technology monitor - great american group 2015 — technology monitor 4 industry trends —...

TRANSCRIPT

1 March 2015 — Technology Monitor

Technology Monitor (Inventory & Equipment)

1 March 2015 — Technology Monitor

Trend Tracker

NOLVs: NOLVs increased for semiconductor

companies as sales and margins improved. NOLVs

were mixed for most other technology segments

due to variations in sales and/or gross margins, and

remained relatively consistent for servers, given

steady demand.

Sales Trends: Sales increased for semiconductors

and the related capital equipment due to higher

memory chip sales amid strong smartphone

demand, and for storage hardware due to the

increased use of hard drives in cloud and other

applications, as well as higher solid state drive

(“SSD”) demand.

Sales were mixed for printed circuit boards

(“PCB”)/electronic manufacturing services (“EMS”),

as some companies benefited from higher demand,

while others faced strong international competition.

Sales were also mixed for personal computer

(“PC”) hardware, as some companies enjoyed

rebounding consumer demand, while others

endured slowing commercial demand as well as

competition from smartphones and tablets.

Sales were relatively consistent for servers, with

growth in the x86 server market slowed by server

consolidation via virtualization.

Gross Margin: Gross margins increased for

semiconductors due to higher selling prices and/or

improved operating efficiencies.

Gross margins were mixed for semiconductor

capital equipment, PCBs/EMS, storage hardware,

and servers due to variations in the sales mix and in

operating efficiencies. Gross margins were also

mixed for PC hardware, with increasing margins

for many U.S. companies but decreasing margins

for companies abroad due to foreign exchange

losses and rising labor costs in China.

Inventory: Inventory levels for most technology

segments increased in Q4 2014 versus Q4 2013 to

fulfill generally higher demand. However, server

inventories decreased due to server consolidation

via virtualization.

2 March 2015 — Technology Monitor

Overview

Healthy growth in consumer electronics spending

benefited from surging demand for smartphones,

tablets, and TVs. Smartphones were the top-selling

product, with a 26% year-over-year increase to total

an estimated 1.3 billion shipments in 2014, according

to IDC Global Technology and Industry Research

Organization (“IDC”). Tablet sales climbed 25% to

281 million shipments. LCD TV shipments grew

5.4% as consumers shifted to larger screens, newer

models with Internet connectivity, and LCD versus

plasma displays, and given the HDTV price cuts.

While IT demand remains solid, IT spending slowed

in 2014 due to a more competitive market

environment, which pressured vendors to lower

their prices. Data system spending was the slowest

category, according to Gartner, with a mere 0.4%

increase to $140 billion due to lower-cost storage

options in the cloud and a shift away from high-end

server systems. In addition, device spending growth

was limited by price cuts.

The CEA projects U.S. consumer electronics

shipments will climb 3.0% to $223.2 billion in 2015

versus the prior year, while Gartner forecasts global

IT spending will rise 2.4% to $3.8 trillion.

In 2015, consumer electronics shipments will

continue to be fueled by demand for smartphones

and tablets, which are jointly slated to account for

46% of global technology sales. However,

smartphones are expected to face a slower growth

rate and a lower average price as the market

approaches saturation. TV sales will continue to rise

in 2015 as 1080p units are replaced with 4K screens.

While North America will remain a major revenue

source for the consumer electronics market, the

maturation of the market will result in an increased

share of revenue from China, India, and Africa.

IT spending this year will enjoy gains from stronger

IT budgets, which are expected to rise an average of

4.3%, driven by spending on security tools, cloud

computing, business analytics, development/

upgrades/replacements of applications, and

wireless/mobile products. However, hardware

spending is anticipated to fall as companies

outsource IT operations or move systems to the

cloud for greater efficiency. Other IT products that

may experience slower growth this year include

legacy systems, data centers, on-premises software,

unified communications systems, and storage.

Technology industry growth is largely driven by the use of consumer

electronics products as well as information technology (“IT”) products

and services. In 2014, U.S. consumer electronics shipments increased

3.0% from the prior year to an estimated $216.8 billion, according to the

Consumer Electronics Association (“CEA”), while global consumer

electronics spending climbed 1% to a little over $1.0 trillion. In addition,

Gartner, Inc. (“Gartner”) estimated global IT spending grew 2.1% to $3.7

trillion in 2014.

3 March 2015 — Technology Monitor

Overview

Inventory levels for technology products throughout

the supply chain typically depend on the seasonality

of the related end-products, with stocks built up in

advance of the seasonal selling period and

destocking performed once the build-up has

concluded. Inventory levels are also influenced by

more specific factors, such as the variations in

stocking associated with different fulfillment

models. Some large semiconductor companies, such

as Samsung Electronics Co., Ltd., as well as certain

other parts of the supply chain, such as distributors,

tend to deplete inventory in Q4 (the fourth quarter).

Overall, most major points of the supply chain

currently are at or near seasonal lows for the period

after the 2008 financial crisis. The leaner inventory

levels are due to increased efficiency resulting from

improved ERP (enterprise resource planning) and

EDI (electronic data interchange) systems, OEM

purchasing consolidation, and an emphasis on

increased working capital efficiency to maximize

free cash flow and cash return to shareholders.

U.S.: Holiday season (Black Friday through Christmas) for consumer electronics, Mother’s and

Father’s Day season (May and June) for consumer electronics, Back-to-School season (August and early

September) for computers including desktops, laptops, netbooks, tablets, and smartphones

China: Lunar New Year (late January to mid February), May Day/Labor Day (early May) for

household appliances, Golden Week (first week of October) for electronics products, Singles’ Day

(November 11) for online shopping

4 March 2015 — Technology Monitor

Industry Trends — Semiconductors

A semiconductor, also known as a chip, is a small

conductive wafer typically comprised of silicon and

found in nearly all modern electronics, primarily as a

part of memory chips, microprocessors, commodity

integrated circuits (“ICs”), and complex SOCs

(system on a chip). Semiconductor companies are

continuously working to build smaller, faster, and

cheaper chips to meet demand for increasingly

complex products, and are now outsourcing more

and more of their production to foundry companies

and others in the industry to improve efficiency.

Semiconductor demand is highly cyclical, relying on

demand for end-products such as PCs, cell phones,

and other electronic equipment. In the current era of

modern technology, where a slew of new tech

products constantly and rapidly emerge to render

slightly older and seemingly high-tech products

obsolete, the semiconductor industry is clearly in the

boom stage of the cycle.

In 2014, the global semiconductor industry achieved

record sales of $335.8 billion, which reflects an

increase of nearly 10% from 2013, according to The

Semiconductor Industry Association (“SIA”). Sales

reached record levels for the second consecutive year

and surpassed projections from the World

Semiconductor Trade Statistics organization. The

positive results reflected “broad and sustained

growth across all regions and product categories,”

said John Neuffer, president and CEO of the SIA.

Logic (a digital data processor) was the largest

semiconductor category, with global sales increasing

6.6% to $91.6 billion in 2014 versus 2013.

Memory was the second-largest and the fastest-

growing chip category, with global sales rising 18.2%

to $79.2 billion primarily due to a 34.7% sales jump in

the DRAM memory segment driven by booming

smartphone demand and strong DRAM pricing.

In the Americas, semiconductor sales increased 12.7%

in 2014 versus 2013, with the U.S. market exhibiting

particular strength and leading all global regions

given its double-digit growth.

The momentum is expected to persist through 2015

and beyond with continued semiconductor sales

growth in the U.S. and abroad. Gartner projects

global semiconductor revenue will increase at a

slightly slower rate of 5.4% to $335.8 billion in 2015.

5 March 2015 — Technology Monitor

Industry Trends — Semiconductors

Sales will be fueled by strong growth in application-

specific standard products in smartphones as well as

DRAM and NAND flash in ultramobiles and SSDs,

but partially offset by a reduction in DRAM pricing to

more traditional levels as supply and demand

become more in line with each other this year.

“While mobile phone semiconductor sales will

remain robust, driven by the accelerating shift to

smartphones and 4G Long Term Evolution, there is

concern that weak sell-through for other electronic

equipment categories will result in higher inventory

levels and drag down semiconductor sales in the first

quarter of 2015,” said Jon Erensen, research director

at Gartner.

Semiconductor inventory levels in dollars behaved

seasonally, rising 3.9% in Q3 2014 versus the prior

quarter before falling 0.9% in Q4, as some large

semiconductor companies tend to deplete

inventory in Q4. On a year-over-year basis,

inventory levels climbed 10.4% in Q4.

However, days of inventory trends were much

steadier, with 81 days of inventory in Q4 representing

the second-leanest seasonal level since Q4 2010.

NAND pricing generally declined in 2014 due to an

oversupply, as companies cut DRAM production and

instead boosted NAND flash production amid rising

demand for storage in mobile devices. NAND micro

SD pricing dropped from approximately $0.52 per

gigabyte (“GB”) in February 2014 to $0.32 per GB in

February 2015. Composite NAND spot prices on the

DRAM exchange have also been falling.

6 March 2015 — Technology Monitor

Industry Trends — Semiconductors

Meanwhile, DRAM pricing increased in 2014 due to

short supplies amid reduced capacity, expansion of

DRAM applications, and a diversification of

customers. Over the prior three years, average selling

prices (“ASPs”) of DRAM chips nearly doubled,

according to Semiconductor Equipment and

Materials International (“SEMI”).

Mergers and Acquisitions

In October 2014, Qualcomm, the world’s leading

mobile chipmaker, acquired UK-based

Cambridge Silicon Radio, a multinational fabless

semiconductor company specializing in

connectivity, audio, imaging, and location chips.

In February 2015, Intel agreed to acquire

Germany-based Lantiq, a fabless semiconductor

company specializing in broadband access and

home networking technologies.

The automotive semiconductor sector is also

consolidating due to higher demand for chips

used in infotainment and collision avoidance

applications.

While semiconductor companies are constantly

improving and updating their chip products, these

products have largely remained silicon-based for the

past 60 years. However, a new technology is

emerging that could one day render silicon chips

obsolete: gallium nitride (“GaN”).

Transistors produced from GaN chips can switch on

and off more quickly (making them easier to control)

and can withstand higher voltages than transistors

produced from silicon chips, which should allow

companies to manufacture products that are smaller,

faster, smarter, and more power-efficient.

Currently, GaN transistors are not being used in PC

chips, but are instead utilized in new applications,

such as upgrades to military radar and

communication systems, self-driving car prototypes,

and virtual-reality helmets, as well as innovative

consumer-electronics and medical devices.

Industry inertia may delay the replacement of silicon-

chip transistors with GaN-chip transistors in common

computing applications such as PCs and

smartphones, at least until GaN’s purported

performance and cost advantages become more

evident. According to Bloomberg, analysts project

that GaN-chip transistors will capture over $1 billion

of the silicon-chip transistor market in the next few

years.

Another emerging trend that may spread more

quickly is the incorporation of security features into

chips. Intel and other chipmakers are beginning to

embed security features into wireless chips in an

effort to protect against cyber-attacks.

Intel Corporation (“Intel”)

Qualcomm Incorporated

(“Qualcomm”)

Texas Instruments Incorporated

Taiwan Semiconductor

Manufacturing Company Limited

Samsung Electronics Co., Ltd.

7 March 2015 — Technology Monitor

Industry Trends — Semiconductor Capital Equipment

Semiconductor capital equipment consists of

machines that are used in the production of

semiconductor devices and are located in

manufacturing facilities known as fabs. Front-end

capital equipment accounts for nearly 70% of

industry sales, according to Value Line, Inc. (“Value

Line”), and includes the following types of

equipment: silicon wafer fabrication and processing,

photolithography, resist processing, expose and

write, chemical mechanical planarization (polishing),

chemical vapor deposition, etching, surface

conditioning/cleaning and drying, ion implantation,

sputter, and thermal processing equipment, among

other types.

Back-end equipment comprises the remaining 30% of

industry sales and includes equipment involved in

the assembly, packaging, and testing of ICs.

Like the demand for semiconductors, demand for

semiconductor capital equipment is highly cyclical.

Chip companies order capital equipment based on

their projections for future demand. In the five years

before 2014, manufacturers of memory chips halted

or significantly reduced their capital spending for

new capacity. As a result, memory chip supplies

tightened, boosting memory chip prices in the past

two years and coinciding with increased demand due

to strong sales of mobile devices. Now, memory chip

makers are finally investing in new semiconductor

capital equipment to cash in on the burgeoning chip

demand.

Logic and foundry chip manufacturers are also

joining memory chip makers in heavily investing in

capacity build-up, node shrinking, new material

integration, and advanced packaging in order to

handle new technology challenges.

In 2014, global semiconductor equipment and capital

spending grew 16.4% and 12.9%, respectively, to

$38.9 billion and $65.3 billion, according to Gartner.

Global sales of wafer fab equipment, wafer-level

manufacturing equipment, wafer-level packaging

and assembly equipment, die-level packaging and

assembly equipment, and automated test equipment

increased 16.0%, 16.1%, 19.4%, 13.8%, and 24.0%,

respectively, following sales declines for all categories

in 2013. SEMI estimates U.S. semiconductor

equipment sales jumped 20% to $38 billion in 2014.

Capital equipment sales are expected to continue

rising in 2015, albeit at a slower pace, with projected

increases of 5.6% globally and 15.8% in the U.S.,

according to Gartner and SEMI, respectively.

Semiconductor capital equipment inventory levels

have been on the rise as manufacturers of memory,

logic, and foundry chips are finally investing in new

capacity to fulfill increased chip demand.

8 March 2015 — Technology Monitor

Industry Trends — Semiconductor Capital Equipment

Quarter-over-quarter, inventory levels in dollars

climbed 1.9% and 2.7% in Q3 and Q4 2014,

respectively. On a year-over-year basis, inventory

levels jumped 9.0% in Q4.

After declines in the first half of 2014, days of

inventory began rising in the second half, increasing

from a two-year low 94.2 days in Q2 2014 to 99.9 days

in Q4.

Changes in semiconductor equipment are directed by

advancements in circuit-board technology.

According to Value Line, the ongoing shift to larger

wafers, the development of smaller-geometry chip

designs, and the shift from aluminum to copper

interconnections are the current trends in circuit

board technology that have the most significant

impact on semiconductor equipment.

The transition to larger-sized silicon wafers drives

demand for the newest and most advanced (and,

incidentally, more expensive) wafer production lines,

which boast the highest productivity rate.

The continued reduction in the size of chip geometry

requires manufacturers of semiconductor equipment

to keep pace by producing advanced equipment to

fabricate and test the smaller-geometry chips.

Finally, chip makers’ increased use of copper, versus

aluminum, for interconnections will boost demand

for upgraded equipment, as copper is more difficult

to work with.

Applied Materials, Inc.

ASM Lithography, Inc.

KLA-Tencor Corporation

Lam Research Corporation

Teradyne, Inc.

9 March 2015 — Technology Monitor

Industry Trends — PCBs/EMS

PCBs, the platform upon which semiconductors and

other electronic components are mounted and

electrically interconnected, are the foundation of

virtually all electronics products. Patterns of circuitry

are etched from copper onto PCBs and laminated

together via intense heat and pressure in a vacuum.

PCB categories include rigid PCBs (“RPCBs”), flexible

PCBs (“FPCBs”), and substrate. RPCBs were the only

type in the early stages of the industry, and continue

to account for over 50% of the industry; however,

FPCBs and substrate represent emerging products

and have experienced rapid growth in recent years,

as reported by Research and Markets. Going

forward, large PCB vendors are expected to offer the

traditional RPCBs while also increasing their focus on

FPCBs and substrate.

Due to an increasing trend of offshoring, the majority

of PCB production takes place abroad, with China

being the top producer at nearly 44.2% of global PCB

output. The U.S. accounted for almost 4.7%.

EMS includes companies that are contracted by

OEMs to design, assemble, produce, repair, and/or

test PCB assemblies and the related electronic

components on behalf of the OEMs. EMS companies

may be contracted at different points of the

manufacturing process.

In recent years, greater demand for new features in

smartphones augmented demand for PCBs. Market

research firm IBISWorld, Inc. (“IBISWorld”) reported

communication equipment industries have grown

over the past five years to account for nearly 50% of

the market for the circuit board and electronic

component manufacturing industry.

North American PCB shipments increased 3.4% in

December 2014 versus 2013, according to electronics

industry association IPC, with PCB bookings up 7.9%.

However, shipments for 2014 as a whole declined

0.8% compared to the prior year.

“PCB business in North America was virtually flat in

2014 compared to the previous year,” said Sharon

Starr, IPC’s director of market research. “Strong

orders in the fourth quarter have kept the book-to-bill

ratio solidly in positive territory, which bodes well

for sales growth in 2015.”

North American PCB shipments have been tepid

partially due to strong international competition,

which, compounded with a strong U.S. dollar,

boosted imported PCB volumes. According to

IBISWorld, imports of circuit boards and electronic

components fulfilled an estimated 57.8% of domestic

demand in 2014. Given the increased offshoring of

PCB production, domestic production has decreased.

Research and Markets indicated the global PCB

manufacturing market totaled $62.3 billion in 2013,

which is projected to rise at a compound annual

growth rate of 3.6% to reach $74.3 billion in 2018.

Market volume is also slated to increase, with a

compound annual growth rate of 3.8% to reach 32

billion units in 2018.

North American demand for EMS dipped slightly in

Q1 2014 before climbing in Q2 and remaining

relatively flat throughout the rest of the year,

according to IPC. In December 2014, EMS shipments

totaled approximately $28.5 billion.

10 March 2015 — Technology Monitor

Industry Trends — PCBs/EMS

EMS inventory levels in dollars behaved seasonally,

rising 3.6% in Q3 2014 versus the prior quarter before

slipping 0.5% in Q4. On a year-over-year basis,

inventory levels remained relatively stable, climbing

0.4% in Q4.

Days of inventory exhibited a seasonal spike in Q1,

with 56.1 days of inventory, before dropping to 50.2

days in Q4.

Major manufacturers of PCBs include EMS

companies that are contracted to produce PCB

assemblies for OEMs.

Glass fiber/epoxy laminates, which have served as the

foundational structural substrate in PCBs for decades,

are under pressure from emerging trends that are

leading PCB manufacturers to reconsider their

material options. Among these trends are

miniaturization, improved thermal management,

higher speed and performance, and 3D printing.

E-glass (electric glass) and epoxy resin are expected

to remain the dominant substrates in the near-term,

and manufacturers of glass fiber are reducing yarn

diameters to meet market demand for small devices.

However, research and development programs are

seeking higher-performance materials that could

potentially act as alternatives.

Flextronics International LTD.

Jabil Circuit, Inc.

Sanmina Corporation

Hon Hai Precision Industry Co.,

Ltd.

11 March 2015 — Technology Monitor

Industry Trends — Storage Hardware

Storage hardware includes physical devices used to

store and/or process digital data. Primary devices

consist of system hard drives (including the CPU and

RAM of a system), which store data while the system

is running and are used in PCs, notebooks, printers

and copiers, MP3 players, digital video recorders,

smartphones, home servers, and a variety of other

applications. Secondary devices consist of optical

disk drives (“ODDs”) such as CDs and DVDs,

magnetic devices such as hard disks and magnetic

tapes, SSD memory devices such as USB drives and

memory cards, and magneto-optic disks such as

floppy disks.

Other types of storage hardware include holographic

storage, which provides a 3D projection of the data,

and cloud storage, which uses the internet to store

data at remote devices. Storage capacity is

continuously increasing, particularly for devices such

as hard drives and SSDs.

Hard disk drives (“HDDs”), also known simply as

hard drives, experienced a rebound in shipments last

year after three consecutive years of declines.

According to Coughlin Associates, HDD shipments

declined year-over-year from 2011 through 2013

initially due to the massive flooding in Thailand in

2011, which significantly reduced manufacturing

capacity for HDD components, and later due to a

shift from laptop to tablet computers. However,

HDD shipments increased 2.2% to 564 million units

in 2014 versus 2013 due to the increased use of HDDs

in cloud and other applications, as well as the

stabilization of the laptop market. Coughlin

Associates predicts HDD shipments will climb

slightly in 2015 due to the recovery in the laptop

market as well demand from cloud and emerging

enterprise applications.

However, Trendfocus, Inc. expects slightly lower

HDD shipments due to the gradual decline in

desktop PC sales and the continued encroachment of

SSDs (which are composed of flash memory rather

than moveable parts).

After jumping 82% in 2013, SSD shipments increased

an estimated 60% in 2014, according to Digitimes

Research. Demand remains strong from both

businesses and consumers due to falling NAND flash

prices, thinner notebooks, and an increase in

convertible tablets.

ODD demand has suffered from a shift in demand to

online streaming versus CD, DVD, and Blu-ray disks,

although the “1000-year” M-Disc introduced by

Millenniata may have some staying power, given its

features that are ideal for long-term, write-once

archiving purposes. Magneto optic disk demand has

been dwindling as such products, including floppy

disks, are nearly obsolete amid other cheap options

(namely SSD formats) with faster writing speeds and

higher capacity.

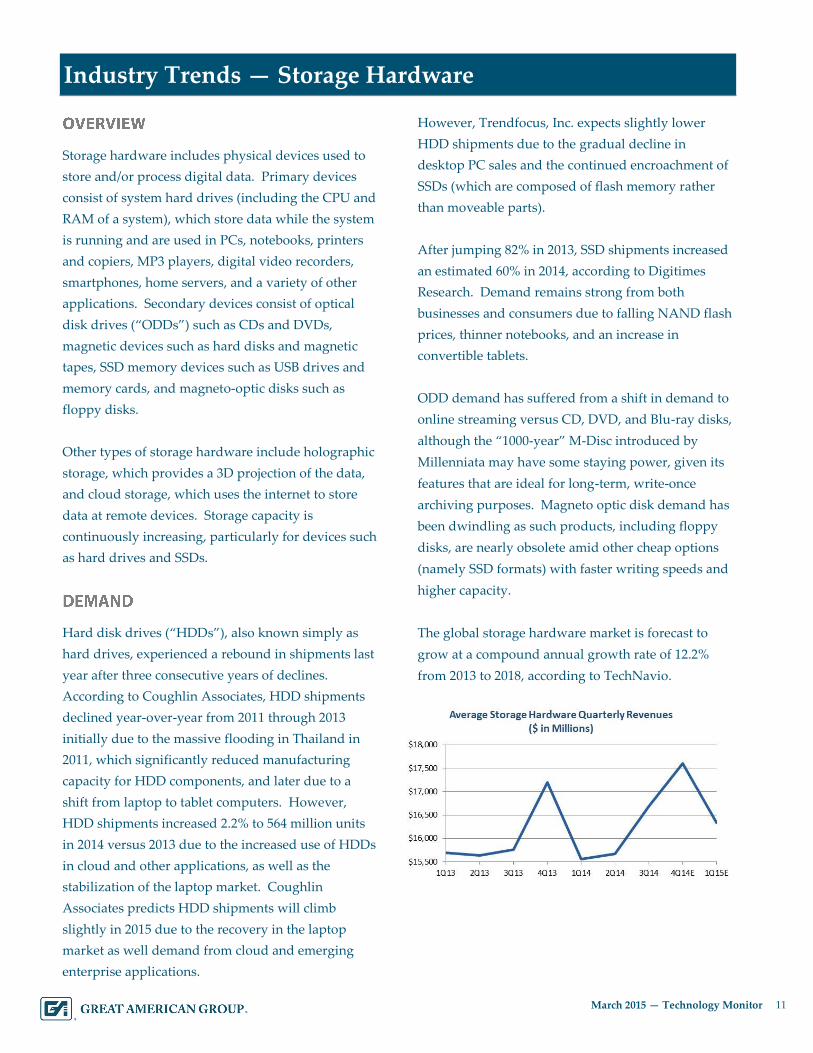

The global storage hardware market is forecast to

grow at a compound annual growth rate of 12.2%

from 2013 to 2018, according to TechNavio.

12 March 2015 — Technology Monitor

Industry Trends — Storage Hardware

IBISWorld indicated high-end hard drives and other

storage devices have experienced relatively flat

pricing over the past five years, in spite of continual

increases in storage capacities, due to the frequent

implementation of more efficient production

methods.

HDD prices were generally stable in 2014, with rising

ASPs in the last two calendar quarters offsetting

lower ASPs the previous two quarters, according to

Coughlin Associates.

IHS reported SSD prices have declined from $1.00 per

GB of capacity in early 2014 to $0.50 per GB by the

summer due to die shrinkage (resulting in more cells

in the same amount of space), increased sales

volumes, improved manufacturing efficiencies, and

greater competition. Prices are slated to drop further

once 3D stacking becomes more popular, significantly

boosting the amount of capacity in the same space, as

NAND flash memory cells are stacked on top of each

other for greater density instead of being two-

dimensional.

Storage hardware inventory levels in dollars

increased 3.1% in Q3 2014 versus the prior quarter

before slipping 0.6% in Q4. On a year-over-year

basis, inventory levels increased 3.1% in Q4 2014.

After rising to 44.3 days in Q2, days of inventory for

storage hardware fell to 41.9 days in Q3 and

remained steady in Q4.

Despite year-over-year declines for most bellwether

companies in the most recent quarter, overall annual

revenues fared better for certain companies. Western

Digital reported an increase in global storage-device

sales from $36 billion in 2013 to $38 billion in 2014,

with another increase to $42 billion projected for

2015, according to Digital Trends. Seagate projected

an 8% increase in revenues, as well as a 7% rise in

shipments.

EMC Corporation (“EMC”)

Hewlett-Packard Company (“HP”)

International Business Machines

Corporation (“IBM”)

NetApp, Inc. (“NetApp”)

Seagate Technology Public

Limited (“Seagate”)

Western Digital Corporation

(“Western Digital”)

13 March 2015 — Technology Monitor

Industry Trends — Storage Hardware

Mergers and Acquisitions

In 2015, HP plans to acquire Aruba Networks, a

wireless networking company specializing in the

mobile market.

In 2014, IBM acquired CrossIdeas, a provider of

identity governance and analytics software. IBM

is seeking acquisitions of cloud companies, as

IBM’s cloud revenue increased 60% in 2014 due

to demand for high-value cloud solutions.

In 2014, NetApp acquired Riverbed Technology’s

SteelStore product line, which supports backup

applications and cloud providers.

In 2014, Seagate acquired Xyratex Ltd., a leading

provider of data storage technology, and Avago

Technology’s LSI flash business, which offers

flash components used in SSDs. Seagate recently

announced a strategic partnership with Micron

Technology, a chip manufacturer, to offer

innovative flash-based storage solutions,

including next-generation SSDs.

In 2014, HGST, Inc., a wholly owned subsidiary

of Western Digital that sells storage hardware,

acquired Skyera, a developer of SSD systems for

scale-out cloud and enterprise data centers.

According to Apparatus, data storage in a typical IT

setting has increased at a rate of 30% to 40% per year,

with this rate accelerating in recent months, due to

more data being generated from numerous sources

and stored for longer periods of time. Rising data

usage is driven by the current use of advanced data

analysis by companies in nearly all industries to assist

in analyzing marketing, financial performance,

staffing, production schedules, and a whole host of

other data.

Providers of cloud services are emerging as major

consumers of storage systems, as they offer their own

servers, storage devices, and systems for other

companies to remotely store data and access

computer services or resources. These other

companies therefore tend to spend less money on

their own on-premises storage hardware and servers,

as they pay cloud storage providers to manage the

storage infrastructure as a service. Providers are

currently working with corporate IT departments

that already maintain on-premises storage systems,

not only to provide services for their active data, but

also to shift their older data into the cloud for long-

term archive and backup storage needs. Private

cloud storage, particularly Tier-2 storage, is slated to

be deployed more widely in 2015 by the government

sector and larger enterprises. Still, the industry

transition from on-premises hardware to the cloud

is not expected to be completed for nearly a

decade, and physical hardware spending will be

supported by overdue upgrades for on-premises

systems.

Storage purchases have been moving from

traditional, mechanical storage formats to flash-based

technologies in recent years, and flash-based SSD

formats are expected to completely replace magnetic

hard drives in the next five years, as SSD technology

can access memory significantly faster than

traditional magnetic drives. Major industry players,

such as EMC, HP, IBM, and NetApp, have begun to

roll out complete flash offerings, including hybrid

and all-flash array (“AFA”) SSD products. As a

result, independent vendors of AFA products are

finding it more difficult to fashion a niche for

themselves to survive in the industry.

Add-on capabilities will become more directly built

into storage solutions, including built-in data

protection, Ethernet interface, and other capabilities

typically offered by separate hardware.

14 March 2015 — Technology Monitor

Industry Trends — PC Hardware

PC hardware includes the physical components of a

computer, such as the monitor, motherboard, CPU,

RAM, power supply, mouse, keyboard, CD-ROM/

DVD-ROM drive, HDD, and other parts. Hardware

may include certain peripherals that connect to a

computer to increase its abilities. Manufacturers

market their PC hardware to distributors or directly

to businesses, governments, and retailers.

According to IBISWorld, revenue for the computer

peripheral manufacturing industry totaled $22.6

billion for 2014, with computer storage devices (CD-

ROM/DVD-ROM drives, HDDs, and SSDs)

accounting for 47.0% of industry revenue and input/

output peripherals (keyboards, mice, monitors,

webcams, microphones) accounting for 32.2%.

In recent years, PC sales were dampened by the

growing popularity of smartphones and tablets.

However, the market may be beginning to stabilize.

According to Gartner, global PC shipments totaled

83.7 million units in Q4 2014, increasing 1% from Q4

2013, with smartphones continuing to receive priority

over PCs in emerging markets such as China and

India. U.S. PC shipments climbed 13.1% over this

period, which marks the fastest growth rate in four

years.

“Installed base PC displacement by tablets peaked in

2013 and the first half of 2014,” said Mikako

Kitagawa, principal analyst at Gartner. “Now that

tablets have mostly penetrated some key markets,

consumer spending is slowly shifting back to PCs.”

However, IDC provided less optimistic results,

indicating global PC shipments declined 2.4% to 80.8

million units in Q4 2014 versus 2013.

IDC indicated that the decline was driven by slowing

commercial demand, although consumer demand is

gradually returning.

“Moving forward, the U.S. PC market should see flat

to slightly positive growth,” said Rajani Singh, Senior

Research Analyst at Personal Computing. “The U.S.

consumer PC market will finally move to positive

growth in 2015, strengthened by the slowdown in the

tablet market, vendor and OEM efforts to rejuvenate

the PC market, the launch of Windows 10, and

replacement of older PCs.”

After declining in Q1 2014, PC hardware inventory

levels have been climbing. Quarter-over-quarter,

inventory levels in dollars increased 6.0% and 1.7% in

Q3 and Q4, respectively. On a year-over-year basis,

inventory levels jumped 7.3% in Q4.

15 March 2015 — Technology Monitor

Industry Trends — PC Hardware

Days of inventory were more volatile, rising sharply

to 16.4 days in Q2 before dropping to 12.4 days in Q4.

Prices for PCs and related equipment have steadily

declined due to the exponential growth in computing

technology each year, which resulted in the related

manufacturing cost savings being passed on to

consumers. Intense competition has also kept prices

relatively low.

In 2014, Lenovo, HP, and Dell led the global PC

market, with market shares of 18.8%, 17.5%, and

12.8%, respectively, according to Gartner. PC

shipments in 2014 for Lenovo, HP, and Dell increased

11.1%, 7.9%, and 9.9% respectively, versus 2013.

Mergers and Acquisitions

In 2015, HP plans to acquire Aruba Networks.

In 2014, Lenovo acquired Google Inc.’s

(“Google”) Motorola Mobility smartphone

business and IBM’s low-end x86 server business.

In 2014, Dell acquired data analysis provider

StatSoft.

Apple acquired 20 companies in 2014, including

low-power display company LuxVue, headphone

producer Beats Electronics, and a variety of apps

and platforms, among other companies.

Compal acquired Toshiba’s European LCD TV

factory in late 2013 and is seeking to acquire PC

and Internet-of-Things (IoT) companies in 2015.

Amid the burgeoning popularity of smartphones and

tablets, demand has risen for more-portable PCs (e.g.,

regular, thin, and light notebooks in addition to

netbooks such as Google’s new Chromebook),

laptops that convert into tablets via detachable/

bendable screens, and PCs with touch-screen

systems. The increased global sales of netbooks, in

particular, indicate that consumers are willing to

sacrifice screen size and computing capability in

favor of portability and easy access to entertainment.

While current high-end computer monitors use either

LCD or LED displays, these technologies are likely to

be replaced by even slimmer, more energy-efficient,

and higher-picture-quality options in the near future,

such as organic LED (OLED) screens. Curved PC

displays are also a developing trend, although only

professionals and enthusiasts are likely to pay a

premium for curved monitors.

Flash-based SSD storage formats are anticipated to

replace magnetic hard drives in the next five years.

Lenovo Group Limited (“Lenovo”)

HP

Apple, Inc. (“Apple”)

Dell, Inc. (“Dell”)

Compal Electronics, Inc. (“Compal”)

Asustek Computer Incorporation

16 March 2015 — Technology Monitor

Industry Trends — Servers

A server is a system of computer hardware and

software that provides network services across a

computer network via computer programs. Many

companies maintain server rooms or data centers that

house continuously operating computer servers,

while others are transitioning their data to remote

cloud-based servers operated and maintained by

third-party providers.

There are a variety of server types, such as

application servers, catalog servers, communications

servers, database servers, and proxy servers, among

others. In addition, the Internet is based upon a

client/server model, with millions of servers

connected to the Internet, including the World Wide

Web, email, online gaming, and database servers,

among others.

Global server shipments and revenue increased 4.8%

and 2.2%, respectively, in Q4 2014 versus Q4 2013,

according to Gartner. In 2014 as a whole, global

server shipments and revenue grew 2.2% and 0.8%,

respectively.

The increased server demand was driven by growth

in the x86 server market as a result of hyperscale data

center deployments (as x86 servers remain the

primary platform used in large-scale data center

build-outs worldwide) and service provider

installations, despite declines in the mainframe and

Unix platforms.

According to Uptime Institute’s 2014 Annual Data

Center Industry Survey, overall data center budgets

are expanding throughout the world, with 62% of

data center organizations receiving large year-over-

year budget increases in 2014 versus only 36% in

2013.

However, data centers are increasingly consolidating

via virtualization, which has slowed shipment

growth.

Gartner projects modest growth in the global server

market this year, supported by further expansion in

the x86 server market due to the growth of integrated

systems, although continued server consolidation

may partially offset the gains.

Server and related hardware inventory levels in

dollars behaved relatively seasonally, rising 0.6% in

Q3 2014 versus the prior quarter before falling 7.4%

in Q4. On a year-over-year basis, inventory levels

declined 4.1% in Q4.

17 March 2015 — Technology Monitor

Industry Trends — Servers

Days of inventory exhibited minor fluctuations, rising

to 27.6 days in Q3 before slipping to 27.1 days in Q4.

In Q4 2014, HP led the global server market with a

27.9% share of the market based on revenue,

although its revenue only increased 1.5% year-over-

year, according to Gartner. Dell maintained a 17.3%

market share and experienced a 16.9% boost in

revenue. IBM and Lenovo maintained market shares

of 12.8% and 7.9%, respectively. IBM’s server

revenue fell 50.6%, while Lenovo’s server revenue

jumped 743.4%, due to Lenovo’s acquisition of IBM’s

x86 server business in Q4.

Server vendors are gradually experiencing a shift in

customers from end-user companies to cloud storage

providers (which serve end-user companies).

According to a recent report by Business Cloud

News, despite slow expected growth in server

shipments, cloud data centers are anticipated to

increase over the next few years to account for nearly

half of all server shipments by 2018.

Server vendors are facing challenges from web

customers, including Facebook, Inc. and Google, that

are custom-designing their own computer servers via

contract manufacturers in Asia, spurring other

similar companies to contemplate following suit. As

a result, server suppliers are offering more attractive

prices, emphasizing software innovations, and

otherwise catering to the needs of major web

customers in order to remain competitive. More

traditional customers, such as banks and government

entities, are also posing a threat by considering

alternative suppliers that could offer lower price

points.

HP

Dell

Lenovo

18 March 2015 — Technology Monitor

Industry Trends — Distribution

Distributors in the technology industry distribute

electronics components and computer products.

According to IBISWorld, communications equipment

and supplies (e.g., telephones, routers, modems,

navigational equipment, and radar) represented the

largest product segment, accounting for 46.3% of

revenue for the current U.S. electronic part and

equipment wholesaling industry.

Electronic parts and equipment (e.g., capacitors,

resistors, connectors, and solar cells) represented

23.6%, semiconductors represented 18.0%, integrated

circuits represented 6.1%, and other goods (e.g.,

computer equipment, storage devices, and peripheral

equipment) comprised the remaining 6.0%.

Distribution revenue grew at an annualized rate of

4.4% over the past five years to reach $366.3 billion, as

reported by IBISWorld, with demand driven by the

proliferation of consumer electronics as well as the

increased use of electronics products in the industrial

sector. Demand for electronic parts, semiconductors,

and circuits grew to support rising demand for

consumer electronics and increased factory

automation, while demand for communications

equipment and telephones fell as consumers adopted

smartphones and other mobile devices.

However, the growth rate for revenue has slowed, as

more manufacturers are sourcing electronic parts at a

lower cost from distributors in China and other low-

labor-cost countries versus U.S. distributors.

Distributors also face challenges from falling prices

for electronics products, an influx of lower-cost

imports, and the increased potential for wholesale

bypass (where customers bypass the distributor and

purchase goods directly from the manufacturer).

As a result, IBISWorld projects industry revenue

growth will slow to an annualized rate of 1.7% over

the next five years to reach $399.2 billion by 2020.

Distributor inventory levels in dollars climbed 2.2%

in Q3 2014 versus the prior quarter before slipping

2.5% in Q4, when distributors deplete inventories.

Year-over-year, inventory levels were up 6.9% in Q4.

In 2014, days of inventory continued to follow

seasonal trends, rising in Q1 and Q3 (to 42.4 and

42.7), but declining in Q2 and Q4 (to 40.7 and 39.0).

19 March 2015 — Technology Monitor

Industry Trends — Distribution

Mergers and Acquisitions

Synnex completed its acquisition of IBM’s

customer relationship management business in

2014.

Arrow plans to acquire immixGroup, an IT

solutions provider, in Q2 2015 in order to expand

its presence in the public sector market.

Ingram acquired Rollouts, an IT services

company, in 2014.

Arrow Electronics, Inc. (“Arrow”)

Avnet, Inc.

Ingram Micro Inc. (“Ingram”)

Tech Data Corporation

Synnex Corporation (“Synnex”)

CDW Corporation

20 March 2015 — Technology Monitor

Machinery and Equipment

The market for late-model, name-brand CNC

(computer numerical control) equipment, less than

eight years of age, remained stable over the last

year following 24 months of steady growth.

Communication systems and equipment designed

and/or configured for specific functions in a

narrow industry, such as portable antenna cells,

have an appeal that is somewhat limited to those

also engaged in the field of communications.

The specific circuit board electronic assembly

industry is poised for a 4% year-over-year decrease

in demand for the next five years. This falls on top

of a 2% decrease this year alone, according to

IBISWorld. However, it is of note that many

lending institutions are entering the PCB sector in

lending activity of late. This has caused somewhat

of a bump in used equipment values for late-model

machinery. While older machines are still in

demand for parts, original equipment

manufacturers are still offering attractive financing

packages on new machines with low interest and

warranties, and are expected to continue to do so,

which will presumably balance out any rise in

used equipment values going forward.

End-users who own the same makes and models of

various technological machinery and equipment

would be ideal prospects for such goods.

However, the amount of similar older equipment

currently available in the used equipment industry

may have resulted in diminished returns, favoring

the buyer, and not the seller.

Specialized, or “job specific,” items do not typically

command strong interest in a liquidation setting.

Often, the cost to re-tool and re-engineer job–

specific machinery and production lines is cost

prohibitive to a speculative buyer.

There is an inherent technological obsolescence

associated with electronically controlled and/or

customized equipment in the “high-tech” sector, as

is readily apparent in the computer and electronics

test equipment manufacturing industries. In a

recovering but cautious manufacturing

environment, buyers coping with the economic

uncertainty correlated to the theoretical liquidation

of these plants are projected to limit their

purchases to equipment for which they have an

immediate need or to items which can be

purchased at significant discounts.

Although economic conditions continue to

improve, many firms continue to shed equipment

related to overcapacity in order to increase

utilization rates and decrease expense and

maintenance costs. In general, such dispositions

by others and the continued technical

advancements routine to the industry may have

affected the desirability of certain machinery and

equipment. In the current manufacturing climate,

sales of production equipment items tend to be

correlated to work moving between suppliers,

rather than to increases in overall volume.

Industry growth leads to shortages of available

new and used equipment, in turn creating greater

demand and higher value for used items. At

present, quondam business failures, consolidation,

and recessional concerns serve to reverse this

condition.

21 March 2015 — Technology Monitor

Technology Reference Sheet

($ in Millions) 2014 2013 Year-Over-

Year Change

Q4 2014

(Estimated) Q3 2014

Quarter-Over-

Quarter

Change

Semiconductors $265,588.7 $238,763.9 11.2% $70,165.9 $68,911.3 1.8%

Semiconductor

Capital Equipment $26,096.5 $22,769.9 14.6% $6,509.6 $6,504.0 0.1%

PCBs/EMS $63,399.1 $62,571.1 1.3% $16,904.8 $15,956.8 5.9%

Storage Hardware $65,524.5 $64,284.0 1.9% $17,601.8 $16,691.7 5.5%

PC Hardware $206,207.3 $204,009.0 1.1% $57,448.9 $48,141.0 19.3%

Servers/Hardware $230,077.9 $238,787.6 (3.6%) $57,592.7 $57,773.7 (0.3%)

Imaging $63,074.1 $64,574.9 (2.3%) $15,410.7 $15,895.5 (3.1%)

Wireless $407,143.0 $345,074.8 18.0% $123,036.0 $92,202.5 33.4%

Telecommunications $141,056.1 $134,026.7 5.2% $35,348.0 $35,362.8 0.0%

Distribution $77,542.8 $69,962.2 10.8% $21,033.9 $19,247.4 9.3%

($ in Millions) 2014 2013 Year-Over-

Year Change Q4 2014 Q3 2014

Quarter-Over-

Quarter

Change

Semiconductors $27,013.9 $25,079.0 7.7% $27,013.9 $27,271.8 (0.9%)

Semiconductor

Capital Equipment $4,412.5 $4,048.2 9.0% $4,412.5 $4,293.9 2.8%

PCBs/EMS $8,563.6 $8,920.8 (4.0%) $8,563.6 $8,607.2 (0.5%)

Storage Hardware $4,174.8 $4,047.8 3.1% $4,174.8 $4,202.8 (0.7%)

PC Hardware $10,136.9 $9,447.2 7.3% $10,136.9 $9,964.9 1.7%

Servers/Hardware $10,591.1 $11,047.6 (4.1%) $10,591.1 $11,438.5 (7.4%)

Imaging $5,259.0 $56,55.9 (7.0%) $5,259.0 $5,691.5 (7.6%)

Wireless $16,262.3 $16,846.8 (3.5%) $16,262.3 $17,104.9 (4.9%)

Telecommunications $6,164.0 $5,696.1 8.2% $6,164.0 $5,949.8 3.6%

Distribution $8,136.0 $7,609.2 6.9% $8,136.009 $8,342. (2.5%)

22 March 2015 — Technology Monitor

Experience

Great American Group, LLC (“GA”) has worked with and appraised numerous companies within the

technology industry, including businesses with revenues ranging from $4 million to over $4 billion. While

our clients remain confidential, they include companies throughout the technology supply chain, including

manufacturers, importers, distributors, and retailers of technology and electronics products, as well as

related parts and accessories. GA’s Machinery and Equipment division has also appraised technology-

related machinery and equipment for resale in the secondary market. GA’s extensive list of inventory

appraisal experience includes:

A provider of IT services and products, including

wireless modules, modems, servers, monitors,

keyboards, and other products.

A provider of IT solutions to businesses,

assembling and installing products such as

servers in addition to offering memory cards and

other data-storage products, as well as software

and networking products.

A provider of servers, data storage devices, and

related hardware and accessories for data centers

at various businesses, offering configurations per

customer specifications.

A large global provider of broadcast equipment

and related products, including cameras, routers,

servers, storage devices, and switchers.

A manufacturer and distributor of single- and

three-phase power transformers built to

customer specifications for companies in the

electrical utility, public power, and industrial

markets.

Distributors of electronics and computer

products, including mobile storage devices, MP3

players, smartphones, laptops, desktop

computers, and other products.

A provider of a variety of consumer electronics

and industrial products, including computers

and consumer electronics under the company’s

private label, which are sold online and to retail

electronics stores, TV retailers, catalogs, and

wholesalers.

An independent distributor of data center

products, primarily including servers and

memory-related products, as well as networking

equipment, storage products, power supplies,

printers, laptops, and other computer hardware,

as well as mobile computing products.

One of the largest wire and cable producers in

North America, offering a wide range of wire

and cable products for use in the residential,

commercial, industrial, retail, electrical

wholesale, and utility construction markets.

GA has also liquidated a number of companies offering technology and electronic products, including

Circuit City, MPC Computers, Pioneer Electronics, and Computer City. In addition to our vast liquidation

and appraisal experience, GA maintains contacts within the technology industry that we utilize for insight

and perspective on recovery values.

GA is a subsidiary of B. Riley Financial, Inc., whose affiliate B. Riley & Co. (“B. Riley”) is nationally

recognized for its highly ranked proprietary equity research. B. Riley’s technology research team has

developed expertise in various technology sectors by performing extensive due diligence on key companies.

Its analysts continuously monitor industry developments and communicate with company management

teams, competitors, suppliers, and customers. B. Riley regularly publishes its research findings through

Research Updates and daily Morning Notes, to which it has provided GA access. B. Riley & Co., LLC is a

member of FINRA and SIPC. For more information, please visit www.brileyco.com.

23 March 2015 — Technology Monitor

Monitor Information

The Technology Monitor relates information covering a variety of technology products from a

manufacturing and wholesaling standpoint, including industry trends and their relation to the

valuation process. As rapid advancements in technology can result in product obsolescence,

our bi-annual Technology Monitor highlights recent market developments as well as emerging

trends and technologies that could potentially shift product demand. GA strives to

contextualize important indicators in order to provide a more in-depth perspective of the

market as a whole.

GA internally tracks recovery ranges for technology products, but we are mindful to adhere to

your request for a simple reference document. Should you need any further information or

wish to discuss recovery ranges for a particular segment, please feel free to contact your GA

Business Development Officer.

GA’s Technology Monitor provides industry trend information for a variety of technology

products. The information contained herein is based on a composite of GA’s industry

expertise, contact with industry personnel, liquidation and appraisal experience, and data

compiled from a variety of well-respected sources believed to be reliable. We do not

guarantee the completeness of such information or make any representation as to its

accuracy.

24 March 2015 — Technology Monitor

Glossary of Terms

AIDC (Automatic Identification and Data Capture): AIDC is the automatic process of identifying objects,

collecting the related data, and entering that data directly into computer systems. AIDC technologies include

barcodes, biometrics (e.g., iris and facial recognition systems), RFID (Radio-Frequency Identification),

magnetic stripes, smart cards, OCR (Optical Character Recognition), and voice recognition.

Capacitor: Originally known as a condenser, a capacitor is a passive two-terminal electrical component that

is used to store energy electrostatically in an electric field. Within a capacitor, the terminals connect to two

metal plates (the electrical conductors) separated by a non-conducting substance (the insulator) such as air,

Mylar, glass, or ceramic, among other materials.

Circuit: A circuit is an electrical device that provides a path for electrical current to flow, thereby allowing

computations, signal amplifications, counting, timing, data movement, and other operations to be performed.

Circuits include discrete and integrated circuits, and are composed of electronic components such as

resistors, transistors, capacitors, inductors, and diodes, which are connected by conductive wires or traces.

CPU (Central Processing Unit): A CPU, also known as the processor or central processor, is the electronic

circuitry within a computer (the “brains” of the computer) that conducts the arithmetic calculations and other

logical, control, and I/O (input/output) operations necessary to carry out the instructions of a computer

program. Most modern CPUs are microprocessors contained on a single integrated circuit chip.

Discrete Circuit: A discrete circuit is constructed from individual electronic components connected by wire,

instead of a single integrated circuit, and is well suited for application-specific designs. Discrete circuits are

typically less time-consuming to build, larger in volume, and faster at loading data than integrated circuits,

but maintain a higher cost because they use more material and are built piecemeal.

DRAM (Dynamic Random-Access Memory): DRAM is a type of RAM (a form of data storage comprised of

small memory chips and installed on a computer’s motherboard) that stores each piece of data on a separate

capacitor. A DRAM chip can therefore hold more data than a SRAM (static RAM) chip, but requires more

power than SRAM. Unlike hard disks and CD/DVD-RWs, RAM devices allow data to be read and written in

nearly the same amount of time, regardless of the order in which data items are accessed.

EMS (Electronics Manufacturing Services): EMS refers to companies that are contracted to design,

assemble, produce, repair, and/or test electronic components and PCB assemblies for OEMs.

Fiber Optic Cable: Fiber optic cable is a high-speed data transmission medium, whereby digital data is

transmitted through the cable via rapid light waves. The cable contains tiny glass or plastic filaments that

carry light beams, and the receiving end of the transmission translates the light pulses into binary values that

a computer can read. Fiber optic cables offer the fastest data transfer rates of any data transmission medium.

25 March 2015 — Technology Monitor

Glossary of Terms

Hard Drive (Hard Disk Drive): A hard drive is a high-capacity, self-contained device that houses the hard

disk and handles the reading, writing, and storage of data on the hard disk. A hard drive is used to

physically store files, folders, and other data in computers and computer-based devices.

Integrated Circuit (IC): An integrated circuit (also known as an IC, chip, or microchip) is formed on one

small plate (currently tens of nanometers in size) of semiconductor material, and is used in traditional

computing. Due to its small size and close proximity of components, an IC performs at a higher level than a

discrete circuit, as the components of an IC can switch quickly and consume minimal power.

LED (Light-Emitting Diode): An LED is an electronic device that emits light when an electrical current

passes through it, and produces brighter light than other types of bulbs while using less energy. LEDs are

now being used as backlight for flat-screen TVs and computer monitors, and are also commonly used for

indicator lights on electronic devices, and in electronic signs, clock displays, and other applications.

LCD (Liquid Crystal Display): LCDs are super-thin displays used in laptop computer screens, flat-panel

monitors, and certain other electronic devices. LCDs display images using the light-modulating properties of

liquid crystals, which do not emit light directly.

Monitor: A monitor is a screen that displays visual output from a computer, cable box, video camera, VCR,

or other video-generating device. A computer monitor uses CRT and LCD technologies to display the

computer’s user interface and open programs, and allows the user to interact with the computer via the use

of a keyboard and/or mouse. A TV monitor uses CRT, LCD, and plasma technologies.

NAND: NAND is a type of flash memory (an electronic non-volatile computer storage device that can be

electrically erased and reprogrammed) primarily used in main memory, memory cards, USB flash drives, and

SSDs (solid-state drives). NAND is ideal for devices to which large files are frequently uploaded and

replaced, such as MP3 players, digital cameras, and USB drives.

POS (Point of Sale) system: A POS system is a system that facilitates and processes a retail transaction (a

sale, return, or order), and typically includes a cash register (comprised of a computer, monitor, cash drawer,

receipt printer, customer display, and barcode scanner) as well as a debit/credit card reader. POS software

can also record sales history, track orders, connect to other systems in a network, and manage inventory.

Power Supply: A power supply is a hardware component that supplies power to an electrical device by

converting the alternating current received from an electrical outlet into direct current supplied to the

computer/electrical device. The power supply also regulates the voltage to prevent overheating.

PCB (Printed Circuit Board): A PCB is a thin fiberglass, composite epoxy, or other laminate-material board

that is etched or printed with conductive pathways that connect different electronic components (e.g.,

transistors, resistors, and ICs) on the PCB. PCBs act as the foundation of many internal computer

components in both desktop and laptop computers, and are also used in other electronic devices.

26 March 2015 — Technology Monitor

Glossary of Terms

Resistor: A resistor is a device designed to resist or control the passage of an electric current, thereby

limiting or regulating the flow of electrical current in an electronic circuit.

RFID (Radio-Frequency Identification): RFID is a system that uses tags (ICs that include a small antenna)

that respond to radio waves in order to track objects, people, or animals. RFID tags can be read by a laser

scanner or recorded by being placed within the range of an RFID radio transmitter, and maintain uses in

merchandise tags, inventory management, airplane luggage, tollbooth passes, credit cards, and animal tags.

Router: A router is a hardware device that routes data from a LAN (local area network) to another network

connection, allowing only authorized machines to connect to other computer systems.

Semiconductor: Semiconductors are the foundation of modern electronics, as devices made of

semiconductors are components essential to most electronic circuits. A semiconductor is a solid substance

that can conduct electricity under certain conditions. The properties of a semiconductor can be modified

based on the impurities added to it and the electrical fields or light applied to it.

Server: A server is a computer that provides data to other computers on a LAN or a WAN (wide area

network) over the Internet. Servers include web servers, mail servers, file servers, and other types of servers,

with each type operating software specific to its purpose. A server also refers to the computer program

running to serve the requests of other programs, known as the clients, by sharing data.

Solder: Solder is a fusible metal alloy used to join together metal workpieces as one solid piece. Soldering is

the process by which metal workpieces are joined via a solder. Electronic soldering is used to connect

electronic components and electrical wiring to PCBs.

Storage Device: A storage device is any type of hardware that stores data. Computer hard drives are the

most common type, with other types including flash memory drives, compact flash cards, and SD cards.

Transistor: A transistor is a basic electrical component that alters the flow of electrical current. The transistor

acts as a switch that can turn a signal on or off by modifying the current between two of its three terminals

(which can connect to other transistors or electrical components). Transistors are the building blocks of ICs.

A series of transistors can also change the amount of current being sent.

Virtualization: Virtualization software enables several operating systems and applications to run on one

physical server (host), creating self-contained virtual machines that act like a real computer. The virtual

machines are isolated from one another and use the host’s computing resources.

Wireless Access Points (Wireless APs): Wireless APs are devices that allow wireless devices to connect to a

wired network using Wi-Fi or related standards. The AP typically connects to a router via a wired network,

but can also be an integral component of a router or wireless modem.

Sources: Techterms.com, www.pc.net, www.wikipedia.org

27 March 2015 — Technology Monitor

Appraisal & Valuation Team

Adam Alexander

President

(818) 884-3737

Ken Bloore

Chief Operating Officer

(818) 884-3737

Paul Arceri

Director

(818) 746-9334

Conrad Van Ryswood

Senior Associate, Technology Specialist

(781) 429-4085

About Great American Group

Great American Group is a leading provider of asset disposition solutions and valuation and appraisal services to a wide range

of retail, wholesale, and industrial clients, as well as lenders, capital providers, private equity investors, and professional

services firms. In addition to the Technology Monitor , GA also provides clients with industry expertise in the form of monitors

for the chemicals and plastics, metals, food, and building products sectors, among many others. For more information, please

visit www.greatamerican.com.

Great American Group, LLC is a wholly owned subsidiary of B. Riley Financial, Inc. (OTCBB: RILY), which provides

collaborative financial services and solutions through several subsidiaries, including: B. Riley & Co. LLC, a leading investment

bank which provides corporate finance, research, and sales & trading to corporate, institutional and high net worth individual

clients; B. Riley Asset Management, LLC, a provider of investment products to institutional and high net worth investors; and

MK Capital Advisors, LLC, a multi-family office practice and wealth management firm focused on the needs of ultra-high net

worth individuals and families.

B. Riley Financial, Inc. is headquartered in Los Angeles with offices in major financial markets throughout the United States

and Europe. For more information on B. Riley Financial, Inc., please visit www.brileyfin.com.

Headquarters

21860 Burbank Blvd. Suite 300 South

Woodland Hills, CA 91367 800-45-GREAT www.greatamerican.com

Mike Marchlik

National Sales & Marketing Director

(818) 746-9306

David Seiden

Executive Vice President, Southeast Region

(770) 551-8114

Ryan Mulcunry

Executive Vice President - Northeast Region, Canada & Europe

(617) 692-8310

Bill Soncini

Senior Vice President, Midwest Region

(312) 777-7945

Drew Jakubek

Managing Director, Southwest Region

(972) 265-7981

Jennie Kim

Vice President, Western Region

(818) 746-9370

Dan Williams

Managing Director, New York Region

(646) 381-9221

Craig A. Ellis

Senior Semiconductor and Capital Equipment Analyst

Co-Director of Research (B. Riley)

(415) 229-4835