the art economy of remote australia

TRANSCRIPT

The Art Economy

of Remote Australia

CRC for Remote Economic Participation

Aboriginal and Torres Strait Islander Art Economies Project

Tim Acker, Curtin University

Introduction

Ninti One: research, innovation and community

development in remote Australia.

Ninti One manages the CRC-REP.

Aboriginal and Torres Strait Islander Art Economies

Project: 2011 > 2016

• 8 researchers/students

2

Who?

Value chains: Dr Alice Woodhead

Art Centre sustainability: PhD – Kim Petersen

Art Centre enabling environment: PhD – Susan

Congreve

Buyer behaviour: Masters – Jessica Booth

E-commerce in Art Centres: Honours – Iris Bendor

Art Centre human resources: Honours – Michelle

Whittle

Art Outside Art Centres: Dr Lisa Stefanoff and others

3

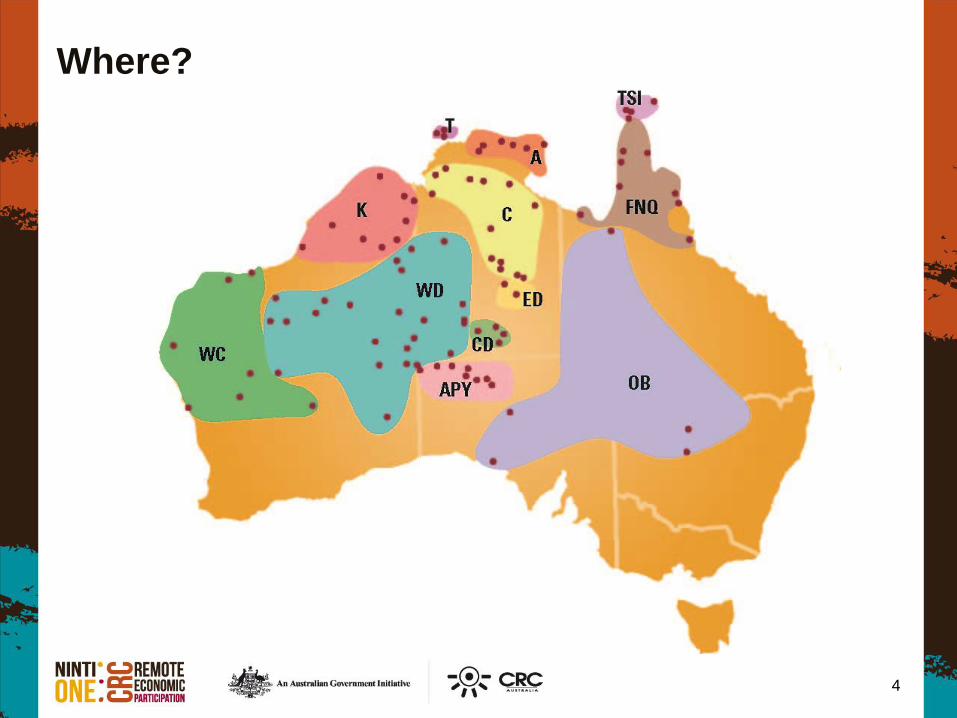

Where?

4

Art Economies Value Chain Project (AEVC)

Understand production and sale of remote-area art.

Aim: enable change and inform artists + art business.

Senate inquiry recommendation.

Value chain analysis: economic not cultural focus.

Primary market focus.

Complicated value chain + cross cultural factors.

Incorporate variability.

Six reports reflecting remote Aboriginal and Torres Strait

Islander art supply chain.

5

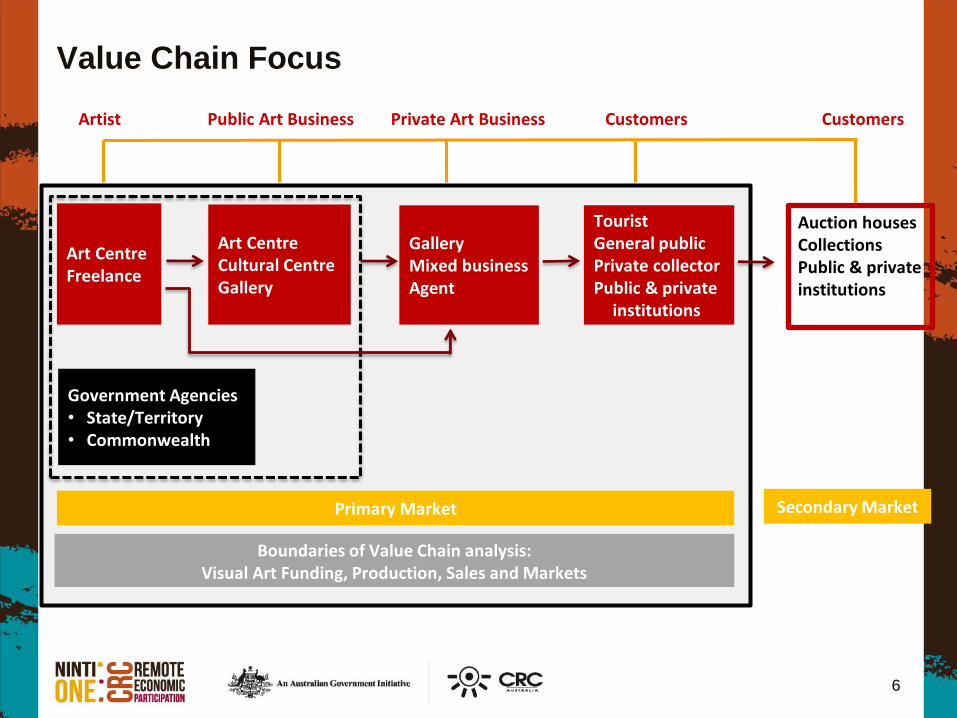

Value Chain Focus

6

Artist Public Art Business Private Art Business Customers Customers

Art Centre Freelance

Art Centre Cultural Centre Gallery

Gallery Mixed business Agent

Tourist General public Private collector Public & private

institutions

Government Agencies • State/Territory • Commonwealth

Auction houses Collections Public & private institutions

Boundaries of Value Chain analysis: Visual Art Funding, Production, Sales and Markets

Primary Market Secondary Market

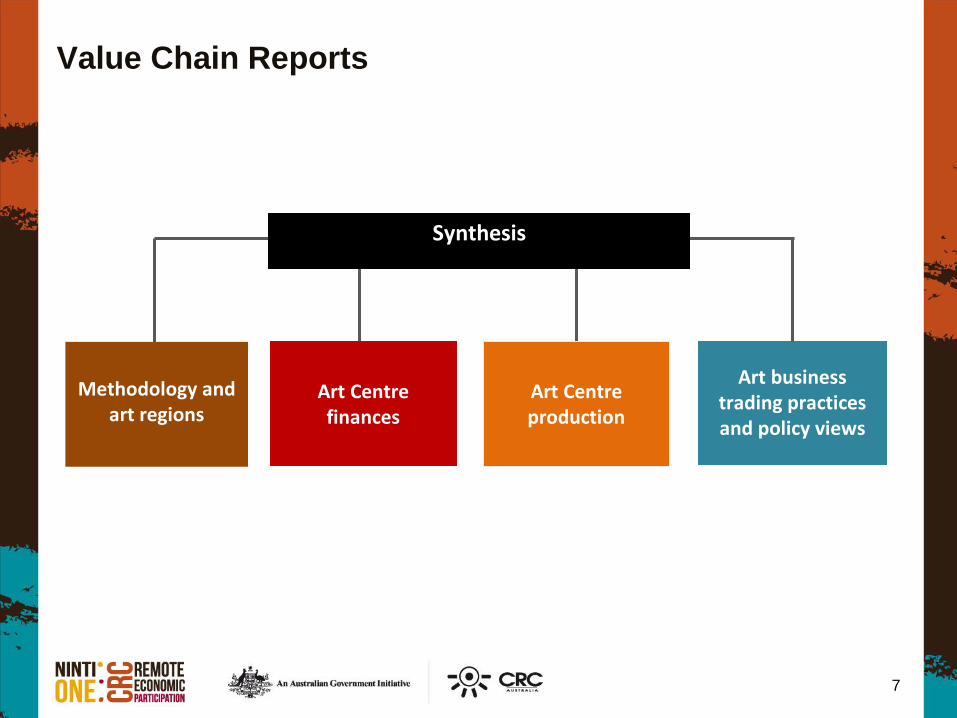

Value Chain Reports

7

Art Centre finances

Art business trading practices and policy views

Methodology and

art regions

Art Centre production

Synthesis

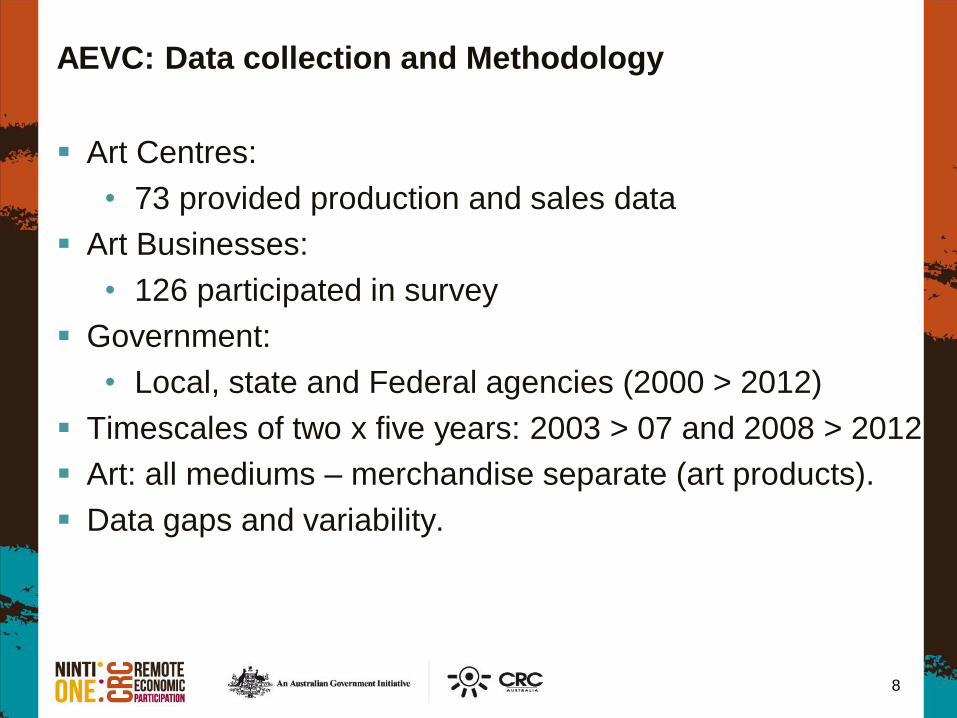

AEVC: Data collection and Methodology

Art Centres:

• 73 provided production and sales data

Art Businesses:

• 126 participated in survey

Government:

• Local, state and Federal agencies (2000 > 2012)

Timescales of two x five years: 2003 > 07 and 2008 > 2012

Art: all mediums – merchandise separate (art products).

Data gaps and variability.

8

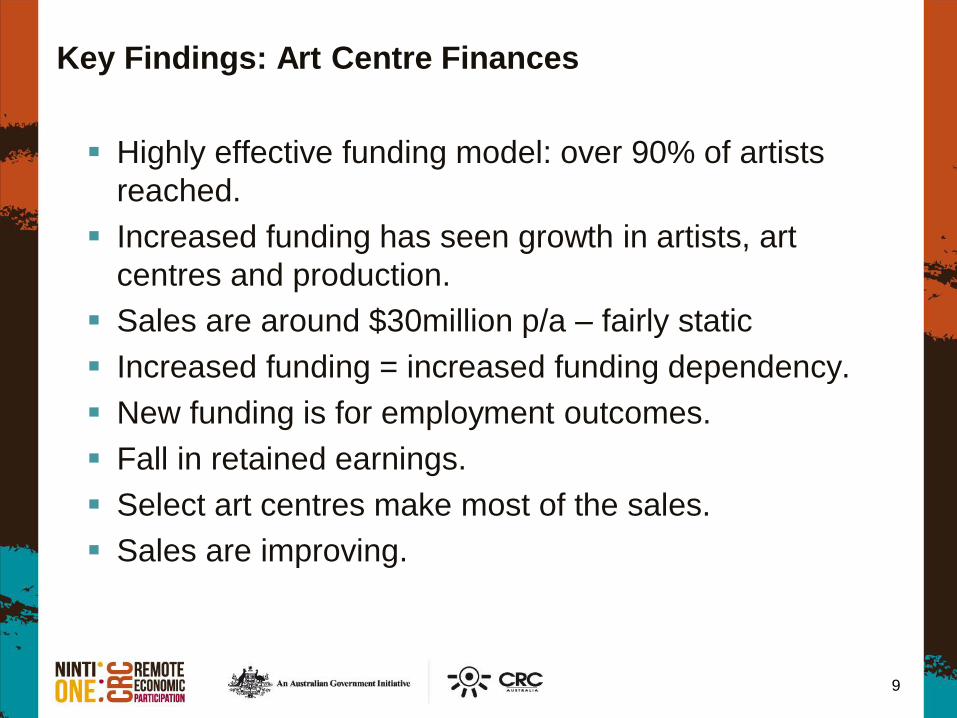

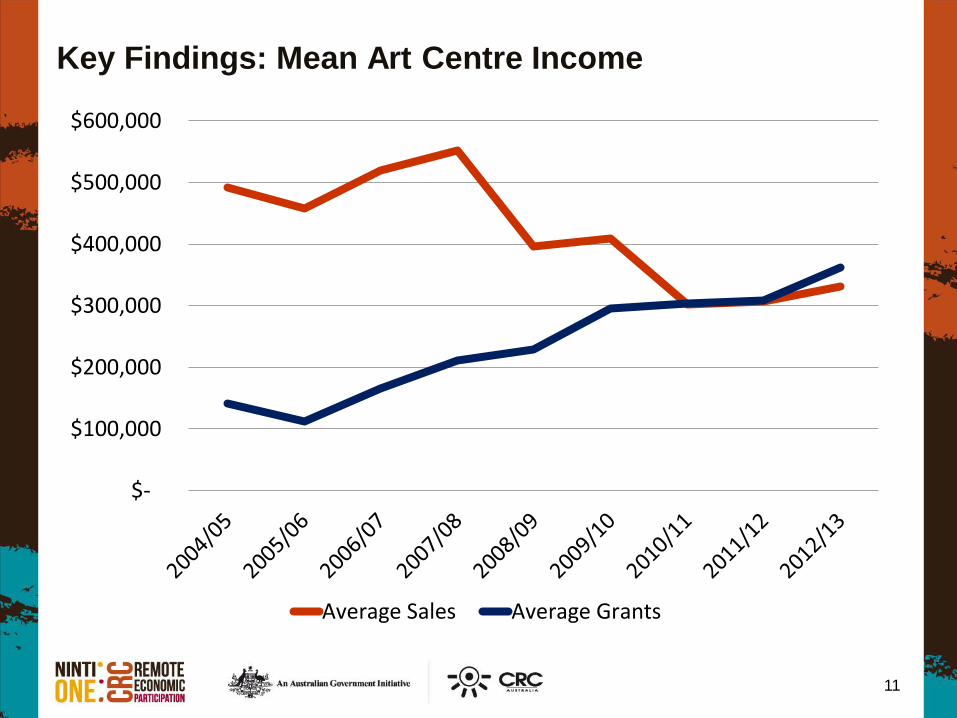

Key Findings: Art Centre Finances

Highly effective funding model: over 90% of artists

reached.

Increased funding has seen growth in artists, art

centres and production.

Sales are around $30million p/a – fairly static

Increased funding = increased funding dependency.

New funding is for employment outcomes.

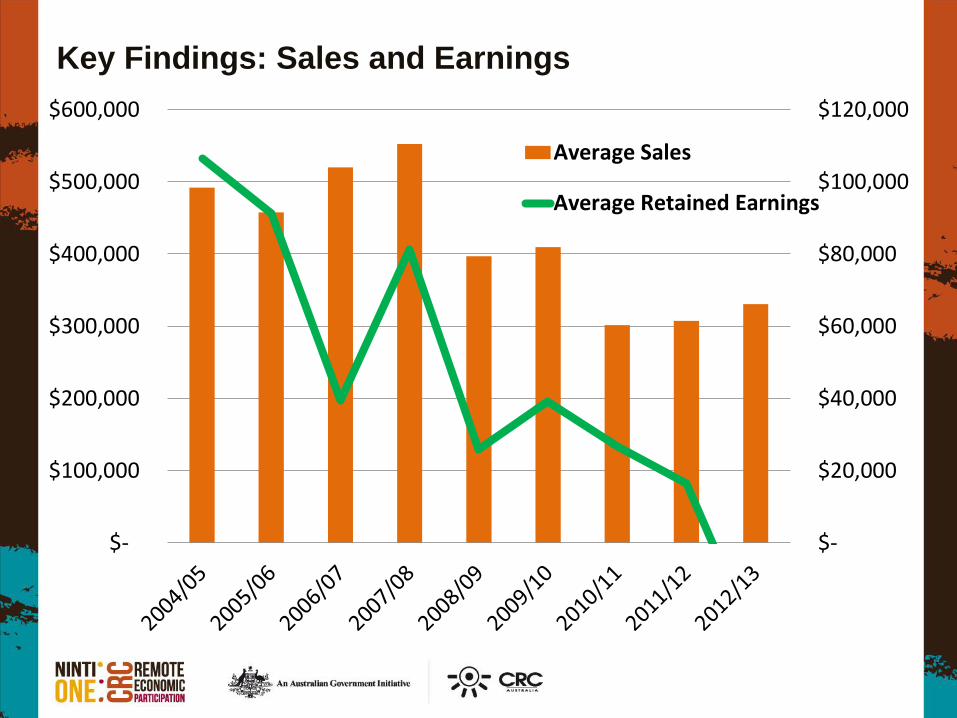

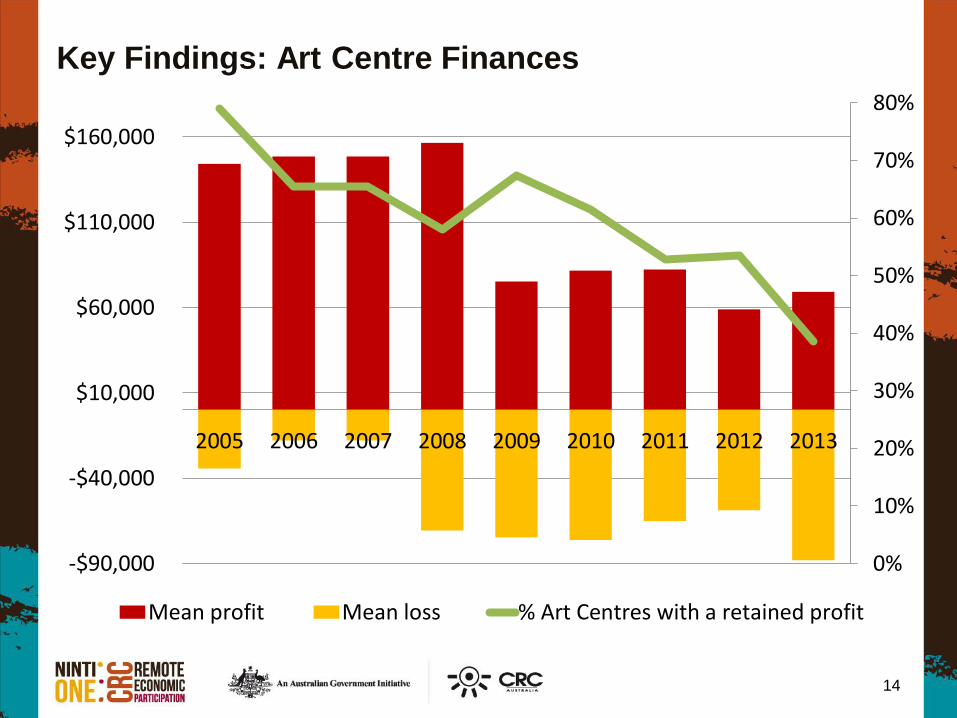

Fall in retained earnings.

Select art centres make most of the sales.

Sales are improving.

9

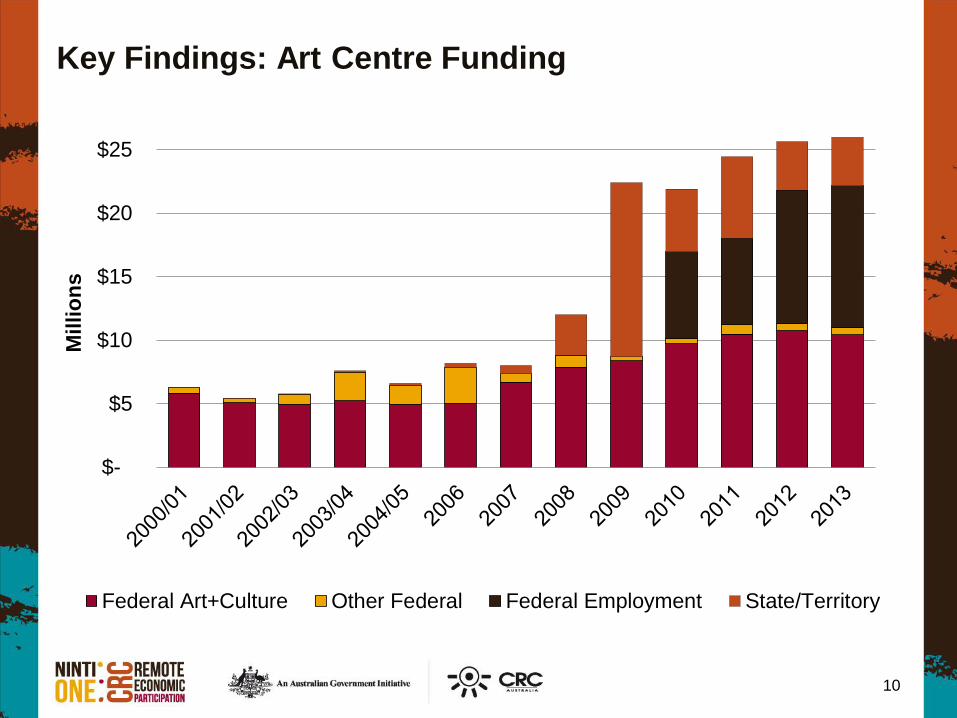

Key Findings: Art Centre Funding

10

$-

$5

$10

$15

$20

$25

Millio

ns

Federal Art+Culture Other Federal Federal Employment State/Territory

Key Findings: Mean Art Centre Income

11

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

Average Sales Average Grants

$-

$100,000

$200,000

$300,000

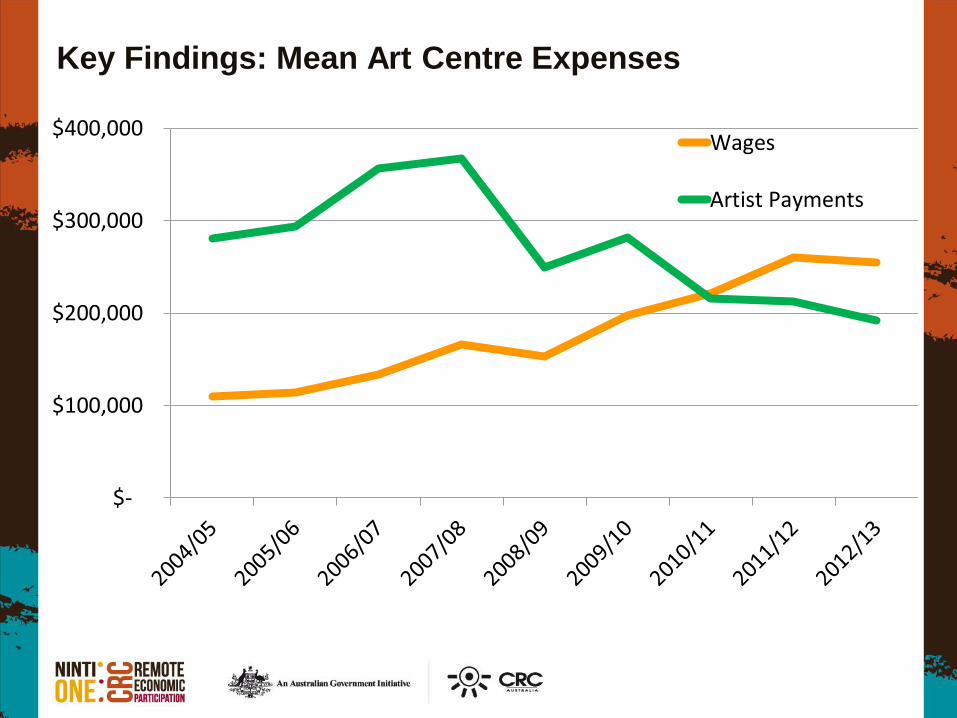

$400,000Wages

Artist Payments

Key Findings: Mean Art Centre Expenses

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

Average Sales

Average Retained Earnings

Key Findings: Sales and Earnings

Key Findings: Art Centre Finances

14

0%

10%

20%

30%

40%

50%

60%

70%

80%

-$90,000

-$40,000

$10,000

$60,000

$110,000

$160,000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Mean profit Mean loss % Art Centres with a retained profit

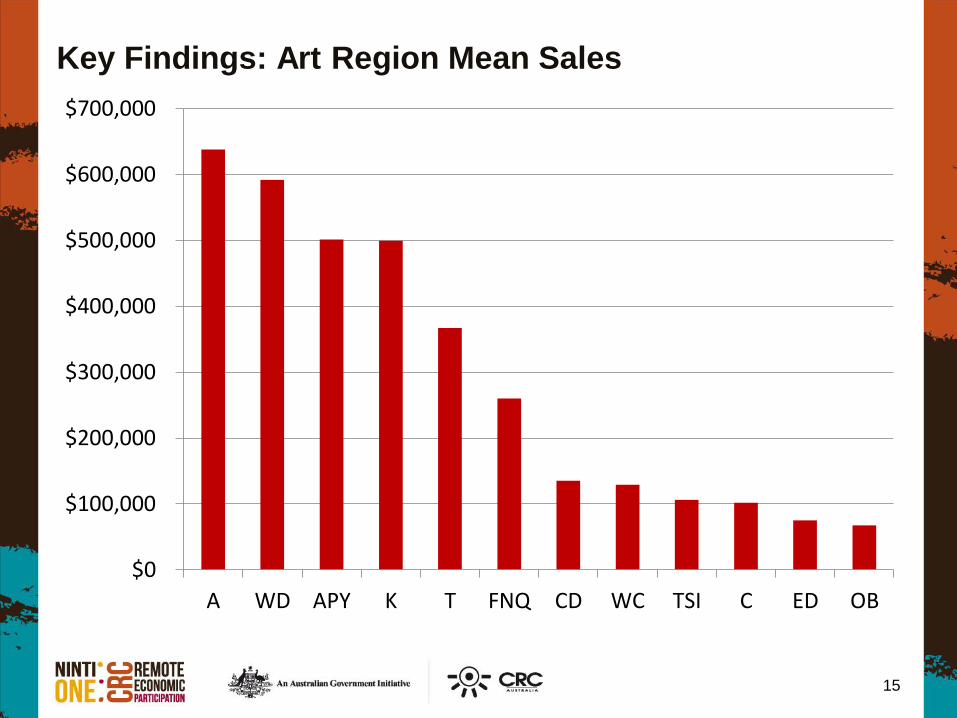

Key Findings: Art Region Mean Sales

15

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

A WD APY K T FNQ CD WC TSI C ED OB

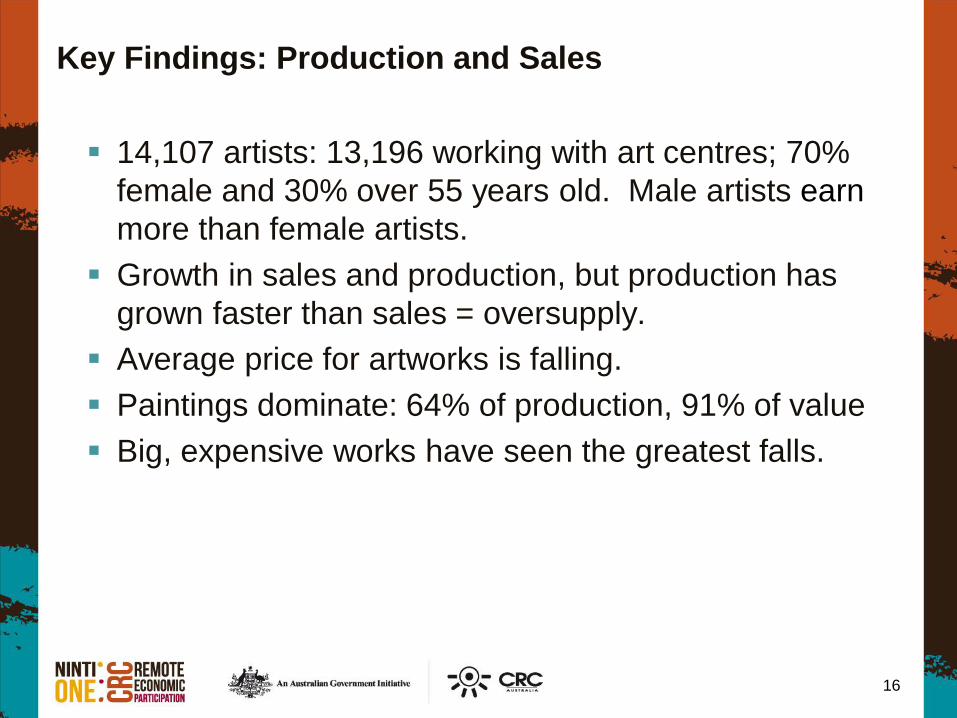

Key Findings: Production and Sales

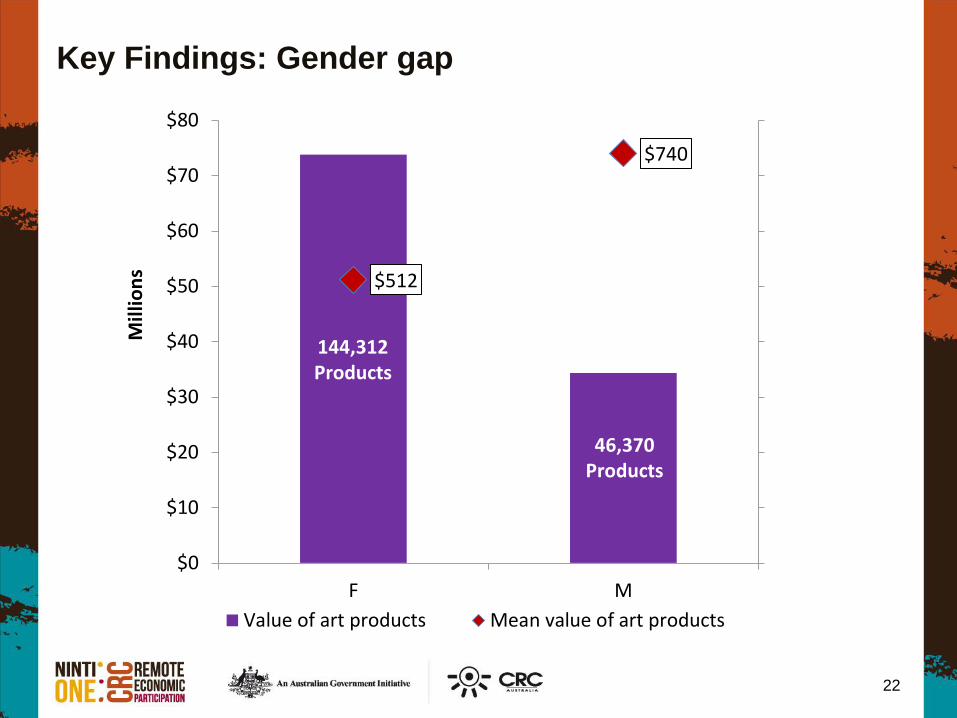

14,107 artists: 13,196 working with art centres; 70%

female and 30% over 55 years old. Male artists earn

more than female artists.

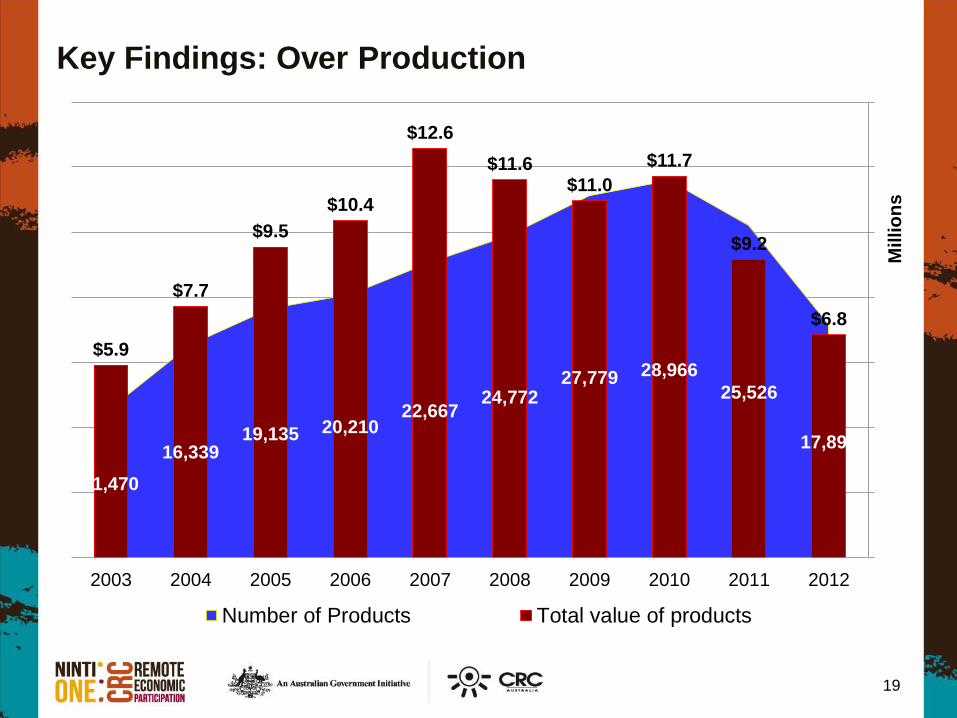

Growth in sales and production, but production has

grown faster than sales = oversupply.

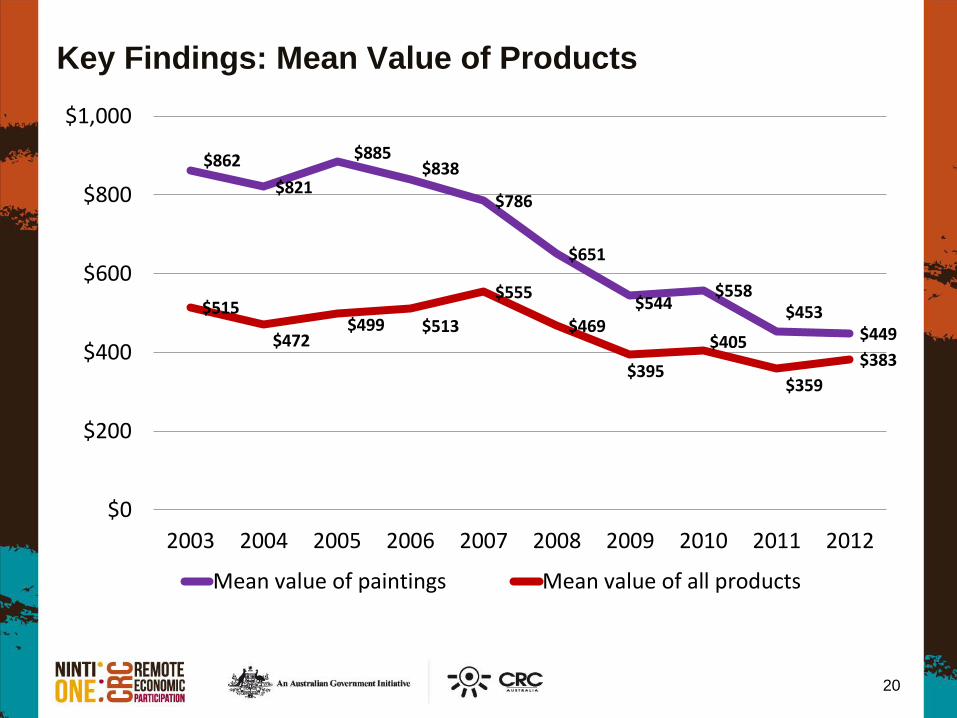

Average price for artworks is falling.

Paintings dominate: 64% of production, 91% of value

Big, expensive works have seen the greatest falls.

16

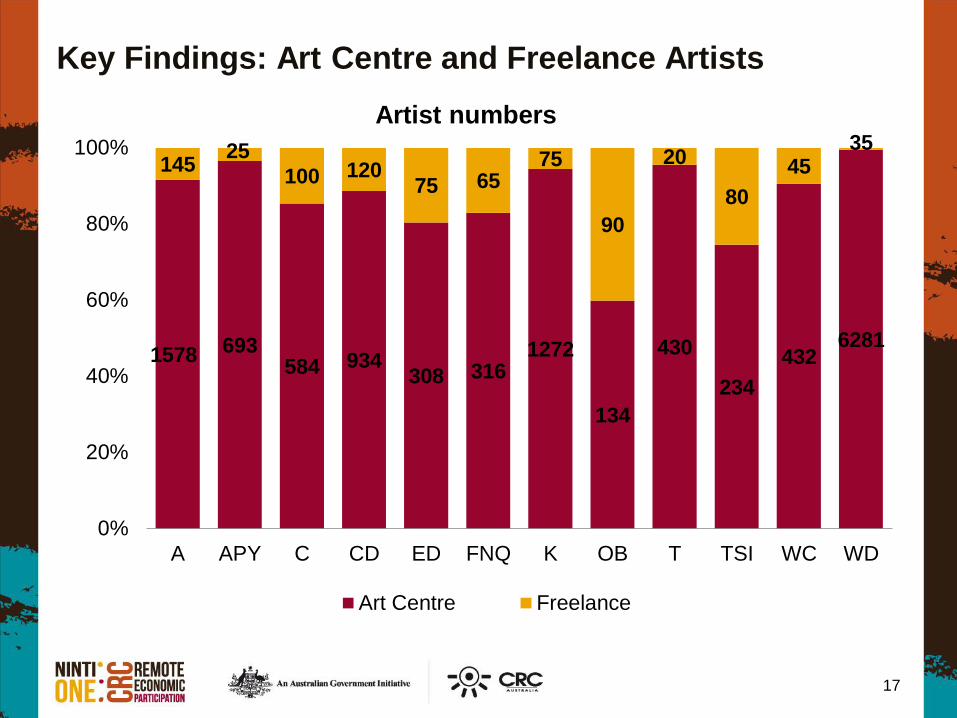

Key Findings: Art Centre and Freelance Artists

17

1578 693 584 934

308 316 1272

134

430

234

432 6281

145 25

100 120 75 65

75

90

20

80

45 35

0%

20%

40%

60%

80%

100%

A APY C CD ED FNQ K OB T TSI WC WD

Artist numbers

Art Centre Freelance

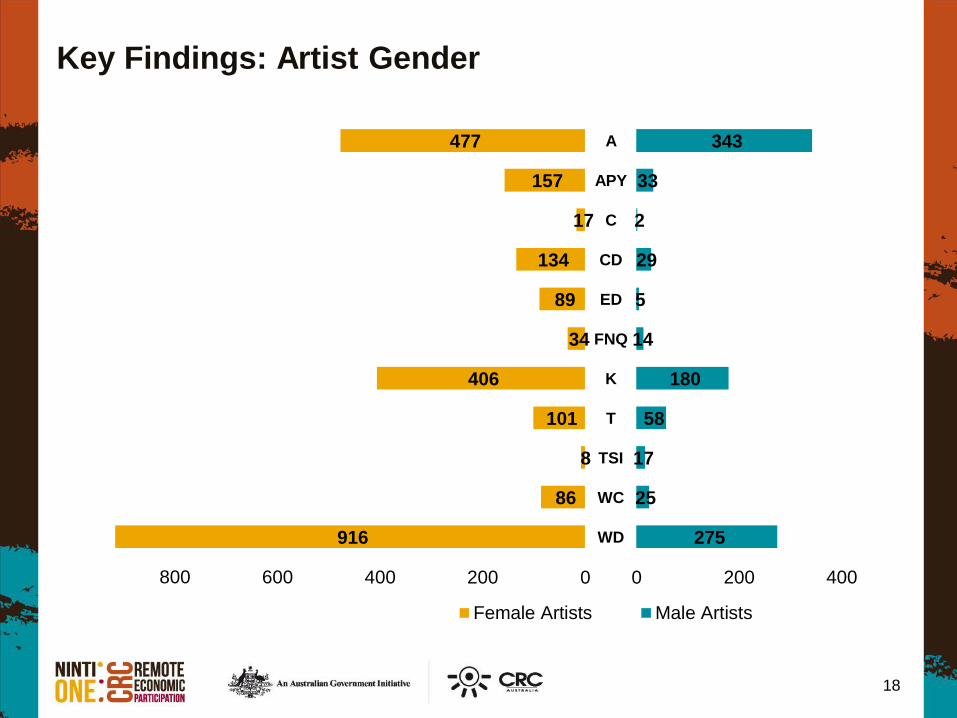

Key Findings: Artist Gender

18

916

86

8

101

406

34

89

134

17

157

477

WD

WC

TSI

T

K

FNQ

ED

CD

C

APY

A

275

25

17

58

180

14

5

29

2

33

343

800 600 400 200 0 0 200 400

Female Artists Male Artists

Key Findings: Over Production

19

11,470

16,339 19,135 20,210

22,667 24,772

27,779 28,966

25,526

17,890

$5.9

$7.7

$9.5

$10.4

$12.6

$11.6 $11.0

$11.7

$9.2

$6.8

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Millio

ns

Number of Products Total value of products

Key Findings: Mean Value of Products

20

$862

$821

$885 $838

$786

$651

$544 $558

$453 $449

$515

$472 $499 $513

$555

$469

$395

$405

$359

$383

$0

$200

$400

$600

$800

$1,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Mean value of paintings Mean value of all products

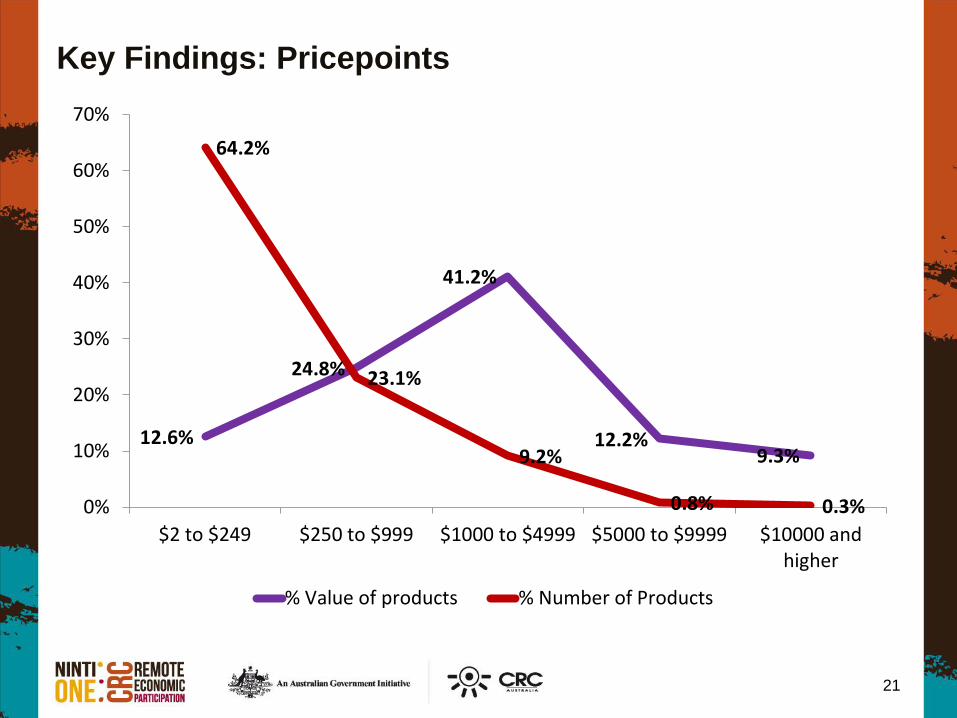

Key Findings: Pricepoints

21

12.6%

24.8%

41.2%

12.2% 9.3%

64.2%

23.1%

9.2%

0.8% 0.3% 0%

10%

20%

30%

40%

50%

60%

70%

$2 to $249 $250 to $999 $1000 to $4999 $5000 to $9999 $10000 andhigher

% Value of products % Number of Products

Key Findings: Gender gap

22

$512

$740

$0

$10

$20

$30

$40

$50

$60

$70

$80

F M

Mil

lion

s

Value of art products Mean value of art products

144,312 Products

46,370 Products

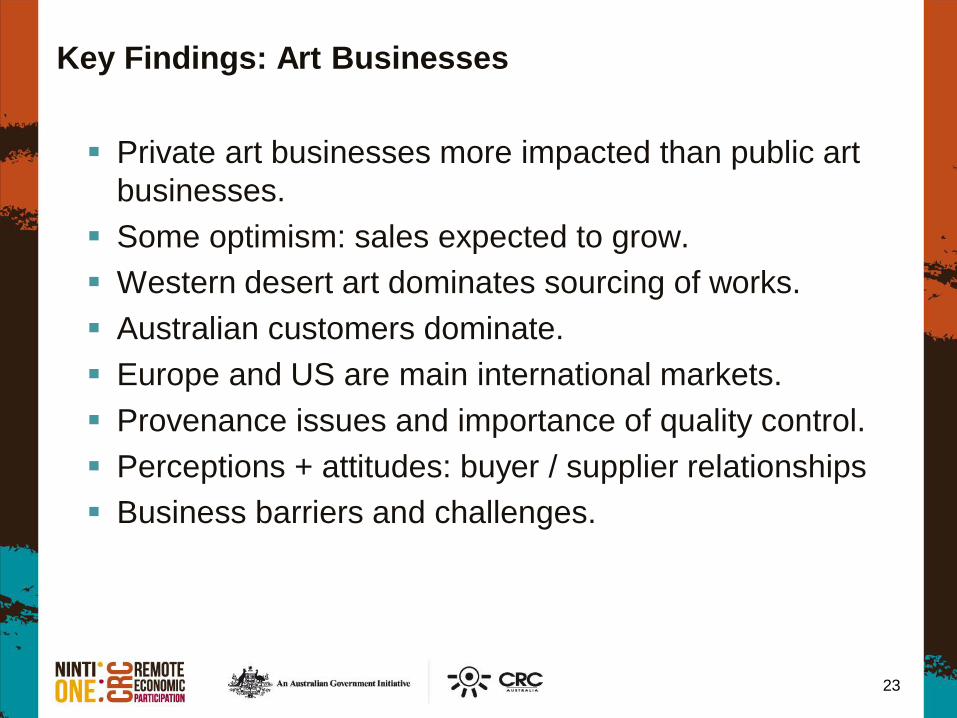

Key Findings: Art Businesses

Private art businesses more impacted than public art

businesses.

Some optimism: sales expected to grow.

Western desert art dominates sourcing of works.

Australian customers dominate.

Europe and US are main international markets.

Provenance issues and importance of quality control.

Perceptions + attitudes: buyer / supplier relationships

Business barriers and challenges.

23

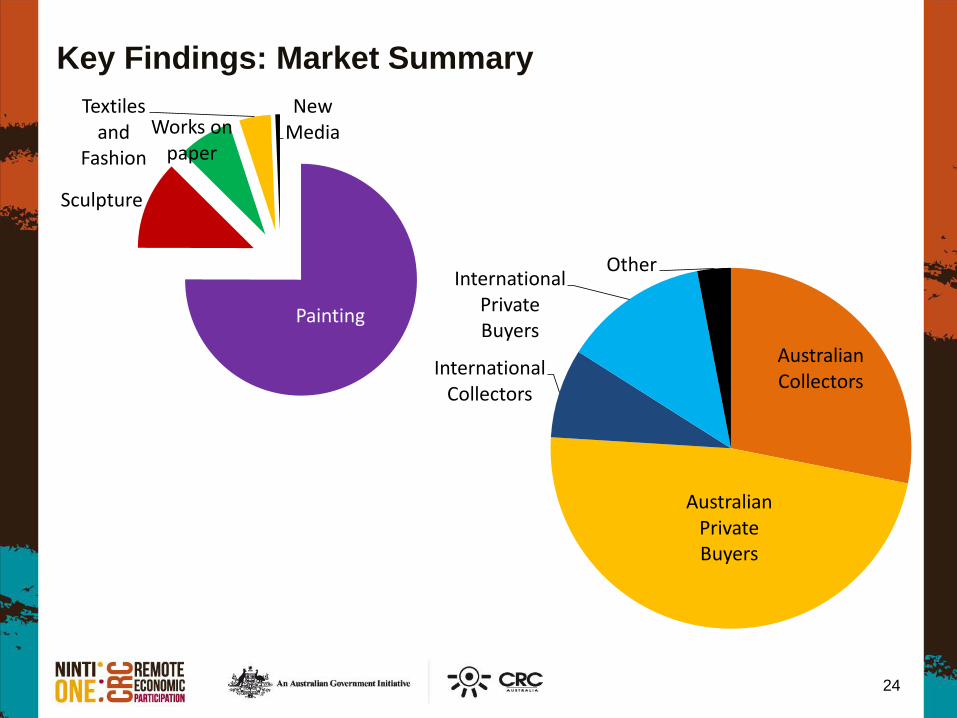

Key Findings: Market Summary

24

Painting

Sculpture

Works on paper

Textiles and

Fashion

New Media

Australian Collectors

Australian Private Buyers

International Collectors

International Private Buyers

Other

Key Findings: International Markets

25

0%

5%

10%

15%

20%

25%

USA/Canada France Germany Rest ofEurope

UK Asia NZ

% o

f to

tal m

arke

t

2008/ 12 2012/16

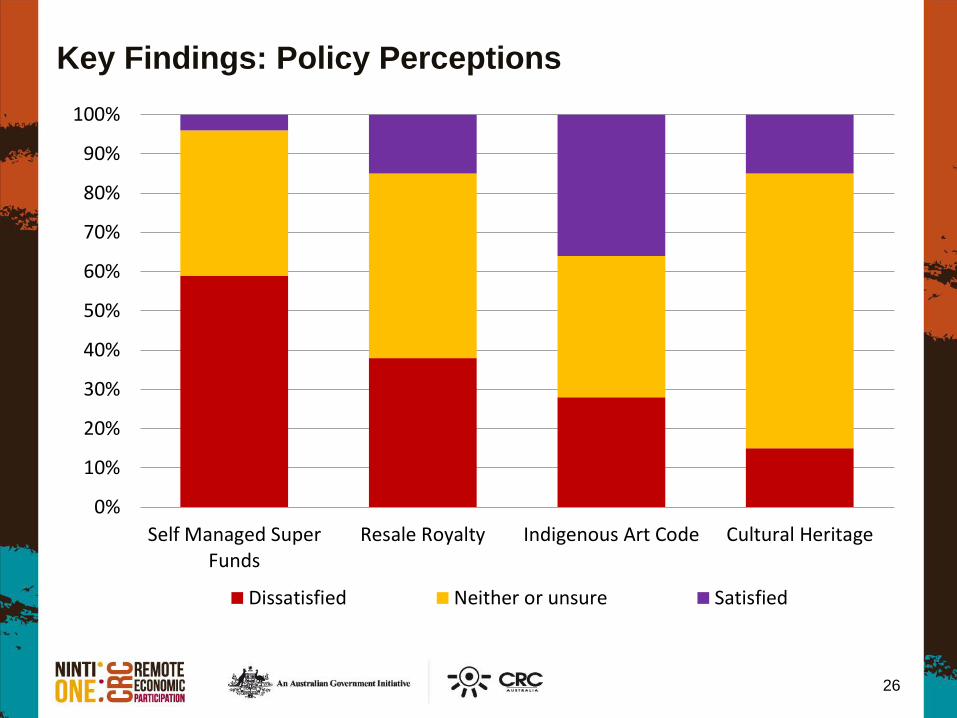

Key Findings: Policy Perceptions

26

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Self Managed SuperFunds

Resale Royalty Indigenous Art Code Cultural Heritage

Dissatisfied Neither or unsure Satisfied

Value Chain Project: Informing and Advocating

Outreach for end-users.

Recommendations/Implications

For artists

For art centres

For other art businesses

For peak bodies

For policy makers/funders

For the research community

27

Project Outputs

Reports and other publications:

• http://crc-rep.com/research/enterprise-

development/aboriginal-and-torres-strait-islander-

art-economies/project-outputs

Art Atlas:

• http://www.users.on.net/~s.moyle/Art_Atlas_Financi

als/atlas.html

28

Other Research Topics

Art Centre sustainability: Kim Petersen

Art Centre enabling environment: Susan

Congreve

Buyer behaviour: Jessica Booth

E-commerce in Art Centres: Iris Bendor

Art Centre human resources: Michelle Whittle

Artsworker employment: various.

Art Outside Art Centres: Dr Lisa Stefanoff and

others

29

30