor Company www.monitor.com