the capabilities and opportunities of non-timber forest...

TRANSCRIPT

The Capabilities and Opportunities of Non-Timber Forest Products

at Malcolm Knapp Research Forest

by

Katja Eisbrenner

Master Thesis

submitted to the Faculty of Forest Sciences & Forest Ecology Georg-August University Göttingen

Institute of Silviculture

Supervising Professors:

Dr. Burghard von Lüpke, Institute of Silviculture, Georg-August University Göttingen

Dr. Cindy Prescott, Department of Forest Science, University of British Columbia

Göttingen, February 2003

i

Table of Contents

Acknowledgments ........................................................................................ iii

1 Abstract................................................................................................... 0

2 Introduction............................................................................................ 0

2.1 OVERVIEW ................................................................................................... 0

2.2 LITERATURE REVIEW ................................................................................... 1

2.3 RATIONALE .................................................................................................. 2

2.4 DEFINITION OF NTFPS ................................................................................. 2

2.5 OVERVIEW OF THE NTFP INDUSTRY IN BRITISH COLUMBIA ........................ 3

2.6 OBJECTIVES & APPROACH ........................................................................... 4

3 Study Site ................................................................................................ 5

3.2 CLIMATE ...................................................................................................... 6

3.3 ECOLOGY ..................................................................................................... 7

4 Methods................................................................................................... 7

4.2 SCREENING .................................................................................................. 8

4.3 EVALUATION ............................................................................................... 9

4.4 RANKING ................................................................................................... 12

5 Results ................................................................................................... 15

5.1 SCREENING ................................................................................................ 15

5.2 EVALUATION ............................................................................................. 16

5.2.1 Floral Greens........................................................................................ 16

5.2.1.2 Christmas Trees and Greens ........................................................... 24

5.2.2 Landscaping Products .......................................................................... 27

5.2.3 Food Products....................................................................................... 32

5.2.3.1 Berries............................................................................................. 32

5.2.3.2 Syrup............................................................................................... 36

5.2.3.3 Cultivated Edible Mushrooms ........................................................ 38

ii

5.2.3.4 Wild Edible Mushrooms................................................................. 43

5.2.3.5 Trout ............................................................................................... 44

5.2.3.6 Wasabi ............................................................................................ 46

5.2.4 Craft Products....................................................................................... 47

5.2.5 Medicinals and Pharmaceuticals.......................................................... 50

5.2.5.1 Medicinal Plants ............................................................................. 50

5.2.5.2 Medicinal Mushrooms .................................................................... 56

5.2.6 Miscellaneous NTFPs ........................................................................... 57

5.2.6.1 Cedar Leaf Oil ................................................................................ 57

5.2.6.2 Firewood ......................................................................................... 62

5.2.6.3 Mushroom Logs.............................................................................. 63

5.2.7 Ecotourism ............................................................................................ 65

5.2.8 Summary of The NTFP evaluation........................................................ 66

5.3 RANKING ................................................................................................... 67

6 Final Discussion.................................................................................... 69

7 Recommendations for MKRF............................................................. 71

8 Conclusion ............................................................................................ 72

9 References............................................................................................. 73

10 Appendices

iii

Acknowledgments

This thesis could not have been written without the help of many people. I am deeply

thankful to Ionut Aron and Paul Lawson for giving me the chance to write this thesis at

Malcolm Knapp Research Forest and for their advice and support. I am grateful to my

supervisor Cindy Prescott at UBC for the encouragement and feedback that I received

through meetings and correspondence. I am thankful to Burghard von Lüpke, my

supervisor at Georg-August University in Göttingen, for making it possible to write the

thesis in co-operation with UBC. I am exceedingly grateful to Yona Sipos Randor for her

help with editing the thesis, and Robert Nuske for the many conversations which kept me

focused. I would like to thank Malcolm Knapp Research Forest staff for their assistance.

Thanks to all who provided information for this report.

0

1 Abstract

Non-Timber Forest Products (NTFPs) such as floral greens and wild mushrooms have

been harvested for over 80 years in British Columbia (BC), Canada. However, only

recently they have received much attention from scientists. Many questions involved with

NTFP management, such as sustainable harvesting or business development, have not

been answered yet. Therefore the Malcolm Knapp Research Forest (MKRF) started a

program to identify its capabilities and opportunities for NTFPs. The MKRF is part of the

University of British Columbia. It is located in the lower Mainland of British Columbia,

and covers over 5000 ha of private land in the Coastal Western Hemlock (CWH)

biogeoclimatic zone. This research was the first step in the process of developing a

strategic plan for implementing NTFPs at MKRF.

It was the objective of this study to identify the economic potential of NTFPs at

MKRF considering education, demonstration and research values. More than 50 NTFPs

with market potential were identified at MKRF through a screening process. For these

NTFPs, exploratory research was carried out to analyze their current market and forest

situation. This was followed by an evaluation to identify NTFPs the “best bets” for

MKRF. Seven NTFPs with market potential were identified and ranked using the

following criteria: Capital Investment, Production and Growing, Harvesting, Ecology,

Education and Research, and Market. After this second evaluation three NTFPs were

classified as “good” for MKRF. Those three are Christmas garlands and wreaths,

Christmas greens and Ecotourism.

2 Introduction

2.1 Overview

The UBC Malcolm Knapp Research Forest was established by a Crown Grant to the

University of British Columbia in 1949. It is located in Maple Ridge, BC and covers over

5000 ha of private land in the CWH Zone. The forest is managed with consideration of

economic aspects, as well as the integration of research, demonstration to the general

public and education. Over the past 10 years Non-Timber Forest Products have gained

more recognition in BC as important sources of foods, medicines, floral greens and

1

cultural histories. They provide job and income opportunities. For this reason, MKRF

became interested in identifying the capabilities and opportunities of NTFPs on site.

2.2 Literature Review

The majority of available literature on NTFPs in the Pacific Northwest1 has been

published in the last 10 years. The first papers were published by Schlosser and Blatner in

the early 1990s, and describe the economic and marketing possibilities of NTFPs with a

focus on floral greens (Schlosser et al., 1991; Schlosser et al., 1992; Blatner, 1995). With

increasing awareness of the economic potential of NTFPs in the Pacific Northwest, the

number of publications has consistently increased since the late 1990s. The publications

cover all NTFP related areas, including economic, social and ecological issues (Hansis,

1998; Pilz et al., 2001; Alexander et al., 2002a; Tedder et al., 2002). Currently, most of

the literature describes and evaluates the existing situation, and identifies further research

needs and unanswered questions. These include establishing guidelines for NTFP

business implementation, achieving economic potentials, and questions about sustainable

harvesting practices.

In 1995 de Geus published one of the first publications on NTFPs in BC. The

findings were that wild mushrooms, and floral greens are of high importance in the

industry (De Geus, 1995). In 1999, Wills and Lipsey analyzed economically valuable

NTFPs in BC and their related industries and designed a strategy for economic

development. One of the few case studies on NTFPs was done on the social and

economic potential in Haida Gwaii (Tedder et al., 2000). Since NTFPs in British

Columbia have just recently gained more attention, specific research into the field is

limited The available publications, however, do indicate economic potential of NTFPs.

A detailed literature review was conducted for each NTFP and is presented in the

results section.

1Oregon (US), Washington (US), British Columbia (Canada)

2

Definitions

2.3 Rationale

MKRF is a self sustained, managed forest interested in diversifying its income sources.

As well, since MKRF is part of UBC, part of its mandate is to provide a facility for

research, demonstration and education in the field of forestry. The combination of applied

research and the high economic potential of NTFPs fits well with MKRFs main

objectives and therefore, the management decided to develop a management and business

strategy for implementing NTFPs. This research project was initiated as the first step in

developing such a strategy at MKRF.

Benefits of NTFP at MKRF

• New income source

• Education and demonstration

• Applied research

2.4 Definition of NTFPs

In the existing literature, various terms are used to describe forest products other than

timber. The terms include: Non-Timber Forest Products, Non-Wood Forest Products,

Specialty Forest Products and Botanical Forest Products. To bring consistency to the

terminology, the Food and Agricultural Organization (FAO) has defined the term Non-

Timber Forest Products as “products from the forest other than timber and pulp including

small things made from wood and fuelwood” (FAO, 1999). This definition is in contrast

to the term Non-Wood Forest Products that excludes all woody material (FAO, 1999).

Regarding the origin of the product the FAO defines: “NTFPs should be derived from

forests and similar land uses”(FAO, 1999).

According to the FAO definition all products harvested from the forest or grown in

Agroforestry systems are considered NTFPs. However it remains unclear if the term

Economically viable means a self-sustainable NTFP business, which does not need any

additional money to operate

A NTFP has economic potential if it has a high chance to be economically viable

3

NTFP used in the Pacific Northwest is interpreted this way. This problem has been

addressed in the literature and several conferences but no agreement has been reached so

far (Davidson-Hunt et al., 1999; Teel and Buck, 2002).

In this thesis the following definition will be used.

Definition

Non-Timber Forest Products include a broad variety of different products types and a

classification within NTFPs by categories is inevitable. Currently, there is no

standardized system for classifying NTFPs and a variety of different systems are used in

the existing literature. For details on the classification system see Chapter 2.6..

2.5 Overview of the NTFP industry in British Columbia

Non-Timber Forest Products have a long history in British Columbia. First Nations

people have used them traditionally for centuries as e.g. food, clothing, medicine (Turner,

2001a). In the early 1900s, the first commercial use of NTFPs was in the floral green

industry (Blatner and Alexander, 1998). This industry, as well as the wild mushrooms

industry, are currently the most economically important NTFP industries in BC (De

Geus, 1995). “In 1997 the NTFP industry employed almost 32,000 people in BC on a

seasonal and full-time basis and produced direct corporate revenues of $280m and

provincial revenues in excess of $630m Cdn” (Wills and Lipsey, 1999). Concurrently, the

timber industry in BC has been declining and the unemployment rate in the forestry

sector increasing (Mitchell, 1998). Recently, the economic potential of NTFPs has

attracted the attention of unemployed forest workers and interested communities to

explore NTFPs as new business opportunities. Some recent NTFP activities in BC

include:

• North Vancouver Island NTFP Demonstration Project, developing a NTFP

strategy for the local community in cooperation with Royal Roads University.

• Centre for NTFPs, Royal Roads University (in development)

NTFPs include all non-timber plant products and associated industries from the forest.

Products harvested from different management systems such as wild-crafting and

Agroforestry are included under this definition.

4

• NTFP profiles for some BC forest districts (BC Ministry of Forests)

• Integration of NTFPs in forest management projects (Berch et al., 2000)

• Agroforestry strategic plan for BC (Agri-Food Canada and Future Funds)

The management of NTFPs involves several complicated issues. The majority (95%) of

the forestland in BC is Crown Land; a licensing system for timber harvesting and a forest

practice code assure good management practices. In contrast to timber harvesting, no

such licensing system exist for NTFPs. This lack of legislation results in problems

regarding the management of these resources and as such, overharvesting has been a

common problem e.g. cascara bark (Rhamnus purshiana) and yew bark (Taxus

brevifolia) (Turner, 2000). Harvesting regulations must address both the ecological

issues, as well as harvesting rights on public lands. First Nations traditionally use NTFPs

and commercial harvesting should not interfere with their rights.

2.6 Objectives & Approach

The process of developing a strategy for implementing NTFPs at MKRF consists of three

phases.

Phase I: Planning:

• Identify NTFPs with market potential in MKRF

Phase II: Implementation

• Develop detailed business plans for the selected NTFPs

Phase III: Evaluation

• Evaluate the operating business – economically, ecologically

Phase I, planning, is used to identify the economic potential of the NTFPs at MKRF. If

the planning phase provides promising results, detailed business plans will be written in

phase II and will be used to verify the results from phase I. If the business plans deliver

positive results, they will be implemented and evaluated in phase III.

This study covers the first phase in the three-step process of a NTFP strategy at

MKRF It is hoped that this report will provide a basis for further decision-making.

5

The objective of this study was to identify the economic potential of NTFPs at

MKRF, including educational, demonstration and research values, as these values are part

of MKRFs main objective. As part of the study, existing and potential NTFPs were

identified and different management systems, including Agroforestry, were considered.

The ideal NTFP for MKRF should have the following characteristics:

• Economically viable

• Ecologically sustainable

• Educational and research value

To fulfill the objectives, an approach was developed with the following steps:

SCREENING

Identify NTFPs with market potential in MKRF

EVALUATION

Verify the potential of screened NTFPs and identify possible NTFPs for MKRF

RANKING

Identify the most promising NTFPs.

3 Study Site

MKRF is located in Maple Ridge, British Columbia, Canada, 60 km east of downtown

Vancouver. MKRF is bordered on the northwest by Pitt Lake at sea level, on the north

and east by Golden Ears Provincial Park with elevations up to 1000m and on the south, it

meets with the urban areas of Maple Ridge. The forest itself is 5,157 hectares, with an

average width (from west to east) of 4 km and an average length (from north to south ) of

13 km, see maps Appendix XI-XIV. The forest is situated on private land, meaning that

the exclusive rights for harvesting and managing the forest belongs to MKRF. This

ownership eliminates the problem of access rights and licensing of NTFP harvests, a

concern that exists elsewhere in the province.

FIRST NATIONS

MKRF is part of the Traditional Territory of the Katzie First Nation Band. The

relationship between MKRF and the Katzie First Nation is very good. NTFPs as part of

their tradition might offer the opportunity for joint projects with MKRF. The Katzie band

6

traditionally uses NTFP for medicines and craft products, and they also have spiritual

significance. The use of NTFPs is also part of a traditional use study the Katzie band is

currently conducting. If this study identifies opportunities for new business development

based on NTFPs the Katzie band have mentioned their interest in developing a joint

venture project. Depending on the NTFP a joint venture could have different forms. This

could include the management of a cedar leaf oil still or the marketing of traditional

medicines.

BC HYDRO RIGHT OF WAY

There are 20 ha of BC Hydro Right of Ways (RoW) within MKRF. The RoW is the area

under the powerlines. This area cannot be forested due to safety regulations and is

brushed manually regularly by BC Hydro. It is owned by MKRF but BC Hydro

ultimately determines the land use of the area. Some areas are of particular interest

because the soils are good and they are easily accessible by roads (see map Appendix

XIV). The areas of interest are currently covered with small trees (alder, willow, birch,

cedar) that do not exceed 3 m in height. The different possibilities for the management of

RoWs for possible NTFPs are discussed in detail in Chapter 5.2.1..

LOON LAKE CAMP

Loon Lake Camp (LLC) is located on the shores of Loon Lake in MKRF. This campsite

has the capacity for 100 guests and is fully catered. The camp has a long tradition of

providing an area for forestry and environmental education as well as outdoor recreation

and is also available for conferences. LLC has a partnership with an outdoor adventure

company Pinnacle Pursuits, which specializes in outdoor education.

3.1 Climate

The CWH climate which characterizes MKRF is defined as “a maritime climate

characterized by mild temperatures with common cloudiness and a small range of

temperatures, wet and mild winters, cool and relatively dry summers, long frost-free

periods and a heavy precipitation most of which occurs during the winter season”

(Klinka, 1976). Annual precipitation ranges from 2200 mm per year at the southern end

of the forest to about 3000 mm per year at the north end. The higher elevation in the

7

north is covered by snow for about four month of the year where the lower elevation in

the south rarely receives snow.

In this climate the forests are dominated by coniferous ("evergreen") trees which are

typically large and fast growing. The common species in MKRF are Douglas-fir

(Pseudotsuga menziesii), western red cedar (Thuja plicata) and western hemlock (Tsuga

heterophylla).

3.2 Ecology

MKRF is entirely within the Coastal Western Hemlock (CWH) biogeoclimatic zone, with

the lower half of the forest in the dry maritime (dm) subzone, and the upper half in the

very wet maritime (vm) subzone. The different zones can be seen in map Appendix XIV.

The Forest currently consists of a few separate age classes. On the older end of the

range, some small patches of 400-year+ old-growth forest remain intact. About half of

the western side of the forest represents 120-year-old stands made up of a mixture of

Douglas-fir, western red cedar and western hemlock. This is due to a large fire in 1868,

which swept through that area of the forest. The eastern half of the forest is covered

mostly by 70-year-old stands. These areas contain mostly western hemlock and western

red cedar and were established through a fire 1931. The major of understory species

found in MKRF include salal (Gaultheria shallon), red huckleberry (Vaccinium ovatum),

Oregon grape (Mahonia aquifolium), vine maple (Acer circinatum), bracken fern

(Blechnum spicant), sword fern (Polystichum munitum), Alaskan blueberry, step moss

(Hylocomium splendens), beaked moss (Kindbergia oregana), lanky moss

(Rhytidiadelphus loreus), and Plagiothecium undulatum (Green and Klinka, 1994).

4 Methods

This chapter describes the approach and methods used to fulfill the objective: Identify the

economic potential of NTFPs at MKRF, including educational, demonstration and

research values. The steps explained in detail in the following subchapters were

undertaken in this study.

SCREENING

Identify NTFPs with market potential in MKRF

8

1. Identify NTFPs with market potential in BC (literature review, Internet research)

2. Verify if NTFPs identified in step 1 currently or potentially could exist in MKRF

3. Develop a classification system with NTFP categories

4. Assign relevant NTFPs to categories

EVALUATION

Identify possible NTFPs for MKRF and verify their potential

1) Review literature

2) Explore markets

3) Assess forest for production possibilities

4) Evaluate the results for each NTFP

5) Identify the limitations at MKRF for each NTFP

6) Make recommendations

RANKING

Identify most promising NTFP

1. Ranking of the recognized NTFPs with market potential

In the following section, the methods used for screening, evaluating and ranking are

explained. The results are presented and justified.

4.1 Screening

NTFPs may be valued culturally, ecologically and economically. Currently, only a small

number of NTFPs have recognized economic value. Therefore, the first step was to

identify those NTFPs with economic value produced in the Pacific Northwest. This part

of the screening process was accomplished using data from a literature review and

information from the Internet.

To get a better overview of the NTFPs they were put into categories. NTFP

categories can be based on their product source (e.g. mushrooms including medicinal and

edible mushrooms), or on their end product use (e.g. food products including berries,

edible mushrooms). Currently there is no standardized categorization system for NTFPs

and as such, it is difficult to compare existing NTFP studies (Chamberlain et al., 1998;

von Hagen and Fight, 1999; Wills and Lipsey, 1999; Berch et al., 2000; Petten, 2001). To

9

maintain consistency it was considered to use a system, which has been used in several

recent BC publications (Berch et al., 2000; The North Island NTFP Demonstration

Project, 2001) and was developed in the Report on Botanical Forest Products in BC de

Geus (1995). Unfortunately, de Geus’ system did not meet the needs of this study

because the categories are based on end products and sources. This study, however is

focused on the economic potential of NTFPs, which means the final marketable product

is important. Therefore a system only including end products was developed.

According to this categorization system, each previously recognized NTFPs with

market potential was assigned to one or multiple categories.

After this list was completed, it was compared with the database on existing plants

species in MKRF. In addition MKRF staff was interviewed to find out about the fungi.

For species that do not currently exist in MKRF, a literature review was conducted to

ascertain their growth potential under managed conditions (e.g. Agroforestry).

4.2 Evaluation

The pre-requisite for the production of a certain NTFP is market demand. In case the

production capabilities of MKRF match the market demand the NTFP has economic

potential. To verify the economic potential of the NTFPs identified through the screening

process, further research was carried out. This research included an assessment of the

current market and forest conditions. No previous research on NTFPs had been

conducted at MKRF. Therefore exploratory2 research was used for the primary data

collection.

MARKET

The market situation for each NTFP is unique and depends on numerous conditions

within the NTFP categories. Although each category pertains to a different industry, the

2 The characteristics of exploratory research are that the data is gathered using less structured

instruments and interviews questions can be open ended. The sample size can be small and the results are

qualitative. Exploratory research can provide significantly insight into given situations. The advantage is

that the research can be adapted to the findings and is more flexible. A disadvantage is that the research is

subjective and qualitative (Zikmund, 2000).

10

keywords describing the market conditions are the same for the different NTFP industries

and were described by the following:

• Demand

• Amount demanded

• Quality

• Price

• Form (Processed/Unprocessed)

• Future expectations

• Legislative regulations

Based on these keywords, the primary data was collected for each NTFP category with a

focus on the individual NTFPs as well other important information with influence on the

economic potential of the NTFPs was assessed.

The information was collected through in-depth interviews, in person, by phone or

via e-mail, with market players (wholesalers, retailers), researchers, producers and

consumers. Sampling methods were based on non-probability sampling such as

judgment, including snowball design and quota, as well as a focus meeting (Churchill,

1992). The characteristics of non-probability sampling are that personal judgment is

involved in the selection process of the data source and the accuracy of the results cannot

be gauged. Judgment sampling involved the selection of participants according to their

specific expertise on the subject. This is called the snowball method when other members

of the target group are identified through recommendations by other respondents (Dillon

et al., 1994). Quota sampling involved selecting a specific number of respondents who

possess certain characteristics important for the research.

The form of the interviews and e-mail communication was kept flexible in order to

adjust to each situation and gain as much information as possible for the specific NTFP

and associated categories. The interviews with the market players were designed to elicit

information regarding the current marketing situation of the NTFP according to the

keywords described above. Researchers were interviewed on different topics depending

on their specialization with NTFPs for example NTFP management, inventory, and

11

ethnobotany. Buyers were contacted using the phonebook, literature, Internet and

personal communication.

Secondary research included information gathered from a variety of sources

including: the Internet, journal articles, existing databases of MKRF, library sources,

Ministry of Forests Canada and USDA Forest Service.

FOREST

The main determinants for the question of whether or not the forest condition for a NTFP

is good are: abundance, sustainability and quality. Although the market and forest

situation were was analyzed separately, the forest data collection depended on the results

of the market research for certain questions, such as quality.

No direct information on the abundance of non-tree species at MKRF was available.

Therefore the abundance of such NTFPs was predicted using alternate sources, such as

biogeoclimatic zone maps. Some of the NTFP species are indicator species for the

biogeoclimatic zones and estimates were possible. In addition, the inventory results from

the North Vancouver Island Project were used. Since the research sites are in the same

zone, it was possible to estimate the quantities based on this information. Personal

communication in the form of interviews with MKRF staff was also used to collect

information on abundance levels. Some of the staff have been working at MKRF for over

25 years and know the forest very well, so they were an important source of information.

Although these methods do not give quantitative information, they are detailed

enough to identify the business potential of the NTFPs. The details are discussed

independently for each NTFP, which are differentiated into 6 categories:

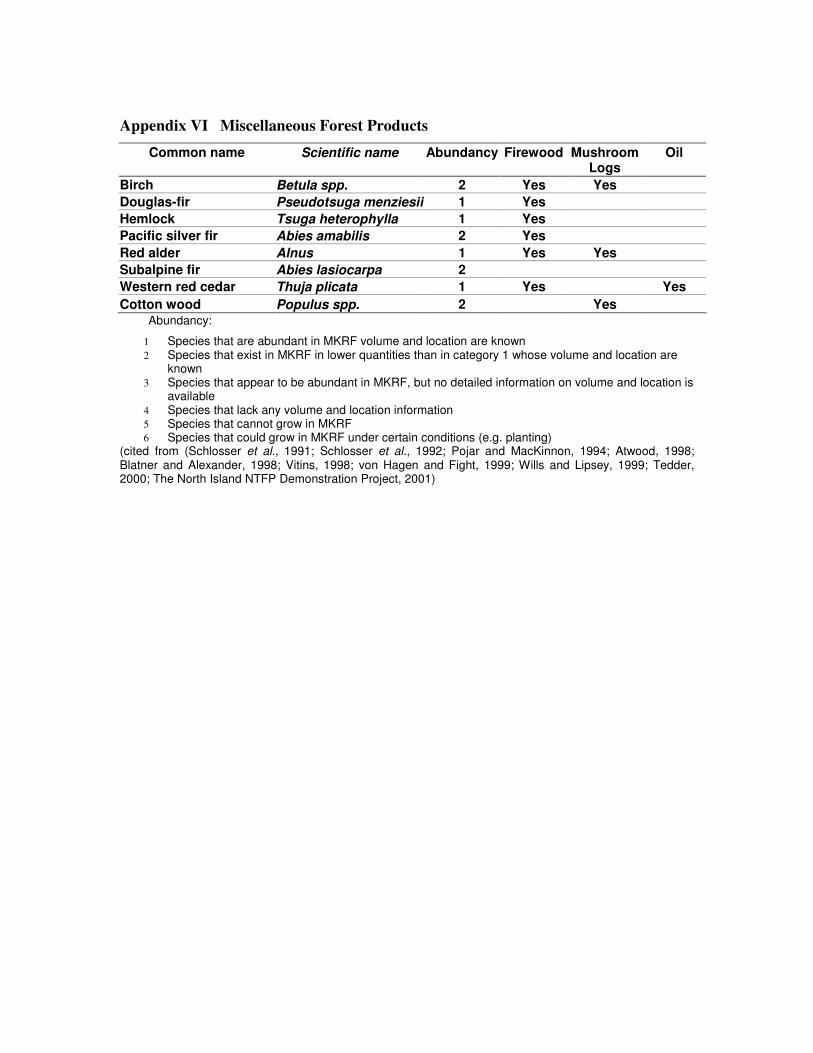

1 Species that are abundant in MKRF volume and location are known

2 Species that exist in MKRF in lower quantities than in category 1 whose

volume and location are known

3 Species that appear to be abundant in the RF, but no detailed information

on volume and location is available

4 Species that lack any volume and location information

5 Species that cannot grow in the RF

6 Species that could grow in MKRF under certain conditions (e.g. planting)

12

To identify whether or not there are sustainability concerns with harvesting of individual

NTFPs information from the literature and Internet, as well as personal communication

was used. In addition to the market and forest condition the educational; research and

demonstration values of the NTFPs were identified. Once the pertinent information was

collected, it was possible to evaluate the NTFPs according to their economic potential,

research, education and demonstration values. In the evaluation the following questions

were addressed:

• Is the market information from the literature review in accord with current

research findings?

• Are there any limitations for the NTFP at MKRF?

• Do production possibilities of MKRF meet market demand?

• Was it possible to answer all the questions posed in the interviews, which are

necessary to identify the economic potential?

• Were problems identified? If yes, what were they?

• What other relevant information was uncovered?

From the results of the evaluation, a list of the limitations and possibilities for each NTFP

was developed. From this list the NTFPs with greatest potential for MKRF were

identified. The NTFPs were then ranked in order to identify the NTFP that best met the

objectives of MKRF.

4.3 Ranking

To identify the best NTFPs from the previously selected NTFPs they were compared and

ranked according to six criteria important for a NTFP business. The criteria included:

Capital Investment, Production and Growing, Harvesting, Ecology, Education and

Research, and Market Situation. To describe the criteria 25 indicators were used. A

detailed description of the indicators can be seen in Appendix IX. The NTFPs were

evaluated according to a system of points ranging from 1 (indicator fulfilled) to 5

(indicator not fulfilled) for each indicator. The more points assigned to a NTFP, the better

its potential at MKRF. The points were summed and the NTFPs ranked for each criterion

individually and for the criteria as a whole.

13

To evaluate the NTFPs according to different objectives the criteria were weighted in

different scenarios. The Equation 1 was used to weight the criteria.

ii

ii w

nm

p *= (Equation 1)

Where:

ip : weighed proportion

im : points gained

in : points possible

iw : weighing factor ( 11

=�=

k

iiw where k is # of categories)

According to the points gained the results were classified as follow:

Diagnosis Percentage of points gained

Very Poor 0 – 25%

Poor 25% - 50%

Satisfactory 50% - 75%

Good 75% - 100%

Table 1: Classification of NTFPs according to percentage

The first scenario was based on the objective to rank the previously-selected NTFPs

according to their economic potential at MKRF.

14

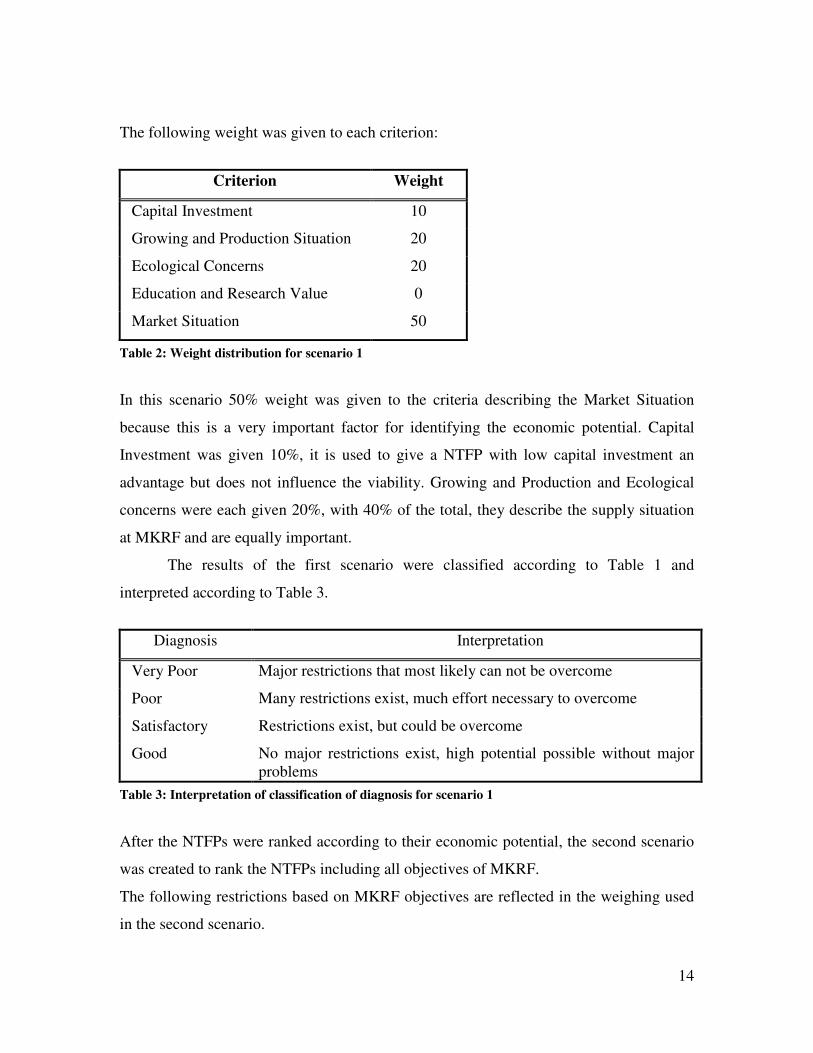

The following weight was given to each criterion:

Criterion Weight

Capital Investment 10

Growing and Production Situation 20

Ecological Concerns 20

Education and Research Value 0

Market Situation 50

Table 2: Weight distribution for scenario 1

In this scenario 50% weight was given to the criteria describing the Market Situation

because this is a very important factor for identifying the economic potential. Capital

Investment was given 10%, it is used to give a NTFP with low capital investment an

advantage but does not influence the viability. Growing and Production and Ecological

concerns were each given 20%, with 40% of the total, they describe the supply situation

at MKRF and are equally important.

The results of the first scenario were classified according to Table 1 and

interpreted according to Table 3.

Diagnosis Interpretation

Very Poor Major restrictions that most likely can not be overcome

Poor Many restrictions exist, much effort necessary to overcome

Satisfactory Restrictions exist, but could be overcome

Good No major restrictions exist, high potential possible without major problems

Table 3: Interpretation of classification of diagnosis for scenario 1

After the NTFPs were ranked according to their economic potential, the second scenario

was created to rank the NTFPs including all objectives of MKRF.

The following restrictions based on MKRF objectives are reflected in the weighing used

in the second scenario.

15

• Economically viable

• Ecologically sustainable

• Educational and research value

This amount weight was given to each of the criteria:

Criterion Weight

Capital Investment 10

Growing and Production Situation 20

Ecological Concerns 20

Education and Research Value 20

Market Situation 30

Table 4: Weight distribution for scenario 2

Capital Investment, Growing and Production and the Market Situation were assigned a

total of 60% of the weight. Education and Research, and Ecological Concerns were each

allocated 20% of the weight. In this way the objectives are represented.

The result presents information on how well the criteria were fulfilled. Since the

weight is based on the objectives it also describes how well the objectives were fulfilled.

Given that economic viability is the main objective, the first scenario has more

importance than the second scenario. The final decision will therefore be based on the

first scenario. The second scenario is important in the case where the first scenario

showed all NTFPs have similar economic potentials. In this case, the second scenario will

provide additional information to decide which NTFP is best for MKRF.

5 Results

The results are presented according to the stages described before Screening, Evaluation

and Ranking.

5.1 Screening

Through the literature review seventy-four NTFP species with economic value were

identified. Out of these seventy-four NTFPs species sixty-six exist or have growth

16

potential in MKRF. The NTFPs were assigned to seven categories, Floral Greens,

Landscaping Products, Food Products, Craft Products, Medicinals, Miscellaneous Forest

Products, and Ecotourism. For a description of how the NTFPs were assigned to the

categories see Appendix I–VI.

5.2 Evaluation

The results of the literature, market and forest research are presented for each NTFP

category with a focus on the specific NTFPs in the following subchapters. The

assessments of species abundance is included in Apendix I - VI, as well as in the

individual NTFP chapter.

5.2.1 Floral Greens

Wild-crafted floral greens are one of the products with an established market in the NTFP

sector in BC since the early 1900’s (Blatner and Alexander, 1998). The major species in

the 1920s remain today salal, evergreen huckleberry, western red cedar, Oregon grape,

and sword fern (Weigand, 2002). Although commercial harvesting of floral greens was

established in the early 1900s (Blatner and Alexander, 1998), the first evaluation of its

economic role was done by Schlosser et al. in (1991). As of 1991 the floral greens

industry employed over 10,000 people in Washington, Oregon and southern British

Columbia and generated an estimated $128.5 US million in sales (Schlosser et al., 1991).

For a detailed list of plants used as floral greens see Appendix I.

An estimated $47.7 million US was paid for plant materials used as floral greens

from NTFPs in 1989, with beargrass (Xerophyllum tenax)� and salal being the most

important species in producer expenditures (Schlosser et al., 1991). At that time,

beargrass was a new product on the market and like salal was exported to Europe. Of the

floral greens in the industry 17% were marketed locally (in the coastal Pacific

Northwest), 52% in the United States, and 31% were exported mostly to Europe. The

industry for floral greens has been rising over the past several decades primarily due to

the development of new products in the floral greens industry. Schlosser et al. (1991) also

indicate that markets in Europe and Pacific Rim have a high potential for future

development. In a more recent study Blatner and Alexander (1998) did not conclude on

the trends for the NTFP industry due to insufficient available data. The difficulty in

17

obtaining data lays part in the entrepreneurial character of the industry, with companies

entering and leaving frequently (Alexander et al., 2002b). Due to this problem other ways

were used to estimate the economic potential of the NTFP part of the industry.

Chamberlain et al. (1998) used the floriculture industry; which had 5 percent annual

growth between 1989 and 1996. Mater (1997) sees an indication for increase in demand

for NTFP floral greens in the numbers presented by the Bureau of Land Management

(BLM) in Washington: “Bough sales increased 143 percent from about 0.51 million

pounds in 1993 to more than 1.24 million pounds in 1995. Moss sales increased almost

660 percent from 27,000 pounds in 1993 to 205,000 pounds in 1995. For evergreens, like

salal and Oregon grape sales increased from 16,000 pounds in 1993 to 89,000 pounds in

1995” (Mater, 1997).

The scarcity of available data also makes it difficult to identify which forces are

responsible for changes in price and market demand (Blatner and Alexander, 1998). The

results of Blatner and Alexander (1998) show that prices for floral greens were variable

over the observed years 1989 to 1996. The prices paid for NTFPs in the Pacific

Northwest are influenced by a number of factors: domestic supply influenced by weather

and management objectives; competing product development elsewhere in the world and

rapid change in tastes and preferences in the floral design industry. In comparison with

the floral greens industry the Christmas greens market is more stable. This is because

Christmas greens are used based on a tradition and do not change as quickly as the floral

greens which are based on consumer taste. De Geus (1995) developed a summary of the

floral greens products harvested in British Columbia. The most important species are in

accordance with Schlosser et al. findings (1991). Although the report is specific to BC,

Schlosser et al. (1991) is referenced for industry data, even though their numbers are for

the entire Pacific Northwest.

The most recent overview of the industry that is most specific to BC was compiled

by Wills and Lipsey (1999). They identified 22 BC businesses in the floral greens

industry with collective gross revenues in 1997 between $55 and $60 million Cdn. The

total number of commercial pickers in BC in 1997 was estimated at 12,000 to 15,000.

salal was by far the number one in floral greens products, accounting for 75-80% of the

sales (Wills and Lipsey, 1999).

18

Although the literature indicates a market potential for floral greens harvested from

the forest it is difficult to draw conclusions on the current situation for new business

development.

In an attempt to estimate the current market situation 14 local wholesalers and

retailers were interviewed by phone and in person to get up-to-date market information

on wild-crafted floral greens. Since ferns, salal and mosses are the major species growing

in MKRF that are used for floral greens, these species were prioritized.

The following information was collected:

• Other than salal there is low market demand for the classic wild-crafted floral

greens

• Most salal is harvested from Vancouver Island and counts for 75%-80% of the

wild-crafted floral greens

• Other wild-crafted plants such as those included in Appendix I account for a very

small demand that is covered by current suppliers

• Sword fern is considered an out-dated item

• Supply from current pickers is more than sufficient

• No change in the market demand is predicted in the near future

• Positive prospects exist for the development of a new product that is nice looking

and not bulky

• An oversupply exists on the market for wild-crafted floral greens

• Market demand for products changes rapidly, depending on consumer taste

• Pickers indicated a demand for moss, but no buyer indicated interest.

One of the major floral brokers in the lower mainland is the United Flower Growers

Auction in Burnaby. In an interview, Cheu Oui Lam from their quality control

department said that the demand is quite low at the moment and the supply is more than

sufficient, bordering on oversupply. She does not see the demand increasing in the near

future and as such there is very little chance that MKRF would be accepted as a casual

shipper to the Auction (C. Lam personal communication). Richard Ross from Western

Evergreen on Vancouver Island sees the situation similarly. He also said that the quality

of salal in MKRF could not compete with the salal from Vancouver Island. Sword fern is

19

not in high demand; out of 100 cases of floral green shipped to Europe, only 5 are sword

fern. This is due to the short shelf life of sword fern and because it is an out-dated

product. Beargrass, which was one of the best sellers in the Schlosser et al. (1991) report,

has decreased in demand and can be purchased from the United States for $0,20 US per

bunch. It would be very difficult for MKRF to compete with this price according to R.

Ross. He also mentioned that the floral greens market is very much dependant on the

tastes and demands of the consumers.

A positive aspect of this consumer drive is that the market can be very open for new

items that can be used in floral arrangements such as curly willow (Salix matsudana var.

tortuosa), and eucalyptus (Eucalyptus globolus). “As long as something looks ‘neat’ is

not bulky and can be added to a bouquet without filling it, anything could be sold to the

floral greenery market. The key to this market is finding something interesting and

marketing” (R. Ross, personal communication). Ernie Meyer from Meyer Floral, another

wholesaler in Vancouver, mentioned in an interview that the market for cut flowers has a

high demand, which local producers cannot currently meet. The future development is

prognosed as very promising. Examples of flowers which could be grown in the forest

are Rhododendron spp. and Hydrangea paniculata, which are sold for $2 - $4 Cdn per

flower wholesale. E. Meyer indicated interest in buying those products.

Although the demand on the market for the forest floral greens is currently quite low,

information was collected on species being marketed. The situation of the forest could

thus be assessed in case the market changes, which is typical for this industry. The forest

species sold at the Burnaby Flower Auction include: Scotch-broom, deer fern, sword

fern, moss, salal, huckleberry, and Oregon grape. The prices achieved for these products

can be seen in Table 5. Salal was top product followed by mosses and Christmas greens.

The lowest sales were for deer fern and Oregon grape. Mosses achieves the highest price

with $3.20 Cdn per bag followed by salal and huckleberry. The greens with the lowest

prices were ferns and Oregon grape. There is a low demand for each of these products at

the Flower Auction. The current suppliers cover the demand for the floral greens and

chances that MKRF would be accepted as a supplier are low. However, when pickers

were interviewed they indicated a high demand for moss and Salal.

20

The major quality requirement for all floral greens is that the plant part has to be free

of imperfections. In addition to this, there are specific quality requirements for each

species.

• Sword fern and deer fern: Each frond must be deep green with few or no

spores, with each frond being between 25 and 40 cm long for sword fern;

being between 15 and 25 cm long for deer fern (see Picture 2) (C. Lam,

personal communication).

• Salal: The quality of plants grown in partial shade provides the best quality

with longer, cleaner branches and fewer blemishes. The branches must have a

minimum of 4 current-year leaves with all older leaves removed. The leaves

must be perfect and free from blemishes, fungus or insect bites. salal is

picked at two different lengths: regular, 28-30 inches and a tip, 20-24 inches

long (see Picture 1) (Cocksedge, 2002).

• Moss: Species in highest demand is lanky moss (Rhytidiadelphus loreus) but

other species can be used as well if they fulfill the requirements. Moss should

be in form of a uniform blanket with good green colouring and is kept and

sold wet for the use in the floral industry. The moss species include: step

moss (Hylocomium splendens), beaked moss (Kindbergia spp), running club

moss (Lycopodium clavatum), and peat moss (Sphagnum spp) (Cocksedge,

2002).

21

Picture 1: Salal, good quality Picture 2: Sword fern, good quality

Source: (Katja Eisbrenner, United Flower Growers Auction)

Species Quantity sold Unit Price per unit $ Cdn

Christmas greens 3069 bunch 1.70

Deer Fern 1650 bunch 0.57

Door Swag 25 unit 5.78

Moss 9314 bag 3.95

Oregon grape 314 stem 0.58

Salal 32817 bunch 2.16

Scotch broom 8974 bunch 1.13

Sphagnum 1400 bag 3.2

Sphagnum dried 40 bag 3.2

Sword Fern 5120 bunch 0.88

Vaccinium spp. 5526 bunch 2.50

Western red cedar 3300 bunch 1.14

Table 5: Average quantities in units, and prices for floral greens sold at the United Flower Growers

Auction between January and December 2001

Source: (United Flower Growers Auction, 2001)

22

FLORAL GREENS AT MKRF

Of the plants used in the floral green industry sword fern, deer fern, maidenhair fern

(Adiantum pedatum), moss spp., Oregon grape, salal, Scotch broom, huckleberry, lanky

moss, step moss and beaked moss are abundant in MKRF. Most of these species are

major understory species in the CWH biogeoclimatic zone.

Current knowledge of the abundance of floral greens can be found in Appendix I.

Sword fern is by far the most abundant species and meets the quality standards of the

industry. The other ferns meet the quality criteria but are not as abundant as sword fern in

MKRF. Although salal is most abundant understory plant in MKRF the quality does not

meet the industry requirements. The majority of the leaves have brown spots, the stems

are too short and the color is not consistent. This problem exists almost everywhere in

MKRF and is probably due to the distance from the coast and the situation of MKRF at

the edge of salal’s ecological range. Mosses are widely abundant and in good quality at

MKRF. One of the interviewed pickers said that MKRF is in one of the best moss

growing areas in BC.

Little information on the sustainability of harvesting floral greens is available. The

definition of sustainable depends on: amount harvested, harvest area, abundance, and

plant species.

From what is known ecologically there are no harvesting concerns at MKRF for fern

fronds. At MKRF they are widely abundant and only the fronds are harvested, which are

annual. For shrub species there are also no ecological concerns, because only part of the

branches are harvested. With the exception for red huckleberry, the plant species do not

have very many branches and grow slow; thus frequent harvesting might cause damage to

the plant. Scotch broom is an exotic and not wanted in MKRF anyway, therefore no

concerns exist. The only major existing concern pertains to harvesting mosses. Mosses

are habitat specific, slow growing and strongly affect the micro-sites and the soil-

moisture content. Moss communities contain a high number of infrequent species; by

large-scale harvesting these rare species could get lost (Atwood, 1998). Since very little

information on the sustainable harvesting of moss is availabe it should only be done in

small patches (Cocksedge, 2002).

23

EVALUATION

The findings from the interviews and the prices of the United Flower Growers Auction

indicate that the current conditions for floral greens vary depending on the product. The

current conditions of the market and MKRF do not provide a good starting point for

development of floral greens at MKRF. This is due the low demand for classical greens

including sword fern, the major floral greens species at MKRF. In addition the current

suppliers cover the demand for the other floral greens. The major sales item in the floral

green industry is salal, but although salal is the most abundant understory species it does

not meet the quality requirements. Of the existing floral green NTFPs, mosses are the

only product of interest for MKRF, because it has high market demand, it meets the

quality requirements and it is abundant in MKRF. However, there are uncertainties as to

ecological effects of wild-crafting moss in the forest. In the literature, moss harvesting is

recommended without concerns in areas prior to further development such as road

building. However, under consideration of the following criteria, moss harvesting might

be an option: harvesting in small patches or strips over large areas and monitored trials

prior to intensive harvesting, management of certain areas instead of wild-crafting.

Although the education and demonstration value are not outstanding, the research value

for moss harvesting is high.

Other than harvesting floral greens from already existing sources in MKRF, there is

the possibility for new product development. The market for floral greens is open to new

products and there are some flowers that grow in a forest setting. For example,

Rhododendron could be raised from cuttings and planted the following year in the forest

or under RoW. After two or three years the plants would start to flower. From the market

research, local demand has been identified and because of the relatively low capital input

and management this would be an option for MKRF. The price they can be sold for are

high and there are no sustainability concerns.

RECOMMENDATION

Of the existing floral greens only, moss harvesting is an option under consideration of the

ecological concerns. New product development of forest-grown flowers should be further

investigated.

24

5.2.1.1 Christmas Trees and Greens

The Christmas tree industry yielded $60 Cdn million in 1998 (Chamberlain et al., 1998).

However, the market for Christmas trees has been fluctuating over the years in part due to

the low prices of trees grown in US plantations (R. Hallman, personal communication).

US imports flood the market and the demand for BC-grown trees slows. The major

species used as Christmas trees in the Pacific Northwest are Douglas-fir (Pseudotsuga

menziesii 50%, followed by noble fir (Abies procera) (40%), grand fir (Abies grandis)

(7%), pine & others (3%) (Rinehold, 1999). The quality requirements are: uniformly

dark, green coloured, evenly layered branches, and a cone shaped form (R. Hallman,

personal communication). However, the requirements vary, depending on the traditional

use of the tree. For example, people with German background, prefer trees with wide

gaps between the branch layers because real candles are traditionally used to decorate the

trees.

Besides Christmas trees, there is a seasonal market for boughs, Christmas garlands

and wreaths from various conifers. Noble fir and western red cedar are the most

important, and subalpine fir, western white pine and Douglas-fir amongst those of lesser

importance (for details see Appendix I) (E. Meyer personal communication). The market

for Christmas greens is more stable than the floral greens market due to traditional use

(Schlosser et al., 1991), with the main harvesting time between October and November.

There is interest on the Vancouver market especially for cedar boughs, wreaths and

garlands. In addition to cedar, noble fir is a highly demanded item that is not yet covered

by suppliers (E. Meyer, personal communication). Because of the traditional market for

Christmas greens and a demand for good quality products the future prognosis is positive.

Depending on the quality the wholesalers Meyers Floral, Abbotsford Cold Storage,

Betty's Best and West Coast Floral buy Christmas greens from different conifers with

cedar as the main item.

The quality requirements for Christmas greens are similar to the floral greens. The

boughs have to be free of imperfections, evenly branched and uniformly coloured without

any brown spots from e.g. rust. They are sold in 3 lb bunches with each bough 22”- 28”

long. Prices paid per bundle are around $1.30 Cdn wholesale per bunch (E. Meyer

personal communication). There is a large opportunity for a value-added product.

25

Christmas wreath and garlands achieve retail prices of $30 Cdn for cedar 18” garlands

and wreaths (Holiday Season Farms, 2002). Basic machines to produce garlands and

boughs can be bought for $90 US; the price for an industrial machine is around $1600 US

(Kelco Industries, 2002). The other advantage is that to produce boughs smaller branches

of only 5” are used. It is therefore easier to meet the quality requirements and even if the

quality for boughs cannot be met the material can be used for garlands and wreathss. The

skills necessary to produce garlands are not very sophisticated and can be easily learned.

CHRISTMAS TREES AND GREENS AT MKRF

In previous years the Forestry Undergraduate Society had grown Christmas trees in

MKRF. However this attempt at marketing was not competitive, due to a higher price and

lower quality, and the plantation was abandoned. A Christmas tree plantation has to be

well maintained in order to meet market requirements. This upkeep includes regular

trimming and spacing of the trees as well as disease control. Different rusts and Swiss

needle cast (Phaeocryptopus gäumanniii) are pests, presenting a high risk for Christmas

tree plantations (Worrall, 2003). Because of the high industry standards, which trees from

forest stands hardly meet, an unmanaged Christmas tree plantation is not an option.

Currently there are no Christmas tree plantations in MKRF.

Of the species used for Christmas greens, western red cedar is the only one abundant

enough at MKRF for Christmas green production. As one of the three most abundant

species in MKRF the supply is guaranteed. In order to meet the quality requirements it is

important to select the stand carefully so the material harvested meets the standard and

the waste is small. There are old railway tracks going through MKRF with free-growing

cedars at the sides. The trees are logged to keep the track clear. This situation presents an

ideal opportunity to gather boughs for Christmas greens because the quality of the boughs

is high because they are grown in the open. Christmas greens can be harvested in

different ways, in larger operations where the trees are grown in a plantation sheering

machines are used to cut the branches, which are congruently collected in a pick-up truck.

In smaller operations pruning tools are used to manually harvest the branches from

standing trees (Landgren and Freed, 1998). The branches are collected and transported to

the processing site. This latter type of harvesting would be a possible practice for MKRF.

Another possibility is to harvest the branches from trees in a logging or thinning

26

operation. In the latter case two concerns must be addressed. The harvesting for the

Christmas greens is seasonal from October to November, so exact planning is necessary

in order to pick the branches fresh. It is doubtful that logged tree branches can meet the

quality requirements because October and November part of the rainy season and the

branches are wet and muddy. However this would have to be verified in a trial.

The seasonality of the product makes Christmas greens a feasible product for a small

business. It could be run by a third party in MKRF who would pay a share of their sales

to MKRF. The MKRF is an excellent site due to: the easy access to the sites; the short

distance to the market in Vancouver; and the facilities, which include a cooler, that could

be used to store the harvested Christmas greens. The raw material, boughs bring in a

lower price than Christmas wreaths and garlands but according to the people in the

business it is a viable operation with experienced pickers do the job (W. Kimber personal

communication; E. Meyer personal communication). It would also be interesting for

MKRF to start its own operation because of the availability of facilities and equipment.

The main problem would be in finding experienced pickers or people who are interested

to learn. Although the job may not seem difficult, people who are working in this

business must be skilled and trained for the operation to meet the high quality

requirements for the greens.

RECOMMENDATIONS FOR MKRF

Growing Christmas trees concurrently in MKRF could only become a viable option if a

niche market is developed (e.g. through the UBC Faculty of Forestry). However even

with a large marketing campaign it would be difficult to gain acceptable profits because

of the strong competition on the market and the high cost of production.

The situation for Christmas greens is different, as there is enough material in MKRF

to produce quality Christmas greens. The capital input in Christmas green harvesting is

low and there are no ecological concerns because the product comes from a tree. The

option of adding value to the Christmas greens by making garlands and wreaths presents

a highly marketable product, with higher revenue margin than the raw material.

27

5.2.2 Landscaping Products

NATIVE PLANTS FOR LANDSCAPING

In contrast to wild-crafting floral greens, the idea of commercially wild-crafting whole

plants for landscaping purposes is relatively new. Native plants from the forest have an

advantage over these plants grown in nurseries because they are fully grown (a desired

characteristic of landscaping plants). NTFP species in that are grown and harvested in

nurseries for landscaping include sword fern and vine maple, both of which are abundant

in MKRF. No literature was available on this topic, so research included interviewing

users (landscape architects) and the current producers of native plants (nurseries). The

BC Landscape Association suggested contacting the architects directly. A short e-mail

questionnaire was sent to the architects and covered the aspects of market research

explained in Chapter 4. The questions posed included: whether they use native plants, if

yes, who were their producers, and whether or not they think it would be possible for a

small-scale production to get access to the market. Out of twelve architects contacted four

replied and answered that they do use native plants although they sometimes have

difficulty finding a supplier. Using native plants has become more popular recently. For

example the City of Richmond required the use of native plants for a large landscape

project (L. Nielsen, personal communication). Native plants are also widely used in the

restoration of stream banks. Scott McLean from BC Hydro reported that they are using

thousands of native plants each year for Riparian area restoration under the RoWs.

Although this information was collected in exploratory research it indicates that there is a

demand by the landscape architects for native plants. The use of native plants was

identified for two main areas: for the restoration of Riparian areas and for use in

landscape architecture. Most of the plants used for these purposes, are currently grown in

nurseries. The nurseries growing native plants mentioned that the demand and sales have

been stable. Their customers include: local governments, landscape contractors, mine

reclamation, and many local restoration projects (P. Vrijmoed, personal communication).

They expect some of the smaller nurseries to drop out or extend their business into other

areas because it appears to be difficult to exist on native plants alone (P. Vrijmoed,

personal communication). It was also mentioned that there was a growing demand for

bigger native plants by landscape architects (P. Woodward, personal communication).

28

However Bruce Peel from Peels Nursery mentioned that they feel there is currently an

oversupply of native plant products. In addition, he does not see how the quality from-

forest grown plants can hold out against nursery-grown plants. It remains therefore

unclear what the current market potential for native plants is.

There are two different forces that are important for the development of the native

plants industry. Firstly, if government legislations created regulations that only native

plants could be used for in for example Riparian area restorations, the market for native

plants would immediately grow. Secondly, the consumer plays a key role in deciding

whether or not use native plants for landscaping. Demand for organic grown products is

high at the moment and there might be the potential for an organic native plants market,

which would secure a market for native plant species. Wild-crafted forest products are

produced without pesticides and are therefore suitable for obtaining organic certification.

However no one has required this type of certification yet (A. Brynne, personal

communication).

The quality requirements for plants in the landscaping industry are high and their

characteristics include: nice appearance, interesting colours, fast growing not too tall.

The quality requirements for plants used in Riparian management include: good rooting

abilities and fast growth rate. The prices paid for a fern in a 1 Gallon pot vary between

$3.50 and 7.50 (Cocksedge, 2002).

FOREST

From the forestry perspective the management and sustainable harvesting of native plants

is of high importance. The removal of native plants from Crown Land is not allowed

without a permit. Therefore a lot of harvesting of plants has been done illegally, which

has a negative impact on the population of wild native plants. For example in

Washington, the overharvesting of wild plants has severely degraded many ecosystems

(J. Whitacre, personal communication). Examples of unsustainable practices can also be

found in BC. There was a case on the Gulf Islands where 1000 Orchid bulbs were stolen

from their native habitat, resulting in a large decrease in the population. Many of these

plants are now probably sold at the nurseries as nursery-grown plants (P. Arcese,

personal communication). The first official harvesting trial on Crown Land was carried

out as part of the North Vancouver Island Demonstration Project (NVIDP). In this case

29

plants were harvested prior to further development (road building). The sustainability of

harvesting native plants for landscaping is a bigger concern than with floral greens

because the whole plant is removed from the forest. Therefore to show that ecologically

sound harvesting techniques are used the terms “salvage harvesting” or "pre-development

harvested plants" have been used to describe plants which would have been destroyed if

not harvested (W. Cocksedge, personal communication). The question arises whether the

definition of salvage harvesting includes sites prior to clearcuts. To date, there is little

information available on the effects of harvesting understory plants in a clearcut on future

plant populations. Since the management of native forest plants for landscaping purposes

has hardly been practiced, very little research has been conducted on these issues. In

addition to salvage harvesting of native plants, co-management, in which the understory

plants of interest are integrated into the management plan for silvicultural system could

be an option.

Another big issue with the harvest of native plants is the transplanting and survival

of the plants. According to several nurseries (including Paige Woodward from the Pacific

Rim Nursery) transplanting must be followed by a resting time, when the plant must be

maintain at the forest-nursery to ensure the survival from the transplanting shock and to

maintain quality. This procedure is time-consuming (1 year or longer depending on the

plant) and costly. However the transplanting viability differs for each plant and as such

the possibility exists to find plants which could be harvested and sold in the same year. In

addition to the transplanting viability of the plants, the quality requirements of the

industry must be considered. Nurseries tend to have better root: shoot ratios than forest

grown plants because they are grown in a controlled environment (B. Peel, personal

communication). However if the ultimate survival rates of the plant are the same, this

indicator might not be important.

NATIVE PLANTS FOR LANDSCAPING AT MKRF

There are several plants growing in abundance in MKRF, which would be suitable for

wild harvest or co-management. The different species of fern with are of interest because

they fulfill the landscaping requirements and are easy to transplant (see Picture 3 and 4)

(Vance et al., 2001).

30

Picture 3: Sword fern, MKRF Picture 4: Sword fern, MKRF

Source: (Katja Eisbrenner)

To verify the viability of transplanting ferns a news group on the internet for native pants

was contacted. Twelve members of this native plant news group, (including gardeners,

teachers, and ecologists) all agree that transplanting sword fern is very easy. They

recommended harvesting in the wet time of the year from November to January although

it is also possible to harvest in the summer. With respect to transplanting technique, they

suggested cutting off the old fronds and keeping the current ones. Younger plants are

easier to transplant because the root balls of older plants are fairly large and become more

difficult to transplant. Therefore it is suggested that only plants which fit in a one gallon

pot are used. Everyone from the news group and MKRF staff who has transplanted sword

fern reported a success rate near 100%.

Thinning is a common silvicultural practice carried out in MKRF each year. The

manager of MKRF has observed that in several sites where Douglas-fir, hemlock and

western red cedar have been thinned, the forest floor is heavily covered by sword fern

within two years. This situation offers the possibility for a co-management strategy, that

integrates the management for the NTFP into the silviculture system. Instead of randomly

harvesting sword fern throughout the forest, the harvesting could be concentrated in

31

certain areas, thereby reducing the scale of disturbance in the forest. As there is no

information available on the response of sword fern to harvesting after thinnings, trials

should be conducted prior to large-scale management. The light increase as a result of the

thinning is assumed to be the trigger for the increase in sword fern growth; this

hypothesis should be tested as well to determine how long sword fern can be managed on

a thinned site.

Vine maple is another plant of interest for landscaping due to its small size and its

colorful foliage in the fall (Vance et al., 2001). The seedlings have a high transplanting

viability (Vance et al., 2001) and MKRF staff have had some good experience with

transplanting it .

Besides the two plants discussed above, there may be other plants at MKRF which

fulfill the characteristics for landscaping plants (for details see Appendix II).

RECOMMENDATION

Further research on sustainable harvesting levels for forest landscaping plants is needed

before large-scale harvesting is carried out. Sword fern and vine maple should be

investigated first because of their known high transplanting viability. The high abundance

of sword fern in MKRF offers a good option to experimentally investigate sword fern

regeneration after harvesting. Before further research is invested the market situation

needs to further investigated and buyers need to be identified.

If further experimental research on the ecological side is conducted the following is

suggested. In a stand with high sword fern abundance after thinning different levels of

harvesting could be carried out and the regeneration observed over time. The light

requirements could be tested in different greenhouse trials. This could be done at UBC

Botanical Garden facilities or a small greenhouse could be built at MKRF. Another set of

trials could determine how well the plants transplant. The success rate could be tested by

taking a number of plants from the site, potting them and observing them over a certain

time. For this trial it would be important to measure the amount of root mass which may

be an important factor in transplanting. One concern with this type of research is that it

takes at least a couple of years before there are results. This process could be started with

trials set up on a small scale as an integrated project with concurrent marketing. If there is

the potential for expansion, the results from these trials could be implemented into the

32

operation. Because of the difficulty for MKRF to establish its own market and the limited

time availability of the staff, it would be beneficial to work with a nursery or another

interested partner. The Pacific Rim Nursery has indicated that they might be interested in

working with MKRF on a project like this (P. Woodward, personal communication). This

option would be very interesting for a Masters Student with particular interest in co-

management of native plants who could get support from the nursery (e.g. in

transplanting techniques). The other option is to offer this project to a nursery interested

in using the forest as their production site. MKRF would maintain the right to design the

trial projects with the nursery access all the information and would ultimately receive a

share from the product sales. The latter option seems to be the most practicable because it

would promote the research in this field with low input from MKRF.

5.2.3 Food Products

Forest-grown food products from non-domesticated species is a specialized niche market,

mainly because of the higher prices for products such as wild berries, syrup and wild-

harvested mushrooms. Although each of the products has their own market they have the

following characteristics in common: higher prices than for cultivated products, sold only

in specialty stores, and smaller demand than farmed products.

5.2.3.1 Berries

Most of the berries on the market are commercially produced. In the Lower Mainland,

berry farming is very popular and blueberries, raspberries and cranberries dominate the

market. Besides farmed berries, wild huckleberries, blueberries blackberries and berries

from salal, Oregon grape have a niche market and can be purchased in specialty stores or

on the Internet. Berries are also sold as fresh or frozen products or used for making

preserves such as jams and jellies. Fresh wild berries are known for their taste and

consumers acknowledge that they are significantly better than farm berries. However

wild berries are not widely available and are in specialty stores due to the high retail price

(P. Woodward, personal communication). Wild berries are more expensive than

commercially grown berries because of higher harvesting and transportation costs. In the

commercial berry industry the harvesting is done with machines and as a result the costs

are very low. Wild berries are handpicked and the costs are much higher because of the

33

labour involved. Depending on the species abundance and amount of berries available the

amount harvested per hour ranges from 2.2 kg salmonberry to 6 kg Oregon grape (see

Table 6) (H. Macy, personal communication). However these numbers change drastically

depending on the amount of harvestable berries available.

Species Oregon grape Huckleberry Salmonberry Salal

Kg/hours 6.0 2.8 2.3 3.0

Table 6: Berries picked at UBC Oyster River Research Farm 2001

Source: (H. Macy, personal communication)

Prices for wild harvested berries vary according to the location where they are picked and

sold, and their quality. The quality criterion for berries varies depending on whether they

are sold as a fresh product or as preserves (Granville Island vendors, personal

communication). Given that they are sold as fresh product and preserves the quality

criteria for berries varies. The appearance of the berries is of high importance when they

are sold as a fresh product while the sweetness of the berries is most essential when they

are used for preserves. The prices for commercially farmed berries range from $2-$4/lb

Cdn retail on the local markets and are as low as $1/lb Cdn wholesale price (K. de Wolfe,

personal communication). Wild harvested berries are sold on the Internet for as much as