the balance sheet accounting 598

DESCRIPTION

TRANSCRIPT

The Balance Sheet

Accounting 598

Fall, 2006

Do we care how things are classified on the financial statements?

What about the balance sheet? How important is classification of items on the balance sheet?

What is important about balance sheet classification...

Current AssetsInvestment and FundsProperty, Plant, and EquipmentIntangiblesOther Assets

Do we care if all debit-balance accounts are classified as assets?

Do we care how we measure those debits? How do people use those debit balances in

decision making? I remember when I took Intermediate Accounting, the professor said that the Balance Sheet was archaic; only the income statement mattered. Do you agree?

Why are we concerned with the definition of assets? With classification of assets?

Assets..(CON 6).

A. [an asset] embodies a probable future benefit that involves a capacity, singly or in combination with other assets, to contribute directly or indirectly to future net cash inflows,

B. A particular entity can obtain the benefit and control others’ access to it, and

C. The transaction or other event giving rise to the entity’s right to or control of the benefit has already occurred.

Assets commonly have other features that help identify them--for example, assets may be acquired at a cost and they may be tangible, exchangeable, or legally enforceable.

However, these features are not essential characteristics of assets. Their absence, by itself, is not sufficient to preclude an item’s qualifying as an asset. That is, assets may be acquired without cost, they may be intangible, and although not exchangeable they may be usable by the entity in producing or distributing other goods or services...

What do you think of the FASB’s definition?

Is the way we value assets on the balance sheet consistent with the above definition?

Under this definition, could any debit on the balance sheet potentially be an asset? What about operating losses of start-up companies?

Under this definition, what does NOT qualify as an asset???

Samuelson

Samuelson believes that the FASB definition that emphasizes future economic benefits (future cash flows) is grounded in future revenues and income measurement. He believes that matching--matching costs against revenues--is the primary focus of this definition. (but remember—revenues are inflows of assets…)

Samuelson believes that the asset definition should concentrate on property rights that are concerned with wealth...and property rights require exchangeability as a feature

Certain deferred charges would be expensed immediately..training costs, relocation costs, plant rearrangement costs, certain pension costs.

Assets...

...What is an Asset, by Walter P. Scheutze, Accounting Horizons, September 1993 (handout)

When he wrote this article, Mr. Scheutze was the Chief Accountant of the SEC.

Last October (1992), after the meeting of the World Congress of Accountants in Washington, DC, the FASB invited standard setters from around the world, and a few other individuals, to meet at the FASB’s offices in Norwalk, Connecticut for a day and a half to share ideas about standard-setting in various countries and at the “international” level. During that conference...I was taken by the lack of agreement on the basic concepts about financial accounting and reporting.

One of those conceptual issues was the definition of an asset. It is clear that one of the major roadblocks to resolving accounting issues here in the United States is lack of agreement on the definition of an asset.

So today I wish to offer, for the consideration of standard setters and others who seek to improve the state of financial accounting and reporting, an alternative definition of an assets. I suggest this alternative definition to be provocative and to stimulate thought and discussion.

“What generally happens in practice, under the FASB’s definition of an asset, is that assets are not recognized unless the reporting enterprise acquires them by paying cash or agreeing to pay cash in the future or someone contributes something to the reporting enterprise in return for an ownership interest in the enterprise.”

Schuetze claims that accountants tend to thing of assets in terms of its cost, not in terms of the asset itself or the future benefit that may flow from it. He gives the example that an when an enterprise discovers something of value, such as oil or gold, it is not recognized as an asset because it has no cost. In other words, the cost defines the asset..

In oil and gas accounting, the asset represented in the balance sheet is the cost of finding the oil and gas reserves, not the reserves themselves...

The cost of many assets does not represent anything close to the “probable future economic benefit” to be derived from the asset.

Defining an asset as a probable future benefit would indicate that if an enterprise owns a truck, the truck per se is not the asset. Rather, the asset is the present value of the cash flows that will come form using the truck.

Users do not see the “truck” as the economic benefit that will come from using the truck.

Similarly, the future benefit of a discovery of mineral deposits generally bears no relationship whatsoever to the costs of finding the deposits,

and the future benefits of successful research and development are not necessarily correlated with the cost of the R&D program.

Scheurtze’s suggested definition...Cash, contractual claims to cash or

services, and items that can be sold separately for cash.

Are there benefits to this definition???

Possible Benefits

“Ordinary” people would understand this definition

It would simplify accounting for assets because the definition is specific and can be easily interpreted (verifiability???)

ComparabilityAfter all, now many of the costs

recognized as assets are not recognized as assets by all enterprises...

Does this alternative definition provide guidance on what measure of cost to use?

Ie., replacement cost, exit value(market value), historical cost, net realizable value, present value of future cash flows...

What does this definition include?

What does this definition EXCLUDE?

Question:

For next time, try to develop your own suggested definition of an asset...

Then what about other Balance Sheet Classifications????

Is Total Assets a meaningful concept?

Liabilities and Stockholders’ Equity

The accounting equation, A = L + OE, highlights the resources the company has and the different interest groups, owners and creditors, who have claims on those assets. Once upon a time, it was not difficult to tell the difference between owners and creditors...

Liabilities

Definition: (Current) Liabilities are probable future sacrifices

of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events (Paragraph 35, CON 6)

Essential Characteristics of Liabilities

Embodies a present duty or responsibility to one or more other entities that entails settlement by probable future transfer or use of assets at a specified or determinable date, on occurrence of a specified event, or on demand

The duty or responsibility obligates a particular entity, leaving it little or no discretion to avoid the future sacrifice

The transaction or other event obligating the entity has already happened (paragraph 36)

Equity

The residual interest in the assets of an entity that remains after deducting its liabilities (Paragraph 49)

Equity stems from ownership rights and involves a relation between an enterprise as owners rather than as employees, suppliers, consumers, lenders, or in some other nonowner role....it is a residual interest: (a) equity is the same as net assets, the difference between the enterprise’s assets and its liabilities, and

(b) equity is enhanced or burdened by increases and decreases in net assets form nonowner sources as well as investments by owners and distributions to owners (paragraph 60)

Inherent in the nature of the ownership in CON 6 is the idea that owners invest in a business with the expectation of benefiting by obtaining a return on their investment if the enterprise is profitable but bear the risk that the enterprise may be unprofitable.

Debt vs. Equity

An essential distinction between debt and equity has been the fact that a liability “embodies obligations to sacrifice future economic benefits by transferring assets or providing a service to another entity in the future, while an equity instrument does not”.

In the past, this statement drew the line between debt and equity, but the the advent of new capital instruments with characteristics of both debt and equity the line has blurred.

Convertible bondsMandatorily redeemable preferred stockNoncontrolling interest in consolidated

subsidiary

Concern of FASB

With the increasing complexity of financial instruments, the current classification in the Balance Sheet of instruments that contain both liability and equity characteristics sometimes results in a lack of representational faithfulness

A second concern is that the Board believes current proposals would enhance convergence with the accounting standards used in other nations.

So what is the current issue??

Liabilities again are currently defined as ...arising from present obligations of a particular entity to transfer assets...

Do you see any problems with this definition???

Obligations that require (or permit at the issuer’s discretion) settlement by issuance of the issuer’s equity shares do not meet the above definition of liabilities because the shares are not assets to the entity

Obligations that settle with equity were classified as equity under the original definition in CON 6.

Can you think of circumstances when the potential issuance of shares would NOT be related to an “ownership relationship” between the issuer and the holder?

(Does Enron ring a bell???)

Think back to the definition of equity...the idea that owners invest in a business

with the expectation of benefiting by obtaining a return on their investment if the enterprise is profitable but bear the risk that the enterprise may be unprofitable.

What if...

the shares to be issued is fixed in terms of value rather than number of shares. What are the risks associated with ownership under these conditions?

While CON 6 requires that obligations settled with equity be classified as equity, the approach FAS 150 places less emphasis on the form of the settlement and looks to the definition and description of equity in CON 6 to assist in determining classification.

The Board has concluded that those obligations should not be classified as equity unless they expose the holder to risks and benefits that are similar to those to which an owner is exposed.

Monetary Value

The notion of monetary value was developed to assist in determining whether the risks of changes in fair value of the issuer’s equity shares to which the holder is exposed are similar to those which a holder of outstanding equity shares is exposed.

If changes in the monetary value of an obligation are caused by, equal to, and in the same direction as changes in the fair value of the issuer’s equity shares throughout the period the obligation is outstanding, the holder of the component is exposed to risks and benefits that are similar to those to which an owner is exposed.

Example

Consider a holder of an obligation that requires settlement by issuance of 1,000 equity shares. If the current fair value of the shares is $20, the monetary value of the obligation is $20,000. If the fair value changes to $21, the monetary value increases to $21,000.

The holder of the financial instrument is exposed to similar risks in changes in fair value as is the holder of the equity shares; an ownership relationship is established and the instrument would be classified as equity.

What would be the application to specific instruments?

Common Stock, Preferred Stock...Preferred Stock that is Mandatorily

Redeemable...LiabilityPreferred Stock that is Mandatorily

Convertible into a Fixed Number of Common Shares--Equity

Preferred Stock that is Mandatorily Convertible into Common shares with a Fixed Dollar Value...liability

Convertible Debt...the basic convertible debt instrument contains (a) an obligation to repay principal (transfer of assets; liability), (b) an obligation to make periodic interest payments (transfer of assets; liability), (c) obligation to issue a fixed number of shares if the conversion is exercised.

How would this be handled under the new statement?

The amounts allocated to the liability component and the equity component are based on their relative fair values at issuance

Callable Convertible Debt...the call option is not treated as a separate component.

The instrument would consist of (a) a callable obligation to repay principal, (b) an obligation to make periodic interest payments, and (c) a callable conversion option exercisable by the holder.

The amount allocated to the conversion option is recorded as equity and the amount allocated to the callable debt is recorded as a liability.

Consolidated Subsidiaries

There has been debate in accounting as to how the noncontrolling interest in a consolidated subsidiary should be reported...as debt or equity, or a category between the two.

Debt

What might make it seem like debt?Vote? Control?Reason for Investment

How About Equity?

Think about the obligations of the corporate entities to the owner and relate this to the definitions of Equity and Debt in the Concepts Statement.

Exposure Draft

Does the new standard answer the question?

The Board did determine that it falls under the current definition of equity and that a new category should NOT be created for the minority interest.

CON 7- Cash Flows

Are Concept Statements GAAP???

Remember, Concept Statements are NOT GAAP. A new Concept Statement is not a new accounting rule and does not require companies to change any of their financial reporting.

So why are concept statements important?

What did we see with the amendment to CON6?

What does that tell us about the importance the Board places on concept statements in the standard setting process?

The last concept statement, CON 6, was published in 1985. No substantial new work was done until recently. Specifically, we now see a proposed amendment to the definition of liabilities and, in February, 2000, CON 7, the first new statement in 15 years.

What does this tell us about the attitude of the current Board toward the Conceptual Framework?

What importance might we attributed to CON 7?

CON 7

Basically, CON 7 states that the time value of money is an important economic fact and accounting should consider it.

What is current practice? Does current GAAP consider the time value of money?

CON 7

CON 7 provides a framework for using future cash flows and present value as the basis for an accounting measurement. The Statement provides general principals governing the use of present value, especially when the amount of future cash flows, their timing, or both are uncertain.

It also provides a common understanding of the objective of present value in accounting measurements.This is the first Concepts Statement to address specific measurements and to articulate a measurement objective.

The Concepts Statement applies to measurements that use cash flow information on the initial recognition of assets or liabilities, in fresh-start measurements, or in interest methods of allocation. It does not address recognition questions, nor does it address when a fresh-start measurement is appropriate.

Objective: To capture, to the extent possible, the economic differences between sets of estimated future cash flows. Because present value distinguishes between cash flows that might otherwise appear similar, a measurement based on the present value of estimated future cash flows provides more relevant information than a measurement based on the undiscounted sum of those cash flows.

The Board concluded that to be relevant in financial reporting, present value measurements must represent some observable measurement attribute of assets and liabilities. Present value measurements should attempt to capture the elements that taken together would comprise fair value; that is, a market price, if one existed.

The Concepts Statement describes techniques for estimating cash flows and interest rates, the role of risk and uncertainty, and the application of present value in the measurement of liabilities.

Industry Perspective

It’s about time! AIMR (Association for Investment Management and Research) “strongly supports the proposed Concepts Statement. We expect that it will enrich financial accounting and reporting. We agree with the objective of the present value approach, to “imitate, to the extent possible, the market’s behavior toward risky assets and liabilities;”

In other words, the new system is an attempt “to imitate the pricing system.”

AIMR believes “present values should be used in financial statement whenever and wherever streams of future cash flows are used to measure assets or liabilities. When dealing with uncertainty, the use of expected values (i.e. probability of expected cash flows) would be a vast improvement.

Implementation Questions

What is the appropriate discount rate?Should the treatment for liabilities be

fundamentally different form the treatment for assets?

Does it make sense in discounting liabilities to use a discount rate lower than the risk-free rate?

Is there a place for the notion of “entity specific” value?

Unfair Value

Dennis Beresford, former Chair of the FASB, in Barrons, May 21, 2001

Beresford believes that the issues in CON 7 may distort information.

Beresford agrees that it is hard to argue that a dollar to be received or paid five years from now has the same worth as a dollar in your pocket today.

But CON 7 goes beyond present values and states that conceptually, companies should record liabilities at “fair value.”

What is the difference between present value and fair value?

When might the difference between “present value” and “fair value” matter?

When a company purchases goods or services at a stated price, the liability it incurs represents fair value, and no accounting issue arises.

But some obligations are recorded for accounting purposes based on estimated amounts that will be expended in some future period..such as warranties.

Assume ABC Company sells a product that includes a full warranty for three years from the date of sale.

What might we expect about the pattern of warranty costs? Would they be equally spread over the 3-year period?

If not, how should that be recorded?Current GAAP does not consider the time

value of money. Rather, the entire estimated future cost of the warranty is accrued at the date of sale and matched against revenue.

Revenue from the sale, cost of manufacturing the product, and estimated warranty cost are included in the same financial statement, and the timing of warranty expenditures is not considered.

CON 7 Implications

Should a lower, time-value adjusted expense for warranties be accrued, with a related liability?

An additional interest expense would be recorded in later years to recognize the amount actually expected to be paid for warranty repair.

Does this make sense conceptually?Is this something that a “prudent user” is

likely to understand? Beresford suggests that recording additional warranty expense in later years does recognize the time value of money, but might be confusing for some users.

Present Value vs. Fair Value

But instead of the present value of the expected cash flows, CON 7 calls for “fair values”…that is, a “market price”.

Does this mean that the warranty obligation should be priced at what the competition might charge for a similar repair, or the cost that ABC would actually incur given their parts and labor markets?

Should profit be recognized on warranty repair, or is that implicit in the sale?

IF ABC spends on average $25 on a warranty repair, but the competition charges $35, how much should be accrued? CON 7 seems to imply $35 should be accrued.

What implications might this have for earnings management???

While the warranty example is hypothetical, the FASB is working on some projects that can be expected to incorporate the concept of fair value.

Asset Retirement Obligations

Expected cost to decommission nuclear power plants, take offshore oil drilling platforms out of service, and other future events that are certainly going to happen but for which the costs are not at all certain. The FASB recently reconfirmed it earlier decision to require these obligations to be recorded at FMV instead of at a company’s own expected cost.

Impairment of PPE

While not the principal issue, part of this proposal focuses on recording certain liabilities at FMV

Liabilities

The Board’s thinking on accounting for financial instruments calls for companies to record bonds and similar debt instruments at FMV.

Thus, a company in financial difficulty that experiences a sharp decline in its credit rating would reduce its liability to the amount that market participants are currently willing to pay. This would result in recognizing a GAIN as the credit rating declines, and a later LOSS if the full face value were paid…in other words, gains for deteriorating results and losses for improvements!

Beresford claims that the Board is focused on “getting the balance sheet right”, but that the result would be that income statements would be potentially misleading.

And these issues all deal with loss contingencies.

What about gain contingencies????(Conservatism… “Fair Disclosure” ...

Relevance)

Income Determination

What does our discussion of the definition of assets, liabilities, and equity mean for income determination?

What is the relationship between the Balance Sheet and the Income Statement?

What possible theories of income determination can you identify?

Matching

Current definition of revenues: Inflows (or enhancements) of assets or settlement of liabilities during a period from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations.

Expenses: Outflows or other using up of assets or incurrences of liabilities during a period from delivering or producing goods, rendering services, or carrying out other activities that constitute the entity’s ongoing major or central operations.

Revenue Recognition: Revenue is generally recognized when realized or realizable and earned...the entity has substantially accomplished what it must do to be entitled to the benefits represented by the revenues.

Matching: Efforts should be matched with accomplishment whenever it is reasonable and practicable to do so.

How well does this concept of income fit with the current emphasis on assets and liabilities?

Is there another theory of income determination that might be considered?

Capital Maintenance

You have no income or loss if you have maintained capital…that is, stockholder’s equity remains unchanged.

What does this mean from a traditional accounting perspective?

How about from an economic perspective?

Wealth Effects

IF your net assets (stockholders’ equity) increases, you have had an increase in wealth, and that is another measure of net income.

How should net assets be measured?

What are the problems with historical cost measurement of wealth?

What do we gain by considering current costs?

What are the problems and weaknesses?

Unrecorded assets (valuation of intangibles!)

Hard to measure wealth as changes in net assets if we do not record all assets.

Is there more than one measure of fair value that might be used?

Cost to firm, competitor’s price..How does this relate to cash flows?

Opportunity costs?What are the measurement issues? Are

there industry effects under our traditional accounting model?

Information and Users

Our primary users, according to CON2, are prudent investors, creditors, and those who advise them...

The SEC believes that quality, transparent financial accounting information is critical to the health of our financial markets.

Expectations Gap..

There seems to be a difference between expectations of many of our users and what accounting and auditing information actually are meant to communicate

There is an expectations gap in auditing. Too often, people believe that audited financial statements are guaranteed to be accurate and free from fraud.

The real scope of the audit and the meaning of the audit report are poorly understood.

The profession changed the wording of standard audit reports more than 10 years ago, but the perception of the public does not seem to have changed.

Similarly, there seems to be an expectations gap with respect to financial reporting in that users do not seem to understand the limitations of financial accounting information, the requirements of GAAP, or the limitations in predicting future results based on current reports.

There are significant challenges to the profession because of this “mismatch” between reality and expectations.

The stature of the profession has erodedLawsuits have become much more

prevalent

Strike Suits

When a company lacks quality accounting, or communication is poor, the threat of a security lawsuit increases dramatically.

Security lawsuits (often called strike suits) charge company officers or directors with fraudulently misleading shareholders.

Although strike suits are sometimes warranted, abuse of the strike suit be stockholders and attorneys has become increasingly prevalent.

Plaintiffs claim that fraud is common in today’s stock market and point to many examples of accounting restatements and trading by corporate insiders while a fraud was allegedly alive in the market. Defendants claim that honest conduct in volatile markets is often mistaken for fraud.

What triggers a strike suit?

A significant decline in stock pricea positive statement by management

followed by a drip in the stocksale of a large portion of stock by

company officials preceding a dropAn unexpected negative statement by

management (i.e.., Cisco’s inventory write-off)

According to one source (http//www.upside.com/texis/mvm/story?id=34712c157b) a strike suit is likely to be filed any time a company’s stock falls more than 20%.

Strike suits often accuse management of announcing a positive event to inflate the stock value, “misleading” investors so that they invest at “inflated” values and then suffering a loss when the “truth” becomes apparent.

Similarly, strike suits may accuse management of not properly informing stockholders on a timely basis when there is bad news.

Often, sales of stock by company management is pointed to as evidence of fraudulent activity

However, given the popularity of stock options, the regular trading in a company’s stock by members of management is not uncommon.

In 1988, a Supreme Court ruling increased the ease of filing securities suits. This caused a dramatic increase in the number of suits filed.

As the number of suits have increased, so has the number of complaints that the suits are frivolous. Strike suits may be filed without any strong standard of evidence, and even the Second Federal Circuit Court (which is the jurisdiction for Wall Street) only requires that plaintiff’s show “motive and opportunity” to commit fraud.

Congress tried to make frivolous suits more difficult to file by passing the Private Securities Litigation Reform Act (PSLRA) in 1995. However, within a year of passing the law, the number of suits actually increased.

According to the Stanford University Securities Class Action Clearinghouse, 1,044 issuers have been named in federal class action securities fraud lawsuits since 1995. In 2000, 211 strike suits were filed. Already in 2001, 105 suits have been filed.

These numbers mean that on average, one new strike suit is filed every day the stock market is open.

The PSLRA tried to increase the requirements to file a strike suit by a providing “safe harbor” for forward-looking statements. The Act also stated that plaintiffs must demonstrate “a strong inference” by company officials to commit fraud, and that these officials must exhibit “recklessness”.

However, these terms were not carefully defined and the Courts have offered different interpretations. It may eventually be considered by the Supreme Court.

Since the PSLRA, a larger percentage of litigation activity centers on allegations of accounting fraud, with revenue recognition issues emerging as a particularly significant cause of litigation. A larger percentage of litigation activity also alleges trading by corporate insiders during periods when frauds are allegedly “alive” in the market.

Costs of Strike Suits

In 1996, the sole cost of defense resulted in an average loss of $4 million per company sued. IN 1996, the average settlement was $8.2 million, which, if there is significant insurance coverage, is less costly than the court defense.

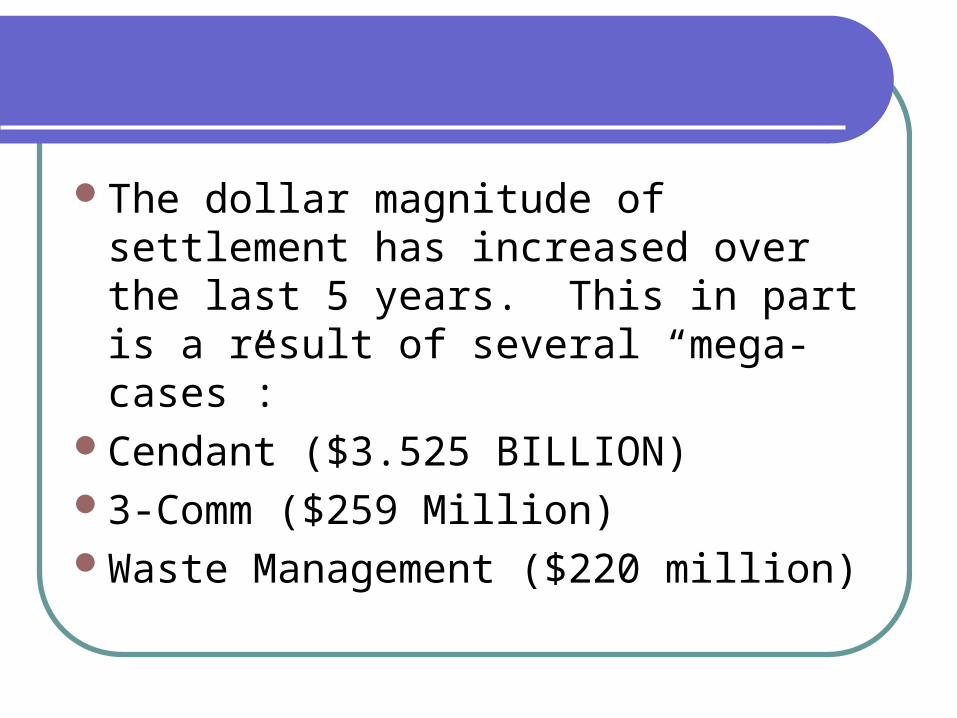

The dollar magnitude of settlement has increased over the last 5 years. This in part is a result of several “mega-cases”:

Cendant ($3.525 BILLION)3-Comm ($259 Million)Waste Management ($220 million)

A tale of one law firm...

Milberg, Weiss, and one of its principals, William Lerach, is one of the most aggressive firms with respect to lawsuits.

In the past 25 years, Milberg Weiss has collected more than $5 billion in judgments and out-of-court settlements from publicly traded companies.

Though $5 billion averages out to $200 million a year over 25 years, the firm recovered $1 billion in the two-year period 1994/95.

There have been as many strike suits filed in the last decade as in the previous 40 years combined. Some feel that Milberg, Weiss is the driving force behind this trend.

While there have been newsworthy mega-suits, a disturbing trend has emerged in the types of companies commonly hit with strike suits. Small firms, particularly high-tech companies, are prime targets for strike suits at least in part because of the volatility of their stock prices.

At least one authority believes “These lawsuits, disruptive and costly for corporations of all sizes, can destroy smaller companies that don’t have the resources to fight.”

Strike suits potentially are a high cost with respect to the entrepreneurial environment.

Another devastating cost is paid by shareholders. The strike suit indirectly impedes a corporation’s willingness to disclose information to users.

An editorial in Business Week states, “They [stockholders] need more information, not less, to protect themselves from stock fraud.

And in today’s environment, even the charge of accounting irregularities, whether or not there is a basis for the charge, can cause a company’s stock price to collapse while simultaneously limiting the availability of alternative sources of capital.

Further, to the extent that suits may be frivolous, it seems like they encourage the expectations gap in financial reporting information and potentially harm the credibility of the accounting profession...