the affordable care act and special needs practice attorneys david lillesand, florida with...

TRANSCRIPT

The Affordable Care Act and Special Needs Practice

Attorneys David Lillesand, Florida with assistance on the materials byCynthia Barrett, Oregon and on the

PowerPoint by David L. McGuffey, Georgia

Legal malpractice fact pattern

The non-institutionalized disabled trust beneficiary dies in 2012. The Medicaid agency receives $1.3 million via the SNT Medicaid lien on the remaining $3 Million of proceeds in the deceased’s Special Needs Trust created in December, 2010.

The heirs sue the Special Needs Planning attorney who drafted the government-approved Medicaid payback trust. The attorney’s legal malpractice carrier promptly settles with the heirs for the attorney’s policy limits of $500,000 and leaves the attorney exposed for the remaining $800,000 judgment.

The State Bar then moves to disbar the attorney for gross negligence on the grounds that extraordinarily bad legal advice led to the unnecessary loss of $1.3 Million to the decedent’s heirs.

Why? The post-mortem Medicaid payback lien could have been completely avoided!

Did ACA End Special Needs Practice?

PPACA Sec. 2002(a) amends 42 USC 1396a(e) at 14(C):

“NO ASSETS TEST. A state shall not apply any assets or resources test for purposes of determining eligibility for medical assistance under the State plan or under a waiver of the plan.”

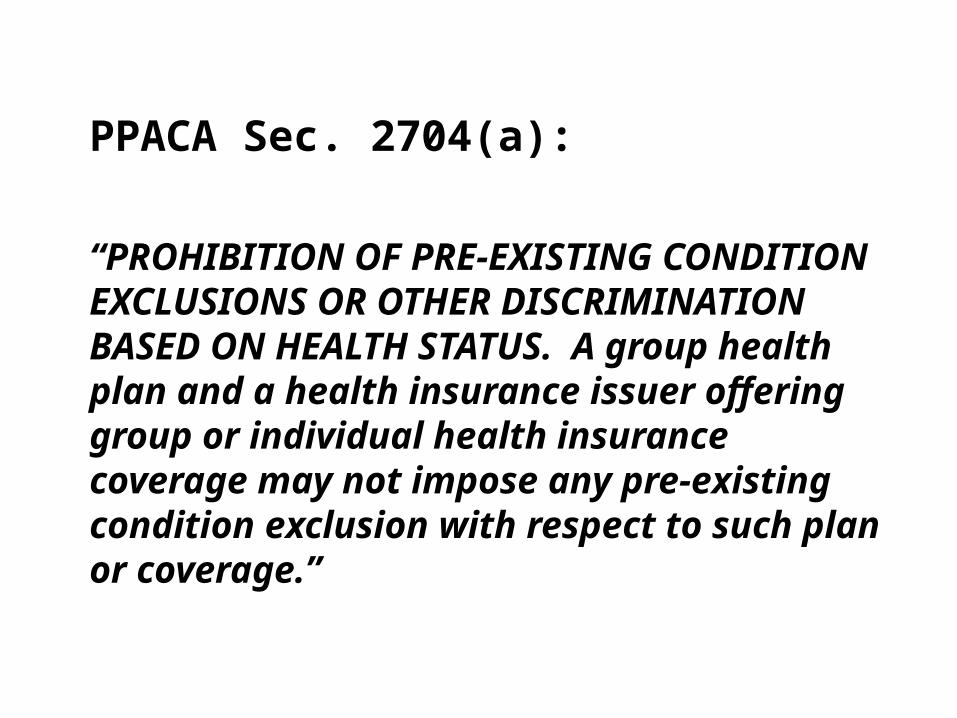

PPACA Sec. 2704(a):

“PROHIBITION OF PRE-EXISTING CONDITION EXCLUSIONS OR OTHER DISCRIMINATION BASED ON HEALTH STATUS. A group health plan and a health insurance issuer offering group or individual health insurance coverage may not impose any pre-existing condition exclusion with respect to such plan or coverage.”

Is my buddy coming for your practice?

What’s the one thing the Dems and GOP agree on?

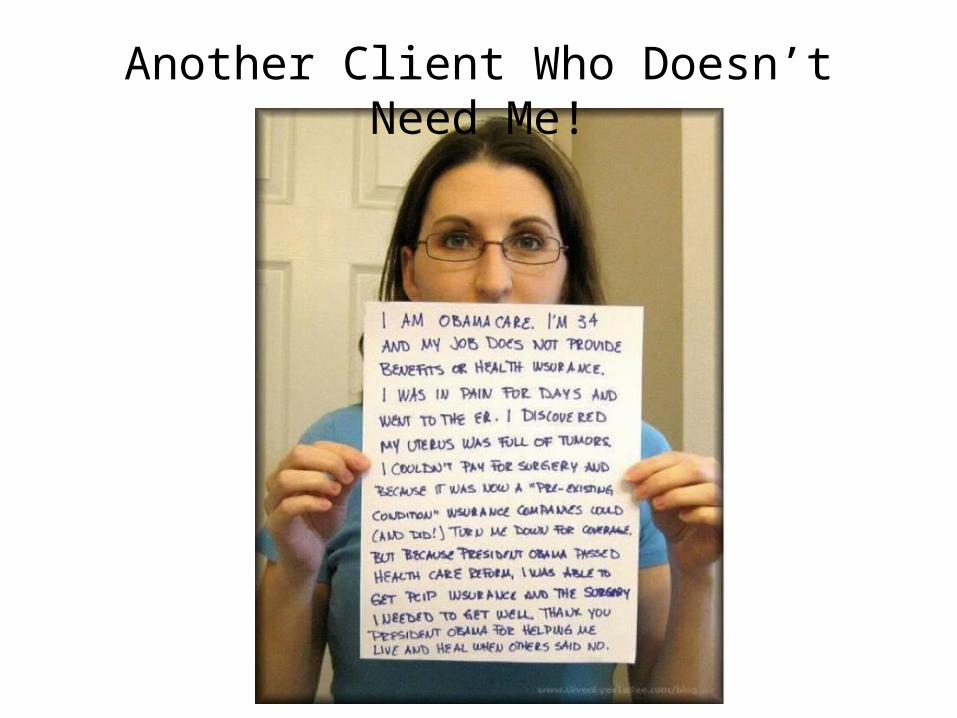

Another Client Who Doesn’t Need Me!

Current Special Needs Practice

Special needs planning is triggered by a potential beneficiary’s pre-existing health problems. The special needs trust is designed to allow publicly funded coverage (Medicaid) to be acquired or continue, and use the trust funds to supplement the federal programs.

Obamacare is Complex

The one sentence section by section analysis of the Act takes 74 pages alone‐ ‐

Republican Plan• All news accounts indicate Republicans would

keep PCIP coverage:– House GOP to offer new health plan

(Politico 1/25/12)– PCIP: The GOP’s Favorite Part of Obamacare

(WSJ 9/21/2010)

• WHY?? PCIP is the GOP alternative to ObamaCare.

How PCIP affects SNT planning today

• REAL health insurance with a fantastic list of the best physicians and hospitals

• NO ATTORNEY'S FEES - no trust required • NO BANK TRUST DEPARTMENT ANNUAL FEES• Revocability – can get out at any time• No pre-existing condition limitations • No annual or lifetime cap on services

• No insurance company rescission • Private health insurance – not

government insurance• Reasonable cost – premiums less than

our law firm’s BCBS policy• Available at any age – birth to 65• No super-low Medicaid service caps• physician services available nationwide• AND NO MEDICAID PAYBACK AT END OF

LIFE!

And unlike Medicaid,

This guy loves to see you coming!!

IMPACT?• The PCIP program will be a tremendous boon for our disabled clients seeking

first class health care

• Families will pay the PCIP premiums – they can provide food and shelter but can’t currently pay for MRIs, CT scans, cancer treatments, etc.

• The program will have a huge negative impact on our non-ICP SNT practices, the “Special Needs” part of the special needs practice, particularly the desirability to prepare d4A SNTs or join d4C pooled SNTs.

• Some clients have already decided to drop their SSDI disability claims because their PCIP insurance covers procedures that Medicare will not.

• Future SSI and SSDI clients will not pursue SSA disability claims

• Those that do will see a much higher percentage of awards – due to the availability of better medical care records

• Some clients have already decided to drop their SSDI disability claims because their PCIP insurance covers procedures that Medicare will not!

• Future SSI and SSDI clients will not pursue SSA disability claims

• Those that do will see a much higher percentage of awards – due to the availability of better medical care records

• The “disability rolls” will go down as fewer people will get sicker if they receive treatment and stay on their medications, and even keep working

• For those claimants who were dubious about filing a disability claim because they didn’t want to be “labeled disabled”, but would do so now only because it’s the only access to medical care, that problem is resolved.

More on the SSDI/SSI Disability Practice side…

Remember!What’s the first criteria

for being eligible to havea valid d4A or d4C Trust?

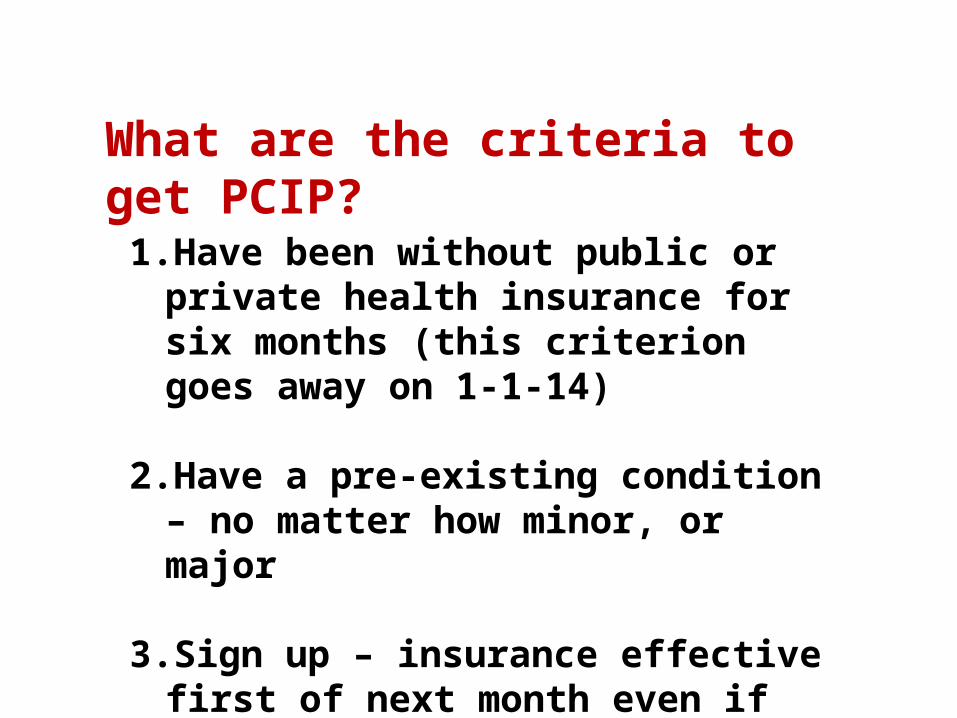

What are the criteria to get PCIP?

1. Have been without public or private health insurance for six months (this criterion goes away on 1-1-14)

2. Have a pre-existing condition – no matter how minor, or major

3. Sign up – insurance effective first of next month even if that is the very next day

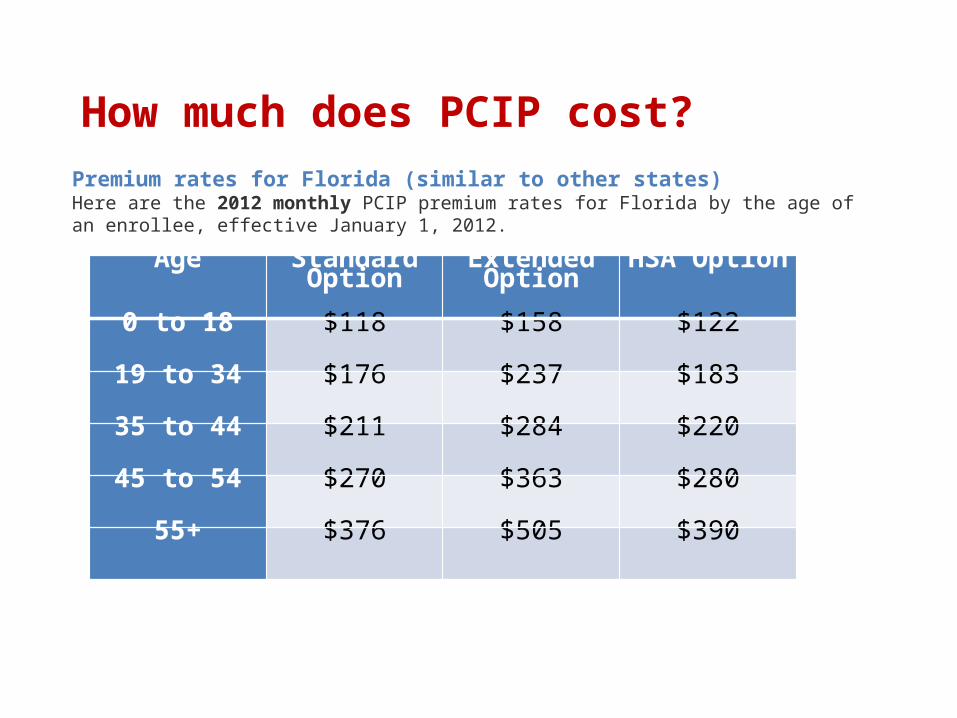

How much does PCIP cost?

Age Standard Option

Extended Option

HSA Option

0 to 18 $118 $158 $122

19 to 34 $176 $237 $183

35 to 44 $211 $284 $220

45 to 54 $270 $363 $280

55+ $376 $505 $390

Premium rates for Florida (similar to other states)Here are the 2012 monthly PCIP premium rates for Florida by the age of an enrollee, effective January 1, 2012.

SNT Clients now!

• Intake:– Make sure you get waiver of right to PCIP

• Drafting:– New provisions will allow trustee to purchase

private health insurance– Compare and shop policies

• Distributions:– Monitored to prevent increase in Modified AGI

That’s 3/2012, what happens on 1-1-2014

when ACA is fully effectuated?

ACA Does:1. Guaranty access

– Despite pre-existing conditions; – No annual limits– No lifetime limits.

2. Continue coverage for children through age 26

ACA Does:

3. Provide Premium Assistance, sliding scale (phased out at $89,000 for family of four)

4. Simplified Access to information through state or federal health exchanges and websites

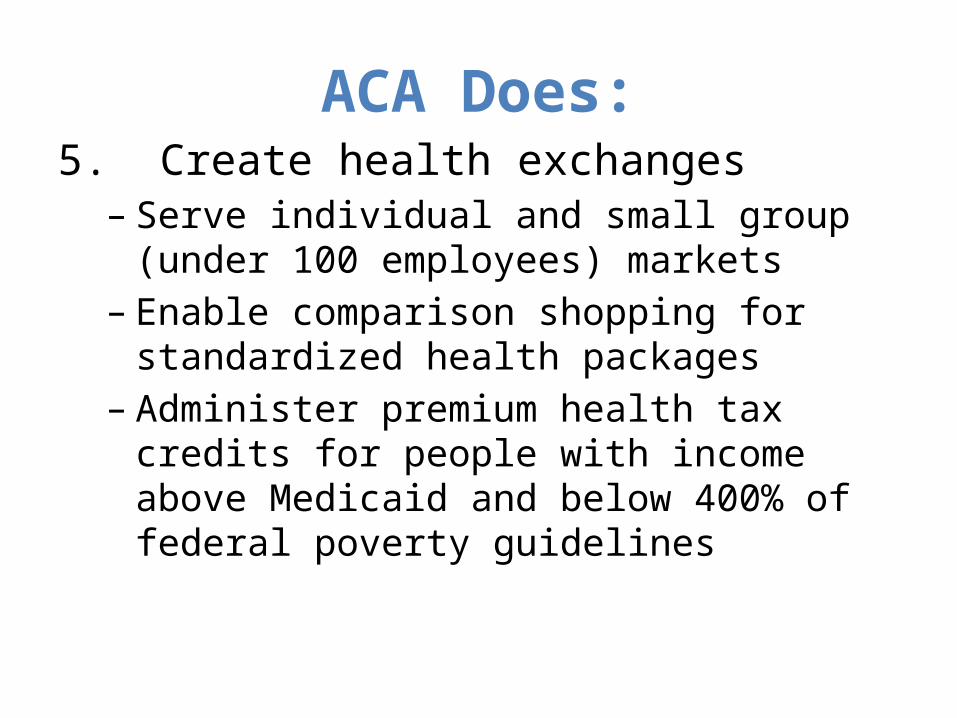

ACA Does:5. Create health exchanges

– Serve individual and small group (under 100 employees) markets

– Enable comparison shopping for standardized health packages

– Administer premium health tax credits for people with income above Medicaid and below 400% of federal poverty guidelines

2012 Annual Federal Poverty Guidelines

Household size 100% 133%

1 $11,170 $14,856

2 15,130 20,123

3 19,090 25,390

4 23,050 30,657

5 27,010 35,923

6 30,970 41,190

7 34,930 46,457

8 38,890 51,724

Food for thought:Minimum wage: $7.25 x 40 hours x 50 weeks = $14,500Minimum wage: $7.25 x 40 hours x 52 weeks = $15,0802012 Earned income breakeven point for SSI recipient = $17,772

ACA Does Not:

1. Change continued need for care managers2. Fund LTC - Public Medicaid ICP and Medicaid

Waiver Programs Unchanged3. Force private insurance to cover facility

based care and HCBS4. Change group health insurance5. Solve coverage disputes with insurers

What does the future hold?

• More guardianships – hospital discharge planning as they avoid re-admissions; and families deal with applying for insurance and dealing with HIPPA privacy, assuring premium payments, and gathering details necessary for the health plan application

• Less trust drafting to access medical care, but for money-management purposes

• SNTs increasingly restricted to the one in twenty client who needs institutional care or its alternatives, HCBS

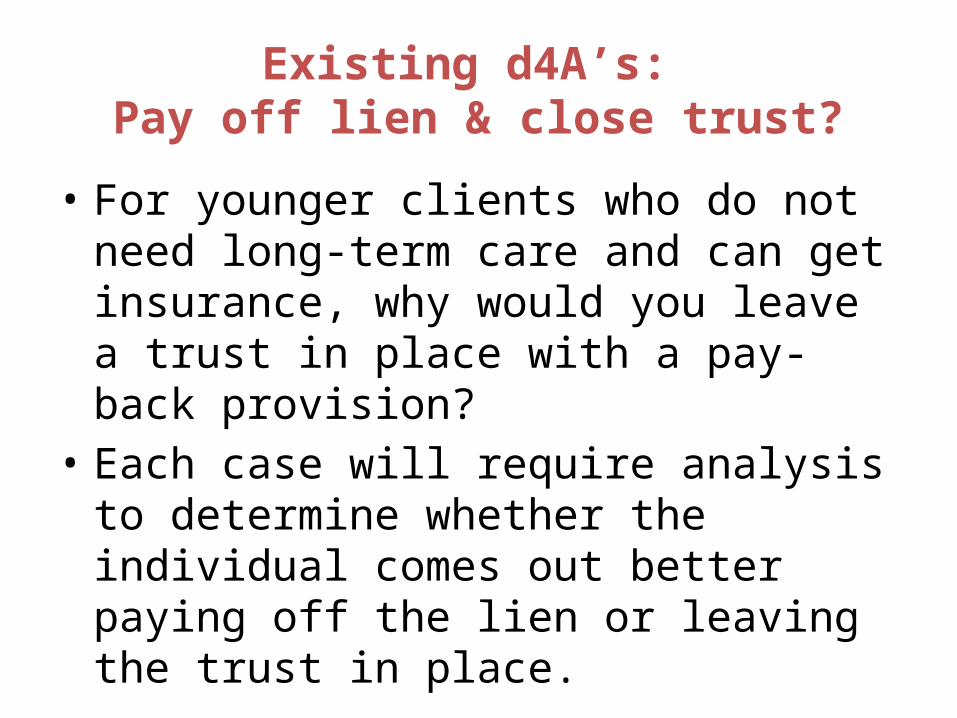

Existing d4A’s: Pay off lien & close trust?

• For younger clients who do not need long-term care and can get insurance, why would you leave a trust in place with a pay-back provision?

• Each case will require analysis to determine whether the individual comes out better paying off the lien or leaving the trust in place.

Future SNT Case Analysis

• Does the client need long-term care now or within the next 60 months or in a Med Waiver program?– Then consider a d4A

• Otherwise, ….do we plan as if the individual is among the 1.2% of Americans under 65 who might need nursing home care? (3% of total population in NHs; 40% of NH residents under 65)

Do we need an SNT?

• Is the individual institutionalized?

• Is it likely the individual will need future long-term care or alternatives, such as Med Waiver?

Future of Special Needs PracticeACA will (or may):

• Reduce personal injury awards since juries will award future premium costs instead of future medicals expenses;

• Reduce the number of Social Security disability claims filed if clients were primarily seeking access to Medicare or Medicaid;

• Reduce number of SSA appeals (often the result of poor documentation);

• Increase subrogation disputes since removal of annual and lifetime limits on coverage may result in tightening of rules; and

• Substantially kill the Elder and Disability Law attorney’s d4A SNT business?

?