terma a/s annual report 2007/08 · 2011-11-29 · 8 annual report 2007/08 management’s review...

TRANSCRIPT

Terma A/S Annual Report 2007/08

www.terma.com

Integrated Systems / Public Safety & Emergency

© Terma 2008Production idworks a/sImages David Bering; Niels Åge Skovbo; Stine S. Nielsen, FLVFOT, RDAF; and TermaPrinting Zeuner Grafisk as

Contents

4 Financial Highlights – Consolidated

5 Highlights of the Year

6 Management’s Review 2007/08

12 Business Areas

15 Group Management

16 Accounting Policies

20 Executive Management’s Statement

20 Independent Auditors’ Report

21 Statement of Income

22 Balance Sheet – Assets

23 Balance Sheet – Equity and Liabilities

24 Cash Flow Statement

25 Notes

Board of DirectorsSvend-Aage Nielsen, ChairmanHolger Lavesen, Deputy ChairmanHenrik StenbjerrePeter DyvigBo LaursenPaul-Werner Johnsen

Executive ManagementJens Maaløe, President & CEO

BankersDanske Bank Holmens Kanal 2–12 1092 København K Denmark

OwnersThrige Holding A/S Copenhagen

AuditorsKPMG Statsautoriseret Revisionspartnerselskab

Flemming Brokhattingen State-Authorized Public Accountant

Jes Lauritzen State-Authorized Public Accountant

Værkmestergade 258000 Århus C Denmark

4 Annual Report 2007/08

DKK million 2007/08 2006/07 2005/06 2004/05 2003/04

Order intake 1,438 957 1,011 1,136 871

Order book, year-end 1,730 1,331 1,379 1,369 1,447

Sales 1,039 1,005 1,001 1,214 1,096

Operating profit 115 96 89 100 85

Financial items (19) (15) (15) (18) (12)

Profit for the year 84 53 53 57 49

Non-current assets 506 455 440 441 438

Current assets 640 561 477 563 693

Assets, total 1,146 1,016 917 1,004 1,131

Capital stock 20 20 20 20 20

Equity 441 366 346 339 320

Allowances 89 69 44 35 29

Long-term liabilities other than allowances 188 144 148 169 141

Current liabilities other than allowances 429 437 379 460 641

Cash flows from operating activities 157 94 97 129 20

Cash flows from investing activities (117) (83) (38) (89) (107)

Portion relating to investments in property, plant, and equipment (28) (33) (21) (54) (66)

Cash flows from financing activities 20 (57) (39) (9) (24)

Cash flows, total 59 (47) 20 31 (112)

Financial ratios

Net profit ratio 11.1 9.5 8.0 8.2 7.8

Return on investments 11.6 10.9 9.2 9.4 7.8

Current ratio 149 128 126 122 108

Equity ratio 38.4 36.0 37.7 33.8 28.3

Return on equity 20.8 14.8 15.4 17.4 15.6

Average number of full-time employees 1,020 965 1,014 1,034 1,010

*Disposalofproperty,land,andequipmentforthefiscalyear2005/2006isnotincluded.

Net profit ratio

=

Return on investments =

Operating assets

= Total assets less cash and cash equivalents, other interest-bearing assets (including stock), and equity interest in affiliated companies

Operating profit* x 100Sales

Operating profit* x 100Average operating assets

Current ratio =

Equity ratio =

Profit/loss for analytical purposes = Profit for the year

Return on equity =Result for analytical purposes x 100Average equity, ex minority interests

Current assets x 100Current liabilities other than allowances

Equity, ex minority interest at year-end x 100Total liabilities at year-end

Definitions:

Financial Highlights – Consolidated

Financial Highlights – Consolidated

Annual Report 2007/08 5

March 2007 The Dutch Defence Material Organization (DMO) tasked Terma with delivery of a self-protection solution for Chinook CH-47F transport helicopters ordered by the Royal Netherlands Air Force (RNLAF). Terma will provide a solution for integration of a laser-based diversion of missile threats.

June 2007 Terma was tasked with delivery of SCANTER 2001 radar systems for the French FREMM frigate

program comprising 17 new frigates. Starting 2008 and continuing until 2010, Terma is tasked with delivering radar systems for navigation, surveillance, and helicopter guidance purposes.

June 2007 The Danish Defence Acquisition and Logistics Organization and Terma signed a contract for

C-Flex command and control systems for the new patrol vessels of the Royal Danish Navy. The contract ensures further development and knowledge of C-Flex within the Danish Navy.

July 2007 The Republic of Trinidad and Tobago selected Terma’s new SCANTER 4100 air/surface surveil-

lance radar as the prime sensor for three new offshore patrol vessels for the national Coast Guard. The ships will be delivered from VT Shipbuilding.

August 2007 Terma was selected by U.S. company Spirit AeroSystems as supplier of aerostructures. Terma is

contracted to manufacture a number of composite structures, including winglets and ailerons for a commercial aircraft project.

December 2007 Terma commenced subassemblies for the first two F-35 production aircraft. The authorization

represents the first F-35 contract awarded to Terma under a long-term agreement with Northrop Grumman. The subassemblies – composite components and aircraft access doors – will be used in the F-35 center fuselage.

December 2007 Saab and Terma signed an extensive cooperative agreement related to the replacement of the

Danish F-16 fighter aircraft. The agreement covers the areas of aviation, space, defense, and civil security. Certain elements of the agreement are subject to Denmark selecting the Gripen Next Generation.

January 2008 Terma was contracted to supply an Emergency Air Situation Display System to the Irish Aviation

Authority for the Air Traffic Control Centers in Dublin and Shannon. January 2008 Terma delivered the first Flight Test Instrumentation Pods for the F-35 aircraft program to

Lockheed Martin Aeronautics Company. Terma is contracted to supply seven items under the System Development and Demonstration (SDD) phase of the F-35 program.

February 2008 The Danish Defence Acquisition and Logistics Organization and Terma entered into an agreement

concerning production and delivery of 3-D/Active Noise Reduction Audio Systems for the Danish F-16s following successful flight tests. The 3-D Audio System will improve pilot reaction time.

February 2008 Terma entered into a contract with the Danish Agency for Governmental Management for the establishment, operation, and maintenance of the shared control room software for the Danish preparedness network’s new digital radio communication system, SINE. Terma is tasked with delivering the crucial link between the control rooms and the individual users.

Highlights of the Year

Highlights of the Year

6 Annual Report 2007/08

For Terma’s 1,150 employees, 2007/08 was fast-paced and filled with significant work efforts and accomplishments, providing year-end results which met the Company’s fiscal year objectives. Every Business Area met the financial targets set for 2007/08 and thereby realized a market position complying with Terma’s objective of being among the leading suppliers within our Business Areas.

Sales for the fiscal year were MDKK 1,039 with a profit before tax of MDKK 95.6.

The year’s intake of orders increased to MDKK 1,438, and the order book at year-end was MDKK 1,730. This constitutes a strengthened foundation for global market growth in the years to come.

Our activities in The Netherlands, the U.S., and Singapore continue to expand, reflecting the importance of being close to customers and strategic partners. Terma North America Inc. contributed by securing important strategic contracts within several of our Business Areas. Established in the beginning of 2007, Terma’s office in Singapore has experienced a high level of Radar Systems contracts in Asia.

Recent years’ targeted investments in product and market development combined with a strong performance and high-quality products and projects have resulted in several valuable and strategic contracts:

– The Aerostructures Business Area delivered the first products and components for the U.S. fighter aircraft F-35 Joint Strike Fighter. The unique competencies and specialized knowledge acquired and further developed via our commitment to this international program have resulted in significant contracts for production of aerostructures for the non-defense aircraft industry.

– The Integrated Systems Business Area entered into a major TETRA technology-based contract with the Danish Government for the supply of control room software for SINE, the future nationwide emergency preparedness network.

A number of new markets with significant business potential are currently cultivated and expected to further develop in the years ahead. Included are several countries in Eastern Europe, now members of NATO, but also India and countries in Asia.

In the 2007/08 fiscal year, Terma experienced an increase in total staff. This took place during a period of continued, heavy worldwide demand for highly skilled employees. Our reputation as an attractive and challenging workplace proved a significant asset to our recruiting efforts.

Terma continuously strives to optimize operational and organizational processes. The result of these initiatives has been an optimization of the current working capital and positive cash flows from operations secured through strong finance management. A solid foundation for investments in equipment, processes, and markets has been established, imperative for Terma’s global growth strategy. Terma’s financial position improved during the fiscal year.

Developments within the foreign exchange market are essential parameters in the financial management of Terma. Despite the declining USD, Terma has minimized the exposure to this currency through forward exchange transactions. However, a continued weak USD will affect our competitiveness in the growing U.S. market. Attempts are made to reduce the exchange risk through counter purchases in USD.

Management’s Review 2007/08

Management’s Review 2007/08 The fiscal year 2007/08 was fast-paced and filled with significant work efforts and accomplishments, providing year-end results which met the Company’s fiscal year objectives. A number of new markets with a significant business potential are currently cultivated and expected to further develop in the years ahead.

Jens Maaløe President & CEO

Radar Systems

8 Annual Report 2007/08

Management’s Review 2007/08

During the fiscal year, a decentralization of internal, central support functions to the Business Areas has been initiated, primarily within Business Controlling, Human Resources, and Quality & Process Management. This process will be continued, aiming to expand the scope and decision authority within the Business Areas.

The process is supported by a stringent structure with establishment of well-defined Business Units within the Business Areas. The structure guarantees a forward-looking focus on market access and related strategies for Terma’s many product areas. Further, it enhances readiness to respond rapidly to changes within our chosen market segments.

With good reason, Terma is comfortable with current trends, and the Terma staff can be very proud of its efforts and the Group’s position. The commitment of our employees is outstanding, and the Board of Directors and the Group Management are greatly appreciative.

Results for 2007/08

The year’s intake of orders was MDKK 1,438 as compared to MDKK 957 in 2006/07, nearly a 50 percent increase. Order book at year-end was MDKK 1,730 as compared to MDKK 1,331 for 2006/07. The increase in order book constitutes a solid basis for the expected growth in the years to come.

Sales for the fiscal year increased by MDKK 34, totaling MDKK 1,039, an organic growth of 3 percent.

The profit before tax amounted to MDKK 95.6, which is an increase of approximately MDKK 15, or 19 percent compared to 2006/07. All Business Areas of the Group contributed with positive results towards the total profit for the year. The increase in profit is a result of the successful extensive initiatives to improve the efficiency of operations.

During 2007/08, Terma maintained a strong focus on Balance Sheet metrics, and the result is satisfactory in view of the sales and order intake levels. Inventories were valued at MDKK 154 which is satisfactory as compared to the order book. The working capital is also consistent with the increased sales activities, investments, and payroll costs. Terma maintained positive cash flows, and the draw on credit facilities was reduced by more than 50 percent as compared to 2006/07.

A decision was made to reduce the capital stock through annulment of Terma’s own stockholding (10 percent). Therefore, Thrige Holding A/S now owns the entire capital stock in Terma A/S. The stock annulment has no effect on the Statement of Income for the 2008/09 fiscal year.

The Board of Directors proposes a dividend payment of MDKK 21.

Outlook for the 2008/09 Fiscal Year

Terma expects organic growth of 10–15 percent, equivalent to

a sales level of MDKK 1,150–1,200. We foresee positive market

trends in Terma’s primary markets and anticipate increases in

order intake commensurate with sales fueled by several major

projects within all five Business Areas.

Despite an increased sales level, the profit before tax is

expected to remain unchanged. In 2008/09, Terma faces

considerable investments in internal development projects

as well as in manufacturing assets in Grenaa to support the

future F-35 Joint Strike Fighter business. The budget for next

year also includes investments in the strengthening of project

management as well as in sales and marketing activities.

Further operational improvements are expected as a result of

the efficiency initiatives which have already been implemented

and which will continue.

An order book totaling MDKK 1,730 at the beginning of 2008/09

constitutes a solid foundation for activities during the year and

provides a sound planning horizon. At the beginning of 2008/09,

Terma experienced a secured sales order level of more than 60

percent.

No significant credit risks exist relative to individual customers

or strategic partners. Political and commercial risks are

assessed prior to entering into major commitments.

Cash flow of foreign currency contracts is hedged. Contribution

ratio of portfolio of new orders is affected to a certain

degree by exchange rate fluctuations, especially of the USD.

However, these are within the framework of ordinary operating

uncertainties.

Business Areas

During the 2007/08 fiscal year, Terma retained focus on the

development of the five Business Areas:

1. Aerostructures: Development and production of advanced

structures and engine components for defense and non-

defense aircraft

2. Airborne Systems: Self-protection equipment for fighter

aircraft, transport aircraft, and helicopters

3. Integrated Systems: Command and control systems for

defense and non-defense purposes

4. Radar Systems: Advanced radar systems for coastal

surveillance and surveillance of airports

5. Space: Mission-critical products and software for space

applications.

The activities of the Business Areas to exploit the market

potential are increasingly supported by the internationally based

offices and subsidiaries in the U.S., The Netherlands, Germany,

and Singapore.

Annual Report 2007/08 9

International Growth Potential

Terma’s future growth potential is anticipated mainly in the global arena, including traditional markets in Europe and the U.S., countries in Eastern Europe which have joined as members of NATO, India, and countries in Asia.

As a result of continuously strengthened financial resources, the continued optimization of business processes and internal processes, and a strengthened global presence, Terma holds a strong position to implement the global growth strategy through organic growth and via acquisitions.

The aerospace and defense market is currently growing. Several NATO countries and India are planning the acquisition of new aircraft and helicopters. Further, participation in international operations necessitates upgrade of existing materiel and development of new solutions. This results in a major interest in Terma products and systems such as electronic self-protection and communication systems for army and navy purposes.

Replacement Aircraft

A conclusive decision by the Danish Parliament as to selection of a new fighter aircraft for the Royal Danish Air Force is expected during 2009. The decision is very important for the future development of Terma and, in particular, the Aerostructures Business Area. During the last 10 years, Terma has followed the situation closely and has entered into agreements with the potential suppliers, i.e. Lockheed Martin (F-35) and Saab (Gripen). At the end of 2007, the Eurofighter consortium decided to suspend its participation in the competition to supply new fighter aircraft.

In December 2007, Terma and Saab/Gripen entered into a significant cooperative agreement with a business potential valued at approximately MDKK 10,000 over a period of 10–15 years, subject to Gripen being selected as replacement fighter aircraft. A similar value potential applies to the agreements and contracts entered into with Lockheed Martin and a number of the company’s key subcontractors for development and production for the F-35.

Involvement in the F-35 program currently includes 12 contracts and framework agreements with a continuously increasing activity level which will reach a long-term peak once serial production is initiated.

Homeland Security

Homeland security is also a growth market for Terma. Radar equipment for coastal surveillance purposes is in great demand, and Terma’s recent contract for control room software for the future Danish emergency preparedness network creates further opportunities for business development within this market segment.

Activities within the Business Areas

The following presents a brief review of strategic initiatives within the individual Business Areas.

Aerostructures

Due to a significant intake of new orders and a high activity level, Aerostructures is experiencing a renewed positive development.

The first products for the U.S. fighter aircraft F-35 Joint Strike Fighter have been designed and delivered. At the end of 2007, Aerostructures delivered the first Test DART Pod to Lockheed Martin, and at the beginning of 2008, intense development efforts were concluded with delivery of the first Gun Pod to General Dynamics. Both programs will proceed with production, and new design and production programs will be initiated in 2008 and 2009, targeting structures for the aircraft fuselage, edges and stabilizers, and engine components.

The F-35 design and production programs embrace new, advanced material and production technologies which are strategically important for Terma’s future development and growth opportunities. This competence building has resulted in a business breakthrough for Aerostructures in the form of a contract with U.S. company Spirit AeroSystems. Terma is contracted to manufacture a number of composite structures, including winglets and ailerons for a commercial aircraft project.

Airborne Systems

The advanced self-protection systems of Airborne Systems combined with the Business Area’s ability to handle quick reaction programs secured contracts with new and existing customers.

The Royal Danish Air Force decided to install Terma’s unique 3-D Audio technology in its F-16 fighter aircraft. This is a valuable reference for the future efforts to promote and market the technology to other customers and platforms such as other types of aircraft and, over time, combat military vehicles such as tanks.

A cooperative agreement was entered into with the National Aerospace Laboratory in The Netherlands for the establishment of a European center of excellence for the self-protection of aircraft and helicopters. This agreement holds promising potential for the Royal Netherlands Air Force regarding electronic warfare (EW) maintenance, service, and training for other existing and new international customers.

As a result of Terma’s long-standing collaboration with the U.S. Air Force and the U.S. Air National Guard within the EW business segment, Terma systems are installed in more than 1,000 U.S. fighter aircraft. Relations have been further strengthened by new contracts and cooperative agreements

Management’s Review 2007/08

10 Annual Report 2007/08

Management’s Review 2007/08

with the U.S. Air Force for upgrades of EW systems (the ALQ-213 Advanced Processor Upgrade Program) and by a multi-year framework contract for EW repair and service with the U.S. National Guard.

Integrated Systems

Integrated Systems’ command and control system C-Flex is installed in all new Royal Danish Navy ships. Its flexible architecture and system reliability have boosted global interest and demand from navies and naval dockyards.

In February 2008, Terma entered into a contract with the Danish Agency for Governmental Management for the supply of control room software for the future digital, nationwide radio communication system, SINE. In the years to come, SINE will be rolled out in Denmark and will ensure that the emergency services, provided by the Fire and Rescue Brigade, the Police, the Defense, the Home Guard, and municipal and regional authorities, can operate on one shared radio network. SINE is to replace approximately 100 local networks and will be used in day-to-day incidents as well as during major, multi-agency events and emergencies.

The control room software is applied to manage resources and to coordinate and manage communication between emergency services control rooms and users of the radio network (Police, Fire Brigade, etc.). It is thus the technical solution which links the control rooms and the individual users of the radio terminals.

Based on multi-year experiences with development of command and control systems for defense purposes, Terma won the contract in an international competition. The contract is strategically important and may over time result in the establishment of a new, independent non-defense business area. A number of countries are currently implementing similar nationwide solutions.

Radar Systems

In 2007/08, Radar Systems continued the growth trend experienced in recent years and further consolidated its strong international position as a leading supplier of radar systems for surveillance and security purposes.

Terma entered into a contract with Latvia for radar systems for coastal and traffic surveillance purposes.

Further, Terma initiated deliveries of radar systems for navigation and surveillance purposes for a major French frigate program.

Activities in Asia have been further strengthened following the establishment of an office in Singapore. At the beginning of 2008/09, the office will be registered as an actual Terma

subsidiary, named Terma Singapore Pte. Ltd. In 2007, Radar Systems landed the first major radar/sensors contract for a VTS system for the Maritime Port Authorities in Singapore.

Space Systems

The Space Systems Business Area retained focus on future assignments of significance in connection with ESA’s scientific missions and the European satellite-based navigation system, Galileo. Further, the Space Systems Business Area is project manager of the international Atmosphere-Space Interactions Monitor (ASIM), a program which will observe the atmosphere from the International Space Station to improve our understanding of the Earth’s climate and its changes.

Efforts were further intensified in the North American market where the demand for Terma’s products and systems is growing.

An Attractive Workplace

At the end of the fiscal year, total staff had increased to 1,150. The extensive recruitment primarily took place in the Danish locations and is based on the increased intake of orders and expectations of continued growth.

Within the last two years, Denmark has experienced a heavy demand for skilled employees and thus a sharpened competition to attract new employees. As a high-tech, specialized Company, Terma enjoys a good reputation as an attractive workplace with excellent opportunities for personal and professional development. In our efforts to attract and retain staff, a number of new employee offers and benefits have been introduced, and office and manufacturing facilities are continuously being renovated and extended.

Terma’s loyal and stable workforce is characterized by a low level of absence due to sickness and a low level of employee turnover. Further initiatives to enhance competence development and job satisfaction are currently being prepared.

Total staff is expected to increase further in the years to come. In view of the continued recruitment strain, this challenge is top priority – requiring from the entire organization and Human Resources in particular new initiatives and targeted branding strategies.

Airborne Systems / Audio Systems

12 Annual Report 2007/08

Business Areas

Aerostructures

Airborne Systems

The Aerostructures Business Area specializes in the design and manufacture of advanced structural parts for the defense and non-defense markets, including products for the F-16 fighter aircraft, the EH101 transport and rescue helicopter, as well as the Gulfstream business jet.

The Business Area has successfully expanded its activities to incorporate the design and manufacture of advanced composite structures for the commercial aircraft industry and has secured its largest single order from this industry.

The F-35 Joint Strike Fighter is a top priority program. Since first involvement in 2004, Terma has secured contracts for seven items, and the first test and SDD products have been delivered. Terma is continuing crucial competence development for the design and manufacture of high quality, complex, and price competitive composite structures for the F-35 program.

In the year to come, Terma will make significant investments to upgrade the manufacturing capabilities and infrastructure to meet

the technology and delivery requirements of the F-35 program.

Terma’s Engine Components Business Unit has successfully designed and manufactured the first Stator Vanes for one of the F-35 engine manufacturers. This is another breakthrough for Terma and it will provide the basis for additional business within a booming market for sophisticated design and manufacture of composite products for high performance commercial and fighter engines.

Aerostructures continuously strives to deliver high quality products for our long-standing customer base as well as for new customers. In early 2008, U.S. aircraft manufacturer Gulfstream, for the third consecutive year, nominated Terma “Top Performer of the Year” for the successful production and delivery of winglets and other structural parts for more than 500 Gulfstream aircraft. The award was succeeded by the signing of a multi-year framework contract for supplies to the Gulfstream.

The Airborne Systems Business Area provides defense electronics

solutions and services for electronic warfare (EW), tactical

reconnaissance, applied aerostructures, and audio systems. The

heavy market demand continues to prevail for the self-protection

systems used in fighters, transport aircraft, and helicopters. These

systems are based on the AN/ALQ-213 system, and to date, this

system has been installed in more than 1,700 aircraft worldwide.

In response to urgent operational requirements, we have rapidly

provided self-protection systems for the RAF Nimrod, GAF Tornado,

and RAF Harrier aircraft.

Together with EADS and in cooperation with the Royal Danish

Air Force, Terma is developing a unique missile warning system

for the F-16 aircraft. The solution includes the 3-D/Active Noise

Reduction Audio System which has now entered series production

following successful, extensive tests and evaluations. The system

significantly improves pilot working conditions and reaction times.

Together with the Northrop Grumman Corporation, Terma has

delivered EW equipment for the Boeing P-8A Multi-Mission

Maritime Aircraft (MMA). The P-8A is selected by the U.S. Navy

as its long-range anti-submarine warfare, anti-surface warfare,

intelligence, surveillance, and reconnaissance aircraft.

Terma continues to support the AWACS program with manufacture

and delivery of advanced wiring harnesses to Boeing and printed

circuit boards to Northrop Grumman. A number of electronics

manufacturing activities have been secured in support of the F-35

Joint Strike Fighter program.

To better serve our U.S. customers, the security cleared facility in

Warner Robins, Georgia, has been expanded to include additional

capabilities for software development, systems integration,

integration testing, and repair services. In addition, an Electronic

Warfare Competence Center (EWCC) is currently being established

in The Netherlands in cooperation with the National Aerospace

Laboratory.

Erik Laursen Senior Vice President

Steen M. Lynenskjold Senior Vice President

Annual Report 2007/08 13

Business Areas

Integrated Systems

Radar Systems

The Integrated Systems Business Area delivers command and control

systems integrated with sensors, effectors, and communication

infrastructure, based on T-Core, the joint integration platform. The

system provides situational awareness in both a military and civilian

context and is used by the Danish Defense and the national emergency

services.

The Royal Danish Navy’s flexible support vessels and inspection vessels

have the naval T-Core version “C-Flex” installed, and an up-scaled

system will be installed in the new Danish frigates. In 2007, the

system was delivered to the Romanian Navy for the Marasesti frigate.

A complete system package with sensors and weapon interfaces for

ocean patrol vessels was launched in 2007 and is currently being

delivered.

The Austrian Army was the first international customer to purchase the

army T-Core version “CWS-Flex” for its air defense system upgrade. In

2007, the T-Core army battle management system “BMS-Flex”

was launched with full communication infrastructure for multiple,

concurrent radio platforms.

In 2007, the flight information management system was delivered to

Naviair, the Danish aviation network service provider, together with the

new radar data processing backup system. A similar information system

was delivered to the National Air Traffic Services (NATS) in the UK.

In 2007, the public safety and emergency T-Core version “T.react” was

selected as the command and control information infrastructure for the

Danish national emergency services; a system to be shared by the Fire

and Rescue Brigade, the Police, the Defense, and the Home Guard. The

contract includes a long-term 24/7 operation and maintenance services

contract.

Common to the navy, army, air force, and homeland security application

suites is the fact that they can share tactical data and are scalable

“plug-and-play” systems with open software interfaces allowing for

further additions of subsystems and interfaces to external systems.

The Radar Systems Business Area designs and delivers advanced

radar systems for the surveillance of coasts, ports, waters, and

vessel traffic for customers worldwide. The international focus on

terror, illegal immigrants, weapons, and drug trafficking means

growing demands for the surveillance of coasts, ports, and

territorial waters.

The SCANTER radar systems are renowned for their unique

capability to detect small and minute targets at long distances

and under all weather conditions. The SCANTER radar family is

currently being enhanced and further developed. It comprises

SCANTER 2001i, SCANTER 4000 and 4100, as well as a wide range

of high performance antennas.

In 2007/08, the market continued its positive trend. The SCANTER

2001i remains the preferred radar for marine and port surveillance.

The sale of 13 SCANTER 2001i systems to Latvia means that it

is now possible to sail under the monitoring of Terma SCANTER

radars from St. Petersburg in Russia through the Baltic Sea and all

the way through Europe’s rivers and canals.

In the Mexican Gulf region, additional orders were received

for systems supporting antidrug trafficking missions, including

SCANTER 4100 systems for Trinidad and Tobago and SCANTER

2001i for Florida and Colombia.

The airport surveillance market has shown significant growth by

way of orders from South African airports, the Dubai Airport, and

additional extensions at several large European airports where

SCANTER radars are already in operation.

The regional office in Singapore has experienced significant

success during the past year. Long-term relations within the

region have been further solidified and additional local staff has

been hired.

Peter Deichmann Senior Vice President

Morten Winterberg Senior Vice President

Business Areas

Carsten Jørgensen Senior Vice President

Space Systems

Terma B.V.

14 Annual Report 2007/08

Richard Jones Senior Vice President Terma B.V.

The knowledge and technology of Danish space research and Danish companies within this market area are world-class. In recent years, an increasing commercial, scientific, and educational interest has manifested itself. These developments have created new opportunities for re-energizing the Danish business and scientific activities within the space industry.

Terma contributes with mission-customized software and hardware products to support a number of the in-orbit pioneering European scientific missions, such as Rosetta, Mars Express, and Venus Express.

On this background, Terma has secured significant contracts for Galileo, the future European satellite navigation system which is expected to be operational in 2013. This includes the portfolio of Terma Space Systems including power supplies, check-out and test systems, and mission control and simulation systems. Terma will develop and deliver the power supplies for the first four satellites with a good opportunity to secure orders for the

delivery of the following 26 satellites when these are procured in 2008/2009.

Currently, Terma is contracted for the development and delivery of software and hardware systems for numerous ongoing and future European, Russian, Canadian, and U.S. satellite missions. Examples of these are Lisa Path Finder with expected launch in 2010, Herschel & Planck with expected launch in 2009, GAIA with expected launch in 2012, the U.S distributed Sensing Experiment, and the Canadian Sapphire mission.

Furthermore, in 2007, Terma entered into a contract with ESA for the man-spaced ASIM mission. Terma is currently responsible for a scientific and industrial team developing a structure of six cameras to be placed outside the International Space Station. The purpose of the mission is to contribute to the study and understanding of how thunderstorms affect the atmosphere and the climate.

Terma B.V., the Dutch subsidiary, is focused on three prime market areas: space, aircraft survivability equipment, and public safety and emergency. This past year has seen a significant effort targeted at expanding the role of Terma B.V. in supporting electronic warfare (EW) products.

Space activities include in-house turnkey system integration and system development specializing in spacecraft test and management systems and the provision of highly specialized consultants to ESTEC. These service contracts have performed well and have met customer requirements.

EW products delivered by Airborne Systems to the Royal Netherlands Air Force (RNLAF) require technical support services, including modification programs. In 2007, Terma B.V. initiated a dialog with the RNLAF to establish a local support facility in Woensdrecht, The Netherlands, for maintenance, repair, and overhaul activities for both fixed-wing and helicopter platforms. This facility, the Electronic Warfare Competence

Center (EWCC), will expand in the future to support similar protection systems from other NATO air forces. The EWCC will start operations in the fourth quarter of 2008.

Specific interest from the Dutch Government is focused on mission-critical systems developed for defense purposes which can be adapted for non-defense use. The recent contract awarded to Integrated Systems to deliver and support the control room software for the Danish preparedness network SINE precedes the approaching intention of the Dutch Government to release an international call for proposals for a new crisis management center. Terma B.V. is now in the process of establishing a consortium with existing international and strong local partners to respond to this request.

Annual Report 2007/08 15

Business Areas and Group Management

Group Management

Terma North America Inc.

James (Jim) Brandt President & CEO Terma North America Inc.

Lars Marcher Executive Vice President, CFO & Operations

Morten Halskov Executive Vice President, Corporate Services

Jens Maaløe President & CEO

Terma North America Inc. (TNA), the U.S. subsidiary of Terma A/S, headquartered in the Washington D.C. area, has now been established as the face to the U.S. customers for all five Terma Business Areas.

A breakthrough was achieved in the Aerostructures Business Area with the competitive win of a contract from Spirit AeroSystems, a U.S. company based in Tulsa, Oklahoma. Terma will manufacture composite components for commercial aircraft.

By leveraging the impressive history of the Airborne Systems AN/ALQ-213 product line for aircraft self-protection and the excellent reputation Terma has with the U.S. Air Force, TNA has positioned itself as the official U.S. Depot Level Maintenance Facility for this system. Terma has been awarded a multi-year repair contract for the hardware and will also perform software maintenance and upgrades for the system. The commitment to this product line and to Terma was further demonstrated by the

U.S. Air Force and the U.S. Air National Guard this past year by the award of a significant engineering development contract for the ALQ-213 Advanced Processor Upgrade Program.

The Radar Systems Business Area achieved success within TNA this past year with the successful award of a contract using U.S. Department of Homeland Security funds to procure Terma radars to be installed in Palm Beach, Florida for coastal surveillance.

An important relationship with Lockheed Martin was formalized within the Integrated Systems Business Area. Terma and Lockheed Martin will co-develop a command and control product for ballistic missile defense (BMD) applications.

Terma’s Space Systems Business Area was also brought on line within TNA this past year. The local presence of TNA business development professionals is expected to result in significant market penetration and new business opportunities.

16 Annual Report 2007/08

Accounting PoliciesThe annual report of Terma A/S for 2007/08 has been prepared in accordance with the provisions applying to class C enterprises (large) under the Danish Financial Statements Act. The Consolidated Financial Statements of Terma A/S are consolidated in the Consolidated Financial Statements of the ultimate Parent Company, the Thomas B. Thrige Foundation, Copenhagen.

Accounting policies applied in the preparation of the annual report are consistent with those of last year.

Consolidated Financial Statements

The Consolidated Financial Statements comprise the Parent Company, Terma A/S, and subsidiaries in which Terma A/S directly or indirectly holds more than 50 percent of the voting rights or which it, in some other way, controls.

The Consolidated Financial Statements are prepared as a consolidation of the audited financial statements of the Parent Company and subsidiaries, which have all been prepared according to the Group’s accounting policies.

On consolidation, intra-group income and expenses, stockholdings, intra-group balances and dividends, and realized and unrealized gains and losses on intra-group transactions are eliminated.

Equity interests in subsidiaries are set off against the proportionate share of the subsidiaries’ fair value of net assets or liabilities at the acquisition date.

Enterprises acquired or formed during the year are recognized in the Consolidated Financial Statements from the date of acquisition. Enterprises disposed of are recognized in the Consolidated Statement of Income until the date of disposal. The comparative figures are not adjusted for acquisitions or disposals.

Acquisitions of enterprises are accounted for using the purchase method, according to which the identifiable assets and liabilities acquired are measured at their

fair values at the date of acquisition. Allowance is made for costs related to adopted and announced plans to restructure the acquired enterprise. The tax effect of the revaluation is taken into account.

Any excess of the cost of the acquisition over the fair value of the identifiable assets and liabilities acquired (goodwill), including restructuring allowances, is recognized as intangibles and amortized on a systematic basis in the Statement of Income based on an individual assessment of the useful life of the asset, however, not exceeding 20 years. Any excess of the fair values of the identifiable assets and liabilities acquired over the cost of the acquisition (negative goodwill), representing an anticipated adverse development in the acquired enterprises, is recognized in the Balance Sheet as prepayments and deferred charges and recognized in the Statement of Income as the adverse development is realized. Negative goodwill, not related to any anticipated adverse development, is recognized in the Balance Sheet at an amount corresponding to the fair value of non-monetary assets. The amount is subsequently recognized in the Statement of Income over the average useful lives of the non-monetary assets.

Goodwill and negative goodwill from acquired enterprises can be adjusted until the end of the year following the acquisition.

Gains or losses on disposal of subsidiaries are stated as the difference between the sales amount or disposal amount and the carrying amount of net assets at the date of disposal, including non-amortized goodwill and anticipated disposal costs.

Foreign Currency Translation

Transactions denominated in foreign currencies are translated at the exchange rates at the transaction date. Foreign exchange differences arising between the exchange rates at the transaction date and at the date of payment are recognized

in the Statement of Income as a financial income or financial costs.

Receivables, payables, and other monetary items denominated in foreign currencies, which are not settled on the Balance Sheet date, are translated at the exchange rates at the Balance Sheet date. The difference between the exchange rates at the Balance Sheet date and at the date at which the receivable or payable arose or was recognized in the latest financial statements is recognized in the Statement of Income as financial income or financial costs.

Derivative Financial Instruments

Derivative financial instruments are initially recognized in the Balance Sheet at cost and are subsequently measured at fair value. Positive and negative fair values of derivative financial instruments are included in other receivables and other payables, respectively.

Changes in the fair value of derivative financial instruments designated as and qualifying for recognition as a hedge of the fair value of a recognized asset or liability are recognized in the Statement of Income together with changes in the value of the hedged asset or liability.

Changes in the fair value of derivative financial instruments designated as and qualifying for recognition as a hedge of future assets or liabilities are recognized directly in the equity. Income and expenses relating to such hedging transactions are transferred from equity on realization of the hedged item and recognized in the same item as the hedged item.

Statement of IncomeSales

Sales comprise the deliveries for the year and the change in value of contract work in process (long-term).

Contract work in process (long-term) is recognized as sales when it reaches the

Accounting Policies

Annual Report 2007/08 17

stage of completion. Accordingly, sales correspond to the sales price of work performed during the year (percentage of completion method).

ProductionCosts

Production costs comprise costs, including depreciation, amortization, and salaries, incurred in generating the sales for the year. Such costs include direct and indirect costs for raw materials and consumables, wages and salaries, depreciation of production plant, and other production costs.

Production costs also comprise research and development costs, which do not qualify for capitalization and amortization of capitalized development costs.

DistributionCosts

Costs incurred in distributing goods sold during the year and in conducting sales campaigns, etc. during the year are recognized as distribution costs. Also, costs relating to sales staff, advertising, exhibitions, and depreciation are recognized as distribution costs.

AdministrativeCosts

Administrative costs comprise expenses incurred during the year for Group Management and Administration, including expenses for administrative staff, office premises and office expenses, and depreciation.

OtherOperatingIncomeandCosts

Other operating income and costs comprise items secondary to the principal activities of the Group, including gains and losses on disposal of intangibles and property, plant, and equipment.

FinancialIncomeandCosts

Financial income and costs comprise interest income and expenses, gains and losses on payables, and transactions denominated in foreign currencies, amortization of financial assets and

liabilities as well as surcharges and allowances under the tax prepayment scheme, etc. Financial income and costs are recognized with the amounts relating to the fiscal year.

TaxonProfitfortheYear

The Group is subject to the compulsory Danish joint taxation method for the Thrige Holding Group’s Danish companies. Subsidiaries are part of the joint taxation from the time of the consolidation in the Group’s financial statements and until the time when they are left out of the consolidation.

Thrige Holding A/S is the administrative company for the joint taxation, and as a consequence, it settles all group tax payments with the authorities.

The current Danish corporate income tax is allocated by payment of the joint taxation contribution between the jointly taxed companies relative to the taxable income. In this respect, companies with tax loss receive joint taxation contributions from companies which have used this loss to reduce their own tax profit.

The tax for the year, which consists of the current corporate tax for the year, the joint taxation contribution, and change in deferred tax – as a consequence of the reduction in the tax rate – is recognized in the Statement of Income with the portion relating to the profit for the year, and directly in the equity with the portion relating to items directly in the equity.

Balance SheetIntangibles

Goodwill

Goodwill is measured at cost less accumulated depreciation.

Goodwill is amortized on a straight-line basis over its estimated useful life.

The carrying amount of goodwill is assessed currently and written down in the Statement of Income to the

recoverable amount, if the carrying amount exceeds the expected future net income from the enterprise or activity to which the goodwill relates.

DevelopmentProjectsinProcess

Development projects in process comprise costs, salaries, and amortization directly or indirectly attributable to the development activities of the enterprise.

Development projects that are clearly defined and identifiable, where the technical utilization degree, sufficient resources, and potential future market or development opportunities in the Group are established, and where it is intended to produce, market, or use the project, are recognized as intangibles, provided that the cost can be measured reliably, and that there is sufficient assurance that future earnings can cover production costs, sales and administrative expenses, and development projects in process. Other development projects in process are recognized in the Statement of Income when incurred.

Capitalized development projects in process are recognized at cost less accumulated amortization or recoverable amount, if this is lower.

Following the completion of the development work, capitalized development projects in process are amortized concurrently with the sales of the developed products alternatively on a straight-line basis over the estimated useful life.

Development projects in process are written down to the recoverable amount, if this is lower than the carrying amount. Annual impairment tests are conducted relative to each development project.

Property,Plant,andEquipment

Land and buildings, plant and machinery, and fixtures and fittings, tools and equipment are measured at cost less accumulated depreciation.

Cost comprises the purchase price and

Accounting Policies

18 Annual Report 2007/08

any costs directly attributable to the acquisition until the date when the asset is available for use. The cost of self-constructed assets comprises direct and indirect costs of materials, components, subcontractors, and wages and salaries.

The cost of leases is stated at the lower value of fair value and the present value of the future lease payments. For the calculation of the net present value, the interest rate implicit in the lease or an approximation thereof is used as discount rate.

Depreciation is provided on a straight-line basis over the expected useful lives of the assets. The expected useful lives are as follows:

Buildings 10–50 yearsPlant and machinery 5–10 yearsFixtures and fittings, tools and equipment 3–7 years

Depreciation is recognized in the Statement of Income as production costs, distribution costs, and administrative expenses, respectively.

Property, plant, and equipment are written down to the recoverable amount, if this is lower than the carrying amount. In case of impairment loss, impairment tests are conducted relative to individual asset or groups of assets, respectively.

Gains and losses on the disposal of property, plant, and equipment are determined as the difference between the sales price less disposal costs, and the carrying amount at the date of disposal. The gains or losses are recognized in the Statement of Income as other operating income or other operating costs, respectively.

EquityInterestsinSubsidiaries

Equity interests in subsidiaries are measured according to the equity method.

Equity interests in subsidiaries are measured in the Balance Sheet at the proportionate share of the subsidiaries’ net asset values calculated in accordance with the Parent Company’s accounting

policies minus or plus unrealized intra-group profits and losses, and plus or minus the remaining value of positive goodwill or negative goodwill, respectively.

Subsidiaries with negative net asset values are measured at DKK 0 (nil), and any amounts owed by such subsidiaries are written down by the Parent Company’s share of the negative net asset value. Where the negative net asset value exceeds the amount owed, the remaining amount is recognized under allowances, if the Parent Company has a legal or constructive obligation to cover the subsidiary’s negative balance.

Net revaluation of equity interests in subsidiaries is transferred to the reserve for net revaluation according to the equity method under equity to the extent that the carrying amount exceeds cost.

On acquisition of subsidiaries, the purchase method is applied, cf. Consolidated Financial Statements above.

OwnStock

Own stock is valued according to the purchase price or a lower market value. An amount corresponding to the capitalized value is reserved under equity, named “Reserve for own stock”.

Inventories

Inventories are measured at cost in accordance with the FIFO method. Where the net realizable value is lower than cost, inventories are written down to this lower value. Cost comprises purchase price plus delivery costs.

Finished goods and work in process are measured at cost, comprising the cost of raw materials, consumables, direct wages and salaries, and indirect production costs. Indirect production costs comprise indirect materials and wages and salaries as well as maintenance and depreciation of production machinery, buildings, and equipment as well as factory administration and management. Borrowing costs are not recognized.

The net realizable value of inventories is calculated as the sales amount less costs of completion and costs necessary to make the sale, and is determined taking into account marketability, obsolescence, and development in expected sales price.

ContractWorkinProcess(long-term)

Contract work in process (long-term) is measured at the sales price of the work performed. The sales price is measured on the basis of the stage of completion at the Balance Sheet date and total expected income from the contract work. When the sales price of a contract cannot be measured reliably, the sales price is measured at the costs incurred or at net realizable value, if this is lower.

Individual contract work in process is recognized in the Balance Sheet under either receivables or payables, depending on the net amount of the sales price less prepayments. Sales costs and costs incurred in securing contracts are recognized in the Statement of Income when incurred.

Receivables

Receivables are measured at amortized cost. Write-down is made to meet expected losses.

PrepaymentsandDeferredCharges

Prepayments and deferred charges, recognized under assets, comprise costs incurred concerning subsequent fiscal years.

Equity–Dividends

Dividends are recognized as a liability at the date when they are adopted at the annual general meeting (time of announcement). The expected dividend payment for the year is disclosed as a separate item under equity.

CurrentTaxandDeferredTax

According to the joint taxation method, as the administrative company, Thrige Holding A/S assumes the liability to the

Accounting Policies

Annual Report 2007/08 19

tax authorities for the corporate tax of the Danish subsidiaries, concurrently with the subsidiaries paying their joint tax contribution.

Current tax payable and receivable is recognized in the Balance Sheet as tax calculated on the taxable income for the year, adjusted for tax on the taxable income of previous years, and for tax paid on account.

Payable and receivable joint tax contributions are recognized in the Balance Sheet under balances for the Parent Company.

Deferred tax is measured under the Balance Sheet liability method on all temporary differences between the carrying amount and the tax base of assets and liabilities. However, deferred tax is not recognized on temporary differences relative to amortization of goodwill disallowed for tax purposes and other items where temporary differences – excluding acquisitions – have arisen on the date of acquisition, without affecting the net income or taxable income.

Deferred tax assets, including the tax base of tax loss allowed for carryforward, are recognized under current assets at the expected value of their utilization, either as elimination in tax on future earnings or offsetting against deferred tax liabilities within the same legal tax entity and jurisdiction.

A readjustment of deferred tax relative to performed eliminations of unrealized, intra-group profit and loss will be carried out.

Deferred tax is measured according to the tax rules and at the tax rates applicable in the respective countries at the Balance Sheet date.

OtherAllowances

Allowances comprise anticipated costs related to restructuring provisions, etc. Allowances are recognized when, as a result of past events, the Group has a legal or a constructive obligation, and it is

probable that settlement of the obligation will result in an outflow of Group resources.

Financial Liabilities

Amounts owed to mortgage banks and credit institutions are recognized at the date of borrowing at the net proceeds received less transaction costs paid. In subsequent periods, the financial liabilities are measured at amortized cost, corresponding to the capitalized value using the effective interest rate. Accordingly, the difference between the proceeds and the nominal value is recognized in the Statement of Income over the term of the loan.

Financial liabilities also include the capitalized residual lease commitment.

Other liabilities, comprising trade payables as well as other payables, are measured at amortized cost.

Cash Flow StatementThe Cash Flow Statement shows the Group’s cash flows from operating, investing, and financing activities for the year, the year’s changes in cash and cash equivalents as well as the Group’s cash and cash equivalents at the beginning and end of the year.

CashFlowsfromOperatingActivities

Cash flows from operating activities are calculated as the Group’s share of the profit adjusted for non-cash operating items, changes in working capital, and corporate tax payable and receivable/joint taxation contribution.

CashFlowsfromInvestingActivities

Cash flows from investing activities comprise payments in connection with acquisitions and disposals of intangibles, property, plant, and equipment, and investments.

CashFlowsfromFinancingActivities

Cash flows from financing activities comprise payments to and from the Group’s stockholders and related costs as well as raising of loans, repayment of interest-bearing debt, and payment of dividends to stockholders.

CashandCashEquivalents

Cash and cash equivalents and credit institutions comprise cash reduced by current bank borrowings and short-term, marketable securities which are subject to an insignificant risk of changes in value.

Segment InformationGroup sales have been allocated according to business segments and geographical markets.

Accounting Policies

20 Annual Report 2007/08

The Board of Directors and the Executive Management have today discussed and adopted the annual report of Terma A/S for 2007/08.

The annual report has been prepared in accordance with the Danish Financial Statements Act. We consider the accounting policies applied to be appropriate. Accordingly, the annual report gives a true and fair view of the Group’s and Parent Company’s assets, liabilities, and financial position at

For Terma A/S Stockholders

We have audited the annual report of Terma A/S for the 1 March 2007–29 February 2008 fiscal year, to include Management’s Statement, Management’s Review, accounting policies, income statements, balance sheet, disclosures in the notes of the Group as well as the Parent Company, and the Group’s statement of cash flows. The annual report is prepared in accordance with the Danish Financial Statements Act.

Executive Management’s Responsibility for the Annual Report

The Executive Management is responsible for preparation and presentation of an annual report that gives a fair presentation in accordance with the Danish Financial Statements Act. This responsibility includes preparation, implementation, and maintenance of internal controls, which are relevant for the preparation and presentation of an annual report, which gives a fair presentation free from material errors, irrespective of such errors being due to fraud or misstatements, in addition to selection and adoption of appropriate accounting policies and provision of accounting estimates, deemed fair in the circumstances.

Independent Auditors’ Report

Executive Management’s Statement29 February 2008, as well as of the results of the Group’s and the Parent Company’s activities and the Group’s cash flows for the fiscal year 2007/08.

We recommend that the annual report be approved at the annual general meeting.

Lystrup,23May2008

Executive Management:

Jens Maaløe, President & CEO

Auditors’ Responsibility and Audit Performed

It is our responsibility to provide an opinion on the annual report based on audit performed. We have conducted our audit in accordance with the Danish auditing standards. These standards require that we live up to ethical requirements and plan and perform the audit with a view to achieving a high degree of certainty that the annual report is free from material misstatements.

Auditing includes actions to achieve audit evidence for the amounts and information disclosed in the annual report. The selected actions depend on the auditor’s assessment, to include assessment of risk of material misstatements in the annual report, irrespective of such errors being due to fraud or misstatements. In the risk assessment, the auditor considers internal controls relevant to the Company’s preparation and presentation of an annual report, which gives a fair presentation with a view to auditing actions appropriate in the circumstances, however, not to express an opinion on the effectiveness of the Company’s internal controls. Furthermore, auditing includes an opinion as to the Management’s adopted accounting policies being appropriate and its accounting estimates

fair, and an evaluation of the overall annual report presentation.

In our opinion, the audit evidence obtained is sufficient and qualified as a basis for our opinion.

Our audit does not give rise to qualifications.

Opinion

In our opinion, the annual report gives a fair presentation of the Group’s and the Parent Company’s assets, liabilities, and financial position at 29 February 2008 as well as the results of the Group’s and Parent Company’s activities and the Group’s cash flows for the 1 March 2007–29 February 2008 fiscal year, in accordance with the Danish Financial Statements Act.

Århus,23May2008

KPMG C.Jespersen Statsautoriseret Revisionsinteressentskab

Flemming BrokhattingenState-Authorized Public Accountant

Jes Lauritzen State-Authorized Public Accountant

Lars Marcher, Executive Vice President, CFO & Operations

Executive Management’s Statement and Independent Auditors’ Report

Board of Directors:

Svend-Aage Nielsen, Chairman

Holger Lavesen, Deputy Chairman

Henrik Stenbjerre

Peter Dyvig

Bo Laursen

Paul-Werner Johnsen

Annual Report 2007/08 21

Notes:Pages25and26

DKK thousand Consolidated Parent Company

Note 2007/08 2006/07 2007/08 2006/07

1, 2 Sales 1,038,548 1,004,664 939,287 904,348

3 Production costs (759,553) (751,063) (683,197) (679,026)

Gross profit 278,995 253,601 256,090 225,322

3 Distribution costs (94,502) (89,602) (85,586) (79,966)

3, 4 Administrative costs (70,016) (67,769) (55,869) (52,684)

Ordinary operating profit 114,477 96,230 114,635 92,672

5 Other operating income 414 174 479 174

5 Other operating costs 0 (676) 0 0

Operating profit 114,891 95,728 115,114 92,846

Profit in subsidiaries before tax - - 1,832 4,692

6 Financial income 1,111 476 1,754 218

6 Financial costs (20,368) (15,907) (23,066) (17,459)

Profit from ordinary activities before tax 95,634 80,297 95,634 80,297

7 Tax on profit from ordinary activities (11,644) (27,492) (11,644) (27,492)

Profit for the year 83,990 52,805 83,990 52,805

Proposed profit distribution

Proposed dividends 21,000 20,000 21,000 20,000

Reserve for net revaluation according to the equity method - - 7,253 (481)

Profit for the year carried forward 62,990 32,805 55,737 33,286

83,990 52,805 83,990 52,805

1 March–29 February

Statement of Income

22 Annual Report 2007/08

DKK thousand Consolidated Parent Company

Note 2008 2007 2008 2007

Assets

Non-current assets

Intangibles

Goodwill 1,207 7,618 1,207 6,592

Completed development projects 128,528 95,999 128,528 95,999

Development projects in process 48,149 21,940 48,149 21,940

8 177,884 125,557 177,884 124,531

Property, plant, and equipment

Land and buildings 189,990 190,841 189,990 190,841

Plant and machinery 37,658 42,763 35,591 39,704

Fixtures and fittings, tools and equipment 17,205 16,312 14,546 14,737

Payment on account and property, plant, and equipment under construction 8,014 4,090 8,014 4,090

9 252,867 254,006 248,141 249,372

Investments

10 Equity interests in subsidiaries - - 74,097 68,417

Own stock 75,188 75,188 75,188 75,188

75,188 75,188 149,285 143,605

Non-current assets, total 505,939 454,751 575,310 517,508

Current assets

Inventories

Raw materials and consumables 57,939 51,176 57,939 51,176

Work in process 114,346 79,040 112,237 72,274

On-account payments from customers (20,448) (8,696) (20,405) (8,696)

Prepayments to suppliers 1,701 1,963 1,701 1,963

153,538 123,483 151,472 116,717

Receivables

Trade accounts receivable 411,550 370,702 394,306 354,049

11 Contract work in process (long-term) 26,425 26,220 26,425 26,220

Amounts owed by subsidiaries - - 3,793 6,734

17 Corporate tax receivable 2,816 1,563 0 0

12 Other receivables 23,713 14,551 21,769 12,634

15 Deferred tax asset 8,175 0 0 0

13 Prepayments and deferred charges 7,456 6,581 7,456 6,581

480,135 419,617 453,749 406,218

Cash and cash equivalents 6,820 17,663 96 13,963

Current assets, total 640,493 560,763 605,317 536,898

Assets, total 1,146,432 1,015,514 1,180,627 1,054,406

Notes:Pages26,27,28,30,and31

Assets29 February

Balance Sheet

Annual Report 2007/08 23

DKK thousand Consolidated Parent Company

Note 2008 2007 2008 2007

Equity and liabilities

Equity

Capital stock 20,000 20,000 20,000 20,000

Reserve for own stock 75,188 75,188 75,188 75,188

Net revaluation according to the equity method - - 12,844 19,448

Profit carried forward 324,320 250,679 311,476 231,231

Proposed dividends 21,000 20,000 21,000 20,000

14 Equity, total 440,508 365,867 440,508 365,867

Allowances

15 Deferred tax 88,775 68,575 88,545 67,272

Allowances, total 88,775 68,575 88,545 67,272

Liabilities other than allowances

Long-term liabilities other than allowances

Employee bonds 3,361 0 3,361 0

Mortgage banks 184,411 144,020 184,411 144,020

16 187,772 144,020 187,772 144,020

Current liabilities other than allowances

Current portion of long-term liabilities 598 4,269 598 4,269

Credit institutions 55,411 125,738 55,411 125,738

Prepayments from customers 120,159 101,003 119,439 98,131

Trade accounts payable 67,556 38,201 65,480 36,820

Amounts owed to Parent Company 8 16 8 16

Amounts owed to subsidiaries - - 56,201 67,528

17 Corporate tax payable 0 407 0 0

18 Other payables 185,645 167,418 166,665 144,745

429,377 437,052 463,802 477,247

Liabilities other than allowances, total 617,149 581,072 651,574 621,267

Equity and liabilities, total 1,146,432 1,015,514 1,180,627 1,054,406

19 Contingent liabilities and security

20 Related parties

Notes:Pages29,30,and31

Equity and Liabilities29 February

Balance Sheet

24 Annual Report 2007/08

DKK thousand Consolidated

2007/08 2006/07

Profit from ordinary activities before tax 95,634 80,297

Adjustments:

Depreciation, etc. 34,959 36,403

Amortization of development licenses previously transferred to contract work in process (long-term) 20,557 27,737

Financial items 19,257 15,431

74,773 79,571

Changes in working capital:

Inventories (19,393) (14,014)

Receivables (37,012) (56,015)

Prepayments received 19,156 13,189

Trade accounts payable and other payables 47,574 11,162

10,325 (45,678)

Cash generated from operations (operating activities) before financial items 180,732 114,190

Financial items (19,257) (15,431)

Cash flows from operations (ordinary activities) 161,475 98,759

Corporate tax paid (4,707) (5,047)

Cash flows from operating activities 156,768 93,712

Capitalized development costs (89,957) (50,803)

Acquisition of property, land, and equipment (28,214) (32,914)

Disposal of property, land, and equipment 806 417

Cash flows for investing activities (117,365) (83,300)

Changes in long-term liabilities 40,081 (22,136)

Dividends paid (20,000) (35,000)

Cash flows from financing activities 20,081 (57,136)

Changes in cash and cash equivalents 59,484 (46,724)

Cash and cash equivalents and credit institutions at 1 March (108,075) (61,351)

Cash and cash equivalents and credit institutions at 29 February (48,591) (108,075)

The Cash Flow Statement cannot be directly derived from the Balance Sheet and the Statement of Income.

1 March–29 February

Cash Flow Statement

Annual Report 2007/08 25

Notes

Non-defense

Defense

Denmark

Outside Denmark

2007/08

63.11 %

36.89 %

2007/08

19.43 %

80.57 %

2006/07

23.74 %

76.26 %

2006/07

35.25 %

64.74 %

1. Segment information - Sales

2. Sales

Consolidated Parent Company

DKK thousand 2007/08 2006/07 2007/08 2006/07

Goods and services 751,230 789,423 651,969 689,107

Contract work in process (long-term) 287,318 215,241 287,318 215,241

1,038,548 1,004,664 939,287 904,348

3. Costs

Parent Company Board of Directors emoluments and remuneration of the Executive Management 3,967 3,946 3,967 3,946

Wages and salaries 475,574 427,973 424,292 375,260

Pensions and other social security costs 25,553 22,963 19,333 16,226

Other staff costs 3,799 3,111 3,566 2,594

508,893 457,993 451,158 398,026

Average number of full-time employees 1,020 965 924 863

4.

Fees paid to auditors appointed at the annual general meeting

Total fees KPMG 1,840 1,896 1,465 1,428

Portion relating to other non-audit services KPMG 1,096 904 738 622

Total fees other auditors 590 550 0 0

Portion relating to other non-audit services other auditors 590 550 0 0

5. Other operating income and costs

Lease income 159 155 159 155

Gain on disposal of non-current assets 255 19 320 19

Other operating income, total 414 174 479 174

Loss on disposal of non-current assets 0 676 0 0

Other operating costs, total 0 676 0 0

6. Financial income and costs

Interest income from subsidiaries - - 647 382

Interest costs to subsidiaries - - 2,785 2,008

26 Annual Report 2007/08

Notes

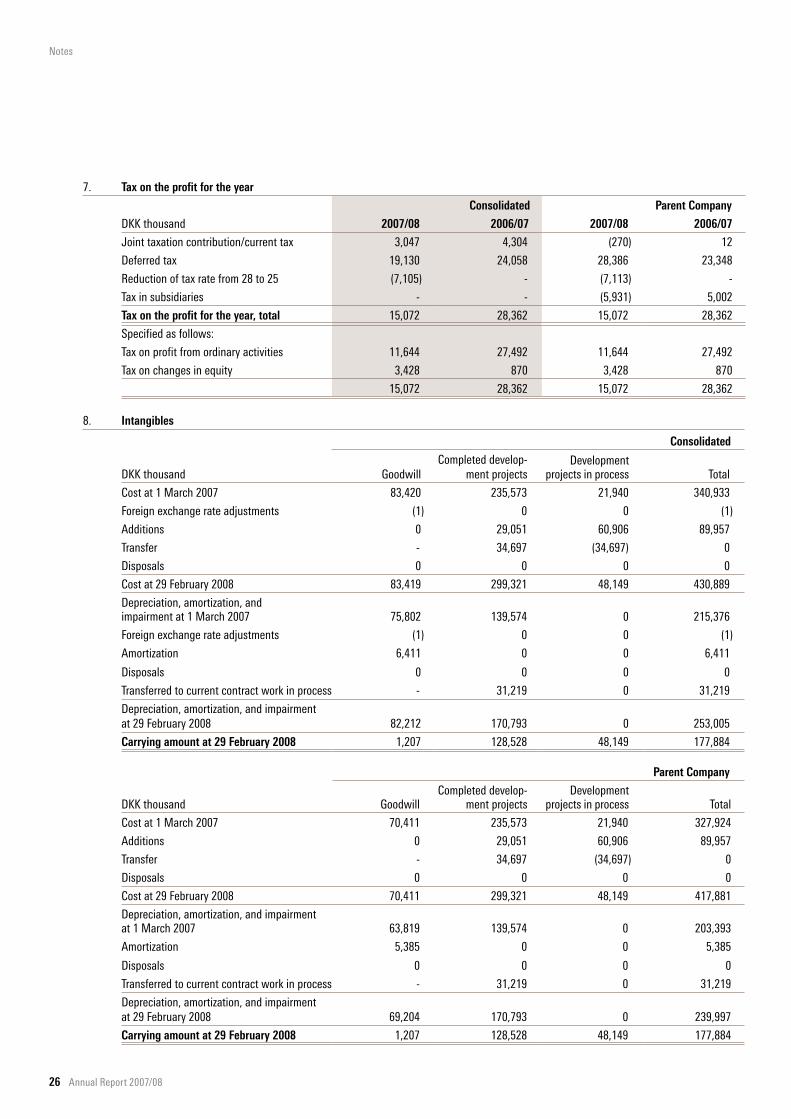

7. Tax on the profit for the year

Consolidated Parent Company

DKK thousand 2007/08 2006/07 2007/08 2006/07

Joint taxation contribution/current tax 3,047 4,304 (270) 12

Deferred tax 19,130 24,058 28,386 23,348

Reduction of tax rate from 28 to 25 (7,105) - (7,113) -

Tax in subsidiaries - - (5,931) 5,002

Tax on the profit for the year, total 15,072 28,362 15,072 28,362

Specified as follows:

Tax on profit from ordinary activities 11,644 27,492 11,644 27,492

Tax on changes in equity 3,428 870 3,428 870

15,072 28,362 15,072 28,362

8. Intangibles

Consolidated

DKK thousand GoodwillCompleted develop-

ment projectsDevelopment

projects in process Total

Cost at 1 March 2007 83,420 235,573 21,940 340,933

Foreign exchange rate adjustments (1) 0 0 (1)

Additions 0 29,051 60,906 89,957

Transfer - 34,697 (34,697) 0

Disposals 0 0 0 0

Cost at 29 February 2008 83,419 299,321 48,149 430,889

Depreciation, amortization, and impairment at 1 March 2007 75,802 139,574 0 215,376

Foreign exchange rate adjustments (1) 0 0 (1)

Amortization 6,411 0 0 6,411

Disposals 0 0 0 0

Transferred to current contract work in process - 31,219 0 31,219

Depreciation, amortization, and impairment at 29 February 2008 82,212 170,793 0 253,005

Carrying amount at 29 February 2008 1,207 128,528 48,149 177,884

Parent Company

DKK thousand GoodwillCompleted develop-

ment projectsDevelopment

projects in process Total

Cost at 1 March 2007 70,411 235,573 21,940 327,924

Additions 0 29,051 60,906 89,957

Transfer - 34,697 (34,697) 0

Disposals 0 0 0 0

Cost at 29 February 2008 70,411 299,321 48,149 417,881

Depreciation, amortization, and impairment at 1 March 2007 63,819 139,574 0 203,393

Amortization 5,385 0 0 5,385

Disposals 0 0 0 0

Transferred to current contract work in process - 31,219 0 31,219

Depreciation, amortization, and impairment at 29 February 2008 69,204 170,793 0 239,997

Carrying amount at 29 February 2008 1,207 128,528 48,149 177,884

Annual Report 2007/08 27

9. Property, plant, and equipment

Consolidated

DKK thousandLand andbuildings

Plant andmachinery

Fixtures andfittings, tools

and equipment

Payment on account and

property, plant, and equipment

under construction Total

Cost at 1 March 2007 316,736 152,417 84,596 4,090 557,839

Foreign exchange rate adjustments 0 (509) (122) 0 (631)

Additions 6,032 8,769 9,489 8,014 32,304

Disposals 0 (4,796) (4,634) (4,090) (13,520)

Cost at 29 February 2008 322,768 155,881 89,329 8,014 575,992

Depreciation, amortization, and impairment at 1 March 2007 125,895 109,654 68,284 0 303,833

Foreign exchange rate adjustments 0 (115) (17) 0 (132)

Depreciation, amortization, and impairment 6,883 12,027 8,393 0 27,303

Disposals 0 (3,343) (4,536) 0 (7,879)

Depreciation, amortization, and impairment at 29 February 2008 132,778 118,223 72,124 0 323,125

Carrying amount at 29 February 2008 189,990 37,658 17,205 8,014 252,867

Depreciated over 10–50 years 5–10 years 3–7 years

At 1 October 2007, the total official annual valuation of Danish properties with a carrying amount of DKK 189,990 thousand amounts to DKK 244,450 thousand. Additions during the year of DKK 6,032 thousand are not included in the annual adjustments of the official property valuations at 1 October 2007.

Parent Company

DKK thousandLand andbuildings

Plant andmachinery

Fixtures andfittings, tools

and equipment

Payment on account and

property, plant, and equipment

under construction Total

Cost at 1 March 2007 238,437 148,470 79,140 4,090 470,137

Additions 6,032 8,703 7,780 8,014 30,529

Disposals 0 (4,796) (4,108) (4,090) (12,994)

Cost at 29 February 2008 244,469 152,377 82,812 8,014 487,672

Depreciation, amortization, and impairment at 1 March 2007 47,596 108,766 64,403 0 220,765

Depreciation, amortization, and impairment 6,883 11,364 7,949 0 26,196

Disposals 0 (3,344) (4,086) 0 (7,430)

Depreciation, amortization, and impairment at 29 February 2008 54,479 116,786 68,266 0 239,531

Carrying amount at 29 February 2008 189,990 35,591 14,546 8,014 248,141

Depreciated over 10–50 years 5–10 years 3–7 years

At 1 October 2007, the total official annual valuation of Danish properties with a carrying amount of DKK 189,990 thousand amounts to DKK 244,450 thousand. Additions during the year of DKK 6,032 thousand are not included in the annual adjustments of the official property valuations at 1 October 2007.

Notes

28 Annual Report 2007/08

11. Contract work in process (long-term)

Consolidated Parent Company

DKK thousand 2008 2007 2008 2007

Contract work in process (long-term) 55,024 47,110 55,024 47,110

Invoiced on account (28,599) (20,890) (28,599) (20,890)

Contract work in process (long-term), net, at 29 February 26,425 26,220 26,425 26,220

12. Other receivables

Insurance 3,377 7,919 3,377 7,919

Hedging instruments 17,114 3,036 17,114 3,036

Other 3,222 3,596 1,278 1,679

Other receivables at 29 February 23,713 14,551 21,769 12,634

13. Prepayments and deferred charges

Deposits 651 590 651 590

License fees 1,153 1,881 1,153 1,881

Other 5,652 4,110 5,652 4,110

Prepayments and deferred charges at 29 February 7,456 6,581 7,456 6,581

Name Registered office Ownership Capital stock

Terma Ejendomme Skive A/S Århus, Denmark 100 % DKK 1,150 thousand

Terma GmbH Darmstadt, Germany 100 % EUR 51 thousand

Terma B.V. Leiden, The Netherlands 100 % EUR 750 thousand

Terma S.r.l. Besozzo, Italy 100 % EUR 10 thousand

Terma North America Inc. Delaware, USA 100 % USD 150 thousand

10. Equity interest in subsidiaries

DKK thousand

Cost at 1 March 2007 39,026

Disposals during the year 0

Additions during the year 12,283

Cost at 29 February 2008 51,309

Net revaluations at 1 March 2007 29,391

Foreign exchange rate adjustments (509)

Dividends paid (13,857)

Profit for the year 7,763

Net revaluations at 29 February 2008 22,788

Carrying amount at 29 February 2008 74,097

Notes

Annual Report 2007/08 29

14. Equity

Consolidated

DKK thousand 2007/08 2006/07

Equity at 1 March 365,867 345,828