the bank of thailand’s framework - oecd. · pdf filethe bank of thailand’s...

TRANSCRIPT

The Bank of Thailand’s Framework for Financial Consumer Protection

and Education HKMA – SFC – OECD Asian Seminar on

“the Evolution of Financial Consumer Protection and Education in Asia” 13 December 2012

Amara Sriphayak Bank of Thailand

Outline

1. Thailand at a Glance 2. Current Financial Consumer Protection Policy 3. Responsible Business Conduct of Financial Service

Providers 4. Key challenges and opportunities

– Regional and Global Levels – National Level – Financial Service Providers – Individuals

2

3

Important Statistics GDP (as of 2011)

345.65 billion USD

Population (as of 2011)

69.5 million

Income per Capita (as of 2011)

4,420 USD

Number of FIs under the BOT’s supervision (as of November 2012)

37

Total Asset of the Thai Financial System* (as of June 2012)

1.28 trillion USD

Financial Access (as of Q1 2010)

85%

1. Thailand at a Glance

* comprising FIs under the BOT’s supervision and other financial service providers Source : Bank of Thailand, Office of The National Economic and Social Development Board, National Statistical Office and The World Bank

4

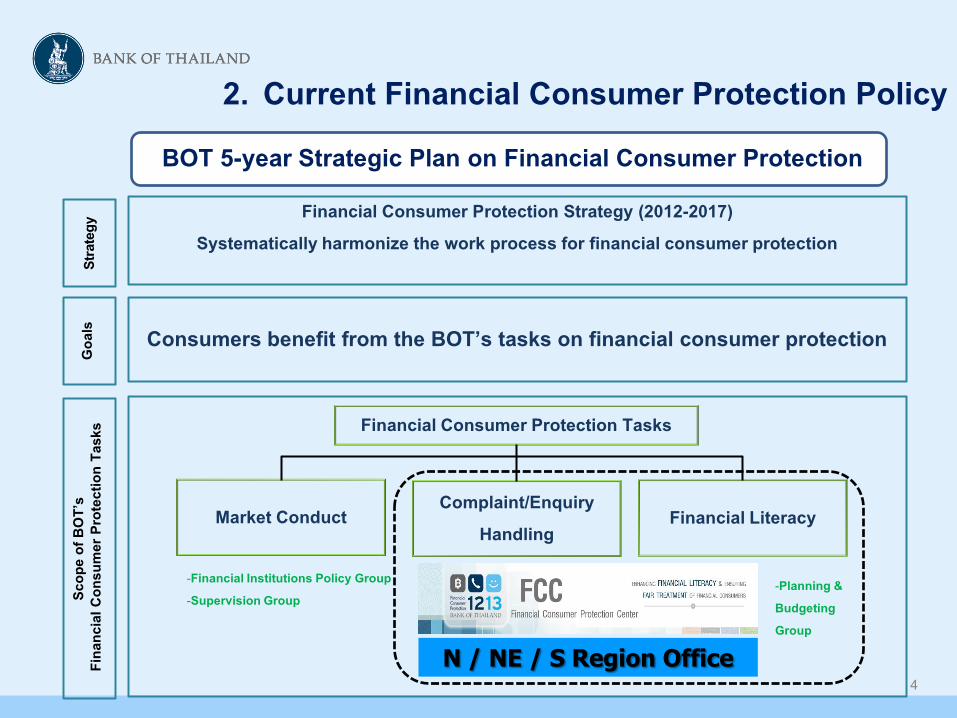

2. Current Financial Consumer Protection Policy

Financial Consumer Protection Strategy (2012-2017) Systematically harmonize the work process for financial consumer protection

Stra

tegy

Consumers benefit from the BOT’s tasks on financial consumer protection

Goals

Sc

ope o

f BOT

’s

Fin

ancia

l Con

sum

er P

rote

ctio

n Ta

sks

Complaint/Enquiry Handling

Financial Literacy Market Conduct

Financial Consumer Protection Tasks

BOT 5-year Strategic Plan on Financial Consumer Protection

-Financial Institutions Policy Group -Supervision Group

N / NE / S Region Office

-Planning & Budgeting Group

5

Number of Complaints : 2,853 • Credits 79% • Deposits 18% • Others 3%

FCC’s Complaint Handling Statistics (Jan – Sep 12)

Top-three Complaints regarding Credits • Debt restructuring (mainly credit cards) • Interests /Fees (miscalculation / high annual fee / prepayment fee) • Refinance (delay in refinancing to other FIs)

Top-two Complaints regarding Deposits • Inaccurate records in customers’ accounts as a result of deposit / withdrawal / transfer transactions (recipients not obtaining transferred money / delays in receiving money / money saved in the accounts missing) • Interests / Fees (high fees / inactivity fee/ ATM fee)

79%

18%

3%

Credits

Deposits

Others

Some issues gathered from consumer complaints are used as inputs in the formation of supervisory policy

2. Current Financial Consumer Protection Policy

6

Financial Literacy Roadmap

• Customer of FIs under BOT Supervision: General public / SMEs

• Related groups that support the work in a field of consumer protection: Police, prosecutor, court officials and DSI

Target Groups

• Financial knowledge (Rights and responsibilities of fin. consumers, fin. planning, key term and related info. of fin. products, and fin. fraud)

• Payment System (e-payment)

• Risk Management

Topics for Financial Education • Easy to understand / in

plain language • Communication channels

through mass media such as newspaper, BOT website, YouTube

Communication Channels and How To

2. Current Financial Consumer Protection Policy

7

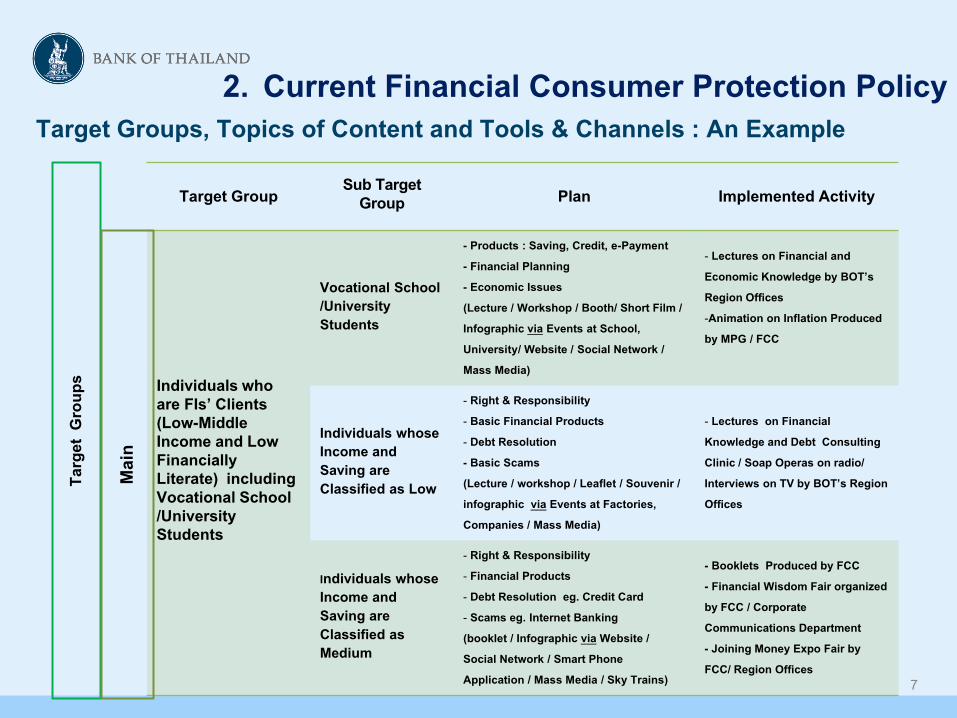

Target Groups, Topics of Content and Tools & Channels : An Example

Targ

et G

roup

s

Target Group Sub Target Group Plan Implemented Activity

Individuals who are FIs’ Clients (Low-Middle Income and Low Financially Literate) including Vocational School /University Students

Vocational School /University Students

- Products : Saving, Credit, e-Payment - Financial Planning - Economic Issues (Lecture / Workshop / Booth/ Short Film / Infographic via Events at School, University/ Website / Social Network / Mass Media)

- Lectures on Financial and Economic Knowledge by BOT’s Region Offices -Animation on Inflation Produced by MPG / FCC

Individuals whose Income and Saving are Classified as Low

- Right & Responsibility - Basic Financial Products - Debt Resolution - Basic Scams (Lecture / workshop / Leaflet / Souvenir / infographic via Events at Factories, Companies / Mass Media)

- Lectures on Financial Knowledge and Debt Consulting Clinic / Soap Operas on radio/ Interviews on TV by BOT’s Region Offices

Individuals whose Income and Saving are Classified as Medium

- Right & Responsibility - Financial Products - Debt Resolution eg. Credit Card - Scams eg. Internet Banking (booklet / Infographic via Website / Social Network / Smart Phone Application / Mass Media / Sky Trains)

- Booklets Produced by FCC - Financial Wisdom Fair organized by FCC / Corporate Communications Department - Joining Money Expo Fair by FCC/ Region Offices

Main

2. Current Financial Consumer Protection Policy

8

Financial Consumers Empowerment Proficient in financial knowledge and competent in making

informed financial decisions

Financial Stability Increase financial inclusion and

greater transparency by FIs

Sustainable and inclusive economic development

Resilience to change

2. Current Financial Consumer Protection Policy

9

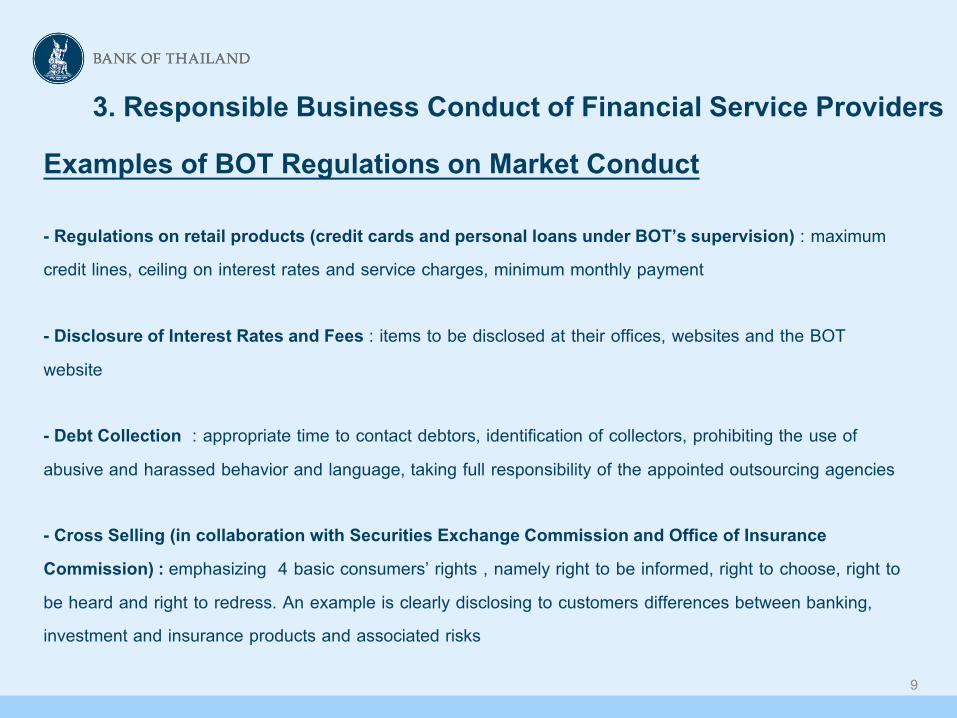

Examples of BOT Regulations on Market Conduct - Regulations on retail products (credit cards and personal loans under BOT’s supervision) : maximum credit lines, ceiling on interest rates and service charges, minimum monthly payment - Disclosure of Interest Rates and Fees : items to be disclosed at their offices, websites and the BOT website - Debt Collection : appropriate time to contact debtors, identification of collectors, prohibiting the use of abusive and harassed behavior and language, taking full responsibility of the appointed outsourcing agencies - Cross Selling (in collaboration with Securities Exchange Commission and Office of Insurance Commission) : emphasizing 4 basic consumers’ rights , namely right to be informed, right to choose, right to be heard and right to redress. An example is clearly disclosing to customers differences between banking, investment and insurance products and associated risks

3. Responsible Business Conduct of Financial Service Providers

10

11

Fees

12

4. Key challenges and opportunities : Regional and Global Levels

Emergence of ASEAN Economic Community (AEC) in 2015 - Enhancing cross-border trade and services and accelerating competition in financial system result in

higher demand for services and more complex financial products Challenges : - Consumers need to be well equipped with financial knowledge and be able to make informed decision - Businesses, especially SMEs, need to understand financial products that would serve their needs.

Differences in Consumer protection mechanisms in various countries - Consumer protection mechanisms in each country vary given unique characteristics of economic and

financial system Challenges : - How to harmonize the regulations to the international standard while each country

have to take into accounts stage of economic and regulatory development as well as levels of consumer sophistication?

- It is necessary to ensure that regulatory framework for consumer protection remains relevant and dynamic

Opportunity regarding both issues : Countries may learn from and share resources & experience with one another and adapt to use in their countries as appropriate

13

4. Key challenges and opportunities: National Level

Enhancing Cooperation among Related Authorities and Agencies Consumer protection and education have been tasked of several authorities and agencies,

ranging from financial regulatory authorities, financial service providers to NGOs.

Challenges : For this worthwhile mission to be accomplished, relevant organizations both public and private sector have to cooperate in a manner that would bring unity, effective resource allocations and focus on the same direction at the same time avoid any overlapping.

Note: As for Thailand, the Financial Literacy Committee chaired by the Permanent

Secretary of Ministry of Finance has been appointed to set the country’s financial education plans and monitor the developments.

14

4. Key challenges and opportunities: Financial Service Providers

Harmonization between prudence, competition and consumer protection Challenges : - Appropriate balance between providing adequate safety for consumer V.S.

promoting competition and financial innovation must be sought (without imposing excessive regulatory costs and burdens on FIs and consumers)

- It is important to encourage financial service providers to realize the importance of fair business conduct (both to consumers and shareholders)

Opportunity : Financial service providers can promote consumer protection through financial education as part of their CSR. This may also help increase a number of customers who look for “ethical” financial service providers.

Disclosure of Information Financial service providers should provide adequate and unbiased information, such all returns and risks

associated with their products, and offer appropriate products to customers. In addition, disclosure of information will be beneficial to customers when it is thoroughly understood.

Challenge : How to balance between amount of information adequate to make informed decision and clear, concise and necessary information has to be identified?

15

4. Key Challenges and Opportunities: Individual Level

Customers’ own responsibilities - Knowing what should be done does not always lead to changes in behavior. Challenge : Factors that affect the individuals’ behaviors and decision making need to be

identified. Examples may be education level, previous experience, financial situation and attitudes.

Opportunities : - One-to-one training programs such as helping employees in factories

solve their debt problems, though criticized as being labor intensive, have proved successful. This group of survivors may also be multipliers to lend a hand to the others.

- Success stories and where to get help should be promoted through several channels to indirectly encourage people to change behavior.