the changing world of network rail simon kirby, managing director infrastructure projects

TRANSCRIPT

The changing world of Network Rail

Simon Kirby, Managing Director Infrastructure Projects

Rail remains a growth industry

Passenger Journeys Since 1999-00

800

900

1,000

1,100

1,200

1,300

1,400

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Year

No

of

Pas

sen

ger

s

Source: ORR, National Rail Trends, 2011

This compares to less than 10% for UK Air and Road over the same period

Record passenger numbers and reduced costs

Controllable OM&R costs vs passenger journeys

800

900

1,000

1,100

1,200

1,300

1,400

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

Jou

rney

s

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

Co

sts

£m

Passenger Journeys Costs

Source: ORR, National Rail Trends, 2011; and Network Rail, 2011

A fundamentally different company in 2012

• Devolved route business units aligned with our customers

• National Centre

• A separate projects business working in collaboration with our supply chain

Devolution - Getting closer to customers

• Increase our responsiveness

• Reduce industry costs

• Offer a seamless service from routes, with support from the centre

• Maintain network benefits

Train image

National Centre - Milton Keynes

A separate projects business working in collaboration with our supply chain

Our aims

• Achieve lower unit costs/ greater

innovation

• A more open project market

• Greater / earlier supply chain engagement

and partnering

• Improve workforce safety

• Increase customer focus

• Wider pipeline of work income

Steve FeatherstoneProgrammeDirectorTrack

Ian IcetonHead of HR

•SCO•NE•EGIP

•Anglia•Kent•Sussex•Wessex•Platform Ext

•LNW•East Mid•BGP•Kings Cross

•Crossrail•Reading•Western•Wales•Electrification

April 2012

Becomes a regionally-based projects delivery business

More closely aligned Network Rail's route teams, our main clients/customers

Overall aim is to safely deliver better value-for-money across all renewal and enhancement

infrastructure projects

Summer 2012

Pilot projects will examine the best way to open up our projects to competition and enable Network

Rail to further develop client capability

April 2013

IP becomes a subsidiary company of Network Rail able to forge new relationships with other (non-

Network Rail) clients

September 2013

As a subsidiary, IP will be able to bid alongside the market for NR project work

The IP Journey: April 2014 (CP5)

The first enhancement and renewal projects are contested in the open market in a consistent manner

Certain projects remain allocated to Network Rail IP

Innovation and value for money from all deliverers open to scrutiny by the industry and other stakeholders

creating a better cost benchmark

15

Collaborative working

Collaborative working - BS11000

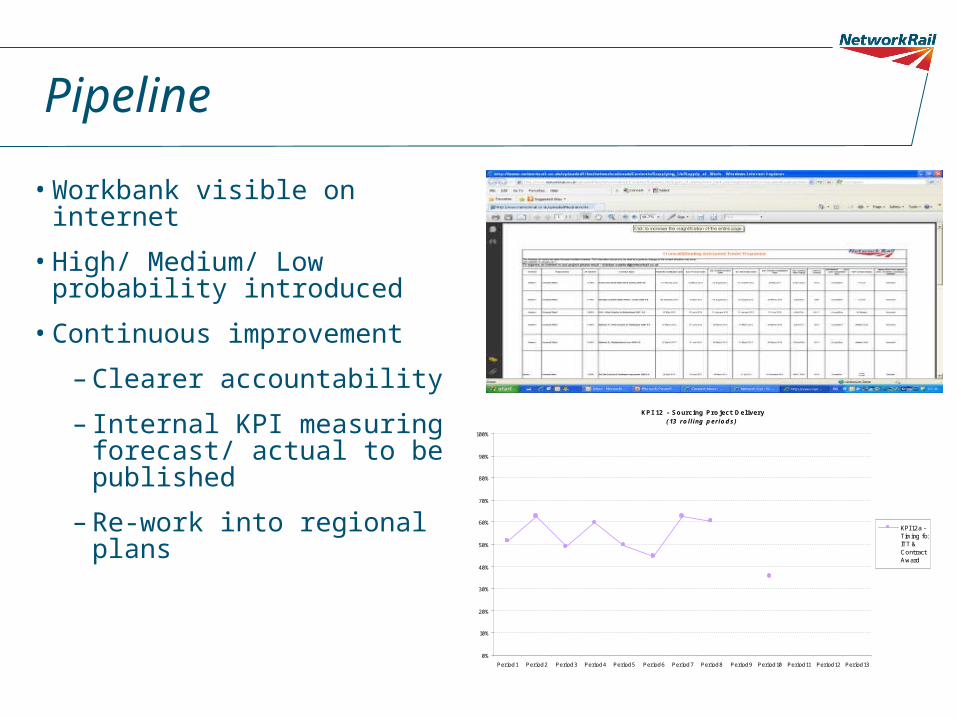

Pipeline

• Workbank visible on internet

• High/ Medium/ Low probability introduced

• Continuous improvement

– Clearer accountability

– Internal KPI measuring forecast/ actual to be published

– Re-work into regional plans

KPI 12 - Sourcing Project Delivery(13 rolling periods)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Period 1 Period 2 Period 3 Period 4 Period 5 Period 6 Period 7 Period 8 Period 9 Period 10 Period 11 Period 12 Period 13

KPI 12a -Timing forITT &ContractAward

Aligned objectives drive innovation

Westbury Lane

© Ipsos MORI

19

Overall satisfaction

* = No. of respondent answers. Base for 2010= 64 respondents, 2011 = 72 respondents, 2012 = 70 respondents. Mean score calculated from 1-5 where 1 = very dissatisfied and 5 = very satisfied

Mean score

3.81

3.11

3.60

Taking into account all of your experiences with Network Rail over the past 12 months as a whole, how satisfied or dissatisfied are you with Network Rail?

Satisfaction continues to improve; the proportion who are dissatisfied is now below the benchmark target of 15%

Date 00.00.00 Presentation title to go here 2020

Building on strong delivery

Project performance is on plan

200

250

300

350

400

450

500

550

Cum Act/F.c 265 310 342 364 381 407 419 430 452 478 496 543

Cum Baseline 242 304 338 363 379 403 417 423 436 481 498 543

Prior Pds Current Pd Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Future

Jan 09 - Q2 2012 2011/12 2012/13 2013/14 Years

Sep-11 - ---------------------------------------------- FORECAST TO GO (CP4) ---------------------------------------------------- CP5

New King’s Cross Western Concourse opened 18th March

King’s Cross

King’s Cross

Blackfriars – PV cells

Date 00.00.00 Presentation title to go here 31

Integrated Ticket Hall – Concourse

Key Output 1 achieved, 10th December 2011

Waverley - West side Glazing view from below

Good progress on FTN/GSM-R

90.4% Complete 2934 sites

GSM-R ConstructionFTN Construction

98.4% Complete14,591 Km

NW Cornor

Reading Station Area Redevelopment

Hitchin

Three Bridges ROC (Rail Operating Centre) in Sussex

Salisbury to Exeter old and new signalling

Simon Kirby, Managing Director Infrastructure Projects

The changing world of Network Rail