ted schroeder agricultural economist kansas state university montana livestock forum and nutrition...

TRANSCRIPT

Ted Schroeder

Agricultural Economist

Kansas State University

Montana Livestock Forum and Nutrition Conference

Bozeman, MT – April 21, 2009

Build Consumer Beef Demand:Build Consumer Beef Demand:Prescription for ProsperityPrescription for Prosperity

www.NAIBER.org

Ted’s ThesisTed’s Thesis

Prosperity of cattle & beef industry is driven by consumer demand

All new $ that flow into your industry originate from consumers

Ted’s ThesisTed’s Thesis

Prosperity of cattle & beef industry is driven by consumer demand

All new $ that flow into your industry originate from consumers

Yet, we continuously make policy, production, and marketing decisions that fail to appreciate this well documented fact!

Retail Choice Domestic Beef Demand IndexAnnual, 1980-2008

88 86 8379 76

70 69 66 65 63 59 58 56 55 53 51 50 52 54 56 55 5963 61 57 58 56

94100

0102030405060708090100

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

Year

Index

(

%

)

Source: USDA, Dept. of Commerce & J. Mintert, K-State Dept. of Ag. Economics Price Deflated By CPI, 1980 =100 for Choice Domestic Beef Demand Index

US Beef Demand, 1980-2008US Beef Demand, 1980-2008

US US KS KS DodgeTotal Beef Fed 7-800 lb CityBeef Demand Cattle Steer Corn

Supply Index Price Price PriceYear (bil. lbs) ($/cwt) ($/cwt) ($/bu)1998 28.9 50 61.84 76.15 2.26

2004 28.8 63 84.52 106.51 2.69

Does Consumer Demand Affect Producer?

$10/cwt of fed, $14/cwt of feeder price increase directly attributable to retail beef demand increase

- John Marsh, Montana State University

1. Safety assured2. Tender3. Flavorful4. Consistently high quality5. Healthy & Nutritious (Nutraceutical)6. Environmentally friendly production7. Animal friendly production8. Locally produced 9. Convenient to prepare10. Competitively priced

What Consumers Collectively Demand

Experience/CredenceAttributes

This means: explicit labeling and brands are essential to convey and assure information

Economy and Beef DemandEconomy and Beef Demand

Personal Disposable Income & Consumption Expenditures, Quarterly at Annual Rate, Seasonally Adjusted,

1982-2008

0

2

4

6

8

10

12

82.1 84.1 86.1 88.1 90.1 92.1 94.1 96.1 98.1 00.1 02.1 04.1 06.1 08.1

Year & Quarter

Trln $

Declining Consumer Income Causes Spending to Decline

Source: Bureau of Economic Analysis

Personal Consumption Expenditures

Personal Disposable Income

Consumer Saving Begins to Ramp Up

Personal Savings as % of Disposable Personal IncomeQuarterly, 1982-2009

-2024681012

82.1 84.1 86.1 88.1 90.1 92.1 94.1 96.1 98.1 00.1 02.1 04.1 06.1 08.1Year & Quarter

Percent

Source: Bureau of Economic Analysis

Consumers Pull Back on Food PurchasesConsumers Pull Back on Food Purchases

Percentage Change in Personal Consumption Exenditures for Food, Annualized Rate, Seasonally Adjusted, 1990-2008

-3

-2

-1

0

1

2

3

1990.1 1992.1 1994.1 1996.1 1998.1 2000.1 2002.1 2004.1 2006.1 2008.1

Date (YR-Qtr)

Per

cen

tag

e C

han

ge

Consumers Are Trading DownConsumers Are Trading Down

Whole Foods

Weekly Value of $10,000 Invested on Jan 2, 2008 in Selected Food Companies, Jan. 2008 - April 2009

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

1/2/2008 4/2/2008 7/2/2008 10/2/2008 1/2/2009 4/2/2009

Date

Va

lue

of

$10

,000

In

vest

ed

McDonalds

Dow Jones Industrial

Whole Foods

Ruth's Hospitality

Food Safety, Health, Nutrition,Food Safety, Health, Nutrition,Product Development, & QualityProduct Development, & Quality

Atkins Diet Boosted Beef DemandBut Atkins Fad Is Over

Net Articles Published Referencing Atkins DietPositive Minus Negative, U.S. Newspapers, Quarterly, 1982-2007

-300-200-100

0100200300400500

82.1 84.1 86.1 88.1 90.1 92.1 94.1 96.1 98.1 00.1 02.1 04.1 06.1

Year & Quarter

Articles

Source: LexisNexis

Medical Journal Info. on Heart DiseasePeaked, Still Having a Negative Effect

Articles Published Referencing Heart Disease & DietMedical Journals, Quarterly, 1982-2007

0

20

40

60

80

100

82.1 84.1 86.1 88.1 90.1 92.1 94.1 96.1 98.1 00.1 02.1 04.1 06.1

Year & Quarter

Articles

Source: Medline

1982-2004 contributed a 9% drop in beef demand

Medical Journal Information

“Over 10 years, eating the equivalent of a quarter-pound hamburger daily gave men in the study a 22% higher risk of dying of cancer and a 27% higher risk of dying of heart disease. That's compared to those who ate the least red meat, just 5 ounces per week.”

Source: Sinha, et al. Arch. Intern. Medicine, March 2009

What the press didn’t say….

Men who eat most red meat study found:A - have 26% higher risk of dying of injury and sudden deathB - have 58% higher risk of dying of all other causes (besides

cancer, heart disease, or sudden injury)

Women who eat most meat study found:C - have a 6% lower risk of dying on injury and sudden deathD - have a 61% higher risk of dying of all other causes

“Over 10 years, eating the equivalent of a quarter-pound hamburger daily gave men in the study a 22% higher risk of dying of cancer and a 27% higher risk of dying of heart disease. That's compared to those who ate the least red meat, just 5 ounces per week.”

Beef Food Safety RecallsClass I & II Recalls, Quarterly, 1982-2007

0

3

6

9

12

15

18

82.1 84.1 86.1 88.1 90.1 92.1 94.1 96.1 98.1 00.1 02.1 04.1 06.1

Year & Quarter

Recalls

Increase in recalls during 2007 resulted In a 2.6% decline in beef demand

Beef Recall ProblemsBeef Recall Problems

Source: U.S. Food Safety Inspection Service

Food Consumed Away from Home Growth Food Consumed Away from Home Growth Benefitted Poultry and Hurt Beef DemandBenefitted Poultry and Hurt Beef Demand

Percentage of Food Consumed Away From HomeQuarterly, 1982-2007

40%

42%

44%

46%

48%

82.1 84.1 86.1 88.1 90.1 92.1 94.1 96.1 98.1 00.1 02.1 04.1 06.1

Year & Quarter

Source: U.S. Department of Commerce

Retail Beef Strip Loin Prices, April 2008

Price ($/lb) Store Description$4.99 Albertson's, Denver, CO Albertson's Supreme Beef$7.84 Wal-Mart, Manhattan, KS Wal-Mart Brand$7.99 HyVee, Lincoln, NE HyVee Blue Ribbon - Hormel

$10.99 Dillons, Manhattan, KS USDA Choice$12.99 Whole Foods, Overland Park, KS Certified Organic$14.99 City Market, Avon, CO Laura's Lean Beef$19.99 Cetak's Gourmet Meats, Lincoln, NE Cetak's & Certified Angus Beef$85.00 Dean & Deluca, Leawood, KS Japan Akaushi Wagyu

Data collected by Kelsey Fraiser

Is a Steak a Steak?

Consumer Awareness About One of Beef’s Positives Is Increasing

Articles Published Referencing Zinc or Iron or Protein & Diet

U.S. Newspapers, Quarterly, 1982-2007

0

100

200

300

400

500

600

700

82.1 84.1 86.1 88.1 90.1 92.1 94.1 96.1 98.1 00.1 02.1 04.1 06.1

Year & Quarter

Article

s

Source: LexisNexis

Can Exports Save US?Can Exports Save US?

Market Shares of Six Leading World Beef Exporters, 2000-2009 (Forecast)

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Year

Mar

ket

Sh

are

(%)

BRAZIL

AUSTRALIA

U.S.

Argentina

Source: Foreign Ag Service, USDA

India

Canada

Brazil Beef Production GrowthBrazil Beef Production Growth

Beef Production by Four Largest Countries, 2000-2009 (Forecast)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Year

1,0

00 M

etri

c T

on

s C

arc

ass

Wei

gh

t

BRAZIL

US

Source: Foreign Ag Service, USDA

China

4.2% Avg.Annual Growth

EU 27

Rodrigo Miranda Vieira

WELL EDUCATED, YOUNGEAGER, ENERGETIC, & CONFIDENT

Our global competition is:Our global competition is:

Looking ForwardLooking Forward Weak U.S. economy hurting beef demandWeak U.S. economy hurting beef demand Product quality & BQA remain importantProduct quality & BQA remain important Food safety problems reducing beef demandFood safety problems reducing beef demand Consumers respond to positive nutritional information Consumers respond to positive nutritional information

needs to be exploitedneeds to be exploited Convenience is importantConvenience is important

Lack of new products holding back beef demandLack of new products holding back beef demandAt home & at HRI levelAt home & at HRI level

Export Market is potential major growth area, Export Market is potential major growth area,

but we gotta get after it!but we gotta get after it!

Ted’s ThesisTed’s Thesis

Prosperity of cattle & beef industry is driven by consumer demand

All new $ that flow into your industry originate from consumers

Yet, we continuously make policy, production, and marketing decisions that fail to appreciate this well documented fact!

Top Five World Pork Exporters, 2000-2009 (Forecast)

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Year

Exp

ort

Mar

ket

Sh

are

(%) U.S.

EU - 27

Canada

Brazil

China

Source: Foreign Ag Service, USDA

Top Three World Poultry (Broiler + Turkey) Exporters, 2000-2009 (Forecast)

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Year

Exp

ort

Mar

ket

Sh

are

(%)

U.S.

Brazil

EU - 27

Source: Foreign Ag Service, USDA

July US Beef Cow Inventory, 1980-2008

20,000

25,000

30,000

35,000

40,000

45,000

1980 1984 1988 1992 1996 2000 2004 2008

Year

1,00

0 H

ead

8% reductionsince 1995

36.1 mln

33.15 mln

Number of Operations with Beef Cows, 1986-2007

600,000

650,000

700,000

750,000

800,000

850,000

900,000

950,000

1,000,000

1,050,000

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Year

Op

erat

ion

s

25% decline

Markets at each stagesupposed to coordinate but system failed

- highly varied product- little price-quality distinction - no incentives to improve

1. Safety assured2. Tender3. Flavorful4. Consistently high quality5. Healthy & Nutritious (Nutraceutical)6. Environmentally friendly production7. Animal friendly production8. Locally produced 9. Convenient to prepare10. Competitively priced

What Consumers Collectively Demand

Experience/CredenceAttributes

This means: explicit labeling and brands are essential to convey and assure information

SAFE?U.S. beef industry lost $3.2 to $4.7 billion in 2004 alone because of lost exports (Coffey et al., 2005)

Annual FSIS Class I and II Beef, Pork, Poultry Recalls, 1990-2007

0

5

10

15

20

25

30

35

40

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

Year

Rec

alls

Beef

Pork

Poultry

Food Safety Concern Major Media Articles, 1990-2007

0

2,000

4,000

6,000

8,000

10,000

12,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

Year

Art

icle

s

"food safety or contamination or (product recall) or outbreak or salmonella or listeria or e. coli or trichinae or campylobacter or staphylococcus or foodborne or bse or (mad cow) or encephalopathy"

Beef

Pork

Fish/Seafood

Poultry

Percentage of Consumers that have Reduced Consumption of Beef Last Five Years Citing Food Safety Concerns

19.6 20.6

31.2

55

0

20

40

60

80

100

Canada US Mexico Japan

Respondent Country

Per

cen

tag

e o

f R

esp

on

den

ts

Survey of 1,000 US, Canadian, Mexican, & Japanese Consumers, 2006

Respondent Country

Country of Origin CANADA US JAPAN MEXICO

Unknown 14% 11% 3% 18%

Australia 58% 46% 70% 31%

Brazil 35% 29% 18% 26%

Canada 92% 52% 31% 42%

Japan 43% 36% 85% 30%

Mexico 21% 17% 13% 66%

United States 70% 82% 8% 46%

Percentage of Respondents Indicating Beef from Various Percentage of Respondents Indicating Beef from Various Origins is “somewhat” or “very” safe foodOrigins is “somewhat” or “very” safe food

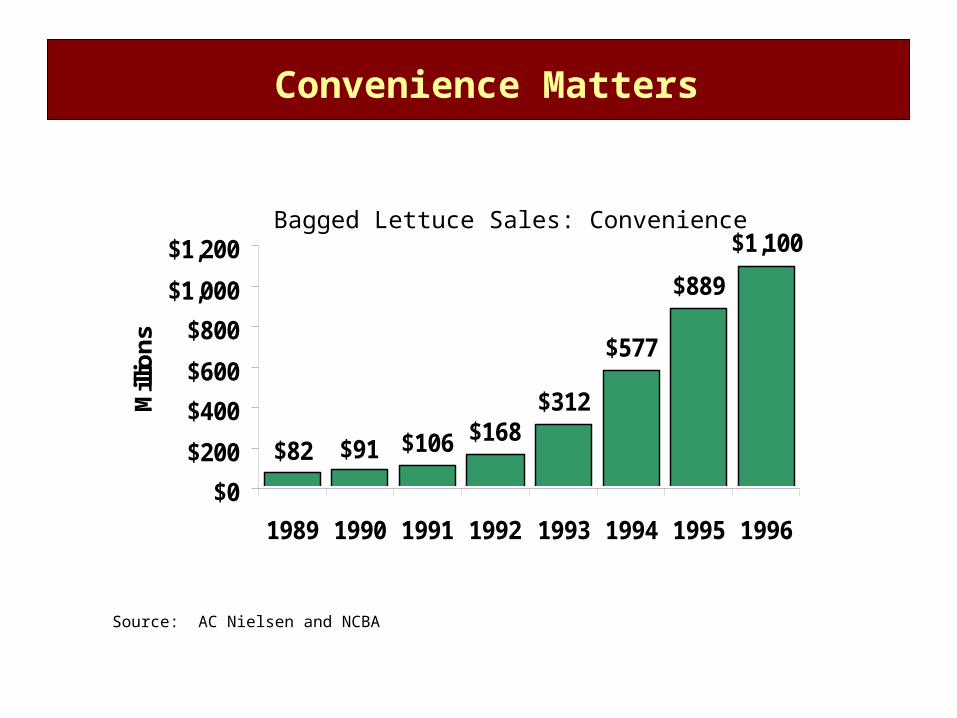

Convenient to Prepare?

Convenience Matters

Shredded Cheese Sales Increase 84%

Source: AC Nielsen and NCBA

$739$828 $888

$956

$1,079$1,196

$1,316 $1,358

$400

$600

$800

$1,000

$1,200

$1,400

1991 1992 1993 1994 1995 1996 1997 1998

Sa

les

(m

illi

on

s)

$106 $168$312

$577

$889

$1,100

$91$82

$0

$200

$400

$600

$800

$1,000

$1,200

1989 1990 1991 1992 1993 1994 1995 1996

Mill

ion

s

Bagged Lettuce Sales: Convenience

Convenience Matters

Source: AC Nielsen and NCBA

1. Fresh Branded Case-Ready Products

2. Meal Packages

Single dish quick fix meal consumer expenditures expanded 83% in 2001 to $141 million – AC Nielsen

472 beef products introduced in 2001Compared to 70 in 1997 - NCBA

3. Food Service

Food service continuesto grow

Diversity of product needs

Quality control in volume are critical

Contracts

What do they require?

Product integrity – quality, consistency

High level of accountability of input supplier

Product safety assurances – mega responsibility/risk

Production practice assurances (including location?)

Traceability

Consistent continuous supply

Five Critical Industry Errors

Postures That What Don’t Work – Long Run:

1. “blind loyalty” - defensiveness

2. “hiding from truth” - secretive (internal & external)

3. “camouflage” - fine print

never ever, naturally raised, natural…

4. “consumers are stupid”

5. “scare tactics”

Five Industry Recommendations

Postures That What Will Work – Long Run:

1. “give ‘em what they want”

2. “show and tell your story”

3. “invest in technology for consumers”

4. “coordinate” – information/send value vertically

5. “give ‘em your 1-800 number”

If we don’t do these, somebody else will!