technical specification document for nibss …...have a solution that will make bill payments...

TRANSCRIPT

TECHNICAL SPECIFICATION DOCUMENT

FOR

NIBSS ELECTRONIC BILLS PAYMENTS (NIBSS e-BillsPay)

Prepared by: Nigeria Inter – Bank Settlement System (NIBSS) Version: 1.3 July 17, 2013

2

Table of Content

Document Control ............................................................................................................... 3

1. Introduction ............................................................................................................. 4

2. Identification of Delivery Channels .......................................................................... 5

3. Transaction Flow ...................................................................................................... 5

4. Integration Modalities to Banks’ Web – based Channels ........................................ 6

5. Integration Modalities to Banks’ Non – Web – based Channels ............................. 8

6. Message Exchange Security ................................................................................... 17

7. Channel Codes ....................................................................................................... 18

8. Response Codes ..................................................................................................... 18

9. Transaction Settlement .......................................................................................... 19

10. Reports ................................................................................................................... 19

11. Dispute Resolution ................................................................................................. 20

12. Requirements from Banks ..................................................................................... 21

3

Document Control

S/N Document Section Changes Version

1. Section 5 Integration Modalities to Banks’ Non – Web – based Channels

Request for list of biller was updated to accommodate details of products, account numbers and subscriber information Section 5.3 Payment Confirmation Notification was added. Section 5.4 Attributes was removed Section 5.2 Request for Information required by Billers/Merchant and NAB was removed Tag definitions were redefined

1.3

2. Section 8. Response

Codes

New Response Codes were added: 69 Customer Details not successfully validated 70 Notification not successfully received

1.3

4

1. Introduction

There is a growing need for Electronic Payments and with the recent circular from the

Central Bank on Cash Policy banks are providing different infrastructures to meet the

specific needs and requirements of their teeming Billers and Customers. It is desirable to

have a solution that will make Bill payments seamless without the added overhead of

paying at specific physical locations.

NIBSS e-BillsPay is an account-number-based, online real-time Credit Transfer product

that enables customers to make payments by leveraging the security provided by the

banks. It enables banks to provide electronic bills payment services through Payment

Channels such as Branch Tellers, Internet Banking (iB), Mobile Banking and Kiosk, etc.

while leveraging on the security measures provided by these channels with a view to

making payments to signed-up Billers. Specifically, e-BillsPay facilitates three types of

payments namely,

Pay Bill, Fees, Premiums, Subscriptions, Levies, Premiums etc (pre-payments and

post-payments)

Revenue Collections

Purchases

Set up Direct Debit Confirmation in favour of a Biller

Standing Instructions

Other third Party Payments

This document is a specification of how the e-BillsPay is to be integrated to the various

payment channels of banks.

5

2. Identification of Delivery Channels

By delivery channels, we mean the channels that banks are required to provide to their

respective customers for the origination of e-BillsPay transactions. The following are

the typical delivery channels:

i. Branch Teller: On the e-BillsPay platform, bank customers can walk into any

branch of their respective banks, and request for a e-BillsPay service. Such

transfers will be facilitated online real – time i.e value delivered to the

beneficiary instantly. The Branch Teller or Customer Service personnel would

perform the required customer authentication check, just as if the customer

had requested a cash withdrawal.

ii. Internet Banking: Most banks provide internet banking facilities that enable

customers to generate financial transactions e.g. account-to-account transfer

within same bank. Leveraging on the respective banks’ Internet Banking

Customer Authentication (i.e. login name, password, and access token),

banks can now use e-BillsPay to provide OLRT payment of Bill payment

services to customers.

iii. Mobile Payments: Banks would be able to provide bill payment services to their

customers on their respective mobile payment channels, with e-BillsPay.

iv. Kiosks: With e-BillsPay, customers can pay bills to billers using Kiosks. The

payment originator would be authenticated with authentication applicable to

kiosks deployed by such banks.

3. Transaction Flow

Banks are required to provide e-BillsPay on Internet Banking delivery channel at a

minimum, at the commencement of e-BillsPay Live operations. All transactions

originate from the sender’s bank and also terminate at biller’s bank. Assuming a

customer wants to pay bills through internet banking platform, below is the flow:

6

1. The customer logins in with his/her user name and password.

2. NIBSS e-BillsPay Link provided on Internet Banking platform will be clicked by the

customer.

3. This link displays a list of signed up billers the customer can pay to.

4. Once one of the billers in the list is selected, the customer is shown a page

where he/she is expected to enter basic information required by that specific

Biller. Amount will be entered for services with fixed amount; however, in the

case of products/services with variable amount, the customer will be required to

enter the amount.

5. A confirmation page is displayed to the customer where his/her details with the

billers and other information entered are displayed for the customer.

6. Upon confirmation, the customer’s account is debited by the customer’s bank

and a credit leg of the transaction originated and sent via NIBSS Instant

Payments (NIP) to the beneficiary’s bank account.

7. For billers with billing systems, customer account is automatically notified and

updated. Where service has been suspended, the account would be activated

and services made available to customers immediately.

8. And for billers without billing system, alerts (SMS or email) are generated and

sent to such billers.

9. Billers shall be provided remote access to the NIBSS e-BillsPay transaction

database for online real-time enquiries, transaction confirmation, and report

generation.

10. A receipt is displayed to the customer indicating status of transaction. On the

receipt, the customer can enter his/her email address for a copy to be sent to

his/her email. Additionally, the customer can print a copy.

4. Integration Modalities to Banks’ Web – based Channels

NIBSS will enrol billers into e-BillsPay system while the banks will enrol and authenticate

customers on their payment channels and also handle financial aspect of the

7

integration. Banks will provide a hyperlink ‘NIBSS e-BillsPay’ on the home page of their

internet banking platform. This would be hyperlinked to a page NIBSS would provide

with only one parameter passed. This parameter will contain information in the XML

format below in encrypted form (based on NIP Software Security Module (SSM)):

<?xml version="1.0" encoding="UTF-8" ?> <PaymentChannelRequest> <SourceBankCode>0XX</SourceBankCode> <ChannelCode>1</ChannelCode>

<TransactionDateTime>YYMMDDHHmmss</TransactionDateTime> <UniqueNumber>000000000001</UniqueNumber>

<OriginatorName>Victor Iseyemi</OriginatorName> <CustomerAccountNumber>0001234562</CustomerAccountNumber> <EchoData>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</EchoData> <HashValue>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</HashValue> </PaymentChannelRequest>

After the customer has successfully picked the biller of his/her choice and

entered/selected the appropriate information the biller requires to activate his/her

account, NIBSS will pass the following information to the bank’s payment channel in the

XML format below in encrypted form (based on NIP SSM):

<?xml version="1.0" encoding="UTF-8" ?> <PaymentChannelResponse> <SessionID>0XX0YY100913103301000000000001</SessionID> <SourceBankCode>0XX</SourceBankCode> <DestinationBankCode>0YY</DestinationBankCode> <ChannelCode>1</ChannelCode> <CustomerAccountNumber>0001234562</CustomerAccountNumber> <CustomerName>Victor Iseyemi</CustomerName> <BillerAccountNumber>0001234561</BillerAccountNumber> <BillerName>XYZ Nigeria Limited</BillerName> <BillerID>2222222222</BillerID>

<Narration>Payment for Goods</Narration> <Amount>1000.00</Amount> <TransactionFee>100.00</TransactionFee>

<PaymentReference>1111111111</ PaymentReference> <EchoData>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</EchoData> <HashValue>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</HashValue> </PaymentChannelResponse>

8

As soon as debit has occurred and the credit leg of the transaction consummated, the

payment channel is expected to pass the following information in encrypted form

(based on NIP SSM) as a parameter in Hyper Text Transfer Protocol (http) for the display

of a receipt:

<?xml version="1.0" encoding="UTF-8" ?> <PaymentChannelReceipt> <SessionID>0XX0YY100913103301000000000001</SessionID> <EchoData>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</EchoData> <HashValue>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</HashValue> </PaymentChannelReceipt>

The variable name of the parameter to be passed in http is ‘e-BillsPay’.

It is important to note that the Session ID is 30 characters in length and will follow the

format below:

Char 1 – 3: Senders bank’s code

Char 4 – 6: Destination Bank’s code

Char 7 – 18: Date and time (in the format yymmddHHmmss – HH is 24 hour clock)

Char 19 – 30: 12 – character unique number (either serial # or random number)

The amount is the exact figure in two decimal places and without comma to separate

thousands.

The EchoData tag is a tag used to indicate information that is to be returned back to the

source of transaction.

5. Integration Modalities to Banks’ Non – Web – based Channels

This integration is based on Web Services. Methods are exposed for various functions

such as request for list of billers, information required by selected billers/merchants or

9

NAB. Methods accept one input as string and return string as output in XML format.

And both input and output strings are in XML format and fully encrypted with NIP

Software Security Module (SSM). Also, it is important to note that NIP SSM is based on

PGP Encryption standard.

The methods required to be exposed on the Web Services are:

5.1 Request for Billers Details:

This method will be implemented as a notification service from e-BillsPay to Partner

Institution’s interface. This means it is the Partner Institution that is to expose this

method while e-BillsPay is to call it and populate it with its list of Billers/Merchants. This

method will be called periodically (at agreed interval) by e-BillsPay to advise Partner

Institution’s interface of updated list of Billers. The Billers will be sent in batches of a

maximum of fifty (50).

010 Biller List Notification Request:

<?xml version="1.0" encoding="UTF-8" ?> <BillerListNotificationRequest> <Header> <NotificationNumber>120310000000000001</NotificationNumber> <DestinationCode>0XX</DestinationCode> <NumberOfRecords>2</NumberOfRecords> </Header> <Billers> <Biller> <BillerID>0000000001</BillerID> <BillerName>ABC Nigeria Limited</BillerName>

<Products> <Product>

<ProductID>0000000001</ProductID> <ProductName>Product1</ProductName> <Account>

<AccountNumber> 0001234562 </AccountNumber> <AccountName> ABC Nigeria Limited </AccountName> <BankCode>0XX</BankCode>

10

</Account> <Amount>0.00</Amount> <TransactionFee>100.00</TransactionFee>

</Product>

<Product> <ProductID>0000000002</ProductID> <ProductName> Product2 </ProductName> <Account>

<AccountNumber> 0001234562 </AccountNumber> <AccountName> ABC Nigeria Limited </AccountName> <BankCode>0XY</BankCode>

</Account> <Amount>0.00</Amount> <TransactionFee>100.00</TransactionFee> <ProductFormDetail>

<FormDetail> <Title>Customer Maiden Name

</Title> <Type>Alpha</Type> <MaxLength>30</MaxLength> <Required>False</Required>

<DefaultValue></DefaultValue> </FormDetail> <FormDetail>

<Title>Customer Maiden Name </Title>

<Type>Alpha</Type> <MaxLength>30</MaxLength> <Required>False</Required>

<DefaultValue></DefaultValue> </FormDetail>

</ProductFormDetail> </Product>

<Product> <ProductID>0000000003</ProductID> <ProductName> Product3 </ProductName> <Account>

<AccountNumber>0001234562 </AccountNumber> <AccountName> ABC Nigeria Limited </AccountName> <BankCode>0ZY</BankCode>

</Account> <Amount>0.00</Amount>

11

<TransactionFee>100.00</TransactionFee> <ProductFormDetail>

<FormDetail> <Title>Transaction Amount

</Title> <Type>Decimal</Type> <MaxLength>20</MaxLength> <Required>True</Required> <DefaultValue></DefaultValue>

</FormDetail> </ProductFormDetail>

</Product> </Products> <CommonFormDetails>

<FormDetail> <Title>Customer Number</Title> <Type>Numeric</Type> <MaxLength>20</MaxLength> <Required>True</Required> <DefaultValue> </DefaultValue>

</FormDetail> <FormDetail>

<Title>Transaction Amount</Title> <Type> Decimal </Type> <MaxLength>15</MaxLength> <Required>False</Required> <DefaultValue> </DefaultValue>

</FormDetail> </CommonFormDetails>

</Biller> <Biller> <BillerID>0000000002</BillerID> <BillerName>XYZ Nigeria Limited</BillerName>

<Products> <Product> <ProductID>0000000001</ProductID> <ProductName>Product1</ProductName> <Account>

<AccountNumber>0001234571 </AccountNumber> <AccountName>XYZ Nigeria Limited </AccountName> <BankCode>0XX</BankCode>

</Account> <Amount>10000.00</Amount> <TransactionFee>100.00</TransactionFee>

</Product> <Product>

12

<ProductID>0000000002</ProductID> <ProductName> Product2</ProductName> <Account>

<AccountNumber>0001234581 </AccountNumber> <AccountName> XYZ Nigeria Limited </AccountName> <BankCode>0XY</BankCode>

</Account> <Amount>10000.00</Amount> <TransactionFee>100.00</TransactionFee>

</Product> <Product> <ProductID>0000000003</ProductID> <ProductName> Product3</ProductName> <Account>

<AccountNumber>0001234561 </AccountNumber> <AccountName> XYZ Nigeria Limited </AccountName> <BankCode>0ZY</BankCode>

</Account> <Amount>10000.00</Amount> <TransactionFee>100.00</TransactionFee>

</Product> </Products> <CommonFormDetails>

<FormDetail> <Title>Client ID</Title> <Type>Numeric</Type> <MaxLength>10</MaxLength> <Required>True</Required> <DefaultValue> </DefaultValue>

</FormDetail> <FormDetail>

<Title>Transaction Amount</Title> <Type>Decimal </Type> <MaxLength>0</MaxLength> <Required>True</Required> <DefaultValue> </DefaultValue>

</FormDetail> <FormDetail>

<Title>Email Address</Title> <Type>AlphaNumericSymbol</Type> <MaxLength>50</MaxLength> <Required>False</Required> <DefaultValue> </DefaultValue>

</FormDetail>

13

<FormDetail> <Title>Customer Name</Title> <Type>Alpha</Type> <MaxLength>30</MaxLength> <Required>True</Required>

<DefaultValue> </DefaultValue> </FormDetail> <FormDetail>

<Title>Location</Title> <Type>List</Type> <Required>True</Required> <ListItem>

<Item>Lagos</Item> <Item>Kaduna</Item> <Item>Enugu</Item> </ListItem> </FormDetail>

</CommonFormDetails> </Biller> </Billers> </BillerListNotificationRequest>

011 Biller List Notification Response

<?xml version="1.0" encoding="UTF-8" ?> <BillerListNotificationResponse>

<NotifcationNumber>120310000000000001</NotifcationNumber> <DestinationCode>0XX</DestinationCode> <NumberOfRecords>3</NumberOfRecords> <ResponseCode>00</ResponseCode>

</BillerListNotificationResponse>

5.2 Customer Information Validation

This method will be implemented as a notification service from Partner Institution’s

interface to e-BillsPay. This means it is e-BillsPay that is to expose this method while

Partner Institution’s Interface is to call it and notify e-BillsPay of customer information

to be validated with the Biller/Merchant or NAB. This method will be called at the point

of transaction before customer confirms payment by Partner Institution’s interface.

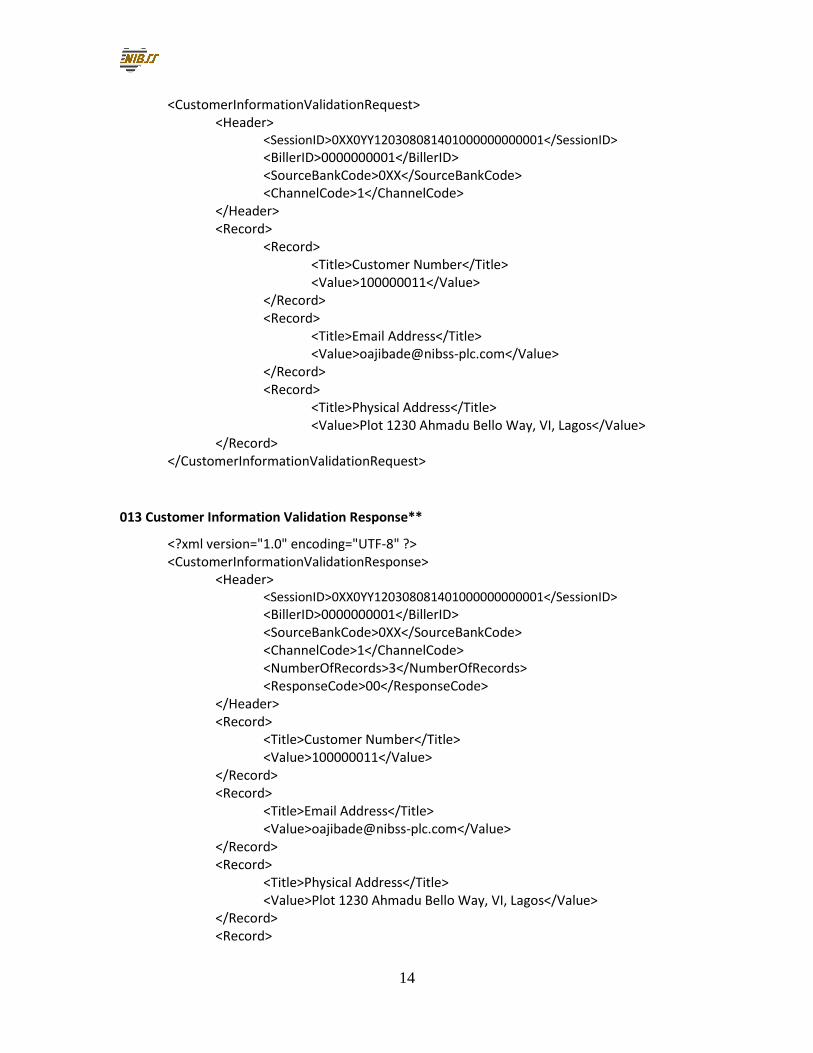

012 Customer Information Validation Request

<?xml version="1.0" encoding="UTF-8" ?>

14

<CustomerInformationValidationRequest> <Header> <SessionID>0XX0YY120308081401000000000001</SessionID>

<BillerID>0000000001</BillerID> <SourceBankCode>0XX</SourceBankCode> <ChannelCode>1</ChannelCode> </Header> <Record> <Record> <Title>Customer Number</Title> <Value>100000011</Value>

</Record> <Record>

<Title>Email Address</Title> <Value>[email protected]</Value>

</Record> <Record>

<Title>Physical Address</Title> <Value>Plot 1230 Ahmadu Bello Way, VI, Lagos</Value>

</Record> </CustomerInformationValidationRequest>

013 Customer Information Validation Response**

<?xml version="1.0" encoding="UTF-8" ?> <CustomerInformationValidationResponse> <Header> <SessionID>0XX0YY120308081401000000000001</SessionID>

<BillerID>0000000001</BillerID> <SourceBankCode>0XX</SourceBankCode> <ChannelCode>1</ChannelCode> <NumberOfRecords>3</NumberOfRecords> <ResponseCode>00</ResponseCode>

</Header> <Record> <Title>Customer Number</Title> <Value>100000011</Value>

</Record> <Record>

<Title>Email Address</Title> <Value>[email protected]</Value>

</Record> <Record>

<Title>Physical Address</Title> <Value>Plot 1230 Ahmadu Bello Way, VI, Lagos</Value>

</Record> <Record>

15

<Title>Service Charge</Title> <Value>100.00</Value>

</Record> <Record>

<Title>Value Added Tax</Title> <Value>5.00</Value>

</Record> <Record>

<Title> Total Transaction Amount </Title> <Value>1105.00</Value>

</Record> </CustomerInformationValidationResponse>

**Please note that additional information can be returned during validation.

5.3 Payment Confirmation Notification

This method will be implemented as a notification service from Partner Institution’s

interface to e-BillsPay. This means it is e-BillsPay that is to expose this method while

Bank’s Interface is to call it and notify e-BillsPay of customer payment details to be

notified to Biller/Merchant or NAB. This method will be called at the end of financial

transaction.

014 Payment Confirmation Request: <?xml version="1.0" encoding="UTF-8" ?>

<CustomerPaymentConfirmationRequest> <SessionID>0XX0YY120312103301000000000001</SessionID>

<ChannelCode>1</ChannelCode> <TransactionID>3061744156218930</TransactionID> <PayerName>Adewale Dora Bala</PayerName> <PaymentAmount>10000.00</PaymentAmount> <SourceBankCode>058</SourceBankCode> <HashValue>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</HashValue>

</CustomerPaymentConfirmationRequest> 015 Payment Confirmation Response:

<?xml version="1.0" encoding="UTF-8" ?> <CustomerPaymentConfirmationResponse>

<SessionID>0XX0YY120312103301000000000001</SessionID> <TransactionID>3061744156218930</TransactionID> <ResponsCode>00</ResponseCode> <HashValue>xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx</HashValue>

16

</CustomerPaymentConfirmationResponse>

5.4 Tag Definitions S/N Tag Definition

1. BillerListNotificationRequest Tag for Biller List Notification request

2. BillerListNotificationResponse Tag for Biller List Notification response

3. CustomerInformationValidationRequest Tag for customer information validation request

4. CustomerInformationValidationResponse Tag for customer information validation response

5. CustomerPaymentConfirmationRequest Tag for customer payment confirmation request

6. CustomerPaymentConfirmationResponse Tag for customer payment confirmation response

7. Header Contains information common to all records in a batch

8. NotificationNumber Number identifying notification

9. DestinationCode Code identifying the destination of transaction

10. NumberOfRecords Number of records in a batch

Billers Tag for list of Billers

Biller Tag for record of each biller

11. BillerID Number identifying a biller

12. BillerName Name of biller

13. Products Tag for a collection of products

14. Product Tag for record of each products

15. ProductID Number identifying a product

16. ProductName Name of product

17. Account Tag for a record of Account details

18. AccountNumber Bank Account number of Biller where fund is to be remitted to

19. AccountName Bank Account Name of Biller

20. BankCode Code identifying bank of Biller

21 Amount Transaction expressed in two decimal places with the following conditions:

1. If amount is greater than zero, amount is attached to product

2. If amount is zero then customer need to enter amount

22. TransactionFee Fee charged per transaction

23. CommonFormDetail Tag for collection of form details. Whenever there are no common fields among the product, this field is empty but

17

present.

24. ProductFormDetail Tag for collection of form details specific to a product. If there are no fields specific to a product, this tag is empty but present.

25. FormDetail Tag for each record of fields of information subscriber/customer is to provide.

26. Title Name of an item in a record

27. Required Condition for if record is mandatory or optional. It has too values:

1. True: Mandatory required. 2. False: optionally required.

28. Type Data type of an item in a record. Possible values are:

1. Numeric: all numbers 2. Decimal: floating type to two(2)

decimal points 3. Alpha: all alphabets 4. AlphaNumericSymbol: could

contain alphabets, numbers or special symbols

5. ***List: records of values from which a customer/subscriber can select from.

***whenever value of Type is “List”, tags MaxLength and DefaultValue will be absent

29. MaxLength Maximum length of a value in a record. When not applicable, it is zero (0).

30. DefaultValue Value of a record set by default

31. ListItem Tag for collection of lists

32. Item Tag for records of list type record

33. SourceBankCode Bank Code of Subscriber or payer

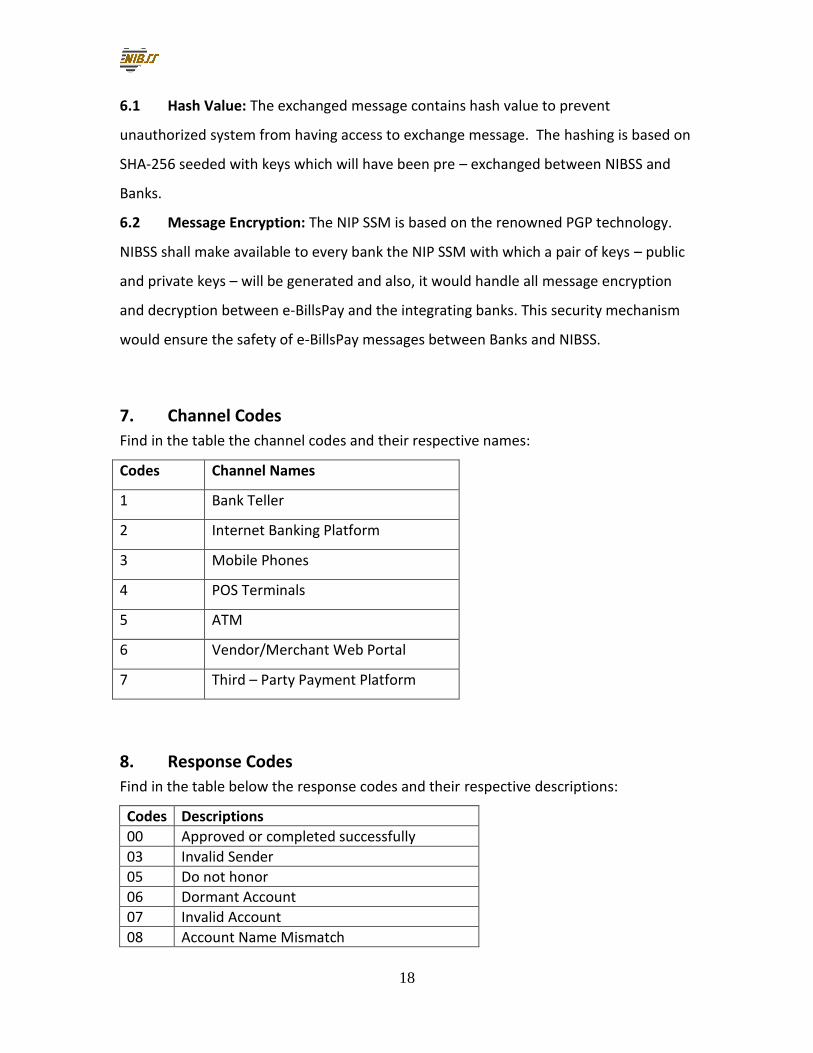

6. Message Exchange Security

There are two (2) levels of security:

18

6.1 Hash Value: The exchanged message contains hash value to prevent

unauthorized system from having access to exchange message. The hashing is based on

SHA-256 seeded with keys which will have been pre – exchanged between NIBSS and

Banks.

6.2 Message Encryption: The NIP SSM is based on the renowned PGP technology.

NIBSS shall make available to every bank the NIP SSM with which a pair of keys – public

and private keys – will be generated and also, it would handle all message encryption

and decryption between e-BillsPay and the integrating banks. This security mechanism

would ensure the safety of e-BillsPay messages between Banks and NIBSS.

7. Channel Codes

Find in the table the channel codes and their respective names:

Codes Channel Names

1 Bank Teller

2 Internet Banking Platform

3 Mobile Phones

4 POS Terminals

5 ATM

6 Vendor/Merchant Web Portal

7 Third – Party Payment Platform

8. Response Codes

Find in the table below the response codes and their respective descriptions:

Codes Descriptions

00 Approved or completed successfully

03 Invalid Sender

05 Do not honor

06 Dormant Account

07 Invalid Account

08 Account Name Mismatch

19

09 Request processing in progress

12 Invalid transaction

13 Invalid Amount

14 Invalid Batch Number

15 Invalid Session or Record ID

16 Unknown Bank Code

17 Invalid Channel

18 Wrong Method Call

21 No action taken

25 Unable to locate record

26 Duplicate record

30 Format error

34 Suspected fraud

35 Contact sending bank

51 No sufficient funds

57 Transaction not permitted to sender

58 Transaction not permitted on channel

61 Transfer limit Exceeded

63 Security violation

65 Exceeds withdrawal frequency

68 Response received too late

69 Customer Details not successfully validated

70 Notification not successfully received

91 Beneficiary Bank not available

92 Routing error

94 Duplicate transaction

96 System malfunction

9. Transaction Settlement

Settlement of all transactions will be done once in a day and at a cut – over time of 2pm.

NIBSS will handle the settlement of all transactions that passes through the e-BillsPay,

and effect settlement on a next-day basis as it is done with card payments.

10. Reports

e-BillsPay shall make available transaction reports to both the Collecting & Billers’ Banks

and billers at the end of every settlement cycle. The reports would be made available on

the operational web – based NIBSS Financial Reports Delivery Platform.

20

11. Dispute Resolution

Dispute Resolution will be based on the Procedure below:

a. The Sender lodges complaint(s) with his/her bank.

b. The Sender’s bank performs first level check such as:

i. Authenticate Sender ii. Confirms that account was debited

iii. Checks for auto-reversal iv. Is Transaction in Store and Forward repository etc

c. Based on the first – level check ascertaining that the dispute is indeed genuine,

the sender’s bank logs the issue on the NIP Dispute Resolution System (DSR).

d. DSR stores the disputes and alerts the Beneficiary’s Bank.

e. The Beneficiary’s Bank receives the alert and verifies dispute from the

transaction traces and logs.

f. The Beneficiary’s Bank through the DSR responds with a ‘complaint valid’ or

‘complaint invalid’.

g. If response is not received from the Beneficiary’s Bank within 72 hours, NIBSS

would recover the contested fund automatically from the Beneficiary’s Bank

back to the Sender’s Bank.

h. If the response from the Beneficiary’s Bank is ‘complaint invalid’, no further

action will be taken. However, if there is a repeat lodgement by the Sender’s

Bank of this complaint, it would be referred to Arbitration Panel (comprising

representatives of the two banks of involved and NIBSS) for resolution and the

decision of the Panel will be final.

i. If the response from the Beneficiary’s Bank is ‘complain valid’, it would notify the

DRS which, would based on this instruction, recover funds from the Beneficiary’s

Bank to the Sender’s Bank for final disbursement to the Sender.

21

12. Requirements from Banks

For integration to e-BillsPay, the following will be required from Banks:

1. Integration to the Nigeria Central Switch (NCS) Infrastructure.

2. Integration to the NIBSS Instant Payment (NIP) Infrastructure.

3. Development of required interface on Internet Banking Platform as specified in

Section 4 above.

4. Banks are required to provide NIBSS e-BillsPay interfaces on their internet

banking channel at the minimum. NIBSS would readily provide assistance and

support to banks, where necessary.