the activity base a measure of what causes the incurrence of a variable cost. units produced miles...

TRANSCRIPT

The Activity Base

A measure of what causes the

incurrence of a variable cost.

A measure of what causes the

incurrence of a variable cost.

UnitsUnitsproducedproduced

UnitsUnitsproducedproduced

Miles driven

Miles driven

Machine hours

Machine hours

Labor hours

Labor hours

5-1

Minutes Talked

To

tal L

on

g D

ista

nce

Tel

eph

on

e B

illTrue Variable Cost Example

A variable cost is a cost whose total dollar amount varies in direct proportion to

changes in the activity level.

Your total long distance telephone bill is based on how many

minutes you talk.

5-2

Minutes Talked

Per

Min

ute

Tel

eph

on

e C

har

ge

Variable Cost Per Unit Example

A variable cost remains constant if expressed on a per unit basis.

The per minute cost of long distance calls

is constant, for example, 10¢ per

minute.

5-3

Extent of Variable CostsThe proportion of variable costs differs across organizations. For example . . .

A public utility withA public utility withlarge investments inlarge investments inequipment will tendequipment will tend

to have to have fewerfewervariable costs.variable costs.

A public utility withA public utility withlarge investments inlarge investments inequipment will tendequipment will tend

to have to have fewerfewervariable costs.variable costs.

A manufacturing companyA manufacturing companywill often have will often have manymany

variable costs.variable costs.

A manufacturing companyA manufacturing companywill often have will often have manymany

variable costs.variable costs.

A merchandising companyA merchandising companyusually will have a usually will have a highhigh

proportionproportion of variable costs of variable costslike cost of sales.like cost of sales.

A merchandising companyA merchandising companyusually will have a usually will have a highhigh

proportionproportion of variable costs of variable costslike cost of sales.like cost of sales.

A service companyA service companywill normally have a will normally have a highhigh

proportionproportion of variable costs. of variable costs.

A service companyA service companywill normally have a will normally have a highhigh

proportionproportion of variable costs. of variable costs.

5-4

Step-Variable CostsA resource that is obtainable only in large chunks (such as maintenance workers) and whose costs

increase or decrease only in response to fairly wide changes in activity.

A resource that is obtainable only in large chunks (such as maintenance workers) and whose costs

increase or decrease only in response to fairly wide changes in activity.

Volume

Co

st

5-5

RelevantRange

A straight line closely

approximates a curvilinear

variable cost line within the

relevant range.

A straight line closely

approximates a curvilinear

variable cost line within the

relevant range.

Activity

To

tal

Co

st

Economist’sEconomist’sCurvilinear Cost Curvilinear Cost

FunctionFunction

The Linearity Assumption and the Relevant Range

Accountant’s Straight-Line Accountant’s Straight-Line Approximation (constant Approximation (constant

unit variable cost)unit variable cost)

5-6

Number of Local Calls

Mo

nth

ly B

asic

T

elep

ho

ne

Bill

Total Fixed Cost Example

Your monthly basic telephone bill is

probably fixed and does not change when you make more local calls.

A fixed cost is a cost whose total dollar amount remains constant as the activity level changes.

5-7

Number of Local Calls

Mo

nth

ly B

asic

Tel

eph

on

e B

ill p

er L

oca

l Cal

l

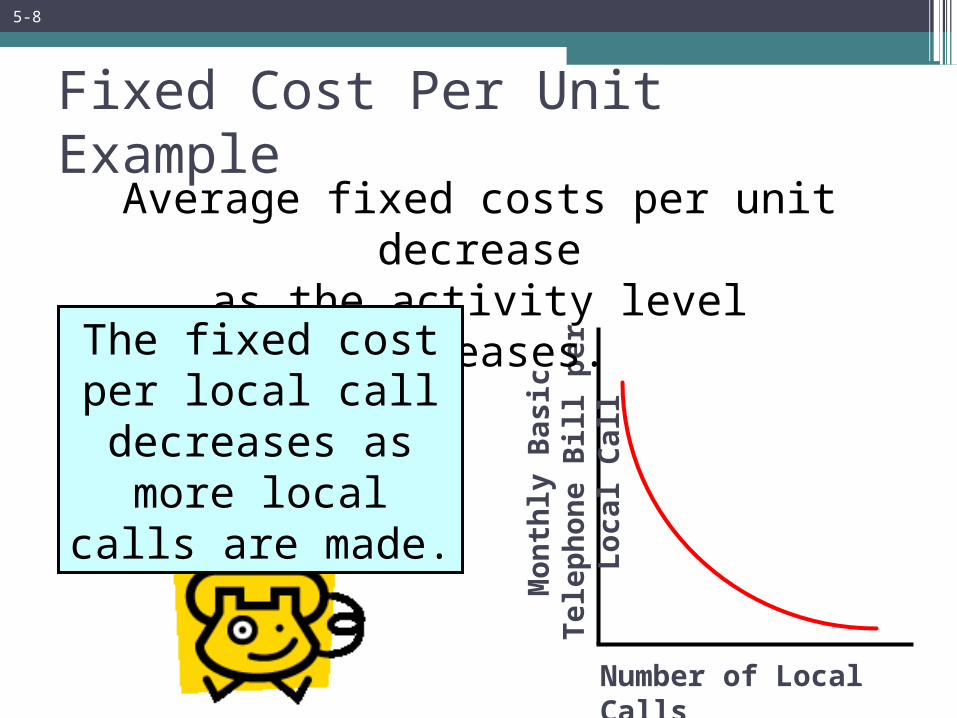

Fixed Cost Per Unit ExampleAverage fixed costs per unit decrease

as the activity level increases.

The fixed cost per local call decreases as more local calls

are made.

5-8

ExamplesAdvertising and Research and Development

ExamplesAdvertising and Research and Development

ExamplesDepreciation on Buildings and

Equipment and Real Estate Taxes

ExamplesDepreciation on Buildings and

Equipment and Real Estate Taxes

Types of Fixed Costs

DiscretionaryMay be altered in the short-term by current managerial decisions

DiscretionaryMay be altered in the short-term by current managerial decisions

CommittedLong-term, cannot be significantly reduced

in the short-term.

CommittedLong-term, cannot be significantly reduced

in the short-term.

5-9

The Trend Toward Fixed Costs

The trend in many industries is toward greater fixed costs relative to variable costs.

As machines take overAs machines take overmany mundane tasksmany mundane taskspreviously performedpreviously performed

by humans, by humans, ““knowledge workersknowledge workers””

are demanded forare demanded fortheir minds rathertheir minds rather

than their muscles.than their muscles.

As machines take overAs machines take overmany mundane tasksmany mundane taskspreviously performedpreviously performed

by humans, by humans, ““knowledge workersknowledge workers””

are demanded forare demanded fortheir minds rathertheir minds rather

than their muscles.than their muscles.

Knowledge workersKnowledge workerstend to be salaried,tend to be salaried,highly-trained, andhighly-trained, and

difficult to replace. Thedifficult to replace. Thecost to compensatecost to compensate

these valued employeesthese valued employeesis is relatively fixedrelatively fixed

rather than variable.rather than variable.

Knowledge workersKnowledge workerstend to be salaried,tend to be salaried,highly-trained, andhighly-trained, and

difficult to replace. Thedifficult to replace. Thecost to compensatecost to compensate

these valued employeesthese valued employeesis is relatively fixedrelatively fixed

rather than variable.rather than variable.

5-10

Is Labor a Variable or a Fixed Cost?

The behavior of wage and salary costs can differ across countries, depending on labor regulations, labor contracts, and custom.

In France, Germany, China, and Japan,management has little flexibility in adjusting

the size of the labor force.Labor costs are more fixed in nature.

In France, Germany, China, and Japan,management has little flexibility in adjusting

the size of the labor force.Labor costs are more fixed in nature.

Most companies in the United States continueto view direct labor as a variable cost.

Most companies in the United States continueto view direct labor as a variable cost.

5-11

Ren

t C

ost

in

T

ho

usa

nd

s o

f D

oll

ars

0 1,000 2,000 3,000 Rented Area (Square Feet)

0

30

60

Fixed Costs and Relevant Range

90

Relevant

Range

Total cost doesn’t change for a wide range of activity,

and then jumps to a new higher cost for

the next higher range of activity.

Total cost doesn’t change for a wide range of activity,

and then jumps to a new higher cost for

the next higher range of activity.

5-12

Mixed Costs

Fixed Monthly

Utility Charge

Variable

Cost per KW

Activity (Kilowatt Hours)

To

tal

Uti

lity

Co

st

X

Y

Total mixed cost

5-13

Analysis of Mixed Costs

Account analysisAccount analysisEach account is classified as eitherEach account is classified as either

variable or fixed based on the analyst’svariable or fixed based on the analyst’s knowledge of how the account behaves. knowledge of how the account behaves.

Account analysisAccount analysisEach account is classified as eitherEach account is classified as either

variable or fixed based on the analyst’svariable or fixed based on the analyst’s knowledge of how the account behaves. knowledge of how the account behaves.

Engineering ApproachEngineering ApproachCost estimates are based on an Cost estimates are based on an

evaluation of production methods,evaluation of production methods,and material, labor and overhead and material, labor and overhead

requirements.requirements.

Engineering ApproachEngineering ApproachCost estimates are based on an Cost estimates are based on an

evaluation of production methods,evaluation of production methods,and material, labor and overhead and material, labor and overhead

requirements.requirements.

5-14

The Scattergraph MethodUse one Use one

data point data point to estimate to estimate

the totalthe totallevel of level of activity activity and the and the

total cost. total cost.

Use one Use one data point data point to estimate to estimate

the totalthe totallevel of level of activity activity and the and the

total cost. total cost. Intercept = Fixed cost: $10,000

0 1 2 3 4

*

Mai

nte

nan

ce C

ost

1,00

0’s

of

Do

llars

10

20

0

***

**

**

*

*

Patient-days in 1,000’s

X

Y

Patient days = 800Patient days = 800

Total maintenance cost = $11,000Total maintenance cost = $11,000

5-15

The High-Low MethodThe The variable cost variable cost

per hourper hour of of maintenance is maintenance is

equal to the change equal to the change in cost divided by in cost divided by

the change in hours.the change in hours.

The The variable cost variable cost per hourper hour of of

maintenance is maintenance is equal to the change equal to the change

in cost divided by in cost divided by the change in hours.the change in hours.

= $8.00/hour$2,400

300 hours

Hours Total CostHigh 800 9,800$ Low 500 7,400 Change 300 2,400$

5-16

The High-Low Method

Total Fixed Cost = Total Cost – Total Variable CostTotal Fixed Cost = Total Cost – Total Variable Cost

Total Fixed Cost = $9,800 – ($8/hour Total Fixed Cost = $9,800 – ($8/hour × 800 hours)× 800 hours)

Total Fixed Cost = $9,800 – $6,400Total Fixed Cost = $9,800 – $6,400

Total Fixed Cost = Total Fixed Cost = $3,400$3,400

5-17

The High-Low Method

Y = $3,400 + $8.00Y = $3,400 + $8.00XXThe Cost Equation for Maintenance

5-18

Least-Squares Regression Method

A method used to analyze mixed costs if a scattergraph plot reveals an approximately linear

relationship between the X and Y variables.

A method used to analyze mixed costs if a scattergraph plot reveals an approximately linear

relationship between the X and Y variables.

This method uses This method uses allall of the of thedata points to estimatedata points to estimatethe fixed and variablethe fixed and variablecost components of acost components of a

mixed cost.mixed cost.

This method uses This method uses allall of the of thedata points to estimatedata points to estimatethe fixed and variablethe fixed and variablecost components of acost components of a

mixed cost.mixed cost.The goal of this method isThe goal of this method isto fit a straight line to theto fit a straight line to thedata that data that minimizes theminimizes the

sum of the squared errorssum of the squared errors..

The goal of this method isThe goal of this method isto fit a straight line to theto fit a straight line to thedata that data that minimizes theminimizes the

sum of the squared errorssum of the squared errors..

5-19

The Contribution FormatTotal Unit

Sales Revenue 100,000$ 50$

Less: Variable costs 60,000 30

Contribution margin 40,000$ 20$

Less: Fixed costs 30,000

Net operating income 10,000$

Total Unit

Sales Revenue 100,000$ 50$

Less: Variable costs 60,000 30

Contribution margin 40,000$ 20$

Less: Fixed costs 30,000

Net operating income 10,000$

The contribution margin format emphasizes cost behavior, by separating costs into fixed and variable categories. Contribution margin covers fixed costs and provides for income.

The contribution margin format emphasizes cost behavior, by separating costs into fixed and variable categories. Contribution margin covers fixed costs and provides for income.

5-20

The Contribution Format

Used primarily forUsed primarily forexternal reporting.external reporting.

Used primarily byUsed primarily bymanagement.management.

5-21

Overview of Absorption and Variable Costing

Direct Materials

Direct Labor

Variable Manufacturing Overhead

Fixed Manufacturing Overhead

Variable Selling and Administrative Expenses

Fixed Selling and Administrative Expenses

VariableCosting

AbsorptionCosting

ProductCosts

PeriodCosts

ProductCosts

PeriodCosts

5-22

Unit Cost Computations

Harvey Company produces a single product with the following information available:

5-23

Unit Cost ComputationsUnit product cost is determined as follows:

Selling and administrative expenses arealways treated as period expenses and

deducted from revenue as incurred.

5-24

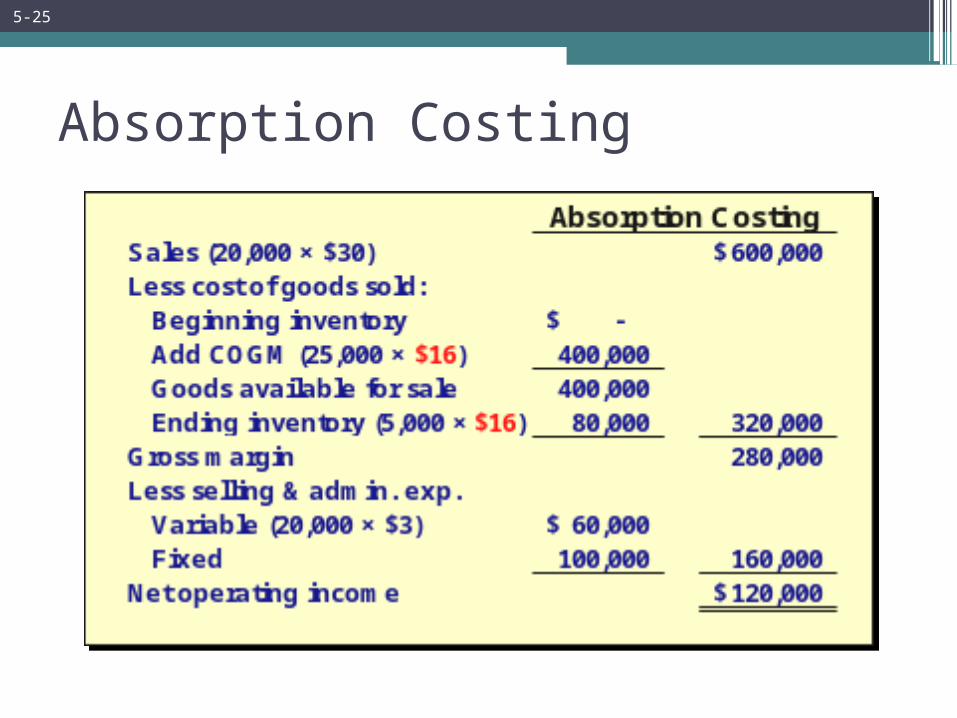

Absorption Costing

5-25

Variable CostingSales (20,000 × $30) 600,000$ Less variable expenses: Beginning inventory -$ Add COGM (25,000 × $10) 250,000 Goods available for sale 250,000 Less ending inventory (5,000 × $10) 50,000 Variable cost of goods sold 200,000 Variable selling & administrative expenses (20,000 × $3) 60,000 260,000 Contribution margin 340,000 Less fixed expenses: Manufacturing overhead 150,000$ Selling & administrative expenses 100,000 250,000 Net operating income 90,000$

Variable CostingSales (20,000 × $30) 600,000$ Less variable expenses: Beginning inventory -$ Add COGM (25,000 × $10) 250,000 Goods available for sale 250,000 Less ending inventory (5,000 × $10) 50,000 Variable cost of goods sold 200,000 Variable selling & administrative expenses (20,000 × $3) 60,000 260,000 Contribution margin 340,000 Less fixed expenses: Manufacturing overhead 150,000$ Selling & administrative expenses 100,000 250,000 Net operating income 90,000$

Variablemanufacturing

costs only.

All fixedmanufacturing

overhead isexpensed.

Variable Costing

5-26

Comparing Absorption and Variable Costing: Year 1

Let’s compare the methods.

5-27

Summary of Key Insights

NOI = net operating income

5-28