the bioeconomy in the oecd countries and beyond · the bioeconomy in the oecd countries and beyond...

TRANSCRIPT

Robert Wells

Head of Biotechnology Unit, OECD

28 October 2010

1

The Bioeconomy in the OECD Countries and Beyond

Main Themes

• What is the OECD and why does it matter?

• The importance of Innovation

• The Bioeconomy is here… and it’s here to stay.

• Industrial/Environmental Biotechnology: the potential and the challenges

• Key messages

2

What is the OECD?

• Born after World War II to coordinate/implement the “Marshall Plan” for reconstruction of Europe

• Advises governments on economic, social and technological policies (science, innovation, health etc…) and contributes to economic growth and globalisation

• Today the OECD has 33 member countries in North America, Europe, and Asia-Pacific. 2 more waiting at the door.

• Enhanced Engagement Countries: Brazil, China, India, South Africa

• Global Forum on Biotechnology (Agreed 27/10/2010)

3

OECD Global Outreach

4

World Population in 2030

Source: Salim Sawaya, based on medium variant of the UN Population Division’s “World Population Prospects: The 2006 Revision Population Database”

Innovation is Key

6

Innovation is key to growth...

Contributions to labour productivity growth, 1995-2006, in %

* Investment in intangibles and multi-factor productivity growth

account for between two-thirds and three-quarters of labour

productivity growth.

-1

0

1

2

3

4

5

6

Intangible capital MFP Non-ICT capital

ICT capital Tangible capital Labour quality

... and innovation increasingly happens

across borders

(institutions, countries, disciplines).

8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Share of patents with foreign co-inventors (%)

1993-1995 2003-2005

Source: OECD Patent Database.

New global players have

emerged … Contributions to growth in global R&D, 1996-2001 and 2001-2006

(in billion constant US PPP and %)

37%

16%

23%

15%

7%

13%

10%

13%

11%

30%

12%

13%

0

20

40

60

80

100

120

140

160

180

1996-2001 2001-2006

Other non-OECD (2)

China

Other OECD (1)

Japan

EU-27

United States

Note: (1) Australia, Canada, Iceland, Korea, Mexico, New Zealand, Norway and Turkey

(2) Argentina, Brazil, India, Israel, Russian Federation, Singapore, South Africa, Chinese Taipei

Source: OECD.

How the BRICS stack up…

Global R&D, percentage share

0

1

2

3

4

5

6

7

8

China Russian Federation

India Brazil South Africa

1996

2005

10

11

GERD as % of GDP

BERD as % of GDP

Industry financed GERD as % GDP

Triadic patents per million population

Scientific articles per million population

% of firms with new-to-market product innovations (as a % of all firms)

% of firms undertaking non-technological innovation (as a % of all

firms)

Business funded R&D in the HE & GOV sectors

Patents with foreign co-inventors

% of GERD financed by abroad

Researchers per thousand total employment

Science & Engineering degrees as % of all new degrees

% of population aged 25-64 with tertiary degree

Russian Federation Average

Gross expenditure on R&D (as a

percentage of GDP, 1990-2008)

OECD, Main Science and Technology

Indicators database, May 2010

0.0

0.5

1.0

1.5

2.0

2.5

OECD average Russian Federation %

GERD as a percentage of GDP

Educational attainment

13

0

10

20

30

40

50

60 %

Percentage of population aged 25-64 with a tertiary

degree (2008) - OECD, Education database 2010

The Bioeconomy is here… and

it’s here to stay

14

Biotech reliance on Science…

Reliance of patents on science citations

(biochemistry papers cited by pharmaceutical patents)

57.7

64.8

48.6

58.8

30.7

58.9

81.9

9.0

6.3

11.7

21.7

18.4

28.0

6.6

17.6

22.7

15.4

10.4

9.8

6.0

4.3

3.9

5.4

14.3

8.4

14.1

13.3

7.6

0% 20% 40% 60% 80% 100%

United States

Japan

United Kingdom

Germany

France

China

Korea

Higher education Government Industry Non profit

Hospital Other NA

Sequencing Output

16 Source: MR Stratton et al. Nature 458, 719-724 (2009)

Rapidly declining genome

sequencing costs • Some say the $1000 genome will arrive in

20201, but this could be much sooner

• Complete Genomics will soon start sequencing 8 genomes or more for $20K each and 1,000 genomes $5K each2

• The Archon X-Prize for genomics is offering a $10 million prize to the first team to sequence 100 human genomes at a cost of less than $10,000 per genome in less than 10 days

(1) Carlson, R. (2007), Genome Synthesis and Design Futures: Implications for the US Economy, Bio-Era.

(2) Duncan, D. (2009), Complete Genomics Sequences 14 Genomes, MIT Technology Review.

Overwhelming challenge to

global health • MALARIA - 300 million, 2 million deaths

annually. • HEPATITIS C - 170 million chronically infected

with Virus. Four million infected each year; 80% chronic, 20% cirrhosis, 5% liver cancer.

• HEPATITIS B - 2 billion people . 400 million people chronically infected and 1 million people die each year.

• TB - One third of the world is infected with M. tuberculosis with 10 million cases every year accounting for two million deaths.

• HIV - Approximately 50 million infected. 3.9 million deaths in 2005.

• OTHERS - Some outbreaks are still relatively unknown - cholera still causes close to 120,000 deaths per year.

18

Number of publications identifying a

drug-gene relationship (3yr running avg)

19 Source: OECD, based on PharmGKB database as of December 10, 2007.

Diseases for which genetic testing is available

20

Source: OECD, based on GENETests (2007), www.genetests.org/, accessed 14 December 2007.

Chemical and biotech sales per

segment 2007

OECD Outlook on Industrial

Biotechnology

25,3%

31,0%

22,5%

21,2%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

59,2%22,4%

14,5%

3,9%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

Chemical sales per segment 2007

100% = 1,383 billion Euro

Biotech sales1) per segment 2007

100% = 48 billion Euro

1,5% of base

chemicals

4,8% of

specialty

chemicals5,4% of

consumer

chemicals

18,7% of

active pharma

ingredients

1) Sales of chemical products made by biotechnological processes and not chemical processes

Source: CEFIC Facts & Figures January 2009, market evaluation of FESTEL CAPITAL from May 2009

Chemical and biotech sales per

segment 2017

OECD Outlook on Industrial

Biotechnology

33,3%

21,4%

24,8%

20,5%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

51,3%

25,0%

17,1%

6,6%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

Chemical sales per segment 2017

100% = 2,212 billion Euro

Biotech sales1) per segment 2017

100% = 340 billion Euro

10,0% of base

chemicals

13,1% of

specialty

chemicals22,3% of

consumer

chemicals

47,9% of

active pharma

ingredients

1) Sales of chemical products made by biotechnological processes and not chemical processes

Source: CEFIC Facts & Figures January 2009, Market evaluation of FESTEL CAPITAL from May 2009

GM crop plantings 2008

23

Source: Salim Sawaya, based on data from James (2008). Notes: (1) Countries planting less than 1,000,000 hectares in 2007 include: Australia (200,000 ha), Bolivia (600,000 ha), Burkina Faso (<50,000), Chile (<50,000),

Colombia (<50,000), Czech Republic (<50,000), Egypt (<50,000), Germany (<50,000), Honduras (<50,000), Mexico (100,000 ha), Philippines (400,000 ha), Poland (<50,000), Portugal (<50,000), Slovakia (<50,000), Spain (100,000 ha), Romania (<50,000), and Uruguay (700,000 ha).

What governments do makes a

difference

24

25

(indexed on 1980=1.0, Annex 1 ratification countries)

Policy can induce greater innovation

Patenting in climate mitigation technologies relative to all sectors

Regulation has had a major

impact on public research

26

GM field trials by public research organisations in Europe and North America

0

50

100

150

200

250

300

350

400

Europe North AmericaSource: OECD, based on the UNU-MERIT field trial database.

0

50

100

150

200

250

300

350

400

Europe North America

And business research too!

27

Source: OECD, based on the UNU-MERIT field trial database.

Notes: (1) A total of 16,399 GM field trials were conducted in Australia, Canada, European Union, Japan, Mexico, New Zealand,

Switzerland, and the United States by private firms from 1990 to 2007.

(2) 3,944 field trials were conducted by European seed firms and subsidiaries between 1990 and 2007 inclusive. This

includes firms based in the European Union and Switzerland.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Share of private GM field trials conducted by European firms

By 2030, emerging economies will

become the world’s bread basket • Strong evidence that European agbio R&D has slowed

down significantly

• Developing country activity has increased

– Of the 8 countries planting more than a million ha of GM crops, 6 are non-OECD countries

– Over 550 biotech field trials have occurred in 47 non-OECD countries

– Major agricultural biotechnology programmes

Country Agricultural biotechnology R&D spending (in USD PPP)

Brazil 350 million per year over next 10 years

China 120 million per year (24 million going to GM rice)

India 100 million per year

Multi-faceted and Interdisciplinary

nature of Green Technologies

Main barriers within each of the three pillars for

successful delivery of industrial biotechnology

30

Pillar Barriers

Science and

Technology Base

Fragmentation of funding and

policies

Lacking analysis of national

strengths

Interdisciplinary research

Capital

Weak marketplace

Capital for scale-up

High costs for feedstock

Human Resources

Inability to evaluate future HR needs

Gap between education programmes

and industry needs

Poor attractiveness to young

individuals

.

Public energy-related R&D

expenditures in OECD countries

the scope of green technology

Bioenergy R&D

32

Public R&D expenditures for bioenergy and the share of total energy R&D in IEA countries

Notes: Includes public R&D energy expenditures for Canada, EU-15, Japan, New Zealand, Norway, Korea, Switzerland , and the

United States. R&D spending is in USD millions at 2006 prices using PPP.

Source: Authors, based on IEA, 2008.

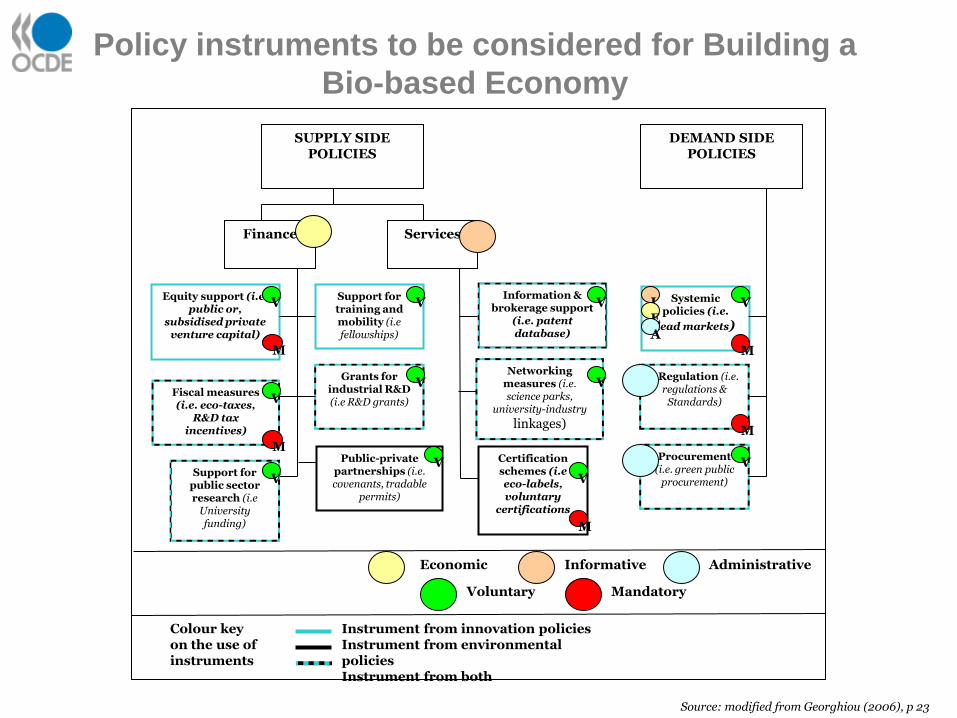

SUPPLY SIDE POLICIES

Finance Services

Equity support (i.e. public or,

subsidised private venture capital)

Support for training and mobility (i.e fellowships)

Fiscal measures (i.e. eco-taxes,

R&D tax incentives)

Public-private partnerships (i.e. covenants, tradable

permits)

Grants for industrial R&D (i.e R&D grants)

Information & brokerage support

(i.e. patent database)

Networking measures (i.e. science parks,

university-industry

linkages)

DEMAND SIDE POLICIES

Systemic policies (i.e.

lead markets)

Regulation (i.e. regulations &

Standards)

Procurement (i.e. green public

procurement)

Certification schemes (i.e eco-labels, voluntary

certifications

Support for public sector research (i.e

University funding)

M

M

M

V

V

V

Instrument from innovation policies Instrument from environmental policies Instrument from both

Colour key on the use of instruments

V

V

V

Economic Informative

Voluntary Mandatory

Administrative

V

V

M

I E A

V V

M

V

Source: modified from Georghiou (2006), p 23

Policy instruments to be considered for Building a

Bio-based Economy

Preparing the foundation • Optimal benefits from the bioeconomy will

require identifying and preparing for a range of possible futures to prevent locking-in inferior technological solutions

• Agriculture: encourage biotech use by improving access to technologies for use in a small markets and by small firms

• Health: support long terms follow-up research comprehensive health record systems

• Industry: reward environmentally sustainable technologies (e.g. high energy density biofuels)

35

• Ensure that incentives for private investment are better aligned with the public interest

• Continue developing regulatory systems that incorporate pharmacogenetics

• Support long term research, using population-based medical databases, into health outcomes

• Cope with long-term impacts of regenerative and personalised medicine on healthcare, including data confidentiality, healthcare delivery, and doctor-patient relationships

36

Prepare for a costly but beneficial

revolution in healthcare

Don’t neglect agriculture and industry

37

• The solution is not to reduce R&D expenditures in health, but to encourage substantially greater public and private investment in other applications of biotechnology.

Promote bioeconomy integration

• Innovative use of knowledge networks and markets

– Collaborative mechanisms for maximizing the benefits of intellectual property

• Development of innovative governance structures in biotechnology

– Invent new structures or retrofit existing ones

39

And more generally …

• Don’t cut R&D support coming out of the crisis. Recovery will depend on it in the medium term.

• Understand and utilise national innovation systems within the evolving networked model of innovation

• Protect investment in intellectual assets and create new models to share and leverage such assets

• Mobility matters – The demand for talent is inescapable. The networked model feeds on it.

• Current systems of prioritisation and governance need to evolve post-crisis – prioritisation, evaluation & subsidiarity,

…and…

• Need to design institutional structures that facilitate multilateral co-operation in STI for global challenges

40

Contacts: www.oecd.org/sti/innovation

www.oecd.org/biotechnology

41