the ads group - cfo

TRANSCRIPT

Brad Smith, President & CEO

Tom Bogan, CEO

M A R C H - 2 0 1 6

c f o t e c h o u t l o o k . c o m

Sriram Padmanabhan, SVP,

NIIT Technologies

CXO INSIGHTS

Tom Berquist, CFO,

TIBCO Software

CFO INSIGHTS

Kevin Held, CFO,

TradingScreen

IN MY OPINION

Adaptive Insights:

A Trailblazer in Budgeting and

Forecasting

Tom Bogan, CEO

$10

34March 2016

Borrowing Base:The Daily Benchmark

By Peter Stone, CFO, The ADS Group

I started my professional career as a staff accountant for a large regional public accounting firm. As time passed, my knowledge

expanded and my responsibilities changed with promotions to senior accountant and audit manager. Having worked in public accounting for approximately eight years, I wanted to learn more about the operations aspect of business and the daily challenges

outside of GAAP compliance. My desire to learn was pushing me to expand outside of the firm and my career at auditing historical transactions was about to change.

My career path is similar to other CPA’s who have left public accounting. I was fortunate to have built trusting relationships with my clients and along the way, and was offered a CFO position for a privately-held manufacturing

CFO Insights

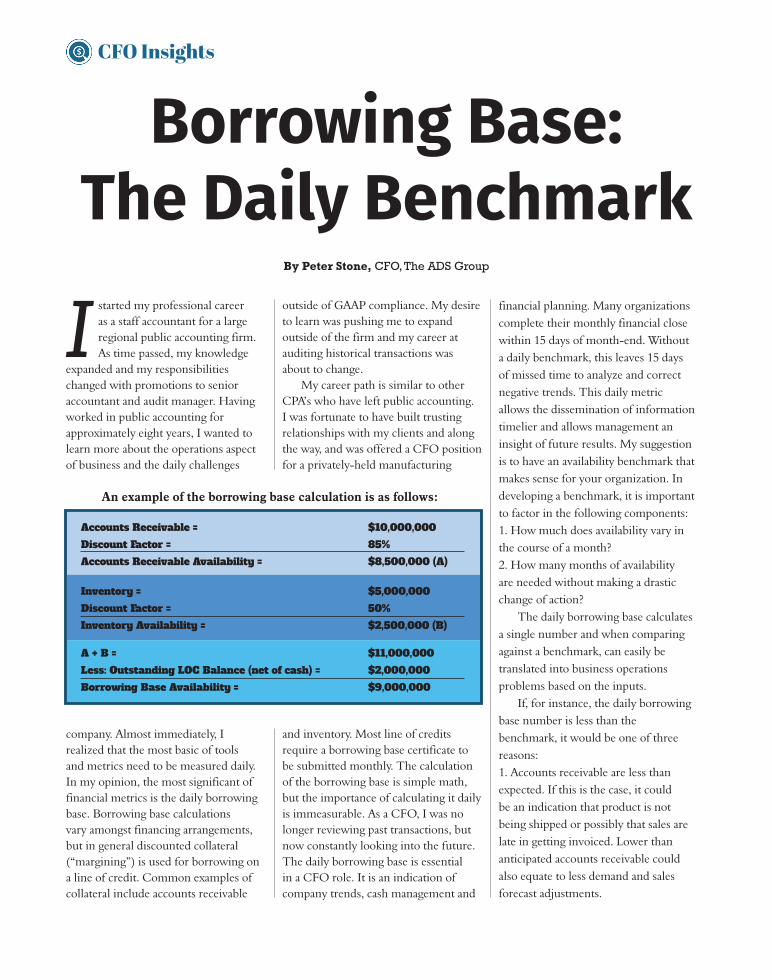

An example of the borrowing base calculation is as follows:

Accounts Receivable = $10,000,000

Discount Factor = 85%

Accounts Receivable Availability = $8,500,000 (A)

A + B = $11,000,000

Less: Outstanding LOC Balance (net of cash) = $2,000,000

Borrowing Base Availability = $9,000,000

Inventory = $5,000,000

Discount Factor = 50%

Inventory Availability = $2,500,000 (B)

company. Almost immediately, I realized that the most basic of tools and metrics need to be measured daily. In my opinion, the most significant of financial metrics is the daily borrowing base. Borrowing base calculations vary amongst financing arrangements, but in general discounted collateral (“margining”) is used for borrowing on a line of credit. Common examples of collateral include accounts receivable

and inventory. Most line of credits require a borrowing base certificate to be submitted monthly. The calculation of the borrowing base is simple math, but the importance of calculating it daily is immeasurable. As a CFO, I was no longer reviewing past transactions, but now constantly looking into the future.The daily borrowing base is essential in a CFO role. It is an indication of company trends, cash management and

financial planning. Many organizations complete their monthly financial close within 15 days of month-end. Without a daily benchmark, this leaves 15 days of missed time to analyze and correct negative trends. This daily metric allows the dissemination of information timelier and allows management an insight of future results. My suggestion is to have an availability benchmark that makes sense for your organization. In developing a benchmark, it is important to factor in the following components:1. How much does availability vary in the course of a month?2. How many months of availability are needed without making a drastic change of action?

The daily borrowing base calculates a single number and when comparing against a benchmark, can easily be translated into business operations problems based on the inputs.

If, for instance, the daily borrowing base number is less than the benchmark, it would be one of three reasons:1. Accounts receivable are less than expected. If this is the case, it could be an indication that product is not being shipped or possibly that sales are late in getting invoiced. Lower than anticipated accounts receivable could also equate to less demand and sales forecast adjustments.

34March 2016

Borrowing Base:The Daily Benchmark

By Peter Stone, CFO, The ADS Group

I started my professional career as a staff accountant for a large regional public accounting firm. As time passed, my knowledge

expanded and my responsibilities changed with promotions to senior accountant and audit manager. Having worked in public accounting for approximately eight years, I wanted to learn more about the operations aspect of business and the daily challenges

outside of GAAP compliance. My desire to learn was pushing me to expand outside of the firm and my career at auditing historical transactions was about to change.

My career path is similar to other CPA’s who have left public accounting. I was fortunate to have built trusting relationships with my clients and along the way, and was offered a CFO position for a privately-held manufacturing

CFO Insights

An example of the borrowing base calculation is as follows:

Accounts Receivable = $10,000,000

Discount Factor = 85%

Accounts Receivable Availability = $8,500,000 (A)

A + B = $11,000,000

Less: Outstanding LOC Balance (net of cash) = $2,000,000

Borrowing Base Availability = $9,000,000

Inventory = $5,000,000

Discount Factor = 50%

Inventory Availability = $2,500,000 (B)

company. Almost immediately, I realized that the most basic of tools and metrics need to be measured daily. In my opinion, the most significant of financial metrics is the daily borrowing base. Borrowing base calculations vary amongst financing arrangements, but in general discounted collateral (“margining”) is used for borrowing on a line of credit. Common examples of collateral include accounts receivable

and inventory. Most line of credits require a borrowing base certificate to be submitted monthly. The calculation of the borrowing base is simple math, but the importance of calculating it daily is immeasurable. As a CFO, I was no longer reviewing past transactions, but now constantly looking into the future.The daily borrowing base is essential in a CFO role. It is an indication of company trends, cash management and

financial planning. Many organizations complete their monthly financial close within 15 days of month-end. Without a daily benchmark, this leaves 15 days of missed time to analyze and correct negative trends. This daily metric allows the dissemination of information timelier and allows management an insight of future results. My suggestion is to have an availability benchmark that makes sense for your organization. In developing a benchmark, it is important to factor in the following components:1. How much does availability vary in the course of a month?2. How many months of availability are needed without making a drastic change of action?

The daily borrowing base calculates a single number and when comparing against a benchmark, can easily be translated into business operations problems based on the inputs.

If, for instance, the daily borrowing base number is less than the benchmark, it would be one of three reasons:1. Accounts receivable are less than expected. If this is the case, it could be an indication that product is not being shipped or possibly that sales are late in getting invoiced. Lower than anticipated accounts receivable could also equate to less demand and sales forecast adjustments.

35March 2016

Peter Stone

2. Inventory is less than expected. If inventory is less than expected it is could be an indication that raw materials are at risk of falling below re-order points and procurement may incur expediting charges. Running out of inventory components could have drastic negative effects on the production workforce and meeting ship deadlines.3. The outstanding balance on the line of credit is higher than expected. This input is based on variance throughout

the course of the month when establishing the initial benchmark. Cash flow can have large swings on a daily basis for items such as bi-weekly payroll and weekly check runs. Whereas inventory consumption and accounts receivable should be more linear throughout the course of the month, depending on your product and industry.

Regardless of the situation, the daily metric allows the identification of a po-tential problem and allows for timely resolution and correction. When compared to the established benchmark daily, a more in-depth investigation can be com-pleted.

Not only does the daily borrowing base allow for better cash flow management,

but it can also be utilized when performing check runs and negotiating terms with vendors. The metric can be provided to lenders more frequently leading to increased communication and mitigating any surprises. The daily borrowing base allows for superior financial planning insight. As management initiatives are carried out, it is the preservation of availability that helps support identified growth initiates to be taken advantage of.

The daily availability calculation is easy math. The frequency of the calculation is what makes it a valuable tool. Regardless of a lending requirement to submit a borrowing certificate monthly, it is more for the benefit of the organization as to where the company is headed. Unlike public accounting and ensuring everything is accounted for correctly in the past, this metric is an indication of things to come.

$

My desire to learn was pushing me to expand outside of the firm and my career at auditing historical transactions was about to change