test6

DESCRIPTION

articol marketingTRANSCRIPT

Accountants’ attitudes toward advertising:a longitudinal study

Kenneth E. Clow

College of Business Administration, University of Louisiana Monroe, Monroe, Louisiana, USA

Robert E. StevensSchool of Business, Southeastern Oklahoma State University, Durant, Oklahoma, USA

C. William McConkeyCollege of Business Administration, University of Louisiana Monroe, Monroe, Louisiana, USA, and

David L. LoudonSchool of Business, Samford University, Birmingham, Alabama, USA

AbstractPurpose – The purpose of this study is to examine the attitude of accountants towards advertising and to investigate changes in attitude that mayhave occurred between 1993 and 2004.Design/methodology/approach – Data were collected from accountants using a mail survey approach in 1993 and using an e-mail survey approachin 2004. Questions on the two surveys were identical and a random sample of accountants was selected for each study. Statistical tests were used tocompare responses from 1993 with responses in 2004.Findings – Analysis of the results revealed significant positive shifts in the attitudes accountants have toward advertising of accounting services.Negative attitudes toward various aspects of advertising shifted to either a neutral or a positive position. This dramatic, positive shift in advertisingattitudes by accountants occurred while skepticism towards advertising remained relatively high, overall, among the general public. Between the twotime periods, changes in the use of various marketing tools (such as web sites to attract new clients) were also found to have occurred. In addition, theuse of marketing professionals by accounting service providers increased substantially over the 11-year time period of the longitudinal study.Research limitations/implications – Sample selection and size create some concern about generalizability of the study. With any random sampleselection process, the view of the non-respondents is not known nor whether those who responded tended to have a higher level of acceptance ofadvertising.Originality/value – For marketing professionals, this shift to a more positive attitude by accountants provides opportunities to offer greater marketingand advertising services. This shift also signals an increasing awareness on the part of accountants to market their services.

Keywords Accountants, Advertising, Professional services, Accounting

Paper type Research paper

An executive summary for managers and executive

readers can be found at the end of this article.

Literature review

In 1977, the Supreme Court ruled in the Bates v. State Bar ofArizona (1977, 97 S. Ct. 2691, 34 U.S., L.W. 4895) case that

professional codes of ethics that specifically banned

advertising had to be rewritten to reflect changes in the law.Professional organizations could no longer prohibit their

members from advertising. Prior to 1977, the practice of

advertising by accountants, although not illegal, was regarded

as unethical and a violation of the accountant’s professional

code of ethics. That sentiment was held by most accounting

professionals. A study by Dyer and Shimp (1978)

approximately one year prior to the Supreme Court ruling

found that a large majority of respondents was strongly

opposed to accountant advertising. Opposition was

particularly strong among older accountants and those

practicing in larger, corporate-oriented firms. In addition,

most accountants were also strongly opposed to an “anything

goes” advertising approach where all forms of information

content (including price) and all available media (including

television) are acceptable.A study in 1978, immediately following the Supreme Court

decision, found only 7 percent of accountants surveyed

planned to advertise (Markham et al., 2005). Thirteen years

later in 1991, another study found that accounting firms that

had been in business for more than ten years never planned to

advertise, in keeping with the concept of advertising being

unethical. But for firms that had been in business for less than

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0887-6045.htm

Journal of Services Marketing

23/2 (2009) 125–132

q Emerald Group Publishing Limited [ISSN 0887-6045]

[DOI 10.1108/08876040910946387]

Received: June 2006Revised: January 2007Accepted: March 2007

125

five years, 65 percent were currently advertising or planning

to advertise in the future (Markham et al., 2005).The reluctance to advertise was partially due to local, state,

and national accounting professional societies not following

the Bates ruling by the Supreme Court. An investigation by

the Federal Trade Commission (FTC) found the prohibition

against accounting association members advertising was often

not removed. After the FTC investigation, a consent decree

was signed by the American Institute of Certified Public

Accountants (AICPA) on August 9, 1990. The AICPA agreed

in the decree not to punish its members for using solicitation,

pricing, advertising, and other marketing practices (Bose and

Law, 2003).Research conducted after the Bates Supreme court ruling,

but prior to the FTC consent decree with the AICPA tended

to find negative perceptions toward advertising among

professionals generally, not just accountants (Traynor,

1984). For example, Darling (1977) researched attitudes

toward professional advertising held by accountants,

attorneys, dentists, and physicians toward advertising and

found significant differences between these four groups’

attitudes. Although all of the groups had a negative perception

of advertising, accountants and attorneys were more positive

about the potential role of advertising in their professions.

Hite and Fraser (1988) conducted a meta-analysis of attitudes

toward advertising by professionals and found that

professionals continued to be reluctant to use advertising.

They feared that negative impacts on image, credibility, and

dignity were likely, with little benefit forthcoming to

consumers.These findings are not surprising considering the general

widespread skepticism of advertising by consumers. Calfee

and Ringold (1994) presented empirical evidence that the

majority of consumers believed that advertising is often

untruthful; that it attempts to persuade people to buy things

they do not need; and that it should be more strictly

regulated. Based on public opinion polls, they concluded that

approximately 70 percent of consumers had this skeptical

view of advertising and that this view had been held for over

60 years that the data were available.This skepticism was corroborated in a study by Ford et al.

(1990) that examined skepticism of claims made by search,

experience, or credence goods. Skepticism was greater for

experience and credence type of goods than for search goods.

Accounting services would fall into the former group, and

thus, face a higher level of skepticism.After the FTC consent decree, attitudes of accountants

toward professional advertising continued its dichotomous

structure. Older accountants and larger CPA firms remained

opposed to advertising and were reluctant to engage in any

form of marketing, while younger accountants and smaller

firms were more open to advertising. In fact, younger partners

felt that if their firms were to grow, they must advertise and

follow brand-building strategies (Gamble et al., 2000).Based on this history of accountants and their attitude

toward professional advertising, it is time to explore whether

current practitioners’ attitudes toward advertising have

become more favorable as older accountants have retired

and younger individuals have filled those vacancies. Other

issues that need to be addressed are:1 How has the use of various marketing services and tools

changed over the last ten years?

2 How has the ranking of various marketing tools used

changed during this time period?

This study was designed to answer these types of questions.

Methodology

Data were collected in 1993 via survey questionnaires mailed

to a randomly selected sample of accountants located

throughout the contiguous 48 United States. The mailing

list was obtained from a mailing list broker who prepared the

sample. One thousand questionnaires were mailed and 243

were returned yielding a 24.3 percent response rate.

Questionnaire topics included practice characteristics,

personal characteristics, attitudes toward advertising, and

their own use of advertising, advertising agencies, other

marketing tactics, and marketing expenditures. In terms of

the firm’s practice, data collected included years of practice,

whether solo or group, area of specialty (if any), geographic

market area, and annual revenues of the firm.Data were collected in the 2004 study through an Internet

survey. Bulk email addresses from a commercial database

were used to contact a random sample of accountants. An

email was sent to potential respondents asking them to

cooperate in the study by clicking on a link that took them

directly to the survey. The survey questionnaire was the same

one used in the mail survey 11 years earlier. A total of 4,000

e-mails were sent, 3,121 of these were delivered and 106

responded yielding a 3.39 percent response rate based on

delivered e-mails.The two samples were comparable in terms of firm and

individual demographic characteristics. The average number

of years the accounting firm had been in practice was 16 to 20

years in 1993, compared to 21 to 25 years in 2004. In both

samples, the highest percentage of respondents was for those

firms with less than $500,000 in annual income. For both

studies, the majority of respondents were in a group practice.

In terms of individual characteristics, approximately 70

percent of both studies’ respondents were males. The 2004

respondent group was slightly older, with the highest

percentage being 50 to 59 years of age, compared to 40 to

49 for the 1993 study.Although the two studies used different methods of

distributing questionnaires, the responses are comparable.

Research has shown that the two methods used – mail and e-

mail – do not produce significant differences in responses

and, therefore, are appropriate for a comparative study

(McConkey et al., 2003).Attitudinal measures on 19 statements were obtained by

using a seven-point Likert scale ranging from strongly

disagree (1) to strongly agree (7). The statements were

patterned after those used by Dyer and Shimp (1978) and

were used in both the 1993 and 2004 studies. These

statements covered four investigative areas:1 Philosophical reasons for and against advertising.2 Economic issues related to advertising.3 Issues related to the potential impact of accounting

services advertising.4 Issues concerning the implementation of accounting

services advertising.

Additional questions probed respondents’ use of various

marketing tools, external service providers, and possible

Accountants’ attitudes toward advertising: a longitudinal study

Kenneth E. Clow et al.

Journal of Services Marketing

Volume 23 · Number 2 · 2009 · 125–132

126

reasons why more marketing is not being done by the

accounting firms.Several analytical approaches were used in the study. First,

the percentage and mean responses to each of the attitudinalstatements were computed for the purpose of determining the

direction of response patterns. Second, t-tests were used totest for significant differences in attitudinal responses betweenthe two studies. Third, a chi-square test was used to analyze

the differences in the two data sets for the percent usingvarious marketing services and tools. The null hypothesisunder the test was that the attitudinal scores in the 1993 study

and the scores in the 2004 study do not differ.

Results of attitudinal questions

Not only were significant differences in attitude foundbetween the 1993 study and the 2004 study, but there were

also shifts in the use of various marketing tools. Thesechanges are discussed below.Tables I-IV show the findings of the 19 attitudinal

statements. Although a seven-point Likert scale was used

for these questions, the tables report only the percentages ofindividuals who indicated some level of agreement ordisagreement with each statement. Respondents who

indicated no opinion (4 on the seven-point scale) are not

included in the percentage totals, but are included in

calculating the mean for each question. The percentage whoagreed with the statement would include everyone whoindicated “strongly agree,” “moderately agree,” and “slightlyagree.” The reverse would be true for the percentage ofrespondents disagreeing with the statement. Means werecalculated for each question and t-tests were used todetermine significant differences in responses between the

1993 and 2004 studies.

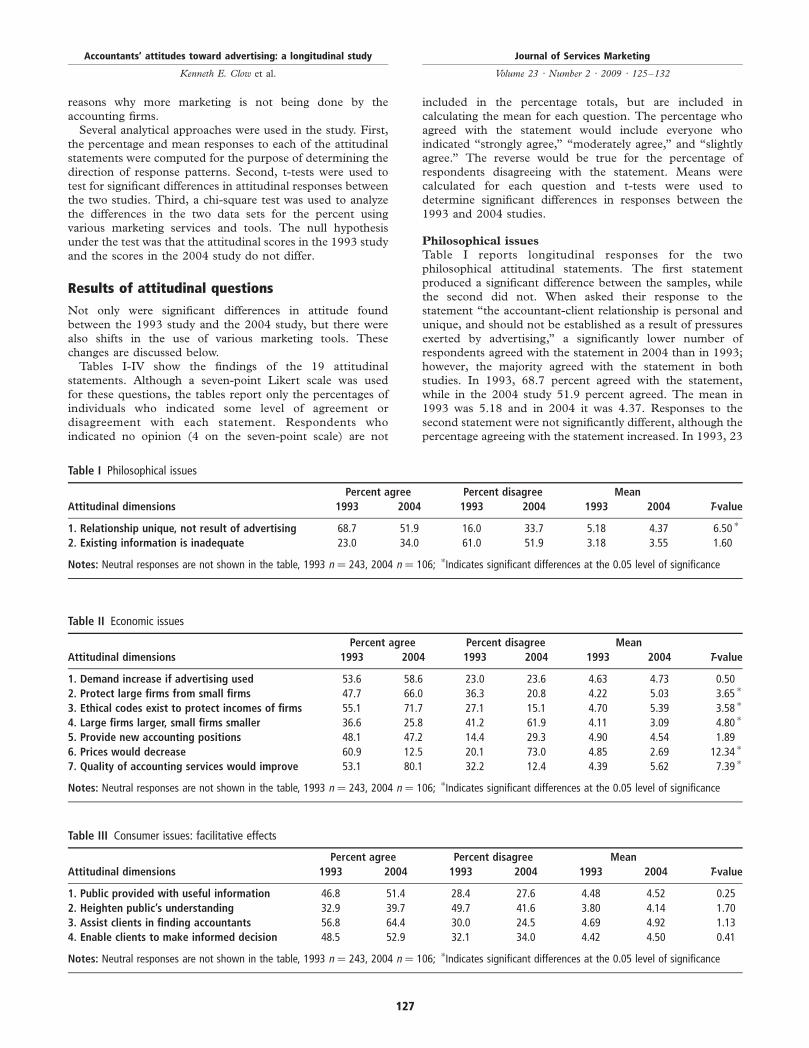

Philosophical issues

Table I reports longitudinal responses for the twophilosophical attitudinal statements. The first statementproduced a significant difference between the samples, whilethe second did not. When asked their response to thestatement “the accountant-client relationship is personal andunique, and should not be established as a result of pressures

exerted by advertising,” a significantly lower number ofrespondents agreed with the statement in 2004 than in 1993;however, the majority agreed with the statement in bothstudies. In 1993, 68.7 percent agreed with the statement,while in the 2004 study 51.9 percent agreed. The mean in1993 was 5.18 and in 2004 it was 4.37. Responses to the

second statement were not significantly different, although thepercentage agreeing with the statement increased. In 1993, 23

Table I Philosophical issues

Percent agree Percent disagree Mean

Attitudinal dimensions 1993 2004 1993 2004 1993 2004 T-value

1. Relationship unique, not result of advertising 68.7 51.9 16.0 33.7 5.18 4.37 6.50 *

2. Existing information is inadequate 23.0 34.0 61.0 51.9 3.18 3.55 1.60

Notes: Neutral responses are not shown in the table, 1993 n ¼ 243, 2004 n ¼ 106; *Indicates significant differences at the 0.05 level of significance

Table II Economic issues

Percent agree Percent disagree Mean

Attitudinal dimensions 1993 2004 1993 2004 1993 2004 T-value

1. Demand increase if advertising used 53.6 58.6 23.0 23.6 4.63 4.73 0.50

2. Protect large firms from small firms 47.7 66.0 36.3 20.8 4.22 5.03 3.65 *

3. Ethical codes exist to protect incomes of firms 55.1 71.7 27.1 15.1 4.70 5.39 3.58 *

4. Large firms larger, small firms smaller 36.6 25.8 41.2 61.9 4.11 3.09 4.80 *

5. Provide new accounting positions 48.1 47.2 14.4 29.3 4.90 4.54 1.89

6. Prices would decrease 60.9 12.5 20.1 73.0 4.85 2.69 12.34 *

7. Quality of accounting services would improve 53.1 80.1 32.2 12.4 4.39 5.62 7.39 *

Notes: Neutral responses are not shown in the table, 1993 n ¼ 243, 2004 n ¼ 106; *Indicates significant differences at the 0.05 level of significance

Table III Consumer issues: facilitative effects

Percent agree Percent disagree Mean

Attitudinal dimensions 1993 2004 1993 2004 1993 2004 T-value

1. Public provided with useful information 46.8 51.4 28.4 27.6 4.48 4.52 0.25

2. Heighten public’s understanding 32.9 39.7 49.7 41.6 3.80 4.14 1.70

3. Assist clients in finding accountants 56.8 64.4 30.0 24.5 4.69 4.92 1.13

4. Enable clients to make informed decision 48.5 52.9 32.1 34.0 4.42 4.50 0.41

Notes: Neutral responses are not shown in the table, 1993 n ¼ 243, 2004 n ¼ 106; *Indicates significant differences at the 0.05 level of significance

Accountants’ attitudes toward advertising: a longitudinal study

Kenneth E. Clow et al.

Journal of Services Marketing

Volume 23 · Number 2 · 2009 · 125–132

127

percent of the respondents indicated that “existinginformation sources (i.e. Yellow pages, association referral

services, lists, etc.) provide inadequate information to guidepotential client’s accountant selection.” The percentageincreased to 34 percent in the 2004 study.

Economic issues

Table II reports the findings from the seven attitudinaldimensions that address the economic issues related toadvertising by accountants. Statement 1 did not have a

significant difference in the responses, although a majority ineach study agreed with the statement that “the demand foraccountants’ services would increase if accountant service

advertising was widely used.” In 1993, 53.6 percent of therespondents agreed with the statement, while 58.6 percentagreed with it in 2004.Responses to the second statement were significantly

different, with the percentage in agreement increasing from

47.7 percent in 1993 to 66.0 percent in 2004. Thus, in the2004 study, almost two-thirds of accountants believe that“one principal effect of the accounting profession’s past

ethical canon against advertising is to protect establishedaccountants and large firms from competition from young

accountants and small firms.” An even larger percentage (71.7percent in 2004), agreed with the statement that “ethicalcodes against advertising exist to maintain and increase the

incomes of practicing accountants.” This was a significantincrease over the 55.1 percent who agreed with the statementin 1993. In 2004, 61.9 percent of respondents indicated

disagreement with the statement “if accountant serviceadvertising was widely used, the large, established firmswould get bigger, while the smaller firms would become even

less competitive than they are at present.” In the 1993 study,41.2 percent of the respondents disagreed with the statement.

Respondents do not see advertising of accounting serviceshelping large, established firms become even larger. In fact,the results appear to indicate that respondents believe

advertising of accounting services will allow smaller firms tobe more competitive.No significant difference in responses was found between

the two studies for the statement that “accountant serviceadvertising would help provide positions for thousands of new

accountants entering the profession.” In fact, the percentageagreeing was almost identical, 48.1 percent in 1993 versus47.2 percent in 2004.A significant difference was found between the two samples

for the statement that the “prices of accounting services

would decrease if accounting service advertising were widelyused.” The t-value was 12.34 with a mean of 4.85 in 1993 and

2.69 in 2004. In 1993, 60.9 percent of the accounting

respondents believed that advertising of accounting services

would drive down the prices they could charge for their

services, thus increasing the belief that advertising would

adversely affect the accounting profession. In 2004, only 12.5

percent believed advertising would drive down prices while 73

percent believed this would not occur.The last economic dimension dealt with service quality. A

significant difference was found between the samples

regarding responses to the statement that “the quality of

accounting services would improve if advertising were widely

used.” In 1993, 53.1 percent indicated agreement while 80.1

percent indicated agreement in 2004. Interestingly, although

accountants appeared to be heavily opposed to advertising in

1993, yet 53.1 percent believed that advertising would

improve the quality of accounting services being offered to

clients, perhaps because of an increased level of

competitiveness.

Consumer issues

Table III reports the findings of the four dimensions that

address the facilitative effects of consumer issues. None of the

dimensions were significantly different indicating no change

in attitudes of accountants over the 11-year period. It is worth

noting, however, that the percentage of respondents who

agree with the statements did increase. The facilitative effects

statements include the following:. The public would be provided with useful information

through the advertising of accountants’ services.. Accounting service advertising would heighten the

public’s understanding of situations where accounting

assistance is needed.. Accounting service advertising would assist potential

clients in knowing which accountants are competent to

handle particular accounting problems.. The information provided the public through accounting

service advertising would enable potential clients to make

a more informed selection of accountants.

A cursory review of the means indicates that approximately

half of accountants believe that advertising of accounting

services provides consumers with useful information, assists

clients in finding the right accountants, and enables clients to

make a more informed decision. Not quite as many

accountants (approximately 40 percent), believe that

advertising would heighten the public’s understanding of

situations when accounting services would be needed.The last six statements deal with the negative effects of

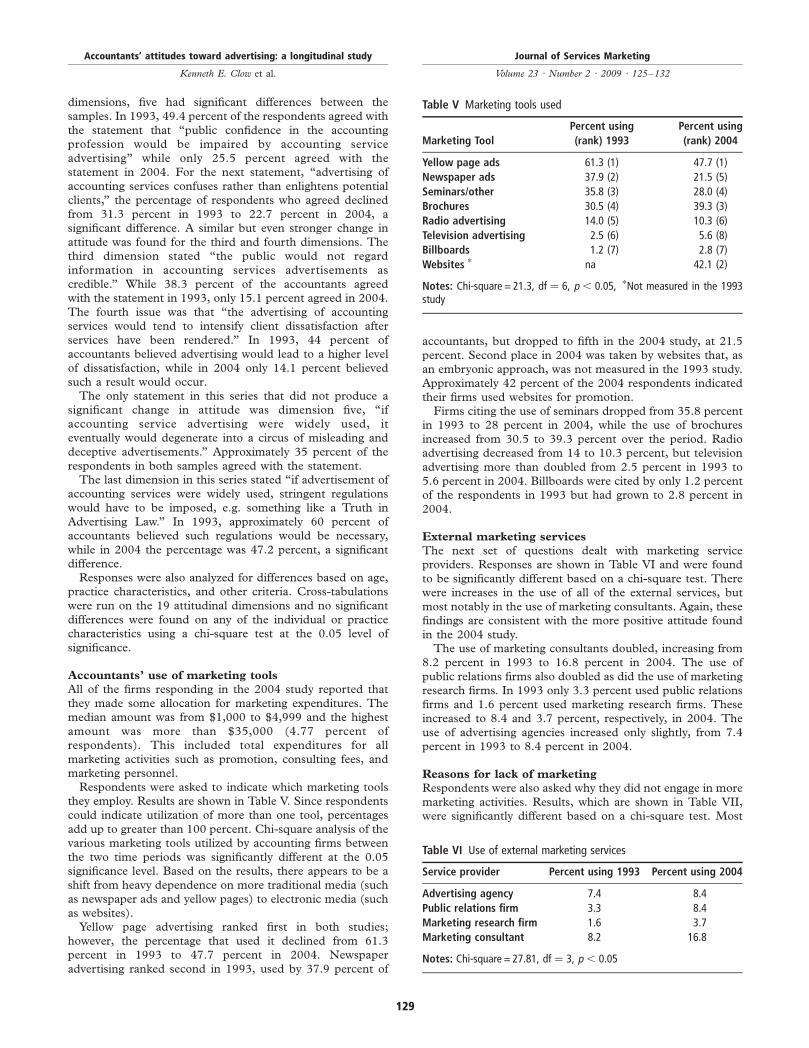

consumer issues. Results are presented in Table IV. Of the six

Table IV Consumer issues: negative effects

Percent agree Percent disagree Mean

Attitudinal dimensions 1993 2004 1993 2004 1993 2004 T-value

1. Public confidence impaired 49.4 25.5 28.8 59.5 4.41 3.33 5.18 *

2. Confuses potential clients 31.3 22.7 38.2 52.8 3.38 3.90 2.68 *

3. Advertising not viewed as credible 38.3 15.1 21.8 58.5 4.23 3.13 6.39 *

4. Intensify client dissatisfaction 44.0 14.1 19.4 59.4 4.45 3.15 7.84 *

5. Degenerate into misleading ads 34.2 35.0 46.4 49.1 3.76 3.75 0.71

6. If ads permitted, regulations needed 60.5 47.2 25.1 39.6 4.75 4.11 4.01 *

Notes: Neutral responses are not shown in the table, 1993 n ¼ 243, 2004 n ¼ 106; *Indicates significant differences at the 0.05 level of significance

Accountants’ attitudes toward advertising: a longitudinal study

Kenneth E. Clow et al.

Journal of Services Marketing

Volume 23 · Number 2 · 2009 · 125–132

128

dimensions, five had significant differences between the

samples. In 1993, 49.4 percent of the respondents agreed with

the statement that “public confidence in the accountingprofession would be impaired by accounting service

advertising” while only 25.5 percent agreed with thestatement in 2004. For the next statement, “advertising of

accounting services confuses rather than enlightens potentialclients,” the percentage of respondents who agreed declined

from 31.3 percent in 1993 to 22.7 percent in 2004, asignificant difference. A similar but even stronger change in

attitude was found for the third and fourth dimensions. Thethird dimension stated “the public would not regard

information in accounting services advertisements as

credible.” While 38.3 percent of the accountants agreedwith the statement in 1993, only 15.1 percent agreed in 2004.

The fourth issue was that “the advertising of accountingservices would tend to intensify client dissatisfaction after

services have been rendered.” In 1993, 44 percent ofaccountants believed advertising would lead to a higher level

of dissatisfaction, while in 2004 only 14.1 percent believedsuch a result would occur.The only statement in this series that did not produce a

significant change in attitude was dimension five, “if

accounting service advertising were widely used, iteventually would degenerate into a circus of misleading and

deceptive advertisements.” Approximately 35 percent of the

respondents in both samples agreed with the statement.The last dimension in this series stated “if advertisement of

accounting services were widely used, stringent regulationswould have to be imposed, e.g. something like a Truth in

Advertising Law.” In 1993, approximately 60 percent ofaccountants believed such regulations would be necessary,

while in 2004 the percentage was 47.2 percent, a significantdifference.Responses were also analyzed for differences based on age,

practice characteristics, and other criteria. Cross-tabulations

were run on the 19 attitudinal dimensions and no significant

differences were found on any of the individual or practicecharacteristics using a chi-square test at the 0.05 level of

significance.

Accountants’ use of marketing tools

All of the firms responding in the 2004 study reported that

they made some allocation for marketing expenditures. Themedian amount was from $1,000 to $4,999 and the highest

amount was more than $35,000 (4.77 percent ofrespondents). This included total expenditures for all

marketing activities such as promotion, consulting fees, andmarketing personnel.Respondents were asked to indicate which marketing tools

they employ. Results are shown in Table V. Since respondents

could indicate utilization of more than one tool, percentages

add up to greater than 100 percent. Chi-square analysis of thevarious marketing tools utilized by accounting firms between

the two time periods was significantly different at the 0.05significance level. Based on the results, there appears to be a

shift from heavy dependence on more traditional media (suchas newspaper ads and yellow pages) to electronic media (such

as websites).Yellow page advertising ranked first in both studies;

however, the percentage that used it declined from 61.3percent in 1993 to 47.7 percent in 2004. Newspaper

advertising ranked second in 1993, used by 37.9 percent of

accountants, but dropped to fifth in the 2004 study, at 21.5

percent. Second place in 2004 was taken by websites that, asan embryonic approach, was not measured in the 1993 study.

Approximately 42 percent of the 2004 respondents indicatedtheir firms used websites for promotion.Firms citing the use of seminars dropped from 35.8 percent

in 1993 to 28 percent in 2004, while the use of brochures

increased from 30.5 to 39.3 percent over the period. Radioadvertising decreased from 14 to 10.3 percent, but television

advertising more than doubled from 2.5 percent in 1993 to

5.6 percent in 2004. Billboards were cited by only 1.2 percentof the respondents in 1993 but had grown to 2.8 percent in

2004.

External marketing services

The next set of questions dealt with marketing serviceproviders. Responses are shown in Table VI and were found

to be significantly different based on a chi-square test. Therewere increases in the use of all of the external services, but

most notably in the use of marketing consultants. Again, thesefindings are consistent with the more positive attitude found

in the 2004 study.The use of marketing consultants doubled, increasing from

8.2 percent in 1993 to 16.8 percent in 2004. The use of

public relations firms also doubled as did the use of marketingresearch firms. In 1993 only 3.3 percent used public relations

firms and 1.6 percent used marketing research firms. Theseincreased to 8.4 and 3.7 percent, respectively, in 2004. The

use of advertising agencies increased only slightly, from 7.4percent in 1993 to 8.4 percent in 2004.

Reasons for lack of marketing

Respondents were also asked why they did not engage in more

marketing activities. Results, which are shown in Table VII,were significantly different based on a chi-square test. Most

Table V Marketing tools used

Marketing Tool

Percent using

(rank) 1993

Percent using

(rank) 2004

Yellow page ads 61.3 (1) 47.7 (1)

Newspaper ads 37.9 (2) 21.5 (5)

Seminars/other 35.8 (3) 28.0 (4)

Brochures 30.5 (4) 39.3 (3)

Radio advertising 14.0 (5) 10.3 (6)

Television advertising 2.5 (6) 5.6 (8)

Billboards 1.2 (7) 2.8 (7)

Websites * na 42.1 (2)

Notes: Chi-square = 21.3, df ¼ 6, p , 0.05, *Not measured in the 1993study

Table VI Use of external marketing services

Service provider Percent using 1993 Percent using 2004

Advertising agency 7.4 8.4

Public relations firm 3.3 8.4

Marketing research firm 1.6 3.7

Marketing consultant 8.2 16.8

Notes: Chi-square = 27.81, df ¼ 3, p , 0.05

Accountants’ attitudes toward advertising: a longitudinal study

Kenneth E. Clow et al.

Journal of Services Marketing

Volume 23 · Number 2 · 2009 · 125–132

129

notable are the downward shifts in “costs too much,” “costsoutweigh benefits,” and “looks unprofessional to clients.”These results are consistent with the shift in attitudes towardsadvertising by accountants discussed earlier. The percentage

of respondents who indicated marketing costs too muchdeclined from 53.1 percent in 1993 to 25.2 percent in 2004.The percentage of respondents who stated marketing costsoutweigh benefits declined from 52.3 to 40.2 percent. Thepercentage of respondents who indicated advertising looks

unprofessional to clients decreased from 29.2 to 17.8 percent.As shown in Table VII, all of the remaining reasons for notusing marketing also declined, although not as much as thefirst three.

Conclusions

Although many changes have taken place in professionalservices marketing since the Bates decision and the FTCconsent decree, this study reveals significant shifts in attitudes

of accountants toward advertising their services. In almost allcases, these shifts represent more favorable attitudes towardadvertising of accounting services compared to the earlierstudy. The fear that advertising would protect larger,established firms and drive down prices was not as evident

in 2004 as it was in 1993. Further, more accountants in 2004believed there will be a positive impact on the quality ofservices provided as a result of advertising, forcing firms tobecome more competitive and more service-oriented towardstheir clients.For many years the accounting profession, as well as other

professional service organizations, had prohibitions againstadvertising, claiming it was unethical. But many accountants,

especially younger accountants and accountants with smalleraccounting firms believed the prohibition was enacted toprotect the large, established firms from encroachment bysmaller firms. This belief increased substantially by 2004indicating an increasing suspicion by accountants concerning

the true reason for enacting the advertising prohibition.Evidently, the FTC’s consent agreement was seen byaccountants as a signal by the federal government and legalsystem that professional organizations’ prohibition ofadvertising by their members constituted an unfair level of

competition and, thus, protected the larger, established firmsfrom more agile and competitive smaller firms.Some of the more dramatic changes in attitudes relate to

the overall attitude towards advertising. Fewer accountants in2004 believed advertising of accounting services would impairthe public’s confidence in accounting services or dilute the

firm’s credibility, confuse potential clients, or intensify

dissatisfaction among clients. This finding is especially

remarkable in light of the general attitude of skepticism by

consumers, with approximately 70 percent of consumers

believing that advertising is untruthful and cannot be trusted.

For accountants to indicate a more positive attitude towards

advertising at a time when the public, as a whole, is skeptical

of advertising highlights the interesting findings of this

research and a shift in attitude by accountants that runs

counter to society’s beliefs.Based on the findings of this study, then, the following

changes are afoot in the accounting profession’s perceptions

of advertising:. Philosophically, respondents have more positive feelings

about the use of advertising to help establish the

accountant-client relationship.. They view the competitive accounting environment as less

susceptible to advertising pressures. They overwhelmingly

reject the notion that advertising protects large,

established accounting firms from competition by small,

young firms; that anti-advertising codes of ethics exist to

maintain and increase the incomes of practicing

accountants; and that widespread use of advertising will

lead to large, established firms getting bigger while small

firms would become less competitive.. They affirm that accounting prices would not decrease as

a result of widespread accounting advertising; nor would it

result in a decline accounting service quality.. They believe that advertising does not impair public

confidence in the accounting profession; is viewed as

enlightening, not confusing, to potential clients; and is

regarded as credible to the public.. Although there is still a sizeable segment who feels the

need for a “Truth in Accountants’ Advertising Law,” it has

shrunk by about one-fourth since 1993.

This positive change in the general attitude towards

advertising resulted in an increased use of advertising by

accountants and the usage of marketing professionals as well

as marketing tools. It is clearly evident that the demand for

marketing services designed specifically for this group should

expand in the future. Many accountants cite the use of yellow

page advertising, websites, brochures, and seminars to

promote their services. Some firms are also using the

services of external marketing service providers and some

have part-time or full-time marketing personnel.

Managerial implications

The results from this study are encouraging for accounting

firms that wish to market their services and for marketing and

advertising agencies who are seeking new clients. From the

standpoint of the accounting firm, using a marketing firm,

advertising agency, or marketing consultant, is no longer

viewed negatively. Such services can be used to design an

accounting firm’s website and design brochures and other

advertisements. Providing this type of information to the

public will benefit potential clients and increase their

perception of the accounting firm’s ability to provide quality

service.This study is especially pertinent to advertising agencies,

marketing firms, and marketing consultants. Accountants are

a legitimate source of clients and should be actively pursued.

Table VII Why more marketing is not used

Reason

Percent

1993

Percent

2004

Costs too much 53.1 25.2

Costs outweigh benefits 52.3 40.2

Looks unprofessional to clients 29.2 17.8

No competitive pressure 25.5 14.0

Not enough knowledge of what to do 19.8 18.2

Looks unprofessional to other accountants 14.0 11.2

Other reasons 19.8 11.2

Notes: Chi-square = 31.52, df ¼ 6, p , 0.05

Accountants’ attitudes toward advertising: a longitudinal study

Kenneth E. Clow et al.

Journal of Services Marketing

Volume 23 · Number 2 · 2009 · 125–132

130

Most now have a positive attitude towards advertising, or at

least, not a negative attitude. They are open to marketing and

advertising approaches and see it as a way of making their firm

more competitive.Based on this study, advertising does not need to focus on

price. Most accountants did not believe prices charged to

clients will decrease. They see just the opposite. Accountants

believe that through advertising of their services, the quality of

service provided to clients will improve. Promoting this higher

level of service is certainly attractive to clients as well as to

accounting firms.While websites will continue to grow in importance, the use

of television advertising doubled during the span of these two

studies and is an attractive medium for advertising of

accounting services. While billboards are a small part of this

advertising picture, its importance has increased and should

be pursued. The one medium that needs less emphasis is

newspapers. This may be due to the feeling that it is more

difficult to project an image of providing high quality service

through newspaper advertising. Television advertising and

brochures provide a more conducive vehicle for conveying

service quality.Because of this shift in attitude, a window of opportunity is

open for advertising agencies, public relations firms,

marketing research firms, and marketing consultants to tap

a market that in the past was largely taboo. Accountants no

longer believe marketing costs too much and looks

unprofessional. While not fully convinced the benefits

outweigh the costs, most understand the need to advertising

and promote their accounting service.

Recommendations for future research

This study found significant changes in the attitudes of

accountants towards advertising their services. Future studies

need to examine the attitude of consumers towards

advertising of accounting services. Does advertising impact

a potential client’s image of an accounting firm? Has a similar

shift occurred or do consumers remain skeptical of advertising

as was found by Calfee and Ringold (1994)?Because accountants are more positively disposed to

advertising, opportunities for marketing professionals should

increase. As a result, research should be conducted as to the

best and most effective marketing tools for accounting

services. In addition, what advertising approaches, appeals,

and executions should be used? This study opens the door to

a number of possible studies into the impact of advertising of

accounting services and the most effective means of

accomplishing that advertising.

References

Bose, K.M. and Law, J.L. (2003), “Impact of the 1990

AICPA-FTC consent decree: a decade later, has anything

really changed?”, Services Marketing Quarterly, Vol. 25

No. 2, pp. 55-66.Calfee, J.E. and Ringold, D.J. (1994), “The 70 percent

majority: enduring beliefs about advertising”, Journal of

Public Policy, Vol. 13, pp. 228-38.Darling, J.R. (1977), “Attitudes toward advertising by

accountants”, The Journal of Accountancy, Vol. 143 No. 2,

pp. 48-53.

Dyer, R.F. and Shimp, T.A. (1978), “Reactions to legal

advertising”, Journal of Advertising Research, Vol. 20, April,pp. 43-51.

Ford, G.T., Smith, D.B. and Swasy, J.L. (1990), “Consumerskepticism of advertising claims: testing hypotheses from

economics of information”, Journal of Consumer Research,Vol. 16 No. 4, pp. 433-41.

Gamble, G.O., Highsmith-Quick, G., Jones, E., Slade, P.D.and Craig, J.L. Jr (2000), “What small and medium-sized

firms think about advertising”, CPA Journal, Vol. 70 No. 2,pp. 52-3.

Hite, R.E. and Fraser, C. (1988), “Meta-analyses of attitudestoward advertising by professionals”, Journal of Marketing,Vol. 52, July, pp. 95-105.

McConkey, W.C., Stevens, R.E. and Loudon, D.L. (2003),“Surveying the service sector: a pilot study of the

effectiveness of mail versus internet approaches”, ServicesMarketing Quarterly, Vol. 25 No. 1, pp. 75-84.

Markham, S., Cangelosi, J. and Carson, M. (2005),“Marketing by CPAs: issues with the American Institute

of Certified Public Accountants”, Services MarketingQuarterly, Vol. 26 No. 3, pp. 71-82.

Traynor, K. (1984), “Accountant advertising: perceptions,attitudes, and behaviors”, Journal of Advertising Research,Vol. 23 No. 6, pp. 35-40.

Corresponding author

Kenneth E. Clow can be contacted at: [email protected]

Executive summary and implications formanagers and executives

This summary has been provided to allow managers and executivesa rapid appreciation of the content of the article. Those with aparticular interest in the topic covered may then read the article in

toto to take advantage of the more comprehensive description of theresearch undertaken and its results to get the full benefit of thematerial present.

Strange to think that there was once a time, not too manyyears ago, when accountants did not advertise their skills and

services. Not only was it at odds with their professional codeof ethics, it was viewed as somehow beneath the dignity of the

calling. And accountants were not the only professionals whoconsidered advertising taboo – attorneys, dentists, and

physicians held similar views. Although many youngeraccountants were convinced that advertising was essential iftheir firms were to grow, the general feeling was a fear that

negative impacts on image, credibility, and dignity were likely,with little benefit for consumers.All that has changed and if you want an accountant these

days you can find any number of them proudly advertising

their expertise, not least on the internet where firms clamor tocompete. For marketing professionals, this shift to a more

positive attitude provides opportunities to offer them greatermarketing and advertising services. Most now have a positive

attitude towards advertising, or at least, not a negative one.They are open to marketing and advertising approaches andsee it as a way of making their firm more competitive.Advertising agencies, PR firms, market research companies,

and marketing consultants can now tap a market that in the

past was largely off limits. Accountants no longer believe

Accountants’ attitudes toward advertising: a longitudinal study

Kenneth E. Clow et al.

Journal of Services Marketing

Volume 23 · Number 2 · 2009 · 125–132

131

marketing costs too much and looks unprofessional. While

not fully convinced that the benefits outweigh the costs, most

understand the need to advertise and promote their service.In “Accountants’ attitudes toward advertising: a

longitudinal study”, Kenneth E. Clow et al. ask:1 How has the use of various marketing services and tools

changed over the last ten years?2 How has the ranking of various marketing tools used

changed during this time?

Based on their findings, the following changes are afoot in the

accounting profession’s perceptions of advertising:. Philosophically, respondents have more positive feelings

about the use of advertising to help establish the

accountant-client relationship.. They view the competitive accounting environment as less

susceptible to advertising pressures. They overwhelmingly

reject the notion that advertising protects large,

established accounting firms from competition by small,

young firms; that anti-advertising codes of ethics exist to

maintain and increase the incomes of practicing

accountants; and that widespread use of advertising will

lead to large, established firms getting bigger while small

firms would become less competitive.. They affirm that accounting prices would not decrease as

a result of widespread accounting advertising; nor would it

result in a decline in accounting service quality.. They believe that advertising does not impair public

confidence in the accounting profession; is viewed as

enlightening, not confusing, to potential clients; and is

regarded as credible to the public.. Although there is still a sizeable segment who feels the

need for a “truth in accountants’ advertising” law, it has

shrunk by about one-fourth since opinion was previously

tested in 1993.

This positive change in the general attitude towardsadvertising resulted in an increased use of advertising byaccountants and the usage of marketing professionals as wellas marketing tools. It is evident that the demand formarketing services designed specifically for this groupshould expand in the future. Many accountants cite the useof yellow page advertising, websites, brochures, and seminarsto promote their services. Some firms are also using theservices of external marketing service providers and somehave part-time or full-time marketing personnel.All of which is encouraging for accounting firms that wish

to market their services and for marketing and advertisingagencies who are seeking new clients. Accountants are alegitimate source of clients and should be actively pursued.Based on this study, advertising does not need to focus onprice. Most accountants did not believe prices charged toclients will decrease. They see just the opposite. Accountantsbelieve that through advertising their services, the quality ofthe service provided will improve. Promoting this higher levelof service is certainly attractive to clients as well as toaccounting firms.While websites will continue to grow in importance, the use

of television advertising has also increased significantly and isan attractive medium for advertising accounting services.While billboards are a small part of this advertising picture,their importance has increased and should be pursued. Theone medium that needs less emphasis is newspapers. Thismay be due to the feeling that it is more difficult to project animage of providing high quality service through newspaperadvertising. Television advertising and brochures provide amore conducive vehicle for conveying service quality.

(A precis of the article “Accountants’ attitudes toward advertising:a longitudinal study”. Supplied by Marketing Consultants forEmerald.)

Accountants’ attitudes toward advertising: a longitudinal study

Kenneth E. Clow et al.

Journal of Services Marketing

Volume 23 · Number 2 · 2009 · 125–132

132

To purchase reprints of this article please e-mail: [email protected]

Or visit our web site for further details: www.emeraldinsight.com/reprints