the banking industry after the financial tsunami: a hong ... - 0945 - federick ma.… · the...

TRANSCRIPT

The Banking Industry after the Financial Tsunami:A Hong Kong Perspective

Presented by Prof. Frederick MaPresented by Prof. Frederick Ma

Change in Power - Rise of Chinese Bank

Top Ten of the Banking Industry by Market Capitalization

1. Industrial and Commercial Bank of China2. China Construction Bank3. HSBC Holdings PLC4. JP Morgan Chase5. Agricultural Bank of China6. Bank of China7. Bank of America8. Wells Fargo & Co9. CitiGroup INC10. Rodovid Bank

Source: Bloomberg, as of 31 Aug 2010

Others25.1%

China16.5%

Europe14.7%

US13.9%

UK8.1%

Japan5.0%

Brazil4.8%

Canada4.6%

Australia4.4%

Switzerland3.0%

China Presence in Top 500 Banks by Market Capitalization

Source: Bloomberg, as of 31 August 2010

Change in Power - Rise of Chinese Bank

Overseas Acquisition and Expansion of Chinese Bank

• Acquisition – ICBC acquires ICBC Asia (10 Aug 2010)BOC acquires Heritage Fund Management SA (23 Jul 2008)CMB acquires Wing Lung Bank (2 June 2008)ICBC acquires Standard Bank Group (25 Oct 2007)

• Joint Venture – BOC & Temasek Holding (15 Mar 2010)Bank of Beijing & Bank of Nova Scotia (28 Aug 2008) CCB & Bank of America (6 Sep 2007)ABC & Credit Agricole SA (23 Sep 2006)

Change in Power - Rise of Chinese Bank

Source: Bloomberg

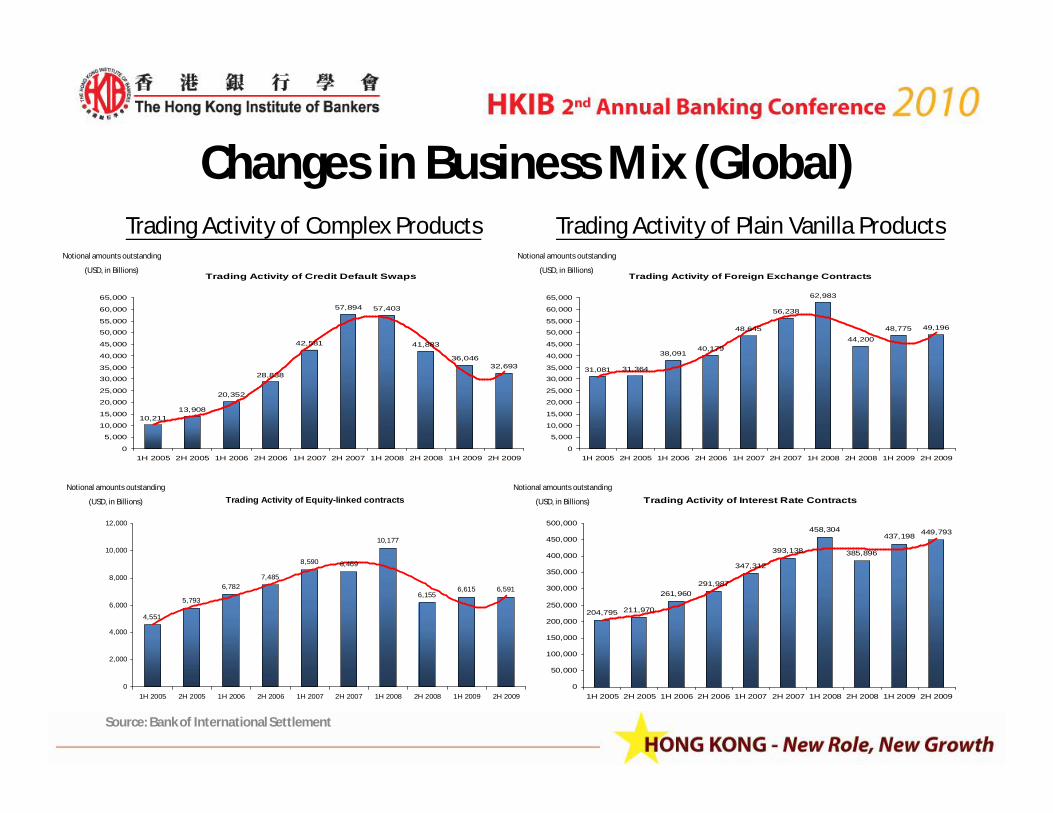

Changes in Business Mix (Global)Trading Activity of Complex Products

Trading Activity of Equity-linked contracts

4,551

5,793

6,7827,485

8,590 8,469

10,177

6,1556,615 6,591

0

2,000

4,000

6,000

8,000

10,000

12,000

1H 2005 2H 2005 1H 2006 2H 2006 1H 2007 2H 2007 1H 2008 2H 2008 1H 2009 2H 2009

Source: Bank of International Settlement

Notional amounts outstanding

(USD, in Billions)

Trading Activity of Credit Default Swaps

10,21113,908

20,352

28,838

42,581

57,894 57,403

41,883

36,04632,693

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

1H 2005 2H 2005 1H 2006 2H 2006 1H 2007 2H 2007 1H 2008 2H 2008 1H 2009 2H 2009

Notional amounts outstanding

(USD, in Billions)Trading Activity of Foreign Exchange Contracts

31,081 31,364

38,09140,179

48,645

56,238

62,983

44,200

48,775 49,196

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

1H 2005 2H 2005 1H 2006 2H 2006 1H 2007 2H 2007 1H 2008 2H 2008 1H 2009 2H 2009

Notional amounts outstanding

(USD, in Billions)

Trading Activity of Interest Rate Contracts

204,795 211,970

261,960291,987

347,312

393,138

458,304

385,896

437,198 449,793

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

1H 2005 2H 2005 1H 2006 2H 2006 1H 2007 2H 2007 1H 2008 2H 2008 1H 2009 2H 2009

Notional amounts outstanding

(USD, in Billions)

Trading Activity of Plain Vanilla Products

Changes in Business Mix (Global)

Source: Board of Governors of the Federal Reserve System

Consumer Credit Outstanding in US(Billions of dollars, not seasonally adjusted)

Yr 2005 2291.7

Yr 20062385.7

Yr 20072522.8

Yr 20082561.1

Yr 20092448.8

Yr 1H 2010 2418.5

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Percentage change at annual rate

Changes in Business Mix (Global)

Fall of Investment Banks

• De-leveraging & Written Down of Market Capital – Market cap by 40% (on average) after crisis– I-banks used to be highly leveraged: Bear Stearns – 30X (equity)

• Falls – Bear Stearns acquired by JP Morgan Chase (16 Mar 2008)– Merrill Lynch acquired by Bank of America (14 Sep 2008)– Lehman Brothers bankrupted (15 Sep 2008)

• Transformation – Goldman Sachs and Morgan Stanley transform from independent investment banks into commercial banking holding companies. (22 Sep 2008)

Source: Bloomberg

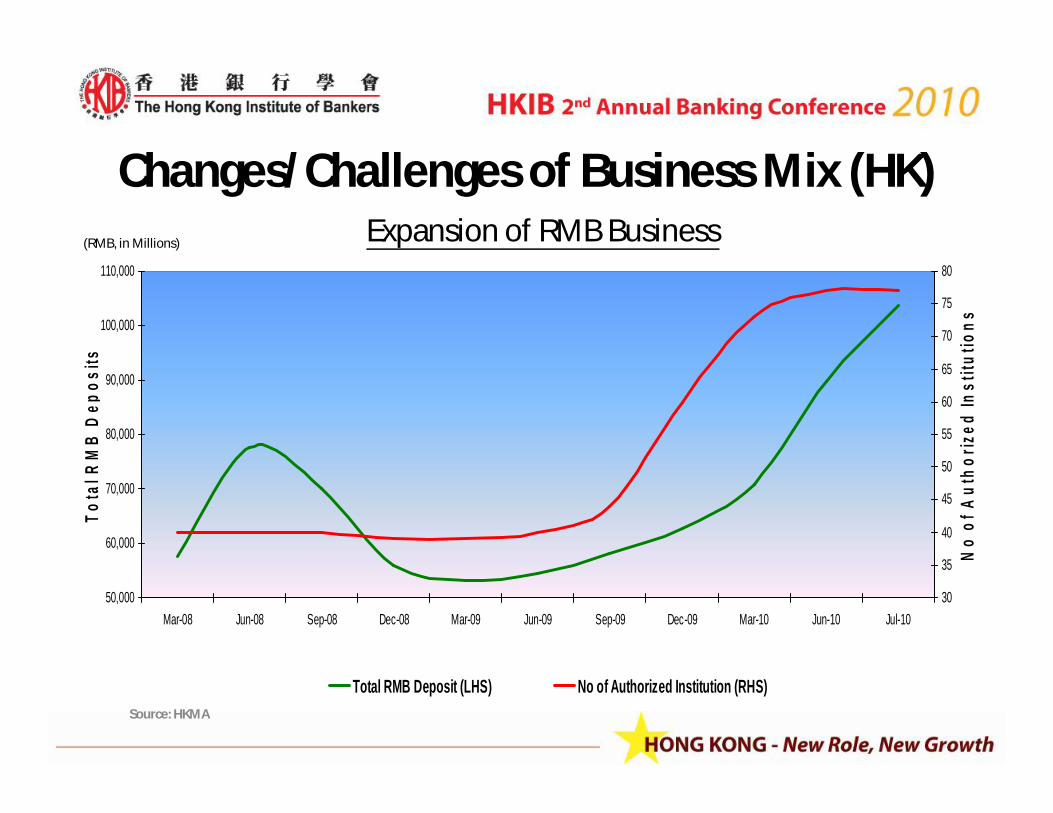

Changes/Challenges of Business Mix (HK)

Loan Growth by Type

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Loan

Gro

wth

YoY

(%)

'Dec 07 'Jun 08 'Dec 08 'Jun 09 'Dec 09

MortgageFinancial ConcernsConstruction, Property Development/InvestmentCredit Card

Source: HKMA

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Loan

Gro

wth

YoY

(%)

'Dec 07 'Jun 08 'Dec 08 'Jun 09 'Dec 09

Trade Finance Loan for use in HK Loan for use outside HK

Loan Growth by Sector (Use in HK)

Changes/Challenges of Business Mix (HK)Low Interest Rate Environment – Pressure on Net Interest Margin(%)

HSBC HSB BOCHK BEA DBS HK Wing Hang

Yr 2007 2.37% 2.23% 2.07% 1.90% 2.36% 1.90%

Yr 2008 2.36% 2.36% 2.00% 1.85% 2.02% 1.84%

Yr 2009 1.92% 1.90% 1.69% 1.80% 2.05% 1.82%

Source: Banks & Fitch

Year Bank

1.30%

1.40%

1.50%

1.60%

1.70%

1.80%

1.90%

2.00%

1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08 1Q 09 2Q 09 3Q 09 4Q 09

Reta

il B

anks

Net

Inte

rest

Mar

gin

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

1M H

IBO

R

Retail banks net interest margin quarterly annualised ( LHS ) 1M HIBOR quarterly average ( RHS )

Source: HKMA

Changes/Challenges of Business Mix (HK)Banks strike for Loan Growth

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Dec 2004 Dec 2005 Dec 2006 Dec 2007 Dec 2008 Dec 2009

Loans in HK Loans outside HK Trade Finance Others(HKD, in Billions)

Source: HKMA

Changes/Challenges of Business Mix (HK)Expansion of RMB Business

Source: HKMA

50,000

60,000

70,000

80,000

90,000

100,000

110,000

Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Jul-10

Tota

l RM

B D

epos

its

30

35

40

45

50

55

60

65

70

75

80

No

of A

utho

rized

Inst

itutio

ns

Total RMB Deposit (LHS) No of Authorized Institution (RHS)

(RMB, in Millions)

Challenges from Current Business Mix

• Growth opportunities: Private Banking– Emerging wealth management business from High-Net-

Worth-Individuals from Mainland China

• Industry responses in face of new opportunities:– Major banks to increase headcounts in Asia-Pacific to

serve the growing high-earning segment

Change in Regulatory Environment (US)

Dodd-Frank Wall Street Reform and Consumer Protection Act (Effective 21 Jul 2010)

• Promote the financial stability of the United States by improving accountability and transparency in the financial system

• To end "too big to fail"

• To protect the American taxpayer by ending bailouts

• To protect consumers from abusive financial services practices

Change in Regulatory Environment (US) Key provisions:• Increasing monitoring, supervision and investor protection

– Establishment of Financial Stability Oversight Council, Office of Financial Research & of Bureau of Consumer Financial Protection

– Enhanced capital requirement and leverage limit

• Expanded scope of liquidation to prevent “too big to fail”– Orderly Liquidation Authority

• Strengthened Volcker Rule and bank regulation– Prohibitions on proprietary trading and investment in & sponsoring PE/ HF

• Increased regulation of OTC Swap Market– From OTC to exchange traded

Change in Regulatory Environment (EC)

• New regulatory bodies created on 23 Sep 2009 with increased regulatory power

– European Systemic Risk Board (ESRB)

– European System of Financial Supervisors (ESFS)

• Establishment of European Securities and Markets Authority (ESMA)

– Includes provisions to prohibit financial products when there is a risk to investor protection

– Widens scope of the ability to develop technical binding standards

Change in Regulatory Environment (UK)

From Financial Services Authority (FSA) to Bank of England (BOE)• Announcement on 16 Jun 2010 of the plan to abolish the FSA

& separate its responsibilities to new agencies & BOE

• New bodies that will be in operation by the end of 2012– Financial Policy Committee– Prudential Regulation Authority– Consumer Protection Markets Authority– Banking Commission

Change in Regulatory Environment (HK)•• Guideline on Remuneration SystemGuideline on Remuneration SystemHKMAHKMA- Adopt Fixed and Variable Incentives, Mix of instruments or

Long Term Performance - Include both financial and non-financial factors- Impact on AI’s supervisory CAMEL rating and existing

minimum capital requirements- Enhance public disclosure of remuneration- Expect to take prompt action and achieve consistency with

its principles within 2010

Source: HKMA & SFC

•• Business practices (Wealth Management)Business practices (Wealth Management)

HKMAHKMA

- Physical Segregation of Business

- Full Audio Recording for Investment Transactions

- Enhanced Suitability

- Pre-investment Cooling Off Period (PICOP)

SFCSFC

- New Structured Investment Product Handbook

- Cooling Off Period for Long Tenor Products

- Investors Characterization

Change in Regulatory Environment (HK)

•• The Basel III Accord (Basel Committee on Banking Supervision)The Basel III Accord (Basel Committee on Banking Supervision)–– Time Frame Time Frame –– phase in from phase in from 1 January 20131 January 2013 through to through to 1 January 20191 January 2019

Banks in HK are not much affected in view of current capital level Banks in HK are not much affected in view of current capital level ((average Total Capital = 15.7%, Common Equity average Total Capital = 15.7%, Common Equity 10.4%10.4%))

Latest Development in Regulatory Environment

Source: Bank of International Settlement

Conclusions – A HK Perspective

We are faced with the challenges…We are faced with the challenges…- To repair professional/industry image

- To regain investor/consumer confidence

- To adjust business strategies in light of more stringent regulatory & operating environment

Yet with the new opportunities…Yet with the new opportunities…- Increased mobility: Cross-border businesses & new potential

customer group - Mainlanders

- The Internationalization of RMB:

- Hong Kong’s role as the offshore RMB center

- Potential development of a whole range of RMB products

What to expect?What to expect?- Local banking industry will continue to be competitive

- Mainland Chinese banks’ presence will be stronger in the future (M&A?)

Conclusions – A HK Perspective

Thank You