tgi & cálidda earnings call 1 q 2015

TRANSCRIPT

May 27th 2015

1Q 2015 TGI RESULTS AND KEY DEVELOPMENTS

DisclaimerThis presentation contains statements that are forward-looking within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements are only predictions and are not guarantees of future performance. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements include, among other things, statements concerning the potential exposure of TGI, its consolidated subsidiaries and related companies to market risks and statements expressing management’ expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as “anticipate”, “believe”, “could”, “estimate”, “expect”, “intend”, “may”, “plan”, “objectives”, ”outlook”, “probably”, “project”, “will”, “seek”, “target”, “risks”, “goals”, “should” and similar terms and phrases. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Although TGI believes that the expectations and assumptions reflected in such forward-looking statements are reasonable based on information currently available to TGI’s management, such expectations and assumptions are necessarily speculative and subject to substantial uncertainty, and as a result, TGI cannot guarantee future results or events. TGI does not undertake any obligation to update any forward-looking statement or other information to reflect events or circumstances occurring after the date of this presentation or to reflect the occurrence of unanticipated events.

Table of contents

1. Overview

2. Key updates

3. Operational and Financial performance

4. Expansion Projects

Appendix

1. EEB Overview

1. OVERVIEW

Overview

5

Stable and growing Colombian economy with sound investment environment

Constructive and stable regulatory framework

Largest natural gas pipeline system in Colombia

Stable and predictable cash flow generation, strongly indexed to the US Dollar

Strong and consistent financial performance

Experienced management team with solid track record in the sector

Expertise, financial strength and support of shareholders

Natural monopoly in a regulated environment

Strategically located pipeline network

Pipeline networkPipeline network

TGI history

6

Company historyCompany history

HighlightsHighlights

Owns ~60% of the national pipeline network (3,957 km) and transports 48% of the gas consumed in the country

−Serves ~70% of Colombia’s population, reaching the most populated areas (Bogota, Cali, Medellin, the coffee region and Piedemonte Llanero, among others)

−Has access to the two main production regions, La Guajira and Cusiana/Cupiagua

Cartagena Refinery

Barrancabermeja Refinery Bucaramanga

Bogota

NeivaCali

Medellin

3.15 tcf

1.97 tcf

EasternProducers:EcopetrolEquion

Upper Magdalena Valley

Lower and Middle Magdalena Valley

NorthernProducers:ChevronEcopetrol 1.89 tcf

Ballena

Cusiana

ReferencesTGI Pipelines

Natural Gas ReservesCityFieldRefinery

Third Party Pipelines

Source:Mining and Energy Planning Unit. National Hydrocarbons Agency.

1997 2005 2006 2007 2008 2009 2010 2011 2012 2013

Start of Ecogas Privatization Process

Creation of TGI Inaugural bond

issuance (Fitch Rating: BB)

Transfer of first BOMT pipeline (GBS)

Pipelines exchange with Promigas

CVCI capitalization for USD 400 Mn

Transfer of second BOMT pipeline (Centragas)

Cusiana expansion phase I: start of operations

Refinancing of subordinated debt with EEB

Awarded investment grade rating by S&P

Headquarters relocation from Bucaramanga to Bogota

Redesign of organizational structure

Creation of Ecogas Ecogas assets awarded to EEB

TGI takes over the O&M of owned pipelines

EEB acquired the remaining stakes in Transcogas

Ballena expansion: start of operations

Merger of TGI and Transcogas

Refinancing of bonds issued in 2007 (Fitch Rating: BB+)

Cusiana expansion phase II: start of operations

TGI takes over the O&M of compressor stations

Awarded investment grade by Moody’s and Fitch 2014

EEB acquired 31.92% stake

Sabana Compressor starts operations

Fitch upgrades rating from BBB- to BBB

First dividend distribution

Paci

fic

Oce

an

Caribbean Sea

VEN

EZU

ELA

2. KEY UPDATES

Key updates

8

Since 2H 2011 TGI has executed a strategy to improve its credit ratings in order to (i) reduce financial expenses, (ii) provide better access to debt capital markets and (iii) broaden its potential investor base

On August 2014, Standard & Poor’s affirmed the TGI corporate debt and issuer rating in ‘BBB-‘, perspective stable

On October 28th, Fitch Ratings upgraded TGI’s corporate debt and issuer rating from ‘BBB-’ to ‘BBB’, with stable perspective

Baa3 Stable OutlookBBB Stable Outlook BBB- Stable Outlook

TGI´s credit ratings

Final steps of TGI’s stake (31.92%) acquisition by parent company (EEB)

EEB closed TGI’s stake acquisition in 2H2014, through the acquisition of 100% of IELAH (SPV) domiciled in Spain.

As part of the transaction structured by EEB, IELAH should merge with TGI and the debt of that entity will be in TGI´s BS. Currently the company is working on that merger and it is expected to close it at the end of 2015.

Current outstanding debt of IELAH is USD 569 MM, after a partial repay (USD 76 MM) done in March 2015.

TGI started the convergence process from ColGAAP to IFRS Mandatory transition period began on January 1, 2014 and the issuance date of the first

comparative financial statements under IFRS will be December 31, 2015 Since 2013, TGI carried out activities regarding preparation and adjustment of the resources

needed to advance in the process of convergence to IFRS in accordance with legal requirements TGI with technical support from external advisors, determined the effects that such changes will

have on the financial statements Some specific impacts are still being analyzed by TGI

Transition to International Financial Reporting Standards - IFRS

Key updates

Regulation perspectives

■ The last tariff review was approved by the CREG Resolution No. 126 in August 2010 and became effective for TGI in December 2012 (CREG Resolution No. 121). The tariff methodology review process takes place every 5 years, but the actual tariff application is usually delayed (previous tariff period was effective from December 2003 to December 2012, a total of 9 years)

■ According to CREG, new regulation is expected to be approved between 2015 – 2016, with the updated tariffs coming into effect between 2017 – 2018 (the starting point for the 5 year-period is set by the CREG approval of the new tariff methodology)

■ Based on TGI’s analysis and taking into account the latest available data parameters for its calculations (1), the new regulatory WACC is estimated at 11,63% for capacity and 14,30% for volume. (12,30% weighted average)

Aug. 2010

New tariff methodology proposition for discussion

End of current tariff period

Final tariff methodology

Final regulatory WACC

Information request for charges

Charge approval by CREG

Request for reinstatement

Approval of final charges and implementation of new WACC

Approval of charges

Information reporting to CREG

Termination of public information audit stage – demands and expressions of interest from third parties

Dec. 2014

Aug. 2015

Sep. 2015

Jan. 2016

Jun. 2016

Jul. 2016Dec. 2016

Beginning of current tariff period

Tariff review process – Estimated CREG schedule

Tariffs become effective for TGI

Dec. 2012

5 year regulatory period

(1) As of march 2015

Key updates

3. OPERATIONAL AND FINANCIAL PERFORMANCE

Solid operational performance

(1)The trend line refers to the ratio: Firm contracted capacity/available capacity. The Available capacity differs from the Total Capacity as TGI requires a percentage of it for its own use. Source: Company information.

Network lengthNetwork length(km)

CapacityCapacity(MMscfd)

Firm Contracted Capacity(1)Firm Contracted Capacity(1)

(MMscfd)

Transported VolumeTransported Volume Load factorLoad factor(MMscfd) (%)

Pipeline & Compression Stations Reliability Pipeline & Compression Stations Reliability

20

3,529

3,7743,774

3,9573,9573,9573,957

396 422 420 422454

494.387470

2012 2013 2014 LTM 15 1Q

99.6% 99.7% 99.8% 100.0%

96.0% 96.5% 96.5%99.0%

Pipeline systemCompression system

2009 2010 2011 2012 2013 2014 LTM 15 1Q

69% 71%

58% 59%61% 64% 62%

2009 2010 2011 2012 2013 2014 2015 1Q

437485

560604 625

668 669

92% 90% 92%

85%88%

94% 94%

478548

618

730 730 734 734

Stable and predictable cash flow generation

TGI’s revenues are highly predictable, with approximately 99,6% coming from regulated tariffs that are reviewed al least every 5 years, ensuring cash flow stability and attractive rates of return

Main sectors served by the Company (79(1)% of revenues) present stable consumption patterns (no seasonality)

The Company enjoys excellent contract quality

− 100% of TGI’s contracts are firm contracts with an average life of 8,19 years

− 89% of regulated revenues are fixed tariffs, not dependent on transported volume

− Extremely low sensitivity of EBITDA to changes in exchange rate

13

Revenues breakdownRevenues breakdown(% of revenues)

(1) Includes Distributors, Ecopetrol´s refinery and Natural gas for Vehicles.

TGI’s revenues are highly predictable as a result of regulated tariffs and stable consumption

as of March 31- 2015

By Client

Distributors62%

Refinery13%

Thermal16%

Traders3%

Vehicle4%

Others2%

By Sector

Ecopetrol14%

Gas Natural 25%

Gases de Occidente

17%

EPM 11%

Isagen 8%

Others25%

2009 2010 2011 2012 2013 2014 LTM 15 1Q

172196

226250

323 332 328

68.1% 66.7% 66.8%64.1%

69.4% 70.8% 70.5%

Revenues (3) Gross profit and Gross margin (3)Revenues (3) Gross profit and Gross margin (3)

(US$ in millions – EOM exchange rate for each period)

(US$ in millions – EOM exchange rate for each period) (US$ in millions – average exchange rate for each period)

(1) FFO for the years 2009 - 2013 is presented under ColGaap standards as net income plus depreciation, amortization and provisions, adjusted for effect from exchange rate and hedges. 2014 and LTM 1Q 2015 is presented under IFRS as net income plus depreciation, amortization and provisions, adjusted for effect from exchange rate , hedges, and the impact of deferred taxes.

(2) On 2012 FFO includes the LM transaction premium~ USD 69 million (one time event)(3) Figures for the years 2009 - 2013 are presented under ColGaap standards. 2014 and 1Q 2015 are presented under IFRS. IFRS figures are preliminary subject to changes, independent auditor’s revision and Shareholders Assembly approval

TGI Financial performance

(US$ in millions – EOM exchange rate for each period)

2009 2010 2011 2012 2013 2014 LTM 15 1Q

252294

338

390

465 468 466

2009 2010 2011 2012 2013 2014 LTM 15 1Q

196222

257289

359 371 371

78% 75% 76% 74% 77% 79% 80%

2009 2010 2011 2012 2013 2014 LTM 15 1Q

96 108 117 133

268305 316

Funds from operations (1) (2) (3)Funds from operations (1) (2) (3)EBITDA and EBITDA Margin(3)EBITDA and EBITDA Margin(3)

CASH AND EQUIVALENTS (1) TOTAL ASSETS (1)CASH AND EQUIVALENTS (1) TOTAL ASSETS (1)

LIABILITIES (1)LIABILITIES (1)

(US$ in millions – end-of-year exchange rate for each period) (US$ in billions – end-of-year exchange rate for each period)

(US$ in billions – end-of-year exchange rate for each period)

TGI Financial performance

PPE (1)PPE (1)

(US$ in billions – end-of-year exchange rate for each period)

2009 2010 2011 2012 2013 2014 LTM 15 1Q

11071

182160

364

207

275

2009 2010 2011 2012 2013 2014 LTM 15 1Q

1.802.12

2.562.88 2.98 2.81 2.85

2009 2010 2011 2012 2013 2014 LTM 15 1Q

1.25 1.30 1.34 1.40 1.40 1.60 1.65

0.55 0.811.22 1.48 1.58 1.21 1.20

Liabilities Equity

2009 2010 2011 2012 2013 2014 LTM 15 1Q

0.620.77

1.401.67

1.49

2.28 2.27

(1) Figures for the years 2009 - 2013 are presented under ColGaap standards. For 2014 and 1Q 2015 are presented under IFRS. IFRS figures are preliminary subject to changes, independent auditor’s revision and Shareholders Assembly approval

(x)

Note: Total debt includes senior debt, subordinated debt and mark-to-market.

(1) Figures for the years 2009 - 2013 are presented under ColGaap standards. For 2014 and 1Q 2015 are presented under IFRS. IFRS figures are preliminary, subject to changes, independent auditor’s revision and Shareholders Assembly approval

(2) Interest coverage ratio calculated as EBITDA / net interest

Debt / EBITDA (1)Debt / EBITDA (1)

Interest coverage (1)(2)Interest coverage (1)(2)

(x)

Net debt / EBITDA (1)Net debt / EBITDA (1)

(x)

(x)

Financial performance

Senior Debt / EBITDA (1)Senior Debt / EBITDA (1)

(x)

2009 2010 2011 2012 2013 2014 LTM 15 1Q

5.6 5.44.9

4.23.5 3.3 3.3

2009 2010 2011 2012 2013 2014 LTM 15 1Q

5.1 5.1

4.23.7

2.5 2.7 2.6

2009 2010 2011 2012 2013 2014 LTM 15 1Q

3.8 3.73.4

3.0

2.5 2.3 2.3

2009 2010 2011 2012 2013 2014 LTM 15 1Q

2.0 2.02.5

4.0

5.96.3 6.6

4. EXPANSION PROJECTS

Description: TGI will increase existing capacity of Armenia and Chinchina branches with the construction of two new loops; Armenia Branch: 37.5 km 8” loop parallel to exiting 6” pipeline and Chinchina – Santa Rosa – Dosquebradas Branch: 7.5km 3” loop parallel to existing 3” pipeline

Cost: ~$ 28 mm

Status: — Engineering stage— Expected Completion: 2017

Expansion projects pipeline

Description: Adapt compression stations, delivery and receipt locations along the Ballena - Barrancabermeja pipeline so that it can transport natural gas in both directions, in order to allow natural gas to be transported from the central region to the north

Cost: ~$ 20 mm

Expected Completion:

2016

Ballena – Barrancabermeja Bidirectionality

Description: Increase capacity in 20 mmcf/d by adapting Vasconia, Miraflores, Puente Guiillermo compression stations

Cost: ~$ 31 mm

ExpectedCompletion: Dec. 2015

Cusiana Phase III

Cusiana - Apiay – Villavicencio - Ocoa

Description: BOMT ContractIncrease capacity in 32 mmscf/d. 2 New compression stationsCusiana – Apiay 32 mmcfdApiay – Ocoa 7 mmcfd

Cost: ~USD $ 48 mm

ExpectedCompletion: 1H 2017

Eje Cafetero Branches

Investor Relations

For more information about TGI please contact to:

Antonio José Angarita VegaCFO

+57 (1) 3138400 - ext [email protected]

Sergio Andrés Hernández AcostaFinance Manager

+57 (1) 3138400 - ext. [email protected]

Fabián Sánchez AldanaIR Advisor - EEB

+57 (1) 3268000 - ext. [email protected]

http://www.tgi.com.co

Appendix 1 – EEB Overview

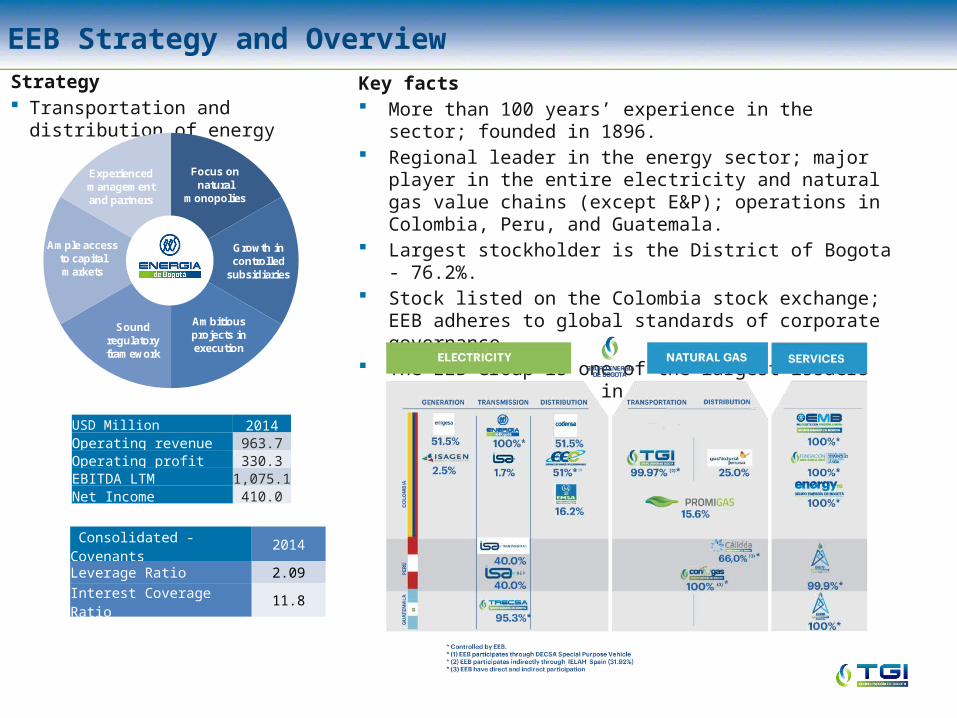

EEB Strategy and OverviewStrategy Transportation and distribution

of energy

Key facts More than 100 years’ experience in the sector; founded in

1896. Regional leader in the energy sector; major player in the

entire electricity and natural gas value chains (except E&P); operations in Colombia, Peru, and Guatemala.

Largest stockholder is the District of Bogota - 76.2%. Stock listed on the Colombia stock exchange; EEB adheres

to global standards of corporate governance. The EEB Group is one of the largest issuers of equity and

debt in Colombia

USD Million 2014Operating revenue 963.7Operating profit 330.3EBITDA LTM 1,075.1Net Income 410.0

Consolidated - Covenants 2014Leverage Ratio 2.09Interest Coverage Ratio 11.8

Focus on natural

monopolies

Ample access to capital markets

Ambitious projects in execution

Growth in controlled

subsidiaries

Sound regulatory framework

Experienced management and partners

Cálidda´s Q1 2015 Results

I. Introduction and Perspectives

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

23

Table of Contents

I. Introduction and Perspectives

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Table of Contents

24

Introduction and Perspectives

25

I. Introduction and Perspectives

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Table of Contents

26

Cálidda has a client base of 278,028 customers. In the first quarter, 23,023 new clients have been connected . Now in the residential segment, we have presence in 17 districts of our concession area.

During the first quarter, 279 km of network were built, being mostly polyethylene (270 km), whereby the distribution system reached a total of 4,957 km of underground pipelines.

Even though Total Revenues from the first quarter decreased 9% (because of less investments – IFRIC 12), the Total Adjusted Revenues increased 23%.

In this quarter the EBITDA and adjusted EBITDA margin grew, mostly driven by an increase in the distribution tariff.

Significant Developments

2) Total Adjusted Revenues exclude Pass- through and IFRIC 12 revenues.3) EBITDA Last twelve months.4) Adjusted EBITDA Margin excludes Pass-through and IFRIC 12 revenues.5) Interest Coverage: EBITDA / Financial cost.

27

Significant Developments

1) Clients who are in front of Cálidda's distribution network.

Operational Results ( YTD ) Q1 2015 Q1 2014 Var %

Accumulated Clients: 278,028 185,941 50%

Invoiced Volume (MMCFD): 695.2 663.4 5%

Network Lenght (km): 4,957 3,779 31%

Potencial Clients 1 497,111 369,629 34%

Financial Results ( YTD ) Q1 2015 Q1 2014 Var %

Total Revenues (USD MM): 129.3 142.3 -9%

Total Adj. Revenues (USD MM) 2 : 52.1 42.3 23%

EBITDA (USD MM) 3 : 96.8 72.1 34%

Adjusted EBITDA Margin 4 : 49.5% 48.8%

Interest Coverage (x) 5 6.6x 5.5x 21%

I. Introduction and Perspectives

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Table of Contents

28

Commercial Performance

29

Residential & Commercial Residential & Commercial

Cálidda has residential presence in 17 districts and industrial network in more than 34 districts within Lima & Callao (Metropolitan area).

Cálidda connected residential customers in the Province of Callao and in March began commercial activities in the district of Ate.

During Q1 2015, Cálidda added 22,706 clients in the Residential segment and 309 clients in the Commercial segment.

Residential

Industrial

Natural gas pipeline

Main grid expansion

Callao

2009 2010 2011 2012 2013 2014 Q1 20150

50,000

100,000

150,000

200,000

250,000

300,000

18,75634,619

63,602

103,090

163,129

254,280

277,295

Commercial Performance

30

Clients Segments Growth Highlights

No new power generators where connected in Q1 2015.

3 new industrial plants were connected during Q1 2015.

In January, independent customers like Alicorp, Refineria La Pampilla and Andina de Cementos Unión, increased their Firm Distribution service in 2.0 MMCFD.

5 new NGV stations joined Cálidda’s distribution system and almost 200,000 converted vehicles are attended in the City of Lima.

Power Generation

Industrial

GNV Stations

2009 2010 2011 2012 2013 2014 Q1 201502468

1012141618

8

1113 13

16 16 16

2009 2010 2011 2012 2013 2014 Q1 20150

150

300

450

600

321360

394429

466 489 492

2009 2010 2011 2012 2013 2014 Q1 20150

100

200

300

400

0

50,000

100,000

150,000

200,000

250,000

103143 172 192 206 220 225

81,029103,712

126,586151,781

171,541197,154

200,173

NGV Stations Converted Vehicles

Commercial PerformanceVolume Sold (Invoiced)MMCFD

As of March 2015, Take-or- Pay contracts amounted 541 MMCFD, 79% of total invoiced volume. In Q1 2015 the volume sold increased 5% compared to Q1 2014, due to an increase of volume mostly explained

by the Power Generation segment.

YoY: + 5%

31

2009 2010 2011 2012 2013 2014 Q1 2014 Q1 2015

52.2%

63.9%

71.6%71.6%

72.5%

74.2% 74.4%75.0%

34.0%

25.0%

19.2%

18.1%

17.2%

16.0% 15.9%15.1%

13.4%

10.6%

8.8%

9.7%

9.6%

9.0%9.0%

9.0%

182

303

457

508

577

679663

695

Total MMPCD

Residential & Commercial

NGV Stations

Industrial

C

AGR (09 -1

4)= + 30%

Commercial Performance Volume Sold by Client Segment (MMCFD)

NGV StationsNGV Stations Residential & CommercialResidential & Commercial

IndustrialIndustrialPower GenerationPower Generation

32

YoY: +6% YoY: -1%

YoY: +5%

YoY: +37%

2009 2010 2011 2012 2013 2014 Q1 2014 Q1 20150

100

200

300

400

500

600

95

193

327364

418

504 494521

CAGR('09-'14): 40%

2009 2010 2011 2012 2013 2014 Q1 2014 Q1 20150

20

40

60

80

100

120

62

7688 92

99109 106 105

CAGR('09-'14): 1

2%

2009 2010 2011 2012 2013 2014 Q1 2014 Q1 20150

10

20

30

40

50

60

70

24

32

40

4956

61 5963

CAGR('09-'14): 20%

2009 2010 2011 2012 2013 2014 Q1 2014 Q1 20150.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0.81.3

1.9

2.9

3.9

5.8

4.6

6.4

CAGR('0

9-'14):

47%

I. Introduction and Perspective

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Table of Contents

33

Operational Performance

Distribution System Infrastructure Distribution System Infrastructure

Network EfficiencyNetwork Efficiency

In Q1 2015, Cálidda’s has built 279 km, out of which 9 km were steel high pressure network while the remaining 270 km were polyethylene pipelines.

The total network now reaches 4,957 km of underground pipelines.

The network penetration rate has increased to 56% due to Cálidda’s commercial strategy to focus in low income districts where the savings produced by the use of natural gas against other alternative fuels are more appreciated.

34

Clie

nts

(‘000

)

2009 2010 2011 2012 2013 2014 Q1 20150

1,000

2,000

3,000

4,000

5,000

6,000

273 303 359 387 408 428 437701

1,0201,465

2,163

2,996

4,2494,520

9741,324

1,824

2,550

3,404

4,6784,957

Steel Network Polyethylene Network Total

km

2009 2010 2011 2012 2013 2014 Q1 20150

100

200

300

400

500

600

-10%

0%

10%

20%

30%

40%

50%

60%

19 35 64

104

164

255 278

94 126

174

244

331

466 497

20%

28%

37%42%

50%55%

56%

Total Clients Potential Clients*

(*) Clients who are in front of Cálidda's distribution network.

Operational Performance (Cont’d)

35

Calidda´s pipeline current capacity is 420MMCFD (from City Gate Lurín to Lima). Independent and regulated customers located down flow Lurín use nearly 295MMCFD, equivalent to 70% of our capacity.

Cálidda has enough Gas Supply (Pluspetrol) and Gas Transportation service (TGP) to attend its regulated customers.

Calidda Capacity 420 MMCFD

Gas178MMCFD

Transport204 MMCFD

Edegel Ventanilla

Enersur

Edegel Santa Rosa

Kallpa

Kallpa – Las Flores

Cálidda's City Gate

Thermal Plants (Clients)

Conventions

Cálidda Capacity = 420MMCFD

Regulated Clients + Independent Clients

(149MMCFD) (146MMCFD)

Termochilca

Fénix

Independent Clients

(Power Generators)

= 400MMCFD

Mar-15

* Based on 2014 Figures

Mar-15

Jan-14 Apr-14 Jul-14 Oct-14 Jan-150

150

300

450

Regulated Clients Independent Clients

Jan-14 Apr-14 Jul-14 Oct-14 Jan-1580

120

160

200

240

Regulated Clients

I. Introduction and Perspective

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Table of Contents

36

Financial PerformanceTotal Adjusted Revenues by Segment

2

1) Total Adjusted Revenues exclude Pass-through and IFRIC 12 revenues.2) Installation Services Revenues include revenues from connection fees and financing.3) Others: mainly derived from network relocation and other non recurrent services.

3

37

As of March 2015, 62% of Adjusted Revenues are volume related and 38% comes from installation services revenues and other revenues.

In this quarter, other revenues have increased substantially compared to previous periods because of extraordinary revenues that came from relocation services.

Residential & Commercial Industrial NGV Stations Power Generation Installation Services Others

Q1 2015 Total Adjusted Revenues1 Q1 2015 Total Volume (MMCFD)

1%

15%

9%

75%

Financial PerformanceMillion US$

Funds from Operations (FFO)1Funds from Operations (FFO)1

EBITDA & Adj. EBITDA Margin (%)EBITDA & Adj. EBITDA Margin (%)Total RevenuesTotal Revenues

38

Debt & Net Debt / EBITDADebt & Net Debt / EBITDA

2) Net Debt = Debt - Cash Balance. 1) FFO = Net Profit + Depreciation + Amortization

2

2009 2010 2011 2012 2013 2014 Q1 2014 Q1 2015

43 64 103 125 146 186

42 52

116125

201245

315326

100 77

160188

304

370

461512

142 129

Total Adjusted Revenues Pass-through & IFRIC 12 Series3

YoY: -9%

CAGR( 09 - 14): 2

6%

2009 2010 2011 2012 2013 2014 LTM Q1 2015

1929

5964

72

9197

44.5% 46.1%

57.6% 51.6% 49.3%

49.1% 49.5%

EBITDA Adjusted EBITDA Margin

2009 2010 2011 2012 2013 2014 LTM Q1 2015

12 18

40 43

36

57 57

2009 2010 2011 2012 2013 2014 LTM Q1 2015

3.9x 3.9x

2.8x 3.0x

4.4x

3.5x 3.3x

3.1x 3.1x

2.3x 2.3x

3.0x 2.6x 2.5x

Debt / EBITDA Net Debt / EBITDA

Financial MetricsMillion US$

Interest Coverage3Interest Coverage3 FFO / Net DebtFFO / Net Debt

Debt / Capitalization2 (%)Debt / Capitalization2 (%)Total Debt1Total Debt1

3) In 2013 ratio does not include 2013’s debt prepayment penalties (USD 7.8 MM)

1) Total Debt: net of debt associated costs.

39

2009 2010 2011 2012 2013 2014 LTM Q1 2015

2867

119 149

318 318 318

4747

4747

75 114

166 196

318 318 318

Senior Debt Shareholders' Subordinated Debt

2009 2010 2011 2012 2013 2014 LTM Q1 2015

41.4%

49.8%54.1%

49.2%

56.6%53.2% 52.6%

2009 2010 2011 2012 2013 2014 LTM Q1 2015

3.5x 3.8x

5.8x 5.5x 5.6x 6.3x

6.6x

2009 2010 2011 2012 2013 2014 LTM Q1 2015

20.9% 20.2%

28.9% 28.3%

16.8%

23.9% 23.7%

2) Capitalization: Equity + Debt

CapExCapExNet IncomeNet Income

EquityEquityTotal AssetsTotal Assets

Equity Injection:

$35MM

Equity Injection:

$25MM

40

Financial Metrics (Cont’d)Million US$

2009 2010 2011 2012 2013 2014 LTM Q1 2015

$106 $115 $141

$202

$244

$280 $287

2009 2010 2011 2012 2013 2014 LTM Q1 2015

$7 $10

$26 $27

$17

$35 $34

2009 2010 2011 2012 2013 2014 Q1 2015

48 5032

63

92 83

16

353

33

5

51 50

8596 98

83

Secondary Network Main Network

2009 2010 2011 2012 2013 2014 LTM Q1 2015

$218 $289

$383

$492

$648 $696 $704

I. Introduction and Perspective

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Table of Contents

41

Conclusions

42

I. Introduction and Perspective

II. Significant Developments

III. Commercial Performance

IV. Operational Performance

V. Financial Performance and Key Metrics

VI. Conclusions

Annexes:

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Table of Contents

43

For more information about Cálidda, please contact our Investor Relations team:

http://calidda.com.pe/inversionistas/

http://www.grupoenergiadebogota.com.co

Adolfo HeerenCEO

Rafael Andrés Salamanca RodriguezInvestor Relations Advisor GEB

+57 1 326 8000 – ext. [email protected]

Isaac FingerCFO

+51 1 625 7310 [email protected]

Investor Relations

44

Gabriela Vasquez - MejíaFinance Management

+51 1 625 7390 [email protected]

Strong Sponsorship withOptimal Experience

Leading energy holding company with interests across the electricity and natural gas sectors in Colombia, Peru and Guatemala.

Founded in 1896, controlled by the Distrito de Bogotá since 1956 with a 76.2% ownership stake.

Leader in the Energy Sector: major player in the transmission and distribution of electricity and natural gas.

– Only vertically-integrated and one of the largest natural gas distribution and transportation companies in Colombia.

– Founded in 1974 by the government of Colombia. Currently controlled by Grupo Aval.

– Major player in the gas distribution sector in Colombia through Gases de Occidente, Surtigas and Gases del Caribe.

– Participation in the power distribution in Colombia and telecommunications sector in Panama and Costa Rica.

– EEB has 15.6% stake in Promigas.

Controlling Investments

Non Controlling Investments

Non Controlling Investments

Controlling Shareholder – 60% Ownership in CáliddaControlling Shareholder – 60% Ownership in Cálidda

Shareholder – 40% Ownership in CáliddaShareholder – 40% Ownership in Cálidda

Controlling Investments

45

Experienced and ProvenManagement Team & Board

Board of Directors

Management Team

46

Chief Operating

Officer

JorgeMonterroza

Years in industry:18 years

Years at Cálidda:4 years

Chief Executive OfficerAdolfo Heeren

Years in Industry: 17 yearsYears at Cálidda: 3 years

Chief Commercial

Officer

CarlosCerón

Years in industry:17 years

Years at Cálidda:3 years

ChiefProcurement

Officer

PatriciaPazos

Years in industry:18 years

Years at Cálidda:10 years

Chief FinancialOfficer

IsaacFinger

Months in industry:8 months

Months at Cálidda:8 months

Chief Human Resources

Officer

RosarioJiménez

Years in industry:6 years

Years at Cálidda:6 years

Chief External Affairs Officer

TaniaSilva

Years in industry:3 years

Years at Cálidda:2 years

Chief Legal and

Regulatory Officer

AmadeoArrarte

Years in industry:13 years

Years at Cálidda:11 years

Chief Strategy Officer

TatianaRivas

Years in industry:7 years

Years at Cálidda:7 years

Chief Internal Auditor

CarolinaHernández

Years in industry:9 years

Years at Cálidda:7 years

PresidentRicardo Roa

Barragán

Participation in the Boards of Codensa,

Emgesa, Gas Natural, REP Perú, Cálidda,

Contugas, Trecsa and President of

Transportadora de Gas Internacional TGI.

Luis BetancurEscobar

Served as Director of Fondo Financiero

Desarrollo Urbano.

President of Colombia's

restructuring of the Energy and Gas

Regulatory Commission

Jose Elias Melo Acosta

President of Corporación Financiera

Colombiana S.A

Minister of Colombia's Treasury and Public Credit and Labor and

Social Security

departments.

Antonio CeliaMartínez-Aparicio

President ofPromigas

Served on the board of directors of various companies in the

natural gas sector.

Mauricio MontoyaBozzi

Over thirteen years of professional

experience in Project Management, New

Business Structuring and Strategic

Planning.

David Alfredo Riaño Alarcón

President of Transportadora de Gas Internacional

TGI.

19 years of experience in the energy sector

and utilities.

Luis ErnestoMejía Castro

Director ofPromigas.

Minister of Mines and Energy and

Vice Minister of Hydrocarbons

and Mines.

Disclaimer

The information provided here is for informational and illustrative purposes only and is not, and does not seek to be, a source of legal or financial advice on any subject. This information does not constitute an offer of any sort and is subject to change without notice.

Cálidda and its Shareholders expressly disclaim any responsibility for actions taken or not taken based on this information. Neither Cálidda nor its Shareholders accept any responsibility for losses that might result from the execution of the proposals or recommendations herein presented. Neither Cálidda nor its Shareholders are responsible for any content that may originate with third parties. Cálidda or its Shareholders may have provided, or might provide in the future, information that is inconsistent with the information herein presented.

47