the added value of an operating system audit to an...

TRANSCRIPT

Thesis:

The added value of an operating system audit to an IT

General Controls audit

S.A.H. Cobelens MSc.

2174332

September 6, 2013

Vrije Universiteit Amsterdam

The added value of an operating system audit to an IT General Controls audit 2

Abstract

The threat of information leakage, financial misstatements or fraud from financial IT

solutions is imminent. Accountancy firms have to trust on information coming from these

systems and deal with a world where new cyber-attacks are daily news. Accountancy firms

continuously develop their audit approach to mitigate (new) risks in a more effective and

efficient way. Auditors are often unsure of whether to include a thorough operating system

parameter check in their IT General Controls audit approach. This thesis explores the added

value of an operating system parameter check to an ITGC audit. This is done by inspecting a best

practice, testing it at three companies and creating a risk analyses per parameter category.

The added value of an operating system audit to an IT General Controls audit 3

Acknowledgements

I would like to thank my thesis supervisor Rene Matthijsse for helping and guiding me

through the whole thesis process. Besides that I would like to thank my colleagues for their

import and thought on the subject. Last but not least I thank my family and friends for their

support.

The added value of an operating system audit to an IT General Controls audit 4

Table of contents

Acknowledgements .....................................................................................................................3

1. Introduction .........................................................................................................................7

1.1 Introduction .......................................................................................................................7

1.2 Research question ..............................................................................................................8

1.3 Contribution ......................................................................................................................8

1.3.1 Academic Relevance: .................................................................................................8

1.3.2 Managerial Relevance:................................................................................................8

1.4 Research design: ................................................................................................................9

1.5 Thesis structure .................................................................................................................9

2. Theoretical Background .................................................................................................... 10

2.1 A brief history of IT audits .............................................................................................. 10

2.2 IT General Controls ......................................................................................................... 11

2.3 ITGC in the financial statement audit .............................................................................. 12

2.4 The structure of IT General Controls ............................................................................... 14

2.5 Auditing of the ITGCs ..................................................................................................... 16

2.6 Information security ........................................................................................................ 17

3. Hypotheses ........................................................................................................................ 24

3.1 Conceptual Framework .................................................................................................... 24

3.2 Hypotheses ...................................................................................................................... 25

3.3 Control Variables ............................................................................................................ 26

4. Case study methodology ........................................................................................................ 27

4.1 Research Methods ........................................................................................................... 27

4.1.1 Observation .............................................................................................................. 27

4.1.2 Preliminary information gathering ............................................................................ 27

4.1.3 Theory formulation ................................................................................................... 28

4.1.4 Hypothesizing ........................................................................................................... 28

4.1.5 Further scientific data collection ............................................................................... 28

4.1.6 Data analysis and conclusion .................................................................................... 29

4.2 Sample selection .............................................................................................................. 29

5. Case study findings ............................................................................................................... 30

5.1 Company profile .............................................................................................................. 30

The added value of an operating system audit to an IT General Controls audit 5

5.1.1 Company A .............................................................................................................. 30

5.1.2 Company B ............................................................................................................... 30

5.1.3 Company C ............................................................................................................... 30

5.2 Outcome .......................................................................................................................... 30

5.3 Analysis of results ........................................................................................................... 32

5.3.1 Accounts ................................................................................................................... 32

5.3.2 Audit policy .............................................................................................................. 32

5.3.3 Detailed Security Auditing ........................................................................................ 33

5.3.4 Event log .................................................................................................................. 33

5.3.5 Windows Firewall ..................................................................................................... 34

5.3.6 Windows Update ...................................................................................................... 34

5.3.7 User Account Control ............................................................................................... 35

5.3.8 User Rights ............................................................................................................... 35

5.3.9 Security options ........................................................................................................ 36

5.3.10 Terminal services .................................................................................................... 36

5.3.11 Internet Communication ......................................................................................... 37

5.3.12 Additional security settings ..................................................................................... 37

5.4 Other factors .................................................................................................................... 38

5.4.1 Costs of the operating system parameter check ......................................................... 38

5.4.2 Type of operating system(s) in use ............................................................................ 38

5.4.3 No extra comfort ....................................................................................................... 38

5.4.4 Politics and time ....................................................................................................... 39

6. Validation of hypotheses ....................................................................................................... 40

6.4.1 WH1: An operating system parameter audit will only give comfort over the operating

system layer ...................................................................................................................... 40

6.4.2 WH2: Operating system comfort is essential for reliance on application controls ...... 40

7. Conclusions ........................................................................................................................... 41

8. Limitations and further research ............................................................................................ 43

References ................................................................................................................................ 44

Appendix I: Detailed results ...................................................................................................... 45

The added value of an operating system audit to an IT General Controls audit 6

List of tables and figures

Figure 1..................................................................................................................................... 13 Figure 2..................................................................................................................................... 15 Figure 3..................................................................................................................................... 21

The added value of an operating system audit to an IT General Controls audit 7

1. Introduction

1.1 Introduction

Companies use a variety of software solutions for their financial administration. These

financial software solutions (e.g. SAP, Oracle, PeopleSoft and Navision) have been implemented

in thousands of companies worldwide. Software solutions often have a client-server architecture

which means they can be reached within a network and are therefore likely to be a target for

people with the wrong intentions (Albornoz Mulligan, 2007). The machines that run these

financial software solutions need to be hardened in order to respond to the increasing amount of

risks from the connected world. There are best practices available for the setup of the system

environments and there are tools to check them.

The threat of information leakage, financial misstatements or fraud from financial IT

solutions is imminent and it is a complex matter where there is no single control that mitigates all

the risks. For example, users with broad privileges in a financial system can bypass controls like

the 4-eyes principle to make unauthorized adjustments, database administrators can edit tables

and change user information, and system administrators can get access to the database and the

software. This shows that multiple levels of computer system security need to be taken into

account for a company in order to be able to trust its businesses processes to such financial

software. Its accountants need to obtain comfort about the completeness, accuracy and validity of

the data coming from the system in order to do their work.

Accountancy firms, who sign off the financial statements, rely heavily on data coming

from these systems and therefore need to be sure of the completeness, accuracy and validity of

the data it generates. In order to gain this comfort an IT General Control (ITGC) audit is

performed as part of the financial statement audit. This is an audit on all controls that apply to

relevant system components, processes, and data of the IT environment (ISACA, 2013).

Accountancy firms continuously develop their audit approach to mitigate (new) risks in a

more effective and efficient way. Auditors are often unsure of whether to include a thorough

operating system parameter check in their ITGC audit approach. This thesis explores the added

value of an operating system parameter check to an IT General Controls audit.

The added value of an operating system audit to an IT General Controls audit 8

1.2 Research question

A company uses an operating system baseline security scan as part of their ITGC audit.

This security scan checks the system settings of the operating systems against a best practice

published by the Center for Internet Security (CIS). The outcome of the scan is an overview of

the many system settings and their compliance against the best practice. Audit teams are often

not aware what the added value of such a baseline scan is for their ITGC audit and when they

can or should use it. What comfort does this security baseline scan give the IT auditor regarding

the ITGCs and when should an auditor consider performing such a scan?

How does a baseline security scan on operating systems parameters add value to an ITGC

audit?

In order to answer the research question, several sub questions have to be answered:

What is the place of operating system parameters in the IT General Control environment?

What kind of comfort and assurance can result from an operating system parameter

baseline scan to the ITGC audit?

Under which conditions should an ITGC auditor consider using an operating system

parameter baseline scan?

1.3 Contribution

1.3.1 Academic Relevance:

This research tries to add academic value to both topics making the choice for auditors

more sound as whether to use an operating system baseline security scan for their IT General

Control work. There exist a lot of best practices but not much academic literature is found

regarding ITGCs and operating system security baselines.

1.3.2 Managerial Relevance:

A business unit tries to sell baseline scans as part of an IT audit (ITGC). Audit teams are

sometimes unsure and are wondering what comfort they will get with a baseline scan and how it

can make impact at the client. Several baseline scans have been done. It is important for IT audit

The added value of an operating system audit to an IT General Controls audit 9

processes to understand what the most common and notable findings are and what is their impact

is on the IT General Controls.

1.4 Research design:

This research intends to study the use of an operating system parameter baseline scan as

part of an IT General Control audit, how the operating system parameters can be linked the IT

General Control environment, what kind of comfort an auditor would get doing an operating

system parameter audit and when it would be a viable audit approach. The link between the

ITGC environment and the operating system parameters will first be determined by a literature

study. Based on the outcome an operating system parameter check will designed and performed

in a case study environment. Based on the theoretical background and results from the case study

the impact to the ITGC audit will be determined and recommendation will be formulated and

documented.

1.5 Thesis structure

The structure of this thesis can be broken down into three main parts. The first part

consists of a general introduction concerning what will be researched as well as the theoretical

foundations of the thesis. Furthermore all relevant literature concerning operating system

parameters and ITGCs will be discussed.

The second part is about the methodological aspect of the thesis. In this section, a

conceptual framework is constructed based on the research questions and literature review.

Moreover, the methodology of this research is explained. This section will also elaborate on the

design and execution of the case study.

Finally, the last part of this thesis will consist of the presentation of results, discussion of

the results, limitations and future research and conclusion.

The added value of an operating system audit to an IT General Controls audit 10

2. Theoretical Background

2.1 A brief history of IT audits

Over the course of the years businesses have become more and more dependent on

information coming from IT systems. In the 60’s one of the first frauds using IT systems was

detected at the Equity funding Corporation of America. Also in The Netherlands auditors became

aware that information systems more and more became part of the business and therefore needed

to be taken into account for the audit. This shift in thinking had a great impact on accountants

and the financial statement audit. Accountants formed ideas about information systems, their

place in the administrative organization and how to audit them. Some accountants started to

specialize in the audit of information systems which meant the birth of the IT auditor.

When the 3270-terminal was released on the markets in the 70’s it allowed mutations to

be entered real-time on the computer. This replaced the physical processes and controls that were

used with the so called ponskaarten. Because now anyone could make mutations, the accountants

had no comfort over the reliability of the information generated by the system. In order to

mitigate the risks associated to such information systems the segregation of duties principle and

authorization matrixes were introduced.

In the 80’s the field of IT audits was further developed. Data centers and IT projects

became a focus point for IT auditors. In 1988 the Dutch National Bank released a memorandum

that stated that IT is an essential part of a business that supports its solvability and liquidity. This

confirmed that the IT environment is essential for the financial statement audit.

The 90’s introduced the client/server architecture which replaced a lot of main frames and was

adopted in many projects. Next to that new IT developments methodologies were developed

based on the client/server architecture which promised more efficient projects with shorter

durations. Because of an increase in computer systems and applications best practices like ITIL

were developed to manage the new IT infrastructure.

The 00’s marked the introduction of further integration of IT with the business,

development of best practices and continuously new challenges for the control of the IT

environment. New upcoming technologies and initiatives like Cloud-computing and Bring Your

Own Device challenge management and auditors to find a way to implement these advances in a

controlled manner (Comte, 2009).

The added value of an operating system audit to an IT General Controls audit 11

2.2 IT General Controls

From the founding thoughts about administrative organizations it is said that proper

internal controls need to be in place to ensure the reliability of information processed by

information systems (Starreveld, 2002). These controls can be divided into organization, logical

and physical controls.

In accounting and auditing, internal control is defined as a process affected by an

organization's structure, work and authority flows, people and management information systems,

designed to help the organization accomplish specific goals or objectives. It is a means by which

an organization's resources are directed, monitored, and measured. It plays an important role in

preventing and detecting fraud and protecting the organization's resources, both physical (e.g.,

machinery and property) and intangible (e.g., reputation or intellectual property such as

trademarks) (COSO, 2013).

Because of the increasing reliability on IT systems, controls were developed and best

practices formed to control the IT environment. Two control “frameworks” have been devised to

assist both management and auditors in designing and assessing controls in computerized

environments. One is the Information Technology Control Guidelines (IT Guidelines), first

published by the Canadian Institute of Chartered Accountants (CICA) in 1970 (in its 3rd edition

in 2011). The other is the Control Objectives for Information and related Technology (COBiT)

developed by the Information Systems Audit and Control Association (ISACA) (GFS, 2013).

IT controls are a subset of the internal controls of an organization. In literature (Jenkins,

1992) internal controls are often divided into

User controls; manual controls

Application controls; programmed controls

ITGC; general IT management controls

User controls are defined as manual internal controls. The goal of user controls is to generate

reliable information for the input into information systems, to take action based on information

or signals from an information system and to control an information system in a proper manner.

Manual elements in internal control may be less reliable than automated elements because they

can be more easily bypassed, ignored, or overridden and they are also more prone to simple

The added value of an operating system audit to an IT General Controls audit 12

errors and mistakes. Consistency of application of a manual control element cannot therefore be

assumed.

Application controls can be defined as programmed controls in applications. The goal of

application controls is to create segregation of duties in applications and to ensure the reliability

of the data.

IT general controls (ITGC) are controls that apply to all system components, processes, and

data for a given organization or information technology (IT) environment. The objectives of

ITGCs are to ensure the proper development and implementation of applications, as well as the

integrity of programs, data files, and computer operations (ITGC, 2013).

2.3 ITGC in the financial statement audit

Accountants need to be sure that the published financial statements are being prepared

reliably. Also called Financial Statement Line Items (FSLI), they give an overview of the

financial figures and position of the organisation (Berger, 2003). The controls in the ITGC are an

aid to mitigate IT risks that the company faces in the preparation of the financial statements. The

IT risks need to be identified and appropriate controls need to be in place to mitigate these risk.

IT risks can be divided into two types: IT-dependent and IT-specific risks (PwC Audit Guide,

2012). The ITGC mitigate the IT-dependent and IT-specific risks

IT-dependent risks are risks that directly stem from comfort that the ITGC should provide

the organization. There are three types of IT dependent risk areas: Automated Control Integrity

(ACI), Report Integrity (RI) and Access Integrity (AI). Access Integrity is the risk area about

controls that can be bypassed to gain unauthorized access to systems and applications. Risks in

the Automated Control Integrity area are risks coming from automated application and system

functions that haven´t been properly tested and implemented. Report Integrity risks are the risks

associated with the reliability of the system generated reports.

IT-specific risks are risks that are inherent to IT-systems such as hardware/software

changes outside of the normal business processes. The primary risk areas Direct Data Access

(DDA), Data Integrity (DI) and Applications Controls in Computer Operations (ACCO). Direct

Data Access risks involve all the risks that can lead to unauthorised access to data, to the change

of data and to the destruction of data. Data Integrity risks involve all the risks that can lead to

The added value of an operating system audit to an IT General Controls audit 13

damaged or lost data. Applications Controls in Computer Operations risks involve errors in batch

jobs or interfaces leading to incomplete or unreliable (financial) data.

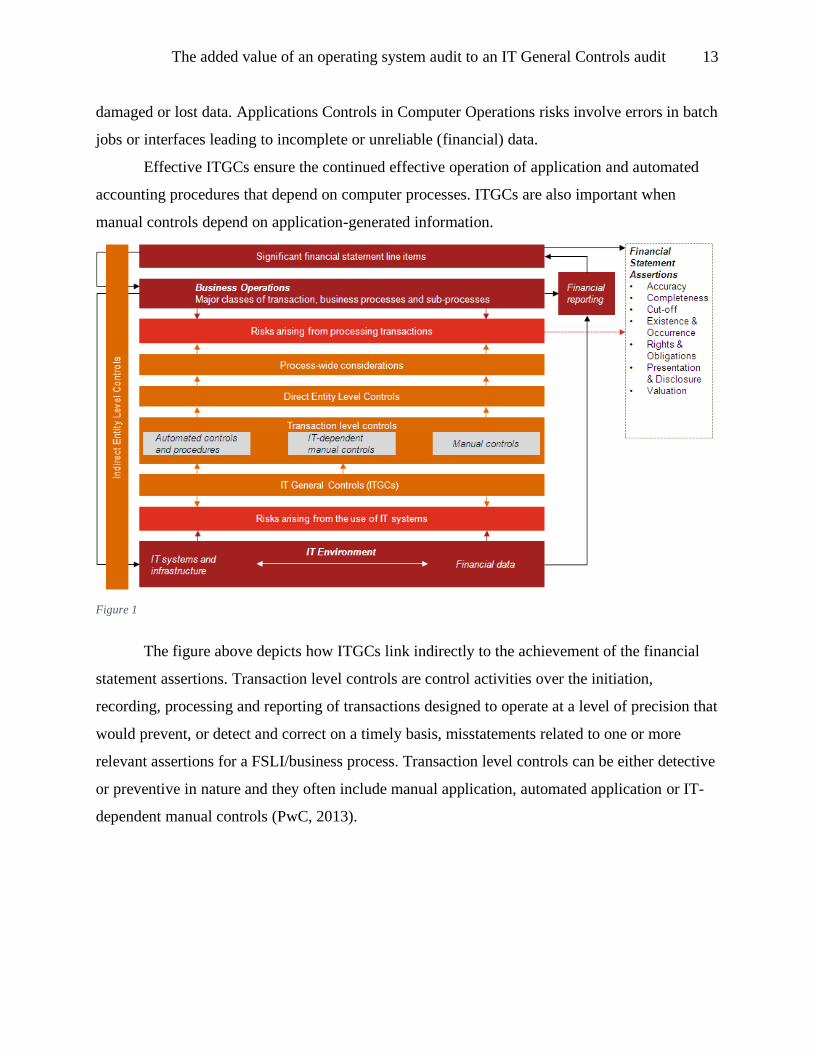

Effective ITGCs ensure the continued effective operation of application and automated

accounting procedures that depend on computer processes. ITGCs are also important when

manual controls depend on application-generated information.

Figure 1

The figure above depicts how ITGCs link indirectly to the achievement of the financial

statement assertions. Transaction level controls are control activities over the initiation,

recording, processing and reporting of transactions designed to operate at a level of precision that

would prevent, or detect and correct on a timely basis, misstatements related to one or more

relevant assertions for a FSLI/business process. Transaction level controls can be either detective

or preventive in nature and they often include manual application, automated application or IT-

dependent manual controls (PwC, 2013).

The added value of an operating system audit to an IT General Controls audit 14

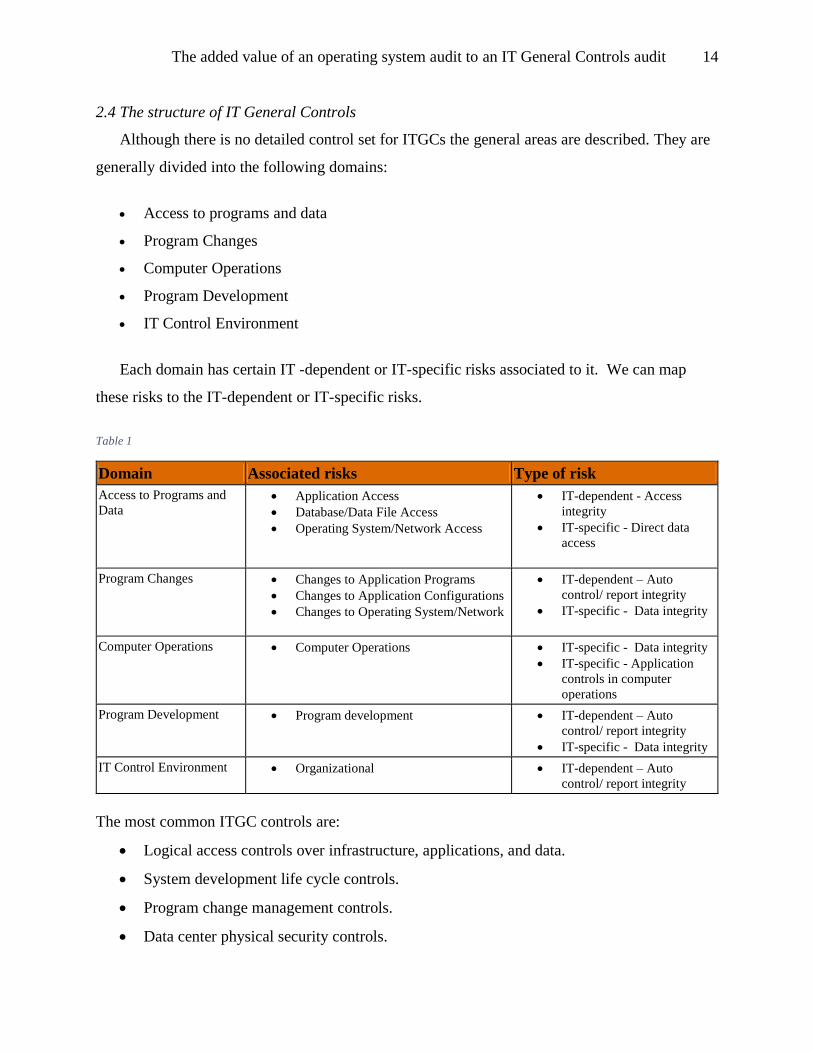

2.4 The structure of IT General Controls

Although there is no detailed control set for ITGCs the general areas are described. They are

generally divided into the following domains:

Access to programs and data

Program Changes

Computer Operations

Program Development

IT Control Environment

Each domain has certain IT -dependent or IT-specific risks associated to it. We can map

these risks to the IT-dependent or IT-specific risks.

Table 1

Domain Associated risks Type of risk

Access to Programs and

Data Application Access

Database/Data File Access

Operating System/Network Access

IT-dependent - Access

integrity

IT-specific - Direct data

access

Program Changes Changes to Application Programs

Changes to Application Configurations

Changes to Operating System/Network

IT-dependent – Auto

control/ report integrity

IT-specific - Data integrity

Computer Operations Computer Operations IT-specific - Data integrity

IT-specific - Application

controls in computer

operations

Program Development Program development IT-dependent – Auto

control/ report integrity

IT-specific - Data integrity

IT Control Environment Organizational IT-dependent – Auto

control/ report integrity

The most common ITGC controls are:

Logical access controls over infrastructure, applications, and data.

System development life cycle controls.

Program change management controls.

Data center physical security controls.

The added value of an operating system audit to an IT General Controls audit 15

System and data backup and recovery controls.

Computer operation controls.

(ITGC, 2013)

Figure 2 shows the domains and associated controls.

IT General Controls

Systems Development

Computer Operations

Program Changes Access to programs and dataIT Control

Environment

Application security administration

Operating system security

administration

Network / connection security

administration

Application logical security

Operating system logical security

Network logical security

Application powerful accounts

Operating system powerful accounts

Network powerful accounts

Database administration

Direct data access via App/Network/

OS/Util.

Specification and authorisation

Constructing

Testing

Implementation

Documenting and training

Segregation of duties

Report integrity

Batch processing

Interface processing

Monitoring of computer processing

Backups

Computer centre operations

Initiation, analysis and design

Contructing

Testing

Data conversion

Implementation

Documentation and training

Segregation of duties

IT strategy

IT organisation

Risk management

Figure 2

(PwC, 2013)

The added value of an operating system audit to an IT General Controls audit 16

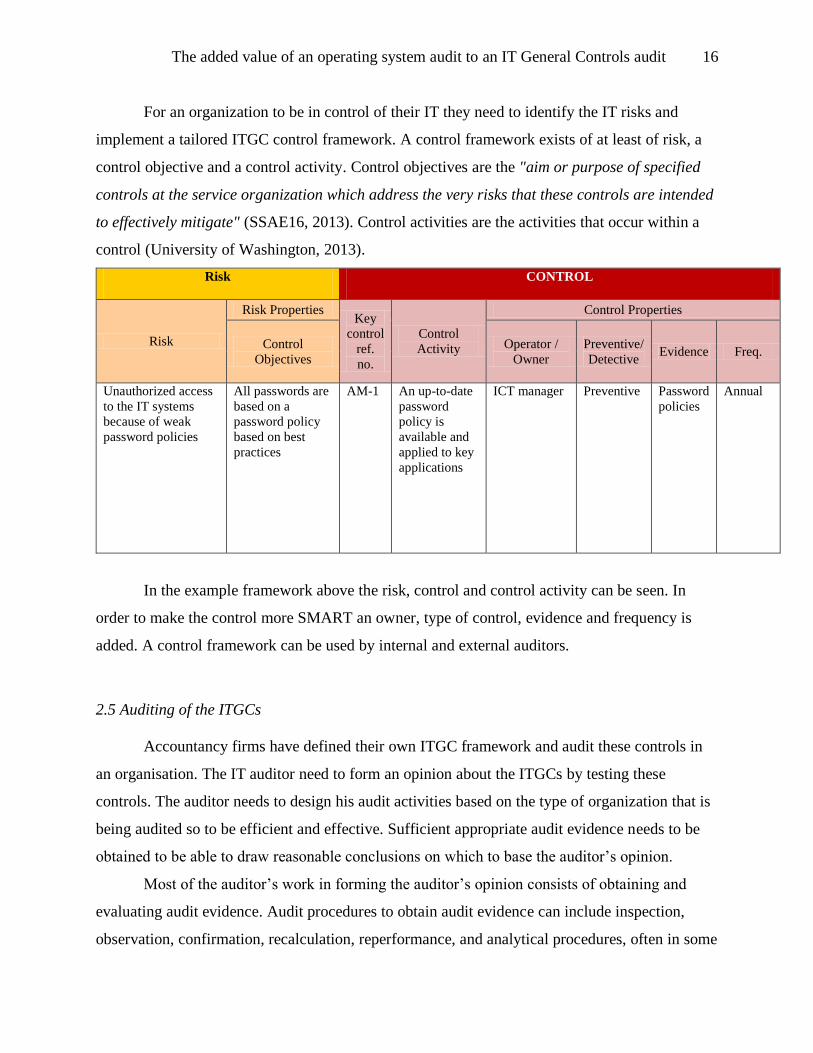

For an organization to be in control of their IT they need to identify the IT risks and

implement a tailored ITGC control framework. A control framework exists of at least of risk, a

control objective and a control activity. Control objectives are the "aim or purpose of specified

controls at the service organization which address the very risks that these controls are intended

to effectively mitigate" (SSAE16, 2013). Control activities are the activities that occur within a

control (University of Washington, 2013).

Risk CONTROL

Risk

Risk Properties Key

control

ref.

no.

Control

Activity

Control Properties

Control

Objectives

Operator /

Owner

Preventive/

Detective Evidence Freq.

Unauthorized access

to the IT systems

because of weak

password policies

All passwords are

based on a

password policy

based on best

practices

AM-1 An up-to-date

password

policy is

available and

applied to key

applications

ICT manager Preventive Password

policies

Annual

In the example framework above the risk, control and control activity can be seen. In

order to make the control more SMART an owner, type of control, evidence and frequency is

added. A control framework can be used by internal and external auditors.

2.5 Auditing of the ITGCs

Accountancy firms have defined their own ITGC framework and audit these controls in

an organisation. The IT auditor need to form an opinion about the ITGCs by testing these

controls. The auditor needs to design his audit activities based on the type of organization that is

being audited so to be efficient and effective. Sufficient appropriate audit evidence needs to be

obtained to be able to draw reasonable conclusions on which to base the auditor’s opinion.

Most of the auditor’s work in forming the auditor’s opinion consists of obtaining and

evaluating audit evidence. Audit procedures to obtain audit evidence can include inspection,

observation, confirmation, recalculation, reperformance, and analytical procedures, often in some

The added value of an operating system audit to an IT General Controls audit 17

combination, in addition to inquiry. Reasonable assurance is obtained when the auditor has

obtained sufficient appropriate audit evidence to reduce audit risk to an acceptably low level.

The sufficiency and appropriateness of audit evidence are interrelated. Sufficiency is the

measure of the quantity of audit evidence. The quantity of audit evidence needed is affected by

the auditor’s assessment of the risks of misstatement (the higher the assessed risks, the more

audit evidence is likely to be required) and also by the quality of such audit evidence (the higher

the quality, the less may be required).

Appropriateness is the measure of the quality of audit evidence; that is, its relevance and

its reliability in providing support for the conclusions on which the auditor’s opinion is based.

The reliability of evidence is influenced by its source and by its nature, and is dependent on the

individual circumstances under which it is obtained (International Standards of Auditing, 2009).

2.6 Information security

The term ‘information security’ means protecting information and information systems

from unauthorized access, use, disclosure, disruption, modification, or destruction in order to

provide

Integrity, which means guarding against improper information modification or

destruction, and includes ensuring information non-repudiation and authenticity;

Confidentiality, which means preserving authorized restrictions on access and disclosure,

including means for protecting personal privacy and proprietary information; and

Availability, which means ensuring timely and reliable access to and use of information.

Which is often depicted in the CIA triad as seen below (Cornell, 2013)

.

The added value of an operating system audit to an IT General Controls audit 18

Figure 3

In order to ensure the confidentiality, integrity and availability of information and

information systems companies often implement an access management, change management,

business continuity and risk management process.

Access to protected information must be restricted to people who are authorized to access

the information. The foundation on which access control mechanisms are built start with

identification and authentication. Identification is an assertion of who someone is or what

something is. Authentication is the act of verifying a claim of identity. Information security uses

cryptography to transform usable information into a form that renders it unusable by anyone

other than an authorized user; this process is called encryption.

Change management is a formal process for directing and controlling alterations to the

information processing environment. This includes alterations to desktop computers, the

network, servers and software. The objectives of change management are to reduce the risks

posed by changes to the information processing environment and improve the stability and

reliability of the processing environment as changes are made.

Business continuity is the mechanism by which an organization continues to operate its

critical business units, during planned or unplanned disruptions that affect normal business

operations, by invoking planned and managed procedures.

Risk management is the process of identifying vulnerabilities and threats to the

information resources used by an organization in achieving business objectives, and deciding

what countermeasures, if any, to take in reducing risk to an acceptable level, based on the value

The added value of an operating system audit to an IT General Controls audit 19

of the information resource to the organization (CISA, 2006). These four processes are also part

of the ITGC audit as described in paragraph 2.4 (Information security, 2013).

2.7 Operating System security

Businesses store their financial information on computer systems. These computer

systems enable employees to access, modify and delete information. The operating system is the

heart of the computer system that allows hardware and software applications to communicate

with each other and share resources as can be seen in the multiple definitions of an operating

system.

Software designed to control the hardware of a specific data-processing system in order to allow

users and application programs to make use of it. (Answers, 2013)

The collection of software that directs a computer's operations, controlling and scheduling the

execution of other programs, and managing storage, input/output, and communication

resources. (Dictionary, 2013)

An operating system (OS) is software, consisting of programs and data, which runs on computers

and manages the computer hardware and provides common services for efficient execution of

various application software. (Wikipedia, 2013)

For example consider a program that allows a user to enter her password. The operating

system provides access to the disk device on which the program is stored, access to device

memory to load the program so that it may be executed, the display device to show the user how

to enter her password, and keyboard and mouse devices for the user to enter her password. Of

course, there are now a multitude of such devices that can be used seamlessly, for the most part,

thanks to the function of operating systems. The most used operating systems by businesses are

Microsoft Windows and the different UNIX variants.

Ensuring the secure execution of all processes depends on the correct implementation of

resource and scheduling mechanisms. First, any correct resource mechanism must provide

The added value of an operating system audit to an IT General Controls audit 20

boundaries between its objects and ensure that its operations do not interfere with one another.

For example, a file system must not allow a process request to access one file to overwrite the

disk space allocated to another file. Also, file systems must ensure that one write operation is not

impacted by the data being read or written in another operation. Second, scheduling mechanisms

must ensure availability of resources to processes to prevent denial of service attacks. For

example, the algorithms applied by scheduling mechanisms must ensure that all processes are

eventually scheduled for execution. These requirements are fundamental to operating system

mechanisms.

A lot of people, or at least lots of email addresses, web sites, and network requests, want

to share stuff that aim to circumvent operating system security mechanisms and cause computers

to share additional, unexpected resources. The ease with which malware can be conveyed and the

variety of ways that users and their processes may be tricked into running malware present

modern operating system developers with significant challenges in ensuring the security of their

system’s execution.

There’s an ongoing battle between operating system developers and hackers to secure and

breach operating systems. The term “secure operating system” is both considered an ideal and an

oxymoron. Systems that provide a high degree of assurance in enforcement have been called

secure systems, or even more frequently “trusted” systems. However, it is also true that no

system of modern complexity is completely secure. The difficulty of preventing errors in

programming and the challenges of trying to remove such errors means that no system as

complex as an operating system can be completely secure. (Jaeger, 2008)

Because an operating system plays such a vital role in an information system its security

has a direct impact on applications and their data as can be seen in figure 3. All data that comes

from outside the system needs to pass the operating system layer.

The added value of an operating system audit to an IT General Controls audit 21

Figure 3

Operating system settings are highly customizable in order to be tailored to the needs of

the user. This means that the user is also responsible for a secure implementation of configurable

settings.

2.8 Operating System configuration for Windows Server 2008

Apart from the inherent design of the operating system the configuration of parameters

also plays a role in the secureness of the operating system. There are many types of operating

systems that can be configured in a variety of different ways. Researching all these operating

systems would be too exhausting for this thesis. This research will therefore look at the settings

for one of the most used operating systems for servers, Windows Server 2008 (Wikipedia, 2013).

Windows Server 2008 was released by Microsoft on February 27, 2008. It is the successor to

Windows Server 2003.

The Center for Internet Security (CIS) helps organizations improve their security

posture by reducing risk resulting from inadequate technical security controls. One way of doing

The added value of an operating system audit to an IT General Controls audit 22

this is by publishing security configuration benchmarks for operating systems. The security

configuration benchmark for Windows Server 2008 was released on September 30th, 2011 and

includes many parameter settings recommendations (CIS, 2011). Each recommendation contains

a description, rationale, remediation, audit, default value and reference. For example for the

enforce password history control we see the following recommendation.

1.1.1 Enforce password history Description This control defines the number of unique passwords a user must leverage before a previously

used password can be reused. For all profiles, the recommended state for this setting is 24 or

more passwords remembered.

Rationale Enforcing a sufficiently long password history will increase the efficacy of password-based

authentication systems by reducing the opportunity for an attacker to leverage a known

credential. For example, if an attacker compromises a given credential that is then expired,

this control prevents the user from reusing that same compromised credential.

Remediation To establish the recommended configuration via GPO, set the following to the value

prescribed above:

Computer Configuration\Windows Settings\Security Settings\Account

Policies\Password Policy\Enforce password history

Audit Navigate to the GPO articulated in the Remediation section and confirm it is set as prescribed.

Default Value 24 passwords remembered

References CCE-2237-6

There are more than a hundred recommendations like this for Windows Server 2008. This

shows one of the complexities of securing the operating system. It is always a balance of security

versus usability. All these settings can be broken down and ordered into the following categories

or controls.

Category Settings

Accounts Password and account settings. These settings all

contribute to the logical access security.

Audit Policy Settings regarding the logging of events and changes to

the operating system. For example the logging of

access attempts and changes to user rights and policies.

Detailed Security Auditing These are more specified auditing settings like the

logging of changes to the security state of the system,

when a register object is accessed or whether the

results of a validation test are logged

Event Log These settings are about the retention of the system

logging and some technical settings.

Windows Firewall Settings in this area are about the setup of the Windows

Firewall that is part of operating system.

Windows Update Settings regarding the installation and download of

new patches

The added value of an operating system audit to an IT General Controls audit 23

User Account Control Settings regarding the behaviour of the operating

system when operations are being performed that

require elevated privileges

User Rights Defines which type of users can do certain types of

actions like logon, shutdown or change the system

time.

Security Options Specific security settings fall in this category like

interactive logon, Microsoft network client, network

access and system settings.

Terminal Services Remote desktop settings

Internet Communication Settings regarding the use of local resources over a

network connection like printing or publishing files.

Additional Security Settings Additional settings like disable remote desktop sharing,

turn of autoplay and registery policy processing.

Most of the categories would fall under the ITGC domain ‘Access to programs and data’

except for the Windows Update category which would fall under ‘Computer operations’.

2.9 Influence of operating system settings on the IT General Controls

As can be seen in previous paragraphs the operating system is only one of the parts that

together can form a secure information system environment. Logically it protects the

applications, data and system resources but once a program or user is allowed access it cannot

control the implications of that access. For example the operating system cannot control the

behaviour of a user within an application or the content of data that is being send and received.

Nevertheless it is an essential part of the security because it does protect data from external and

internal threats in a way that applications cannot do.

There is not one setting that determines how secure an operating system is and therefor

an auditor always has to look at combination of settings. Some settings can have a higher impact

than others. Not being able to rely on the operating system for access to programs and data

controls undermines the application controls. In practice most operating systems including

Windows Server 2008 have a basic level of security configured which means that reliance on the

operating system is not binary and can be partial.

Financial statement audits always have a time period in scope. In order for an auditor to get

some comfort over the operating system settings for a certain period the changes to the settings

need to be logged. Which means an auditor either has to rely on the change management process

or has to inspect the event logs that the server generates (if this logging is enabled).

The added value of an operating system audit to an IT General Controls audit 24

3. Hypotheses

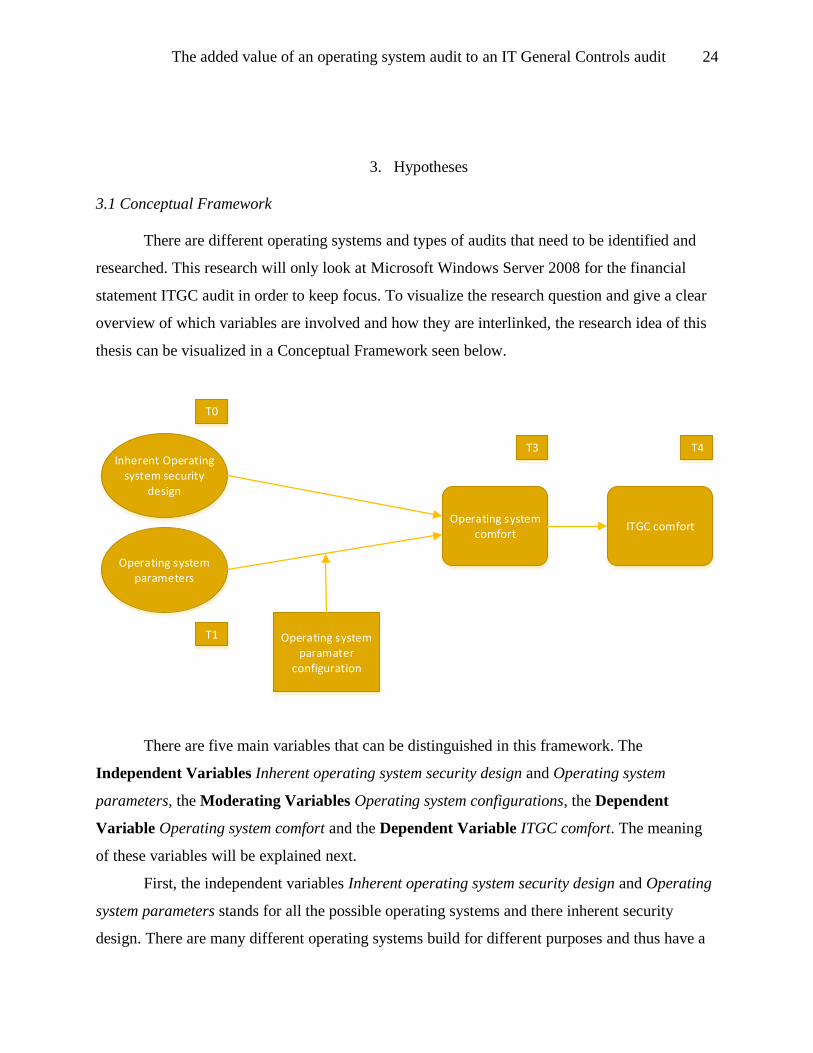

3.1 Conceptual Framework

There are different operating systems and types of audits that need to be identified and

researched. This research will only look at Microsoft Windows Server 2008 for the financial

statement ITGC audit in order to keep focus. To visualize the research question and give a clear

overview of which variables are involved and how they are interlinked, the research idea of this

thesis can be visualized in a Conceptual Framework seen below.

Inherent Operating system security

design

Operating system parameters

Operating system comfort

ITGC comfort

Operating system paramater

configuration

T0

T1

T3 T4

There are five main variables that can be distinguished in this framework. The

Independent Variables Inherent operating system security design and Operating system

parameters, the Moderating Variables Operating system configurations, the Dependent

Variable Operating system comfort and the Dependent Variable ITGC comfort. The meaning

of these variables will be explained next.

First, the independent variables Inherent operating system security design and Operating

system parameters stands for all the possible operating systems and there inherent security

design. There are many different operating systems build for different purposes and thus have a

The added value of an operating system audit to an IT General Controls audit 25

different security design. A company has to think about this when they choose the operating

system for their applications. Next to the inherent design they also have to make sure that the

operating system is setup and configured according to their security needs

Secondly, Operating system configuration is the moderating variable in this framework.

It entails the actual configuration of the operating system. This variable influences the dependent

variables based on parameter configuration.

The forth variable Operating system comfort is one of the dependable variables in this

framework. It entails the combination of security design and configuration leading to a level of

comfort that can be placed on the operating system.

Finally, the dependent variable ITGC comfort is about the contribution of the Operating

system comfort to the IT General Controls audit. If an audit looks at application controls,

Operating system comfort must be obtained.

3.2 Hypotheses

With the conceptual framework set up, specific working hypothesis can be set up to test

the framework. Working hypotheses (WH) are a “provisional, working means of advancing

investigation”; they lead to the discovery of other critical facts (Dewey, 1938). Working

hypotheses are linked to exploratory studies (Shields, 2006). They are never proven but are

supported by empirical evidence.

Building on the research questions the working hypothesis will explore the subject in

more detail. Based on the literature background the following working hypothesis were created.

WH1: An operating system parameter audit will only give comfort over the operating

system layer

As depicted in Figure 3 the operating system is the layer between applications, data and the

network. Auditing the operating system parameters will therefor only give comfort over the

implementation of information security on the OS layer.

The added value of an operating system audit to an IT General Controls audit 26

WH2: Operating system comfort is essential for reliance on application controls

Because the operating system manages system resources and data the systems needs to be

secured in a way that minimizes the risk of unauthorized use of the system resources. Using an

application, even in a client/server architecture, requires some form of operating system access

and thus exposes the application and data to certain threats.

3.3 Control Variables

In order to answer the research question and the sub-questions the relationships between

the main variables have to be tested. The formulated working hypotheses can then be, based on

the results either be supported or not. However, it is possible that the results of this study are

influenced by other variables that were not included in the framework. For this study it will be

hard to exclude all the other variables that might influence the Dependent Variable ITGC comfort

and thus influence the outcome of this study.

The Inherent Operating system security design is a variable that greatly influences the

Operating system comfort but is tricky to measure. As (Jaeger, 2008) argues that no operating

system of great complexity can be completely secure a feeling of its security can be obtained by

looking at its history of secureness and design philosophy.

Although the methodology for performing an IT General Control audit tries to be as

objective as possible there is still a lot of room for an auditor’s opinion and so called professional

judgment. Companies are almost never 100% alike, technology develops fast and there are many

variables that influence IT security, yet auditors often work on a tight time schedule with limited

budget. Therefore an auditor has to form an opinion as best as possible and can only give

reasonable or limited assurance.

The added value of an operating system audit to an IT General Controls audit 27

4. Case study methodology

4.1 Research Methods

The purpose of this research is to find out what the added value of an operating system

audit is for the IT General Controls. In order to do this, this study tries to find out the theoretical

place of an operating system in the IT General Control framework and audit methodology.

Secondly, an operating system parameter audit is performed and the added value to the ITGC

audit is discussed. The methodology used for exploring the hypothesizes is a case study.

This study uses the hypothetico-deductive method that according to (Sekaran, 1992)

involves seven research steps: observation, preliminary information gathering, theory

formulation, hypothesizing, further scientific data collection, data analysis and logically

deducing conclusions from the results obtained.

4.1.1 Observation

By being a professional auditor for a big firm and studying IT-audit the researcher is

aware of discussions and hot-topics in the field of IT-audit. The company the researcher works

for has been using a tool the last couple of years to audit operating system parameters and the

results of these settings are being sent back to audit teams. It was observed that auditors often do

not know how to interpret the results and what the added value to the audit is. They noticed that

it makes an impact at the client if they present the results but the exact meaning and impact for

the ITGC audit as part of the financial statement audit is unclear. The researcher felt like this was

an interesting area that lacked enough academic or pragmatic literature and needs to be clarified.

4.1.2 Preliminary information gathering

Preliminary information gathering is the search for information in order to build up the

researchers understanding towards the area (Sekaran, 1992). In order to do so a research proposal

was written. Google, work experience and the PwC audit guide were the basis for further

preliminary information gathering. The topics of financial statement audits, IT General Controls,

auditing and operating systems were explored. Most concrete information was not found in

academic literature but in white-papers and best-practices.

The added value of an operating system audit to an IT General Controls audit 28

4.1.3 Theory formulation

The theory formulation is done by literature research and is necessary in order to get a

good understanding of what is already known about the topic to save valuable time and make

sure the wheel doesn’t get invented for the second time. Not only operating system and IT

General Control literature is relevant for the theory formulation but also related literature in order

to develop a theoretical framework. The goal of this theoretical framework is to put the topic in

perspective.

Most of the literature research was done via Google and Google Scholar which can

search through many (academic) databases. Beside online literature research the researcher has

access to internal audit methodology material from PwC, one of the four big accountancy and

consulting firms, in the form of the PwC audit guide. This guide describes the companies audit

methodology in order to deliver high quality audits.

4.1.4 Hypothesizing

From the theoretical framework educated guesses were made regarding the outcome of

the research question. These working hypotheses are presented in chapter 3.2. They represent a

tentative statement of a relationship between two variables that have yet to be empirically tested.

This study will try to test these hypotheses and the empirical results will either hold and support

the hypotheses or discard it.

4.1.5 Further scientific data collection

In order to test the hypotheses further scientific data has to be collected. In order to find

out about the added value of an operating system audit this study will perform an operating

system audit at three companies that uses Microsoft Windows Server 2008 as platform for their

IT environment.

4.1.5.1 The operating system design

In order to get an understating of the inherent operating system security design, literature

research is performed by looking at the builders design philosophy, responsiveness to security

issues and global opinion.

The added value of an operating system audit to an IT General Controls audit 29

4.1.5.2 The operating system parameters

Based on the CIS best practice a parameter scan will be performed at a company. The

researcher will use his professional network to find three companies willing to do an operating

system parameter scan.

The researcher will provide a script that companies need to run on their Windows Server

2008 Domain Controller. This script will check the parameters and output the results into a text

(.txt) file. The results of this file be analyzed using a tool called Easy2Audit. Easy2Audit is a

benchmarking website where you can upload the results of the script and it will generate a

graphical representation of the results.

4.1.6 Data analysis and conclusion

After all the scans are performed the case information per company will be stated and the

results will be evaluated. The research will make use of Easy2Audit’s benchmark tool to make a

graphical representation of the results from whereon the researcher will further investigate. Next

to that the parameters, baselines values and results will be put into a table.

For the baseline, the recommended settings for an enterprise domain controller are used

because we are testing the enterprise domain controllers. The other recommended settings in the

CIS baseline are for Special Security – Limited Function (SSLF) systems. The companies in our

sample do not have a higher than average risk profile so it was chosen not to use the

recommended SSLF settings.

4.2 Sample selection

The samples used in the research are companies that run a Microsoft Windows office

environment that is managed by Active Directory and the domain controllers run on Microsoft

Windows Server 2008. Domain controllers distribute the companies IT policies and

configuration settings to all computers that are in the office network. This means that a domain

controller is a key system in a network and needs to be secure. The configuration of the domain

controller does not necessarily apply to the computers in the domain but it can indicate the level

of thought that was given to security. If a domain controller is compromised a hacker has the

potential to access all systems that are part of the Active Directory network.

The added value of an operating system audit to an IT General Controls audit 30

5. Case study findings

Three Dutch companies participated in this study which are anonymized for privacy and

security reasons. This study took place between January 2013 and June 2013. The system

administrators first tested the scripts on their test environment before running them on the

production. It took each administrator about an hour to test the scripts, run the scripts on the

production environment and send the results.

5.1 Company profile

5.1.1 Company A

The first company is a medium sized company with about 500 employees active in the

food industry. Their ERP system, SAP, is used primarily for sales, purchasing and finance. They

run a Windows environment which is administrated by two domain controllers. There is no

single sign-on so in order to login to SAP a separate username and password have to be used.

5.1.2 Company B

The second company is a small company operating in the gambling machine market.

They use Exact for their enterprise resource planning and run a Windows environment.

5.1.3 Company C

Company C is a medium sized software company operating in the supply chain logistics

industry. Their ERP system, SAP, is used primarily for sales and purchasing. They run a

Windows environment which is administrated by two domain controllers. There is no single

sign-on so in order to login to SAP a separate username and password have to be used.

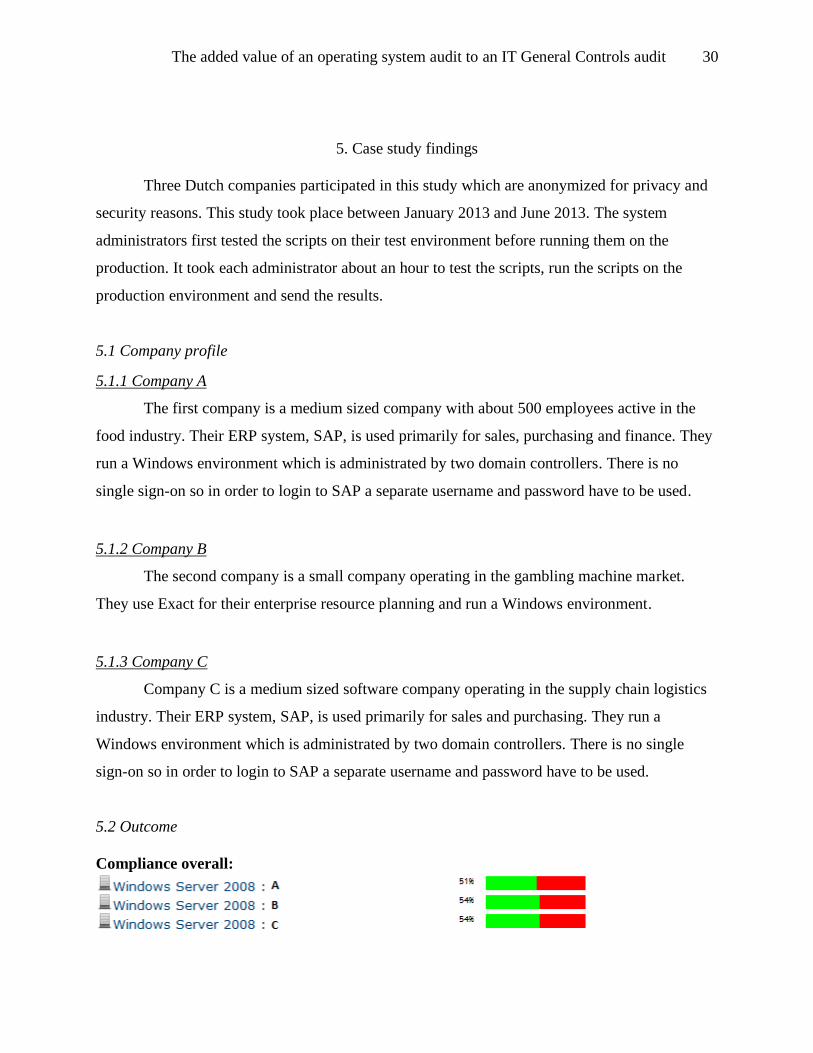

5.2 Outcome

Compliance overall:

The added value of an operating system audit to an IT General Controls audit 31

Company A:

Company B:

Company C:

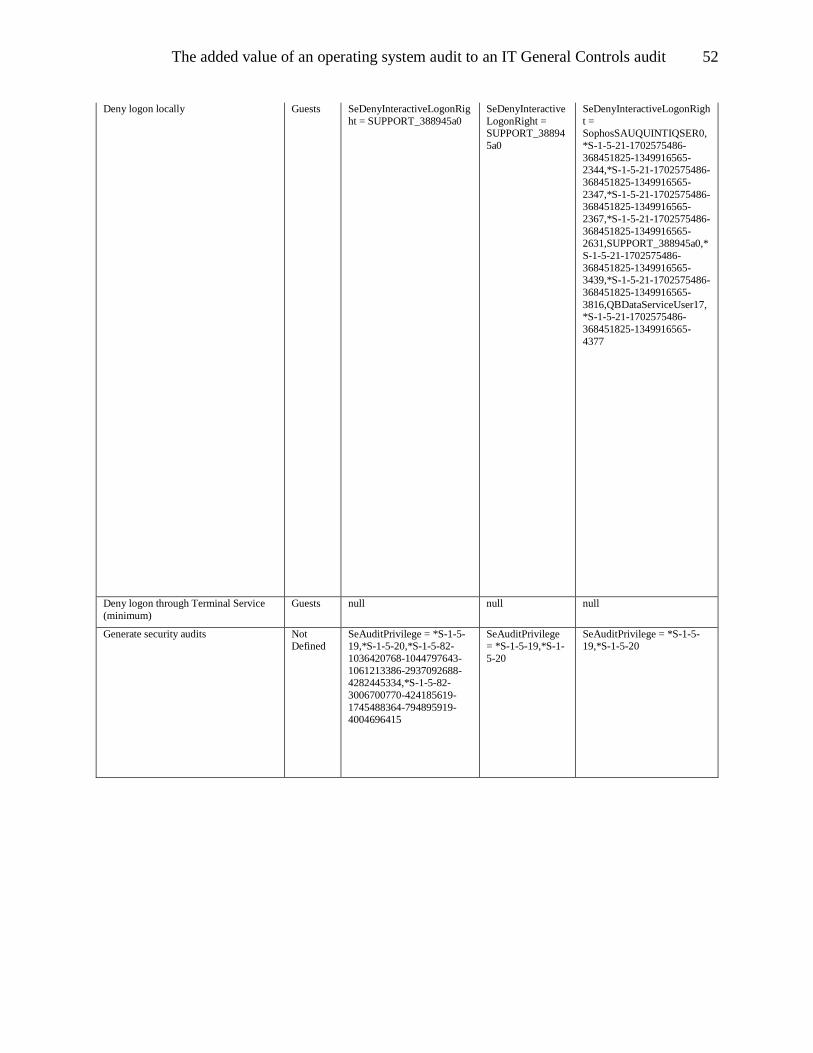

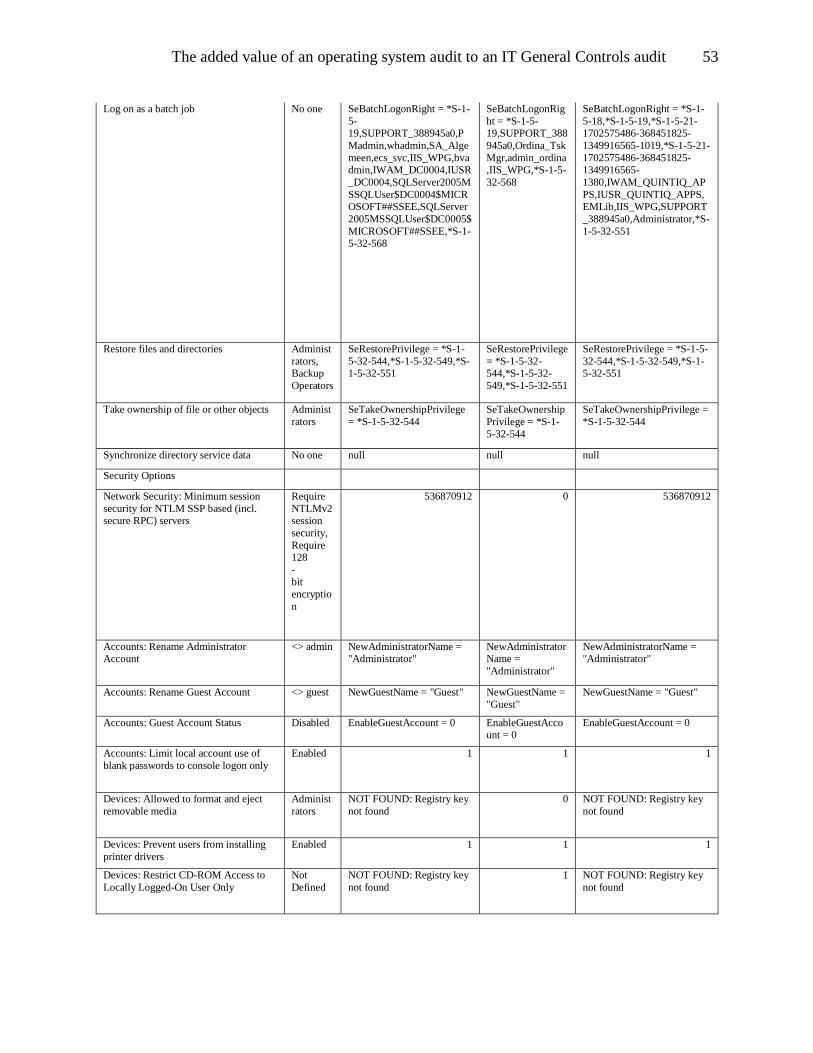

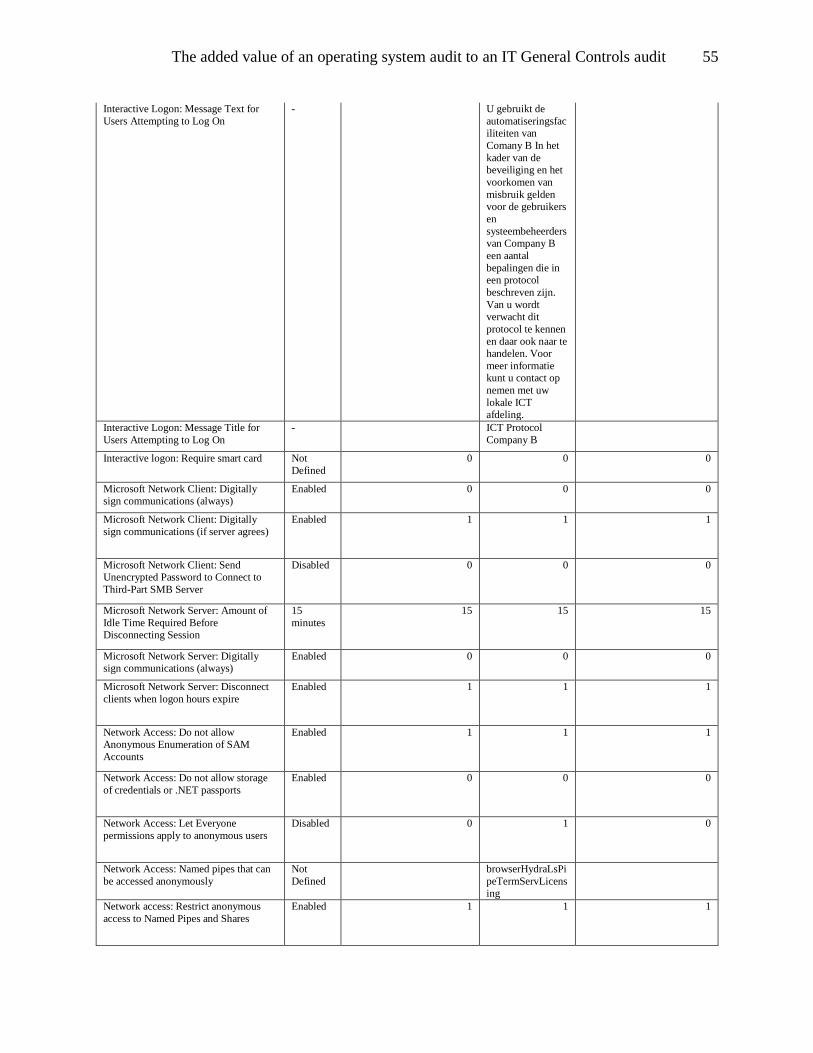

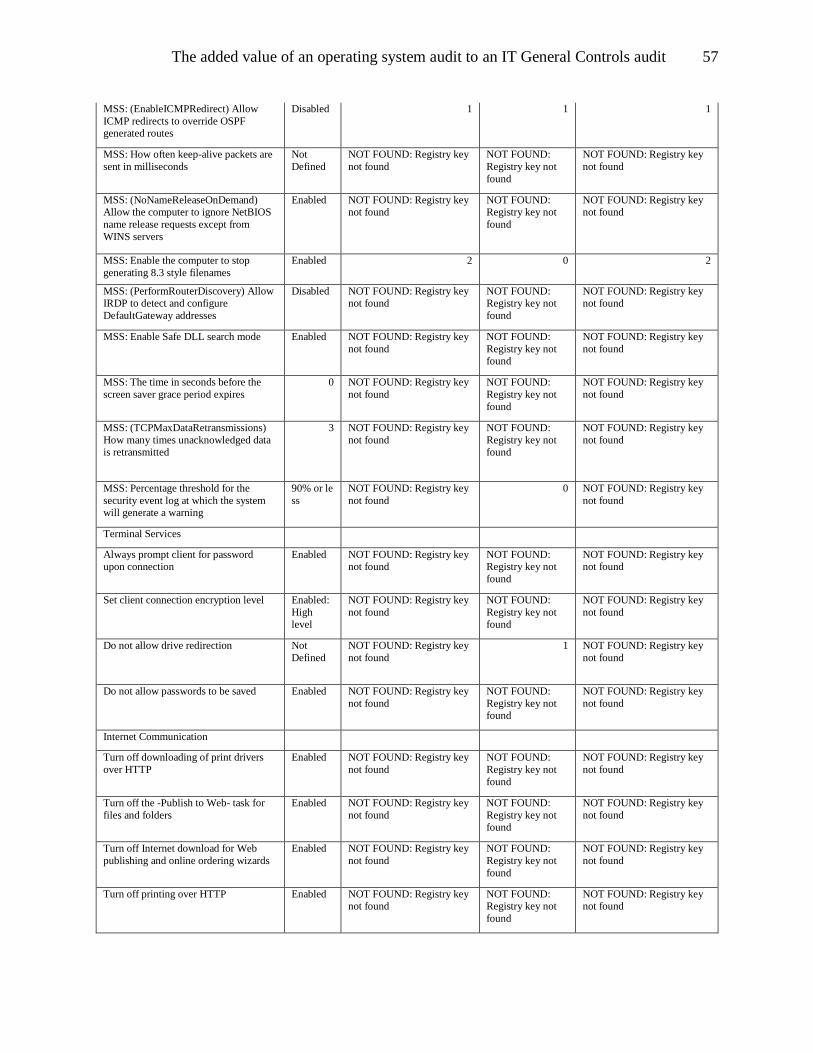

The more detailed results can be found in Appendix I.

The added value of an operating system audit to an IT General Controls audit 32

5.3 Analysis of results

In this paragraph, the results will be discussed that were obtained from the scans and the

theoretical framework. First the parameter categories and their audit impact are discussed. Once

the audit impact of the parameters is determined non-technical factors are discussed. A complete

overview of the results can be found in chapter 5. Thereafter results aside from the Working

Hypothesizes are presented.

5.3.1 Accounts

In the ITGC framework the account settings can be placed in the Access to programs and

data domain and they directly influence the logical operating system security. They can also

influence application and data access if there are no further mitigation controls defined.

Finding Impact Likelihood Risk

Decreased efficacy of the

password based

authentication control

Unauthorized users get

administrator access to

the critical systems, their

applications and data.

Unauthorized access to

financial data and

applications can lead to

misstatement, fraud and

can threaten the business

continuity

Medium Medium. This control can

directly influence access

to financial data and thus

cause financial

misstatements

Our results show that none of the companies have implemented a secure password policy. In

company C the password based authentication control is operating at a bare minimum without a

minimum password length making it simple to guess or brute force attack the password.

5.3.2 Audit policy

In the ITGC framework the audit policy can be placed in the Computer operations

domain under monitoring of computer processing. The event log is filled based on the audit

policy. This can be classified as a detective control for inspection of (potential) problems

The added value of an operating system audit to an IT General Controls audit 33

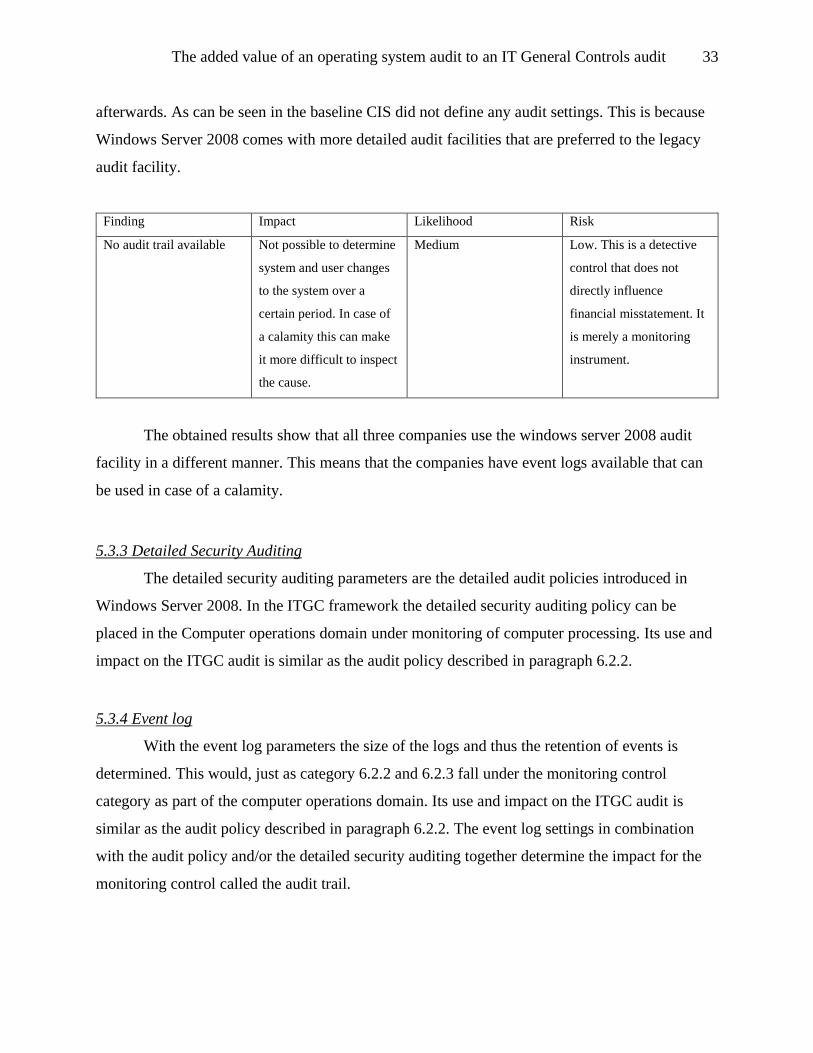

afterwards. As can be seen in the baseline CIS did not define any audit settings. This is because

Windows Server 2008 comes with more detailed audit facilities that are preferred to the legacy

audit facility.

Finding Impact Likelihood Risk

No audit trail available

Not possible to determine

system and user changes

to the system over a

certain period. In case of

a calamity this can make

it more difficult to inspect

the cause.

Medium Low. This is a detective

control that does not

directly influence

financial misstatement. It

is merely a monitoring

instrument.

The obtained results show that all three companies use the windows server 2008 audit

facility in a different manner. This means that the companies have event logs available that can

be used in case of a calamity.

5.3.3 Detailed Security Auditing

The detailed security auditing parameters are the detailed audit policies introduced in

Windows Server 2008. In the ITGC framework the detailed security auditing policy can be

placed in the Computer operations domain under monitoring of computer processing. Its use and

impact on the ITGC audit is similar as the audit policy described in paragraph 6.2.2.

5.3.4 Event log

With the event log parameters the size of the logs and thus the retention of events is

determined. This would, just as category 6.2.2 and 6.2.3 fall under the monitoring control

category as part of the computer operations domain. Its use and impact on the ITGC audit is

similar as the audit policy described in paragraph 6.2.2. The event log settings in combination

with the audit policy and/or the detailed security auditing together determine the impact for the

monitoring control called the audit trail.

The added value of an operating system audit to an IT General Controls audit 34

5.3.5 Windows Firewall

The windows firewall controls the incoming and outgoing connections and is thus part of

the access to programs and data domain. Companies often have a dedicated firewall controlling

all the network traffic. This often results in a de-activated Windows Firewall which can be seen

in the results where none of the companies have any firewall rules determined. An auditor should

establish that the client uses a dedicated firewall. If this is not the case then the whole network is

open for the outside world and that alone would pose a serious security hazard. The risk analyses

done for this category assumes a dedicated firewall.

Finding Impact Likelihood Risk

No firewall settings

configured.

Administrators can

overwrite Group policy

settings that exposes the

system to remote attacks.

However, in case of a

dedicated firewall this

might have no impact

Low. Low. All network activity

is controlled by a

dedicated firewall.

5.3.6 Windows Update

The windows update parameters define how Windows handles available updates. This

would fall under the Access to programs and data domain since ensuring that the latest updates

and patches are installed minimizes the potential of a successful hack through a known

vulnerability. However, the settings alone do not tell anything about the patch level of the server

and thus not much can be said about the patch level of the machine.

Finding Impact Likelihood Risk

Windows update settings

do not enforce the

positive behavior of

installing updates

No impact. Low. Low. These settings do no

tell anything about the

patch level of a machine

but can indicate a non-

adequate patch

management process.

The added value of an operating system audit to an IT General Controls audit 35

5.3.7 User Account Control

User Account Control aims to improve the security of Microsoft Windows by limiting

application software to standard user privileges until an administrator authorizes an increase of

elevation. This would ensure that malicious software would not be able to perform administrative

tasks on the operating system. This control would fit under operating system security in the

Access to programs and data domain.

Finding Impact Likelihood Risk

UAC is not enabled

Software uses

administrator operating

system functions to

perform malicious

actions.

Medium Medium. Once a system

is infected with malware

it might perform

malicious actions that

impact the integrity of the

system

In the results we can see that all companies have UAC enabled in some manner. Company C has

implemented in the most secure way so that even admin approval is required for admin accounts.

5.3.8 User Rights

The user rights parameters would also fall under the Access to programs and data

domain. They manage which users and/or user groups can perform certain high risk or

administrative functions. It also impacts some of the system security design functions.

Finding Impact Likelihood Risk

User rights are not setup

based on the least

authorizations principle

Unexpected users can

perform high risk or

administrative functions

which can compromise

the systems availability

and integrity

Medium Medium. The attack

surface is increased

unnecessarily.

In the results we can see that all three companies have defined and limited most user rights to

appropriate users or groups.

The added value of an operating system audit to an IT General Controls audit 36

5.3.9 Security options

The security options parameters are a set of security options influencing various

functionalities like accounts, devices, domain membership, logon, Microsoft network client,

network and system. Operating system security administration is the ITGC topic that this would

be placed in.

Finding Impact Likelihood Risk

Security options do not

adhere to the best practice

Attackers could

potentially benefit from

the security mis-

configuration

compromising the system.

Low Medium. The security

options are not configured

tightly which increases

the chance of a successful

attack.

The companies have set about 60% percent of the security options according to best practice.

5.3.10 Terminal services

With terminal service, users can login to a server from a remote location. The parameters

deal with encryption, the password mechanism and drive redirection. In the ITGC framework we

can find these settings under operating system logical security.

Finding Impact Likelihood Risk

The terminal service

connection is more

vulnerable to eaves

dropping because of the

lower level of encryption.

Attackers can potentially

access remote servers via

a locally saved terminal

service shortcut.

Unauthorized access to

the server through

terminal services.

Medium High. Unauthorized

access through terminal

services makes it easy for

an attacker to compromise

the system.

The added value of an operating system audit to an IT General Controls audit 37

The results default values apply for all except company B, who disabled drive allocations.

5.3.11 Internet Communication

The best practice recommends to disable all unnecessary internet options that come with

Windows Server 2008 for hardening purposes. Operating system security administration in

Access to programs and data would be the ITGC domain this relates to.

Finding Impact Likelihood Risk

Unnecessary internet

options enabled

Increased exposure to

malicious content,

unstable drivers and

potential loss of

information.

Medium Medium. The system has

unnecessary functions

enabled that can disrupt

the system and lead to

information leakage when

an administrators is not

careful.

None of the companies have changed any of the default values leaving these options enabled,

thus unnecessarily increasing their risk.

5.3.12 Additional security settings

The additional security settings are settings that can further harden the system. The

difference with the security options is that the security options can have multiple possible values

and the additional security settings are more binary. Only three out of the 11 settings have to be

set according to the best practice which relate to operating system security and logical access in

the Access to programs and data domain.

Finding Impact Likelihood Risk

Additional security

settings not configured

Increased number of

options that an attacker

can benefit from to

compromise the system

Low Medium. The options that

are not set according to

the best practice can be

key for an attacker to

compromise the system.

The added value of an operating system audit to an IT General Controls audit 38

None of the companies have changed any of the default values leaving these options enabled,

thus unnecessarily increasing their risk.

5.4 Other factors

Aside from the value of the parameter audit there many other factors that can influence

whether an auditor should use an operating system parameter scan. These factors are drawn from

the researchers audit experience.

5.4.1 Costs of the operating system parameter check

Most audits are performed for an agreed upon fee and thus have a limited budget.

Although an operating system parameter check is no rocket science it will take an auditor at least

a couple hours to perform. There are many cases, especially when small companies are audit

which often have a very tight budget, where a couple hours is already quite an expense on the

budget. This means that an auditor will have to decide how to spend his hours most effectively in

order to gain the most comfort.

5.4.2 Type of operating system(s) in use

Although there are baselines for the most common operating systems it is possible that a

company uses a legacy or customized operating system. In these cases it will be a time

consuming task to get any comfort about that operating system and comfort needs to be obtained

in a different manner.

5.4.3 No extra comfort

There could be situations where testing the operating system parameters would lead to no

extra comfort. For example when a server or computers are not connected to an external

network. When it is known that the ITGC audit will lead to limited or no-comfort the additional

comfort obtained by performing an operating system audit will be minimal.

The added value of an operating system audit to an IT General Controls audit 39

5.4.4 Politics and time

Companies can be reluctant to perform scripts from third-parties, such as the auditor,

because they fear it can disrupt the system. In these cases the scripts will need to go through a

test procedure before they can be ran on a production environment. This can take quite some

time depending on the company’s organization as it has to go through (multiple) steps of

approval. This might influence the usability of an operating system parameter audit because of

the time factor. Some companies might outright refuse to run a script on their server which

means the auditor will have to inspect the settings himself or find some other way to obtain them,

probably increasing the time-spend and thus the costs.

The added value of an operating system audit to an IT General Controls audit 40

6. Validation of hypotheses

In this chapter the working hypotheses are discussed.

6.4.1 WH1: An operating system parameter audit will only give comfort over the operating

system layer

As noted in paragraph 6.2 the parameters influence the access to programs and data and

computer operations ITGC domains. Within these domains operating system security, operating

system logical security, operating system powerful accounts, network powerful accounts, direct

data access and network logical security are influenced. Because the operating system is the

heart of a system it is logical that all these categories are influenced. The results obtained from

the operating system audit give all the information needed to formulate an opinion regarding the

operating system layer. However the information can also tell the auditor something regarding

the security policy of the company, the manner of hardening they applied and their user account

policy. The results support the working hypotheses in the sense that it will only give comfort

about the operating system layer. It does however give an auditor additional information that

might influence his audit approach and opinion.

6.4.2 WH2: Operating system comfort is essential for reliance on application controls

There are many settings that an attacker can use to eventually compromise a system.

Once access, or worse, administrator access is obtained an attacker can further penetrate the

system directly accessing or modifying unprotected data. Secured data can also be stolen or

attempts can be made to breach the security. User account data can be tried to log into

applications and if a company has single sign-on enabled access is immediately obtained. All this

can lead to a bypass of application controls. Because of the layers in computer systems, comfort

can only be obtained of a layer if the layers below are reliable. The literature and results support

the working hypothesis that operating system comfort is essential for reliance on application

controls.

The added value of an operating system audit to an IT General Controls audit 41

7. Conclusions

The intention of this research was to determine the added value of an operating system

audit to the IT General Controls audit by answering the research question ‘How does a baseline

security scan on operating system parameters add value to an ITGC audit?’. A literature study

provided the context and role of operating systems within the ITGCs. A best practice for

Windows Server 2008 configuration settings was used to test three companies against this

baseline. This led to (1) a risk analysis of the security categories and (2) insight into the

company’s compliance and the link between the parameters. To answer the research question

three sub questions have to be answered.

First of all, what is the place of operating system parameters in the IT General Control

environment? As can be seen in the analysis of results, chapter 5.3, all the parameters were

analysed and the results show that they can be linked with the access to programs and data and

computer operations ITGC domains. This demonstrates that they have a place in the IT General

Control framework and thus should be taken into account when performing an ITGC audit.

Secondly, what kind of comfort and assurance can result from an operating system

parameter baseline scan to the ITGC audit? It was found that there are many parameters that an

attacker can leverage to compromise an operating system. Once access, or worse, administrator

access is obtained an attacker can further penetrate the system directly accessing or modifying

unprotected data. Secured data can also be stolen or attempts can be made to breach its security.

User account data can be used to log into applications and if a company has single sign-on

enabled access is immediately obtained. All of this can lead to a bypass of application controls.