term for our times todd ewing vice president, term life and direct marketing

Post on 21-Dec-2015

216 views

TRANSCRIPT

TERM FOR OUR TIMES

Todd EwingVice President, Term Life

and Direct Marketing

For producer use only. Not for distribution to the public.

Increase Your Term Sales Profitability

Reduce Expenses & Improve Placement Ratios

– Tools & Resources

– Programs

– Underwriting & New Business Processing

Expand Term Market

– Sales ideas for new markets

– Sales ideas for larger cases

For producer use only. Not for distribution to the public.

Reduce Term Expenses

Transamerica Opportunity Program (TOP 25)

Easily add or extend existing coverage with an additional 25-year term up to $1M coverage

No medical exam*

More than 50 eligible carriers

Must have been fully underwritten, with blood work and issued Standard or better

* This is not a Guaranteed Issue program. Qualification for coverage depends on the answers to health questions set forth in the new application. Subject to underwriting approval. Underwriting includes Medical Information Bureau (MIB) screening, nonmedical, face page of previously issued term policy, and additional requirements which may be imposed based on information from MIB. Program is subject to withdrawal at any time without notice by the Company.

For producer use only. Not for distribution to the public. 4

TOP 25 Program

Issue Ages: 18 - 55 Policy Minimum: $100,000 Policy Maximum depends on rolling window from the

original policy date to the application date:

Multiple policies may be issued up to the designated maximum face amount, however, new coverage under TOP may never be greater than $1 million in total per individual life per lifetime. Additionally, coverage maximums are limited to normal Company maximum retention.

If issued within:Available Maximum

Face Amount:

One Year $1,000,000

Three Years $750,000

Five Years $500,000

For producer use only. Not for distribution to the public.

TOP 25 In-Force Marketing

5

www.tatransact.com

For producer use only. Not for distribution to the public.

TOP 25 Policy Owner Report

6

Policy Number

Qualified for $1M if app is dated prior to:

Qualified for $750 if app

is dated prior to:

Qualified for $500K if app is

dated prior OWNER NAMEOWNER

ADDRESS1 OWNER CITY OWNER STATE

30492734 11/6/2011 11/6/2013 Abby Landers 2045 Lawndale St Herndon PA

39486293 8/19/2010 8/19/2012 8/19/2014 Kelly Valentina 38495 Palo Alto DriveVienna NC

40937384 7/16/2011 Shawn Marlow 1963 Gelmund Way Elliston GA

48237692 2/7/2012 2/7/2014 Bobby Sabre P.O. Box 2004 Springfield MO

49283740 10/14/2010 10/14/2012 10/14/2014 Reggie Lopez 837 N. 10th St Rolling Hills OR

41293847 7/24/2010 7/24/2010 7/24/2010 Orange Studio Inc.22904 Orchid Ln Pasadena TX

40589575 9/1/2011 Tommy Kannin 1805 Main St Orlando ME

43893920 11/13/2010 11/13/2012 11/13/2014 Chad Dillon 34 Reede Rd Lansing AK

43957866 8/28/2010 8/28/2012 8/28/2014 Harper Lee 3239 Oakdale Blvd Billings DE

49998221 6/22/2011 Jennifer Gill 392 Cleveland Ave Honolulu NY

For producer use only. Not for distribution to the public.

TOP 25 Policy Owner Marketing

Easily mail merge letters to policy owners

7

For producer use only. Not for distribution to the public.

Other TOP 25 Tools

For Producers TOP 25 Tool kit

Brainshark Tutorial

For Consumers Brochure

Pre-Approach Letter

8

Tools Available on TransACT (www.tatransact.com)

For producer use only. Not for distribution to the public. 9

iGO Increases Profitability

Over 80 Transamerica Agencies Use iGO

Functionality• Producers submit business online & “In Good Order” for all term products• eApplication, eSignature and eSubmission• Ability to print and complete• Online Go/No-Go functionality for the Agency

Benefits• Reduces errors on apps• Avoids duplicate entries• Cycle times reduced for app processing• Eliminates the need to FastStart cases manually

For producer use only. Not for distribution to the public.

iGO Increases Profitability

10

Reduces errors and missing information,

so apps are submitted “In Good

Order”

For producer use only. Not for distribution to the public.

iGO Increases Profitability

11

eApplication, eSignature and

eSubmission capabilities reduce

cycle times up to 14 days!

For producer use only. Not for distribution to the public.

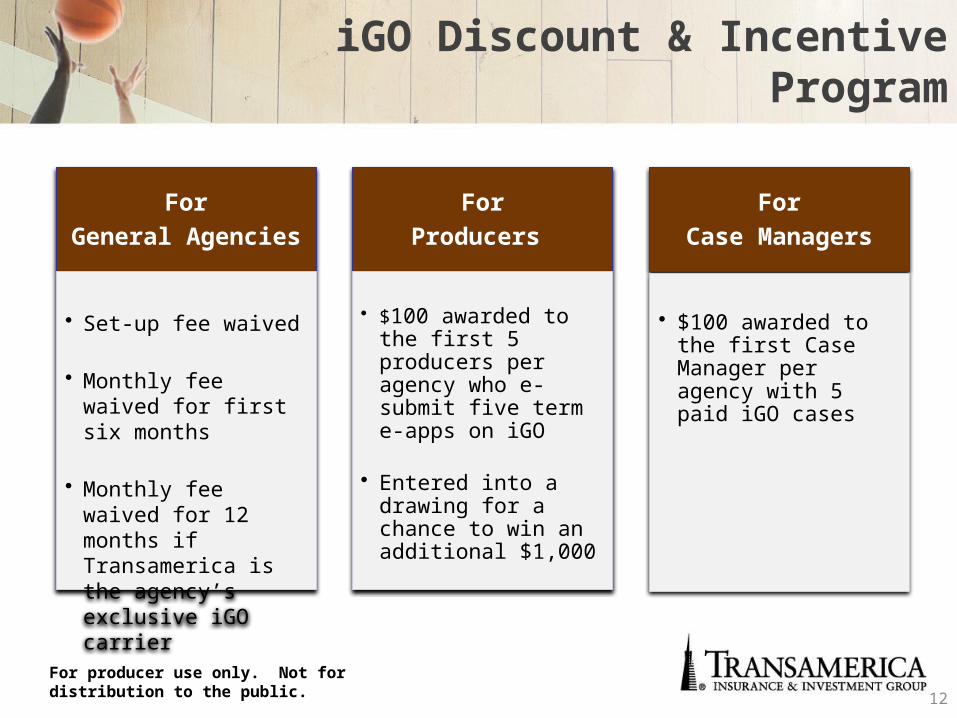

iGO Discount & Incentive Program

12

For

General Agencies

• Set-up fee waived

• Monthly fee waived for first six months

• Monthly fee waived for 12 months if Transamerica is the agency’s exclusive iGO carrier

For

Producers

• $100 awarded to the first 5 producers per agency who e-submit five term e-apps on iGO

• Entered into a drawing for a chance to win an additional $1,000

For

Case Managers

• $100 awarded to the first Case Manager per agency with 5 paid iGO cases

For producer use only. Not for distribution to the public.

Increase Placement Ratios

New “Case Manager” structure: Reduces cycle times Increases management of pending business Scalable for spikes in growth

13

Case Coordinators

Home OfficeCase Manager

Home OfficeAsst. Case Manager

For producer use only. Not for distribution to the public.

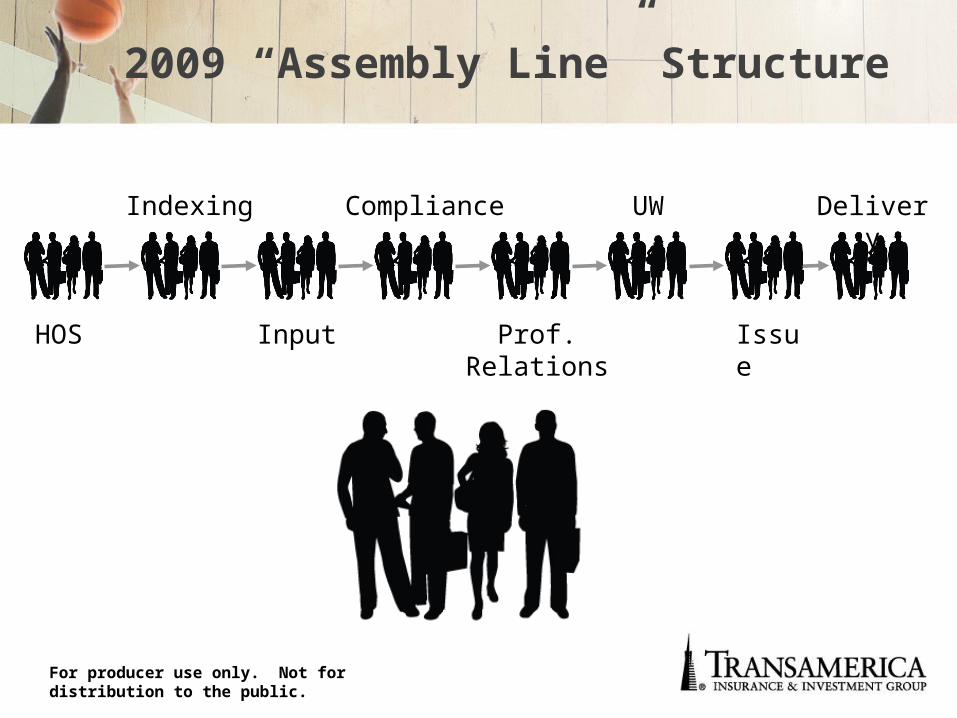

2009 “Assembly Line” Structure

HOS

Indexing

Input Prof. Relations

DeliveryUW

Issue

Compliance

For producer use only. Not for distribution to the public.

Your Home Office Case Coordinator

AGENCY CASE MANAGER

Owns case from submit to paid

Handles all case input, manages requirements, policy issue, delivery requirements and paying cases

Key link to underwriters

Communicates policy status to you

Troubleshoots to keep cases moving

UnderwritersCase Coordinator

For producer use only. Not for distribution to the public.

Your Home Office Case Manager

Your key contact for any issues

Proactive management of all pending business

Monitors life cycle of a case and troubleshoots to keeps all new business moving

Case Manager Assistant Case Manager

For producer use only. Not for distribution to the public.

Key Benefits

Increased customer focus

Accountability and ownership for each case

Single point of contact and correspondence

More effective and proactive communication on policy status

For producer use only. Not for distribution to the public.

Key Benefits

Reduced handoffs / increased coordination between New Business & Underwriting

Maximizes underwriters focus on underwriting

Thorough management of pending business

Reduces cycle times and improve placement ratios

Scalable for spikes and growth

For producer use only. Not for distribution to the public.

Increase Placement Ratios

Large number of recent underwriting enhancements including:

Improved family history guidelines

Preferred status for asthmatics

MCAS for cognitive testing

Improvements to low-substandard risk offers

Preferred status opportunity for certain cancers

19

For producer use only. Not for distribution to the public.

Enhanced Underwriting“Making Life A Little Easier”

For producer use only. Not for distribution to the public.

Expand Term Market

Older Issue Ages Discounts for Laddering policies Advanced Premium Discounts* Return of Premium Option on 20 & 30 year term Reverse Quote Tool Income Protection Option

*Interest credited by Transamerica to premium paid under the Advanced Premium Agreement is taxable and will be reported to the IRS in a Form 1099-INT if in excess of $10.

For producer use only. Not for distribution to the public.

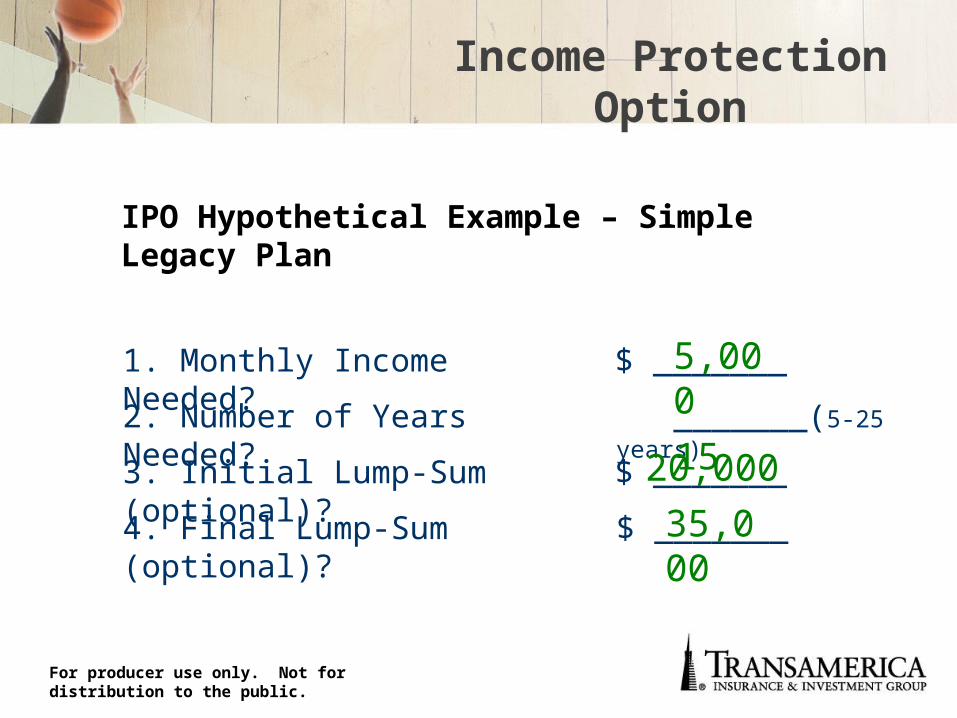

3. Initial Lump-Sum (optional)? $ _______

1. Monthly Income Needed? $ _______

2. Number of Years Needed? _______(5-25 years)

4. Final Lump-Sum (optional)? $ _______

1520,000

35,000

5,000

IPO Hypothetical Example – Simple Legacy Plan

Income Protection Option

For producer use only. Not for distribution to the public.

Guaranteed Monthly Income StreamInitial Lump Sum

Back EndLump Sum

Guaranteed Monthly Income StreamInitial

Lump SumFinal

Lump Sum

$$$$

$$

IPO Hypothetical Example

Mortgage Payments

Medical Bills

Wedding

$5,000 for 15 yearsHouse Down

Payment

College Tuition

$20,000 initialRetirement

Living Expenses

$35,000 final

Income Protection Option

(Multiple Beneficiary Feature For Term IPO Coming soon!)

For producer use only. Not for distribution to the public. 24

Income Protection Option (IPO)

Front end lump sum

Monthly Income StreamBack end lump sum

$10,000 minimum $10,000 minimum5 – 25 years / $100 minimum

Available at no additional cost

Can be modified prior to the death of the insured

Income Protection Option

For producer use only. Not for distribution to the public.

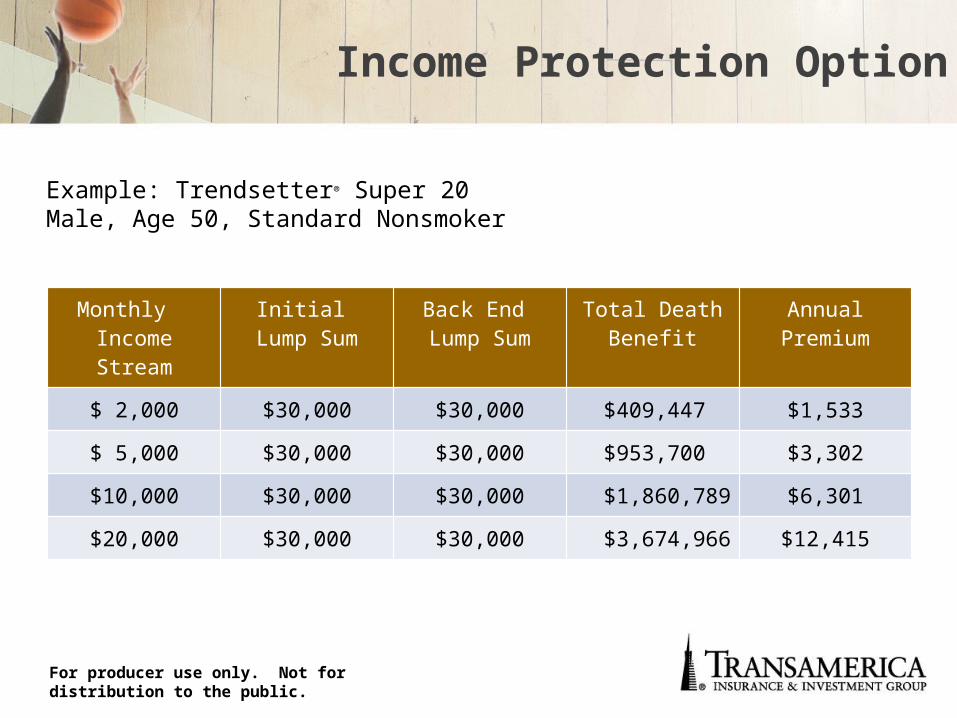

Income Protection Option

Monthly Income Stream

Initial Lump Sum

Back End Lump Sum

Total Death Benefit

Annual Premium

$ 2,000 $30,000 $30,000 $409,447 $1,533

$ 5,000 $30,000 $30,000 $953,700 $3,302

$10,000 $30,000 $30,000 $1,860,789 $6,301

$20,000 $30,000 $30,000 $3,674,966 $12,415

Example: Trendsetter® Super 20Male, Age 50, Standard Nonsmoker

For producer use only. Not for distribution to the public.

Tax-Equivalent Yield

Return of Premium (ROP) rider available on Trendsetter® Super 20 & Super 30

100% guaranteed return of premium at the end of level premium period*

Income Tax Free

28% Tax Bracket

30% Tax Bracket

20-Year ROP rider

3.5% 4.9% 5.0%

30-Year ROP rider

4.25% 5.9% 6.1%

Tax-Equivalent Yield

*Excludes premiums for any substandards and other riders.

For producer use only. Not for distribution to the public. 27

Expand Term Market: Older Issue Ages

Asset Repair Strategy

Client Profile: Ages 60-78

Concerns– Significant Portfolio Losses from Market Volatility

– Asset Gap

– Minimize Potential Family Conflict

For producer use only. Not for distribution to the public. 28

Potential Solutions Use a portion of assets for retirement

Leave a lesser amount to children and grandchildren

Use term insurance to “repair” assets and provide a legacy

Asset Repair Strategy

For producer use only. Not for distribution to the public. 29

How many years does it take to reset $500,000 back to $1,000,000?

$1,296,871

$1,079,462

$814,447

Account Balance in

10 years

$3,363,750

$2,330,479

$1,326,649

Account Balance in

20 years

$805,255

$734,664

$638,141

Account Balance in

5 years

$500,00010%

$500,0008%

$500,0005%

Current Balance

Previous Total Assets: $1,000,000

Current Total Assets: $500,000

$2,088,624

$1,586,085

$1,039,464

Account Balance in

15 years

Asset Repair Strategy

For producer use only. Not for distribution to the public. 30

$1,000,000 assets formerly earmarked for children and grandchildren

Asset value now $500,000

Policy Review reveals he was fully underwritten for a policy earlier this year but he lapsed his policy due to cost.

Mr. Recover applies for a Trendsetter® Super 25 policy

Annual premium = $9,685

No medical exams with TOP 25 program

Frees assets to use during retirement

Able to leave $500,000 to children and grandchildren

Previous Total Assets: $1,000,000

Current Total Assets: $ 500,000

Mr. Will Recover, age 65, Nonsmoker

Asset Repair Using TOP 25

For producer use only. Not for distribution to the public.

The Blended Family Market

Blended families outnumber traditional families in the United States1

65% of remarriages involve children from the prior marriage and from stepfamilies2

One of three Americans is now a stepparent, a stepchild, a stepsibling, or some other member of a blended family1

More than half of Americans today have been, are now or will eventually be in one or more step situations during their lives1

31

1U.S. Census conducted in 2000

2U.S. Census conducted in 1990

For producer use only. Not for distribution to the public.

The Blended Family

Families where husband and/or wife bring children and assets from a previous relationship

32

ChildChild

2nd Spouse

2nd Spouse

ChildChildChildChild

SpouseSpouse

For producer use only. Not for distribution to the public.

The Blended Family

33

Pay for college education in the event of his death Minimize conflict among family members

Mike’s Concerns:

MikeMike CarolCarol

From Previous Marriage

JanJan

Cindy Cindy

MarshaMarsha

From Current Marriage

For producer use only. Not for distribution to the public. 34

MikeAge 47MikeAge 47

CarolAge 40CarolAge 40Jan

Age 7Jan

Age 7

CindyAge 2CindyAge 2

MarshaAge 10MarshaAge 10

$1,553

$890

$420

$243

Annual Premiums

with Laddering*

$29,565

$18,800

$7,515

$3,250

Cumulative Premiums

without Laddering*

Total Savings: $3,035

$1,766

$940

$501

$325

Annual Premiums

without Laddering*

$26,530

$17,800

Cumulative Premiums

with Laddering*

$6,300

$2,430

$1,050,000Total:

$500,000

$300,000

$250,000

Death Benefit

20 yearsCindy

Term Duration

Beneficiary

15 years

10 years

Jan

Marsha

* Based on Male, age 47 Preferred Nonsmoker

The Blended Family

For producer use only. Not for distribution to the public. 35

College graduates today are entering one of the worst entry-level job markets since the dot-com bust at the start of the decade1

Four in 10 adults age 60 or older are giving money to their adult children1

55% of men and 48% of women ages 18-24 live with their parents2

1 2005 Pew Research Study

2 2007 US Census

The “Empty Nest” turns into a “Crowded Nest”

Boomerang Kids

For producer use only. Not for distribution to the public. 36

Emily(age 26)

Grandma(age 75)

Oops!(age 3)

Greg (age 22)

Bob (age 50)

Laddering with Extended Issue Ages

• 15-year term on Grandma to benefit Bob• 15-year term on Grandma to benefit

grandchildren

Laddering and TOP 25

• 30-year term on Bob to benefit Baby Oops!• 25-year term on Bob to benefit Greg• 20-year term on Bob to benefit Emily

Grandparent Gifting Strategy

For producer use only. Not for distribution to the public.

Transamerica vs. Industry

Source: LIMRA 2009 Q2 Life Insurance Survey

Average Case Size Premium Per Case

$466,837

$433,174$1,375

$933

TransamericaIndustry

TransamericaIndustry

Term Comparison

For producer use only. Not for distribution to the public.

Term Year-in-Review

Increased Rates

IncreasedPolicy Fees Products Decreased

Comp

Transamerica Less than 3% AddedROP Riders

AIG withdrew & modified

Banner

Genworth withdrew ING Lincoln Nat’l modified Prudential West Coast

38

For producer use only. Not for distribution to the public.

Age 50 Age 60

American General $3,364 West Coast Life $9,490

Transamerica $3,400 American General $9,494

ING ReliaStar $3,425 Transamerica $9,550

Lincoln National $3,445 Lincoln National $10,025

West Coast Life $3,460 ING ReliaStar $10,245

Banner $3,575 Genworth $10,765

Genworth $3,624 Banner $10,905

Trendsetter® Super 20

Annual Premiums: Male, Standard Nonsmoker, $1 Million

Premiums effective as of 12/15/09.

For producer use only. Not for distribution to the public.

Next Tip-Off to Sales

Save the Date: April 13, 2010

Is Premium Finance Dead?

Featuring:

David EisenbergDirector, Premium Finance

For producer use only. Not for distribution to the public. 41

Comparisons in this presentation are not a comprehensive analysis and do not account for possible advantages or disadvantages of the policies compared. Competitors' premiums have been obtained from publicly available sources and are believed to be accurate as of December 2009.

Trendsetter® Super Series (Policy Form Nos. 1-322 11-107, 1-306 11-107, 1-305 11-107, 1-304 11-107, 1-303 11-107, 1-334 11-107, 1-230 11-106; and Policy Form Nos. 3-322 38-109, 3-306 38-109, 3-305 38-109, 3-304 38-109, 3-303 38-109, and 3-334 38-109 in New York) are term life insurance policies issued by Transamerica Life Insurance Company, Cedar Rapids, IA 52499 and Transamerica Financial Life Insurance Company, Purchase, NY 10577. Premiums increase annually for Trendsetter Super YRT, and beginning in year 11 for the 10-year policy, in year 16 for the 15-year policy, in year 21 for the 20-year policy, in year 26 for the 25-year policy, and in year 31 for the 30-year policy.

Policy forms and numbers may vary, and these policies may not be available in all jurisdictions. Insurance eligibility and premiums are subject to underwriting.

Transamerica Financial Life Insurance Company is authorized to conduct business in New York. Transamerica Life Insurance Company is authorized to conduct business in all other states.

OLA 2055C 0310