the coming of energy democracy - midwest renewable energy fair

TRANSCRIPT

T H E C O M I N G O F E N E R G Y D E M O C R A C Y

TA K I N G C H A R G E O F O U R E N E R G Y F U T U R E

John Farrell Director of Energy DemocracyJune 17, 2016

Presentation to the Midwest Energy Fair

A Q U E S T I O N

S M A R T P H O N E I M A G E Did you get one of these…

Photo credits: Donnie Ray Jones and Billy Brown via Flickr

D I S R U P T I O N

From your landline phone

company?

A B O R I N G PA S T

“There is one great advantage that must follow regulation, and

that advantage is protection"

F I R S T S TAT E O V E R S I G H T O F M O N O P O LY U T I L I T I E S ( C . 1 9 0 5 )

T H I S C O U L D TA K E A

W H I L E …

“We come to work each day to do what we did the day before”

A D I F F E R E N T E R A

S AV I N G S T H R O U G H P S Y C H O L O G Y

1,221 kWh

846 kWh

448 kWh

Efficient neighbors

All neighbors

YOU

Bill date: Jul 1 -Jul 31Great

Good

More than average

>You used 47% less than your efficient neighbors

HOW YOU’RE DOING

S AV I N G S T H R O U G H P S Y C H O L O G Y

1,221 kWh

846 kWh

448 kWh

Efficient neighbors

All neighbors

YOU

Bill date: Jul 1 -Jul 31Great

Good

More than average

>You used 47% less than your efficient neighbors

HOW YOU’RE DOING

1-3% savings

D E M A N D M A N A G E M E N T

D E M A N D M A N A G E M E N T

1 utility, 330 megawatts =

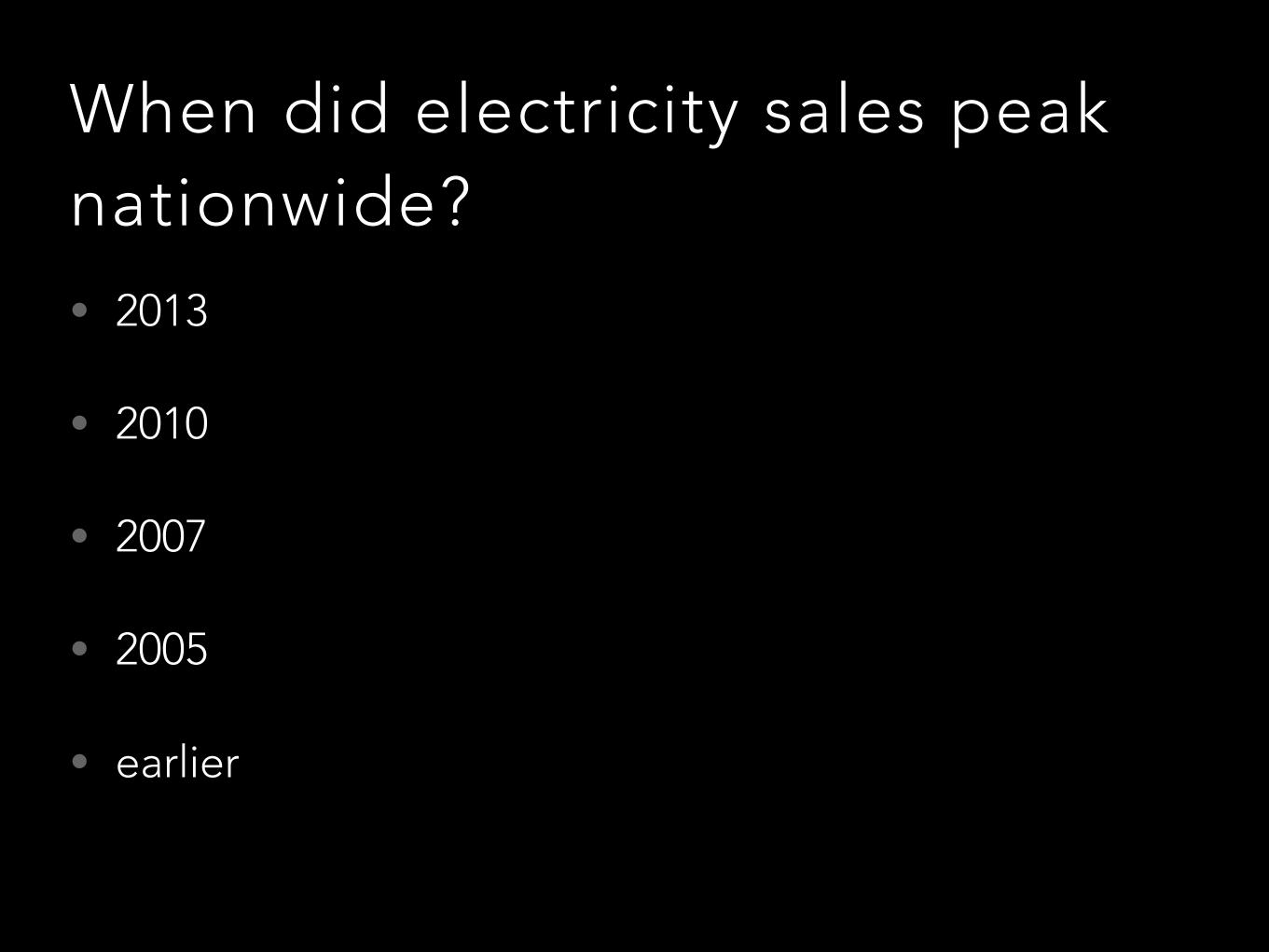

When did electricity sales peak nationwide?• 2013

• 2010

• 2007

• 2005

• earlier

3.2

3.3

3.4

3.5

3.6

3.7

3.8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

P E A K

S TA G N A N T R E TA I L S A L E S

trillion kilowatt-hours

What is the last year fossil fuel provided > 60% of new power plant capacity?

• 2013

• 2010

• 2007

• 2005

• earlier

Perc

ent o

f new

cap

acity

0%

20%

40%

60%

80%

100%

Fossil fuel Renewable

Gig

awat

ts a

dd

ed (w

hite

line

)

0

10

20

30

40

50

2003 2005 2007 2009 2011 2013 2015Q2

R I S I N G R E N E W A B L E E N E R G Y S H A R E

June 10, 2015

of new power plant capacity

Perc

ent o

f new

cap

acity

0%

20%

40%

60%

80%

100%

Coal Gas Wind Small Solar Big Solar

U . S . P O W E R P L A N T C A PA C I T Y A D D I T I O N S(annual megawatts, AC)

Sources: EIA and SEIA

Gig

awat

ts a

dd

ed (w

hite

line

)

0

10

20

30

40

50

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Q1

C O S T P R E S S U R E S

Lower wholesale prices mean utilities with excess generation sell for less

N O W M O V I N G FA S T

1 I N S TA L L E V E R Y 6 0 S E C O N D S

I N C O N T R A S T

0

7,500

15,000

22,500

30,000

$0.00

$2.50

$5.00

$7.50

$10.00

2000 2002 2004 2006 2008 2010 2012 2014

Weighted Avg. Cost ($/W)

Cumulative Capacity (MW)

SOLAR INSTALLS DRIVE RAPID PRICE DECLINE

B AT T E R I E S E V E R Y W H E R E

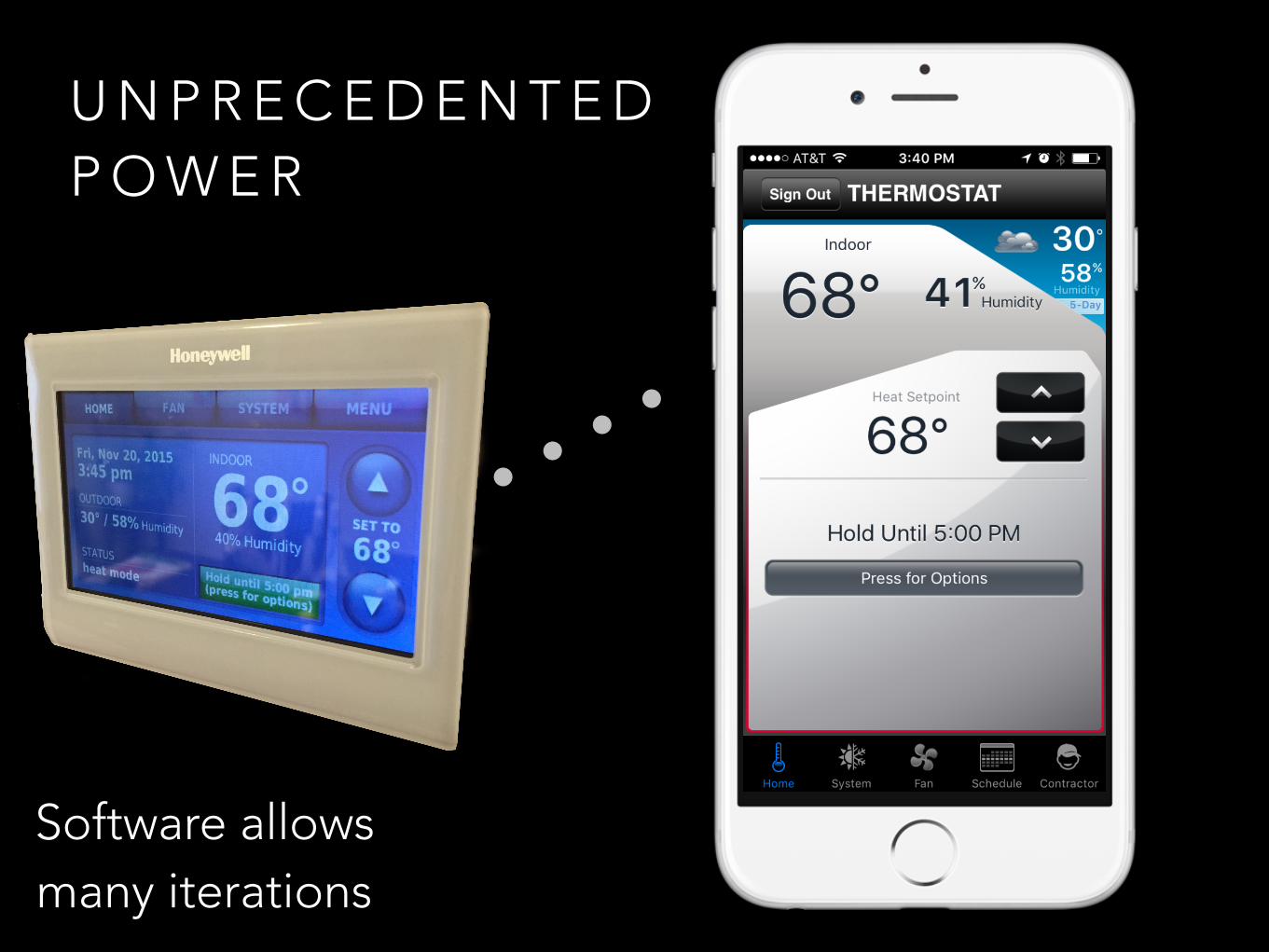

U N P R E C E D E N T E D P O W E R

Software allows many iterations

2007 2008 2011 2012 2013 2013 2014 20142009 2010

A W H O L E N E W W O R L D

Minster POPULATION 2,806

P E R C E N T O F H O U S E H O L D S W I T H

S O L A R

15%

In 20 years…

R . I . P.

U N P R E C E D E N T E D O P P O R T U N I T Y

$ 3 6 0 B I L L I O N

23%

49%

All buildings Source: http://www.nrel.gov/docs/fy16osti/65298.pdf

R O O F T O P S O L A R P O T E N T I A L 2 0 1 6

POTENTIAL PERCENT OF POWER FROM LOCAL

ROOFTOP SOLAROver 50% 40 to 50% 25 to 40% 11 to 25%

2008 data

40-50%25-40%

Over 50%

Over 50%

25-40%

40%

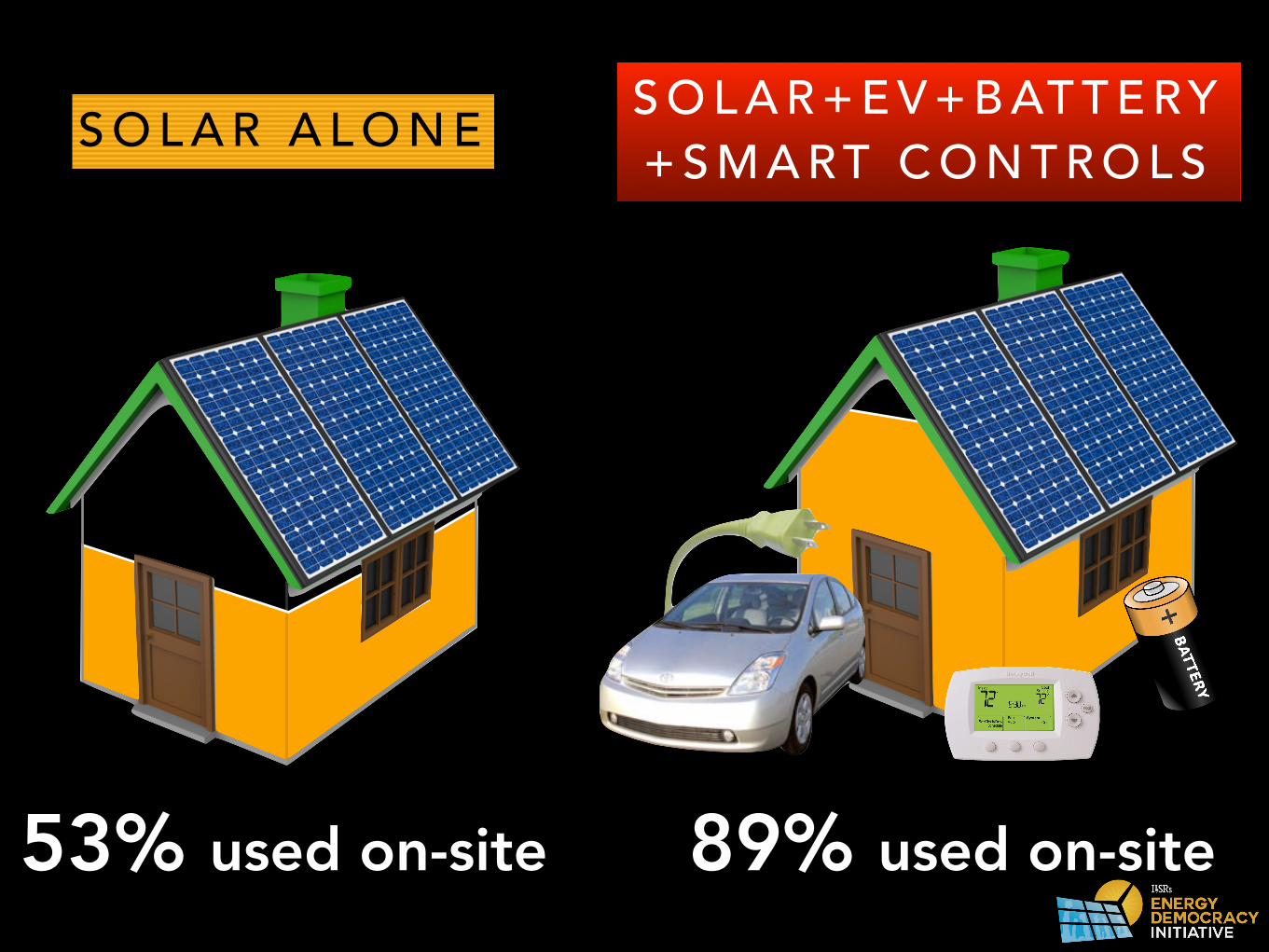

53% used on-site

S O L A R A L O N E S O L A R + E V + B AT T E R Y + S M A R T C O N T R O L S

89% used on-site

B I G B E N E F I T S

R E N E WA B L E B E N E F I T S

0

3

6

9

12

15

Jan-2002 Jan-2004 Jan-2006 Jan-2008 Jan-2010 Jan-2012 Jan-2014

Natural Gas Price

Wind and Sun Price

D I S T R I B U T E D B E N E F I T S

Solar on Littlestown Hospital

D I S P E R S I N G 1 - M W S O L A R P L A N T S R E D U C E S I N T E G R AT I O N C O S T S

0

1

2

3

4

1 solar project 5 solar projects 25 solar projects

0.3¢

1.1¢

3.9¢

cents per kilowatt-hour

Credit: USDA

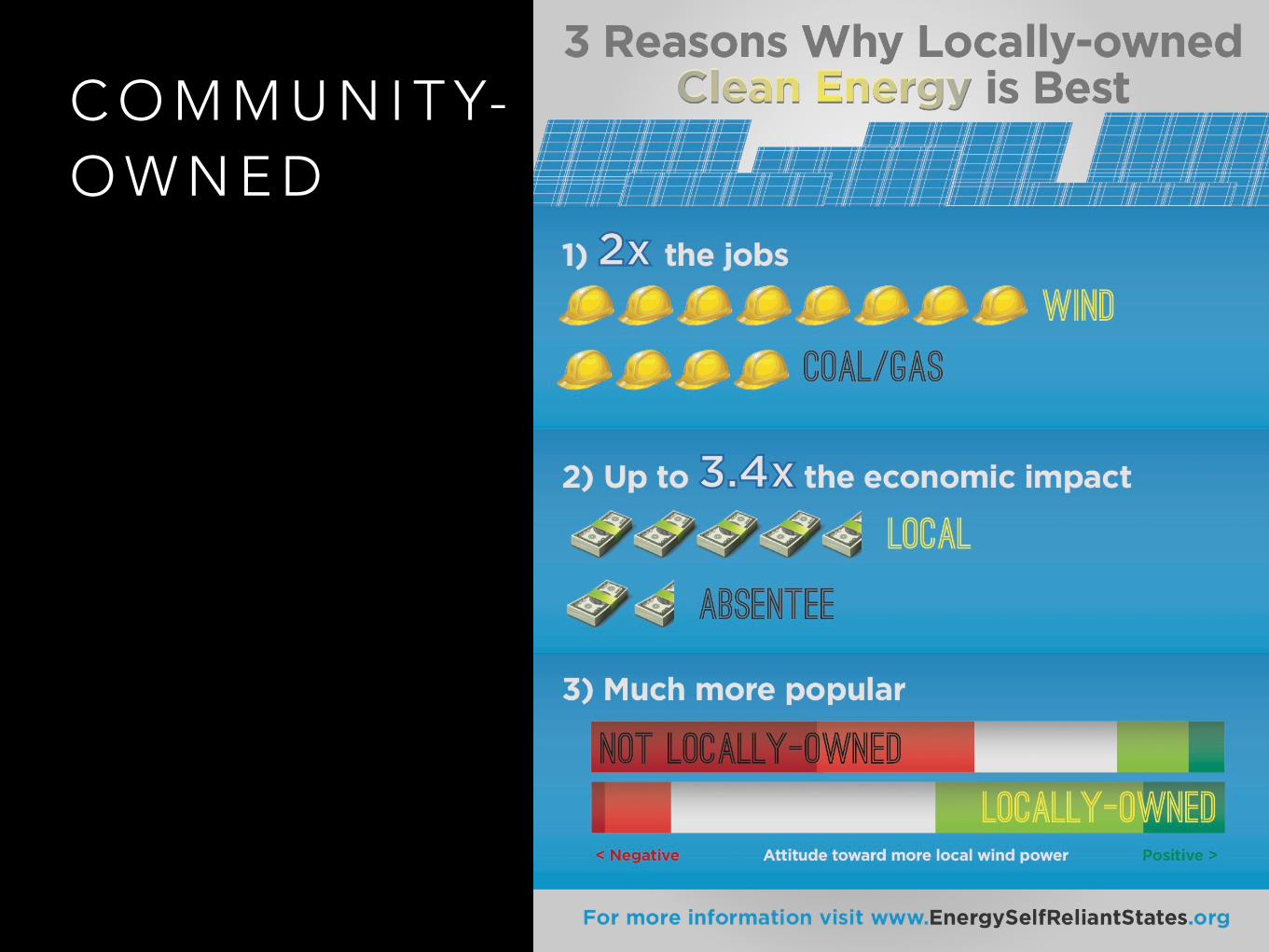

L O C A L E C O N O M I C B E N E F I T S

1 megawatt

$2.5 million

20 jobs

Source: ILSR, 2014

$5.4 million in energy savings

How Green Energy Farmers busted the barriers:

Formed several, unrelated LLCs with only Iowa owners.

State regulation Pass-through to individualsFor a limited time, the Production Tax Credit was available as a cash grant, more easily used by ordinary investors.

Sold to the utilityElectricity was sold via a power purchase agreement to the utility.

C O M M U N I T Y-O W N E D

O L D R U L E S

U T I L I T Y R U L E S A R E A N T I Q U E

A Q U E S T I O N

What are some rules we’ve already adopted?

Timeline of State Renewable Energy Standards

1983 1991 19991998199719961994

NE

NJ

TX

NV

NM WACADE

CT

MT

DCMD

HI

MN

MN

WIIA

IA

VT

PA

YEAR UPDATED

Sources: C2ES, DSIRE

YEAR ADOPTED

2000 2001 2002 20062005

OR

NC

NH

AZ MN

NV

NY

RI

CO

NM NJ

(30 total)

2003 20102004 200920082007

MA MI

MO

OH

IL

KS

WI

CT

PANM

NVMNCT

DE

CA

AZ

TXNVCO

CTCOCA

WINJHICT

NJ

TXPANMNJMNMEMD

MDMADEDC

NVMNMEILHIDC

DECO

RIOR NY

NJMD

Timeline of State Energy Efficiency Standards

1999 2000 20082007200620052004

CA

CO

CT

HI

IL

MD

MI

MN

NV

NM

NY

OH*NC

PA

PA

RITX

TX

VT

WA

YEAR UPDATED

Source: ACEEE, 2014, http://bit.ly/eers-timeline

YEAR ADOPTED

2009 2010 2011 201420132012

IA

ME

MA

OR

CA

HI

NV

AZ

AR WI

CT

NM

(25 total)

* “paused” in 2013

N E W R U L E S

E N E R G Y D E M O C R A C Y I N A C T I O N

GRID AS COMMONS

= super efficient buildings

A solution that New York is

pursuing

C O N E D

T R A N S PA R E N T P R I C I N G

Day NightNight

-6%

T R A N S PA R E N T P R I C I N G

Peak energy use

PECO, 2015

The utility adds a monthly assessment to the customer’s bill to pay for energy savings improvements, with the savings greater than the monthly cost.

A utility customer signs up for better insulation, a rooftop solar array, or a share of solar on a nearby building.

1

2

M A K I N G C L E A N E N E R G Y E A S I E R T H A N A C R E D I T C A R D S W I P E

F I N A N C I N G : O N - B I L L R E PAY M E N T

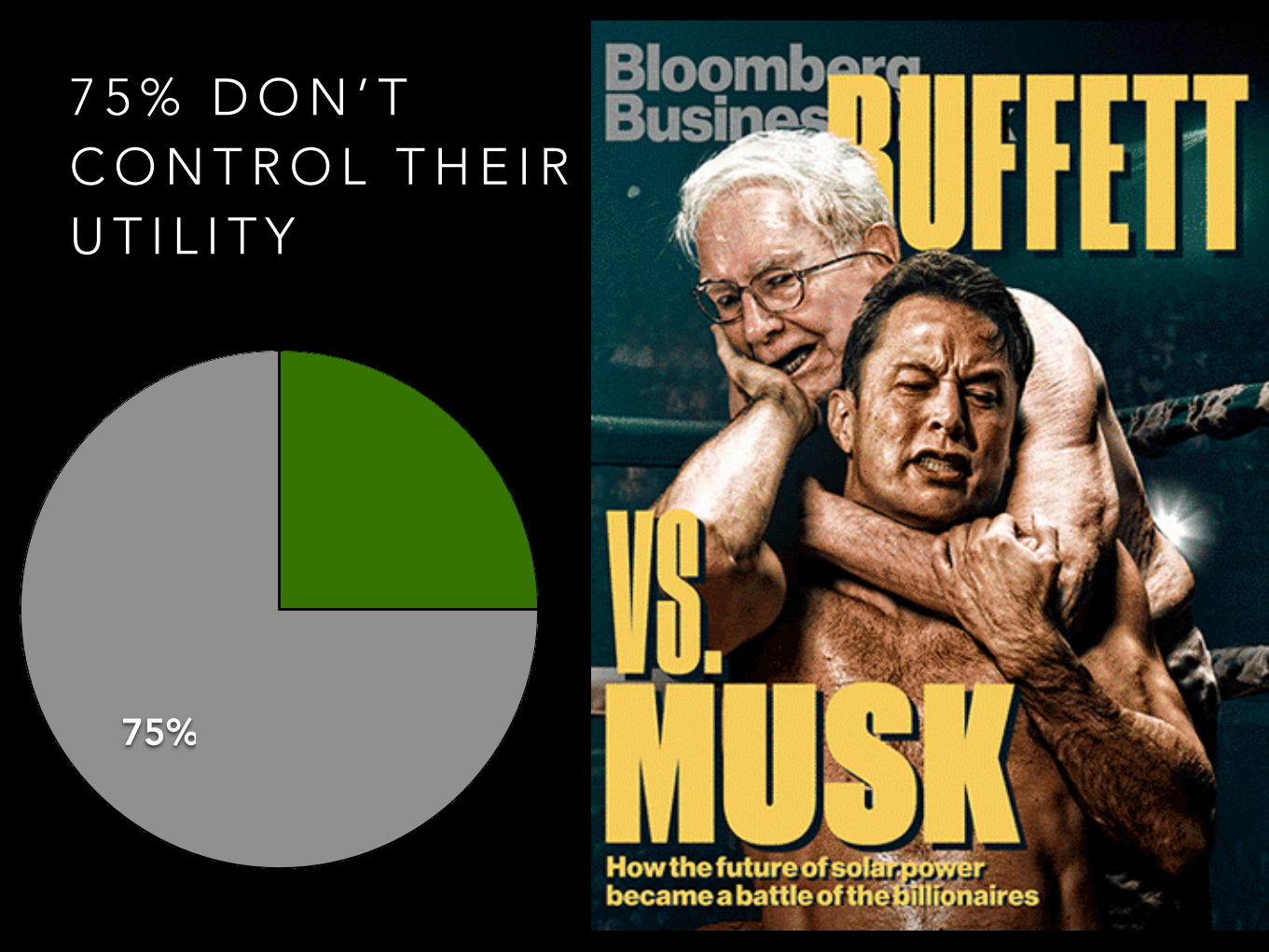

H O W D O W E C H A N G E ?

2 5 % C O N T R O L T H E I R U T I L I T Y

25%

Sacramento Municipal Utility District

Farmer’s Electric Cooperative

Georgetown Utility Systems

7 5 % D O N ’ T C O N T R O L T H E I R U T I L I T Y

75%

B - C O R P O R AT I O N

N E W Y O R K

T H A N K Y O U !@johnffarrell

www.ilsr.org

C H A N G I N G T H E R U L E S

P R O V I D I N G T O O L S

1 0 0 % R E N E WA B L E L O C A L E C O N O M Y

H U M A N S C A L E

L O C A L O W N E R S H I P

D E M O C R AT I C A U T H O R I T Y

I L L U S T R AT I N G T H E V I S I O N