the agenda for financial sector reform in sub-saharan africa thorsten beck

TRANSCRIPT

The agenda for financial sector reform in Sub-Saharan Africa

Thorsten Beck

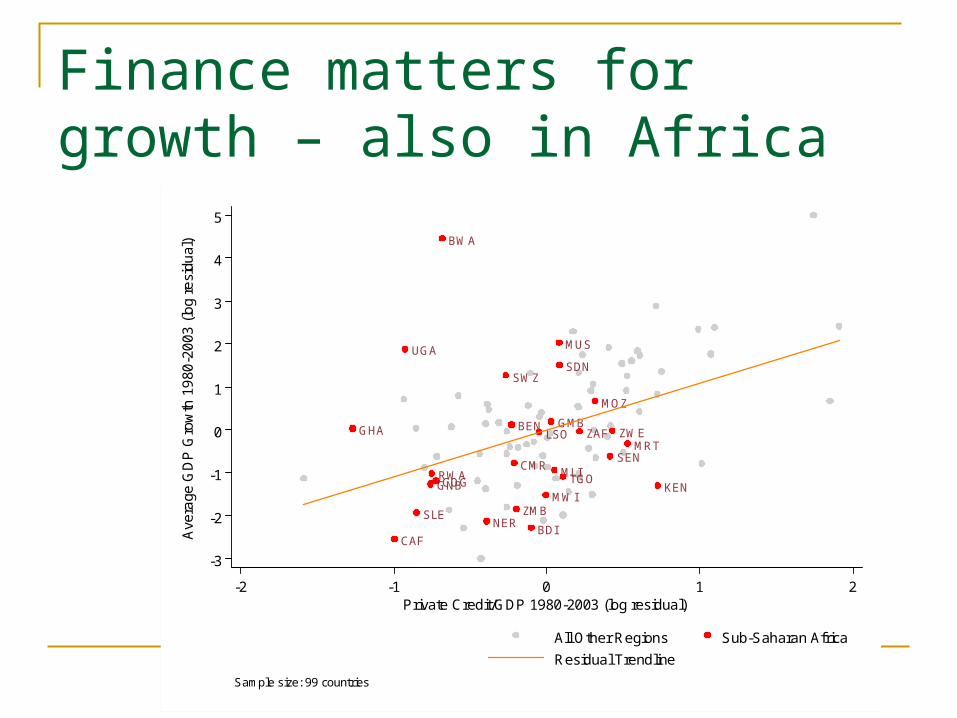

Finance matters for growth – also in Africa

BDI

BEN

BWA

CAF

CMR

COG

GHAGMB

GNB KEN

LSO

MLI

MOZ

MRT

MUS

MWI

NER

RWA

SDN

SEN

SLE

SWZ

TGO

UGA

ZAF

ZMB

ZWE

-3

-2

-1

0

1

2

3

4

5

Ave

rage

GD

P G

row

th 1

980

-20

03 (

log

resi

dual

)

-2 -1 0 1 2

Private Credit/GDP 1980-2003 (log residual)

All Other Regions Sub-Saharan Africa

Residual Trendline

Sample size: 99 countries

Finance is also pro-poor

BWA

BFA

BDI

CMR

CIV

ETH

GMB

GHA

KEN

LSO

MDG

MWI

MLIMRT

NER

NGA

RWA

SEN

ZAFUGA

ZMB

ZWE

-0.20

-0.10

0.00

0.10

0.20R

esid

uals

-2.00 -1.00 0.00 1.00 2.00

Residuals

Sub-Saharan Africa

All Other Regions

Sample size: 68 countriesTime period: Source:

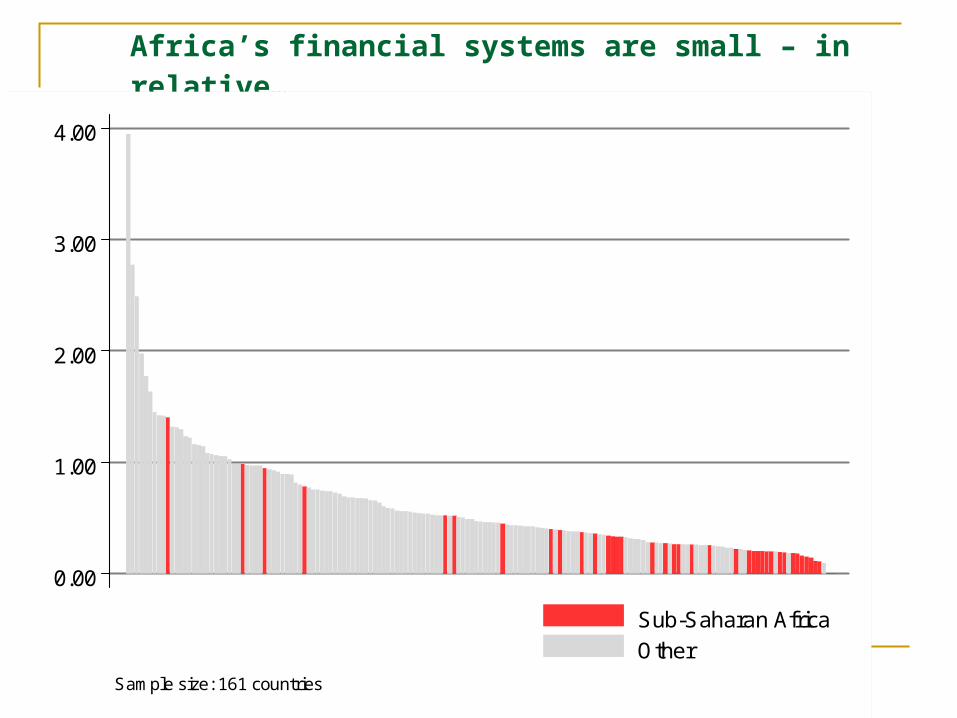

Africa’s financial systems are small – in relative…

0.00

1.00

2.00

3.00

4.00

Sub-Saharan Africa

Other

Sample size: 161 countries

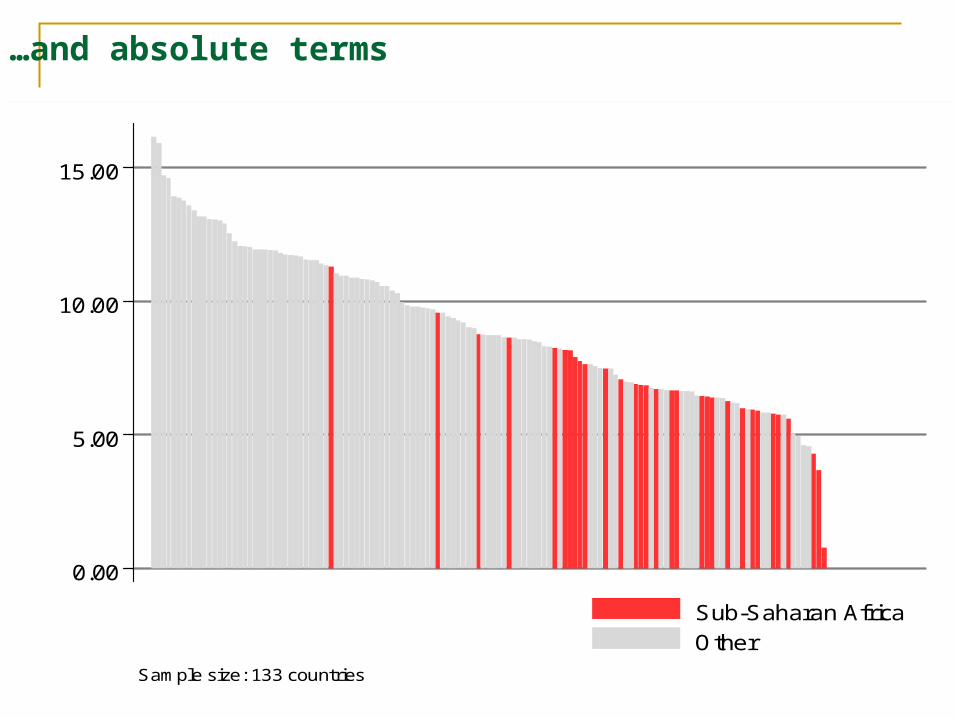

0.00

5.00

10.00

15.00

Sub-Saharan Africa

Other

Sample size: 133 countries

…and absolute terms

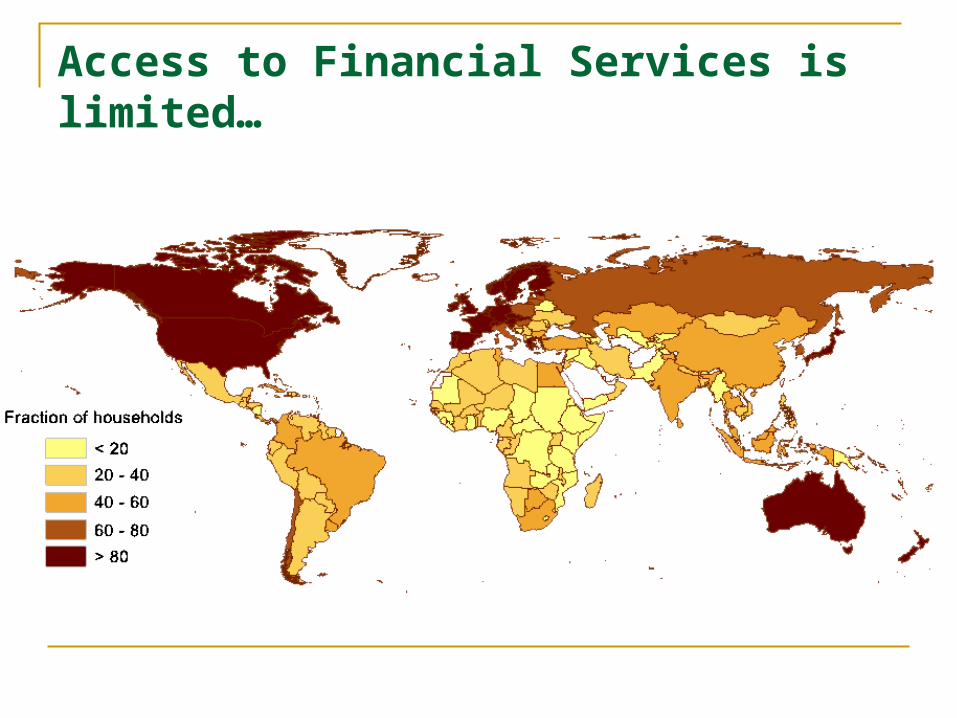

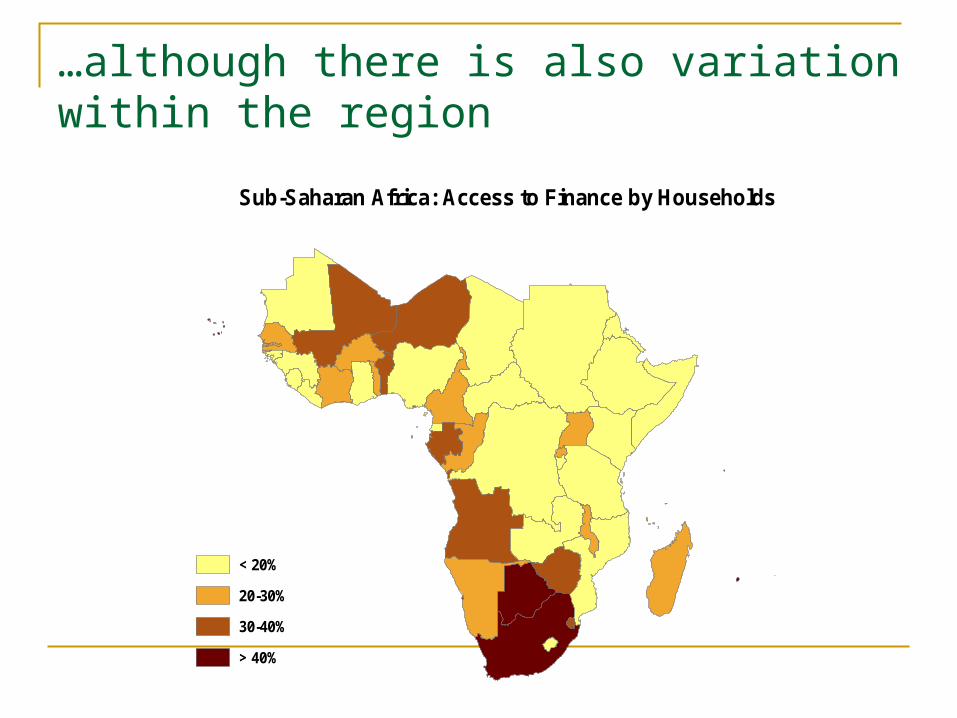

Access to Financial Services is limited…

…although there is also variation within the region

< 20%

20-30%

30-40%

> 40%

Sub-Saharan Africa: Access to Finance by Households

Banking is expensive – as can be observed in net interest margins…

0.00 0.05 0.10 0.15netintmargin

Sub-Saharan Africa

South Asia

Middle East & North Africa

Latin America & Caribbean

High-income

Europe & Central Asia

East Asia & Pacific

Sample size: 133 countries

Regional Distributions

… and costly…

0.00 0.05 0.10 0.15overhead

Sub-Saharan Africa

South Asia

Middle East & North Africa

Latin America & Caribbean

High-income

Europe & Central Asia

East Asia & Pacific

Sample size: 135 countries

Regional Distributions

.. but still profitable

-0.20 0.00 0.20 0.40roe

Sub-Saharan Africa

South Asia

Middle East & North Africa

Latin America & Caribbean

High-income

Europe & Central Asia

East Asia & Pacific

Sample size: 136 countries

Regional Distributions

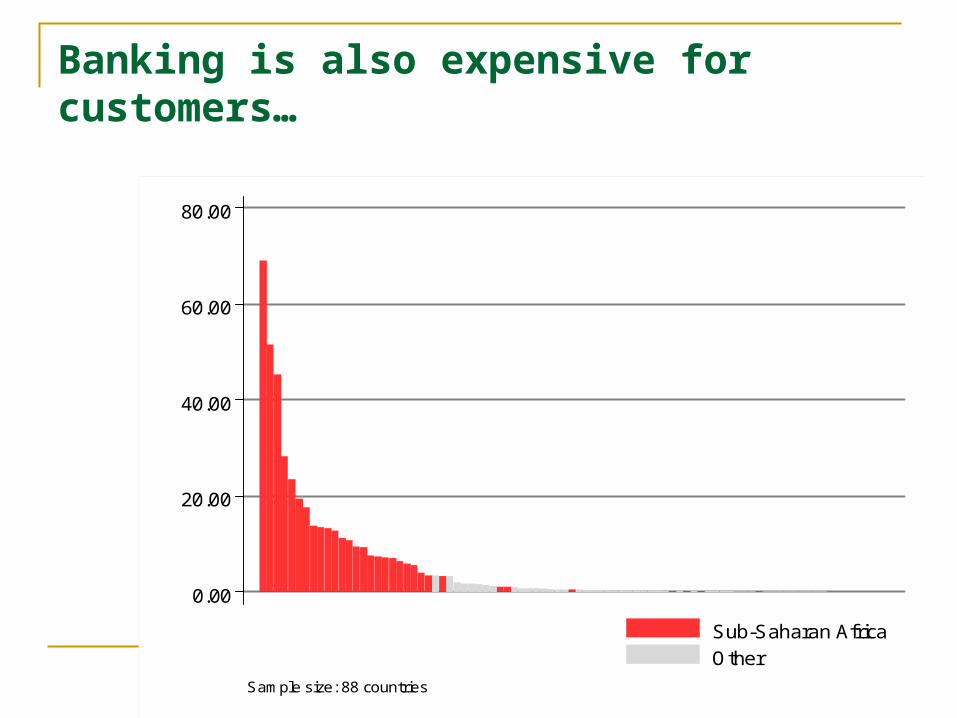

Banking is also expensive for customers…

0.00

20.00

40.00

60.00

80.00

Sub-Saharan Africa

Other

Sample size: 88 countries

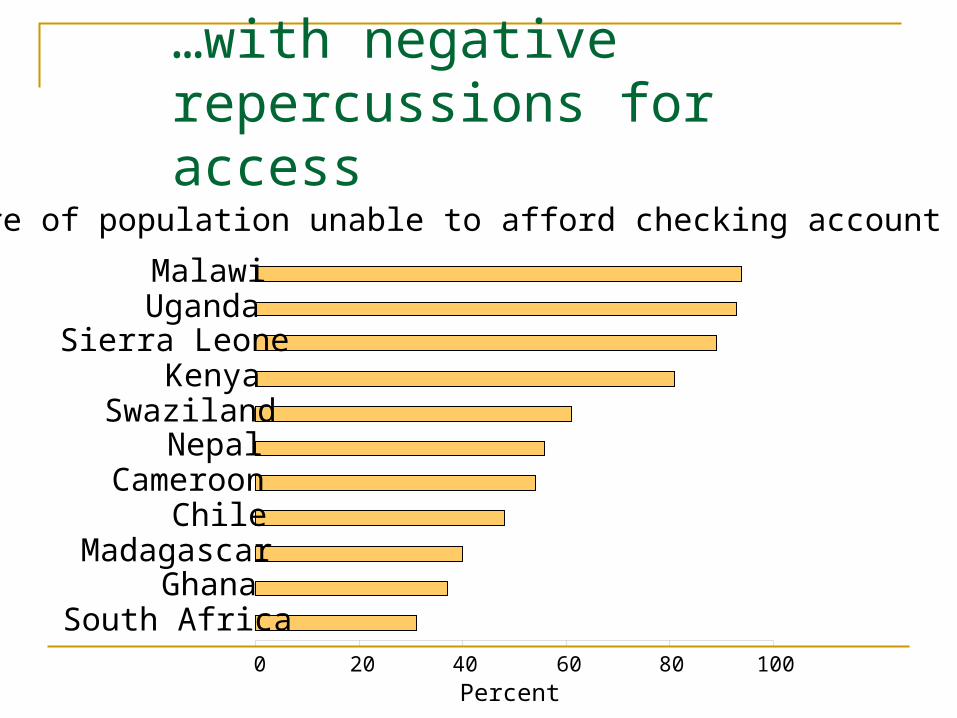

…with negative repercussions for access

Share of population unable to afford checking account fees

0 20 40 60 80 100

South AfricaGhana

MadagascarChile

CameroonNepal

SwazilandKenya

Sierra LeoneUgandaMalawi

Percent

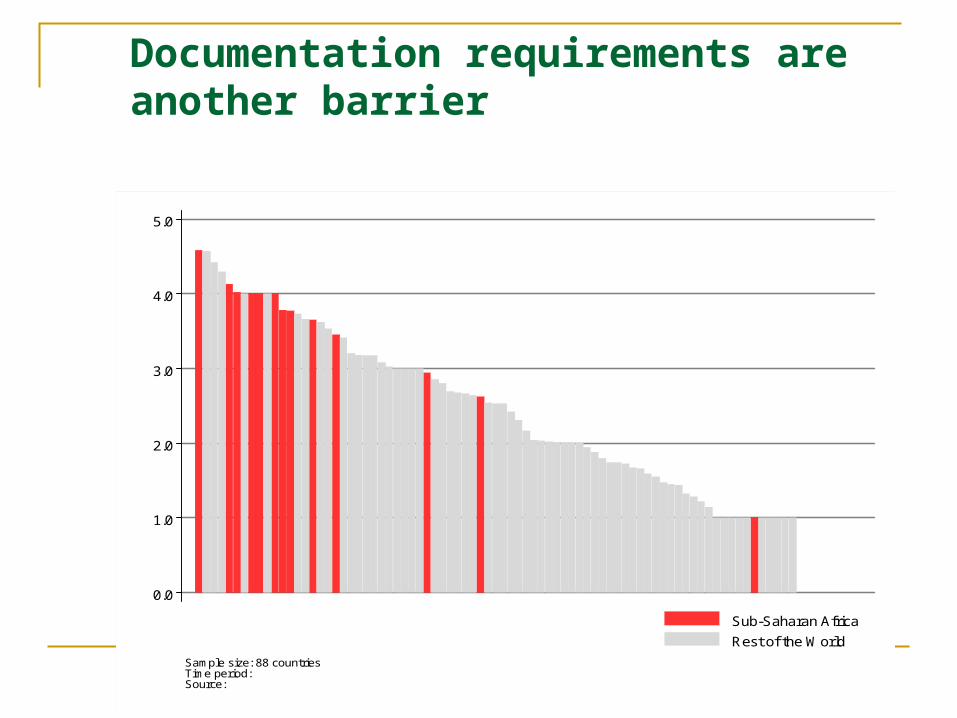

Documentation requirements are another barrier

0.0

1.0

2.0

3.0

4.0

5.0

Sub-Saharan Africa

Rest of the World

Sample size: 88 countriesTime period: Source:

Capital markets are even less developed

0.00

1.00

2.00

3.00

Sub-Saharan Africa

Other

Sample size: 101 countries

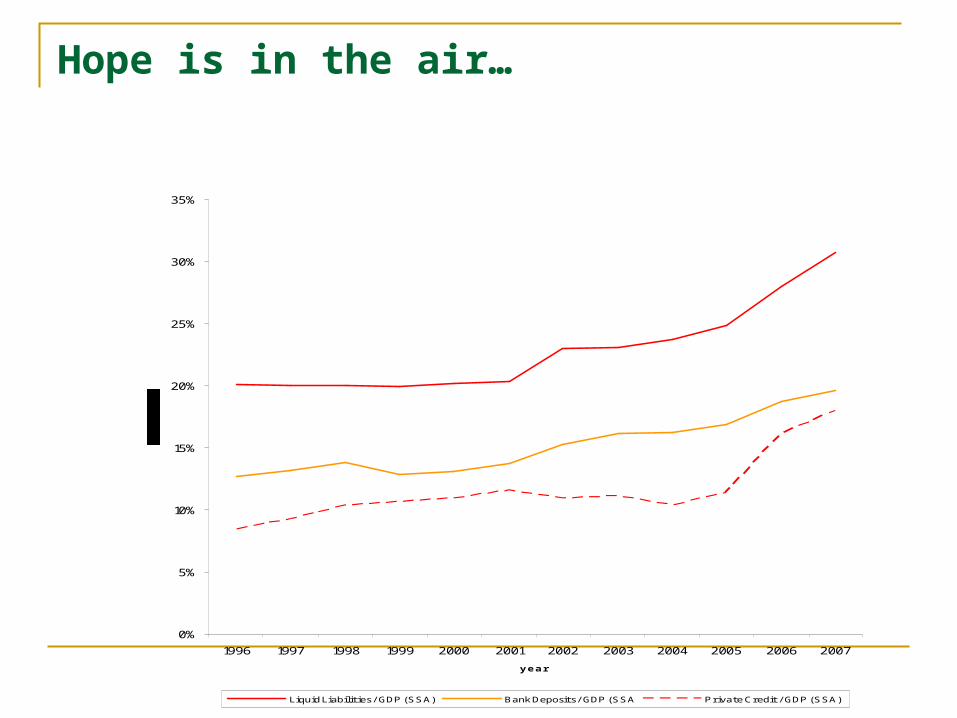

Hope is in the air…

0%

5%

10%

15%

20%

25%

30%

35%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

year

Liquid Liabilities / GDP (SSA) Bank Deposits / GDP (SSA Private Credit / GDP (SSA)

Finance is more in line with economic development than before

ALBARG

AUSAUT

BEL

BGD

BGR

BLZBOLBRA

CANCHE

CHL

COL

CRI

DEU

DNK

DOM

DZAECU

EGY

ESP

FIN

FRA

GBR

GRC

GTM

GUY

HKG

HNDHUN

IDN

IND

IRL

IRN ITAJOR

JPNKOR

LAO

LKA

LUX

LVA

MACMAR

MEX

MYS

NLD

NZL

PAK

PAN

PERPHL

PNG

PRT

PRYSLV

SWE

THA

TTOTUN

URY

USA

VEN

BENBFA

BWA

CIVCMR

ETH

GABGNB

KEN

LSOMDG

MLIMOZ

MUS

MWI SENSYC

TCD

TGO

ZAF

ZMB

-1.00

-0.50

0.00

0.50

1.00

1.50

Pri

vate

Cre

dit t

o G

DP

/infla

tion

resi

dual

-4.00 -2.00 0.00 2.00GDP per capita/inflation residual

Sub-Saharan AfricaOtherFitted values

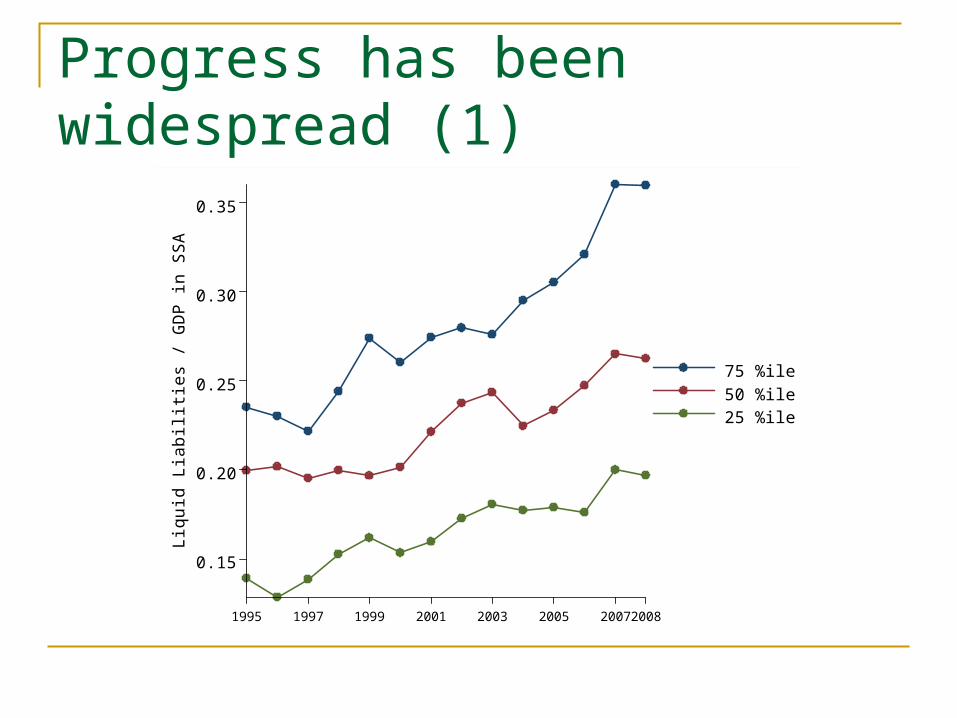

Progress has been widespread (1)

0.15

0.20

0.25

0.30

0.35

Liqu

id L

iabi

litie

s / G

DP

in S

SA

1995 1997 1999 2001 2003 2005 20072008

75 %ile

50 %ile25 %ile

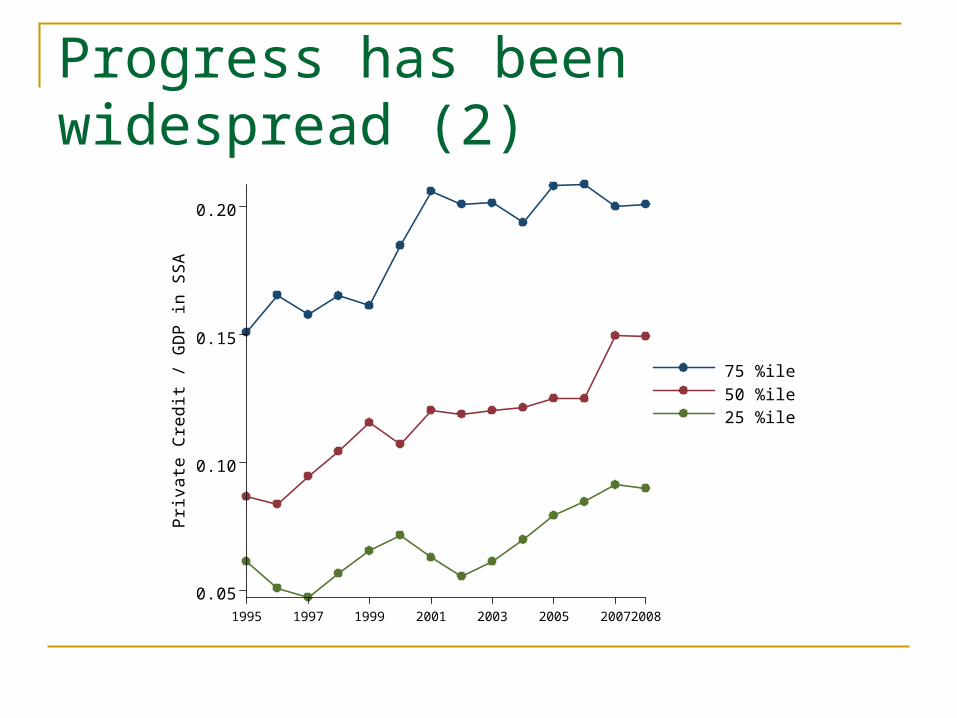

Progress has been widespread (2)

0.05

0.10

0.15

0.20

Pri

vate

Cre

dit /

GD

P in

SS

A

1995 1997 1999 2001 2003 2005 20072008

75 %ile

50 %ile25 %ile

Africa in the current crisis

No direct impact No toxic assets Little if any household lending Not as closely integrated

Indirect, second-round effects Parent banks – not as much as feared Real sector linkages (commodity and non-commodity exporters) Remittance flows Higher government financing needs International capital flows Parent banks at risk? Not the case Reforms of regulatory frameworks

Working in a new global environment Globalization has brought many advantages,

but also: Drying up of global capital funds

No alternative to globalization in most LICs, but: More emphasis on domestic resource mobilization More emphasis on regional integration

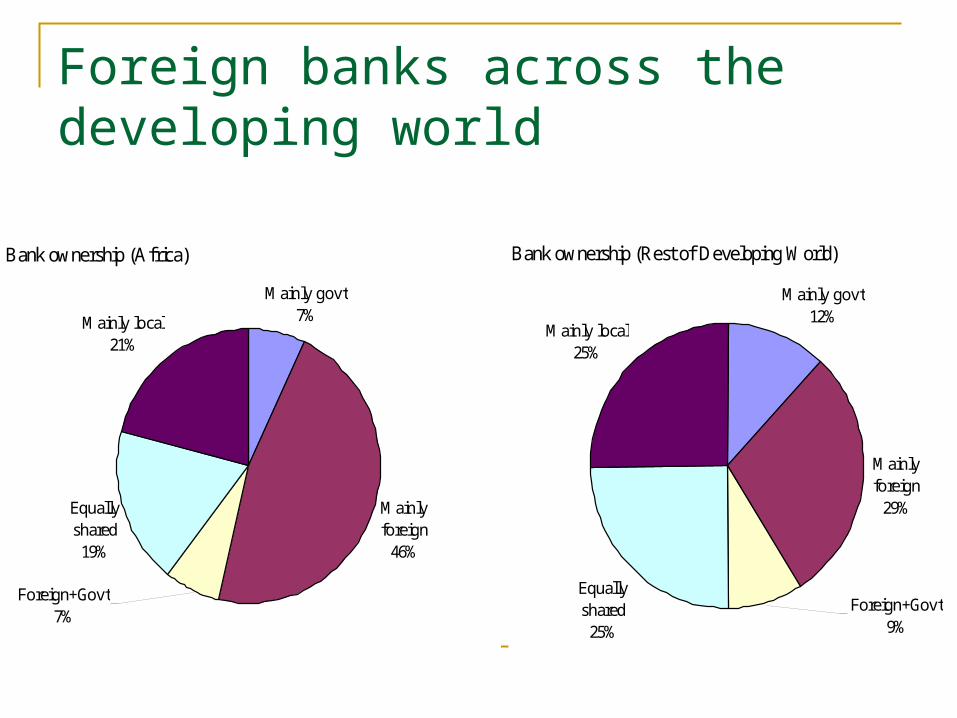

Foreign banks across the developing world

Bank ownership (Africa)

Equally shared

19%

Mainly local21%

Mainly govt7%

Mainly foreign

46%

Foreign+Govt7%

Bank ownership (Rest of Developing World)

Foreign+Govt9%

Mainly foreign

29%

Mainly govt12%

Mainly local25%

Equally shared

25%

Regulatory reform in the North -

the downsides of heavy regulatory hand Rent seeking, corruption, political capture Killing off markets – caveat emptor Negative repercussions for access to finance Consumer protection vs. systemic risk

Pyramids vs. derivative markets

Role of government – has the paradigm shifted again? Role of markets vs. government in the current

crisis Role of government in crisis resolution vs.

permanent role of government in financial sector

Activism vs. modernism

Regulatory lessons from the big crisis - from Pittsburgh to Lilongwe Macro-prudential supervision

Do LIC supervisors have the necessary information Pro-cyclical capital regulation? Benchmark in LICs?

Boundaries of regulation Heavy regulatory hand called for? Benefits of securitization Restrictions on certain activities

Strengthening prudential regulation LICs typically more conservative anyway How much information can LIC supervisors get and process?

Role of credit rating agencies Hmmm….

Role of consumer protection, financial literacy, disclosure

Cooperation for large multi-national banks MoUs??? Colleges of supervisors??

Can we apply Coase theorem? Incentives!!! Resources!! The role of IFIs

Long: ring-fence, short: branches Contingency planning Old vs. new foreign banks

Cooperation among LICs

Regional integration

Unfulfilled potential Over-ambition might be a problem – focus on

subregions, different speeds Benefits from technical cooperation Harmonizing regulatory frameworks

Branches instead of subsidiaries Reap benefits of scale economies Important: adjust financial safety net accordingly (see

problems in Europe) Intra-regional capital account liberalization

Looking beyond stability

Even in these times… Fostering financial development and access is important In most countries, it is central bank that is natural champion

Looking beyond the focus on tax havens and AML/CFT Risk-based approach to not undermine access to financial

services The current crisis underlines the necessity for

fundamental reforms in financial infrastructure as period of “cheap money” is over

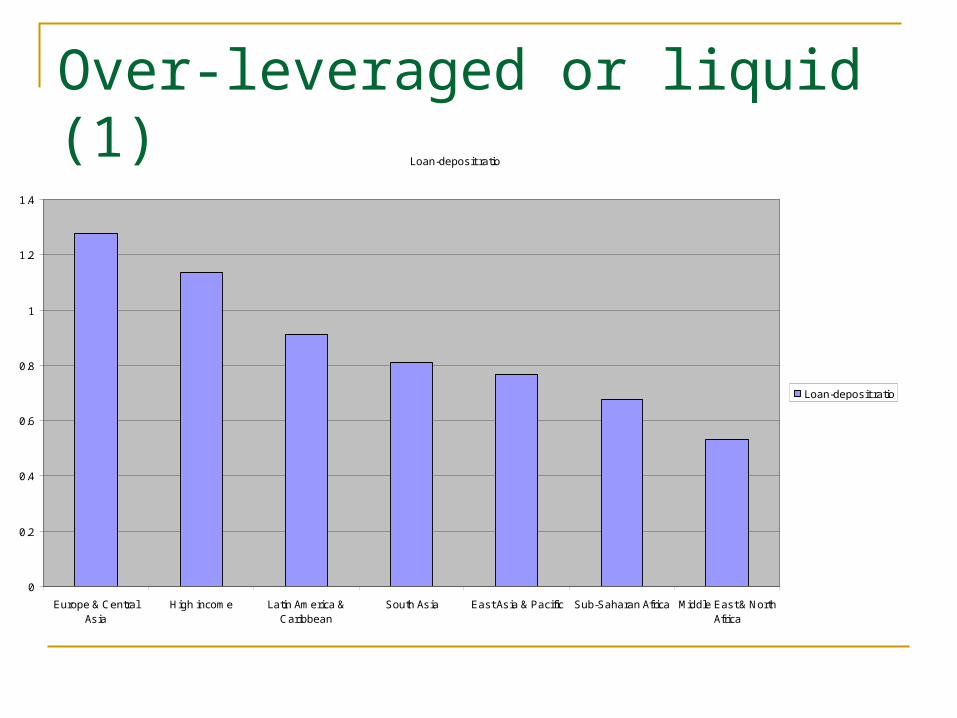

Over-leveraged or liquid (1)Loan-deposit ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Europe & CentralAsia

High income Latin America &Caribbean

South Asia East Asia & Pacific Sub-Saharan Africa Middle East & NorthAfrica

Loan-deposit ratio

Over-leveraged or liquid (2)Loan-deposit ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

High income: OECD Upper middle income High income: nonOECD Lower middle income Low income

Loan-deposit ratio

Financial sector policies in developing countries – looking ahead Financial innovation

Use of technology Competition from non-banks

Trade-off deepening/broadening and stability One size does not fit all Take trade-off into account in regulation

Focus on clients, less on institutions Financial service provision Consumer protection, transparency, over-indebtedness

Learn from each other

Who does what?

Looking beyond G20 Role for WB to represent non-G20 Complementary role for bilaterals in G20 (DfiD, BMZ,AFD

etc.) What kind of assistance?

Look beyond sub-sectoral support Linking diagnostics (FSAP – new model?) with technical

assistance Move beyond (away?) from international standards Focus more on big-picture financial sector development

policies