technical assistance consultant’s report · tenaga listrik), developing new and renewable energy...

TRANSCRIPT

Technical Assistance Consultant’s Report

This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents.

Project Number: 48323-001 January 2018

Republic of Indonesia: Sustainable and Inclusive Energy Program (Financed by the Agence Française de Développement and the

Technical Assistance Special Fund)

Appendix E: PLN PV Procurement Workshop Support Appendix F: Renewable Incentives FGD 1—Current Policies Appendix G: Renewable Incentives FGD 2—Financing Gaps

Prepared by Castlerock Consulting, Indonesia in association with Economic Consulting Associates Ltd, United Kingdom and PT. Q Energy South East Asia, Indonesia

For Coordinating Ministry for Economic Affairs Ministry of Energy and Mineral Resources Ministry of Finance Perusahaan Listrik Negara

E-1

SIEP Final Report – January 2018

APPENDIX E: PLN PV PROCUREMENT WORKSHOP REPORT

REPORT Technical Assistance to PLN: Workshop on Solar PV Procurement 23-24 May 2017

E-2

Acknowledgement This report was prepared by Castlerock Consulting under a policy and technical assistance grant administered by the Asian Development Bank (ADB): Sustainable and Inclusive Energy Program (PATA 8826-INO). Inputs were provided by PT Synergy Engineering, Mott MacDonald, and Hadiputranto, Hadinoto and Partners. Disclaimer The views expressed in this publication are those of the authors and do not necessarily reflect the views and policies of the Asian Development Bank (ADB) or its Board of Governors or the governments they represent. ADB does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequence of their use. The mention of specific companies or products of manufacturers does not imply that they are endorsed or recommended by ADB in preference to others of a similar nature that are not mentioned. By making any designation of or reference to a particular territory or geographic area, or by using the term “country” in this document, ADB does not intend to make any judgments as to the legal or other status of any territory or area.

E-3

Executive Summary Under Government Regulation No. 79 of 2014 on the National Energy Policy, the Government of Indonesia has targeted new and renewable energy to provide 23% of primary energy needs by 2025 (up from 6% in 2015). This target has been reaffirmed in the National Energy Plan signed by President Joko Widodo in January 2017. In addition, the country’s Nationally Determined Contribution to the Paris Agreement of 2015 calls for a 29% reduction greenhouse gas emission by 2030. As the state-owned enterprise for electricity supply, PLN (Perusahaan Listrik Negara – State Electricity Company) has planned accordingly to develop electricity by utilizing renewable energy. As stated in the Electricity Supply Business Plan (Rencana Usaha Penyediaan Tenaga Listrik, RUPTL) 2017-2026, PLN plans to expand electricity generation capacity to fulfill demand growth and to increase their supply by utilizing local energy resources, especially renewable energy. By November 2016, total installed capacity of generation in Indonesia had reached 51,915 MW which consists of PLN-owned generation of 39,859 MW, independent power producer (IPP)-owned generation of 8,867 MW and rented generation of 3,192 MW. Out of this total, 44% of total capacity is from coal power plants, 29.3% from gas power plants, 11.1% from diesel power plants, 8.9% from hydro power plants, 3.2% from oil-steamed power plants, 2.6% from geothermal, and 0.2% from various renewable energy. In January 2017, the Ministry of Energy and Mineral Resources (MEMR) issued broad-based guidelines for purchasing electricity from renewable energy sources. Ministerial Regulation MEMR (Peraturan Menteri Energi dan Sumber Daya Mineral, Permen ESDM) No.12/2017 establishes pricing and selection guidance for all forms of renewable energy (including solar photovoltaic, wind, hydropower, biomass, biogas, municipal waste, and geothermal). This regulation requires PLN to purchase electricity from renewable sources with reference to national targets, prioritize the dispatch of renewable-based generation projects below 10 megawatts (MW) as “must-run” plants, and develop standardized procurement documents and power purchase agreements (PPAs). It requires tendering of wind and solar projects in in packages of at least 15 MW each and provides a benchmark price for all renewable generation technologies. The state-owned electricity corporation, PLN, plans to issue several tenders for solar and wind power procurement under this new regulation in the coming months, representing the first large-scale tenders for renewables in the country. The first tender will be for a combined 167 MW of solar power plants in Sumatera. The benchmark price will be tied to local average cost of generation (Biaya Pokok Penyediaan, BPP), which is approximately USD 7 cents/kWh. PLN plans to subsequently tender solar packages for Kalimantan, Maluku and Papua, and West Java. As stipulated by Permen ESDM 12/2017, PLN is also preparing standard power purchase agreements (PPAs) and standard bidding documents. As part of on-going assistance for clean energy development, ADB, in collaboration with AFD, has been providing support to PLN with tender preparation. ADB conducted a one-week consultation with PLN with a team comprising a solar PV specialist, power system planner, and other specialists in Jakarta. The workshop was designed to help PLN have a better understanding of solar PV procurement. It covered grid connection issues, solar PV development issues, and commercial

E-4

and legal issues. The workshop was followed up by one day of in-depth one-on-one consultations between PLN engineers and the consultants. Representatives from PLN Headquarters and Regional Offices attended the workshop and one-on-one consultations. Representatives from ADB and AFD also attended the series of activities. The main findings from the workshop are as follows:

The effectiveness of solar PV procurement is still an issue for PLN. The grid code and distribution code do not adequately address renewable energy integration, particularly given the intermittent nature of wind and PV power generation.

The selection of projects was largely conducted in an ad hoc manner, with the bolstering of areas with forecast power deficits being the main criterion for project selection. As a result, many projects do not appear to be technically feasible due to grid conditions.

PLN has not conducted any grid-connected solar PV procurement to date. The rationale and objectives of the solar procurement seems unclear for some PLN Regional Office staff.

PLN seeks performance guarantees from IPPs, but guaranteeing energy production from solar and other intermittent power projects is not possible due to their intermittent and uncertain nature. For solar PV, PLN’s PPA instead works on the basis of guaranteeing plant capacity under defined operating conditions. However, this approach is not used elsewhere in the world.

E-5

SIEP Final Report – January 2018

Contents Executive Summary ......................................................................................................... E-3 Introduction ...................................................................................................................... E-6

Background .................................................................................................................. E-6 Objective ...................................................................................................................... E-6 Proposed Assistance ................................................................................................... E-6 Agenda ......................................................................................................................... E-7

Presentation ..................................................................................................................... E-7 Integration of Intermittent Renewable Power Plant in Power System Planning ........... E-7 Grid Impact Studies for Integrating Utility Scale Solar PV into PLN Networks ............. E-8 Solar PV Generation in the Region .............................................................................. E-8 Solar Development Challenges in Indonesia ............................................................... E-9 Procurement of Solar PV Projects ............................................................................. E-10 Solar PV Power Purchase Agreement ....................................................................... E-10

Findings ......................................................................................................................... E-11 Recommendation for next step ...................................................................................... E-12 Appendix 1: Workshop’s Agenda ................................................................................... E-14 Appendix 2: Workshop’s Documentation ....................................................................... E-16

E-6

Introduction

Background 1. The Government of Indonesia recognizes that a climate-friendly social and economic development path is a key factor for sustainable development. The government has set the target to reduce emissions by 29% by 2030, and this reduction could reach 41% subject to availability of international support. In addition, the government has set an ambitious target of 23% of renewable energy share in its primary energy mix by 2025 in the 2014 National Energy Policy, which has been reaffirmed in the National Energy Plan. To increase renewable energy production in the electricity mix, the Ministry of Energy and Mineral Resources (MEMR) of the Republic of Indonesia stipulated Ministerial Regulation No. 12/2017 on Utilization of Renewable Energy Resources for Electricity Supply. 2. According to the Electricity Law No. 30/2009, the government is obliged to control the electricity supply. Through national electricity company Perusahaan Listrik Negara (PLN), the government controls electricity supply, distribution, and demand. Ministerial Regulation No.12/2017 also mandates (i) PLN to purchase electricity from renewable energy generators to achieve the targeted energy mix and electrification targets, and (ii) the manner in which PLN may procure electricity supply from various renewable energy resources. 3. In PLN’s Electricity Supply Business Plan (RUPTL, Rencana Usaha Penyediaan Tenaga Listrik), developing new and renewable energy is one of PLN’s policy objectives. Therefore, PLN is planning to develop new and renewable energy in the form of geothermal, hydro, wind, solar, and bioenergy. Furthermore, PLN is obliged to treat renewable energy projects with a capacity below 10MW as “must run” plants. PLN must procure solar PV and wind projects through open tender. Adequate preparation of the tender process is the key to achieve positive outcomes and low prices. The required preparation includes (i) technical analysis (i.e. resource quality analysis and grid studies), and (ii) commercial analysis. However, PLN has only limited resources and capacity to develop proper criteria based on technical and commercial studies.

Objective 4. The Asian Development Bank (ADB) and Agence Francaise de Developpment (AFD) are jointly providing technical assistance to PLN to support the renewable energy procurement preparation. The objective of the support is as follows: a. To improve PLN’s knowledge on renewable energy tendering preparation b. To improve the capacity of PLN’s staff on the tendering process. c. To provide PLN with methods and support to evaluate the suitability of particular

sites for solar PV development from the standpoint of grid conditions. d. To provide inputs for preparation of a standard power purchase agreement (PPA)

and standard bidding documents in purchasing renewable energy by PLN.

Proposed Assistance 5. ADB-AFD initiated the assistance with a 3-day consultation with a team comprising: Solar PV Specialist Power System Planner Other specialists (legal expert, renewable energy tender specialist) 6. The assistance included a one-day workshop, covering technical issues and commercial issues on solar PV procurement process.

E-7

7. Key technical and commercial issues for PLN were discussed during the workshop. This covered grid integration (injection from renewable energy and stability), technical and economic criteria for tendering, and key aspects in the PPA for renewable energy. Lessons learned from renewable energy procurement, primarily solar PV, from selected countries were presented as well. This aims to increase PLN’s knowledge on solar PV so they can prepare proper tendering processes and criteria in the future.

Agenda 8. The assistance was conducted in 4th week of May (please see attachment 1 for detailed agenda), with detailed scheduled as follows: 22 May – Afternoon – Kickoff meeting within the team to discuss issues 23 May – workshop at PLN on solar PV procurement – technical and commercial

issues 24 May – detailed one-on-one consultations in small groups at PLN - with engineers

from PLN Wilayahs and Pusat.

Presentations

Integration of Intermittent Renewable Power Plant in Power System Planning 9. Renewable energy (RE) penetration into power systems globally will continue to grow rapidly as has been forecasted by the International Energy Agency in their Energy Outlook 2015, as well as BP in their energy outlook. Both analyses show that renewable energy will be the highest growth in electricity power production compared to other types of primary energy resources. One of the reasons for this is the declining price of RE, mainly solar and wind. A defining characteristic of RE is energy from a sustainable natural resource, but production is intermittent, which makes RE more difficult to integrate into power systems. 10. Economic evaluation of RE rests mainly on the capital expense as operation and maintenance expense is minor. Economic evaluation will depend principally on construction cost, and its economic life and discount rate, which reflects the cost of financing. Other important parameters that must be considered are availability of RE resources and their characteristics. This will determine the productivity of RE. 11. RE resource availability will determine the energy that is produced, hence it will determine the economic viability as well. There are several publicly available sources of information on resource availability but they are usually not as detailed and accurate as needed for an in-depth, investment-grade analysis. At least using this information, we can estimate and approach the characteristic.

12. One such source of information is the Energy Sector Management Assistance Program (ESMAP) World Solar Irradiation Atlas (http://globalsolaratlas.info/). This site provides average solar irradiation around the world with 1 km-sq resolution. This allows us to estimate production of a solar power plant anywhere in the world.

13. Intermittency is one challenge that must be considered when integrating RE into power systems. There are several mitigations that are available and implementable for RE intermittency. These include site size limitation, multiple site diversity, storage, fast response conventional generation elsewhere on the grid and forecasting of RE output. These mitigations will be more effective if supported by regulation, such as grid and distribution code. 14. There are several simulation tools for integrating RE into power system capacity expansion planning. One of the simulation tools is PLEXOS Simulator by Energy Exemplar.

E-8

This simulation will optimize capacity planning (long term), create a production simulation by optimizing available resources, and show chronologic dispatch of each power plant. 15. Sumba Island was used as a case study in the presentation. Data on solar and wind have hourly resolution for 1 year and were extended into 10 years of simulation time. Results of the simulation show that a combination of RE (solar & wind) and fossil energy (gas engine) is needed in Sumba. This shows that fossil fuel is still needed, while RE will minimize the consumption of LNG. Fossil fuel is still needed for supporting capacity need, while RE will support on energy need. This sort of capacity expansion planning should be followed by grid impact studies.

Grid Impact Studies for Integrating Utility Scale Solar PV into PLN Networks 16. This presentation describes a structured approach to performing grid impact studies for the interconnection of utility scale solar PV into PLN’s networks. Because PLN is responsible for hundreds of separate electricity grids around Indonesia, a single “one size fits all” approach and assessment criteria is neither practical nor advisable. Rather, the concept of “weak” and “strong” grid connections are introduced taking into account the characteristics of the network relative to the power plant to be connected. 17. Weak grid connections are subdivided into high impedance and low inertia connection points. A weak high impedance connection point is one that has a Short Circuit Ratio (SCR) of less than 3 (as per IEEE Std 1204). These types of connection points are typically characterized by long radial upstream feeders and low short circuit levels, leading to issues relating to voltage regulation / stability and increases in active power losses. 18. A weak low inertia connection point is associated with the connection of a large power plant relative to the frequency response characteristics of the system, i.e. the power plant has a large influence on the frequency of the system. It is proposed that a connection point is weak if the Stiffness Ratio (SR) is less than 4. Low inertia connection points are typically associated with small isolated power systems with a high mix of diesel or gas engine generator capacity (i.e. low inertia machines). The key issues surrounding low inertia connection points are frequency stability and issues with conventional generator dispatch and loading (such as maintaining minimum machine loading and spinning reserve). 19. Lastly, strong connection points are those that have SCR >3 and SR >4. In such cases, there are no major issues foreseen in the connection of solar PV plants and standard grid impact studies apply for checking the evacuation of the power to the grid and short circuit contributions.

Solar PV Generation in the Region 20. Despite huge resources and ambitious national and regional targets, uptake of solar in South East Asia (SEA) has been limited so far. The main barriers identified so far include:

– Data availability for preliminary assessments, – Grid connection and integration, – Access to land, – Regulatory frameworks (complex, frequently changing), – Perception of high cost still exists, – Very short timelines for bid preparations, – Local content expectations, – Access to financing, – Poor track record of some projects.

E-9

21. These barriers can be overcome by an adequate procurement approach and lessons learned from existing projects in the region. Various approaches that could be applied to minimize the cost of energy in equatorial regions include the following:

– Optimisation of DC/AC ratio – East / East-West facing orientation – Layout optimization for complex terrain – Component selection based on latest technical developments and the site

conditions. 22. Procurement rules should allow new trends that provide value for money, as long as they don’t compromise the robustness of the projects. Current engineering, procurement and construction (EPC) cost in SEA region is ~USD 1,000/kWp for utility scale projects with good access. A very clear downward trend in cost can be observed, but conditions vary greatly and so do costs. All technical and commercial elements need to be considered when comparing tariffs achieved internationally (as evident from the comparison between Dubai and Indonesia projects):

– Irradiation – Economies of scale – Local content restrictions – Land cost – Responsibility for grid interconnection costs – Taxes and import duties – Country, currency and off-taker risk – Financing costs, and – PPA term and escalation provisions

Solar Development Challenges in Indonesia 23. Solar resource estimation is not yet mature for the Indonesian context. It is necessary to consider both ground-measured and satellite-derived data to ensure confidence in revenue estimates, to capture (i) long-term climate; (ii) modelling uncertainty; (iii) microclimate effects; and (iv) any impacts from air pollution. 24. BMKG (Indonesia Agency for Meteorology, Climatology and Geophysics) has more than 60 meteorological stations with solar irradiation measurements. However, this information is not easily accessible to developers and consultants and its quality needs to be assessed. 25. Adequate site assessment is key for a successful project. Logistics can have a huge impact on the delivery of the project and need to be factored in the design and procurement. 26. Lessons from elsewhere in the SEA region regarding design and equipment selection remain relevant, for example:

– Material selection to avoid corrosion, – Enclosures for electrical components adequate for high temperatures and

humidity, – Flood mitigation and drainage design,

27. During operations, inverter outages are typically the key revenue risk under plant owner control:

– Nuisance trips from low isolation resistance, particularly during damp periods (e.g. from DC cable selection; damage to cable insulation; poorly specified ducting; inadequate drainage),

– Nuisance trips due to over-voltage and/or coordination of settings (e.g. for varied AC cable lengths),

– Lack of local maintenance or spares storage base, particularly for inverter suppliers without a prior installed base in the country.

E-10

28. Grid-related constraints on power sales remains a central concern for island networks (this was discussed in more detail by the other presenters).

Procurement of Solar PV Projects 29. Auctions represent best practice for RE procurement, providing price discovery and control over volumes and cost. Auction risks can be managed by adequate selection of design features: demand, qualification requirements, winner selection and seller liabilities. There is no single formula for successful auctions, but ensuring competition is key. 30. Valuable lessons learned from South African REIPPP, Scaling Solar and Kenyan auctions study were discussed. A multi-stage, solar specific auction seems appropriate as a first step in Indonesia. The option of pre-selected sites or at least pre-selected area/connection substation should be explored.

Solar PV Power Purchase Agreement 31. The presentation highlights the Indonesian solar power purchase agreement, which is a new model power purchase agreement and relatively different compared to the previously issued model agreement in 2013. 32. The presentation first covered the contractual structure and objectives of a power purchase agreement and the roles of the parties involved in a power project in order to get a general understanding where a power purchase agreement sits and why it is an important project document. 33. The presentation points out key terms of a power purchase agreement as they relate to different stages of the project, such as construction, operation, and power supply. Under the terms of the power purchase agreement, an IPP would be required to construct a power plant and the transmission line, and be ready to operate by a certain targeted commercial operation date. The contract will also define consequences of delay, force majeure, term and termination etc. 34. The solar power purchase agreement introduced by PLN suggests key differences in terms of supply guarantee from other power purchase agreements. For example, in thermal PPAs, energy supply guarantee is possible due to constant fuel source, whilst for solar power purchase agreement, it is impossible for the IPP to guarantee if the sun will shine or for how long, and therefore, a guarantee is feasible only with respect to plant capacity under defined operating conditions. However, this type of guarantee is not used elsewhere in the world; elsewhere it is accepted that PV is intermittent and projects are sized and located so that the system can compensate for variation in output. The presentation also addresses the differences in the tariff components for solar power projects where it only comprises components A (capital cost recovery), B (fixed and variable O&M) and C (transmission line capital cost recovery). 35. The presentation further addresses the key concerns relating to Regulation of the Minister of Energy and Mineral Resources No. 10 of 2017 on the terms of a power purchase agreement ("Reg 10"), which does not apply to solar projects, but PLN indicates that it wants to follow the same principles under Reg 10 for solar power purchase agreements. Some of the key concerns are relating to the build-own-operate-transfer (BOOT) model, Force Majeure conditions (PLN is relieved of payment obligations where PLN cannot take power due to (natural) Force Majeure, thereby PLN shifts government force majeure risk to power developers), and the take or pay period, which should be set by taking into account the debt period.

E-11

Findings 36. The following points are the findings from the workshop and one-on-one consultations with PLN’s staff:

Planning departments from the PLN Wilayahs were given the responsibility to select the quotas and projects (capacity and location) for the upcoming solar PV tenders.

From discussions with planning staff, the selection of projects was largely conducted in an ad hoc manner, with the bolstering of areas with forecast power deficits being the main criterion for project selection. As a result, there are many projects that do not appear to be technically feasible since the local grid conditions were not assessed.

No technical assessment studies were performed for the selection of the solar PV projects. It appears that PLN has no simulation models for most of the smaller isolated grids.

During the breakout session, the Sumatera projects were categorized into Strong, Weak (Low Inertia) and Weak (High Impedance) connections based on a preliminary screening. PLN will follow up by collecting the required technical data to conduct a more detailed evaluation.

The participants from procurement divisions were new and had never done any procurement to date. They expect that the solar procurement would be rolled-out in Java next year.

The rationale and objectives of the solar procurement seem unclear to some PLN staff. The workshop was useful to share knowledge and increase buy-in among stakeholders.

The allocation of capacity for the announced solar tenders is decided by the planning teams of each Wilayah. It appears that the solar capacity is selected only based on a simple threshold (e.g. no more than 5% of the total peak generation capacity in each system). It seems that no specific grid studies are being conducted to select the capacity allocation or the interconnection point of the projects.

An area of concern for the participants (shared by the consultant team) is the feasibility of interconnection and dispatch of future solar PV projects.

Procurement documents were not available for review by the consultant, and the below findings are purely based on verbal communications from PLN, which in some cases presented some contradictions.

The basic structure of the procurement seems reasonable with a staged process: prequalification (PQ) and request for proposal (RFP) stage; and multi-round approach: one region first and then lessons learned to be applied to next regions.

The PQ is focused on the capabilities of the prospective bidders to develop, build and operate the project. It includes legal, financial and track-record requirements.

The RFP package seems to be still under preparation. The contents of the RFP are unclear; it was mentioned that it includes a draft PPA, details of the project sites and the point of interconnection. However, based on subsequent discussions, it seems that the last two items are actually not included.

The evaluation is based on a combined technical and financial score. The weights are not clear at this stage but in other PLN procurement processes the technical component can have up to a 60% weight.

E-12

The tender timelines are challenging for the bidders, with one week to respond to the PQ and one month to respond to the RFP. Considering that the prequalified bidders are provided with little information (no solar data, no interconnection study) and that the project site is not pre-selected by PLN, one month seems insufficient to prepare a well-informed proposal.

There is a local content requirement in the tender process. While this is feasible for some components and beneficial to develop local industry, it should be carefully considered not to affect the competitiveness. At the moment, it would seem that the PV module local content requirement effectively means that there is only one possible Tier 1 supplier.

The documentation of the Scaling Solar initiative was shown to the participants, with particular focus on the up-front advisory work to select the project site, define the project capacity and the technical limits of the interconnection; and the Minimum Functional Specifications.

Guaranteeing supply of energy for solar and other intermittent power projects is not possible for intermittent power project, and the possible approach is by way of guaranteeing the plant capacity under defined operating conditions (Though this is not used elsewhere in the world. Elsewhere PV projects are sized and located so that the power system can accommodate the variability of PV output);

The relief of PLN's payment obligation due to PLN’s inability to take power caused by a force majeure event and the shifting government force majeure risk to developers are major bankability concerns;

There is no restriction for PLN to set take or pay at full term of PPA; and There is no regulatory requirement for solar projects to be set on a BOOT

basis;

Recommendations for next steps 37. PLN is undertaking significant efforts to increase the uptake of solar in their system. The upcoming tenders show some positive features, but the overall impression is that they might not attract enough competition; bidders will be pricing the risks/uncertainties associated in the absence of information, and the lack of upfront grid impact/interconnection studies may compromise the feasibility of some projects. 38. Throughout our interactions during the workshop we have identified several areas of future work. Below are some proposed follow-up actions which could be supported by ADB-AFD and carried out by independent consultants:

Assist PLN with technical evaluation of projects already selected for upcoming solar PV tenders (starting with the Sumatera tender packages) when all data is collected

Assist PLN with developing clearly defined assessment criteria and framework for conducting grid impact studies. The studies can be further developed into integration of intermittent RE in power system planning, penetration level of intermittent RE, and mitigation of intermittency studies.

Assist PLN with developing the grid code and updated distribution code for renewable energy integration.

PLN (or a consultant) to conduct whole of system studies for each of the major grids (e.g. Sumatera interconnected system, Jawa-Bali, etc.) that incorporates all intermittent power plants in the system. This is done to determine system-level limits for solar PV and wind penetration.

E-13

Solar resource: the solar irradiation data recorded by BMKG meteorologicalstations is currently not accessible. Technical support to compile, assess and makethis data easily available would significantly benefit solar development in thecountry.

Tender documents: independent review and update of the current tender designand the existing tender documents: RFQ, RFP (project agreements, studies,technical requirements) and evaluation criteria.

Grid integration, as elaborated by other presenters:o Review and update of Grid Code for integration of intermittent renewable

energy generation;o System studies for each of the major grids to determine potential

penetration of renewables.

Terms of reference for upfront work required to define project sites, project capacityand technical limits of the interconnection of future tender processes.

Capacity building within the relevant PLN teams on procurement, solar/wind energyand grid impact studies.

In order to promote and support for the development of solar power projects, PLNshould consider adopting a model of power purchase agreement that applies riskallocation principles, and removing the major bankability concerns raised by Reg10;

There must be an integrated view and actions taken by the Government, PLN andstakeholders in respect of solar projects development and for this purpose, it isimportant for the Government to issue an implementing regulation that governs thedevelopment of intermittent power projects.

E-14

Appendix 1: Workshop’s Agenda ADB-AFD Support to PLN on RE Procurement Venue: PLN Pusat, Jakarta, Indonesia Participants: Representatives from PLN Pusat and PLN Wilayah Date: May 22, 2017

Time Agenda Speaker 13.00 pm – 15.00 pm

Kickoff meeting representatives from ADB, AFD, and PLN

Led by Toru Kubo Asian Development Bank

Date: May 23, 2017

Time Agenda Speaker 9.00 am – 9.30 am

Registration

9.30 am – 10.30 am

Session 1: Grid impacts on integrating renewable energy

9.30 – 10.00 am Integration of renewable power in system planning

I Made Rosakya Castlerock Consulting

10.00 – 10.30 am

Grid impact studies for integrating utility-scale solar PV plants into PLN networks

Dharma Susanto Castlerock Consulting

10.30 – 10.45 am

Coffee/Tea Break

10.45 – 12.15 pm

Session 2: Solar PV Development

10.45 – 11.15 am

Solar PV generation in the region Mr. Inaki Perez Solar Team Leader, Mott MacDonald

11.15 – 11.45 am

Solar development challenges in Indonesia

Mr. Inaki Perez Solar Team Leader, Mott MacDonald

11.45 – 12.15 pm

Solar procurement program Mr. Inaki Perez Solar Team Leader, Mott MacDonald

12.15 – 1.30 pm Lunch Break 1.30 - 2.30 pm Session 3: Legal and commercial issues 1.30 - 2.00 pm Legal issues on solar PV

development Baker MacKenzie

2.00 – 2.30 pm Commercial issues Baker MacKenzie 2.30 – 2.45 pm Coffee/Tea Break 2.45 – 3.45 pm Q&A Session

Date: May 24, 2017

Time Agenda Speaker 8.30 – 09.00 am

Registration

09.00 – 10.30 am

One-on-one consultation on solar pv development Resource person: Inaki Perez, Mott McDonald

10.30 – 12.00 pm

One-on-one consultation on grid impacts Resource person: Castlerock Consulting

E-15

Time Agenda Speaker 8.30 – 09.00 am

Registration

12.00 – 1.00 pm

Lunch Break

1.00 – 3.00 pm One-on-one consultation on legal and commercial issues Resource Person: Baker MacKenzie

E-16

Appendix 2: Workshop’s Documentation

E-17

F-1

SIEP Final Report – January 2018

APPENDIX F: RENEWABLE INCENTIVES FGD 1 – CURRENT POLICIES

This appendix contains four presentations from MEMR, DEN, INDEF and BKPM which is presented during the first FGD. The first FGD mainly discuss about the current policy in Indonesia's RE sector.

These presentations are provided below.

KEMENTERIANESDM1

KEMENTERIAN ENERGI DAN SUMBER DAYA MINERALDIREKTORAT JENDERAL ENERGI BARU TERBARUKAN DAN KONSERVASI ENERGI

FGD Percepatan Investasi Energi Terbarukan, Jakarta 31 Juli 2017KEMENTERIANESDM

2

Outline

I. Kebijakan dan Peraturan Pengembangan EBTKE 3

II. Potensi dan Target Penyediaan Energi Primer EBT 5

III. Pengembangan Energi Terbarukan berdasarkan RUPTL dan Roadmap EBT 7

IV. Penyederhanaan Perizinan dan Insentif 10

V. Upaya Pengembangan EBT 13

VI. Tantangan dan Kemitraan Strategis 16

KEMENTERIANESDM3

Proses bisnis yang semakin jelas, terukur,sederhana dan cepat

Penggunaan teknologi yang efektif, efisiendan memberikan keekonomian proyekyang bagus

Peningkatan kompetensi sumber daya manusia

yang meliputi pengetahuan, keahlian dan

pengalaman

I. KEBIJAKAN PERCEPATAN PENGEMBANGAN EBTKE

KEMENTERIANESDM4

1. Undang-undang Nomor 30 tahun 2007 tentang Energi; Undang-undang ini merupakan regulasi payung, meskipun memberikan penekanan khusus terhadap EBT Pasal 20 ayat (3) mengamanatkan bahwapenyediaan energi baru dan energi terbarukan wajib ditingkatkan oleh Pemerintah dan pemerintah daerah sesuaidengan kewenangannya;

2. Undang-undang Nomor 30 tahun 2009 tentang Ketenagalistrikan;

3. Undang-undang Nomor 21 tahun 2014 tentang Panas Bumi;

4. Undang-undang Nomor 16 tahun 2016 tentang Pengesahan Paris Agreement To The United Nations Framework Convention On Climate Change

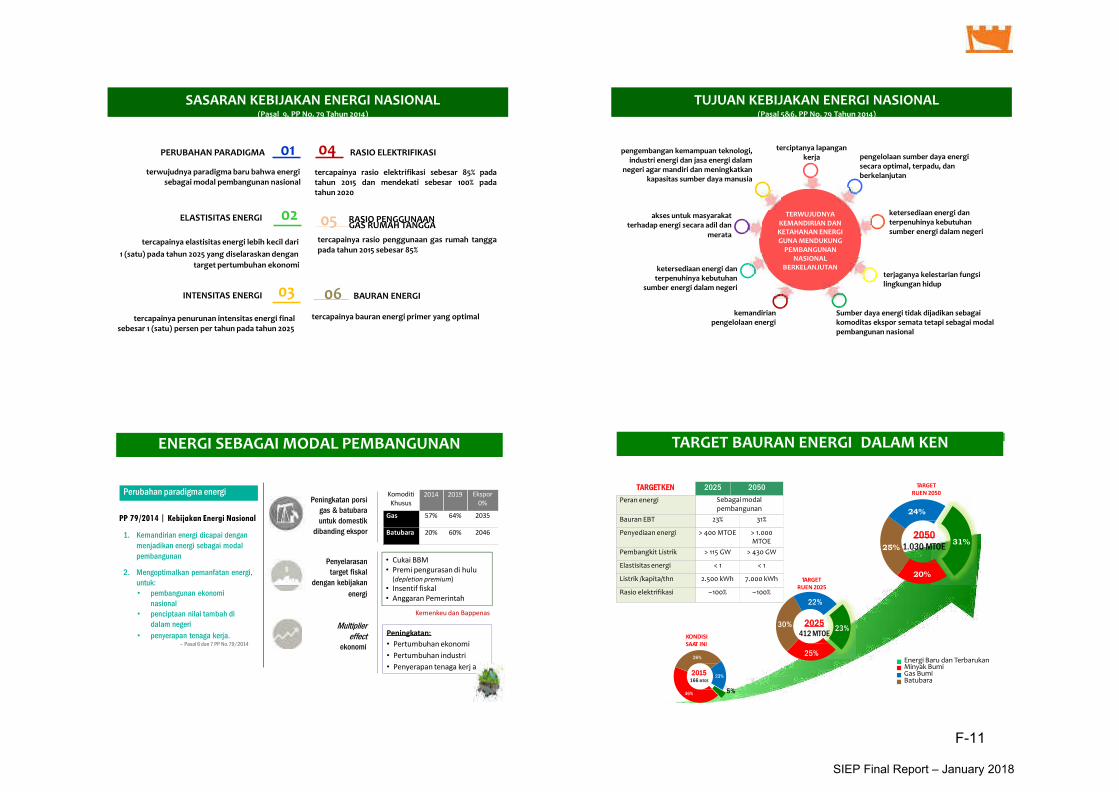

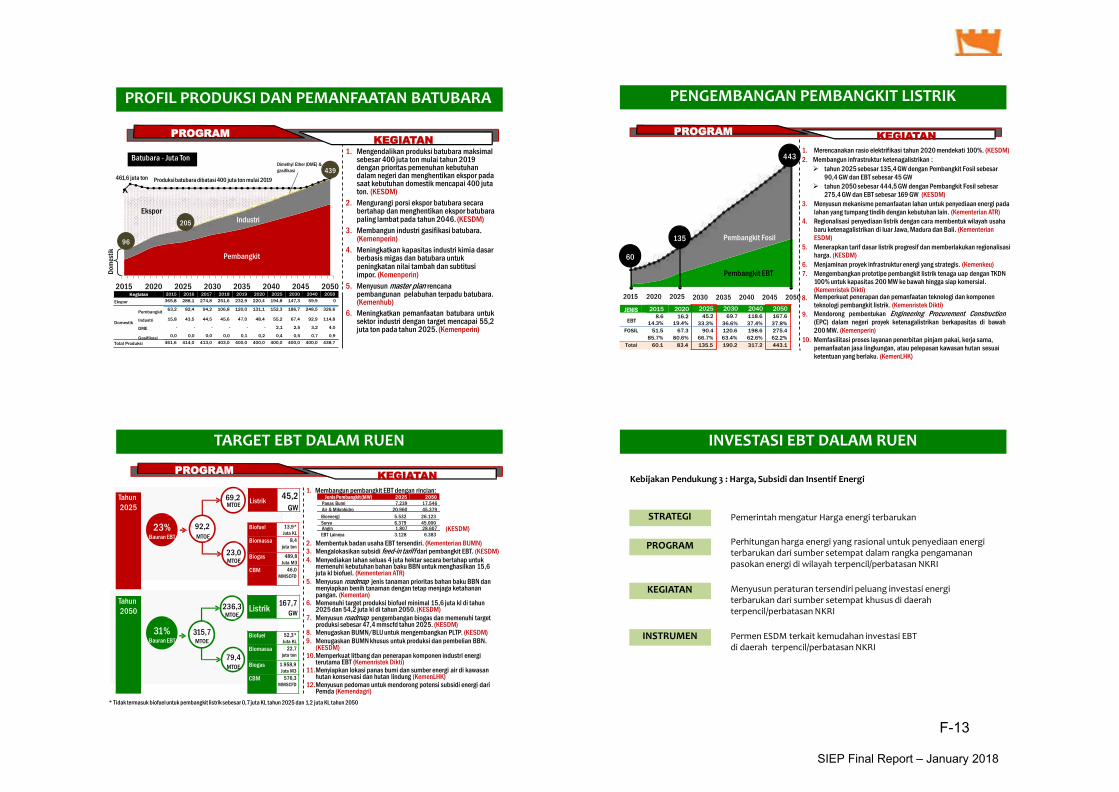

5. Peraturan Pemerintah Nomor 79 tahun 2014 tentang Kebijakan Energi Nasional, Pasal 9mengamanatkan bahwa peran Energi Baru dan Energi Terbarukan paling sedikit 23% tahun 2025 dan paling sedikit 31% tahun 2050 sepanjang keekonomiannya terpenuhi;

6. Peraturan Pemerintah Nomor 7 Tahun 2017 tentang Panas Bumi untuk Pemanfaatan Tidak Langsung;

7. Peraturan Presiden Nomor 4/2016 tentang Percepatan Infrastruktur Ketenagalistrikan, Pasal 14 mengamanatkan bahwa pelaksanaan percepatan infrastruktur ketenagalistrikan mengutamakan pemanfaatanenergi baru dan terbarukan;

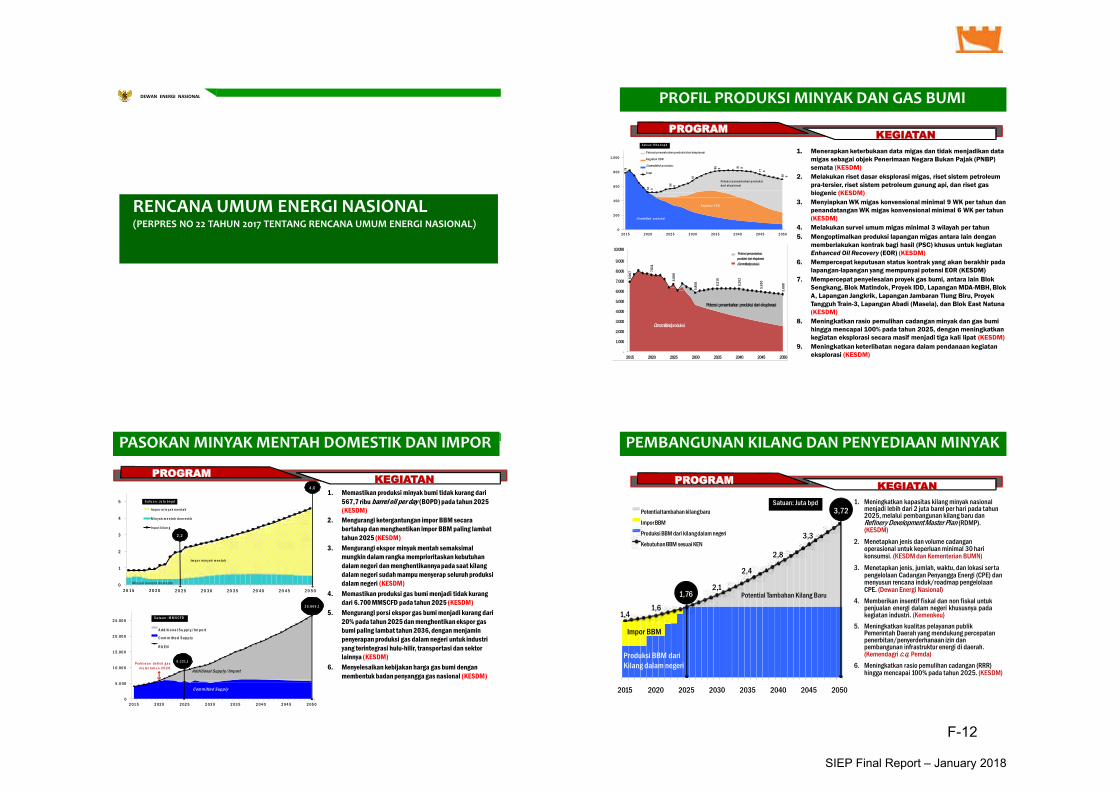

8. Peraturan Presiden Nomor 22/2017 tentang Rencana Umum Energi Nasional (RUEN);

9. Peraturan Menteri ESDM Nomor 12 Tahun 2017 tentang Pemanfaatan Sumber Energi Terbarukanuntuk Penyediaan Tenaga Listrik dan Peraturan Menteri Nomor 43 Tahun 2017 tentang Perubahan atas Permen ESDM Nomor 12 Tahun 2017 tentang Pemanfaatan Sumber Energi Terbarukan untukPenyediaan Tenaga Listrik;

10. Peraturan Menteri ESDM Nomor 39 Tahun 2017 tentang Pelaksanaan Kegiatan Fisik PemanfaatanEnergi Baru dan Energi Terbarukan;

11. Beberapa Peraturan Menteri Keuangan tentang insentif fiskal dan non fiskal pengembangan EBT.

I. Peraturan Pendukung Energi Baru Terbarukan

KEMENTERIANESDM5

II. Potensi Energi Baru Terbarukan

Kapasitas terpasang

Pembangkit saat ini

Rencana

Pembangunan Pembangkit

59.656 MW

35.000 MW+7.500 MW

New project

Potensi :

75 GW + 19,3 GW

Realisasi

PLTA 5,124 GW

PLTMH 0,162 GW

(1,19%)

441,7 GW8,80 GW

(2% terhadap potensi)

Air Surya Panas Bumi

Angin Bioenergi

Potensi : 207,8 GWp

Realisasi

PLTS 0,085 GWp

(0,02%)

Potensi

Sumber Daya : 11,0 GW

Reserve : 17,5 GW

Realisasi

PLTP 1,65 GW

(0,36%)

Potensi : 60,6 GW

Realisasi

PLTB :1,1 MW

(0,0002%)

Laut

Potensi

PLT Bio : 32,6 GW

BBN : 200 Ribu Bph

Realisasi

PLT Bio : 1,78 GW (0,4%)

Potensi : 17,9 GW

Energi FosilCadangan

TerbuktiProduksi Akan habis

Minyak Bumi 3,6 miliar barel 288 Juta barel 13 tahun

Gas Bumi 100,3 TSCF 2,97 TSCF 34 tahun

Batubara 7,2 miliar ton 434 juta ton 16 tahun

KEMENTERIANESDM6

23%

25%

30%

22%

II. Target Penyediaan Energi Primer EBT Tahun 2025

92,2MTOE

69,2MTOE

23,0MTOE

Biofuel 13,69juta kilo liter

Biomassa 8,4juta ton

Biogas 489,8juta m3

CBM46,0

mmscfd

Listrik

EBT 45

GW

1. PLT Panas Bumi, 7,2 GW

2. PLT Hidro, 17,9 GW

3. PLT Mikrohidro, 3 GW

4. PLT Bioenergi, 5,5 GW

5. PLT Surya, 6,5 GW

6. PLT Angin, 1,8 GW

7. PLT EBT lainnya, 3 GW

EBT

Minyak

GasBatubara

~ 400

MTOE

Kapasitas Pembangkit Listrik Nasional 135 GW

Kapasitas Pembangkit Listrik EBT 45 GW

Berdasarkan Peraturan Presiden Nomor 22 Tahun 2017 tentang

Rencana Umum Energi Nasional (RUEN)

F-2

SIEP Final Report – January 2018

KEMENTERIANESDM7

III. Pengembangan Energi Terbarukan berdasarkan RUPTL

Total Indonesia

Wilayah Maluku & PapuaWilayah Sulawesi & Nusa Tenggara

Wilayah KalimantanWilayah Sumatera

No Pembangkit Listrik Kapasitas Total

1 Panas Bumi MW 6.290

2 Air MW 12.343

3 Mini/Mikro Hidro MW 1.694

4 Surya MWp 57

5 Bayu MW 570

6 Biomas/ Sampah kota MW 597

7 Laut MW 0

8 Bio-Fuel Ribu KL 6.572

Total MW 21.549

No Pembangkit Listrik Kapasitas Total

1 Panas Bumi MW -

2 Air MW 1.056

3 Mini/Mikro Hidro MW 10

4 Surya MWp -

5 Bayu MW 15

6 Biomas/ Sampah kota MW 41

7 Laut MW -

8 Bio-Fuel Ribu KL 830

Total MW 1.257

No Pembangkit Listrik Kapasitas Total

1 Panas Bumi MW 3.305

2 Air MW 4.284

3 Mini/Mikro Hidro MW 983

4 Surya MWp 5

5 Bayu MW -

6 Biomas/ Sampah kota MW 274

7 Laut MW -

8 Bio-Fuel Ribu KL 411

Total MW 8.851

No Pembangkit Listrik Kapasitas Total

1 Panas Bumi MW 400

2 Air MW 2.323

3 Mini/Mikro Hidro MW 221

4 Surya MWp 52

5 Bayu MW 170

6 Biomas/ Sampah kota MW 21

7 Laut MW -

8 Bio-Fuel Ribu KL 4.423

Total MW 3.186

No Pembangkit Listrik Kapasitas Total

1 Panas Bumi MW 2.150

2 Air MW 4.562

3 Mini/Mikro Hidro MW 437

4 Surya MWp -

5 Bayu MW 250

6 Biomas/ Sampah kota MW 206

7 Laut MW -

8 Bio-Fuel Ribu KL 439

Total MW 7.965

No Pembangkit Listrik Kapasitas Total

1 Panas Bumi MW 75

2 Air MW 118

3 Mini/Mikro Hidro MW 43

4 Surya MWp -

5 Bayu MW -

6 Biomas/ Sampah kota MW 55

7 Laut MW -

8 Bio-Fuel Ribu KL 469

Total MW 290

Berdasarkan RUPTL 2017 – 2026 PT. PLN Persero

Wilayah Jawa-Bali

KEMENTERIANESDM8

*Asumsi: Filipina (1.870 MW) dan Amerika (3.450 MW) tidak mengalami penambahan kapasitas

0 37110

7.560 35

205 215 165 220

866

450

858

650

1,175

999

0

500

1000

1500

2000

2500

3000

-

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

7,000.0

8,000.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Ta

mb

ah

an

Ka

pa

sita

s (M

W)

Re

nca

na

Ka

pa

sita

s (M

W)

Rencana Kapasitas Tambahan Kapasitas

Kapasitas Terpasang (per Juli 2017) :

1.698,5 MW Penambahan kapasitas

terpasang 2017 terdiri dari:

1.PLTP Ulubelu Unit 4 (55 MW) (COD

25 April 2017)

2.PLTP Karaha Unit 1 (30 MW)

3.PLTP Sorik Marapi (Modular, 20 MW)

4.PLTP Sarulla Unit 2 (110 MW)

Indonesia

peringkat ke-2

dunia melampaui

Filipina

Indonesia

peringkat ke-1

dunia melampaui

Amerika

III. Roadmap Panas Bumi (1/2)

KEMENTERIANESDM9

ROADMAP BIODIESEL (Minimum)

Sektor April 2015 Januari 2016 Januari 2020 Januari 2025

Usaha Mikro, Usaha Perikanan, Usaha Pertanian,

Transportasi, dan Pelayanan Umum (PSO)

15% 20% 30% 30%

Transportasi Non PSO 15% 20% 30% 30%

Industri dan Komersial 15% 20% 30% 30%

Pembangkit Listrik 25% 30% 30% 30%

B2 – B7,5 B10 B15 B20

III. Roadmap Mandatori BBN (2/2)

Implementasi Biodiesel

KEMENTERIANESDM10

IV. Perizinan dan Non Perizinan

1. Ditjen EBTKE telah mengelola 6 jenis perizinan dan 25 jenis non perizinan.

2. Penyederhanaan perizinan telah dilakukan dengan pelimpahan 3 perizinandilaksanakan oleh BKPM antara lain:

1. Penugasan Survei Pendahuluan Panas Bumi

2. Izin Panas Bumi

3. Izin Penggunaan Gudang Bahan Peledak Panas Bumi

3. Penyederhanaan non perizinan telah dilakukan dengan pelimpahan 1 non perizinanyang dilaksanakan oleh BKPM, penghapusan 9 non perizinan dan saat ini dalamproses penghapusan 8 non perizinan lainnya.

4. Ditjen EBTKE tetap mengelola 3 jenis perizinan dan 7 jenis non perizinan.

63

25

7

02468

10121416182022242628

Awal Akhir

Perizinan (P) Non Perizinan (NP)

P : 3 ke BKPM

NP : 1 ke BKPM

9 dihapus

8 dalam proses dihapus

KEMENTERIANESDM11

IV. Insentif Fiskal dan non Fiskal (1/2)

11

No. Tax Allowance Bea Masuk Pendanaan

1. Peraturan Pemerintah No. 1 Tahun 2007 jo. PP

No. 62 Tahun 2008 jo. PP No.52 Tahun 2011

memberikan fasilitas berupa pengurangan PPh

netto 30% dari nilai investasi selama 6 tahun,

penyusutan dan amortisasi dipercepat.

Keputusan Menteri Keuangan No.

766/1992 memberikan fasilitas berupa

impor barang operasi oleh Pengusaha

untuk keperluan Pengusahaan sumber

daya Panasbumi tidak dipungut Bea

masuk, Pajak Pertambahan Nilai, Pajak

Penjualan atas Barang Mewah dan

Pajak Penghasilan.

Peraturan Menteri Keuangan No.

139/PMK.011/2011 mengatur tata cara

pemberian jaminan kelayakan usaha PT.

Perusahaan Listrik Negara (Persero)

untuk pembangunan pembangkit tenaga

listrik dengan menggunakan energi

terbarukan, batubara, dan gas yang

dilakukan melalui kerjasama dengan

pengembang listrik swasta.

2. PMK Nomor 144/PMK.011/2012 memberikan

fasilitas pajak penghasilan untuk penanaman

modal di bidang-bidang usaha tertentu

dan/atau di daerah-daerah tertentu berupa

pengurangan PPh netto 30% dari nilai investasi

selama 6 tahun, penyusutan dan amortisasi

dipercepat

Peraturan Menteri Keuangan No.

78/PMK.010/2005 memberikan fasilitas

pembebasan bea masuk atas impor

barang untuk kegiatan pengusahaan

Panas Bumi berdasarkan kontrak

sebelum berlakunya UU No. 27 Tahun

2003 tentang Panas Bumi.

Peraturan Menteri Keuangan -No.

03/PMK.011/2012 yang mengatur tata

cara pengelolaan dan

pertanggungjawaban fasilitas dana panas

bumi geothermal.

3. PMK Nomor 159/PMK.010/2015 memberikan

fasilitas pengurangan pajak penghasilan badan

paling banyak 100% dan paling sedikit 10%.

Peraturan Menteri Keuangan No.

177/PMK.011/2007 memberikan fasilitas

Pembebasan bea masuk atas impor

barang untuk kegiatan usaha hulu

minyak dan gas bumi serta panas bumi.

-

KEMENTERIANESDM12

IV. Insentif Fiskal dan non Fiskal (2/2)

12

No. Tax Allowance Bea Masuk Pendanaan

4.

PMK Nomor 89/PMK.010/2015 mengatur tata

cara pemberian fasilitas pajak penghasilan

untuk penanaman modal di bidang usaha

tertentu dan/atau di daerah tertentu serta

pengalihan aktiva dan sanksi bagi wajib pajak

badan dalam negeri yang diberikan fasilitas

pajak penghasilan.

Peraturan Menteri Keuangan No.

021/PMK.011/2010 memberikan fasilitas

perpajakan dan kepabeanan untuk

kegiatan pemanfaatan sumber energi

terbarukan

-

5.

PMK Nomor 268/PMK.03/2015 mengatur tata

cara pemberian fasilitas dibebaskan dari

pengenaan pajak pertambahan nilai atas impor

dan/atau penyerahan barang kena pajak

tertentu yang bersifat strategis dan tyata cara

pemnbayaran pajak pertambahan nilai barang

kena pajak tertentu yang bersifat strategis yang

telah dibebaskan serta pengenaan sanksi

Peraturan Menteri Keuangan No.

70/PMK.011/2013 Perlakuan Pajak

Pertambahan Nilai dan Pajak Penjualan

atas Barang Mewah atas Impor Barang

Kena Pajak Yang Dibebaskan dari

Pungutan Bea Masuk

-

F-3

SIEP Final Report – January 2018

KEMENTERIANESDM13

Penugasan kepada BUMNPemerintah akan memberikan penugasan kepada BUMN Panas Bumi dalam rangka pengembangan hulu

dan hilir panas bumi berdasarkan UU 21 tahun 2014

Penugasan Survei Pendahuluan + EksplorasiInvestor yang memenuhi persyaratan memiliki kesempatan untuk mendapatkan Penugasan Survei

Pendahuluan hingga tahap eksplorasi. Sebagai insentif wilayah kerja akan dilelang melalui mekanisme

penunjukan langsung

Pengeboran Eksplorasi oleh Pemerintah & Geothermal FundMengoptimalkan pemanfaatan dana Geothermal Fund sebesar USD 300 juta yang dikelola oleh PT. SMI

untuk melakukan eksplorasi sebelum pelelangan WKP. Hal ini juga sebagai upaya mitigasi risiko untuk

menurunkan risiko kegagalan dalam pengembangan panas bumi.

Pelelangan WKP Indonesia TimurPemerintah akan fokus melakukan pelelangan WKP di wilayah Indonesia Timur khususnya di daerah yang

memiliki BPP setempat lebih tinggi dari BPP Nasional

V. Upaya Pengembangan Panas Bumi (1/3)

KEMENTERIANESDM14

V. Upaya Pengembangan Bioenergi (2/3)

1. Mandatori Bahan Bakar Nabati B-20 (80% Solar, 20% Biodiesel),

2. Biogas Nasional, Non Komersial (Investasi Pemerintah) dan Semi Komersial (Penerapan

Subsidi Parsial)

3. Pengembangan Bioenergi Berbasis Hutan, Bekerjasama dengan Kementerian

Kehutanan, merupakan Pencadangan kawasan hutan produksi yang khusus diperuntukan

untuk pembangunan hutan energi sebagai sumber bahan baku bioenergi

4. Pulau Ikonis Energi Terbarukan (Sumba Iconic Island), Penyediaan sumber energi

baru terbarukan di Pulau Sumba, NTT sebesar 100% pada tahun 2025.

5. Biomassa Untuk Listrik, Pembangunan Pembangkit Listrik Tenaga Biomassa dengan

menggunakan bahan baku limbah biomassa dan sampah kota

KEMENTERIANESDM15

V. Upaya Pengembangan Aneka EBT (3/3)

1. Mendorong prioritas pengembangan Aneka EBT: Jangka pendek 1-3 tahun: PLTS (5.000 MW), PLTM/ PLTMH dan PLTB; Jangka menengah 4 – 7 tahun: Pengembangan PLTA, PLT Gasifikasi Batubara

(PLTGB), PLT Gelombang Laut (PLTGL);

2. Upaya pemerataan energi melalui penyediaan akses energi modern dengan EBT

melalui Dana Alokasi Khusus (DAK);

3. Penyusunan Road Map Aneka EBT bidang Energi Samudera, Hidro, Surya, Angin,

Batubara Tergaskan dan Nuklir;

4. Penyusunan SNI dan SKKNI bidang Aneka EBT.

KEMENTERIANESDM16

VI. Tantangan

1. Penyamaan pola pikir dalam pengembangan EBTKE masih

perlu ditingkatkan;

2. Skema bisnis dan Insentif belum optimum;

3. Teknologi masih tergantung dari Luar Negeri (TKDN kecil);

4. Harga relatif masih mahal;

5. Potensi/Cadangan perlu diperbaharui;

6. Skala kecil dan tersebar;

7. Sistem Interkoneksi masih terbatas;

8. Masih terdapat resistensi masyarakat.

KEMENTERIANESDM17

VI. Kemitraan Strategis

Berperan aktif dalam mendorong pemanfaatan

EBTKE;

Sebagai penerima manfaat, ikut berkontribusi

dalam menjaga keberlanjutan pemanfaatan

EBTKE;

Ikut berkontribusi dalam diseminasi informasi

pemanfaatan EBTKE.

Government

Academy Bussiness

Community

Melakukan inovasi teknologi sekaligus

menyiapkan inkubator untuk komersialisasi

Melakukan survei dan kajian potensi EBTKE

Melakukan kajian kebijakan terutama

bagaimana memanfaatkan hasil riset

Melakukan kajian teknologi sebelum

dikembangkan pemerintah

Bersama-sama meningkatkan TKDN

Mendorong transfer teknologi informasi

Menyusun regulasi dan kebijakan;

Fasilitator;

Memberikan pembinaan dan pengawasan;

Melaksanakan program di bidang EBTKE;

Diseminasi informasi program EBTKE;

Pemerintah wajib mengembangkan sumber daya EBT

dan meningkatkan efisiensi energi

Melakukan pengusahaan EBTKE;

Memproduksi EBTKE;

Berkontribusi dalam penerimaan negara dan

kegiatan ekonomi.

EBTKE

KEMENTERIANESDM18

www.esdm.go.id

F-4

SIEP Final Report – January 2018

KEMENTERIANESDM19

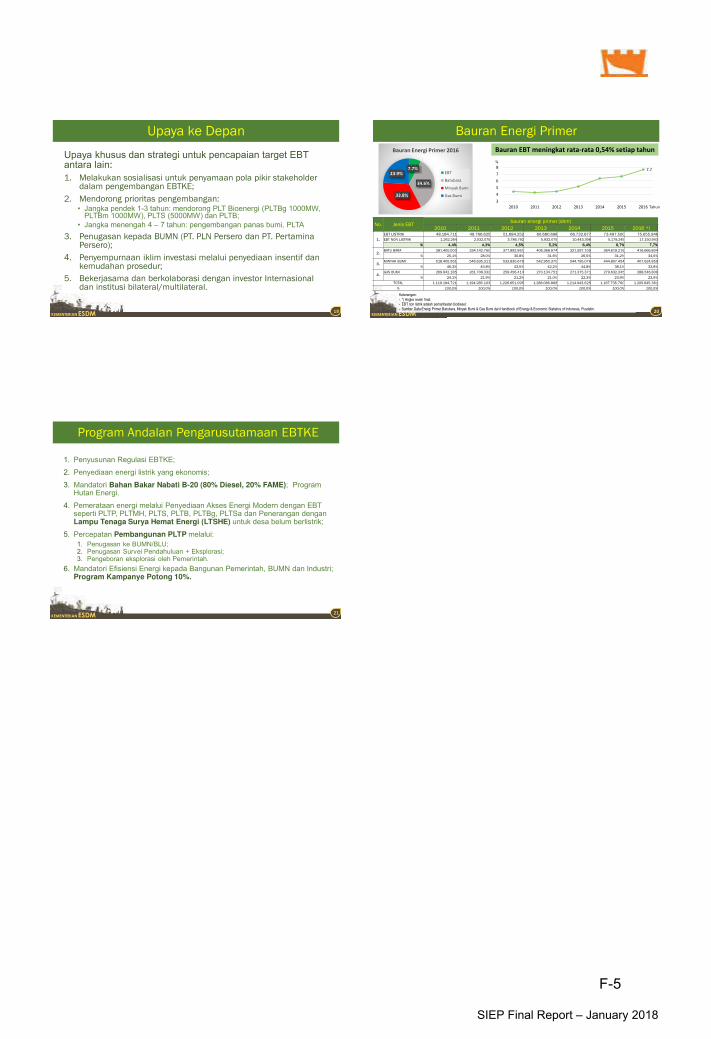

Upaya ke Depan

Upaya khusus dan strategi untuk pencapaian target EBTantara lain:

1. Melakukan sosialisasi untuk penyamaan pola pikir stakeholder dalam pengembangan EBTKE;

2. Mendorong prioritas pengembangan:• Jangka pendek 1-3 tahun: mendorong PLT Bioenergi (PLTBg 1000MW,

PLTBm 1000MW), PLTS (5000MW) dan PLTB;• Jangka menengah 4 – 7 tahun: pengembangan panas bumi, PLTA

3. Penugasan kepada BUMN (PT. PLN Persero dan PT. PertaminaPersero);

4. Penyempurnaan iklim investasi melalui penyediaan insentif dan kemudahan prosedur;

5. Bekerjasama dan berkolaborasi dengan investor Internasionaldan institusi bilateral/multilateral.

KEMENTERIANESDM20

7.7

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015 2016

%

Tahun

Bauran Energi Primer

Keterangan:

- *) Angka revisi/ final;- EBT non listrik adalah pemanfaatan biodiesel;

- Sumber Data Energi Primer Batubara, Minyak Bumi & Gas Bumi dari Handbook of Energy & Economic Statistics of Indonesia, Pusdatin.

Bauran EBT meningkat rata-rata 0,54% setiap tahun

No. Jenis EBTbauran energi primer (sbm)

2010 2011 2012 2013 2014 2015 2016 *)

1.

EBT LISTRIK 48.184.711 49.766.625 51.684.252 60.680.698 66.732.677 73.497.500 75.655.946

EBT NON LISTRIK 1.262.264 2.032.075 3.786.792 5.932.075 10.443.396 5.179.245 17.150.943

% 4,4% 4,3% 4,5% 5,2% 6,4% 6,7% 7,7%

2.BATU BARA 281.400.000 334.142.760 377.892.961 406.368.974 321.597.105 364.619.216 416.666.804

% 25,1% 28,0% 30,8% 31,6% 26,5% 31,2% 34,6%

3.MINYAK BUMI 518.405.561 546.635.311 533.830.676 542.950.370 544.795.076 444.807.454 407.624.859

% 46,3% 45,8% 43,5% 42,2% 44,8% 38,1% 33,8%

4.GAS BUMI 269.942.185 261.708.332 259.456.414 270.134.751 271.375.371 279.632.345 288.546.809

% 24,1% 21,9% 21,2% 21,0% 22,3% 23,9% 23,9%

TOTAL 1.119.194.721 1.194.285.103 1.226.651.095 1.286.066.868 1.214.943.625 1.167.735.760 1.205.645.361

% 100,0% 100,0% 100,0% 100,0% 100,0% 100,0% 100,0%

7.7%

34.6%

33.8%

23.9%

Bauran Energi Primer 2016

EBT

Batubara

Minyak Bumi

Gas Bumi

KEMENTERIANESDM21

Program Andalan Pengarusutamaan EBTKE

1. Penyusunan Regulasi EBTKE;

2. Penyediaan energi listrik yang ekonomis;

3. Mandatori Bahan Bakar Nabati B-20 (80% Diesel, 20% FAME); Program Hutan Energi.

4. Pemerataan energi melalui Penyediaan Akses Energi Modern dengan EBT seperti PLTP, PLTMH, PLTS, PLTB, PLTBg, PLTSa dan Penerangan denganLampu Tenaga Surya Hemat Energi (LTSHE) untuk desa belum berlistrik;

5. Percepatan Pembangunan PLTP melalui:

1. Penugasan ke BUMN/BLU;2. Penugasan Survei Pendahuluan + Eksplorasi; 3. Pengeboran eksplorasi oleh Pemerintah.

6. Mandatori Efisiensi Energi kepada Bangunan Pemerintah, BUMN dan Industri; Program Kampanye Potong 10%.

F-5

SIEP Final Report – January 2018

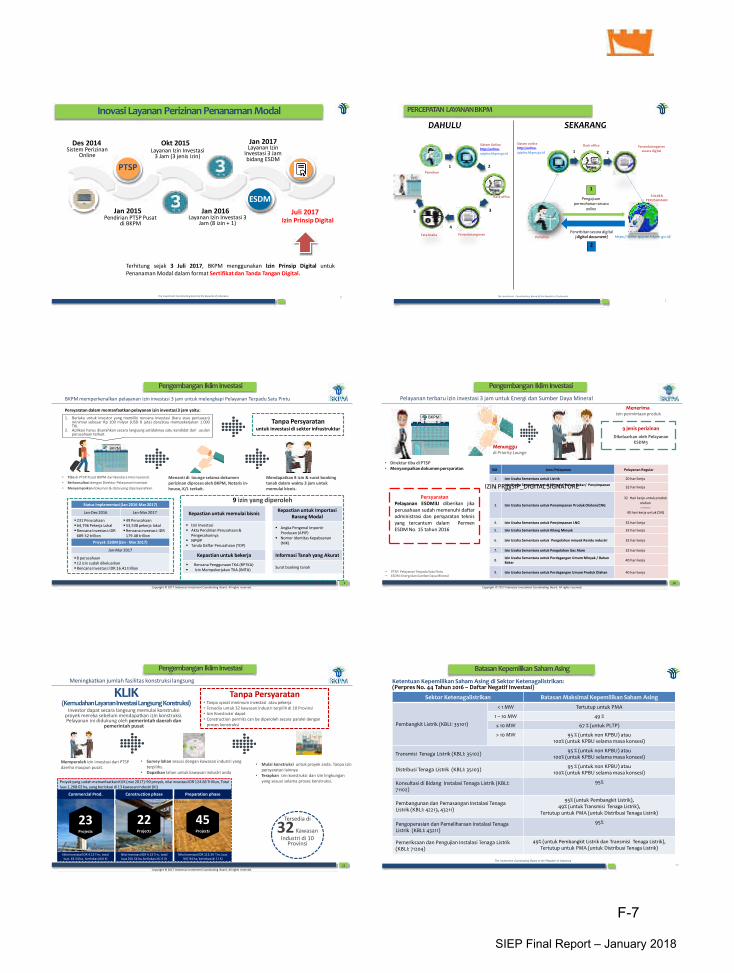

© Badan Koordinasi Penanaman Modal, 2017

Jakarta, 31 Juli 2017

Up Date Kebijakan Investasi Mendorong Pembangunan Pembangkit Listrik Energi Baru Terbarukan

Deputi Bidang Perencanaan Penanaman Modal, BKPMTamba P. Hutapea

Disampaikan pada FGD Percepatan Investasi Energi Terbarukan, Kemenko Bidang Perekonomian

The Investment Coordinating Board of the Republic of Indonesia

2

2

Realisasi Investasi

(dalam Miliar USD) 2010 2011 2012 2013 2014Total

2010-142015 2016

2017

(SMT 1)2018* 2019*

Total

2015-19*

PMA 16.4 19.5 24.6 28.6 28.5 117.6 29.3 28.9 15.6 38.1 43.8 171

PMDN 6.7 8.4 10.2 13.6 14.5 53.5 14.4 15.8 9.6 22.9 27.9 98.6

Total Realisasi 23.2 27.9 34.8 42.2 43.0 171.0 43.6 44.7 25.2 61.0 71.8 269.7

Target Realisasi Investasi

*nilai tukar 1 USD = IDR 13,000.-• 2010-2012, Nilai Tukar 1 USD = Rp 9,000

• 2013 (Q I and Q II), Nilai Tukar 1 USD = Rp 9,300 (berdasarkan APBN 2013)

• 2013 (Q III and Q IV), Nilai Tukar 1 USD = Rp 9,600 (berdasarkan APBN 2013)

• 2014 (QI-QIII) Nilai Tukar 1 USD = Rp 10,500 (berdasarkan APBN 2014)

• 2014 (QIV) Nilai Tukar 1 USD = Rp 11,600 (berdasarkan APBN-P 2014)

• 2015 Nilai Tukar 1 USD = Rp 12.500 (berdasarkan APBN-P 2015)

• 2016 Nilai Tukar 1 USD = Rp 13.900 (berdasarkan APBN-P 2016)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

FDI DDI TargetPMA PMDN

The Investment Coordinating Board of the Republic of Indonesia

3

InfrastrukturProgram

Ketenagalistrikan35 GW

24 PelabuhanLaut

Pertanian Tanaman PanganPerkebunan

JagungSapi

Industri

Industri Padat Karya TekstilMakanan &Minuman

Furnitur Mainan

Industri SubstitusiImpor

Kimia & Farmasi Besi & Baja

Industri BerorientasiEkspor

Alat ElektronikaMinyak KelapaSawit & Produk

Turunannya

Produk Kayu, Pulp, & Kertas

Otomotif

Mesin Produk KaretIkan & Produk

TurunannyaUdang

Industri Hilir SumberDaya Alam

Cokelat GulaBatubara (Smelter)

Industri Kemaritiman Galangan Kapal PemancinganPenyimpanan(Cold Storage)

Kawasan Pariwisata, KawasanEkonomi Khusus dan Kawasan

Industri

KawasanPariwisataStrategis

MICE 8+11 KEK15 Kawasan

Industri Baru

Sektor Prioritas Investasi

Prioritas Investasi

The Investment Coordinating Board of the Republic of Indonesia

4

PMA

55%

PMDN

45%

Realisasi Proyek EBT (2009 – 2016)

PPMA : USD 1,75 Milliar

PMDN : USD 1,43 Milliar

Total : USD 3,18 Milliar

PMA

82%

PMDN

18%

Rencana Proyek EBT (2009 – 2016)

PMA : USD 61,59 Miliar

PMDN : USD 13,69 Milliar

Total: USD 75,28 Milliar

Rencana danRealisasi Investasi Sektor Ketenagalistrikan

PLTA,

188,483

PLTAL15

PLTB1,562

PLTBg14.442

PLTBm1.916

PLTM212,321

PLTMH

19.442

PLTP

1,426

PLTS

39,192PLTSA

3,162 PLTBg dan PLTBm

10

TOTAL KAPASITAS

RENCANA PEMBANGKIT EBT (MW)

2009 - 2016

Catatan:

PLTS: Pembangkit Listrik Tenaga Surya

PLTSa: Pembangkit Listrik Tenaga Sampah

PLTBg: Pembangkit Listrik Tenaga Biogas

PLTBm: Pembangkit Listrik Tenaga Biomassa

PLTA: Pembangkit Listrik Tenaga Air

PLTB: Pembangkit Listrik Tenaga Bayu/Angin

PLTAL: Pembangkit Listrik Tenaga Arus Laut

PLTM: Pembangkit Listrik Tenaga Minihidro

PLTMH: Pembangkit Listrik Tenaga Mikrohidro

PLTP: Pembangkit Listrik Tenaga Panas Bumi

The Investment Coordinating Board of the Republic of Indonesia

5

Pelayanan

Terpadu Satu

Pintu (PTSP)

Pusat BKPM

SatuPintu

22 Kementerian/

Lembagaterintegrasi

3-hourIzin Investasi 3

Jam

All sectors128 izindidelegasikankepada BKPM

17,238Izin diterbitkan

dalam Jan-Des

2015

KLIKKemudahan

Investasi

Langsung

Konstruksi

90%PTSP Daerah telah terbentuk. 61% PTSP Daerah menerapkan e-licensing

3-hourIzin Investasi

untuk Sektor

Infrastruktur

Industri, ketenaga-listrikan, minyak & gas bumi, pariwisatasatu pintu

PTSP PusatBKPM

Perbaikan Pelayanan Investasi

The Investment Coordinating Board of the Republic of Indonesia

6

2 41Pengajuan Izin

PrinsipPTSP PUSAT

Pengajuan InsentifBisnis

PTSP PUSAT

Pengajuan IzinBisnis

PTSP PUSAT

Proses perizinan untuk penanaman modal asing, antar provinsi, dan strategis:

3Pengajuan Izin Operasi

PTSP Daerah

Jenis Izin Unit TerkaitIzin Lokasi PTSP Daerah Regional/Kota

Izin Konstruksi PTSP Daerah Regional/Kota

Sertifikat Lahan Pertanahan Regional/Kota

Izin Lingkungan Regional Environment Office

HO (Hinderordonnantie) PTSP Daerah Regional/Kota

Insentif Unit TerkaitTarif Import Perpajakan

Tax Allowance Kementerian Keuangan

Tax Holiday Kementerian Keuangan

O&G Recommendation Kementerian Perdagangan,Kementerian ESDM

Izin pemanfaatan hutan Kementerian Lingkungan Hidup danKehutanan

PTSP pusat meliputiperwakilan dari 22 Kementerian/Lembaga

PTSP pusatmenyelenggaran layananproses izin 3 jam

Fasilitas KLIK pada 32kawasan industri & KEK

Kegiatan bisnis bisasegera dimulai

*Syarat & Ketentuan berlaku

BKPM telah menyempurnakan layanan One-Stop Service /PTSP Pusat

Source: BKPM

F-5

SIEP Final Report – January 2018

F-6

SIEP Final Report – January 2018

The Investment Coordinating Board of the Republic of Indonesia 7

Des 2014Sistem Perizinan

Online

Jan 2015Pendirian PTSP Pusat

di BKPM

Okt 2015Layanan Izin Investasi

3 Jam (3 jenis izin)

Jan 2016Layanan Izin Investasi 3

Jam (8 izin + 1)

Jan 2017Layanan Izin

Investasi 3 Jam bidang ESDM

Juli 2017Izin Prinsip Digital

Inovasi Layanan Perizinan Penanaman Modal

PTSP

ESDM

Terhitung sejak 3 Juli 2017, BKPM menggunakan Izin Prinsip Digital untuk

Penanaman Modal dalam format Sertifikat dan Tanda Tangan Digital.

online-spipise.bkpm

5

2

DAHULU SEKARANG

Sistem onlinehttp://online-

spipise.bkpm.go.id

Sistem Onlinehttp://online-

spipise.bkpm.go.id

Back office Penandatanganansecara digital1

1 2

Pemohon

FOLDERPERUSAHAAN

Back officePengajuan

permohonan secaraonline3

4Penerbitan secara digital

(digital document)PenandatangananTata Usaha https:// .go.id/Pemohon

The Investment Coordinating Board of the Republic of Indonesia

1

2

1

PERCEPATAN LAYANANBKPM

Copyright © 2017 Indonesia Investment Coordinating Board. All rights reserved.

9

BKPM memperkenalkan pelayanan izin investasi 3 jam untuk melengkapi Pelayanan Terpadu Satu Pintu

Persyaratan dalam memanfaatkan pelayanan izin investasi 3 jam yaitu:

BKPM

1. Berlaku untuk investor yang memiliki rencana investasi (baru atau perluasan)minimial sebesar Rp 100 milyar (USD 8 juta) dan/atau mempekerjakan 1.000TKI.

2. Aplikasi harus diserahkan secara langsung setidaknya satu kandidat dari usulanperusahaan terkait.

• Tiba di PTSP Pusat BKPM dari Bandara Internasional.

• Berkonsultasi dengan Direktur Pelayanan Investasi.

• Menyampaikan dokumen & data yang dipersyaratkan.

Menanti di lounge selama dokumen

perizinan diproses oleh BKPM, Notaris in-

house, K/L terkait.

Mendapatkan 8 izin & surat booking

tanah dalam waktu 3 jam untuk

memulai bisnis.

9 izin yang diperoleh

Kepastian untuk memulai bisnisKepastian untuk Importasi

Barang Modal

Izin Investasi

Akta Pendirian Perusahaan &

Pengesahannya

NPWP

Tanda Daftar Perusahaan (TDP)

Angka Pengenal Importir

Produsen (APIP)

Nomor Identitas Kepabeanan

(NIK)

Kepastian untuk bekerja Informasi Tanah yang Akurat

Rencana Penggunaan TKA (RPTKA)

Izin Mempekerjakan TKA (IMTA)Surat booking tanah

Tanpa Persyaratanuntuk investasi di sektor infrastruktur

Status Implementasi (Jan 2016-Mar 2017)

Jan-Dec 2016 Jan-Mar 2017

231 Perusahaan

64,796 Pekerja Lokal

Rencana Investasi: IDR

689.52 trillion

49 Perusahaan

53,538 pekerja lokal

Rencana investasi: IDR

179.48 trillion

Proyek ESDM (Jan - Mar 2017)

Jan-Mar 2017

8 perusahaan

12 izin sudah dikeluarkan

Rencana Investasi: IDR 16.41 trillion

Pengembangan IklimInvestasi

Copyright © 2017 Indonesia Investment Coordinating Board. All rights reserved.

10

• Direktur tiba di PTSP• Menyampaikandokumen persyaratan.

MenerimaIzin permintaan produk

BKPM

9 jenis perizinan

Dikeluarkan oleh PelayananESDM3

Persyaratan Pelayanan ESDM3J diberikan jika

perusahaan sudah memenuhi daftar

administrasi dan persyaratan teknis

yang tercantum dalam Permen

ESDM No. 15 tahun 2016

Menunggudi Priority Lounge

• PTSP: Pelayanan Terpadu Satu Pintu• ESDM: Energi dan Sumber Daya Mineral

NO Jensi Pelayanan Pelayanan Regular

1. Izin Usaha Sementara untuk Listrik 20 hari kerja

2.Izin Usaha Sementara untuk Minyak/ Bahan Bakar/ Penyimpanan

LPG32 hari kerja

3. Izin Usaha Sementara untuk Penyimpanan Produk Olahan/CNG

32 Hari kerja untuk produk

olahan

---------

40 hari kerja untuk CNG

4. Izin Usaha Sementara untuk Penyimpanan LNG 32 hari kerja

5. Izin Usaha Sementara untuk Kilang Minyak 32 hari kerja

6. Izin Usaha Sementara untuk Pengolahan minyak Residu industri 32 hari kerja

7. Izin Usaha Sementara untuk Pengolahan Gas Alam 32 hari kerja

8.Izin Usaha Sementara untuk Perdagangan Umum Minyak / Bahan

Bakar40 hari kerja

9. Izin Usaha Sementara untuk Perdagangan Umum Produk Olahan 40 hari kerja

Pelayanan terbaru izin investasi 3 jam untuk Energi dan Sumber Daya Mineral

Pengembangan IklimInvestasi

IZIN PRINSIP_DIGITAL SIGNATURE

Copyright © 2017 Indonesia Investment Coordinating Board. All rights reserved.

11

Meningkatkan jumlah fasilitas konstruksi langsung

KLIK(Kemudahan Layanan Investasi Langsung Konstruksi)

Tanpa Persyaratan• Tanpa syarat minimum investasi atau pekerja

• Tersedia untuk 32 kawasan industri terpilih di 10 Provinsi

• Izin Konstruksi dapat

• Construction permits can be diperoleh secara paralel dengan

proses konstruksi

Investor dapat secara langsung memulai konstruksi proyek mereka sebelum mendapatkan izin konstruksi. Pelayanan ini didukung oleh pemerintah daerah dan

pemerintah pusat

Memperoleh izin investasi dari PTSP

daerha maupun pusat.

• Survey lahan sesuai dengan kawasan industri yang

terpilihs.

• Dapatkan lahan untuk kawasan industri anda

• Mulai konstruksi untuk proyek anda. Tanpa izin

persyaratan lainnya

• Terapkan izin konstruksi dan izin lingkungan

yang sesuai selama proses konstruksi.

23Projects

Commercial Prod.

Nilai investasi IDR 4.13 Trn, total

luas 63.54 ha, berlokasi di 6 KI

22Projects

Construction phase

Nilai investasi IDR 4.13 Trn, total

luas 256.54 ha, berlokasi di 11 KI

45Projects

Preparation phase

Nilai investasi IDR 113.34 Trn, luas

947.94 ha, berlokasi di 11 KI

Proyek yang sudah memanfaatkan KLIK (mei 2017): 90 proyek, nilai investasi IDR 124.66 Trilliun, Total

luas 1,268.02 ha, yang berlokasi di 13 kawasan industri (KI)

Tersedia di

32 Kawasan

Industri di 10 Provinsi

Pengembangan IklimInvestasi

The Investment Coordinating Board of the Republic of Indonesia

12

Sektor Ketenagalistrikan Batasan Maksimal Kepemilikan Saham Asing

Pembangkit Listrik (KBLI: 35101)

< 1 MW Tertutup untuk PMA

1 – 10 MW 49 %

≤ 10 MW 67 % (untuk PLTP)

> 10 MW 95 % (untuk non KPBU) atau100% (untuk KPBU selama masa konsesi)

Transmisi Tenaga Listrik (KBLI: 35102)95 % (untuk non KPBU) atau

100% (untuk KPBU selama masa konsesi)

Distribusi Tenaga Listrik (KBLI: 35103)95 % (untuk non KPBU) atau

100% (untuk KPBU selama masa konsesi)

Konsultasi di Bidang Instalasi Tenaga Listrik (KBLI: 71102)

95%

Pembangunan dan Pemasangan Instalasi Tenaga Listrik (KBLI: 42213, 43211)

95% (untuk Pembangkit Listrik), 49% (untuk Transmisi Tenaga Listrik),

Tertutup untuk PMA (untuk Distribusi Tenaga Listrik)

Pengoperasian dan Pemeliharaan Instalasi Tenaga Listrik (KBLI: 43211)

95%

Pemeriksaan dan Pengujian Instalasi Tenaga Listrik(KBLI: 71204)

49% (untuk Pembangkit Listrik dan Transmisi Tenaga Listrik), Tertutup untuk PMA (untuk Distribusi Tenaga Listrik)

Ketentuan Kepemilikan Saham Asing di Sektor Ketenagalistrikan:(Perpres No. 44 Tahun 2016 – Daftar Negatif Investasi)

Batasan Kepemilikan Saham Asing

F-5

SIEP Final Report – January 2018

F-7

SIEP Final Report – January 2018

The Investment Coordinating Board of the Republic of Indonesia

13

PAJAK PENGHASILAN(TAX ALLOWANCE)

PP No. 9/2016 jo PP No. 18/2015

145 bidangusaha(Daftar bidang usaha dalamLampiran PP 9/2016)

30% darijumlahinvestasiPengurangan penghasilannetto selama 6 (enam) tahun, yaitu sebesar 5% per tahun

Penyusutan dan amortisasi yang

dipercepat.

Pajak Penghasilan atas

penghasilan dividen yang

dibayarkan kepada subjek

pajak luar negeri selain

bentuk usaha tetap di

Indonesia

≤ 10%

• berlokasi di Kawasan

Industri dan/atau Kawasan

Berikat

• melakukan

pembangunan

infrastruktur• menggunakan bahan baku

dalam negeri ≥70%.

Kompensasi kerugian 5-10 tahun, bagi

perusahaan yang:• menyerap tenaga kerja

500-1.000 orang

• melakukan kegiatan

penelitian dan

pengembangan (R&D)

• melakukan reinvestasi

• melakukan ekspor ≥30% dari penjualan.

PEMBEBASAN PAJAK PENGHASILAN (TAX HOLIDAY)

PMK No.159/PMK.010/2015

5-15yearsPembebasan Pajak Penghasilan sejak TahunPajak dimulainya produksi komersial. Dapatdiperpanjang hingga maksimum 20 tahundengan diskresi Menteri Keuangan.

Industri Pionir1. Industri logam hulu

2. Industri pengilangan

minyak bumi;

3. Industri kimia dasar

organik yang

bersumber dari minyak

bumi dan gas alam

4. Industri permesinan yang

menghasilkan mesin

industri

5. Industri pengolahan

berbasis hasil pertanian,

kehutanan, dan

perikanan

6. Indsutri telekomunikasi,

informasi dan komunikasi

7. Industri transportasi

kelautan

8. Industri pengolahan yang

merupakan industri

utama di Kawasan

Ekonomi Khusus (KEK);

dan atau

9. Infrastruktur ekonomi

non KPBU.

Pengurangan Pajak Penghasilan Badan:

10% -1 00 % dari Pajak Penghasilan badanyang terhutang.

> IDR1TrilliunRencana Investasi: (USD 80 Juta)

Untuk industri telekomunikasi, informasi dankomunikasi (ICT):

≤ 50 % dari Pajak Penghasilanbadan yang terhutang.

IDR50Miliar - IDR1TrilliunRencana Investasi:

PEMBEBASAN BEA MASUK(IMPORT DUTY FACILITY)

PMK No.176/PMK.011/2009 jo.

PMK No. 76/PMK.011/2012 jo. PMK

188/PMK.010/2015

PMK No. 66/PMK.010/2015

Pembebasan Bea Masuk atas Impor

Barang Modal dalam rangka

Pembangunan atau Pengembangan

Industri Pembangkitan Tenaga Listrik

untuk Kepentingan Umum

2 tahunPembebasan bea masuk atasimpor mesin

2 tahunPembebasan bea masuk atas

impor barang dan bahan untuk

keperluan produksi sesuai

kapasitas terpasang

4 tahun (tambahan2 tahun)Pembebasan bea masuk atas impor

barang dan bahan untuk keperluan

tambahan produk apabila

menggunakan mesin dalam negeri:

>30% daritotal nilaimesin

Insentif Investasi Sektor Energi

The Investment Coordinating Board of the Republic of Indonesia 14

Fasilitas Impor Barang Modal

Percepatan dan kepastian dalam pemrosesan customs clearance

Lebih cepat dan pasti•Tidak perlu screening barangmodal.•Memotong waktu pemrosesan dari 3-5 hari menjadi hanya 30 menit.

Persyaratan mudah• Proyek dalam tahap konstruksi• Memenuhi kewajiban pelaporan

LKPM Triwulanan ke BKPM• Rekomendasi dari BKPM

PENYELESAIAN KEPABEANAN (CUSTOMS

CLEARENCE)

4 status pengecekan kepabeanan:

•Jalur Merah untuk perusahaan baru.

Dilakukan pemeriksaan fisik & dokumen

sebelum barang dipindahkan dari

pelabuhan.

•Jalur KuningHanya dilakukan pengecekan dokumen

sebelum barang dipindahkan dari

pelabuhan.

•Jalur HijauPengecekan dokumen dilakukan setelah

barang dipindahkan dari pelabuhan.

•Prioritas Mitra Utama untuk perusahaan

dengan track record yang terbukti baik. Tidak

diperlukan pengecekan.

Fasilitas Baru:

Peningkatan Statusdari jalur merah ke jalur hijau untuk

perusahaan baru yang dalam tahap

konstruksi

Perbaikan Iklim Investasi

The Investment Coordinating Board of the Republic of Indonesia

15

No.JenisEnergiTerbarukan

Pelaksanaan Pembelian

Tarif

Jika

BPP S ≤ BPP NJika

BPP S > BPP N

1. PLTS PV (Surya)Pelelangan berdasarkan kuota kapasitas yangditawarkan

100% x BPP S Maksimum 85% x BPPS

2. PLTB (Bayu/Angin)Pelelangan berdasarkan kuota kapasitas yangditawarkan

100% x BPP S Maksimum 85% x BPPS

3. PLTA (Air)

Harga Patokan Kesepakatan para pihak Maksimum 100% BPPS

Pemilihan Langsung Harga ditentukan pada proses pemilihan langsung

a. Tenaga Air ≤ MW: Capacity Factor paling sedikit 65%b. Tenaga Air > 10 MW: Capacity Factor tergantung kebutuhan sistem

4. PLTBm (Biomassa)Harga Patokan (Kapasitas ≤ MW) 100% x BPP S Maksimum 85% x BPPS

Pemilihan Langsung (Kapasitas > 10MW) Harga ditentukan pada proses pemilihan langsung

5. PLTBg (Biogas)Harga Patokan (Kapasitas ≤ MW) 100% x BPP S Maksimum 85% x BPPS

Pemilihan Langsung (Kapasitas > 10MW) Harga ditentukan pada proses pemilihan langsung

6.PLTSa (SampahPerkotaan)

Harga Patokan Kesepakatan para pihak Maximum 100% BPP S

7. PLTP (Panas Bumi) Harga Patokan Kesepakatan para pihak Maximum 100% BPP S

BPP Pembangkitan sistem setempat dan rata – rata BPP Pembangkitan nasional merupakan BPP Pembangkitan nasional pada tahun sebelumnyayang telah ditetapkan oleh Menteri berdasarkan usulan PT PLN (Persero).

(Permen ESDM No. 12 Tahun 2017 sebagaimana telah diubah dengan Permen ESDM No. 43 Tahun 2017)

Catatan: BPP S: Biaya Pokok Penyediaan Sistem SetempatBPP N: Biaya Pokok Penyediaan Nasional

Sumber: Kementerian ESDM, 2017

Harga Pembelian Tenaga Listrik EBT

The Investment Coordinating Board of the Republic of Indonesia

16

BPP Pembangkitan PT PLN (Persero) Tahun 2016(Periode 1 April 2017 – 31 Maret 2018)

Catatan:• Dalam hal sampai dengan akhir periode belum terdapat penetapan besaran BPP Pembangkitan terbaru, maka BPP Pembangkitan di atas tetap berlaku

sampai dengan ditetapkannya besaran BPP Pembengkitan terbaru.• Dalam hal terdapat lokasi tertentu yang belum terlistriki oleh PLN dan belum terdapat penetapan besaran BPP Pembangkitan, maka besaran BPP

Pembangkitan ditetapkan sebesar sama dengan besaran BPP Pembangkitan tertinggi.

Sumber: Kepmen ESDM 1404 K/20/MEM/2017

10.39

9.28

8.07

10.14

7.86 7.77

13.66

12.17

6.51 6.51 6.51 6.52 6.54 6.62

12.43

9.04

10.20

12.75

8.10

13.68

17.52 17.32

13.54

7.39

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00(sen US$ per kWh)

BPP Sistem Setempat

BPP Pembangkitan Nasional

Produksi Tenaga Listrik

The Investment Coordinating Board of the Republic of Indonesia

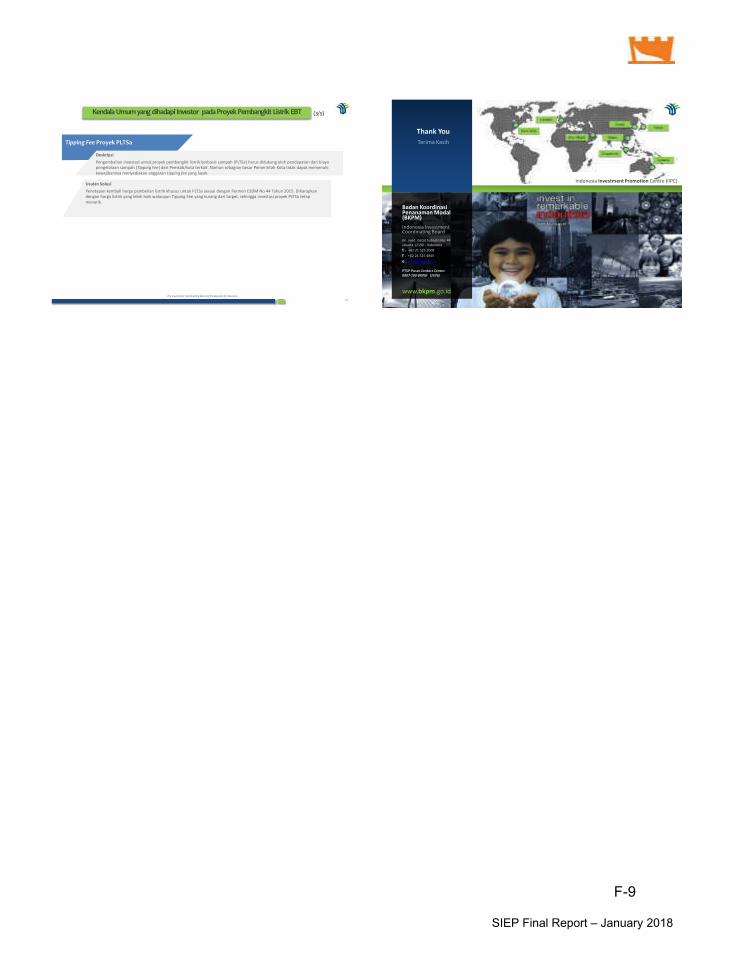

17

2. One Stop Service

Deskripsi

Sejak diberlakukannya harga beli listrik EBT berdasarkan Permen No. 12/2017, maka pasar menganggap harga tersebut sangat

rendah dan tidak layak untuk investasi suatu proyek pembangkit listrik EBT di Indonesia. Bahkan berapa investor yang sudah

punya izin prinsip dan izin konstruksi tidak dapat merealisasikan proyeknya.

Hal ini terjadi karena dukungan pemerintah tidak berubah/belum optimal sejak penerbitan Permen tersebut. Padalah diketahui

rendahnya harga beli listrik di UEA yang dijadikan referensi/benchmark penerbitan Permen ESDM 12/2017 adalah karena adanya

dukungan dan insentif yang maksimal dari pemerintah negara tersebut.

Kondisi ini tentunya akan menjadikan target pengembangan pembangkit EBT 23 % tahun 2025 sulit tercapai.

Deskripsi

Batas kepemilikan saham asing hanya 49% untuk pembangkit di bawah 10 MW sangat tidak menarik, khususnya untuk EBT.

Karena karakteristik kapasitas pembangkit proyek EBT pada umumnya (PLTS, PLTB, PLTM) kecuali PLTP dan PLTA adalah di bawah

10 MW.

Harga Pembelian Listrik EBT

Batas Kepemilikan Saham Asing

Usulan Solusi

1.Perlunya insentif fiskal (tax holliday) baru untuk bidang usaha pembangkit EBT.

2.Perlu dukungan pemerintah yang lebih maksimal (Kementerian ESDM), misalnya pembebasan lahan ditanggung oleh

pemerintah lewat APBN atau pembebasan dilakukan oleh pengembang dan kemudian diganti oleh LMAN.

3.Khusus untuk PLTP, Insentif dan dukungan khusus dari pemerintah sangat diperlukan karena proyek ini membutuhkan

investasi besar dan risiko yang besar sejak tahap eksplorasi. Bentuknya selain pembebasan lahan oleh swasta, juga dukungan

perbankan nasional dalam memberikan bunga pinjaman yang murah dan, proses perizinan yang cepat.

Usulan Solusi

Perubahan DNI ketentuan maksimum kepemilikan saham asing khusus untuk pembangkit EBT diatas 1 MW adalah 95 %.

(1/3)Kendala Umumyang dihadapi Investor pada Proyek Pembangkit Listrik EBT

The Investment Coordinating Board of the Republic of Indonesia

18

Deskripsi

Penyelesaian perizinan untuk proyek pembangkit listrik terutama di daerah (Izin Lokasi, Izin Lingkungan, IMB) sering

membutuhkan waktu yang panjang dan tidak pasti. Salah satu penyebabnya adalah belum adanya standarisasi dokumen

perizinan dan Standard Operating Procedure (SOP), sehingga pelayanan perizinan tidak sama di setiap daerah. Seringkali proyek

pembangkit listrik EBT yang merupakan Proyek Strategis Nasional atau Prioritas Nasional terhambat pemberian izinnya karena

kurangnya dukungan pemerintah pusat dan daerah dalam mempercepat realisasi proyek-proyek dimaksud.

Sementara itu, investor memiliki batas waktu 1 tahun untuk menyelesaikan perizinannya sesuai waktu Financial Close yang

disepakti dengan pihak PT PLN.

Perizinan Pusat dan Daerah

.

Usulan Solusi